Chapter 1

Richard Mack

Mack Real Estate Group, New York, New York, USA

Understand the potential downside of a deal

It is a rudimentary principle of portfolio management theory to incorporate alternative assets as part of a diversified portfolio. One of the most popular alternative investments for sophisticated investors is real estate. While it serves as a partial hedge against inflation, it is also a way to enjoy the potential of a steady cash flow stream.

Within the real estate space, institutional investors are probably most attracted to the private equity arena. Real estate private equity funds have been attracting large amounts of capital with assets under management reaching an all-time high as of the end of 2017 of $811 billion.1 One private equity real estate giant is Richard Mack.

In His Own Words

I was at the top of my class in high school, but not in college. I guess I wanted to have fun, experience being in a fraternity and think creatively away from my major, but I was a hard worker and later regretted my lack of academic discipline in college. By the time I entered college, my father had established himself as a very successful developer. I graduated at a time when people commonly assumed that the son of a successful businessperson was not capable. When I started working, I felt that I had a lot to prove.

I graduated from the Wharton School at the University of Pennsylvania and was very lucky to get a job with Shearson Lehman Hutton. Despite expectations, I didn’t always work for my father, and he did not find me my first job. I was fortunate to meet Bill Kahn, a managing director at Shearson Lehman Brothers, in their real estate investment banking group. He took a chance on me. Maybe he saw that I was passionate about hard work and real estate investments. Maybe he wanted a relationship with my father. Either way, he offered me a job, and real estate investment banking seemed a natural fit. I always enjoyed doing things that required self-motivation, creativity, and hard work. I also felt that growing up I had learned a lot about development at the dining room table and that I had an aptitude for real estate. That’s pretty much how I ended up getting into the business.

In real estate investment banking in the late 1980s, profit was driven by tax syndications, powered by accelerated depreciation rules for real estate or tax arbitrage. Those loopholes all closed in 1986. By the late 1980s real estate investment banking was in retrenchment. I was forced to restart my career in 1990 just after getting started. Within six months, there was a massive firing across the real estate investment banking division at Shearson. Four of five managing directors and their teams were let go. The one remaining managing director would not even interview me because I was “a rich kid.”

Fortunately, I preemptively made two moves: (1) I reached out to my old boss from when I was a summer intern in the facilities department at Shearson, and (2) I applied to law schools. I got the job and shortly after that got into law school.

Shearson was then owned by American Express and their facilities departments were combined. While my experience was brief, I will never forget the lessons that I learned there. The most interesting experience I had in the facilities department, and the one that was the most exciting, occurred during a very weak real estate leasing market. I was sent to Long Island in New York to negotiate with a landlord a renewal for American Express, one of the largest companies in the world. American Express had backup computer systems in a Long Island distribution/office building. The landlord could have tripled the rent and American Express would have stayed: the cost to move the equipment was prohibitive. Instead, I was able to negotiate a significant rent reduction based upon market rents having fallen. This experience made me realize the power of information in real estate, what it means to be a tenant, and what corporations/users see when looking at real estate.

The Big Opportunity

The early 1990s was a really bad time for real estate. As I was graduating from law school, my father invited me to join him in his foray into real estate private equity with Leon Black. They were forming Apollo Real Estate. With an initial $500 million fund, this untested real estate private equity concept would pursue “distressed” investment opportunities in the United States and Europe. I enjoyed this experience because I got to live through all the initial stages of creating a real estate investment company, the advent of the real estate private equity business, and the highs and lows (but predominantly highs) of successfully closing on many dozens of equity and debt investment opportunities.

So far in my career, I’ve been involved in the investment of more than $16 billion of equity in real estate transactions all over the globe that I would estimate to have a value of more than $80 billion. While the fund business would prove to be tremendously interesting and lucrative, I always remember the first significant money I made for myself, which was not through the equity fund business. It was something I did on my own, and taught me the value of being opportunistic and the importance of not relying on others (i.e., fund investors) to take a risk that I was not prepared to take on my own.

In my mid-twenties, I bought land with three radio towers on it, paying ground rent, in Montauk, New York. The towers on the land were owned by the tenants, but the land lease was very short. Other buyers at the time were concerned that the tenants would move the towers or that satellites would replace cell towers completely. I was not sure about the technology, but I was pretty sure that the town would not allow these towers to be moved to another location. As a result, I was able to buy the cash flow at a six multiple, a very attractive number to me. I was betting that the underlying demand for users of those towers would increase because cell phone usage would have to increase and that satellite would be too expensive. It was the beginning of the mobile communications era.

I was able to put up the money myself with another partner who wanted to invest. I had to borrow recourse debt, which meant I had to pledge personal collateral to the bank. Fortunately, after all my diligence and efforts, it turned out that our investment thesis was correct, and demand for these towers skyrocketed.

More importantly, there were no competing radio towers anywhere nearby, and the town was not going to approve new ones. Because of this, I took title to the towers and quadrupled the EBITDA by converting subtenant income into direct income from the telecommunications companies. In retrospect, the investment seems straightforward, but at acquisition this seemed a risky proposition. In fact, I could not get a nonrecourse loan. I had to leverage my whole life in order to get help from the bank. So, I put my guts on the line and I was lucky. Not only was I was able to dramatically increase the NOI, I eventually sold the towers at a 14 multiple.

The lesson to learn from the radio tower deal is that sometimes real estate is mispriced, and for a short period of time, the market players will overlook this. Sometimes, you will see a shift in the market or realize that technology’s going to make a change, and you can be one of the people who realize early that the shift will eventually lead to a shift in real estate value. The success of this project left me brimming with confidence and I have tried to leverage these lessons for the benefit of the many partners who have entrusted me with their capital over the years.

The Polish Job

One of my favorite deals took place in Poland in 2004, just before the country joined the European Union. A company called Metro had built a large portfolio of shopping centers all across the nation and was looking to exit. They wanted to take their money out of Poland and start investing in China.

These shopping centers were purpose-built to be occupied by Metro’s several large big-box/category killer concepts. Metro had a hypermarket tenant, an electronics retailer tenant, a “do it yourself”/Home Depot tenant, a “dress for less” tenant, and a big-box sports concept. Metro would add a McDonalds, a video store, and other service tenants to the mix and create a big-box center/mall. They built these centers as a way to have a first mover advantage and launch their retailers in Poland quickly. Metro had no reason to own the real estate long term; they had better uses for their capital than real estate and therefore, they just wanted out of the Polish hard assets. They had tried to list the portfolio on the Polish stock exchange as a REIT. When this failed, they valued certainty. This allowed us to negotiate a good deal. We bought these shopping centers for €775 million, refinanced them at €840 million a year later, when Poland formally entered the EU, and then sold 50 percent of the properties at an even higher valuation. We were able to generate an annualized rate of return of more than 100 percent on that deal over a long hold period and a multiple on equity of more than 5x—not because I’m a genius, but because we made the right call on Poland early and had the right partner in the Mitzner family. When Metro needed to sell quickly and wanted an experienced landlord in Poland that they could trust and live with over a long term, we were the natural choice. Apollo-Rida, our joint venture with the Mitzners, was established and ready to take advantage of the opportunity.

How did this happen? In 1996 a famous Pole and former professional tennis player, Woitek Fibak, took me on my first trip to Poland. After that trip I became convinced that Poland was never going back to communism. This was not a universally held belief.

However, I also realized that most of the local real estate people were inexperienced, or, worse, were likely to try to take advantage of a foreign investor. Luckily, we had a relationship with the Mitzner family. The patriarch was a Holocaust survivor who had moved back to Warsaw.

Apollo-Rida built its first office building in Poland with an 18 percent unlevered yield on cost, something unheard of in the West. That was followed by many more developments and acquisitions, including the acquisition of the Warsaw Trade Tower from Daewoo of Korea.

In 1996, I bet that Poland was headed in the direction of the West. I thought that they would be allowed into the European Union, their market would grow rather than shrink, and the value of these properties would rise—but I had to convince my partners, which was not easy. I had to make a compelling case.

During my time there, I saw massive opportunity. There was a large supply-and-demand imbalance. Demand was four to five times higher than supply, according to the market info I gathered. Before you begin to think that I’m clairvoyant, I didn’t discover these numbers simply walking around office buildings, warehouse buildings, and shopping centers and watching people; together with the Mitzners we spent significant time with brokers, market consultants, tenants, and customers. The local leasing brokers would provide lists of tenants that could not find space. Incredibly, these tenants were major credit multinationals. Their demand was well in excess of the existing stock of modern space.

At the time, many investors were bearish and worried that Poland would slide back into communism, taking their investments with it. Rather than listen to newspapers or pundits on television, I went to speak in person to the people who were living in this economy. We discussed the growing middle class and the availability of low-cost labor. The information I gathered got me very excited. I concluded that the availability of cheap, well-educated labor and a large population starved for Western products would be irresistible to multinational companies that wished to produce and sell in country.

People kept asking me, “Are they going back to communism?” I was just a kid at the time, but it was people my age who were to determine Poland’s future. They wanted freedom and prosperity and I saw they were prepared to work hard to achieve them. It was being on the ground and speaking to a myriad of people that allowed me to make a comfortable bet against Poland’s reversion back to communism.

The venture finally sold off its last shares in that deal in 2018, more than 20 years after my first trip. In this deal, like others before and some that would come, I realized that information is a very big advantage. You just can’t beat the value of local knowledge and boots on the ground.

Local Knowledge

Often money is made on the macro side of investing; you get the trend right and the trend is your friend. Buying real estate from the Resolution Trust Corporation (RTC) in the early 1990s was one of these great macro bets. Macro bets in real estate tend to be cyclical bets about timing, which means that you need to be able to make micro bets to generate excess returns when markets are in equilibrium. As it relates to micro bets, it is important to realize that land appreciating in value is the primary way to make money in real estate, because buildings depreciate. And that always comes down to location.

Knowing the details of the region where you are investing is of critical importance in real estate. Profit in purchasing land is the combination of local knowledge to find the right property and an understanding the macro principle of where you are in the current real estate cycle.

To succeed as a developer, I deeply believe you must stick to the region you know the best. You must understand the micro. Going outside your local area can be very dangerous—which leads me to my worst deal.

The Radio Tower King

After my success with the radio tower deal in Montauk, I thought to myself, “Hey, I know some things about radio towers. Now that we are doing private equity deals, let’s go and do more.” While we were looking for a large investment opportunity in radio towers, two junior members of my team uncovered something that seemed interesting. It was the opportunity to buy a radio tower construction firm.

The contractor’s pitch was that communication companies were asking him to deploy cell equipment towers and when no tower was built in a coverage area, he would be able to build them and lease space to the carriers. Unfortunately, this sale/leaseback pitch was simply not true.

I was a young 30-something back then, relying on very bright 20-somethings. Bottom line, we did not perform sufficient due diligence on the construction partner because we wanted to believe that he was acting in good faith. Unfortunately for us, he was not. Additionally, the numbers convinced us that it didn’t matter if we built towers at all because the income from construction itself was so good.

The problem was that the projections provided to us were wildly optimistic and bordering on fraudulent. Our business was real estate, and getting into contracting, which is a completely different industry, required a different skill set. We discovered that the contractors were lying to us about their ability to land contracts and own the towers. We got played.

We had a really good idea, but a good idea is not enough to guarantee success on its own. If you invest with the wrong people, rely on flawed documentation, or don’t fully understand the mechanics of the asset, you are doomed to failure.

I accept full responsibility for the loss we took on this investment. These mistakes led my worst deal to directly follow my first exciting deal. It was a good lesson.

The Stroke of a Pen

A single law change—the 1986 tax reform bill—put more than a few developers out of business. But in retrospect, it was this change in the tax law in the mid-1980s that set up Apollo and other real estate private equity fund managers for success. In the early 1990s, our company, Apollo Real Estate, made a great deal of money cleaning up the excesses that resulted from overdevelopment, overvaluation, and overlending in the 1980s.

Because of accelerated depreciation and tax syndication, many investments were made purely for tax reasons. When the law on accelerated depreciation changed, values collapsed and many real estate developers and banks lost a lot of money. The Resolution Trust Company was created to clean up the mess—to liquidate the assets of the banks and savings and loan companies.

In response to the unprecedented need for real estate capital, many of the large institutions that dominate the real estate market today were created or expanded dramatically. Real estate private equity funds, commercial mortgage-backed securities, and real estate investment trusts are examples.

Investment Philosophy

There are two primary areas you must understand to succeed in real estate: The micro and the macro, or the overall state of the real estate business and the particulars of each deal.

The most important question I ask myself in any deal is, “What is the current or expected cash flow that the property is producing and why?”

Determining this cash flow is critical. Although there are many subjective factors in every single deal, knowing how much money a property can generate is the one objective fact you can base your decisions on. You’re looking at both absolute and relative returns. You can assess if the risk and returns warrant the investments.

Talking about numbers and assessing risk isn’t nearly as glamorous or exciting as the subjective factors. Everyone thinks they are more important and love to talk about them, but those factors change all the time.

Don’t get caught up in that conversation just because it’s interesting. Focus on the factors that remain consistent. I always ask myself two questions when assessing an opportunity:

- 1. What do I firmly believe about this property that other people don’t believe?

- 2. If I’m wrong, what happens to me and to my investors?

The second question is far more important than the first. I’m trying to assess the potential downside. What will happen if every single one of my beliefs and assumptions is completely wrong? How hard will the downside be?

Knowing the downside of any deal is far more important than knowing the upside. When you are using this critical thinking process, success comes down to whoever has the better information.

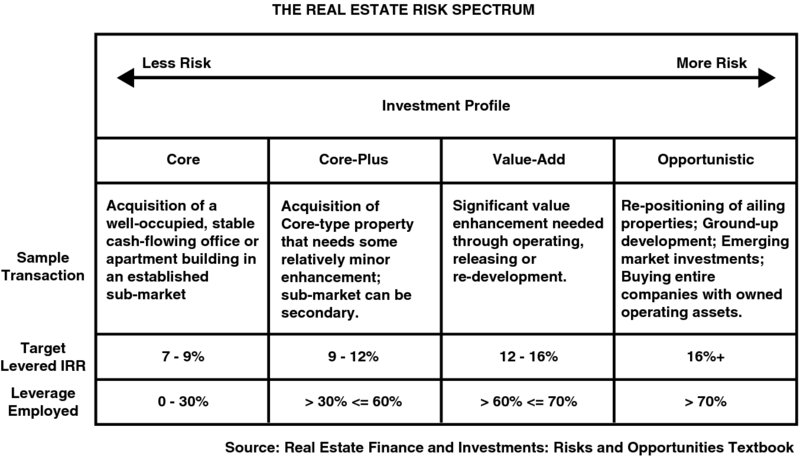

Within real estate investing at the property level, assets are usually clustered into four main categories based on investment strategy and perceived risk (see Figure 1.1):

Figure 1.1 Four categories along the spectrum of real estate risk.

Starting Over

New real estate investors like to ask me what I would do if I were starting over. Most people at the top of the mountain struggle to give actionable advice because they are too far removed. They don’t remember what it’s like at the start of their journey. It was too long ago.

When seeking a mentor and wisdom, approach local investors and try to find someone who is doing what you want to be doing in real estate—someone who is more successful than you and still remembers what it’s like to be in your position.

I started my real estate career almost 30 years ago and, as much as I’d like to say my memory is rock solid, my perspective is inevitably going to be colored by the lens of time.

Big Opportunities

In the United States right now, because of the regulatory environment, I see institutional ownership of debt as a very good opportunity with good risk-adjusted returns. In Europe, I consider value-add to be a more interesting space. In Mexico and Latin America, mezzanine financing and preferred equity for development is an interesting opportunity.

In Asia, in general, it’s very tough to get in as an outside investor, particularly in China. It’s going to take a period of local financial distress for us private equity outsiders to get a real foothold there. Watch the news for an Asian downturn or a time for Asian businesses to be more open to outside investment, especially in mainland China. That’s when the opportunities will start to appear.

Emerging markets in the world offer the biggest growth opportunities, but they also have the biggest risk. Growth is not only an indication of opportunity in real estate; sometimes, the flow of capital can be even more important.

You have to find the right fit to match your passion. If you are looking to get into property development, and you want to be at the start of something brilliant, then you can go to emerging markets. They’re building new things and taking amazing risks, and you can really create. You can be there for the first chapter of the story.

If your primary goal is to not lose money, there are better markets in which to focus your attention. A lot of people use real estate to support their pension, not just as a resource, but to provide returns later in life. That means you can take a lower risk for a lower return investment. That’s also a good approach.

A Little Leverage

Our business at Mack Real Estate Group has been building a lot of multifamily properties because home ownership has declined significantly in the last ten years. Right now, it’s shifting to a renter’s market.

As you look at the United States, the two biggest assets are in decline: office space and retail space. Having said that, there will be some great winners and losers in each of these segments, so you need to evaluate every single company on an individual basis.

Real estate financing is like a drug; if you use it correctly, it can have incredible beneficial results. But if you overuse it, then it can kill you.

Real estate is such a capital-intensive business. It’s very convenient to leverage debt, but the danger of debt is that a single shift in the market can push you underwater. This happened to so many developers early in the 1990s, and it’s how we were able to buy assets at very favorable prices.

In developed economies, it’s very hard to make projects work without the prudent use of leverage. Everything’s so expensive in developed spaces. You have to be far more strategic in order to achieve significant returns.

The success of every project is determined by timing. Be aware of how the markets are shifting and where the real estate market is in each cycle. We’re in the second-longest expansion in the United States´ history right now. Believe it or not, that bubble’s going to wear off soon. Valuations have increased dramatically over the last eight years (since 2010), but you should be prepared for that next downturn; it might be a harsh one.

Not every piece of investment wisdom comes from the world of finance. Wayne Gretzky, one of the greatest hockey players of all time, said what made him great is that he skates to where the puck is going to be, not where it currently is. It’s the power of anticipating. I apply this to real estate to mean filling the needs that currently don’t exist but where you believe the demand is coming, and having the vision to see that clearly. The most important thing when it comes to investing successfully in the real estate market is to see where the market is going to be in one, two, and five years.

The biggest mistake people make is when they believe in their own nonsense and get high on their own supply. It’s where you engage in speculative behavior because of overconfidence. Do not believe in yourself 100 percent; always hedge your risk.

If you slip from strategic investment into speculating, if your success depends upon a shift in the market, be prepared to lose. Speculating is where a lot of money is made, but it’s also where a lot of money is lost. When people speculate, they ignore the downside, and often, that downside comes calling. True long-term and strategic investing is about limiting your downside and being patient. There is a difference.

With every single deal—and I can’t stress this enough—it’s better to seek for a smaller downside than a bigger upside. There’s always another deal, whether very big or very small. No matter how long one stays in this game, and no matter how successful someone is, everyone has a story about a deal that went bad. Most of the deals that go bad do so because someone got overconfident and ignored the potential downside.

It’s exciting to get in real estate. It gets your blood pumping. There’s so much opportunity. But it’s also where so many people fail. As you look at every deal, as you approach every opportunity, do not get blinded by overconfidence. Never tell yourself that this is the one deal that won’t go wrong.

Technology

Technology will have a big impact on real estate, but it will probably affect it less than other industries. Retail is already getting disrupted, and e-commerce does need physical space. That’s why distribution is doing so well. Retail is probably going to need smaller spaces that are closer to home.

People continue to build offices, but office densification, office hoteling, outsourcing, and artificial intelligence are not bullish trends for office space.

Technology has led to a shift in the supply side of the hotel business. Every single person renting a room or their home on Airbnb is now in the hotel business. This platform will fundamentally change the hotel industry, but that industry will not go away. Ultimately, certain people will still want to stay in hotels. The extras that hotels offer will become more critical: the hotel restaurant, the concierge, the superior experience, and the help. When you stay at a hotel and ask for directions, they hand you a map. They’ll call a taxi for you. We can do most of those things with apps now. But that experience, the ability to have room service and great amenities, is what will keep hotels from shutting down.

People still like hospitality. They like experiences. They like flexibility. They will pay for them. This truth applies not just to the hotel market but to the residential, office, and retail markets. This is one of the lessons we all need to take from the emergence of coworking companies.

Keep the Faith

Mindset and skills are not the same things. You have to strengthen your mindset, or success is not a possibility. If you don’t believe in yourself, nobody else will.

This is where the advice gets hard: How do you find a balance between not believing in yourself and believing in yourself too much?

Instead of constantly struggling to find the right balance in how much to trust yourself, make your decisions from a place of logic and not emotion. Study the risk and potential downside of each deal before making any decision. Surround yourself with people who will disagree with you.

This will help you to stay in between those two ends of the market—from going too slow to going too fast, from not believing in yourself enough to try and make any deal to believing in yourself so much that you make a bad deal. In between, we can maintain our balance with proper research, information, and numbers.

It’s important to be self-critical and to maintain the balance between humility and confidence. It’s a very fine line, and every day, you have to wake up and walk that line without veering too far to either side.

People who lack humility might be right on numerous occasions. But when they are wrong, they rarely get second chances.

As a leader and investor, be humble and allow people around you to speak up and give you the input you need. Pair a belief in yourself with a strong sense of humility.

If we lack technical skills, believing in ourselves can be very dangerous. We need to combine our research, knowledge, and experience with belief, and that’s when we can achieve real success.

My Philosophy

I’m very fortunate that my role model and mentor is my father—someone I respect so much both as a human being and as a businessman. He has a great deal of respect for everyone around him. His commitment to giving back to the community has been deeply instilled within me, and he taught me the honor of keeping my word, understanding that the world is round, and that behaving honorably has its own rewards.

I’m a big fan of Theodore Roosevelt. He is the president who transformed the United States into a global leader. He had the vision to do things that might have been expensive and unpopular, like digging the Panama Canal. But he led without fear, and he had the nobility to step away from the presidency. It’s an incredible lesson to me on leadership and values.

I read at least one newspaper every single day and several on the weekends. I am a big consumer of nonfiction works, particularly those about leadership and business affairs. I see great value in spending time with my family and exercising. I’m an avid cyclist, and I just love spending time with kids and watching them as they play sports.

This leads me to my final pieces of advice. Your word and your reputation are more important than money. Once you lose those, it doesn’t matter how much money you have. People will stop wanting to do deals with you, or they’ll look at ways to get just a little bit more out of you.

Being productive is one of the keys to self-worth. No matter how successful you get, it’s never time to sit on your laurels. Selflessness is the key to happiness. You get more when you give than when you get. Contributing to society is wrapped up in hard work; work hard so you can give back more. You can’t take anything with you when you pass away. All you have left are the good deeds you carried out in this life, and those are the most important things.

Key Principles

- Having access to good information should provide you with power.

- There are times in every cycle where some real estate is mispriced, and for a short period of time, the market players will overlook this. Work diligently to find these opportunities.

- It’s very convenient to debt, but the danger of debt is that a few small shifts in the market can cause you to lose your entire investment. If you use debt, do so prudently.

- Land appreciating in value is the primary way you make money in real estate. And that always comes down to location and timing. To be profitable when purchasing real estate, you must have local knowledge to find the right property and to understand where you are in the current real estate cycle, which is timing.

- If you are a real estate developer or plan to be one, you should focus on the region you know best. Going outside your local area can be very dangerous.

- Be humble and surround yourself with smart people who will tell you what they think.

- Keeping your word and behaving honorably has wonderful rewards.

Exercise

When we look to invest in the stock market we are usually inundated with warnings regarding the inherent risks involved in this potential investment. In real estate, however, the average person is more likely to see advertisements claiming just the opposite: that it is easy to make quick money and take no risk. This is almost never the case. Prudent investors understand that if they are in the business of real estate they are in the business of taking risks, and they must become expert risk managers. The key is to learn how to mitigate risk. Therefore, imagine you had a $100 million dollar fund right now to go invest in real estate, where would you be in the risk return spectrum? Are you prone to taking on higher risk to get higher returns and are therefore opportunistic? Which sectors in real estate would you look to invest in? Why? What geographies? How would you mitigate most of the risks?