IV.6

Risk Model Risk

IV.6.1 INTRODUCTION

Portfolio risk is a measure of the uncertainty in the distribution of portfolio returns, and a risk model is a statistical model for generating such a distribution. A risk model actually contains three types of statistical models, for the

(a)portfolio's risk factor mapping,

(b)multivariate distribution of risk factor returns, and

(c)resolution method.

The choice of resolution method depends on the risk metric that we apply to the risk model. In this chapter we shall be focusing on VaR models, so the choice of resolution method is between using different analytic, historical or Monte Carlo VaR models.

The choices made in each of (i)–(iii) above are interlinked. For instance, if the risk factor mapping is a linear model of risk factor returns and these returns are assumed to be i.i.d. multivariate normal, then the resolution method for estimating VaR is analytic. This is because historical simulation uses an empirical distribution, not an i.i.d. normal one, and under the i.i.d. normal assumption there is no point in using Monte Carlo simulation because it only introduces sampling error into the exact solution, which may be obtained using an analytic formula.

Of course, the distribution of portfolio returns has an expected value, and if the risk model is also used to forecast this expected value then we could call the model a returns model as well. What we call the model depends on the context. For instance, fund managers normally call their model a returns model, or an alpha model, because the primary purpose is to provide a given level of performance. But most clients also require some limit on risk, and fund managers should take care to assess risk in the same statistical model as they assess expected returns, i.e. using their alpha model.

What about banks? Banks accept risks from their clients because they are supposed to know how to hedge them. Since the main business of banks is risk rather than returns, a risk manager in banking will call his model for generating portfolio return distributions a risk model. Banks account for profits and losses in their balance sheets and they use expected returns (or expected P&L) in risk adjusted performance measures. But those figures are only for accounting and capital allocation purposes. Banks often use risk models that are quite different from the models used to compute the expected returns (or P&L) on their balance sheets. More often than not their risk model assumes that all activities earn the risk free rate, even though their balance sheets and their economic capital estimates may use different figures for expected returns.

It is important to specify the expectation in the risk model. For instance, volatility is one, very common, risk metric that represents the extent to which the realized return can deviate from the expectation of the risk model distribution. Of course, it says nothing at all about deviations from any other expected return, and the market risk analyst must be careful to specify the expected return that this volatility relates to. Suppose the expected return is fixed by some external target. Unless the target happens to be the expected value of the risk model distribution, the risk model volatility says nothing at all about whether this target will be outperformed or underperformed. One cannot just assume the expected return is equal to the target without changing the risk model. Unless the model is changed to constrain the expected return to be the target – and this will also change the volatility in the model – the model is not appropriate for measuring risk relative to the target.1 But this chapter is not about expected returns, and it is not until Chapter IV.8 that we shall be concerned with the interplay between risk and expected return. Here we focus on the accuracy of risk models, and we begin by putting the questions we ask about this into two categories:

- Model risk. Which models should we use for the risk factor mapping, for modelling the evolution of the risk factor returns and for the resolution of the model to a single measure of risk? How do the three sub-models' statistical assumptions affect the accuracy of the risk model's risk forecasts?

- Estimation risk. Given the assumptions of the risk model, how should we estimate the model parameters, and how do these estimates affect the accuracy of our risk measures?

Notice that we call the second type of model risk ‘estimation risk’ rather than sampling error. Estimation risk includes sampling error, i.e. the variation in parameter estimates due to differences in sample data. But it may also be that more than one estimation method is consistent with the risk model assumptions, and this is a different source of estimation risk. For instance, if the risk factor returns are assumed to be multivariate normal then we could apply either equally or exponentially weighted moving averages to estimate the risk factor returns covariance matrix.2 Different estimation methods will give different parameter estimates, based on the same assumptions and given the same sample data.

To answer the questions about model risk and estimation risk above we need a methodology for testing the accuracy of a risk model. In the industry we call such a methodology a backtest. In academia we call it an out-of-sample diagnostic (or performance) analysis. Since the term ‘backtest’ is shorter, we shall use that term in this chapter. Several academic studies report the results of backtesting VaR models. Notably, Berkowitz and O'Brien (2002) and Berkowitz et al. (2006) suggest that the VaR models used by banks are not sufficiently risk-sensitive to generate the short-term VaR estimates they need.3 And the results of Alexander and Sheedy (2008) suggest that risk models based on constant parameter assumptions cannot forecast short-term risk accurately, even at the portfolio level. Both volatility clustering in portfolio returns and heavy-tailed conditional return distributions are required for accurate VaR and ETL forecasts at high confidence levels and over short-term horizons.

The outline of this chapter is as follows. Section IV.6.2 clarifies the different sources of risk model risk and estimation risk. Section IV.6.3 derives some simple confidence intervals for VaR. Section IV.6.4 presents the core, technical part of this chapter. We first describe the general methodology for backtesting and then discuss the simple backtests required by regulators. Then we describe a more sophisticated and informative type of backtest based on the Kupiec (1995) test for coverage and the Christoffersen (1998) test for conditional coverage. Thereafter we cover backtests based on regression, which may provide a means of identifying why the VaR model fails the backtest, if it does. We describe a method for backtesting ETL due to McNeil and Frey (2000) and the application of bias statistics in the normal linear VaR framework. We also discuss backtests that examine the accuracy of the entire portfolio return distribution. As usual, Excel examples are provided to illustrate how each test is implemented, and we end the section by describing the results of some extensive backtests performed by Alexander and Sheedy (2008). Section IV.6.5 concludes.

IV.6.2 SOURCES OF RISK MODEL RISK

This section introduces the main sources of model risk and estimation risk in risk models, explaining how the two risks interact. For instance, if the risk factor returns are assumed to be multivariate normal i.i.d., in which case the model parameters are the means and the covariance matrix of these returns, then the estimation of the covariance matrix cannot be based on a GARCH model; it can only be based on a moving average model, because returns are not i.i.d. in GARCH models. So in this case estimation risk depends on the choice between three alternatives: an equally weighted covariance matrix, an exponentially weighted moving average with the same smoothing constant for all risk factors, or an orthogonal EWMA covariance matrix estimate. Further to this choice, the choice of sample data and, in the case of the EWMA matrices the smoothing constant, also influences sampling error, which is a part of estimation risk.

Sampling error in statistical models has been studied for many generations and estimated standard errors of estimators that we commonly use are well known. Almost always, in an unconditional (i.i.d.) framework, the larger the estimation sample size the greater the in-sample accuracy of the estimator. But this does not necessarily imply that we should use as large a sample as possible for VaR and ETL estimation. Apart from the fact that backtests are out-of-sample tests, we might encounter problems if the risk model is an unconditional model, because backtests are usually performed using short-term, time-varying forecasts. So there is no guarantee that larger estimation sample sizes will perform better in backtests. Indeed, the opposite is likely to be the case, because the VaR and ETL would become less risk sensitive.

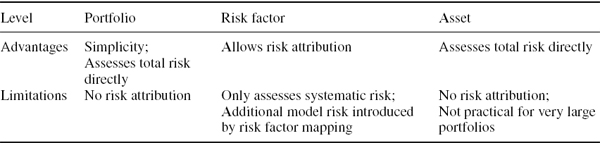

In this section we shall examine the decisions that must be made at each step of the risk model design, from the models used for risk factor mapping, risk factor returns and VaR resolution to the choice of sample data and estimation methodology. We already know from previous chapters that portfolio risk may be assessed at the portfolio level, the risk factor level or even at the asset level. Each approach has its own advantages and limitations, which are summarized in Table IV.6.1. This section assumes that portfolio risk is assessed at the risk factor level, as it will be whenever the model is used for risk attribution, and we focus on the model risk that is introduced by the use of a risk factor mapping.

Table IV.6.1 Advantages and limitations of different levels of risk assessment

IV.6.2.1 Risk Factor Mapping

The main focus of academic research and industry development has been on the specification of the risk factor returns model, with much less attention paid to the model risk arising from the risk factor mapping itself. However, the type of risk factor mapping that is applied, and the method and data used to compute factor sensitivity estimates, could each have a considerable impact on the VaR and ETL estimates.4

Effect of Vertex Choice on Interest Rate VaR

Suppose a portfolio is represented as a sequence of cash flows.5 Given a set of vertices for the risk factor mapping, we know that we should map the cash flows to these vertices in a present value, PV01 and volatility invariant fashion. Following the method explained in Section III.5.3.4, we can do this by mapping each cash flow to three vertices. We now ask which fixed set of vertices should be chosen for the risk factor mapping. For instance, should we use vertices at monthly or 3-monthly intervals? And does this choice matter – how much does it influence the VaR estimate?

EXAMPLE IV.6.1: MODEL RISK ARISING FROM CASH-FLOW MAP

Estimate the 1% annual VaR of a cash flow with a present value of $1 million in 250 calendar days, when it is mapped in a present value, PV01 and volatility invariant fashion to three vertices, and these vertices are:6

- 8 months, 9 months and 10 months;

- 6 months, 9 months and 12 months.

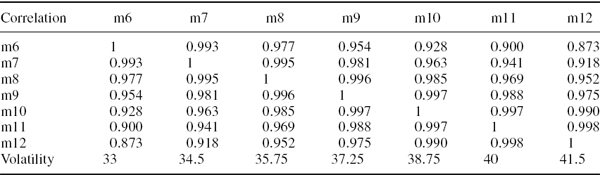

The correlation matrix of continuously compounded discount rates at monthly maturities, and their volatilities (in basis points per annum), are shown in Table IV.6.2. In each case base your calculations on the assumption that the changes in discount rates are i.i.d. with a multivariate normal distribution.

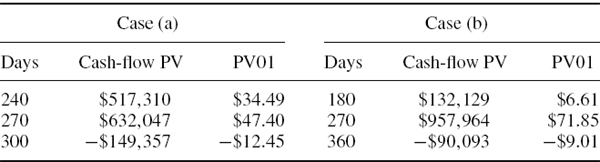

SOLUTION In each case we map the cash flow to the three vertices using the methodology explained in Section III.5.3.4 and illustrated in Example III.5.3. That is, first we use linear interpolation on variances to estimate the volatility of the 250-day discount rate, and also calculate the covariance matrix corresponding to the volatilities and correlation. Then we apply the Excel Solver to compute the cash-flow mapping, and the result is shown in the columns headed cash-flow PV in Table IV.6.3. Next, we compute the PV01 vector of the mapped cash flow, as described in Section IV.2.3.2, and the results are shown in the columns headed PV01.7Finally, we use the PV01 vector to calculate the 1% annual normal linear VaR, using the usual formula (IV.2.25). The results for the 1% annual VaR are $5856.56 in case (a) and $5871.18 in case (b).

Table IV.6.2 Discount rate volatilities and correlations

Table IV.6.3 Computing the cash-flow map and estimating PV01

The above example shows that the choice of vertices for the cash-flow map makes little difference to a normal linear VaR estimate, even over an annual horizon. The 1% annual VaR of a cash flow with present value $1 million is 0.5856% of the portfolio value when mapped to monthly vertices, or 0.5871% of the portfolio value when mapped to quarterly vertices. Readers can verify, using the spreadsheet for the above example, that even when interest rates are more volatile and have lower correlation than in the above example, the influence of our choice of vertices in the risk factor mapping on the interest rate VaR is minor.

The reason for this is that if the VaR is proportional to the portfolio volatility, as it is in the normal linear VaR model, the choice of the three vertices to map to should not influence the result because the VaR should be invariant under the mapping.8 However, if we had used a VaR resolution method based on historical simulation then the difference between the two results could have been greater. Typically there are thousands of cash flows, and then the precision of the historical VaR estimate could be significantly affected by the choice of vertices for the cash-flow map. But this choice is far less crucial than other choices that the market risk analyst faces. For example, the choice of multivariate distribution to use for the interest rate changes, and the decision to assume they are i.i.d. or otherwise, would have a much more significant influence on the VaR estimate than the choice of vertices in the cash flow map.

Effect of Sample Size and Beta Estimation Methodology on Equity VaR

Now suppose we have spot exposures in a stock portfolio. There may be little or no flexibility regarding the choice of market risk factors. For instance, a hedge fund market risk analyst may be estimating portfolio risk in the context of a pre-defined returns model with many factors. By contrast, a market risk analyst in a large bank will probably, for the sake of parsimony, be using a single broad market index for each country. Sometimes there is a choice to be made between two or more broad market indices, but usually these indices would be highly correlated and so the choice of index is a relatively minor source of model risk. Thus, in the case of an equity portfolio held by a bank, the main sources of risk factor model risk are the sample data and the methodology that are used to estimate the market betas. The estimation of a market beta in the single index model is the subject of Section II.1.2. There we compare the ordinary least squares (OLS) and exponentially weighted moving average (EWMA) methods, illustrating the huge differences that can arise between the two estimates.9

Whilst fund managers are likely to base capital allocation on a returns model that uses many risk factors, with OLS estimates for risk factor betas, market risk analysts require fewer risk factors but more risk sensitive estimates for their betas. Risk managers may choose between:

- fund manager's OLS beta estimates, which are typically based on weekly or monthly data over a sample period covering several years;

- OLS betas based on daily data over a smaller sample, under the belief that these are more risk sensitive than the fund manager's betas;10 or

- EWMA or GARCH time-varying beta estimates.

We shall now illustrate the effect of this choice on the VaR estimate, in the context of a very simple portfolio.

EXAMPLE IV.6.2: MODEL RISK ARISING FROM EQUITY BETA ESTIMATION

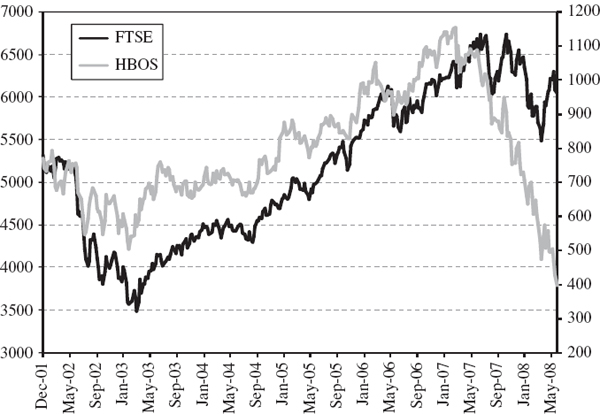

On 30 May 2008, estimate the 1% 10-day systematic VaR of a position currently worth £4 million on Halifax Bank of Scotland (HBOS) PLC, using the FTSE 100 index as the market factor.11 Compare your results when both the beta estimate and the index volatility estimate are based on:

(a)OLS estimation using weekly data since 31 December 2001;

(b)OLS estimation using weekly data since 28 December 2006

(c)OLS estimation using daily data since 31 December 2001;

(d)OLS estimation using daily data since 28 December 2006;

(e)EWMA estimation using weekly data with a smoothing constant of 0.95;

(f)EWMA estimation using weekly data with a smoothing constant of 0.9;

(g)EWMA estimation using daily data with a smoothing constant of 0.95;

(h) EWMA estimation using daily data with a smoothing constant of 0.9.

In each case base your calculations on the assumption that the returns on the stock and the index are i.i.d. with a bivariate normal distribution.

SOLUTION The stock and the index prices since 31 December 2001 are shown in Figure IV.6.1.12 The effects of the credit crunch on the stock price are very evident here: its price tumbled from a high of nearly £12 per share in January 2007 to only £4 per share by the end of May 2008. The stock returns volatility was clearly much higher at the end of the sample than it had been, on average, over the sample period, and this will be particularly reflected in the EWMA volatility estimate (h), which has a low value for the smoothing constant. The stock's index beta will currently also be much lower according this EWMA estimate because the correlation between the stock and index returns, which was fairly high during the years 2002–2006, had become very low indeed by the end of the sample.

Figure IV.6.1 HBOS stock price and FTSE 100 index

We shall estimate the VaR using the usual normal linear formula, expressing VaR as a percentage of the portfolio value. That is, the 100α% h-day VaR estimate is given by

![]()

where ![]() is the beta estimate for HBOS relative to the FTSE 100 index and

is the beta estimate for HBOS relative to the FTSE 100 index and ![]() is the estimate of the index volatility. In each of the cases (a)–(h) we use a different estimate for

is the estimate of the index volatility. In each of the cases (a)–(h) we use a different estimate for ![]() and for

and for ![]() . These and the resulting 1% 10-day VaR estimates, in percentage and nominal terms, are displayed in Table IV.6.4.13

. These and the resulting 1% 10-day VaR estimates, in percentage and nominal terms, are displayed in Table IV.6.4.13

Table IV.6.4 OLS and EWMA beta, index volatility and VaR for HBOS stock.

Considering the OLS estimates (a)– (d) first, we find that the betas are fairly similar whether they are based on weekly or daily data over either estimation period, but the index volatility estimates are much higher when based on daily data. As a result, the VaR estimates are greater when based on daily data. This is expected because, unless the returns are really i.i.d. as we have assumed, the volatility clustering effects are likely to be more pronounced in daily data. However, when there is volatility clustering it is not correct to scale VaR using the square-root-of-time rule. Instead we should use a GARCH model, which has a mean reversion in volatility, and the square-root-of-time rule does not apply.

For the VaR there is much less variation between the four different OLS estimates (a)– (d) than there is between the four different EWMA estimates (e)– (h). These range from 4.72% to 14.68% of the portfolio value, i.e. from £188,796 to £587,358! In this case the choice between weekly and daily data has a great effect on the VaR estimate, and so does the choice of smoothing constant in the EWMA. It is the product of the volatility and the beta that we use in the VaR so the daily data could lead to either a higher or a lower value for VaR than the weekly data.14 In this case, it turns out that the daily data give the lower VaR estimates.

The above example illustrates some important points:

- When short-term VaR estimates are scaled to longer risk horizons using the square-root-of-time rule, a large model risk is introduced.15 Although we should base daily VaR estimates on daily data, weekly data may provide more accurate VaR estimates over a 5-day or longer risk horizon.

- When the EWMA methodology is applied the choice of smoothing constant has a very significant effect on the VaR estimate. The problem with EWMA is that this choice is ad hoc.16

- Calculating equity VaR by mapping to major indices is fraught with difficulties. The mapping methodology (e.g. the OLS or EWMA) and the choice of parameters (e.g. estimation period, or smoothing constant) may have an enormous influence on the result. Completely counterintuitive results could be obtained, such as the result shown in column (h) above. More generally, a high risk portfolio could be uncorrelated with the market, in which case it would have a very small beta. Thus its systematic VaR could be very low indeed.

A few months later, during September 2008, HBOS became insolvent. In this light, even the largest VaR estimate in the example above would seem too conservative. However, market risk capital is not for holding against this type of loss. It is only for covering everyday losses, usually in a balanced portfolio of shares. To quantify losses that arise from stress events such as the insolvency of a major bank, stress VaR analysis should be used.

IV.6.2.2 Risk Factor or Asset Returns Model

Much of our discussion in previous chapters has concerned the specification of the risk factor or asset returns model, i.e. the way that we model the evolution of the risk factors (or assets) over the risk horizon. The analyst faces several choices here and the most important of these are now reviewed.

1. Should we assume the returns are i.i.d. or should we capture volatility clustering and/or autocorrelation in returns?

This choice influences both the VaR estimate itself and the way that we scale VaR over different risk horizons, if this is done. Numerous examples and case studies in the previous four chapters have discussed the impact of volatility clustering and autocorrelated returns on VaR.17 In each case the importance of including volatility clustering effects in VaR estimates over risk horizons longer than a few days was clear. And, for a linear portfolio, we showed that even a small degree of autocorrelation in returns can have a significant impact on the scaling of short-term VaR to long-term risk horizons.

2. Should the distribution be parametric or historical?

At the daily frequency the historical distribution captures all the features of returns that we know to be important such as volatility clustering, skewness and leptokurtosis. It does this entirely naturally, i.e. without the complexity of fitting a parametric form. But to estimate VaR over a horizon longer than 1 day we need an h-day distribution for portfolio returns, and for reasons explained in previous chapters it is difficult to obtain an h-day historical distribution using overlapping data in the estimation sample. The exception is when we use filtered historical simulation (FHS), where the volatility adjusted historical distribution is augmented with a parametric dynamic model such as GARCH. An alternative to historical simulation is to find a suitable parameterization of the conditional distributions of the risk factor returns and to model these in a dynamic framework.

The advantages and limitations of both the parametric and the empirical (historical) approaches to building a statistical model for risk factor returns have been discussed earlier in this text. In Chapter IV.3 we described the influence of this choice on VaR estimates for a linear portfolio and in Chapter IV.5 we examined option portfolios, comparing Monte Carlo with historical VaR estimates.18 It is unlikely that the h-day risk factor return distributions based on historical data without filtering will provide VaR estimates that are as accurate as those based on appropriate parametric representations of the conditional risk factor return distributions. FHS may be more or less accurate than Student t EWMA VaR, but we cannot draw any conclusion without backtesting the performance of different models, as described later in this chapter.

3. If parametric, should the risk factor return distribution be normal, Student t, mixture or some other form (e.g. based on a copula)?

Our empirical exercises and studies have demonstrated, convincingly, that daily returns are usually neither i.i.d. nor normally distributed.19 Typically, both daily and weekly returns exhibit skewed and leptokurtic features. When volatility clustering is included and the model has a conditional framework, as in GARCH, it is possible for unconditional distributions to be skewed and leptokurtic even when conditional distributions are normal. But when skewness and leptokurtosis in portfolio returns are very pronounced even conditional distributions should be non-normal. Hence, for a daily VaR estimate to be truly representative of the stylized empirical features mentioned above, non-normal conditional distributions should be incorporated in the risk model at this stage.

What about VaR estimates over a horizon of a month or more? If daily log returns are i.i.d. then their aggregate, monthly log return has an almost normal distribution, by the central limit theorem. And if daily log returns exhibit volatility clustering their aggregates still (eventually) converge to a normal variable, even though the central limit theorem does not apply.20 Thus the decision about parametric form for the risk factor return distributions depends on the risk horizon. For example, whilst non-normal conditional models for risk factor return distributions are important for short-term VaR estimates, they are not especially useful for long-term VaR estimates. For long-term risk factor return distributions we may be fine using the multivariate normal i.i.d. assumption. Again, a complete answer can only be given after backtesting the models that are being considered.

4. How should the parameters of the risk factor returns model be estimated?

Even once we have fixed the distributional assumptions in parametric VaR estimates, the method used to estimate parameters can have a large impact on the VaR estimates. For instance, the RiskMetrics™ VaR estimates given in Example IV.2.26 are all based on the same i.i.d. normal assumption for risk factor returns, with an ad hoc value chosen for the smoothing constant. But the estimated VaR can differ enormously, depending on the sample data and the methodology used to estimate the risk factor returns model parameters. On changing the assumptions made here, a VaR or ETL estimate could very easily be doubled or halved! And we have seen that if the estimates are based on historical data, the sample size used to estimate the model parameters has a very significant impact on the VaR estimate. So, as well as backtesting the risk factor returns model, we also have to backtest the sample size, and/or anything else which determines the values that are chosen for the model parameters.

In summary, the four previous chapters have informed readers about the consequences of their decisions about the choices outlined above. Using numerous empirical examples and case studies to illustrate each choice, it has been possible to draw some general conclusions. For convenience, these conclusions are summarized below.

- If returns are autocorrelated, this affects the way that we scale the VaR estimate to longer horizons. Positive autocorrelation increases the VaR, and negative autocorrelation decreases the VaR.

- Incorporating volatility clustering makes the VaR estimate more risk sensitive. It will increase the VaR estimate if the market is currently more volatile than usual, and decrease the VaR estimate if the market is currently less volatile than usual.

- Parametric models for returns may produce VaR estimates that are less than or greater than the VaR estimates based on empirical return distributions. Often the empirical VaR estimates are greater than normal VaR estimates based on the same historical data, but this depends on the estimation sample and on the confidence level at which VaR is estimated.

- When the functional form of parametric distribution has leptokurtosis and negative skewness, the VaR at high confidence levels will be greater than the normal VaR. However, the opposite is the case at lower confidence levels.

- The data and methodology that are applied to estimate the parameters of the risk factor mapping and the returns model parameters can have a huge effect on the VaR estimate. However, it is not easy to know a priori how this choice will affect a particular VaR estimate.

When building a VaR model a market risk analyst enters a labyrinth where the path resulting from each choice leads to further choices, and each path branches into several paths. The outcome from each path is difficult to predict and outcomes resulting from quite different paths could be similar, or very different indeed. Given the myriad decisions facing the market risk analyst about the risk factor or asset return distributional assumptions, and given that the choices made play such an important role in the estimation of VaR and ETL, it is helpful to offer some guidance.

First, an analyst should choose distributional assumptions, including the assumptions about parameter values, that reflect his beliefs about the evolution of risk factor returns over the risk horizon. These assumptions need not be unique; indeed, the analyst may hold a distribution of beliefs over several different scenarios. In particular, these assumptions need not be based on the empirical distributions observed in the past, unless historical simulation is used to resolve the model. But it is sensible to base assumptions for short-term VaR estimates on current market conditions. For instance, at the time of writing, in the wake of the credit crisis, it is hardly feasible that equity markets and credit spreads will return to their previous levels of volatility within a short risk horizon. So the parameter estimates for short-term VaR estimation should take the current market conditions into account, even when subjective values are used rather than estimating model parameters from historical data.

Secondly, the analyst should build his model on sound principles, based on all the information that he believes is relevant to the evolution of the risk factors over the risk horizon. Nevertheless, building a model that – in the analyst's view – properly represents the returns process is not necessarily the same thing as building an accurate model. So the third point of guidance is to recognize that by far the most important aspect of building a risk model is the backtesting of this model.

The main purpose of this chapter is to explain how to perform backtests. Backtests need to be run using several alternative model assumptions. These assumptions concern the evolution of risk factor return distributions and the estimation of factor model parameters. The backtest results will tell the analyst how accurate the VaR and ETL estimates are for each of the models he is considering, using out-of-sample performance analysis that embodies the way that the model is actually used.

The model construction is based on many decisions, as we have explained above. And each choice facing the analyst should be backtested. Thus an analyst must invest much thought, time and effort into comparing how different model specifications perform in out-of-sample diagnostic tests. Backtests should be based on an estimation sample that is rolled over a long historical period. Additionally, the backtest data may include hypothetical scenarios that are designed to evaluate model performance during stressful markets.

IV.6.2.3 VaR Resolution Method

If historical VaR estimates at extreme quantiles are required there are several ways in which semi-parametric or parametric methods can be applied to fit the lower tails of the empirical portfolio returns or P&L distribution.21 Or, if we require historical VaR estimates over a risk horizon longer than a few days, then filtering the evolution of returns over the risk horizon has a very significant impact on the VaR estimates. And if Monte Carlo VaR estimation is used, there are several advanced sampling and variance reduction techniques that could be applied to reduce the sampling error.22

The only way to decide which VaR resolution method best suits the positions that the analyst must consider is to invest considerable time and effort in backtesting different approaches. Such research is likely to take months or years, but it is one of the most interesting parts of the analyst's job. Given the turmoil that has hit many markets during the year preceding the publication of this book, senior managers may be predisposed to allocate resources in this direction. Distributions that are approximated using Cornish–Fisher expansion may offer significant improvement on backtesting results for a standard historical VaR model. Adding filtering to simulate 3-day risk factor returns may have little impact on the quality of the 3-day backtest results. We do not know how much value is added by refining the VaR resolution method unless we do the backtests. However, sophisticated resolution methods may be less important to senior management than applying other types of refinements to enterprise-wide risk models. The implementation of an enterprise-wide VaR model that is capable of netting the risks of a large corporation is a huge undertaking, and aggregation risk in enterprise-wide risk estimates is by far the most important aspect of enterprise-wide risk model risk.23 Indeed, a market risk analyst may be well advised to accept a simple kernel fit and a simple EWMA filtering if he is using historical VaR, so that he can focus resources on the major challenge of aggregating different market risks across the firm.

IV.6.2.4 Scaling

Market risk analysts are also faced with a decision regarding the holding period of the VaR and ETL estimates. Should we estimate VaR and ETL directly over every risk horizon that is applied? The alternative is to estimate them over a short risk horizon and then scale them up, somehow, to obtain the VaR and ETL over a longer risk horizon. But how should this scaling be done? The answer depends on the type of portfolio (whether linear, or containing options) and the resolution method.

In the normal linear VaR model it is straightforward to implement either of these alternatives. In fact, if the risk factor returns are multivariate normal and i.i.d. and the expected excess return is zero, scaling will produce identical results to estimation directly over an h-day horizon. This is because we can scale either the covariance matrix or the final VaR estimate using the square-root-of-time rule. The exception is when the portfolio is not assumed to return the risk free rate. In that case, VaR does not scale with the square root of time, even when returns are i.i.d., and we should estimate the normal linear VaR directly over the risk horizon. And when the portfolio is assumed to return the risk free rate, as is usually the case in banks, but the portfolio returns are positively (negatively) autocorrelated, we should scale up short-term VaR to be greater than (less then) the VaR that is implied by a square-root scaling rule.

In the historical VaR model without filtering, the use of overlapping data truncates the tail of the portfolio return distribution, so that ETL (and VaR at extreme quantiles) can be seriously underestimated. So unless we add some parametric filtering for modelling dynamic portfolio returns over the h-day horizon we are initially forced to estimate VaR and ETL at the daily level. As explained in Section IV.3.2, it may be possible to uncover a power law scaling rule, to extend the daily VaR to longer horizons, but this can only be applied to linear portfolios, or to estimate the dynamic VaR of option portfolios.24 If there is no power law or if it is not the square root of time, using a square-root-of-time rule can lead to a very serious error in long-term VaR estimates.

In the Monte Carlo VaR model we can either estimate VaR directly over the risk horizon or, under certain assumptions, scale up a short-term VaR estimate to a longer horizon. If the risk factor returns are multivariate normal i.i.d. the two approaches only give the same result for a linear portfolio.25 For option portfolios the two approaches to estimating long-term VaR yield different results. The approach that is used will depend on the portfolio's valuation (i.e. Taylor approximation versus full valuation) and the rebalancing assumption for the portfolio over the risk horizon.26

IV.6.3 ESTIMATION RISK

Even in the context of a single risk factor returns model and a single VaR resolution method, VaR estimates can vary enormously according to our choice of sample data and our choice of estimation methodology. For example, the resolution method may be a standard historical simulation, in which case the risk factor return distribution will be a simulated empirical distribution, but VaR estimates can be very sensitive to the sample size, i.e. the number of historical simulations used. In fact, the case study in Section IV.3.3.1 showed that the sample size is a much more important determinant of the VaR estimate than the resolution method.

For another example, under the normal i.i.d. assumption for returns, a risk factor covariance matrix might be estimated using an equally weighted average of the previous T daily returns, the estimation sample size T being chosen fairly arbitrarily. Or we may use an exponentially weighted moving average with some ad hoc value for the smoothing constant λ. In both these cases we can estimate the standard error of the estimator.27 It is useful to extend these standard errors to an approximate standard error for a VaR estimate. These standard errors could indicate, for example, whether there is a statistically significant difference between two different VaR estimates. Alternatively, they can be used to obtain an approximate confidence interval for a VaR estimate. That is what we do in this section: we derive approximate confidence intervals for VaR estimates, based on both analytic and simulation VaR resolution methods.

IV.6.3.1 Distribution of VaR Estimators in Parametric Linear Models

If the portfolio is expected to return the risk free rate, the VaR estimate in the normal or Student t linear model behaves like volatility. For a fixed significance level α and a fixed risk horizon of h days, the 100α% h-day VaR estimate is a constant times the portfolio volatility. If this volatility is estimated using an equally weighted average of squared returns based on a sample of size T, or if it is estimated using EWMA with a given λ, we can derive the confidence interval for VaR from the known confidence interval for volatility, as described below.

Normally Distributed Portfolio Returns

The assumption that portfolio returns are i.i.d. normal leads to the formula

where ![]() is the estimated standard deviation of the portfolio's daily returns. For simplicity, we assume the portfolio is expected to return the risk free rate.

is the estimated standard deviation of the portfolio's daily returns. For simplicity, we assume the portfolio is expected to return the risk free rate.

Since the quantile Φ−1(1 − α) of the standard normal distribution and the square root of the holding period ![]() are both constant, we may use the standard error of the standard deviation estimator to derive a standard error for the VaR estimate. In Section II.3.5.3 it is proved that the standard error of the equally weighted standard deviation estimator

are both constant, we may use the standard error of the standard deviation estimator to derive a standard error for the VaR estimate. In Section II.3.5.3 it is proved that the standard error of the equally weighted standard deviation estimator ![]() , when it is based on a sample of size T, is approximated by

, when it is based on a sample of size T, is approximated by

Hence, in this case the standard error of the VaR estimator at the portfolio level is approximately equal to

In Section II.3.8.5 it is proved that the standard error of the EWMA standard deviation estimator ![]() , when it is based on a smoothing constant λ, is approximated by

, when it is based on a smoothing constant λ, is approximated by

Hence, the standard error of the VaR estimator at the portfolio level is approximately equal to

EXAMPLE IV.6.3: CONFIDENCE INTERVALS FOR NORMAL LINEAR VAR

Portfolio returns are assumed to be i.i.d. and normally distributed. When the portfolio volatility is estimated as 20%, estimate the 100α% h-day normal linear VaR and its approximate standard error for different values of α and h,

(a) an equally weighted model with a sample size 100, and

(b) EWMA with a smoothing constant of 0.94.

How do your results change for different sample sizes in (a) and for different smoothing constants in (b)?

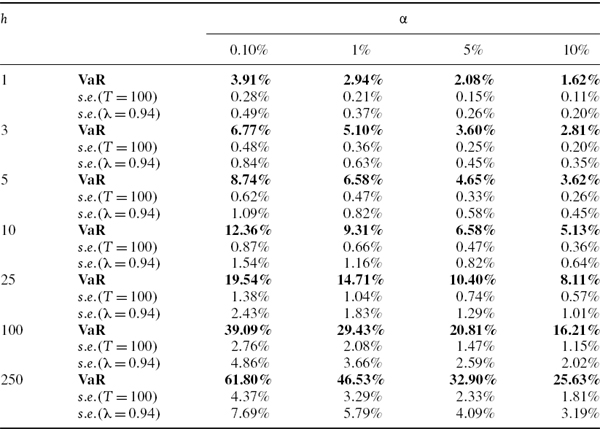

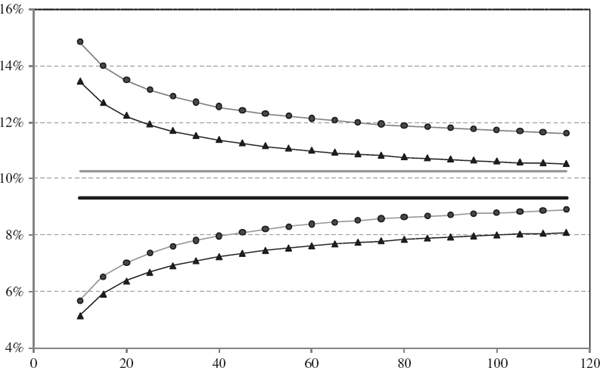

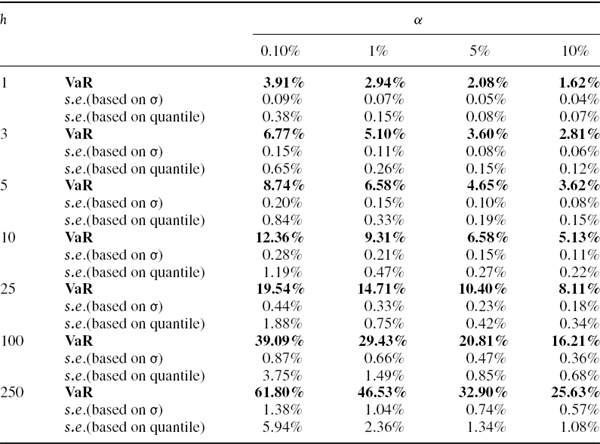

SOLUTION The VaR estimates based on (IV.6.1) and their standard errors based first on (IV.6.3) with T = 100, and then on (IV.6.5) with λ = 0.94, are calculated in the spreadsheet for different values of α and h, and the results are displayed in Table IV.6.5. The VaR estimates and their standard errors increase with both the risk horizon and the confidence level. For our choice of parameters, i.e. T = 100 and λ = 0.94, the EWMA VaR estimates are less precise than the equally weighted estimates, since their standard errors are always greater.

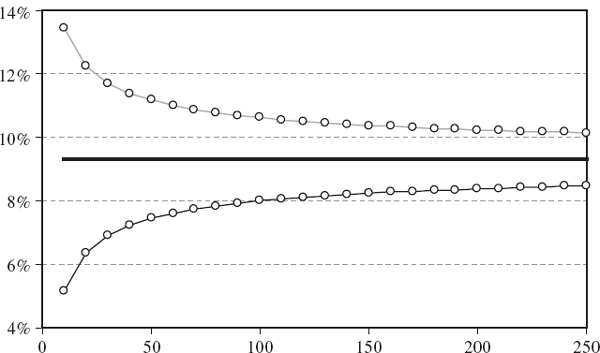

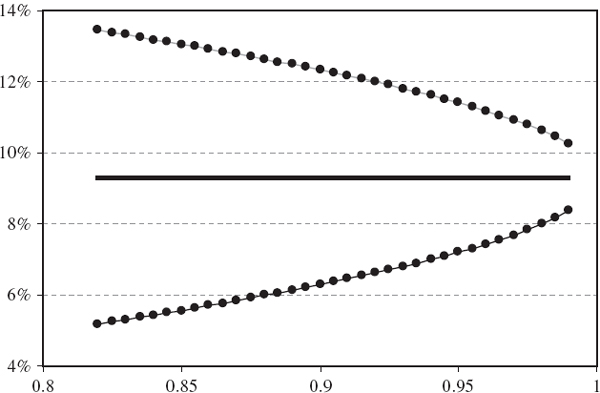

How do these standard errors behave as the sample size changes in the equally weighted model, or as the smoothing constant changes in the EWMA model? Figure IV.6.2 depicts the 1% 10-day normal linear VaR estimate (by the horizontal black line at 9.31%) and two-standard-error bounds, based on the equally weighted estimate (IV.6.3) for different values of T. Figure IV.6.3 depicts the same VaR estimate of 9.31% and two-standard-error bounds based on the EWMA estimate (IV.6.5) for different values of λ. Both graphs are based on the assumption that returns are i.i.d. and the portfolio volatility is 20%. The standard errors decrease as the sample size increases in the equally weighted model, and decrease as the smoothing constant increases in the EWMA model.

The equally weighted variance estimate is a sum of i.i.d. variables,28 so by the central limit theorem its distribution converges to a normal distribution. But the VaR estimate behaves like the square root of the variance.29 In fact, the standard errors shown in these figures are approximated using Taylor expansion, as in Section II.3.5.3, without knowing the functional form of the volatility estimator.

Table IV.6.5 Normal linear VaR estimates and approximate standard errors

Figure IV.6.2 1% 10-day VaR with two-standard-error bounds versus sample size

Figure IV.6.3 1% 10-day VaR with two-standard-error bounds versus EWMA λ

Student t Distributed Portfolio Returns

From our discussion in Section IV.2.8.2 we know that the one-period VaR estimate based on an assumed i.i.d. Student t distribution for portfolio returns, with ν degrees of freedom, is

where σ is the standard deviation of the portfolio's daily returns and the portfolio is expected to return the risk free rate. When h is relatively small the errors from square-root scaling on a Student t distribution are not too large, so a very approximate formula for the 100α% h-day VaR,30 as a proportion of the portfolio value, is

When h is more than about 10 days (or more, if ν is relatively small) the normal linear VaR formula should be applied, because the sum of h i.i.d. Student t distributed returns will have an approximately normal distribution, by the central limit theorem.

In the linear VaR model the leptokurtosis of a Student t distribution usually increases the 1% VaR estimate and its estimated standard errors, relative to a normal distribution assumption. Figure IV.6.4 compares the 1% 10-day VaR estimate, and the two-standard-error bounds, based on normal returns and based on Student t returns with 6 degrees of freedom.31 As in the previous figures the sample size is shown on the horizontal axis, and we suppose that the portfolio volatility is 20%, but this – and the degrees of freedom and other parameters – can be changed in the spreadsheet. As expected, the confidence intervals become wider under the Student t assumption, but the main effect of the leptokurtosis that is introduced by the Student t distribution is to increase the 1% VaR estimate itself, from 9.31% 10.26%. This is depicted by the horizontal grey line in the figure, and the two-standard-error bounds on the student t VaR are depicted by the lines with circle markers.

Figure IV.6.4 1% 10-day VaR with two-standard-error bounds – Student t versus normal

When linear VaR estimates are based on a multivariate elliptical (i.e. normal or Student t) i.i.d. model for risk factor returns, estimation risk arises from the covariance matrix estimator which, as we know from Chapter II.3, can be equally weighted or exponentially weighted. In the case of equities, another important source of estimation risk arises from the model used to estimate the factor betas. The risk factor return distribution parameters, and the factor betas are not necessarily based on the same model, or even on the same sample. And even when they are, it is quite complex to estimate the standard error of a quadratic form: the VaR estimator is a non-linear estimator and so its variance does not obey simple rules.

IV.6.3.2 Distribution of VaR Estimators in Simulation Models

Rather than derive an approximate formula for the multivariate elliptical linear VaR estimates, we might consider using an approximate standard error for a quantile estimator directly, as explained below. But these standard errors are much less precise than those considered in the previous subsection. That is because those derived from the variance estimator, whilst still approximate, utilize the normality (or Student t) assumption for the portfolio returns, whilst the standard errors for quantile estimators use no information about the return distribution (other than that it be continuous) and – so that we can derive a relatively simple form for the standard error of a quantile estimator – they employ a very crude assumption that the density is constant in the relevant region of the tail.

When VaR estimation is based on historical or Monte Carlo simulation, sampling error can be a major cause of estimation risk. Even in the standard historical model (i.e. the model with no parametric or semi-parametric volatility adjustment or filtering of returns) sampling error can introduce considerable uncertainty into the VaR estimate. Sampling error is usually much easier to control in the Monte Carlo VaR model but, unlike standard historical simulation, the Monte Carlo approach is also prone to estimation risk stemming from inaccuracy in parameter estimates.

For instance, using a normal i.i.d. model for portfolio returns in Monte Carlo VaR, we have a sampling variation which depends on the number of Monte Carlo simulations, and we also have a standard error of the VaR estimate arising from the volatility estimator, as described in the previous subsection. Variance reduction techniques – and using a very large number of simulations – can reduce sampling variation substantially, so the parameter estimation risk and the more general model risk arising from the choice of parametric form tend to dominate the standard error of the Monte Carlo VaR estimate. Quite the opposite is the case for the standard historical simulation VaR model. Here there are no parameters to estimate so the historical sample size has everything to do with the efficiency of the quantile estimator.

As a proportion of the portfolio value, VaRh,α is −1 times the α quantile of an h-day portfolio return distribution. So standard errors for historical VaR may be derived from an approximate distribution for the estimator of an α quantile, based on a random sample size T.

Let us denote the α quantile estimator based on a random sample size T by q(T, α). First we derive the distribution of the number of observations less than the α quantile, denoted X(T, α). Then we translate this into a distribution for p(T, α) = T−1X(T, α), the proportion of returns less than the α quantile. Finally. we derive the distribution of q(T, α) = F−1(p(T, α), where F denotes the distribution function of the portfolio returns, using an approximation.

Since the sample is random, X(T, α) has a binomial distribution with parameters T and α. Hence, its expectation and variance are Tα and Tα (1 − α), respectively.32 But as T → ∞ and when α is fixed, a special case of the central limit theorem tells us that the binomial distribution converges to a normal distribution,

Dividing both the numerator and the denominator of this statistic by T, we have

We have already used this result to derive approximate confidence intervals for quantiles, and a numerical example to demonstrate this is given in Section II.8.4.1. But here we want to derive an approximate standard error for the quantile in large samples. So, on noting that p(T, α) = F(q(T, α), we first write (IV.6.8) as

Following Kendall (1940), we now assume that F is approximately linear ‘in the material range of the sampling distribution’. That is, we use the local approximation

![]()

where f(q(T, α) is the density function at q(T, α). In other words, the density function is assumed to be flat in the region of the tail that we are considering. Substituting this in (IV.6.9) gives an approximate distribution for q(T, α) as

In particular, an approximate standard error for the quantile estimator q (T, α) is given by

Since the 100α%VaR is − q(T, α), it has the same standard error as q(T, α).

The formula just derived requires knowledge of the portfolio return distribution, and in particular of its density function f. Then it may be applied to estimate approximate standard errors for historical VaR estimates. However, these standard errors are based on a very strong assumption about the shape of the tail of the distribution, i.e. that it is locally flat. So the standard errors (IV.6.11) are very approximate indeed. To demonstrate this, the following example compares standard errors that are estimated using (IV.6.11) with those based on (IV.6.3) in the case where the density function in (IV.6.11) is known to be normal.

EXAMPLE IV.6.4: CONFIDENCE INTERVALS FOR QUANTILES

Given a random sample of size 1000 from a normal distribution with known mean zero and volatility 20%, derive the approximate standard errors (IV.6.11) for 100α% h-day VaR, for different values of α and h. How does the result change with the random sample size? Compare these standard errors with the estimated standard errors (IV.6.3) that are based on sampling error in equally weighted volatility estimators.

SOLUTION When the distribution is known to be normal with mean zero and volatility σ, the quantile estimate q(T, α) is given by the Excel function NORMINV (α, 0, σ), and this is independent of the sample size T. The first factor on the right-hand side of (IV.6.11), i.e. f(q(T, α)−1, is given by the Excel function

![]()

and the dependence of the estimated standard error on sample size only enters through the second factor ![]() in (IV.6.11).

in (IV.6.11).

In the spreadsheet we compute (IV.6.11) for different values of α and h and with a sample size of 1000. Results are summarized in Table IV.6.6, which is similar to Table IV.6.5 except that, for comparison with the quantile-based standard errors, the sample size for the equally weighted volatility-based standard errors is 1000 rather than 100. As a result, the estimated standard errors based on σ are much smaller than those in Table IV.6.5.

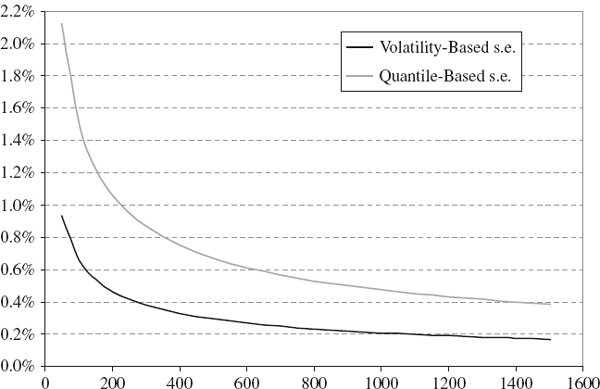

Figure IV.6.5 depicts the estimated standard error of the 1% 10-day VaR estimate based on (a) the equally weighted volatility estimator for σ and (b) the quantile estimator. As in the example above, we assume the population is normal with mean zero and volatility 20%, so the VaR estimate is 9.31% of the portfolio value. The figure shows the effect that sample size has on the standard error of the VaR estimate. For small samples, the precision of the quantile estimates is very low. For every sample size, the quantile-based standard error is approximately twice the size of the volatility-based standard errors.33

Table IV.6.6 VaR standard errors based on volatility and based on quantile

Figure IV.6.5 Standard errors of 1% 10-day VaR estimate Note: This graph assumes portfolio returns are normal with volatility of 20%.

IV.6.4 MODEL VALIDATION

This section presents a series of increasingly complex approaches to VaR model validation through out-of-sample forecast evaluation techniques that are commonly termed backtests. Failure of a backtest indicates VaR model misspecification and/or large estimation errors, and regression-based backtests may also help diagnose the cause of a model failure.

IV.6.4.1 Backtesting Methodology

A backtest takes a fixed portfolio, which we shall call the candidate portfolio, and uses this portfolio to assess the accuracy of a VaR model. The term ‘candidate portfolio’ is used to denote a portfolio that represents a typical exposure to the underlying risk factors. If the portfolio is expressed in terms of holdings in certain assets or instruments, we assume the weights or the holdings are fixed for the entire backtest.34 More usual is to express the portfolio in terms of a risk factor mapping, in which case – for a dynamic VaR estimate – we assume the risk factor sensitivities are constant throughout the backtest.

The result of a backtest depends on the portfolio composition, as well as on the evolution of the risk factors and the assumptions made about risk factor return distributions when building the model. Thus, it is possible for the same VaR model to pass a backtest for portfolio A, but fail a backtest for portfolio B, even when the portfolios have identical underlying risk factors.

We should perform a backtest using a very long period of historical data on the asset or risk factor values. Otherwise the test will lack the power to reject inaccurate VaR models. And because we need to base the test on a very large non-overlapping sample, backtests are usually performed at the daily frequency. So in the following we shall assume we have a large sample of daily returns on all the relevant risk factors. The entire data period will often encompass many years. For instance, more than 10 years of daily data are needed to backtest ETL, as described later in this section. The longer the backtest period, the more powerful the results will be.

First, assuming the VaR estimate will be based on historical data,?35 we fix an estimation period which defines the sample used to estimate the VaR model parameters. We tend to use much shorter estimation periods for parametric linear VaR models and Monte Carlo VaR models than we do for historical simulation VaR models. And in the parametric models, the estimation period also tends to increase with the risk horizon. This is because smaller samples yield VaR estimates that are more risk sensitive, i.e. that respond more to changes in the current market conditions.

Then we employ a rolling window approach as follows. The estimation sample is rolled over almost the entire data period, keeping the estimation period constant, starting at the beginning of the data period. We fix the length of the risk horizon, and the test sample starts at the end of the estimation sample. If the risk horizon is h days, we roll the estimation and test periods forward h days, and we keep rolling the estimation and test samples over the entire data period until the test sample ends on the last day of our data period. In this way, we do not use overlapping data in the test sample.

Figure IV.6.6 illustrates the rolling window approach: the bold line at the bottom indicates the whole sample covering the entire historical data period. The estimation and test samples are shown in black and grey, respectively; during the backtest these are rolled progressively, h days at a time, until the entire sample is exhausted.

Figure IV.6.6 Rolling windows with estimation and test samples

For example, consider a sample with 10,000 daily observations where the estimation sample size is 1000 days and the risk horizon is 10 days. The backtest proceeds as follows. Use the estimation sample to estimate the 10-day VaR on the 1000th day, at the required confidence level. This is the VaR for the 10-day return from the 1000th to the 1010th observation. Then, assuming the VaR is expressed as a percentage of the portfolio value, we observe the realized return over this 10-day test period, and record both the VaR and the realized return.36 Then we roll the window forward 10 days and repeat the above, until the end of the entire sample. The result of this procedure will be two time series covering the sample from the 1010th until the 10,000th observation, i.e. covering all the consecutive rolling test periods. One series is the 10-day VaR and the other is (what econometricians call) the 10-day ‘realized’ return or P&L on the portfolio. The backtest is based on these two series.

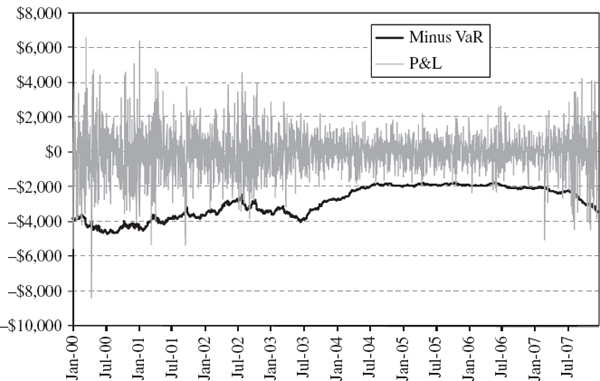

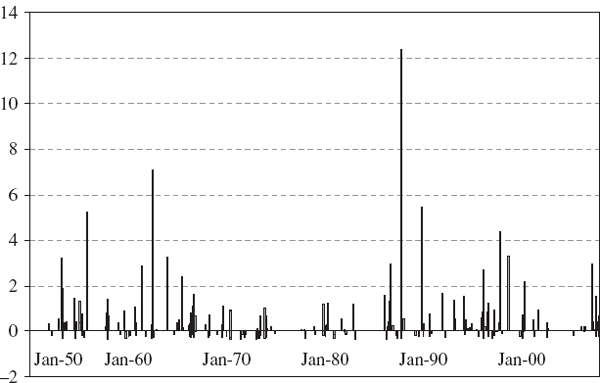

Figure IV.6.7 depicts two such series that will form the basis of most of the backtests that are illustrated in this section.37 The backtest sample, which is constructed from all the consecutive test periods, is from January 2000 until December 2007. For simplicity there will be 2000 observations in many of the backtests, and we shall base the tests on the 1% daily VaR. So we expect the VaR to be exceeded 20 times (in other words, the expected number of exceedances is 20). Exceedances occur when the portfolio loses more than the VaR that was predicted at the start of the risk horizon.38 We have depicted the series −1 times the VaR prediction in the figure so that the exceedances are obvious when the grey P&L line crosses the black VaR line; for instance, an exceedance already occurs on the very first day of the backtest sample. In total the VaR is exceed 33 times, not 20 times, in this figure. By changing the parameters in the spreadsheet readers will see that the 5% daily VaR is exceeded 105 times instead of 100 times.39 It appears that our VaR estimates may be too low because a higher VaR would give fewer exceedances. How can we use this information to construct a statistical test of the hypothesis that the VaR estimates provide accurate forecasts?

Figure IV.6.7 1% daily VaR and daily P&L

Most backtests on daily VaR are based on the assumption that the daily returns or P&L are generated by an i.i.d. Bernoulli process. A Bernoulli variable may take only two values, which could be labelled 1 and 0, or ‘success’ and ‘failure’. In our context, we would call ‘success’ an exceedance of the VaR by the return or P&L, and further assign this the value 1. Thus we may define an indicator function Iα,t on the time series of daily returns or P&L relative to the 100α% daily VaR by

Here Yt+1 is the ‘realized’ daily return or P&L on the portfolio from time t, when the VaR estimate is made, to time t + 1.40

If the VaR model is accurate and {Iα, t} follows an i.i.d. Bernoulli process, the probability of ‘success’ at any time t is α. Thus the expected number of successes in a test sample with n observations is nα. Denote the number of successes by the random variable Xn, α. From Section I.3.3.1 we know that our assumptions imply that Xn, α has a binomial distribution with parameters n and α. Thus

The standard error of the estimate, ![]() , provides a measure of uncertainty around the expected value. Due to sampling error we are unlikely to obtain exactly the expected number of exceedances in a backtest; instead we should consider a confidence interval around the expected value within which it is very likely that the observed number of exceedances will fall. When n is very large the distribution of Xn, α is approximately normal, so a two-sided 95% confidence interval for Xn, α under the null hypothesis that the VaR model is accurate is approximately

, provides a measure of uncertainty around the expected value. Due to sampling error we are unlikely to obtain exactly the expected number of exceedances in a backtest; instead we should consider a confidence interval around the expected value within which it is very likely that the observed number of exceedances will fall. When n is very large the distribution of Xn, α is approximately normal, so a two-sided 95% confidence interval for Xn, α under the null hypothesis that the VaR model is accurate is approximately

For instance, if n = 2000 and α = 1% the standard error is ![]() . So, based on (IV.6.15), a 95% confidence interval for the number of exceedances is approximately (11.28, 28.72). The observed value of 33 exceedances for the 1% daily VaR in Figure IV.6.7 lies outside this interval, so obtaining such a value is likely to lead to a rejection of the null hypothesis, but this depends on the particular backtest that we employ. The rest of this section describes different backtest statistics, most of which are based on the exceedances that have been described above.

. So, based on (IV.6.15), a 95% confidence interval for the number of exceedances is approximately (11.28, 28.72). The observed value of 33 exceedances for the 1% daily VaR in Figure IV.6.7 lies outside this interval, so obtaining such a value is likely to lead to a rejection of the null hypothesis, but this depends on the particular backtest that we employ. The rest of this section describes different backtest statistics, most of which are based on the exceedances that have been described above.

IV.6.4.2 Guidelines for Backtesting from Banking Regulators

Section IV.8.2.4 describes the use of VaR models for estimating regulatory market risk capital and, in particular, the use of a multiplier to convert VaR estimates into the minimum market risk capital requirement. Banking supervisors will only allow internal models to be used for regulatory capital calculation if they provide satisfactory results in backtests. The 1996 Amendment to the 1988 Basel Accord contains a detailed description of the backtests that supervisors will review and models that fail them will either be disallowed for use in regulatory capital calculations, or be subject to the highest multiplier value of 4.

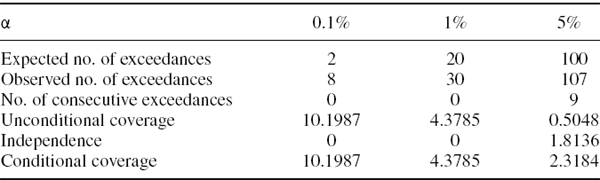

Regulators recommend a very simple type of backtest, which is based on a 1% daily VaR estimate and which covers a period of only 250 days. Hence, the expected number of exceedances is 2.5 and the standard error of the number of exceedances, i.e. the square root of (IV.6.14), is ![]() . Regulators wish to guard against VaR models whose estimates are too low. Since they are very conservative they will only consider that models having 4 exceptions or less as sufficiently accurate. These so-called green zone models have a multiplier of 3. If there are between 5 and 9 exceptions, the model is yellow zone, which means it is admissible for regulatory capital calculations but the multiplier is increased as shown in Table IV.6.7. A red zone model means there are 10 or more exceptions. Then the multiplier takes its maximum of value 4, or the VaR model is disallowed.

. Regulators wish to guard against VaR models whose estimates are too low. Since they are very conservative they will only consider that models having 4 exceptions or less as sufficiently accurate. These so-called green zone models have a multiplier of 3. If there are between 5 and 9 exceptions, the model is yellow zone, which means it is admissible for regulatory capital calculations but the multiplier is increased as shown in Table IV.6.7. A red zone model means there are 10 or more exceptions. Then the multiplier takes its maximum of value 4, or the VaR model is disallowed.

When regulatory capital is calculated using an internal VaR model it is based on 1% 10-day VaR. So why do regulators ask for backtests of daily VaR? It would be difficult to perform a backtest on 250 non-overlapping 10-day returns, since the data would need to span at least 10 years for the backtest to have sufficient accuracy. Is it possible to derive a simple table such as Table IV.6.7 using overlapping data in certain backtests, i.e. to roll the estimation and test periods forward by only one day even when the risk horizon is longer than one day? Then we could not use our standard assumption that exceedances follow an i.i.d. Bernoulli process. Exceedances would be positively autocorrelated (for instance, one extremely large daily loss would impact on ten consecutive 10-day returns) and so, whilst the expected number of exceedances would remain unchanged from (IV.6.13), the variance would no longer be equal to (IV.6.14). In fact, it would be much greater than (IV.6.14) because the exceedances are positively autocorrelated, so the confidence interval (IV.6.15) would become considerably wider and the backtest would have even lower power that it does already.

Table IV.6.7 Basel zones for VaR models

| Number of exceedances | Multiplier for capital calculation |

| 4 or less | 3 |

| 5 | 3.4 |

| 6 | 3.5 |

| 7 | 3.65 |

| 8 | 3.75 |

| 9 | 3.85 |

| 10 or more | 4 |

Nevertheless, in practice 10-day VaR estimates are based on overlapping samples, since we estimate 1% 10-day VaR every day. So we have allowed readers to use most of the spreadsheets for this chapter to examine the pattern of exceedances based on overlapping data. Daily clustering of exceptional losses that exceed the VaR is much more likely when both the VaR estimate and the P&L are based on a 10-day risk horizon. By examining series such as these 10-day returns based on overlapping samples, banks could gauge the likelihood that their minimum regulatory capital may be exceeded on every day during one week, for instance. Formal backtests are difficult to derive theoretically for overlapping estimation samples, but at least banks would be examining the 10-day VaR estimates that they actually use for their risk capital calculations.

Most regulators allow banks to base regulatory capital on daily VaR estimates and then scale these estimates up using a square-root-of-time rule. But this rule is only valid for linear portfolios with i.i.d. normally distributed returns, and since most portfolios have non-normally distributed returns that are not i.i.d., the use of square-root scaling is a very common source of model risk. If regulators changed the number exceedances in green, yellow and red zones to correspond to autocorrelated 10-day VaR estimates, resulting from overlapping estimation samples, then banks would have the incentive to increase the accuracy of 10-day VaR estimates by scaling their daily VaR appropriately, or by estimating 10-day VaR directly without scaling up the daily VaR at all. Another feature of regulatory backtests that is not easy to understand is why they require only 250 days in the backtest. With such a small sample the power of the test to reject a false hypothesis is very low indeed. So, all in all, it is highly likely that an inaccurate VaR model will pass the regulatory backtest.

VaR estimates are based on one of two theoretical assumptions about trading on the portfolio. Either the portfolio is assumed to be rebalanced over the risk horizon to keep its asset weights or risk factor sensitivities constant, or it is assumed that the portfolio is held static so that no trading takes place and the holdings are constant. The assumption made here influences the VaR estimate for option portfolios over risk horizons longer than 1 day. But both assumptions lack realism. In practice, portfolios are actively managed at the trader's discretion, and the actual or realized P&L on the portfolio is not equal to the hypothetical, unrealized P&L, i.e. the P&L on which the VaR estimate is based. In accountancy terminology the unrealized P&L is the mark-to-market P&L, whereas the realized P&L includes all the P&L from intraday trading and is based on prices that are actually traded. Realized P&L may also include fee income, any use of the bank's reserves and funding costs. With these additional items we call it actual P&L and without these it is called cleaned P&L. To avoid confusion, we shall call the hypothetical, unrealized P&L the theoretical P&L.

Many banking regulators (for instance, in the UK) require two types of backtests, both of which are based on the simple methodology described above. Their tests must be based on both realized (actual or cleaned) P&L and on theoretical P&L. Backtests based on theoretical P&L are testing the VaR model assumptions. However, those based on realized 1-day P&L are not testing how the model will perform in practice, as a means of estimating regulatory capital, unless the scaling of 1-day VaR to 10-day VaR is accurate.

IV.6.4.3 Coverage Tests

Unconditional coverage tests, introduced by Kupiec (1995), are also based on the number of exceedances, i.e. the number of times the portfolio loses more than the previous day's VaR estimate in the backtest. They may be regarded as a more sophisticated and flexible version of the banking regulators' backtesting rules described above. The idea was both formalized and generalized by Christoffersen (1998) to include tests on the independence of exceedances (i.e. whether exceedances come in clusters) and conditional coverage tests (which combine unconditional coverage and independence into one test). Section II.8.4.2 described these tests in the context of any model for forecasting either or both tails, or indeed any interval of a distribution. In this subsection we discuss their application to VaR models, which specifically forecast the lower tail of a portfolio returns or P&L distribution.

An unconditional coverage test is a test of the null hypothesis that the indicator function (IV.6.12), which is assumed to follow an i.i.d. Bernoulli process, has a constant ‘success’ probability equal to the significance level of the VaR, α. The test statistic is a likelihood ratio statistic given by (II.8.17) and repeated here for convenience. It is

where πexp is the expected proportion of exceedances, πobs is the observed proportion of exceedances, n1 is the observed number of exceedances and n0 = n − n1 where n is the sample size of the backtest. So n0 is the number of returns with indicator 0 (we can call these returns the ‘good’ returns). Note that πexp = α and πobs = n1/n. The asymptotic distribution of −2ln LRuc is chi-squared with one degree of freedom.

EXAMPLE IV.6.5: UNCONDITIONAL COVERAGE TEST

Perform an unconditional coverage test on the 1% daily VaR for a $100 per point position on the S&P 500 index, where the backtest is based on 2000 observations from January 2000 to December 2007, as in Figure IV.6.7.

SOLUTION We have 33 exceedances based on sample of size 2000. Hence

It is better to compute the log of the likelihood ratio statistic directly, rather than computing (IV.6.16) and afterwards taking the log, because in this way the rounding errors are reduced. Hence, we use the parameter values (IV.6.17) to calculate

![]()

obtaining the value −3.5684. Hence −2ln LRuc = 7.1367. The 1% critical value of a chi-squared distribution with one degree of freedom is 6.6349. So we reject, at the 1% significance level, the null hypothesis that the VaR model is accurate in the sense that the total number of exceedances is close to the expected number.

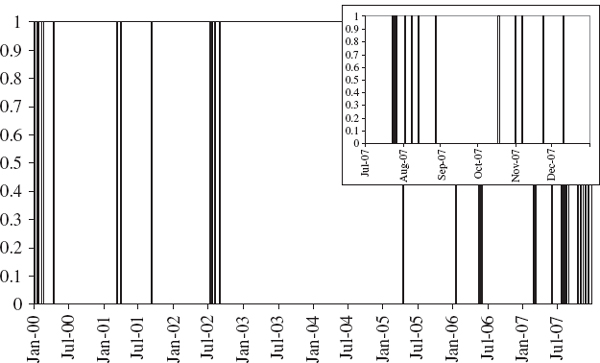

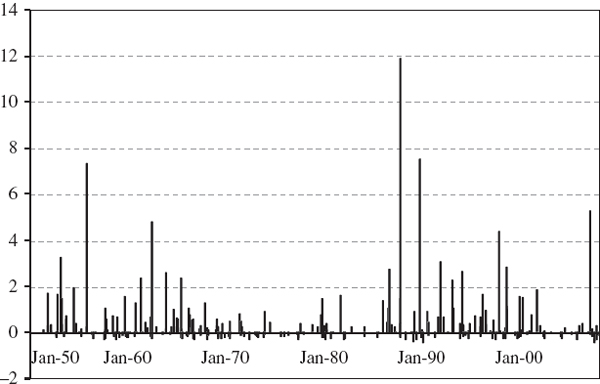

Using the spreadsheet for Example IV.6.5 we can plot the indicator function (IV.6.12) for the case α = 1% and h = 1. This is shown in Figure IV.6.8. It is clear from this figure that the exceedances come in clusters. There are no exceedances at all in 2003 and 2004, but plenty during 2007. In fact, during the last six months of the backtest there are 12 exceedances, shown in the inset to the figure, although the expected number is less than 2.

Figure IV.6.8 Indicator of exceedances

Clustering of exceedances indicates that the VaR model is not sufficiently responsive to changing market circumstances. In the case in point, the last six months of the backtest marked the beginning of the credit crisis. But the normal linear VaR estimates here were based on an equally weighted average of the last 250 squared log returns, so this model does not account for the volatility clustering that we know is prevalent in many markets. Even if the model passes the unconditional coverage test, i.e. when the observed number of exceedances is near the expected number, we could still reject the VaR model if the exceedances are not independent.

A test for independence of exceedances is based on the formalization of the notion that when exceedances are not independent the probability of an exceedance tomorrow, given there has been an exceedance today, is no longer equal to α. As before, let n1 be the observed number of exceedances and n0 = n − n1 be the number of ‘good’ returns. Further, define nij to be the number of returns with indicator value i followed by indicator value j, i.e. n00 is the number of times a good return is followed by another good return, n01 the number of times a good return is followed by an exceedance, n10 the number of times an exceedance is followed by a good return, and n11 the number of times an exceedance is followed by another exceedance. So n1 = n11 +n01 and n0 = n10 +n00. Also let

i.e. π01 is the proportion of exceedances, given that the last return was a ‘good’ return, and π11is the proportion of exceedances, given that the last return was an exceedance. Now we can state the independence test statistic, derived by Christoffersen (1998), as

The asymptotic distribution of −2ln LRind is chi-squared with one degree of freedom.

EXAMPLE IV.6.6: INDEPENDENCE TEST

Perform the independence test for the data of the previous example.

SOLUTION In addition to the results in (IV.6.17) we have only two sets of two consecutive exceedances. The rest are isolated, if only separated by a few days in many cases, as is evident from Figure IV.6.8. Hence,

![]()

Using these values in (IV.6.18) and in (IV.6.19) gives ln (LRind) = −1.2134, so −2ln LRuc = 2.4268. The 10% critical value of a chi-squared distribution with one degree of freedom is 2.7055. Hence, we cannot even reject the null hypothesis that the exceedances are independent at 10%.

Why is the independence test unable to detect the clustering in exceedances that is clearly evident from Figure IV.6.8? The problem is that in the above example we often have a day (or two or three) with no exceedance coming between two exceedances, and the Christoffersen independence test only works if exceedances are actually consecutive. That is because the test is based on a first order Markov chain only, and to detect the type of clustering we have in this example it would have to be extended to a higher order Markov chain, to allow more than first order dependence.

A combined test, for both unconditional coverage and independence, is the conditional coverage statistic given by

The asymptotic distribution of −2ln LRcc is chi-squared with two degrees of freedom. On comparing the three test statistics it is clear that LRcc = LRuc × LRind, i.e.

![]()

For instance, in the above examples we have

![]()

The 5% critical value of the chi-squared distribution with 2 degrees of freedom is 5.9915 and the 1% critical value is 9.2103. Hence we reject the null hypothesis at 5% but not (quite) at 1%.

IV.6.4.4 Backtests Based on Regression

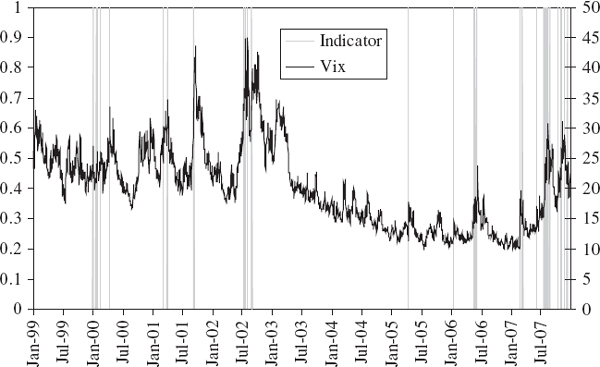

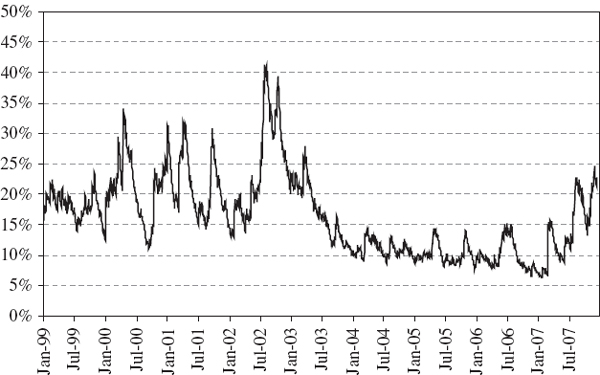

In our empirical examples of the previous subsection, where we were backtesting a normal linear VaR model for a simple position on the S&P 500 index, the results suggested that the clustering of exceedances could be linked to market volatility. This would be the case when a VaR model is not accounting adequately for the volatility clustering in a portfolio's returns. Indeed, such a link is clear from Figure IV.6.9, which shows the indicator of exceedances alongside the Vix (the S&P 500 implied volatility index) over the same period as the backtest. Exceedances are more common when there is a large daily change in the implied volatility, especially when volatility jumps upward after a long period of low volatility. This observation explains why we have so many exceedances during the recent credit crisis, and provides an understanding of how to improve the VaR model. This observation also suggests a backtest based on a regression model that takes the indicator function as the dependent variable and, in this case, the daily change in the Vix as the explanatory variable.

If past information can be used to predict exceedances, the VaR model is not utilizing all the information available in the market. More generally, if we believe that the VaR model is misspecified because it is not utilizing information linked to lagged values of one or more variables, which we summarize in the vector x = (X1,…, Xk), then a backtest could be based on a regression model of the form

Figure IV.6.9 Relation between exceedances and implied volatility

Taking the conditional expectation of this yields

since

But if the model is well specified, then P(It = 1|xt−1) = α. Hence, the backtest is based on the null hypothesis

This can be tested by estimating the parameters using OLS, and then using one of the hypothesis tests described in Section I.4.4.8.

We now illustrate this approach to backtesting using a standard F test of the composite hypothesis (IV.6.24), based on the statistic (I.4.48), repeated here for convenience:

where p is the number of restrictions and ν is the sample size less the number of variables in the regression including the constant. The regression model is estimated twice, first with no restrictions, giving the unrestricted residual sum of squares RSSU, and then after imposing the restrictions in the null hypothesis, to obtain the restricted residual sum of squares RSSR.

EXAMPLE IV.6.7: REGRESSION-BASED BACKTEST

For our S&P 500 normal linear model for 1% daily VaR, implement a backtest using the statistic (IV.6.25) and based on a model of the form