78 ◾ Odyssey—The Business of Consulting

I had delayed going to my dentist because I do not much like the den-

tist’s chair. On one occasion, my dentist asked me why I had taken so long

to make the appointment. I told him that I did not like pain.

He responded with a profoundly wise statement, “You only prolong the pain

by delaying the decision to come to the dentist.” Point taken and lesson learned.

Eight Ways to Increase Your Consulting Revenues

Your survival in the consulting business depends on the generation of rev-

enue, consistent cash flow, and profit. It is surprising how the word “profit”

is frequently absent from the vocabulary of many consultants. The reality

of course is that it is priority number one. The second related priority cen-

ters on how you allocate the money that comes into your business within

that business, that is, admin, marketing, travel expenses, and so forth. That

allocation determines your profit levels. It is critically important to have a

good grasp of your financial well-being on a monthly basis. To grow your

2. Develop

longer-term

retainer-type

contracts.

3. Create

passive or

parallel product

income

streams.

4. Broaden

your strategic

positioning.

1. Expand

your client

base.

1.

E

y

o

u

b

8. Develop

strategic

partnering

relationships.

B

7. Reduce the

cost of client

acquisition.

e business

of consulting

6. Improve

assignment

profit margins.

4.

B

y

our

pos

i

4.

B

.

5. Justify

higher fees by

creating higher

perceived

value.

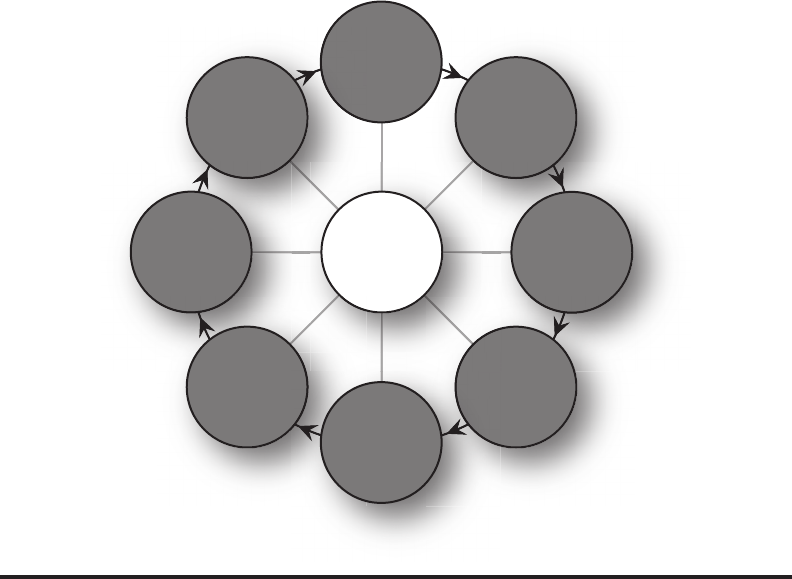

Figure 4.2 Eight ways to increase your consulting revenues.

Applying a Client-Centered Value Strategy ◾ 79

consulting practice, you must develop strategies that will address both rev-

enue and profit growth (Figure 4.2). Here are eight ways to increase your

consulting business and market share:

1. Expand your client base.

2. Develop longer-term retainer-type contracts.

3. Create passive or parallel product income streams.

4. Broaden your strategic positioning.

5. Justify higher fees by creating higher perceived value.

6. Improve assignment profit margins.

7. Reduce the cost of client acquisition.

8. Develop strategic partnering relationships.

Expand Your Client Base and Attract New Clients

The first and most obvious way to increase consulting revenues is simply to

charge out more fees to similar kinds of clients as those you have at present.

It is vital, however, that the clients you identify are Ideal Clients, as dis-

cussed in Chapter 2.

Develop Longer-Term Retainer-Type Contracts

A great way to increase fees is to offer value propositions for extended peri-

ods of time. Explore the possibility of rescoping arrangements with existing

clients to a monthly, quarterly, or yearly basis. Think about what value you

can offer your clients for these extended contracts; are there recurring events

that provide opportunities here? Is the client experiencing particular prob-

lems that only longer-term solutions can solve?

Capitalize on Your Original Cost of Acquisition

byCreatingPassive or Parallel Product Income Streams

Making product sales to your clients can have a double benefit, quite apart

from generating passive, additional income. Embedding tools in the client

organization keeps you in contact with them, something that frequently rep-

resents a challenge for consultants. Moreover, clients can easily forget good

work done for a client. Products such as assessments, books, and e-training

modules serve as a reminder of your value and provide a valuable “keep in

80 ◾ Odyssey—The Business of Consulting

touch” mechanism once an assignment is wound up. Second, these products

can act as high-impact marketing tools before a prospect becomes a client,

for example, a free one-to-one assessment with a follow-up interpretation

session.

Broaden Your Strategic Positioning: Sell Larger Assignments

Obtaining larger assignments—double, triple, quadruple, or even ten times

your current contract size—automatically increases your revenues. Breaking

out of Level 1 and Level 2 product-based assignments to Trusted Advisor

level interventions is the essence of that expansion. Rather than simply

selling time or a product, consider the scope for leveraging your existing

relationship. Think about what you can change in your consulting busi-

ness to obtain significantly larger contracts. The Odyssey Transformational

MasterClass has seen several participants expand their strategic mind-set and

service offerings.

Justify Higher Fees by Creating Higher Perceived Value

To justify higher fees to your client, you must increase the perceived value

of your portfolio of solutions. Value is truly in the eye of the beholder. Your

sales and marketing strategies together with your personal and professional

branding are critical to positively differentiating your offering in the minds of

your clients. Think about your image, your website, and your logo. Do these

suggest to the client that you are a high-value proposition? Ask yourself what

you have to change about who you are and what you do to significantly

increase your charge-out fees.

Improve Assignment Profit Margins:

FocusonIdeal Clients and Solutions

Many consultants tend to overlook the fact that profit is a normal part of

the discourse of business and fail to include a profit margin in their fees.

Maximizing profit margins and careful cash flow management are as impor-

tant as increasing revenues if you are to achieve the ultimate goal of grow-

ing your consulting practice. Case by case, consider how to engineer a better

profit margin from key assignments. The pricing of consultant expertise,

know-how, and face time with the client organization is often overlooked.

Do not neglect admin and fixed costs in calculating fees.

Applying a Client-Centered Value Strategy ◾ 81

Reduce the Cost of Client Acquisition

How you invest your time, money, and energy in acquiring business from

new or existing clients has a critical impact on the financial health and

future prospects of your consulting business. Reducing the cost of client

acquisition is frequently a function of positioning. Are you doing Executive

Briefings (EBs) on a regular basis? Are you seeking ways to position yourself

as a thought leader when you make presentations? Are you presenting to the

right people? Critically assess your positioning process to see how you can

better leverage your existing network. Avoid valueless association meetings.

Evaluate on a cost/benefit basis whether social events simply assuage the

ego and take your time but deliver little or no business opportunity.

Develop Strategic Partnering Relationships

Your expertise, processes, products, or methodology may be very useful to

other consultants and professionals outside your field. For example, lawyers,

accountants, venture capitalists, financial planners, and even banks encoun-

ter problems that require consulting analysis and expertise. These profes-

sionals do not provide these services but you do. Being on the on-call list is

an opportunity to expand your consulting practice. EBs are an excellent way

of getting the word out to potential partners about your services and creat-

ing a referral chain.

The Professional Service Firm

The term “professional service firm” used to refer solely to the regulated pro-

fessions: accountancy, law, medicine, architecture, and so on. Over time, the

definition broadened to include advertising agencies, investment banks, and

consulting firms. Today, there are three aspects of the professional service

firm that place the consulting business squarely within that definition.

Resource Base

Invariably, the consulting firm’s resource base is narrow. It exists

solely in the person of the consultant. The value of the consulting firm

derives exclusively from the technical knowledge, expertise, and experi-

ence possessed by its professional staff. They are knowledge workers;

their professional status derives from what they know.

82 ◾ Odyssey—The Business of Consulting

Organizational Form

Similarly, the organizational form is often small, taking the form of a

sole trader or a partnership with several contracted associates. The cor-

porate model gives a much higher degree of autonomy than that which

typically exists in conventional firms, and may be optimized to deliver

strategic and tax advantage.

Professional Identity

This is a vital component of any consulting firm and captures the

firm’s brand, its presence, how it communicates, its tone, and the very

essence of what it does. Your professional identity reflects the reality

that when the client retains your services, they are essentially buying

you. They understand, through that identity, that you have the expertise

and the presence to provide the services that they need.

Distinctiveness of Professional Service Firms

The consulting business is not like other businesses. Consultants do not sell

standardized products or services. To achieve results for their clients, they must

develop customized solutions, which are then delivered by highly talented pro-

fessionals. The consulting firm differs in its focus, not on volume or transaction

but on delivering the optimal portfolio of solutions to its client base.

Although conventional businesses and consulting businesses may differ

as discussed, there is one way in which they are identical. They both exist

to generate profit. In the context of a highly personalized business, it is easy

to lose sight of this fact. Consultants frequently place too much emphasis

on revenue generation, without focusing on the vital role of profit in their

business. If you are unable to quantify your profit in consulting, it begs the

question, Do you actually have a business?

The reality of course is that consulting has become a highly profitable

business, and as a result, it is growing rapidly. During the last ten years,

consulting has grown by 16% per annum to become a $120 billion indus-

try. There are currently in excess of 1 million consultants plying their trade

across the globe.

It is estimated that the big players in the industry divide half of that $120

billion among them, with the remaining $60 billion spread among smaller

firms and independent consultants. Although the charge-out fees of those

one million consultants averages out at $120,000 per annum, the reality of

course is that fee levels vary widely within the industry. Typically, however,

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.