Chapter 15

Key Lesson #4: Educated and Quantitative

Sam Walton, the founder of Walmart, went to Brazil many years ago to meet with businessmen. He got arrested in the process. The cops thought he was a danger to society because they found him on his hands and knees, measuring the amount of space a store had between its aisles. Even though he was the richest man in the United States at the time this happened, Sam Walton had the modest attitude to understand that there was always more he could learn from competitors and businesses all over the world. These Titans all recognize that the world is simply too vast for them to have a complete understanding of it. They are intellectually curious, and they consistently seek to feed their minds with valuable information. While some of these Titans have prestigious college or master’s degrees, many do not. Their education did not come from school or university but from life experiences, and by learning from others who already achieved their goals. We live in a time when education is on the decline. Many people decide to stop learning new things when they graduate, whether it’s from high school, university, or a postgraduate program. Even more are being graduated from high schools across the country having never really learned how to learn. There is an old Native American saying that translates: “The day you stop learning is the day you start dying.” One of your most important deliberate decisions should be to continue educating yourself. There is always something new to learn. Many of the individuals interviewed in this book started their careers before the home computer even existed. If they chose not to learn how to use this tool or the smartphone, they might not be at the top today. They continually improve, and so should you. Remember that in life you develop a passion for things that you have interest in and that you are educated about. The more you know about a certain field the more you are likely to enjoy it. Every single Titan I interviewed reads at least one major newspaper every morning; a few read up to four. Many subscribe to world-class newsletters like The Memos with Howard Marks at Oaktree Capital Management or Byron Wien’s Market Commentary at Blackstone. There are many other newsletters and you should read some of these to get a well-rounded view of where the market is and where it is likely to go. The Titans join think tanks, Fortune 500 boards, private clubs, and other groups where they get to exchange ideas with elite thinkers. I have heard the finance and real estate expert Bill Ackman say on two different occasions that many of his investment ideas come from reading the Wall Street Journal. Exchanging words with Ronnie Chan, a real estate mogul in China, he said that he has gotten valuable business ideas from reading the newspaper. But it isn’t just about reading the financial and real estate news. Being a world-class real estate investor requires creativity, which comes from understanding many fields and connecting ideas. These Titans are intellectually curious, asking lots of questions and going down different avenues of learning to expand their minds. For instance, Bob Faith read a book by a healthcare consultant, which gave him instrumental ideas about how to carry out the property management in his real estate portfolio. He did not go out and find this information intentionally. It was serendipitous happenstance. As our Titans have repeatedly shared, some of their best business decisions have come from noticing changes in the market before everyone else. Find a source of news that will give you an advantage over your competitors. As different news sources lead either to the left or the right, you need to find the truth somewhere in between. More important than the daily stories you read are the trends you’ll notice. With the amount of information available to us in this digital age, it’s possible to become an expert in diverse business arenas without ever setting foot in the classroom. If all your information is only confined to one field or industry, you will probably be lacking perspective. This is especially true in today’s global interconnected world. Anyone willing to look can get new-found perspectives from books, other literature, and people. Doing so can also help you find anomalies or disruptions in an industry, in a specific market, in a city or neighborhood, or in a particular company. Recognizing the psychology of extremes in markets can lead to attractive entry points. Search your local or university library for thought-provoking books. Subscribe to high quality magazines such as the Economist, the New Yorker, the Atlantic, and so forth. Read newspapers such as the Wall Street Journal, the Financial Times, and the New York Times. Search documentaries. Search the internet. Scroll through your LinkedIn contacts and read the articles and blogs they post there. Each resource is full of opportunities for intellectual feasting. As an example, Ray Dalio, arguably the greatest financial investor of all time and founder of Bridgewater Associates, recently shared this in a LinkedIn post about acquiring knowledge. “Learning must come before deciding. Your brain stores different types of learning in your subconscious, your rote memory bank, and your habits. No matter how you acquire your knowledge or where you store it, what’s most important is that what you know paints a true and rich picture of the realities that will affect your decision.”1 He also recommends that every person read the following four books:2

What would happen if we all kept up an accelerated learning curve for the rest of our lives, and continued to read thought-provoking books and articles? The world would probably be a much more competitive place. If you are reading this then it’s because you do have the desire to continue educating yourself, to develop new skills and capacities. Therefore, I would ask you to do what the Titans recommend, to be that unusual person with an appetite for finding new ideas and solutions. Ronald Terwilliger states that after around 50 years in the development business, he noticed that very few development companies spent much time and energy encouraging their teams to analyze historical supply and demand trends. Only during a recession, once supply started to exceed demand due to overbuilding, and their businesses started to suffer, did they began to question the development business model. He therefore recommends studying past economic and real estate cycles to learn what not to do. Be a student of history. Rohit Ravi studied the history of India. He studied the stories of real estate within South India by reading books and speaking to other experienced and knowledgeable people. He knows when recessions began and when they ended. He knows when there were booms and when they ended because everything got priced in. He knows about the bull markets in real estate and the bear markets. He knows when there were wars and panics in India; he learned how market players and final customers reacted during those times. Because emotions take over during those moments, he learned that these patterns will likely repeat themselves. He also learned that you need to understand the business environments and you must have a vision of the future. However, to think of the future, you should also know the past. So, what are some good questions you can ask yourself when you are studying real estate history? Why did this downturn occur six years ago in the market and what can be learned from it? Can I draw any general or specific conclusions? What are some of the common characteristics of successful developers in this industry? What about developers? Why did some large real estate companies fail in this market or at this time, and what can I learn from that? What are some recurring patterns in this market or within my specific niche? How have zoning laws changed? How has that specific city grown? Remember that we cannot predict the future, but we can learn from the past. We can learn what worked, what didn´t work, and why it didn’t work. Real estate is, in large part, a numbers game. Without fail, every Real Estate Titan I interviewed in this book said the same thing. In addition, every Titan I have ever worked for or done business with is quantitative. This is not to say that they run advanced calculus in their head, but they do have a strong grip of the basic numbers that matter, such as potential sales or rents, development costs, operating costs, capital expenditures, going in and exit cap rates, margins, discount rates, internal rates of return, and so forth. A few of the Titans confessed to starting off their careers without mathematical skills, but through their hunger and curiosity, they learned quickly. They did this by immersing themselves in numbers and surrounding themselves with advisers and successful players to help them develop this skill. Like most things in life, you need to practice, and the more numbers you analyze the better you can become. One thing to note about spreadsheets and other analytical tools, they are only as good as the assumptions you include in them. What I mean is that spreadsheets can provide us whatever results we want and therefore the assumptions that we are projecting will eventually determine how close we are to reality. When we analyze real estate, we must be cold and neutral and not succumb to our desires of wanting to do the deal for personal interest or emotional reasons. One of the most useful tools that allows all the Titans to quickly examine the hundreds of investment opportunities they are offered is a Back of the Envelope (BOTE) analysis. What exactly is a BOTE analysis? It is a relatively simple mathematical computation that uses numerical assumptions to quickly develop a ballpark figure of the types of returns you could expect if you invest in that specific property or investment opportunity. It purposefully does not have too much detail so that you can quickly arrive at a preliminary conclusion and see if the opportunity passes the “smell test.” While the process may seem over simplistic or inaccurate—especially to young investment bankers who are absolute experts at creating sophisticated excel models with incomprehensible formulas and multiple sensitivities—it fulfills its purpose. Most of the time, these complex excel models are not necessary because property level analysis is not advanced science. Let´s run through the main elements required for a BOTE analysis of an existent commercial property. The main assumptions are:

Assume that we are looking to purchase a Class B multifamily building in the outskirts of Cincinnati, Ohio: a 100-unit property (70,000 square feet of leasable space) that is selling for $9.6 million. The property is at 95 percent occupancy and is producing $600,000 in annual revenues and has operating expenses of $120,000. Therefore, it has a net operating income of $480,000.

Because we know that occupancy for the past six years has averaged 95 percent, we are comfortable leaving this assumption untouched and do not assume any increase. We also know that current rents in the building are at market. As we look at the local market info and speak to different local brokers, we notice that the going cap rate of 5 percent is a little higher than market comps (between 5.75 and 6.75 percent) and the acquisition price per unit of $96,000 is also a little higher than recent transactions (note that in multifamily projects “price per unit” is often used as a metric). In addition, because we know that two lenders in the area are willing to finance 60 percent of the transaction at an all-in cost of 5 percent, we realize that the increased leverage would not increase our returns but would decrease the required equity. There are two additional things that we come to learn as we continue our analysis. The first is that these trusted brokers tell us that a new university is opening this year a few miles away, and this will cause net operating income to increase in the coming year by around 8 percent. They base this assumption on a similar situation that occurred in nearby cities. The second thing is that the building will require an immediate capital expenditure investment of $1.5 million according to a local civil engineer expert that already analyzed the property (this is normal since the building is 15 years old). The good thing about these capital expenditures is that they will have to be done in common areas like the pool and gym, so the apartments will go unharmed and can continue with their high occupancy. If we add these two variables to our analysis, then we can assume that the property will cost $10.6 million and will produce a net operating income of $518,400. Therefore, this would represent a going-in cap rate of around 4.9 percent. This would mean that if we were interested in obtaining financing we would have negative leverage, something that is not recommendable. As we analyze this deal, it is also important to examine the acquisition cost versus the replacement cost. We know that our cost is approximately $151 per leasable square foot. However, the trusted brokers and an engineer told us that the replacement cost is at $120 per square foot. With the information at hand, we can conclude that this deal is not too interesting, and we can either put it on hold for now or we can discard it. However, the intent of this analysis is to show you a way in which the Titans analyze real estate deals. Although the Titans are experts in BOTE analysis, there are also many situations in which a more detailed pro forma is required, especially if you have more variables and want to run different scenarios. The uses of a spreadsheet analysis are as follows: For ground up development of commercial real estate, you can see the changes in:

For acquisition of commercial real estate, you can see the changes in:

For ground-up development for sale properties, you can see the changes in:

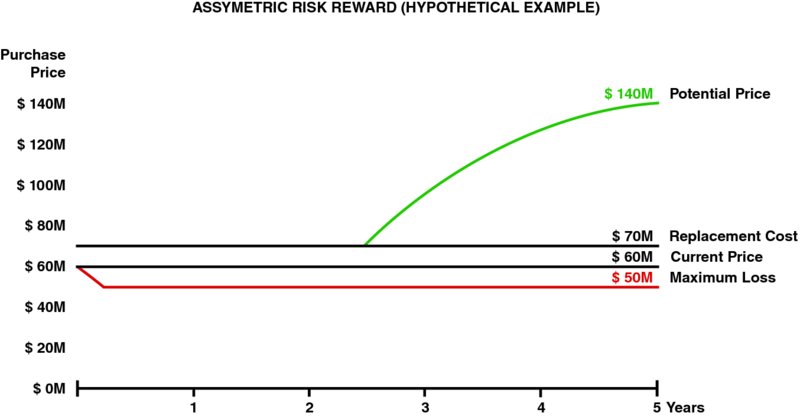

In all the above scenarios, spreadsheets can help you analyze equity and debt needs, financing terms and draws, refinancing terms and costs, tax effects and benefits, dividend and waterfall distributions to partners, and returns and equity multiples. A note about financial models and spreadsheets that the Titans know all too well: Because they are usually projected to have between 7 and 10 years, spreadsheets assume that there will always be an increase in rents and expenses. However, this is likely not the reality because there will be years in which rents will not rise but will fall. This is true even when you have long-term leases in place. Why? Imagine that you have a large tenant like Nike renting a space in your office building and they have a 10-year lease in place but in year 3 you all get hit with a hard recession. During that time it is likely that Nike will ask to renegotiate the lease because numerous other building owners are offering them better space on that same block for a lower rent. Most large tenants will renegotiate lease terms (including rents) during downturns and you have to be ready for this. The moral is therefore to be aware of your assumptions and to run several different downside scenarios. What happens if rents go down by 5 percent? What happens if your occupancy decreases from 95 to 87 percent? An important note on taxes: This book is written for readers from all around the world and therefore does not cover any tax discussion or fiscal issues. Like real estate, the tax code is local, and it is essential for you to begin learning about these codes and fiscal strategies as they pertain to real estate in your city. I would highly recommend you surround yourself with a good tax strategist to help you see how you can save on taxes and create structures that make sense. The bigger a player you are in real estate, the more savings you can have by creating smart tax strategies and structures before making an investment. These savings can result in years of work. As you become more educated and develop your quantitative skills, you will also become better at identifying asymmetric risk reward opportunities. The traditional theory in real estate might seem that you must take on a lot of risk to get high returns. But savvy investors believe quite the contrary. In fact, they usually get higher returns by taking on much less risk. So how do they do this? In simplified terms, they do this by making investments they believe have small risks but potentially big rewards. Because they are very active buyers when everyone else is desperate to sell, they can find bargains. They find investments with strong fundamentals that might look like bad deals at the current time of acquisition, but that with some small changes should ultimately be worth significantly more than what they are paying for it. See the hypothetical example in Figure 15.1 Figure 15.1 A small risk can yield a big reward. In this simple example, investors would be willing to buy at $60 million because they are buying below replacement cost, they have little risk, and they believe that in a few years the price will go to $140 million with some small operational changes. Therefore, they could make $80 million in profit. They also believe that their loss is capped to only $10 million in case of a maximum loss. This approach of 8 to 1 should be very appealing to any investor. See Appendix B for an example of a value-add investment. These Titans understand the power of compounding. I assume that you also do, but just in case you don’t I think it would be good to give an example. Many years ago, a real estate tycoon shared with me an intriguing story that taught me many things about the effects of compounding. For privacy reasons, we will call this person James. Through his relationship with a prominent landowner, James was able to negotiate the acquisition of an off-market vacant property that had residential zoning. Specifically, the landowner could develop two residential towers intended for sale in the outskirts of a very large city in a developing market. Because he had an investor base from past projects he had built, James was able to place a very small deposit to secure the site, let’s assume this amount was $1 (see Figure 15.2). He then had 60 days to turn around with his investors and raise the required equity to buy the property, and have as well some working capital for initial requirements such as design and permits. After he succeeded raising this initial capital, he focused on creating some preliminary designs with a local architecture firm and on obtaining the construction license. James also hired a marketing firm (that he would pay in case the project closed) to help him create some marketing materials to start selling the condos. Figure 15.2 Earnings generate more earnings over time. After accomplishing these diverse feats, James sat down with other investors that he knew and sold most of the units in this project to finance the entire development. Because he had a good reputation he convinced his investors that this was a very attractive opportunity to obtain high returns (+ 30% IRRs), and his company would be in charge of construction and development. James was charging a structuring fee as well as a series of development fees. In a period of six years (24 quarters) he made several million dollars with a $1 investment. Every quarter his money doubled. This is, of course, far from a typical return, but James managed to achieve this. Please note that this example is very specific to emerging markets because in most of these countries you can pre- sell condominiums in developments and use that money to finance the construction. This is not the case in advanced economies like the United States, where the money has to be placed in escrow in order to protect the buyer and ensure that in case the developer does not finish construction, they return the money to buyers. This example above shows how the power of compounding creates a snowball effect that occurs when earnings generate more earnings. You can receive interest not only on your original investment, but also on the dividends and capital gains that accumulate. Therefore, your investment can grow faster and faster as the months and years go by. This concept is very important to understand because it can significantly change your point of view regarding when you should invest, how you should invest, and in what you should invest. The power of compounding is also one of the reasons why experienced real estate players see this asset class as a long-term investment. A successful real estate player is one who can ask the right questions and understand how to mitigate the risk. Make sure you research your market until you comprehend which elements (micro and/or macro) are affecting your investment. With enough knowledge, you’ll begin noticing patterns and trends before your competitors. This type of understanding can lead to better decision-making and planning for the future—like preparing for a sellers’ market when you recognize the signals for one. In real estate, no matter where you are in the world, the volume of development and acquisitions is related to the availability of funds, not to demand. You need to understand demand, but unfortunately many real estate players are not rational. Real estate markets have a history of overbuilding when there’s easy money, without regard for who will occupy those spaces once they’re built. Therefore, be cautious and think of all the potential downsides. Economic downturns are inevitable. History confirms this. The Titans confirm this. We know downturns will come, but we don’t know when they will happen. To prepare for future economic downturns, look at the economic downturns of the past. What caused them? Which businesses collapsed? Which businesses thrived? Study the choices that separated the winners from the losers and implement those in your real estate strategy. This means finding and developing income streams for tough times. Part of this preparation entails always looking at the downside of any project or real estate investment before you proceed. Ask yourself two very simple questions: What would have to happen for this project to fail? Where is demand coming from? As you think about developing an advanced quantitative skillset, know that becoming a master in financing is a must. Chaim Katzman shared his points of view on financing. One of his important recommendations is to keep relatively low leverage on deals (or in case you have a company, on its balance sheet) and have a lot of equity. Financing can seem complicated when you first enter the world of real estate, but the rule of thumb is that when most financial entities are not willing to lend you money, it’s a good time to use leverage. In real estate, consider downturns and recessions as imminent. You need to be ready for a recession on any given day. You need to have your leverage at such a level that you can comfortably survive a two- or three-year period of difficulties. How can you do this? With long-term debt locked in, as well as available lines of credit that can act as shock absorbers to fill the gaps in times when the capital markets are open for refinancing. The line of credit is meant to help you breach periods when the capital markets are not open. Look at what happened to General Growth Properties, a large shopping center REIT that almost failed during the great recession of 2008. Between 2004 and 2008, they spent $7.2 billion in cash to acquire a bunch of shopping malls and a famous land development company. By 2008, General Growth owed more than $25 billion and didn’t have enough liquidity to make the debt payments. They were illiquid. In the real estate business having some liquidity is of crucial importance. What do banks love the most when it comes to real estate? Having really good assets, of course, ones that suffer the least during downturns and generate the cash flows that keep the lending institutions and bond holders very calm. These players know that the cash flows will be there to service the loans in a timely manner. Chaim Katzman also addressed the issue of personal liability and strongly recommended against it. As you study real estate history, you can note that in the 1980s in the United States, a lot of investors and developers got into trouble by agreeing to recourse financing, allowing the bank to access not only the property put up as collateral but also other assets the borrower owns. As Ron Terwilliger also pointed out, “Banks are the ultimate fair-weather friends. When you’re borrowing from a bank and things are going well, they’re your best friends—they’re happy to give you money, and they want to be in a partnership with you. But when things get tough—when there’s a recession or a downturn in the market—banks begin to think like machines. They are no longer your friends.” Pick two properties in your market and find out all you can about them. Practice doing a Back of the Envelop (BOTE) analysis on each one and decide if the opportunities make financial sense. Track them and when they sell, analyze how close you were in your analysis.Read

Feed Your Mind with History

Numbers, Back of the Envelope (BOTE) Analysis, and Spreadsheets

Taxes

Asymmetric Risk Reward

Understanding Geometric Returns

Prepare for Downturns

A Note on Financing

Key Takeaways

Exercise

Notes