While a chapter cannot do justice to the whole credit risk modeling process, we will try to incorporate multiple approaches to model building. Let's start with exploring our data for the mortgage book of a retail bank.

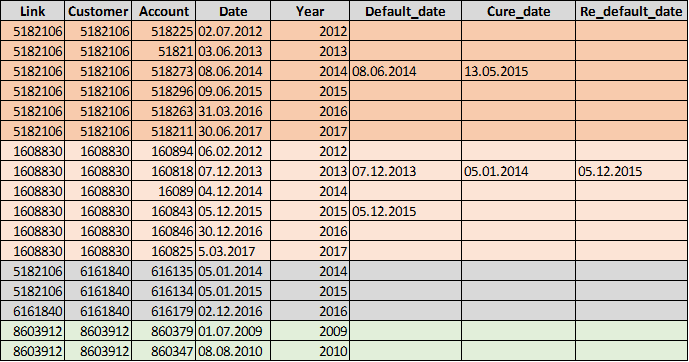

The concept of link, customer, and account is something that most individuals dealing with credit risk modeling will become acquainted with. These concepts can be named differently in organizations, but the relationship remains similar. Individual customers may come together to form a relationship. The variable representing such relationships has been called a link in Figure 3.1. Each customer is also expected to have various lending needs. In the case of mortgages, these lending needs may be mortgage terms across various years, varying interest rates, differing loan to values (LTVs), and so on. Each of these combinations of needs may exist as a product within the bank.

Every borrowing instance from the customer is usually assigned an account or facility ID. This is usually a unique primary key. For simplicity's sake, the following figure only contains one year of data for each account.

In the following example, customers 5182106 and 6161840 have come together to open two accounts, 616135 and 616134. These customers are linked together with the Link ID 5182106. Customer 5182106 seems to be the primary customer in the link. However, in the last account that customer 6161840 has, it has broken its link with the other customer, and has instead become the sole and primary customer attached to the account. There can be many other variables forming a relationship with various ID variables. For instance, collateral pledged to the bank may have its own collateral ID. This will be needed when calculating LGD at a customer level.

A customer may not stay in default for a long period of time. Once the customer meets the obligations of a borrowing account, the account may be considered cured. However, as the following example shows, customer 1608830 has what can be called a double default. Some accounts are closed at default, whereas others return to a cured status. In some data systems, the account may still be kept active, as most recoveries or write-off actions will happen only after the defaults:

The mortgage data in this instance is held in a time series format. The data contains observations from 2009 to 2017. This is a yearly snapshot of the customer's position. It shows the limit assigned to the customer, the drawn amount in the form of utilization, and the LTV ratio. The LTV ratio is calculated as borrowing/collateral. The collateral value may change over time, due to index linking of mortgage valuations over time. The customer may also provide more collateral for additional borrowing, and in some instances, such as account maturities, the collateral might be released, thereby reducing the collateral's value. Collateral, such as stocks and shares, may vary in value much more than fixed assets, such as properties. The collateral type is the nature of the collateral pledged. The portfolio value has been sourced from the credit application of the customer. The postcode index is a ranking of the postcode that has the mortgaged property. This isn't an index of the collateral property where the collateral type is property. The customer type is a flag to hold some profiling information about the customer. Arrears are instances when the customer is late on the account payment. Arrears don't mean that the customer is in default, or will go on to be in default. However, accounts with chronic arrear problems may have a higher probability of ending up in default. An account may be in arrears, but the customer may not be in arrears across various other accounts in the same time period. The following figure represents the independent variables: