INTRODUCTION

ARE YOU PREPARED FOR ANOTHER LOST DECADE AHEAD?

Ahh, the good old days. Remember when investing was fun and easy in the 1990s as investors enjoyed the late stages of a raging bull market? From 1995 to 1999 the S&P 500 posted consecutive annual returns of 38 percent, 23 percent, 33 percent, 29 percent, and 21 percent, respectively. To put that into perspective, a $1 million investment on January 1, 1995, grew to nearly $3.5 million by the turn of the century, and those returns appear tame in comparison to the astronomical fortunes made in the technology-laden Nasdaq index (an 85 percent return in 1999 alone). Ten-, fifteen-, and twenty-year stock market returns sported hefty midteen average annual returns. Back then, investment decisions were fairly easy to make. All an investor had to do was buy a ticket and stay onboard the runaway stock market train heading higher. The undeniable investment mantra drilled into all participants was simply: buy the dips, buy and hold, and sit back and watch your profits multiply. Spectacular stock market gains built over the prior 18 years reinforced a “can’t lose” mentality. Everyone was an investment genius and bragged about it at any opportunity whether it was on the golf course, around the office water cooler, or even during the family Thanksgiving dinner. Day trading replaced many a career—it was more fun and paid better than, say, that boring professional career with the less than adequate attorneys’ salary. Even the most conservative of investors got caught up in the greed contagion, left their risk-averse tendencies behind, and joined the party. Then something happened. As the world entered the new millennium and the year 2000 struck, the investment climate changed dramatically. Something investors had not dealt with since the late 1960s began—a long-term or “secular” bear market emerged. All of a sudden the well-ingrained rules of the investment world changed completely, and portfolio decision making became far more difficult.

More than 10 years later, many investors and members of the financial press recognized that stock prices actually lost ground, labeling this period the “lost decade.” Indeed, the period from January 2000 through December 2009 goes down in history as one of the worst 10-year investment periods ever for stocks. Two severe 50 percent-plus bear markets over the decade demoralized buy-and-hold investors, leading to a −9 percent loss including dividends. A new cold reality set in. Expectations of annual double-digit stock market returns no longer dance in investors’ minds. Stories of individuals leaving their jobs to day-trade are long past—in 2012, people are satisfied just to have a full-time job. Other once dependable investment alternatives have their own legitimate concerns. The myth that real estate is a low-risk investment and only goes up has been thoroughly shattered. Earnings on savings accounts have plummeted to near zero, and after the effects of inflation and taxes are actually negative. Government bond yields are at generational lows and offer little return potential and substantial principal risk if interest rates should go up. Yes, since 2000 investing has been a veritable minefield for most investors. A decade that began with wild-eyed optimism and confidence ended with investors anxious with fear and holding sobered expectations.

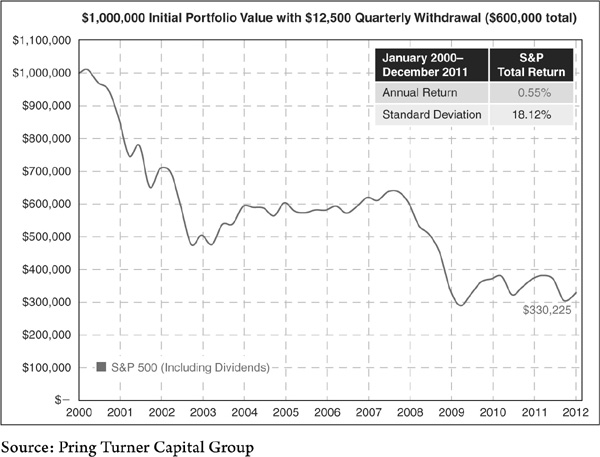

To illustrate our point, let’s take a close look at one couple’s retirement plans and how expectations changed since 2000. Mr. Smith was age 62 when he and Mrs. Smith decided to retire with a sizable nest egg. Using history as a guide, they decide to allocate $1 million of retirement savings to the stock market via a passive index fund. After all, at that time the S&P 500 had delivered 25-year average annual returns of over 17 percent, and since 1900 the performance averaged about 10 percent per year. They figured if they could earn just 10 percent and spend half the earnings, they would be able to leave the remaining 5 percent of earnings to compound. This seemingly sensible strategy would allow their retirement nest egg to continue to grow and even provide a “pay raise” from time to time to offset inflation. They planned to withdraw $50,000 annually ($12,500 quarterly) to help fund their living expenses. This sounded reasonable at the time—the Smiths weren’t being too greedy. At least they thought they made realistic assumptions and had reasonable expectations. After a dozen years in retirement (as 2012 began), Mr. Smith was a 74-year-old retiree, and Chart I-1 shows what happened to the $1 million nest egg.

CHART I-1 Will the Smiths Outlive Their Retirement Nest Egg?

The combination of the “lost decade” for stocks and steady withdrawals for retirement income leaves the Smiths’ nest egg severely depleted. How will they survive a second lost decade?

Combined with a “lost decade” of negative total stock market returns and a steady withdrawal rate, they end the first 12 years of retirement with a portfolio balance of only $330,225. How much longer will they be able to tap that portfolio for living expenses? And what will the Smiths do if, as we suspect and elaborate on in this book, there is another lost decade ahead? When will they run out of money? We will continue to check in with the Smiths throughout this book to better illustrate the financial landscape and offer proactive solutions to help people adapt to the difficult task of surviving and prospering in another lost decade we believe lies ahead.

While it is true that in the very long run stocks go up, it is also true that secular bear markets are a fact of life. These dangerous very long-term time periods where stocks underperform can last 20 years or more. How many of these 20-year periods do you have in your investment lifetime? Can Mr. and Mrs. Smith afford to stick it out with a passive buy-and-hold index approach through another lost decade? By the end of that decade, they will be in their early eighties and eager for the next secular bull market to begin. The question is: Will they have any money left by then? Our point is that in order to be successful, it is vitally important for investors to understand what secular environment they are in. Is it a secular bull market or secular bear market? We know the secular bull markets (like the one from 1982 to 2000) are pretty easy to navigate—simply buy and hold. But, secular bear markets are a different animal altogether with many cyclical ups and downs. Succeeding in a secular bear market takes a lot of hard work, the right tools, and a more flexible investment discipline. Our goal is to thoroughly demonstrate these disciplines so you can successfully maneuver through the remainder of the next lost decade.

The good news is that it is possible to build wealth during a secular bear market, but investors must first discard the buy-and-hold, indexing, and passive asset allocation strategies that worked well in the prior secular bull market. In a negative secular bear market environment the same static methods result in severely inadequate returns. The crucial determinant to building wealth successfully in a secular bear market is to adopt a more proactive plan of action. Even in this difficult, uphill, overall negative atmosphere there will be rewarding opportunities—these are the cyclical upturns that may last two or three years. And these will be followed by cyclical declines where careful risk-management techniques must be employed to protect portfolio values and preserve the hard-earned gains of the prior advance. The key to the successful exploitation of these moves is the application of the proper business cycle forecasting tools and disciplines. The last 150 years of economic and financial history show that markets are linked in a logical way to business activity. The economy goes through a set series of chronological sequences just like the seasons of the year.

Recognizing these “financial seasons” and correctly applying the appropriate asset allocation have always had a beneficial impact on investment returns. Indeed, investors can benefit from understanding the historical, reliable, and sequential relationship of the business cycle to stocks, bonds, and inflation-sensitive assets. With knowledge of business cycles, secular trends, and timely tactical asset allocation, it is possible to create better returns with less risk and, most important, to experience peace of mind.

Some people say it is probably a good idea to learn a little about the author before reading a book. That way the reader can better understand the authors’ biases and point of view. This book is coauthored by the partners at Pring Turner Capital Group—Martin Pring, Joe Turner, and Tom Kopas combine for over 110 years of experience in the financial markets. We also would like to credit associate portfolio manager Jim Kopas for his thorough research work, editing, and digital production efforts, which were invaluable contributions to this project.

For decades, our conservative money management firm has successfully utilized the key elements of the strategies detailed in the pages ahead. Our approach is unique in that it is multifaceted and includes elements of fundamental, technical, and business cycle analysis. The reason we take this wide-ranging view of portfolio management is that our first and overriding goal is careful risk management. In fact, in our office the “cosmic joke” we govern ourselves by is: “We don’t know.” We don’t know specifically what the future will bring. Nobody does. Yet we have to make decisions today, with an unknown future, and come out the other end with a successful outcome for clients. This is why we rely on the repetitive nature of the business cycle and pay a lot of attention to risk management.

Certainly, there are elements of fundamental analysis (quality, value, income), technical analysis (trend analysis, investor sentiment, and monetary policy), and business cycle analysis (economic turning points) that can help smooth out the ride for investors. We see all these elements as layers of risk management for portfolios because we do not exactly know what the future brings. However, with the right combination of tools, it is possible to reduce risk and improve returns.

In terms of our style, we are not day traders, certainly not high-frequency traders, but we are not “buy and hold” types either. Our asset allocations are not passive as is the case with most financial advisors; instead we use a dynamic approach that is determined to a large extent by where we are in the typical four- to five-year business cycle. Allocation changes and sector emphasis around the cycle are made gradually and methodically. As the evidence changes, we change. The important distinction is that our allocation decisions are based on looking at the markets and the economy to determine risk and reward trade-offs for the various asset classes. Conventional wisdom says that you can use age as a determinant for portfolio allocation, with the idea that at age 35 you can take more risk because you have more time to make back the loss. Our view is that regardless of whether you are 35, 55, or 75 years old, you simply do not want too much exposure to stocks going into a bear market–led recession. Being younger and having plenty of time to make money back doesn’t justify losing it in the first place. Secular (very long term) and business cycle–associated bull and bear markets do not discriminate based on age.

We spent time looking back at history to learn from prior secular bear markets. These lessons will help you prepare for what lies ahead. And just what does lie ahead? Our opinion, based on extensive studies of previous secular bear markets, strongly suggests that investors should anticipate and prepare for another “lost decade” for stocks. Expect a decade with more frequent recessions and shorter and less robust recoveries. In fact, we believe that the next 10 years will be even more difficult than the last 10 because of a new emerging menace—inflation! It may not happen right away because of the deflationary difficulties associated with the debt overhang, discussed at great length in Chapter 3. However, we feel that government policy is heading in the direction of monetizing the sizable debt load—the easiest way for politicians to offset the debt buildup is to inflate, or simply print more money. After World War I, during the Weimar Republic in Germany, it took several years of aggressive money printing before prices took off to the extent that the paper currency essentially became worthless. We are certainly not forecasting such extreme conditions, but it is important to note that inflation is a stealth tax that penalizes savers and can wreak havoc on retiree lifestyles. It is an enemy investors have not had to really face since the 1970s and early 1980s. We are on alert.

How prepared are you to meet this new challenge? What if you not only have to deal with a secular bear market for stocks but also a new secular bear market for bonds? If inflation and interest rates rise over the next 10 years, bonds may be just as miserable an investment as stocks have been during the last decade. What if both of those markets face a challenging, deeply cyclical environment? How can you fully prepare? Will you be a victim of market forces or empowered to control your investment destiny?

By the time you get to the end of this book, you will have the critical tools and tactics you need to handle whatever comes your way in another lost decade. We explain how it’s possible to execute two game plans: one designed to protect assets in the cyclical bear markets and another to grow wealth in the cyclical upturns. A constant theme incorporates critical risk-management tools to first protect and then grow wealth throughout both good and bad cycles. For those seeking an even deeper understanding of the material, we provide detailed appendixes that expand on the key topics. Moreover, www.pringturner.com will periodically bring you up to date on our current thinking as well as on the latest charts. Also, a wealth of resources including a reproduction of all the charts and figures in color, useful links, and a video of our business cycle approach to investing can be found at www.mhprofessional.com/mediacenter/. Whether you are a financial professional or individual investor, this book is designed to be an invaluable, practical guide to help you not only survive but also prosper in the second lost decade.