CHAPTER 3

Social Responsibilities of Managers

CHAPTER OBJECTIVES

After reading this chapter, you should be able to:

- Understand the term corporate social responsibility (CSR)

- Enumerate the history and models of CSR

- Elucidate the process of CSR

- List the managers’ responsibilities towards society

- Understand the challenges in CSR implementation

- Enumerate the essence of green management

- List the types of managerial ethics

- Explain the role and relevance of social audit

- Provide an overview of corporate governance

- Understand the need for a harassment-free workplace

India’s Inspirational Managers

Satya Nadella is the Chief Executive Officer (CEO) of Microsoft Corporation- an American multinational technology company. In 2017, Microsoft employed 124 thousand people worldwide and generated $90.0 billion in revenue and $22.3 billion in operating income. The company’s India born chief Nadella is a proponent of social and environmental responsibility. Under his humane leadership, Microsoft has been found to have the second best reputation for Corporate Social Responsibility (CSR) on 2017 global list released by Reputation Institute (RI), a Boston-based consultancy, which analyzed 170,000 company ratings across 15 countries. Microsoft was appreciated for its commitment to enhancing education globally and operating “an open-source platform that fosters perceptions of good citizenship and good governance. According to Nadella, corporate responsibility is both a responsibility and an opportunity to work together to advance societal needs and technology at the same time. At personal level, Nadella has keen interest in ensuring that Microsoft takes responsibility for making both its workplace and products accessible to the disabled. He also meets with the company’s community group for disabled employees on a quarterly basis and speaks at its annual Ability Summit. Keeping the CSR initiatives of Microsoft under Nadella in the background, we shall now discuss the various dimensions of CSR in this chapter.

Introduction

Even in the ancient times, organizations have contributed for social prosperity. For instance, Aristotle has mentioned the need for business to reflect the interest of the society in which their operations are based.1 Every manager must give back something to the society from which they benefited. It gives them knowledge, values, survivability skills, esteem and status. Without a supportive society, managers cannot operate, survive and thrive. Hence, as a member and beneficiary of the society, each manager has an obligation to take effective steps for protecting the society’s welfare.

In the past, the sole aim of organizations was profit-making. Managers did not care for anybody other than their direct and immediate stakeholders. Traditionally, these stakeholders are business owners, management and employees. Organizations for long ignored the interest of other important members of the society like customers and general public. However, growing awareness among the managers about the benefits of the positive relationship between the fulfilment of social needs and long-term economic benefits of a firm changed their attitude.2

Organizations have realized that the labour, capital, technology and physical resources are all supplied by the society alone. Consequently, managers have begun to fulfil their social obligations in their own way. However, these managers may do so out of legal compulsion, popular social pressures, or genuine concern for the well-being of the society. We shall now discuss each of these three reasons.

- Legal compulsion (social obligation)—Legal frameworks compel companies to perform their social responsibility. The Government of India has enacted several legislations to persuade unwilling organizations to discharge their social responsibilities. For instance, the Ministry of Environment and Forest of the Government of India had issued a Charter on Corporate Responsibility for Environmental Protection (CREP) in 2003 for 17 categories of industries. This charter deals with conservation of water, energy, recovery of chemicals, reduction in pollution, elimination of toxic pollutants, process and management of residues by the respective industry. Legal compulsion may become necessary when social responsibility gets little attention in corporate policies, practices and strategies.

- Popular social pressures (social responsiveness)—Corporate responsiveness to social pressures is also a form of corporate social responsibility. While managing relationship with the society, an organization may adopt any one of the three management approaches—tactic, strategic or no action.3 The specific course of action is usually decided on the basis of the organization’s perception of the social pressures. A demand for community development from the public or an environmental issue like pollution, health hazards is an example of social pressure. When the management adopts tactical or strategic approach that aims at fulfilling social needs or relieving social pressure, it is usually called social responsiveness. The management may also decide not to act on such social pressures.

- Genuine concern for the well-being of the society (social responsibility)—While discharging social responsibility, organizations may also be guided by their own desire to behave ethically and contribute genuinely to the economic development of the workers and their families, local communities as well as the society. Managers carry out community welfare activities without any demand or pressure from any section of the society. Organizations of this type normally have strong core values that guide their approach towards society, environment, etc. For instance, TNT express, an Amsterdam-based logistics company, is known for its socially responsible behaviour. It runs a programme called “moving the world,” which involves keeping a group of 50 employees in standby mode at its head office in Amsterdam. The task of this group is to reach out to the people affected by disasters anywhere in the world within 48 hours of the occurrence of the disaster.

Corporate Social Responsibility

Corporate social responsibility (CSR) expects a business to be a good corporate citizen by fulfilling its social responsibilities voluntarily. In fact, CSR is an organization’s moral responsibility to engage in activities that protect and promote the welfare of the society. It is also an organization’s obligation towards people who are affected by its actions and decisions. CSR expects organizations to go beyond their legal requirements in serving the society with their resources. Based on their attitude and actions concerning social responsibilities, organizations can be classified into four categories. They are: (a) legal and responsible, (b) legal and irresponsible, (c) illegal and responsible and (d) illegal and irresponsible. We shall now look at some examples for each of these four categories.

- Legal and responsible—In the 1970s, the Tata group amended its articles of association to make the group always mindful of its social and ethical responsibilities to the customers, employees, shareholders, society and the local communities.

- Legal and irresponsible—Advertisements of liquor companies that encourage liquor consumption.

- Illegal and responsible—Greenpeace activists dressed as tigers blocked the gates of Shastri Bhawan, which houses the Ministry of Coal, demanding that forests in Central India be saved from coal mining.

- Illegal and irresponsible—Some dyeing units in Tirupur district of Tamil Nadu discharged their effluents directly into the earth by sinking pipes deep down the earth, thus causing large-scale ground water pollution.

CSR is, in fact, a form of corporate self-regulation that ensures that organizations comply with the spirit of the legal and ethical standards, and international norms. Through CSR, organizations take the responsibility for their action and also make sure that such actions create a positive impact on the consumers, employees, communities, environment and other stakeholders.

Definitions of Corporate Social Responsibility

The definitions of CSR, in essence, discuss the responsiveness of businesses to the expectations of stakeholders and their attempts to develop a positive impact on the stakeholders through their actions. We shall now see the definitions of social responsibility and CSR.

“Social responsibility can be defined as a business intention beyond its legal and economic obligations to do the right things and act in ways that are good for society.” —R. A. Bucchoiz.4

“Social responsibility of the business encompasses the economic, legal, ethical and discretionary expectations that the society has of organization at a given point of time.” —Archie B. Carroll.5

“Corporate social responsibility is the organization’s obligation to maximize its positive impact and minimize its negative effects in being a contributing member to society, with concern for society’s long-term needs and wants.” —G. P. Lantos.6

“Corporate social responsibility is about the way businesses take account of their economic, social and environmental impacts in the way they operate—maximizing the benefits and minimizing the downsides.” —Nigel Griffiths.7

We may define CSR as an obligation of an organization to the society to improve the quality of life of the community in general and the stakeholders of the business in particular.

Features of Corporate Social Responsibility

The basic features of corporate social responsibility are as follows:

- CSR is an obligation of an organization to the society and its stakeholders.

- It involves the adoption of corporate behaviour to meet the social needs and thus render social justice.

- It aims at improving the quality of life of its stakeholders such as workers and their family members as well as the local community.

- Organizations can fulfil CSR for both business causes (like building business profits and reputation) and normative causes (like meeting social expectations and norms).

- CSR activities of an organization include donations, sponsorships, partnership with non-profit organizations, cause-related marketing (i.e. promoting a company’s product as well as raising money for a common cause), investment in social responsibility-related activities, etc.8

Brief History of CSR

The history of CSR can be traced back to the Industrial Revolution era. When Industrial Revolution arrived, it brought with it factories. These factories are actually centralized workplaces where unrelated people come together and work as a group. This has brought about tremendous changes in the social structures, communities and standard of living of the people. From this beginning, CSR has travelled through different phases of history. We shall now go on a brief journey through different centuries to see the progress made by CSR over a period of time.

CSR in the 18th Century

During the 18th century, the great economist and philosopher, Adam Smith, suggested that the needs and desires of the society could be met effectively through free interaction between individuals and organizations in the marketplace. He further suggested that the individuals acting in a self-interested manner would produce and deliver goods and services that not only earn them a profit, but also meet the needs of others. He also insisted that all marketplace participants should be just and honest in their interactions with others. This period also saw some employers executing social welfare measures out of their own interest and humanitarian concerns. For instance, companies like Cadbury and Rowntree constructed model villages for the benefit of employees and their family members. They also engaged industrial welfare workers to take care of employee welfare.

CSR in the 19th Century

CSR is described as a baby of the 19th century by some subject experts.9 This century witnessed the advent of new technologies. It has resulted in the creation of a large number of jobs and improved living standards. With little or no government interventions, business houses grown big in many countries such as the USA and the UK. As a result, many industrialists became very wealthy and they began to think in terms of giving back something to the society from which they benefited. As a result, modern corporations commenced their CSR activities with a twin-fold objective of: (i) expressing their gratitude and (ii) investing for future business benefits and goodwill. Around this period, employers such as Lever brothers, Great Western Railways, UK, and many other progressive employers viewed their business as big families and provided their employees with community facilities, good houses and libraries.10

CSR in the 20th Century

The 20th century has made important contributions to the growth of CSR. During this period, the social responsibilities of business houses began to be formalized and institutionalized. For instance, the Harvard Business School offered its first course on ethics in 1915. Governments of various nations also established regulatory agencies for shaping CSR benchmarks and monitoring its implementation. Social issues like labour rights, occupational health and safety, and women’s rights dominated the CSR practices of this century. Besides, consumer protection and education, child welfare, environmental protection and corporate transparency also emerged as important themes of CSR in the latter half of this century. Towards the end of this century, some researchers concluded that they found no positive relationship between CSR activities and profit.11

CSR in the 21st Century

The social responsiveness of organizations became their social responsibility during the 21st century. In this century, CSR has emerged as a distinctive movement and a global issue.12 The globalization of economy has made CSR a mainstream activity. Business organizations have also replaced ad hoc initiatives with concrete corporate plans for implementing CSRs. Certainly, the strategic integration of CSR and business objectives is the unique feature of this century.13 This is because entrepreneurs have realized that “what is good for workers—their community, health, and environment—is also good for the business.” In India, corporations focus on social issues like ecological concerns, poverty, population growth, pollution, corruption, and illiteracy as a part of their CSR agenda. Box 3.1 discusses the CSR programmes of IOC.

However, CSR-related mandatory regulations and laws are opposed by some organizations on the ground that they impose unnecessary cost and also kill competition and innovation.14 Similarly, lack of understanding, inadequately trained personnel, non-availability of authentic data and specific information on the kinds of CSR activities required are the common problems that affect the effectiveness of CSR programmes in India.

Models of CSR

Based on the attitude of business organizations towards profit maximization and social responsibilities, researchers have developed three major models of CSR. They are: (i) socio-economic model, (ii) stakeholders’ model and (iii) triple bottom-line model.15 Let us discuss them briefly.

- Socio-economic model—This model maintains that the only responsibility of any business is to supply goods and services to the society at a profit. The proponents of this model consider profit as the only criteria for measuring the efficiency of a business. They also view the social involvement of business as an expense and overemphasize the cost of social involvement.

- Stakeholders’ model—This model views business as a part of the larger society. Besides achieving economic results, such as profit, managers must also fulfil the needs of the stakeholders of the business. The stakeholders are of two types: market stakeholders and non-market stakeholders.

Market stakeholders maintain direct economic transactions with the business. They include employees, shareholders, suppliers, customers and lending agencies. In contrast, non-market stakeholders do not engage in any direct economic exchange with the business organization. However, they are often affected by or affect the actions of the organization. They include general public, NGOs, media, activists, environmentalists and governments.

According to the stakeholders’ model, managers must always remember that the success of the company can be affected positively or negatively by its stakeholders. Since the stakeholders can be precisely identified by the organizations, their needs and requirements can be effectively considered while making decisions.

- Triple bottom-line model—According to this model, the success of a business should be measured only in terms of its financial, environmental and social performances (triple bottom lines). Long-term, sustainable profit can be achieved only when a business firm follows shared objectives instead of single objective, namely, profit. This model suggests that a positive triple bottom-line performance can help organizations in many ways. For instance, it can improve the profitability, shareholders’ value, human capital, environmental capital and social capital of the company.16 Box 3.2 shows the triple bottom-line approach of Tata Power.

Box 3.1

CSR Initiatives by Public-sector Giant IOC

The CSR initiatives of the Indian Oil Corporation (IOC) present an interesting example. IOC has been carrying out CSR activities right from its inception in 1964. The inclusion of CSR goals in its mission statement clearly indicates the importance accorded to such activities by this company. Every year, IOC has been awarding petrol/diesel station dealerships and LPG distributorships to beneficiaries from among Scheduled Castes, Scheduled Tribes, physically handicapped, ex-servicemen, war widows, etc. on priority basis. The CSR activities of IOC also include: (i) medical/health camps on family planning, immunization, pulse polio, eye testing and blood donation, pre and post-natal care, homeopathic medicine, programmes on AIDS awareness, etc.; (ii) 50-bed Swarna Jayanti Samudaik Hospital, Raunchi Bangar, Mathura, Uttar Pradesh; (iii) 200-bed hospital set up by Assam Oil Division, IOCL, at Digboi, Assam; (iv) Assam Oil School of Nursing, AOD, Digboi; (v) Indian Oil Rural Mobile Health Care Scheme; (vi) Indian Oil Educational Scholarship Schemes and (vii) Indian Oil Sports Scholarship Scheme. Further, the Indian Oil Foundation (IOF), a non-profit trust, was created in 2000 to protect, preserve and promote the national heritage, in collaboration with ASI and NCF of the Government of India.35

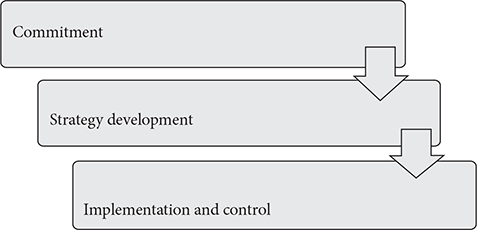

CSR Process

Organizations generally adopt a series of steps for integrating their societal and environmental concerns with their operational plans and objectives. As illustrated in Figure 3.1, CSR initiatives are usually carried out through a three-stage process. They are: (i) commitment, (ii) strategy development and (iii) implementation and control. We shall now discuss them briefly.

- Commitment—While deciding the CSR goal and strategy, it is essential for managers to ascertain the firm’s philosophy and attitude towards the society. In this regard, they can check the vision and mission statements that usually state an organization’s social and ethical concerns. The overall corporate objectives can also help managers in understanding the firm’s attitude and commitment towards the society. Further, companies can also examine their external environment to identify the challenges and threats (e.g. possible damage to the firm’s reputation or government intervention) and opportunities

(e.g. increased resource availability or employee motivation).17 For instance, the absence of civic amenities, poor infrastructure facilities, high illiteracy, corruption, malnutrition, gender inequality, pollution and poverty are a few examples of societal problems. These problems may or may not be the outcome of organizational activities. For instance, emissions by a company’s factory may pollute the air and water resources of its neighbouring locality. In contrast, societal issues like gender inequality and illiteracy may exist independent of the company’s actions.

Once societal problems are identified, companies should choose the specific issues to be addressed. For instance, a company may decide to reduce the problem of high female illiteracy by funding women-specific educational activities. Sometimes, companies may feel it necessary to incorporate their social responsibilities in corporate objectives, vision and mission statements as a way of acknowledging them.

- Strategy development—In this phase, CSR commitment of the company takes a concrete shape. The firm now develops strategies for fulfilling its commitment. While doing so, it normally takes into consideration the stakeholder priorities, nature and intensity of the issue, methods of support required and existing practices/policies. At this stage, companies usually develop medium- and long-term plans and programmes with specific targets. They also mobilize necessary resources and prepare the exact procedure to be followed for implementation.

- Implementation and control—This is the crucial stage in the CSR process. At this stage, CSR plans are communicated to the stakeholders. Effective involvement of stakeholders are achieved through continuous dialogue. The successful CSR practice benefits both the society and the company. For instance, the society may become a better place to live in with CSR intervention. The company may also gain in terms of increased goodwill, public image and better acceptability of the company by the public.

CSR involves resource allocation and spending, it is therefore necessary for companies to monitor all the phases of the CSR process carefully and thoroughly. In this regard, companies can gather necessary feedback from the stakeholders and act on them promptly.

Box 3.2

Triple Bottom-line Approach of Tata Power

The CSR initiatives of Tata Power present an interesting scenario. Tata Power has adopted guidelines formulated by the Global Reporting Initiative (GRI) for its sustainability reporting. The GRI guidelines encompass the triple bottom-line (TBL) approach, which focuses on financial, social and environmental performance. Using these guidelines, Tata Power can report its performance on 79 parameters in these three core areas. Tata Power prepared its first Corporate Sustainability Report in 2003, according to the GRI 2002 guidelines for the period 1 April 2002 to 31 March 2003. The second report titled, “Responsible Growth & Beyond,” for 2008−09 was published in December 2009 according to the new GRI G3 guidelines. The company has declared its intent to report its sustainability performance every two years.36

Figure 3.1

The Process of CSR

Managers’ Responsibility Towards Society

CSR is a voluntary business contribution to the development of the society. It thus requires managers to assume multiple social responsibilities. As seen in Figure 3.2, these responsibilities can be classified into: (i) responsibility towards owners, (ii) responsibility towards employees, (iii) responsibility towards consumers, (iv) responsibility towards governments, (v) responsibility towards the general public and (vi) responsibility towards nature.

These social responsibilities can create an impact within as well as outside the company. We shall now discuss the various responsibilities of managers towards different segments of the society.

- Responsibility towards owners—The responsibility of managers towards their owners is an economic responsibility. Managers are expected to ensure that the owners and shareholders get adequate returns (profit) from the business. Further, the quantum of profit earned in the business should be in proportion to the risk levels of the business. Managers must also ensure that the assets of the business are fully utilized and protected.

Managers must present a true picture of the company’s position to the owners. They should also treat equally the different categories of owners like equity shareholders, preference share holders and debentures. Managers should always keep in mind the stability of the business enterprise while making decisions. They must also make sure that the organization continuously grows and the owners gain from such growth. In brief, owners must have: (a) capital protection, (b) profit maximization, (c) business stability and growth, (d) access to accurate information and (e) equality in treatment.

- Responsibility towards employees—Managers’ responsibility towards employees has economic, legal and ethical dimensions. Managers must provide adequate monetary and non-monetary rewards for the work done by the employees. They should also ensure that the employee selection and promotion processes are just and fair. Employees must be given sufficient opportunities for learning through educational and training programmes at the company’s expense. Employees must also have individual dignity, job security, job autonomy, psychological support and opportunities for participation in management.

Managers must ensure clean, pleasant and healthy work conditions for employees. They should evaluate employee performances systematically and objectively. In a nutshell, employees should have: (i) job security, (ii) adequate remuneration, (iii) productive training, (iv) objective performance evaluation and (v) safe and healthy working conditions.

- Responsibility towards consumers—The support of the customers is critical to the survival and growth of any business. Managers, hence, have some Important responsibilities towards consumers. They must make available adequate quantity of desired quality goods and services at reasonable rates. They must also provide prompt and dependable service to their customers. They must provide effective after-sales services. They should also attend to the customer complaints promptly and sincerely.

Managers should desist from unfair trade practices such as hoarding, adulteration, black marketing, etc. In short, consumers must have: (i) products in desired quality and quantity, (ii) products at fair and just prices, (iii) efficient after sales services and (iv) prompt response for their complaints.

- Responsibility towards governments—The primary responsibility of managers is to ensure that the operations of the business are carried out well within the legal framework, as specified by the government. Managers must also respect the specific rules, guidelines, regulations and norms laid down by the government from time to time. Further, they should pay all the taxes, dues and duties payable to the government fairly and regularly. They should also furnish statutory information about the company (like copy of the balance sheet, etc.) in a true and fair manner to the registrar of companies. In brief, their responsibilities are: (i) observing rules and regulations, (ii) paying taxes and duties and (iii) furnishing true information.

- Responsibility towards the general public—The quality of relationship that an organization has with the general public is crucial to its success. Managers should work systematically to gain public confidence, goodwill and also a positive business image. They must learn to respect the sentiments, beliefs, values and ethos of the people in the community. They should care for the health and safety of the public in general and the neighbours in particular. For instance, Tata Steel educates people about leprosy through advertisements in newspapers and magazines as a part of its health awareness programme.

- Responsibility towards nature—Of late, environment protection is emerging as an important management practice. There is growing awareness among managers about their role and responsibilities in protecting nature due to problems of climate change like global warming, ozone depletion and acid rain. In this regard, organizations must be socially more responsible in their release of pollutants that can affect air, water, etc.18 Managers should also avoid the activities that can harm the flora and fauna, and animal and human life. Further, they should avoid activities that cause destruction of heritage structures such as historical buildings, monuments, etc.

Figure 3.2

Managers’ Responsibility Towards Society

Challenges in the Implementation of CSR

Usually, CSR has a different meaning for different managers depending on their organizations’ philosophy, attitude and environment. But many managerial experts now begun to accept CSR as a tool to achieve the objectives of profit, environmental protection and social equality. The following factors have enhanced the importance of CSR: (i) limited state resources, (ii) increased stakeholders’ interest on organizations’ social and ethical responsibilities, (iii) legal requirements for corporate disclosure and (iv) changing expectations of the public about corporations. Despite these developments, it is a sad fact that CSR is yet to gain widespread recognition and popularity in India. According to the results of a survey conducted by The Times of India group, the slow pace of growth in CSR activities by companies can be attributed to the following challenges:19

- Absence of active community involvement in CSR activities—The following factors have resulted in the poor support for CSR and public participation: (a) poor communication between the sponsoring company and members of communities, (b) little or no public awareness about the role and relevance of CSR in community development and (c) people’s indifference towards CSR projects.

- Absence of local capacities and well-organized NGOs—It is difficult for companies to directly involve themselves in community development projects. Companies therefore seek the cooperation and involvement of local NGOs with adequate manpower. However, most NGOs operating from rural and remote areas lack necessary trained workforce and infrastructure to effectively contribute to the CSR activities initiated by them. This lack of capacity building by local NGOs prevents companies from undertaking large CSR projects in rural, tribal and other remote regions.

- Lack of transparency—Most NGOs are reluctant to disclose information about their existing programmes and capacities, to companies willing to join with them for implementing CSR projects. This lack of transparency on the part of NGOs normally creates trust deficit and affects their ability to work closely with the companies.

- Perceptual differences—Companies and communities often differ in their perception of the CSR initiatives. NGOs often think CSR projects as donor-driven projects and expect companies to take overall responsibility in the long run. In contrast, the companies view CSR initiatives as a local-driven approach with their role restricted to that of major donor. These perceptual differences often affect the long-term viability of the CSR projects.

- Lack of clear-cut guidelines and policies—The absence of clear-cut governmental guidelines relating to CSR activities to be undertaken by companies has reduced CSR’s importance among companies. As of now, the scale of CSR initiatives of companies depends on their business size, profile and philosophy.

- Absence of unified approach in CSR implementation—When more than one company undertakes CSR activities in the same area, duplication of activities often occurs in those areas. This mostly happens because of lack of coordination among local collaborators of companies responsible for CSR activities. Further, unwarranted and unhealthy competitions often result in the wastage of resources.

- Desire to gain quick popularity—NGOs and other local agencies involved in CSR initiatives, at times, engage in event-based programmes just to gain media attention and quick popularity. Such NGOs often ignore the long-term interest of the communities.

Through better strategies, companies can overcome the challenges in the implementation of CSR initiatives. Companies should realize that the successful discharge of their social responsibilities will enable them to reap the benefits of: (i) improved public acceptance, brand image and reputation, (ii) enhanced sales and customer loyalty, (iii) increased ability to attract and retain efficient workforce and (iv) better recognition and patronage from capital holders.

Green Management

Managerial practices that help in the preservation of natural environment is called green management. The term, green, here implies the protection of people’s health through the use of natural products and nature friendly technology. Haden and others define green management as, “an organization-wide process of applying innovation to achieve sustainability, waste reduction, social responsibility and a competitive advantage via continuous learning and development.”20

Generally, green management initiatives require managers to ensure that they: (i) reduce the negative environmental impacts, (ii) comply with the environmental regulations, (iii) adopt appropriate environmental management system and (iv) publish corporate social responsibility reports regularly and sincerely. The extent of green management initiatives of the management can be measured through one or more of the following criteria:21

- Product criterion—The organization’s initiatives and record in the production of environmentally friendly products. Non-polluting and recyclable products (glass, paper, etc.) are examples of these products.

- Technology criterion—This refers to the extent of employment of clean technology in the manufacturing process of the organization. It may involve the adoption of production or assembly processes that cause little or no harm to the environment. Technologies that cause minimum wastage or pollution such as wind power and solar power technology are examples of clean technologies.

- Business ethics criterion—This refers to the adoption of philosophies, policies, practices and procedures by an organization that foster environmental ethics, values and goodness. Box 3.3 shows the green management initiatives of ITC.

As a part of a green management initiative, managers must undertake specific environmental programmes to educate their employees, customers and other stakeholders on the need for and importance of protecting nature. They must also continuously carry out innovations in: (i) products (like developing new products or creating new uses of existing products), (ii) processes (that operate with less output) and (iii) practices (like total quality management).

Managerial Ethics

Ethics, in simple terms, refers to the moral codes that govern the behaviour of the people and also tell them what is right or wrong. Managerial ethics, in turn, are the set of standards that dictate the conduct of the managers when performing their job. They also regulate the internal and external behaviour of the managers. Specifically, ethical codes guide the behaviour of the managers in a decision-making scenario. They help managers evaluate the ethical quotient of their decisions and decide whether their decisions are ethically right or wrong. Managerial ethics are typically different from legal rules as ethical codes are formed by an organization just to guide its own members. Hence, ethical codes need not be the same for all organizations or cultures.

Box 3.3

Green Management Initiatives of ITC

To go green, a company’s senior management and employees must have belief in the philosophy of green management. ITC’s green initiative is a case in point.

The 170,000 sq. ft, ITC Green Centre is the world’s largest zero-per cent water discharge, non-commercial green building. Compared to similar buildings, ITC Green Centre has 30 per cent smaller carbon footprint. ITC has a unique forestry programme to help small and marginal tribal farmers to transform their wastelands into dense plantations. The programme has rejuvenated more than 29,230 hectares of wasteland, generating livelihoods for over 20,000 people and making a substantial contribution to India’s green cover. Using ITC’s Internet stations in villages, it has also launched a programme called the e-Choupal programme to enable the farmers to log on to the ITC-created vernacular Web sites that provide weather forecasts, expert advice on the best farming practices and local, national and international agricultural commodity prices online. The initiative reaches out to over 3 million farmers living across several states.37

Organizational policies, principles, culture and value system usually shape managerial ethics. Ethical codes enable managers to know in advance whether their actions are in conformity with the accepted behaviour or choices. They also outline the duties and responsibilities of managers towards the company’s stakeholders like employees, shareholders, creditors, vendors, distributors, customers, etc. Managerial ethics are typically classified into principle-based ethical codes and policy-based ethical codes.22 Principle-based ethical codes define the basic values of the organization and also include general details of the company’s responsibilities, quality of products and treatment of employees. Policy-based ethical codes describe the procedures to be used in specific ethical situations. These situations may arise when managers face conflicts of interest, ethical dilemma in the observance of laws, etc.

Definitions of Ethics

Ethics oversees the conduct and actions of people. Let us now look at a few definitions of the term.

“Ethics are the principles of conduct governing an individual or a group.” —Manuel Velasquez.23

“Ethics is a set of moral principles that govern the action of an individual or group.” —Appleby.24

“Ethics is a set of standards or a code or a value system worked out from human reason and experience by which free human actions are determined as ultimately right or wrong, good or evil.” —P. S. Bajaj and Raj Agarwal.25

Types of Ethics

Ethics can broadly be classified into three types, namely descriptive ethics, normative ethics and interpersonal ethics. A brief explanation of these terms is provided here.

Descriptive ethics—It is mostly concerned with the justice and fairness of the process. It involves an inquiry into the actual rules or standards of a particular group. It can also mean the understanding of the ethical reasoning process.26 For instance, a study on the ethical standards of business executives in India can be an example of descriptive ethics.

Normative ethics—It is primarily concerned with the fairness of the end result of any decision-making process. It is concerned largely with the possibility of justification. It shows whether something is good or bad, right or wrong. Normative ethics describes what one really ought to do and it is determined by reasoning and moral argument.27

Interpersonal ethics—It is mainly concerned with the fairness of the interpersonal relationship between the superior and the subordinates. It refers to the style of the managers in carrying out their day-to-day interactions with their subordinates. The manager may treat the employees either with honour and dignity or with contempt and disrespect.

Ethical Dilemmas in Managerial Decisions

While making decisions, managers consider four dimensions to evaluate their decisions. They are: (i) instrumental dimensions which involve cost−benefits analysis, (ii) relational dimensions which involve the analysis of the impact of the decisions on the future relationship with the stakeholders, (iii) internal dimensions that focus on the impact of decision on internal capabilities of the firm and (iv) ethical dimensions which refer to the evaluation of the ethical dimensions of the decisions, i.e. whether the decisions are good or bad, right or wrong, etc.28

Managers often face ethical dilemmas while making decisions in the course of their business operations. They feel the ethical pressure when they deal with tricky situations that may result in the violation of basic rights of the workers, overlooking the environmental concerns, etc. Managers may override the ethical dimension of their decisions when it involves higher costs, delayed outcomes, uncertain consequences, and negative personal implications. Managers may also resort to unethical behaviour when they strongly believe that: (i) good business more important than good ethics, (ii) political success and economic improvement are more valuable than ethical behaviour, (iii) opportunities can take precedence over ethical issues and (iv) there is low risk of getting caught while being engaged in unethical behaviour.29

However, when managers consistently apply ethical principles, they stand to gain from their ethically sensible decisions. The long-term benefits of making such ethical decisions include: (i) better business and brand image, (ii) improved employee motivation and morale, (iii) availability of cheaper sources of finance from ethically conscious investors and (iv) enhanced business revenues.

Need for Ethical Policies and Codes

There has been an increased importance among companies to have strong ethical policies and codes. We shall now discuss the need for ethical policies and codes in an organization.

- Code of ethics will enable an organization to create an ethical workplace. Each employee will understand clearly the standard of behaviourv and values of the organization.

- Of late, organizations have fewer levels of management and are pushing decision-making down to line managers. As a result, any decision by an immediate superior can be viewed as personal and subjective by the subordinates and this situation may call for strict adherence to a code of ethics.

- The growing presence of knowledge workers in organizations has necessitated the introduction of strong ethical policies as they are more likely to violate laws and the code of ethics as compared to the earlier generation of workers.

- Visible ethical policies and code can send a clear signal to the employees that the organization is serious about ethics and that it will make no compromise when it comes to dealing with ethical standards and violation.

- Ethical policies will enable managers to evaluate quickly their proposed actions with the company’s code of conduct to determine whether they fit the existing ethical standards.

- Generally, the public image for companies that practice ethical values will be high in the society. As a result, consumers will keep their trust in those companies that ensure fairness in their dealing with the people. Similarly, ethical companies can also attract the best candidates in the labour market with ease.

Thus, it is important for each organization to have a strong code of ethics that focuses on business practices and specific issues such as conflict of interest, accuracy of information, prevention of harassment, safety and environmental compliance. Managers should be the model of ethical behaviour so that employees follow it willingly and voluntarily.

Social Audit—Role and Relevance

Social audit is a relatively new phenomenon for the Indian companies. It is an instrument used to verify the social accountability of organizations. It assesses the performance of the organizations in terms of fulfilment of social, environmental and community goals. It measures the social relevance of organizations by systematically monitoring their chosen social objectives. Certainly, social audit aims at ensuring that firms report their performance relating to social goals regularly. The legislations connected with social audit in India are: (i) Right to Information (RTI) Act, 2005, (ii) National Rural Employment Guarantee Act (NREGA), 2005 and (iii) the 73rd amendment of the Indian Constitution relating to Panchayat Raj institutions that empowered Gram Sabhas to carry out social audits.

Social audit is a continuous process and carried out at periodic intervals. It involves reviewing an organization’s social activities to decide whether such activities truly benefit the society. Social audit normally deals with issues like environmental protection, equal opportunity, ethical issues, quality of work life and consumerism. Ethical issues include unfair trade practices, labour rights violation, human rights violation, etc. As a part of the auditing process, the social auditor normally examines the corporate policies, procedures, practices and departmental guidelines to see whether they comply with the governmental rules and regulatory requirements.

Definitions of Social Audit

A careful verification of social accounting records of an organization is the essence of the definitions of social audit. We shall now see a few definitions of social audit.

“Social auditing refers to the process of identifying, analyzing, measuring, evaluating and monitoring the impact of an organization’s operations on different stakeholders.” —Sage Publications.30

“Social audit is an enquiry into the corporate social accounting records by an outside agency that can opine with a view to attestation and authentication of reports and records.” —John Crowhurst.31

Objectives of Social Audit

Social audits carried out by organizations are expected to fulfil the following objectives:

- To improve the efficiency of community development programmes and projects of organizations.

- To create better awareness among the participants such as the beneficiaries and project managers about the importance and benefits of social programmes of the firm.

- To identify the gaps between societal needs and resource availability of organizations.

- To check the effectiveness of existing organizational policies, practices and procedures in fulfilling the social responsibility of firms.

Types of Social Audit

Social audit, can broadly be classified into six types. They are: (i) social balance sheet and income statement, (ii) social performance audit, (iii) macro−micro social indicator audit, (iv) constituency group attitudes audit, (v) government-mandated audits and (vi) social programme management audit.32 We shall now discuss them briefly.

- Social balance sheet and income statement—This is similar to the financial balance sheet and income statement. It reveals the costs and benefits of social investment to organizations. However, this type of social audit does not have universal applications because it lacks generally accepted accounting standards and guidelines.

- Social performance audit—This audit involves critical examination of the social performance of organizations. The purpose behind this audit is to make future social investments of an organization productive, relevant and timely.

- Micro−macro social indicator audit—This is basically a quantitative audit. As a part of this audit, the quantifiable social performance of a particular year is compared with that of another year to see the company’s progress during that period. This is a micro-social indicator because the assessment involves a single company alone. When the quantifiable social performance of an organization is compared with that of another organization or even with that of the whole industry, it is called macro-social indicator audit. The social indicator may involve an organization’s investments on social projects that aim at enhancing the health and safety or education of the members of the community.

- Constituency group attitudes audit—Constituency group refers to stakeholders who regularly interact with an organization. This audit primarily focuses on identifying and measuring the stakeholders’ expectations so that their social pressures on the organization are effectively handled.

- Government-mandated audits—These types of audits are normally carried out by organizations in deference to governmental regulations and judicial pronouncements.

- Social programme management audit—This audit aims at evaluating the effectiveness of specific programmes of organizations. This audit looks at examining the outcome of social programmes including the effectiveness of the process involved in the implementation of such programmes.

Even though corporate social audits are still in the infancy stage in India, their importance will increase in the future for a variety of reasons. For instance, social audits can help organizations determine the social objectives and budget allocations. They are also capable of improving the reputation and credibility of the sponsoring organizations among the general public. Lastly, they can fine-tune the policies and programmes that guide the social performance of organizations.

Corporate Governance—An Overview

Corporate governance involves a just, fair, efficient and transparent administration of the organization. It emphasizes on the transparency of the decision-making process and fairness in managing the affairs of the company. Corporate governance, gained importance after the ownership and management of companies were separated. Professionals are now engaged to manage companies on behalf of the shareholders. Through proper corporate governance, managers are expected to ensure the satisfaction of all stakeholders by properly structuring, operating and controlling the organization. Corporate governance is actually a system or procedure on how the managers are responsible to their stakeholders. It defines the relationship between a company’s management and its stakeholders, and also improves their mutual trust.

A high-level finance committee report on corporate governance in Malaysia33 makes it amply clear that corporate governance focuses on:

- accountability of management

- continuously improving corporate performance

- transparency in administration

- investor protection and value enhancement

- equitable treatment of stakeholders

- adequate information disclosure and dissemination

- statutory and legal compliance

- ethical and value-based management

- self-evaluation

As a system, corporate governance looks to create trust and confidence among the different stakeholders of the business even if they have competing and conflicting interest. For instance, shareholders and employees usually have a competing claim over the financial resource (like profit) of the business. When employees succeed in their demand for higher remuneration, the profitability and returns available to the shareholders get smaller. In contrast, shareholders get more when employees are paid less. Besides, corporate governance, as a system, focuses on minimizing the operational and financial risks and on managing the changes efficiently. It also attempts to ensure right culture and right focus for the organization.

Managing Sexual Harassment

Indian companies are now a much more diverse place than what they were earlier. Several organizations have made a conscious decision to create gender equality by recruiting more women as part of gender diversity initiatives. Now, there is a growing representation of women to the total labour force of the country. This has positive implications for women empowerment, economic growth and GDP. According to McKinsey Global Institute, India can increase its GDP by Rs 51.50 lakh crore by 2025 by getting more women to work and increasing equality. Due to the increasing presence of women population, it has become essential for organizations to ensure that women are safe in their workplace. Besides ensuring physical safety and security of women employees, managers should make them feel that they work in a harassment-free workplace. This requires managers to promptly address their concerns/complaints about sexual harassment at workplace.

Managers must understand that creating a harassment-free workplace is not a choice but an obligation for them. Managers should also understand the importance of creating a positive work environment where women’s right to equality, life and liberty is fully respected, protected and promoted. This is because the fear of harassment may force women to stay away from jobs resulting in low female workforce participation rate.

Managers must take every possible step to protect women employees from sexual harassment by undertaking adequate awareness campaigns and through punitive actions, if such incidents are reported. The harassment related complaints need to be dealt with skill, maturity and compassion by managers. On its part, the state has enacted the Sexual Harassment of Women at the Workplace (Prevention, Prohibition and Redressal) Act 2013. The primary objective of the Act is to ensure that women feel safe in their workplace and to promote a positive work environment for their greater and effective participation in the work ecosystem.

Top managers should ensure their organization’s compliance with the requirements of this Act. They should also implement the mechanisms needed as per its provisions. The introduction of the act requires the establishment of mechanisms such as the Internal Complaints Committee. This Act places a greater accountability on the employer and top managers with regard to providing a safe work place for women. It also legally requires the companies to ensure the (i) organisation of capacity and skill building programs for the internal complaints committee, (ii) implementation of awareness programmes for all employees, and (iii) listing of penalties and fines.

The Sexual Harassment of Women at the Workplace (Prevention, Prohibition and Redressal) Act 2013 requires fundamental changes in governance frameworks, compliance program and instrumental change in operational ethics and integrity.

Summary

- CSR is an obligation of the organization to the society to improve the quality of life of the community, in general, and the stakeholders of business, in particular.

- The major models of CSR are: (i) socio-economic model, (ii) stakeholders’ model and (iii) triple bottom-line model.

- The stages involved in CSR process are (i) commitment, (ii) strategy development and (iii) implementation and control.

- Managers’ responsibility towards society can be classified into: (i) responsibility towards owners, (ii) responsibility towards employees, (iii) responsibility towards consumers, (iv) responsibility towards governments, (v) responsibility towards the general public and (vi) responsibility towards nature.

- The challenges in the implementation of CSR are: absence of active community involvement in CSR activities, absence of local capacities and well-organized NGOs, lack of transparency, perceptual differences, lack of clear-cut guidelines and policies, absence of cohesive approach in CSR implementation and tendency to gain quick popularity.

- Green management is the organization-wide process of applying innovation to achieve sustainability, waste reduction, social responsibility and competitive advantage by embracing environment-friendly goals and strategies.

- Ethics is a set of moral principles that govern the action of an individual or group. Ethics can be classified into descriptive ethics, normative ethics and interpersonal ethics.

- Social audit is an enquiry into the corporate social accounting records by an outside agency that can opine with a view to attestation and authentication of reports and records.

- Social audit can broadly be classified into: (i) social balance sheet and income statement, (ii) social performance audit, (iii) macro−micro social indicator audit, (iv) constituency group attitudes audit, (v) government-mandated audits and (vi) social programme management audit.

- Corporate governance is the process and structure used to direct and manage the business and affairs of a company towards enhancing business prosperity and corporate accountability.

Review Questions

- State the meaning and definition of CSR.

- Explain briefly the models of CSR with examples.

- Point out the meaning of green management.

- Write a note on managerial ethics.

- Define the term social audit.

- What are the objectives of social audit?

- State the essence of corporate governance.

- How can organizations be classified based on their attitude towards CSR?

Essay-type questions

- Examine the circumstances under which organizations normally perform their social responsibilities.

- Trace the progress made by CSR over a period of time.

- Examine the progress models of CSR with relevant examples.

- Discuss in detail the different stages in the CSR process.

- Enumerate the responsibilities of managers towards different sections of the society.

- Critically evaluate the challenges in the implementation of CSR and also state your strategies to overcome them.

- Explain the importance of green management and the measures taken towards its implementation.

- “Ethical codes guide the behaviour of managers in a decision-making scenario.” In the light of this statement, discuss the role and relevance of managerial ethics.

- Social audit is a relatively new phenomenon in the Indian corporate world. Discuss.

- Elucidate the types of social audit with relevant examples.

- Enumerate the steps to be taken to prevent harassments in organizations.

Case Study

Moving Towards Diversity and Inclusion

Amity Brakes Limited produces automobile spare parts on a large scale and supplies them to several major automobile producers in the world. This Hyderabad based multinational has a commendable sales and profit performance. It is also a market leader in its area of operation. The company has a staff strength of 9,500 on its roll. As part of its platinum jubilee celebrations, the management recently did self introspection of its functioning by analysing the relevance of its mission, vision, policies and programmes covering all aspects of the organization.

As far as HRM was concerned, the management concluded that the workforce composition of the organization was not reflecting the reality of the diversified nature of the labour market. In fact, the HR policy of the company was not offering equal opportunity to all segments of the labour market. The number of women employee in the workforce was insignificant while the number of physically challenged person was trivial. Thus, the company took an administrative decision to change its recruitment policy in a way that would reflect the labour market conditions. Also, its management decided to implement these changes with immediate effect.

The proposal of the management received a mixed response from the employees. A section of the employees viewed the proposal favourably and supported it on the ground that it would do social justice, reflect reality of the market, make optimum utilization of the talents available in the market, and prepare the organization for an inclusive growth. However, another section of the work-force viewed the proposal with doubt and disbelief as they felt a well-performing organization like Amity should not take any unwarranted risk. They also feared the cost of training would go up substantially. Besides, they were afraid that gender related issues could crop up in the organization. Further, they foresaw an additional investment commitment by the management to improve the infrastructure facilities, especially for the physically challenged.

Finally, however the company went ahead with its revised policy and implemented it. It also directed the HR department to do what was necessary for the successful implementation of the diversity based HR policy initiatives. The HR department prepared the ground for the implementation of new ideologies and of the policies of the company. Soon after the proportion of the employees belonging to these categories began to pick up.

Questions:

- How do you view the new proposal of the light of the current performance of the company?

- Do you foresee any problem for the company in the execution stage of the proposal?

- Do you have any better suggestions and strategy for the company to adapt itself to the emerging labour market environment?

Note: The solution for the above case is available at www.pearsoned.co.in/duraipom2e

References

- R. C. Solomon, “Corporate Roles, Personal Virtues—An Aristotelian Approach to Business Ethics” in T. Donaldson and P. H. Werhane, eds., Ethical Issues in Business: A Philosophical Approach (Upper Saddle River: Prentice Hall, 1999), pp. 81−93.

- Stephen P. Robbins, Mary Coulter, and Neharika Vohra, Management, 10th ed. (New Delhi: Pearson Education, 2010), p. 9.

- Pia Lotila, “Corporate Responsiveness to Social Pressure: An Interaction Based Model,” Journal of Business Ethics (2010), 94: 395−409.

- R. A. Bucchoiz, Essentials of Public Policy for Management, 2nd ed. (Upper Saddle River, NJ: Prentice Hall, 1990).

- Archie B. Carroll, “A Three Dimensional Conceptual Model of Corporate Social Performance,” Academy of Management Review (1979), 4(4): 497−505.

- G. P. Lantos, “The Boundaries of Strategic Corporate Social Responsibility,” Journal of Consumer Marketing (2001), 18(7): 600.

- Nigel Griffiths in John Hancock, ed., Investing in CSR—A Guide to Best Practices, Business Planning, and the UK’s Leading Companies (London: Kogan Pages, 2004), p. 6.

- Francesco Perrini, Stefano Pogutz and Antonio Tencati, Developing Corporate Social Responsibility: A European Perspective (Glos, UK: Edward Elgar Publishing, 2006), p. 150.

- Güler Aras and David Crowther, Global Perspectives on Corporate Governance and CSR (Surrey, England: Gower Publishing, 2009), p. 132.

- John Hancock, Investing in CSR—A Guide to Best Practices, Business Planning, and the UK’s Leading Companies (London: Kogan Pages, 2004), pp. 1−2.

- B. R. Agle, R. K. Mitchell and J. A. Sonnenfeld, “Who Matters to CEOs? An Investigation of Stakeholder Attributes and Salience, Corporate Performance, and CEO Values,” Academy of Management Journal (1999), 42: 507−25.

- Jennifer A. Zerk (2006). Multinationals and Corporate Social Responsibility: Limitations and Opportunities in International Law (New York: Cambridge University Press, 2006), pp. 15−29.

- Bryan Horrigan, Corporate Social Responsibility in the 21st Century: Debates, Models and Practices across Government, Law and Business (Glos, UK: Edward Elgar Publishing, 2010), p. 9.

- Nina Boeger, Rachel Murray, and Charlotte Villiers, eds., Perspectives on Corporate Social Responsibility (Glos, UK: Edward Elgar Publishing, 2008), p. 21.

- Liangrong Zu, Corporate Social Responsibility, Corporate Restructuring and Firm’s Performance: Empirical Evidence from Chinese Enterprises (Berlin, Germany: Springer Verlag, 2009), pp. 21−31.

- Ibid., p. 30.

- Regine Barth and Franziska Wolff, eds., Corporate Social Responsibility in Europe: Rhetoric and Realities (Glos, UK: Edward Elgar Publishing, 2009), pp. 15−16.

- Ricky W. Griffin, Management (Mason, OH: South-Western Cengage Learning, 2011), pp. 113−114.

- Nilesh R. Berad, “Corporate Social Responsibility: Issues and Challenges in India,” International Conference on Technology and Management, available at www.trikal.org.

- S. S. Haden, J. D. Oyler, and J. H. Humphreys, “Historical, Practical, and Theoretical Perspectives on Green Management,” Management Decision (2009) 47(7): 1041−55.

- M. Karpagam and Geetha Jaikumar, Green Management: Theory & Applications (New Delhi: Ane Books, 2010), p. 138.

- Richard L. Daft and Dorothy Marcic (2008). Understanding Management (Mason, OH: South-Western Cengage Learning, 2008), p. 127.

- Manuel Velasquez, Business Ethics Concepts and Cases (Upper Saddle River, NJ: Prentice Hall, 1992), p. 9.

- R. C. Appleby, Modern Business Administration, 6th ed. (London: Pitman Publishing, 1994).

- P. S. Bajaj and Raj Agarwal, Business Ethics: An India Perspective (New Delhi: Biztantra, 2004), p. 11.

- John R. Boatright, Ethics and the Conduct of Business, 4th ed. (New Delhi: Pearson Education, 2005), p. 35.

- Ibid.

- Domènec Melé, Management Ethics: Placing Ethics at the Core of Good Management (NY: Palgrave Macmillan, 2012), p. 50.

- Bernard M. Bass, Ruth Bass, and Ruth R. Bass, The Bass Handbook of Leadership: Theory, Research, and Managerial Applications (NY: Free Press, 2008), p. 207.

- Sage Publications, Sage Brief Guide to Corporate Social Responsibility (London: Sage Publications, 2012), p. 201.

- John Crowhurst, Auditing: A Guide to Principles and Practices (London: Cassell, 1982).

- Sage Publications, Sage Brief Guide to Corporate Social Responsibility (London: Sage Publications, 2012), pp. 202−204.

- “The High Level Finance Committee Report on Corporate Governance in Malaysia.” Referred by Lee Leok Soon, “Misgovernance—Who Is to Be Blamed?” Smart Investors, 2003, p. 41.

- Sexual violence is holding back the rise of India’s economy (2018) The Times of India available at https://timesofindia.indiatimes.com.

- http://www.iocl.com (last accessed in May 2014).

- http://www.tatapower.com (last accessed in May 2014).

- http://www.itchotels.in (last accessed in May 2014).