CHAPTER 9

Revolutionary Incumbents

The 1950s was a perilous time for the tradition-bound British monarchy. A young queen’s adaptability, resilience, and agility were essential to repositioning the monarchy for long-term sustainability. Facing similar existential challenges, leaders of established health companies can find durable lessons in change management from studying Queen Elizabeth’s early reign.

In 1952, at the tender age of 25, Elizabeth Alexandra Mary Windsor became Queen of England upon the death of her father King George V. The first two seasons of the popular Netflix series The Crown depict the early years of Queen Elizabeth II’s reign as she assumes her new responsibilities and the monarchy adapts to a rapidly changing postwar world where many questioned the monarchy’s continued relevance.

This was a period of profound social change for Great Britain. Devastated by German bombing and catastrophic human losses during World War II, the country needed to rebuild. At the same time, the English people began a euphoric rush into a modernizing world characterized by growing prosperity, liberalizing social norms, and powerful new technologies, most notably television.

As Elizabeth assumed the throne, the British monarchy was out of step with the British people. Resolutely tradition-bound, it carried on as though nothing had changed. The monarchy’s inability to connect meaningfully with its subjects threatened its relevance. This became apparent in 1957 when a routine speech at a Jaguar factory triggered a constitutional crisis. Performing her ceremonial duties, Queen Elizabeth spoke in a perfunctory and patronizing fashion to the assembled workers:

We understand that in the turbulence of this anxious and active world, many of you are leading uneventful, lonely lives where dreariness is the enemy. Perhaps you don’t understand that on your steadfastness and ability to withstand the fatigue of dull, repetitive work depend, in great measure, the happiness and prosperity of the community as a whole.

The upward course of a nation’s history is due, in the long run, to the soundness of heart of its average men and women. May you be proud to remember how much depends upon you and that even when your life seems most monotonous, what you do is always of real value and importance to your fellow countrymen.

To a people weary of sacrifice, this stiff-upper-lip rhetoric no longer resonated. Lord Altrincham, the same age as the Queen and a staunch monarchist, heard the speech in a dentist’s packed waiting room. The other patients’ distinct lack of interest in and respect for the Queen’s remarks appalled him, but he believed the Queen herself was primarily responsible for the public’s declining interest in the monarchy.

Altrincham circulated a harsh and controversial critique of the Queen in the August 1957 National and English Review, a publication he edited.1 In it, he described the Queen’s speaking style as a “pain in the neck” and attacked her public persona in unsparing terms:

The personality conveyed by the utterances which are put into her mouth is that of a priggish schoolgirl, captain of the hockey team, a prefect, and a recent candidate for Confirmation.

Altrincham’s rebuke created a sensation and resonated with many. In a nationally televised interview with Robin Day, he made a prescient warning that the British monarchy needed to evolve or die. As Altrincham put it,

Until recently, monarchies were the rule and republics the exception, but today, republics are the rule and monarchies very much the exception.

The powerful are often the last to know that their influence has diminished. Loyalists tell them nothing has changed. Conservative instincts persuade them to stay the course. They miss obvious signals that the old rules no longer apply. They’re in more trouble than they realize but often fail to take timely action. Only the agile, adaptive, and resilient survive.

To her great credit, Queen Elizabeth listened to the criticisms and initiated sweeping changes to improve her connection with the British people. She replaced debutante balls with garden parties, began televising her annual Christmas Message, and opened Buckingham Palace to the British people.

Unlike most monarchies that have vanished over the past century, the British Crown continues to navigate an ever-changing world. In Prince Harry’s larger-than-life royal wedding on May 19, 2018, the Queen warmly welcomed once-divorced American Meghan Markle into the royal family. This was a sharp contrast to the traditional royal practice of forbidding marriage with divorcées. The Queen’s uncle Edward VIII abdicated the throne to marry twice-divorced Wallis Simpson, and the Queen herself forbade her sister Margaret from marrying her divorced fiancé Peter Townsend.2 How times change.

Queen Elizabeth’s skill in transforming the Crown’s relationship with the British people has kept the monarchy intact and relevant. Her adaptability to changing circumstances has been the hallmark of her remarkable 60-plus-year reign.

Like the postwar British monarchy, established US health companies confront a daunting transformational challenge. Their traditional business models are unsustainable and resistant to change. Customers and consumers want greater price transparency, care coordination, access, convenience, and value. Companies that meet those needs and deepen their customer connections will thrive as Revolutionary Healthcare takes hold.

There’s no time to waste. December 2017 illustrated how far some established health companies are willing to go to respond to healthcare’s changing market dynamics.

FIVE DAYS IN DECEMBER

When historians chronicle the transformation of the US healthcare system, they will cite the events of December 3–7, 2017, as a major turning point. In that remarkable five-day period, a series of blockbuster announcements rocked the healthcare industry. These transactions signaled that large health companies know status-quo operations are insufficient to meet customer demands for higher-value healthcare services. It’s not enough to get bigger—health companies must also become better by reconfiguring their business models to compete more effectively in the post-transformation marketplace.

Starting December 3, 2017, the following four seminal merger/acquisition announcements occurred:

• December 3: CVS Health announced its intention to acquire Aetna and its 47 million health insurance subscribers for $69 billion. The CVS release stressed that the “transaction fills an unmet need in the current healthcare system and presents a unique opportunity to redefine access to high-quality care in lower cost, local settings whether in the community, at home, or through digital tools.”

• December 4: Advocate Health Care (Illinois) and Aurora Health Care (Wisconsin) agreed to merge their state-leading health systems. Advocate CEO Jim Skogsbergh captured the transaction’s path-breaking aspirations when observing that “this merger is about transforming care delivery and reimagining the possibilities of health as bigger meets better and size meets value to benefit consumers.”

• December 6: UnitedHealth Group announced the acquisition of the DaVita Medical Group (DMG) for $4.9 billion. DMG serves 1.7 million patients annually through 30,000 affiliated physicians at roughly 300 medical clinics in six states. United stressed that the DMG acquisition will advance “care quality, cost and patient satisfaction through integrated ambulatory care delivery systems enabled by information technology and supportive clinical services.”

• December 7: Dignity Health and Catholic Health Initiatives (CHI) announced their intention to merge. The combined organization will be massive, with 700 care sites, 139 hospitals, 159,000 employees, and 25,000 physicians operating in 28 states. CHI’s chief executive officer Kevin Lofton emphasized the importance of building healthier communities: “We are joining together to create a new Catholic health system, one that is positioned to accelerate the change from sick-care to well-care across the United States.”

More evidence of healthcare’s transformational tipping point came on December 19, 2017, when Humana announced it was acquiring Kindred Healthcare’s home health, hospice, and community care businesses in partnership with private equity companies TPG Capital and Welsh Carson. Kindred operates 609 home health, hospice, and nonmedical home-care sites of service throughout the country. “Kindred at Home” will operate as a stand-alone company and enhance Humana’s ability to manage chronic disease patients more efficiently and effectively.

Describing the transaction, Humana CEO Bruce Broussard noted its ability to “advance [the company’s] vision for integrated care delivery . . . while building a transformative platform for the future.” Broussard added that “care in the home is a vital element of improving the health of seniors living with chronic conditions, allowing them to receive services in the comfort of their home, [and spend] less time in [high-cost] institutional settings.”3

2018 MEGAMERGERS

As 2018 unfolded, the hits just kept on coming: Cigna–Express Scripts; Mercy–Bon Secours; Beth Israel Deaconess Medical Center–Lahey Health; not to mention consistent rumors of a Walmart–Humana combination. Then in March 2019, health insurer Centene announced its intention to acquire fellow insurer WellCare, its biggest competitor offering health insurance products on public exchanges.

In January 2018, Amazon, Berkshire Hathaway, and JPMorgan Chase announced their intention to form a new healthcare company to serve their employees. As the New York Times noted:

The alliance was a sign of just how frustrated American businesses are with the state of the nation’s health care system and the rapidly spiraling cost of medical treatment. It also caused further turmoil in an industry reeling from attempts by new players to attack a notoriously inefficient, intractable web of doctors, hospitals, insurers and pharmaceutical companies.4

These announcements represent a major market shift. Value follows payment. Payment formularies are increasingly rewarding integrated health companies that provide superior health prevention, health promotion, and care management. To provide Revolutionary Healthcare, companies must reconfigure operations to deliver better care more conveniently at lower prices. They must keep their customers healthy as well as treat them when they’re sick or injured. They must consistently deliver great customer experience.

The power of bottom-up, market-driven reform emanates from the multiplicity of business models competing to win market share and generate profits. Many companies fail as markets evolve. Some companies succeed spectacularly by delivering more value to customers. This dynamic process constantly reshapes the marketplace.

AVOIDING INDUMBENCY5

Despite the value orientation implied by this torrent of blockbuster M&A transactions, most healthcare companies continue to invest in volume-based business models. This “defensive” strategy will work in traditional fee-for-service markets near term. Longer term, the failure to position an organization to succeed under full-risk contracting carries significant risk.

When incumbents cling to outmoded business practices at the expense of future competitiveness, they become “indumbent.” Indumbent business practices are myopic, rigid, and brittle. They double down on revenue-optimizing strategies dependent on negotiating leverage, while leaving themselves vulnerable to competition from value-seeking companies.

Failing to imagine alternative futures is the greatest risk that confronts established health companies during periods of industry transformation. To avoid nasty surprises, organizations must undertake an honest assessment of their internal strengths and weakness. Leaders must answer these types of fundamental questions to gain full awareness of their company’s strategic positioning and potential vulnerability:

• What is our mission? How well are we fulfilling it?

• What businesses are we in? Do we do them well?

• Who are our customers? How well are we meeting their needs?

• What are our competitive advantages and disadvantages?

• Which risks should we own? Which can we shift to others?

• Is our leadership and governance up to transformational change?

• Are we too dependent on current revenue models?

• How strong is our brand? What does it say about us?

• Do our operations square with our rhetoric?

An in-depth competitive analysis is the critical next step. Understanding market dynamics and competitors’ relative strengths are essential components of any repositioning exercise. Beyond this, health companies must dig into the following aspects of demand-driven change to gain strategic clarity regarding their potential to disrupt current operations:

• Full-risk contracting (episodic bundles and capitated payments)

• Alternative low-cost delivery channels (e.g., telemedicine)

• Price and convenience-driven services and diagnostics

• Consumer-preference healthcare (e.g., alternative medicines)

This type of strategic analysis is essential for all health companies, but particularly for hospital-based companies. Despite their differences in tax status and governance, both not-for-profit and investor-owned health systems have prospered under fee-for-service reimbursement. Healthcare’s activity-based payment models have generated significant operating margins to offset losses associated with weak market positioning, subpar governance, and/or poor execution.

In more stringent and value-based payment environments, health companies must reduce operating costs to achieve positive margins. There is less room for error. Marketplace demands for greater pricing and outcomes transparency are forcing industry consolidation, advancing integrated delivery, and exposing underperforming business lines. Incumbent health companies are repositioning. New competitors are emerging. Performance standards are rising.

Markets are agnostic and results driven. Customers care about quality, costs, and outcomes, not organizational mission or tax status. Given declining provider margins, achieving high volume with minimal quality and cost variation is essential to success (see Figure 9.1).

FIGURE 9.1 Increasing price transparency and new competitors are driving routine healthcare delivery toward commoditization.

As industry consolidation continues and health companies accept more risk, provider and payer business lines are blurring. To excel in this new environment, health companies will need to make tougher resource allocation decisions, adopt more flexible funding approaches, make smart capital/strategic investments, and leverage strategic partnerships. Performance will drive competitiveness.

In Revolutionary Healthcare, health companies will provide care where, when, and how customers want to receive it. Operating in this retail paradigm will require companies to rethink market positioning, strategic alliances, capital formation, and governance. Sustainability requires making the right strategic and resource allocation decisions. It also requires superior execution.

True measures of success relate to outcomes, quality, costs, and customer experience. Health companies with a clear understanding of their competitive strengths and weaknesses make better strategic positioning and resource allocation decisions. They determine when, where, and how they should invest and divest. Then they execute fearlessly.

Indumbent health companies that practice business as usual, that rely on robust fee-for-service payments for sustainability, that fail to address competitive weaknesses, are in for a rude awakening. They will lose market relevance. As Charles Darwin famously observed, “It is not the strongest of the species that survives, nor the most intelligent, but the one most adaptable to change.” The future belongs to Revolutionary Healthcare companies that can adapt to new market realities.

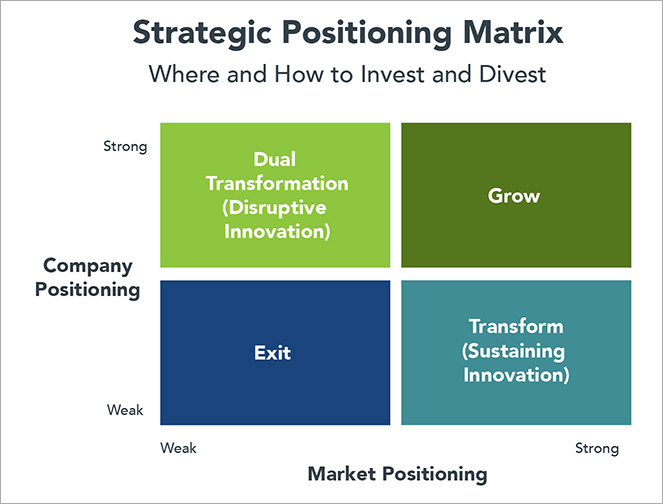

DUAL TRANSFORMATION6

Strong companies in declining markets (see Figure 9.2) need to undertake a form of dual transformation to remain competitive. As industry transformation and disruption unfold, these companies adapt their core business to new market realities while nurturing new business models that position the company for long-term success.

FIGURE 9.2 Company and industry positioning determine strategic choices.

As discussed in Chapter 2, large payers and providers have resisted transitioning to more holistic and value-based business models. They have deeply embedded organizational practices and cultures built for activity-based healthcare delivery and payment. Organizational requirements for assuming care management risk conflict with current business practices and limit strategic flexibility.

Trite but true, change is hard. Many leaders understand that their organizations’ long-term sustainability requires more efficient and effective provision of health and healthcare services. Yet they don’t know how to make the transition from current “sick care” business models to holistic “health care” business models.

Dual transformation is a methodology for making strategic transitions from old-world to new-world business models. Authors Scott Anthony, Clark Gilbert, and Mark Johnson chronicle dual transformation’s architecture and components in their insightful book Dual Transformation: How to Reposition Today’s Business While Creating the Future. Building on their work, authors Clayton Christensen, Andrew Waldeck, and Rebecca Fogg published a 2017 white paper titled “How Disruptive Innovation Can Finally Revolutionize Healthcare.”7 In it, they apply the theory of dual transformation to incumbent health companies.

Dual transformation recognizes that major organizational transformations are not monolithic efforts, but two separate and distinct journeys. “Transformation A” repositions core business operations to adapt over time to marketplace changes. This effort is undertaken even if those changes result in lower revenues profitability. The reason is simple: the development of new capabilities creates “new and better ways to solve old problems.”

“Transformation B” creates separately governed business ventures that develop disruptive business models. Transformation B “solves new problems in related ways.” For example, effective preventive health services reduce acute admissions. This generates superior outcomes that are better for consumers at lower costs. Nevertheless, such desirable outcomes are detrimental to the core business that depends upon acute admissions for revenues and profitability.

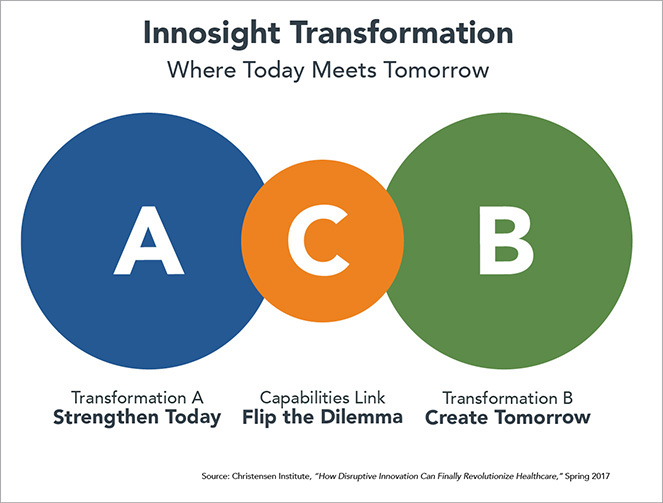

A “capabilities link” sits between Transformations A and B. Senior management judiciously allocates capabilities to sustain Transformation A’s operations while protecting and promoting Transformation B operations as they develop. Operationally, such an approach helps distribute difficult-to-replace assets and capabilities while keeping the organizations separate. It allows each organization to develop its own brand and partnership relationships while attracting the right talent. Essentially, Organization A does A while B does B.

This solution flips “the innovator’s dilemma” discussed in the last chapter. For health companies, it allows the organization to avoid the death spiral created by pursuing only higher-margin activities that benefit higher-profile customers. By design, Transformation A focuses on what’s best for core customers. Meanwhile, Transformation B can develop and pursue its disruptive business model. This often requires the development of entirely new capabilities and new revenue sources (see Figure 9.3).

FIGURE 9.3 Dual transformation enables companies to manage the current business (A) while developing the future business (B). Effectively allocating capabilities (C) is essential to organizational success.

For health systems, Organization A pursues effective and efficient healthcare delivery by “fixing patients when they’re broken” while also “sustaining their health” as appropriate in acute settings. In other words, they will satisfy the first two of the three customer jobs-to-be-done described in Chapter 8. Even as they provide these services, they will also strive to reduce unnecessary treatment activities.

In this way, Organization A will provide the right care at the right time in the right place at the right price. To do so, they will need to coordinate care efficiently, avoid overtreatment and undertreatment, utilize technologies such as telemedicine and smartphone apps, and decentralize care delivery to make it more convenient and less costly for customers.

Meanwhile, Organization B pursues the disruptive business of competing on “health,” not treatment, by fulfilling the last two of the customer jobs-to-be-done: sustaining and enhancing health. In other words, Organization B emphasizes prevention and wellness, areas that are desperately needed but poorly served with fee-for-service medicine. Organization B accomplishes this by providing enhanced primary care services, addressing social determinants of health, and attacking root causes of disease, which are usually social and environmental. Organization B seeks out new customers and new revenue streams through new channels. For example, such businesses may provide alternative medicine, meditation, fitness, and other health services that advance wellness.

“Liberated” data and analytics support both Transformations A and B. For both transformations, data flows to frontline professionals at the right time in the right formats to optimize decision making, resource allocation, and value creation. By focusing on consumers’ health and healthcare needs in this integrated and holistic way, health companies can engage consumers more fully and frequently. This builds brand loyalty and limits customer leakage to competing organizations.

The Fairview Health Services case study presented later in this chapter is a textbook example of dual transformation in action. Whether competing on healthcare or health, such companies optimize performance by delivering superior outputs more efficiently.

PLATFORMING HEALTHCARE8

Adapting to transformative and disruptive change is difficult for companies in any industry. It is particularly challenging for health companies because their current business models and practices conform to artificial supply-driven economics.

Traditional healthcare business models have generated profits but also created significant fragmentation in care delivery and coordination. Health companies must master efficient, convenient, and effective care delivery as they adapt to full-risk payment models for episodic and ongoing care. This makes the “Transformation A” process described above essential to long-term success.

The societal need for acute care services is not disappearing; however, the business mechanics of meeting that need are undergoing transformational and disruptive change. Delivering high-quality outcomes and high-value services will differentiate winning companies. This requires an Amazon-like “platforming” approach to business operations.

Relentless customer focus fuels Amazon’s business practices. The company’s goal is to own customer relationships through low prices, limitless choice, ridiculous convenience, and constant touch points. This strategy reveals a core truth: customers care about outputs (products, services, and customer experience), not the production process.

Platform companies like Amazon, Uber, Airbnb, and Netflix disrupt and reconfigure incumbent business practices. Essentially, they connect suppliers (where costs are) with customers (where the money is) by delivering superior products and services at competitive prices with great customer experience. They prioritize outcomes, not ownership and control.

Despite skewed markets, health companies are not immune from natural laws governing economics, human behavior, and innovation. To thrive in customer-oriented markets, incumbent health companies must redesign operating platforms to deliver better healthcare services at lower prices. They must relentlessly focus on outcomes through business model optimization (see Figure 9.4).

FIGURE 9.4 Great companies focus on outputs, not ownership and control of production functions.

All companies have inputs and outputs. The managerial art of great companies is organizing owned, partnered, and contracted activities to create superior products and services that customers want at competitive prices. Getting the formula right is essential to succeeding in competitive markets.

Traditional health companies invest in facilities and want full production control. Insistence on ownership and control makes these companies asset heavy and strategically flat-footed. They insource even when it’s more efficient to outsource. They frustrate customers. Platform companies are agnostic about ownership and control. They win market share by building efficient, cost-effective, and ever-improving networks of connected capabilities, suppliers, and data, assembled to identify and fulfill customer needs.

Healthcare delivery is complex. It requires coordinated execution across hundreds of business functions. At the same time, buyers of healthcare services increasingly demand performance consistency and pricing transparency. This market pressure pushes health companies to optimize all their physical, human, intellectual, and strategic assets. Confronting this operational challenge, platform companies align with strategic partners to deliver superior products and services. Great strategic partnerships create superior value for customers and partners alike.

Consider Target’s 2015 decision to sell its 1,600 pharmacies and 80 medical clinics to CVS Health for $1.9 billion. This was no ordinary transaction since the pharmacies and clinics remain within Target department stores while operated and branded by CVS. This was great for CVS, but it was also great for Target.

Target realized that it would never develop the scale and expertise necessary to compete effectively in retail pharmacy. Shedding its health business freed Target to focus on its core grocery and merchandising businesses. Target stores benefit from the increased foot traffic provided by new CVS customers. Target customers benefit from improved efficiency, lower costs, and more expansive pharmacy services.9

Kate Vitasek, professor at the University of Tennessee and author of the book Vested Outsourcing,10 studies collaborative business partnerships. Her research reveals that successful strategic partnerships focus on achieving targeted outcomes, establishing clear success measures, aligning incentives, and building mutual trust. In this way, the strategic partners operate from “the same side of the table,” pursuing agreed-upon objectives on predefined terms. Successful strategic partnerships exhibit the following characteristics:

• A mutual focus on client objectives, not transactions or processes

• Incentive-based compensation tied to clearly defined outcomes (e.g., reduced costs, higher sales, fewer errors)

• A shared commitment to mutual learning and adaptive program evolution

• Honest and regular program assessment (what’s working, what’s not, how to be better, new win-win opportunities, and whether the engagement should continue)

Given their importance and the resources required to manage them effectively, Vitasek believes companies should have only a handful of strategic partnerships. The best relationships are mutually beneficial and focused on outcomes.

Healthcare transformation and disruption will emerge largely through service innovation, not product innovation. They will occur as payment programs (risk-based, outcome-focused, bundled, transparent) reformulate incentives and retail-oriented competitors deliver routine healthcare services in new ways.

Healthcare’s essential participants are providers and consumers. An Amazon-like focus on meeting consumers’ jobs-to-be-done will differentiate winning companies. Platform companies will reorganize episodic and ongoing care delivery into discrete service offerings and compete on price and customer experience.

This platforming strategy is already occurring in select markets as evidenced by established and emerging businesses.

• Direct primary care (DPC) practices offer comprehensive services through activated care teams under capitated payment models, freeing them up to meet individual customer needs.

• Laser eye surgery clinics, colonoscopy centers, and freestanding MRI facilities offer transparently priced, low-cost, highly reliable procedures in convenient centers that are open nights and weekends.

• High-volume, high-quality, low-cost specialty surgery centers (i.e., focused factories) like the Hoag Orthopedic Institute are well positioned for profitability under bundled joint replacement payment programs.

• Online price-shopping apps like Vitals, a provider selection and price-comparison service. It matches patients with high-quality providers and offers cash incentives to encourage patients to seek lower-cost treatments.

• Improvements in home infusion services enable patients to receive care delivery at home. Outcomes are better, costs are lower, and patients are happier.

The list goes on. While the types of companies and services described above do not constitute total care integration, they can become effective component parts of service offerings assembled by health-oriented platform companies.

The movement to value-based care negates activity-based revenue optimization by paying for health outcomes, not specific transactions. In its purest form, value-based payments convert hospitals to cost centers. Established health companies are vulnerable to emerging platform companies precisely because their incumbent business models do not solve customers’ healthcare jobs-to-be-done. Pursuing revenue-first business practices as consumerism transforms healthcare is equivalent to fighting gravity. It works for a time but ultimately fails.

By contrast, platform companies are evolving to succeed under healthcare’s bundled and capitated payment models. They are powerful exemplars of revolutionary health and healthcare practices.

Revolutionary Healthcare companies strive to become “total integrators of health” by operating high-functioning, holistic business platforms. Buyers flock to companies that assure high-quality services, transparent prices, and great customer service. The AdventHealth case study later in this chapter illustrates how one revolutionary incumbent is changing everything to become the “connective tissue” for all its consumers’ health and healthcare needs.

Revolutionary Healthcare companies understand their strengths and the risks they should own. They relinquish control to partners and/or vendors that add value and generate better outcomes. They exert a relentless push to achieve competitive advantage by fulfilling consumers’ jobs to be done.

REVOLUTIONARY INCUMBENTS

No incumbent beats disruption and transformation by just doing what it does today better. Disruptive and transformative business models fundamentally challenge current business practices. There is no way to play the old game well enough to win the new game.

Instead, revolutionary incumbents acknowledge and embrace the disruption and transformation roiling the healthcare industry. They adapt operations in ways that improve their long-term strategic positioning and market relevance. Here are several case studies depicting how revolutionary incumbents are changing business models to solve customers’ and consumers’ health and healthcare jobs-to-be-

done.

On a Fairview Day

Fairview Health Services is an integrated health system affiliated with the University of Minnesota and serving the residents of Minnesota through an expansive care continuum. Its portfolio includes 12 hospitals, more than 100 primary and specialty care clinics, more than 70 senior and long-term care facilities, more than 40 retail and specialty pharmacies, pharmacy benefit management services, rehabilitation centers, counseling and home health care services, an integrated provider network, and health insurer PreferredOne.

Under CEO James Hereford’s leadership, Fairview is pursuing dual transformation. Fairview’s Transformation Center is redesigning the company’s healthcare delivery platform (Transformation A) to be leaner, data driven, and customer-centric. At the same time, Fairview’s Primary Care Transformation Design Team is redesigning the company’s primary care platform to compete on health and wellness (Transformation B). These parallel initiatives operate independently but with the same mission of making Fairview the best place for customers and consumers to address all their health and healthcare needs.

Hereford believes care delivery is rapidly moving from inpatient to ambulatory, retail, and home-based care sites. As care moves to lower-cost, more convenient settings, Fairview must rationalize its facilities and capabilities to serve consumers appropriately. This requires both care redesign and a powerful technology platform to guide information exchange and real-time decision making.

To that end, Fairview’s transformation initiatives center on the following three principles:

• One contact does it all. As Hereford puts it, “Fairview needs to vastly simplify how consumers receive service. We make it incredibly hard. We need to own the complexity for the patient. It shouldn’t matter if a patient is seeking a specialty appointment, an answer to a clinical question or a second opinion. There should be just one point of contact.”

• Precise coordination of care across events, settings, and time. Hereford emphasizes that coordination must expand beyond specific episodes of care: “Think about individuals undergoing a health journey over time. Fairview must support, monitor, predict, anticipate, check-in, consult and intervene appropriately on consumers’ behalf consistently and continually.”

• Solve the left-hand/right-hand problem. Hereford notes, “We’re a big system and we’re often not using our capabilities and capacity well. How do we leverage the system most effectively? Fairview must develop the ability to predict demands on resources while enabling staff to anticipate and respond strategically, not reactively. This will improve quality, limit mistakes and reduce costs.”

To operate effectively in complex and dynamic environments, Hereford decided that Fairview’s centralized data and management model needed a makeover. To implement a new delivery model, Fairview has partnered with Qventus, a company that applies AI-powered solutions to optimize patient flow. The Qventus platform ingests data from Fairview’s electronic medical record system and others. It then provides real-time operational and clinical data to frontline personnel who coordinate care within and between Fairview facilities.

With this system, Fairview’s frontline teams can see the larger picture, predict events, and make course corrections in real time. This “team of teams” approach pushes informative data to frontline staff to “nudge” optimal actions. Fairview also uses a combination of existing protocols and “intelligent interventions” that identify operational barriers and coordinate cross-functional activities to streamline patient placement, discharge planning, and ED activity flows. Hereford believes intelligent and timely data exchange is essential to solving consumers’ jobs-to-be-done. “I see this as one of the critical capabilities necessary to transform the experience of our patients. It is part of a larger strategy to redefine how a care delivery system works.”

Moreover, Fairview and the University of Minnesota Medical School are working together to reinvent academic medicine. They are redesigning their combined education, research, and clinical functions to support population health, frontline caregiving (through a master clinician program), social determinants of health, and right-sized tertiary/quaternary care delivery.

With the Minnesota marketplace rapidly migrating toward full-risk payment models, Fairview is pioneering innovative business strategies to deliver superior outcomes and manage associated operational and financial risks.

Guiding Florida Well

GuideWell Mutual Holding Company is a not-for-profit parent company created in 2014 from Florida Blue (the Blue Cross Blue Shield plan in Florida). Florida Blue’s leaders wanted to move beyond insurance provision in Florida to providing holistic, innovative, and transformative services that help “people and communities achieve better health.” Its CEO Pat Geraghty says, “We’re more than an insurance company, we’re a health solutions company.” GuideWell reaches more than 15 million people through its insurance products and provider services. Fewer than half of the people GuideWell serves are traditional Florida Blue policy holders.

GuideWell believes it should be an easy and seamless experience for its customers to choose the right coverage, consult with healthcare providers, and learn about healthy activities. GuideWell employs sophisticated data algorithms to segment their population of members and match people with the right insurance products and healthcare providers. Its service platform includes ED doctors, population health expertise, and in-home care delivery. GuideWell wants to give its customers the right information, the right coverage and the right care at the right places.

GuideWell operates state-of-the-art retail centers where individuals can walk in, discuss their care needs with a clinician, buy individualized health insurance coverage, talk to a dietician, participate in a class, and get a checkup. Geraghty says, “On any day you might see 60 seniors doing yoga. It’s dramatically different than being an insurance company on the sidelines of healthcare.”

GuideWell understands that addressing social determinants of health is essential to individual and community well-being. Seeing the proven links between literacy and lifelong health, GuideWell partnered with Marvel and Disney to create a health-oriented comic book, Habit Heroes, where superheroes applied sunscreen, brushed teeth, ate vegetables, etc. It was a huge hit. Habit Heroes became Florida’s book of the year and was read by teachers to students in all the state’s elementary schools.

GuideWell sponsored Habit Hero programs, where costumed heroes would visit its retail centers around the state. Geraghty said, “At the Jacksonville store, we had 1,000 people waiting to meet Iron Man when the doors opened. While at the center those families enjoyed games and educational activities, ate healthy food, and the kids received baseline health screenings. That’s not selling insurance.”

Beyond the consumer focus, GuideWell works with global leaders in healthcare and start-ups through the GuideWell Innovation Center. The center anchors a health science cluster in Orlando, Florida, where it facilitates collaboration to bring ideas and health solutions to the market quickly.

“We convene around major topics like mental health, cancer, and opioids, facilitating different stakeholders in their innovation round solutions. To address opioids, we had patients, caregivers, providers, law enforcement in to get a 360 view of the issue and outline projects the group can take out and develop,” said Geraghty.

The results of the expanded approach? GuideWell took ACA health exchanges into all 67 Florida counties and grew from 4 million to 5 million members in five years. GuideWell also administers traditional Medicare contracting for the federal government in 12 states and Puerto Rico. In 2017, Florida Blue had the highest member-retention rate of all the Blue Cross Blue Shield companies nationwide. “Retail centers are absolutely one of the key factors that drove that growth. People vote with their feet, and they’ve voted to join and stay,” says Geraghty.

Wasting no time, Geraghty is chairing an effort sponsored by the Florida Council of 100 (Florida’s 100 largest companies) to make Florida the “world’s health capital” and “healthiest place to live in the world.” Geraghty and GuideWell are making no small plans. They’re getting consumers’ health and healthcare “Jobs” done!

The Advent of a New Era

With over 5,000 clinicians and 80,000 employees working in more than 1,000 care sites, AdventHealth (AH; formerly Adventist Health System) operates an integrated care network of hospitals, urgent care centers, home health and hospice agencies, and skilled, compassionate nursing facilities across nine states.

After his wife Paula suffered a serious brain injury in a car accident, AdventHealth CEO Terry Shaw had difficulty finding her appropriate neurological care and strained to navigate through his own health system. They left the hospital with a stack of discharge papers and a good luck wish. Terry felt he and Paula were on their own to manage her care. That experience changed everything at AdventHealth. Shaw is repositioning the company to manage their customers’ entire care journeys wherever it may take them. Here’s how he explains AH’s new operating paradigm:

I never want to not care-manage you, not know where you are. I want to provide health for you where you are on continuum. We’re trying to put connective tissue back into a very disjointed system in a way that lets people understand that someone’s actually here and cares for you.

To bring this paradigm to life, Shaw simplified AdventHealth’s vision statement to five powerful words: Wholistic, Exceptional, Connected, Affordable, and Viable. AH applies these values to four understandable and relatable service standards: Keep Me Safe; Love Me; Make It Easy; and Own It. “Engaging the Consumer” is the first and most important of six new core work imperatives. AH is applying multiple strategies to engage customers. Check them out.

• A sophisticated “Hello Well App” places a powerful new care navigation and education tool in consumers’ hands.

• Partnering with Simplee, AH offers patient-friendly billing with multiple payment options.

• Spending $5 million per year to advance spiritual care.

• The ambitious “Project Fulcrum” aids middle-aged people with chronic disease to reduce stress and lead healthier lives.

• An even more ambitious project is the new AH network card that works like a wallet app through which customers can get lab results, schedule appointments, arrange consults, touch base with spiritual counselors, engage with lifestyle coaches, and more.

Shaw says, “Our goal is to get where our network card is more important to you than your insurance card. . . . I want customers and even their insurance companies to contact AdventHealth first because we take such good care of you.” The other five core work imperatives improve people and products, expand the network, lower the cost, and improve risk management.

With the strategic blueprint finalized, Shaw has gone door-to-door to communicate this new vision to managers and frontline professionals. All 80,000 AH staff, including physicians, are attending multiple “whole care experience” sessions. Terry Shaw says he is “not going anywhere” and is determined that AH will achieve the goal of offering consumers “a continuum of connected care to address every stage of life and state of health.” The Customer Revolution is alive and well at AdventHealth!

Revolutionizing Oral Health

DentaQuest is the nation’s largest Medicaid dental provider serving 27 million Americans across 30 states. It’s working to provide efficient, quality dental care services while also positioning itself as the nation’s leading prevention-based oral health company.

Historically, American medicine has segregated “oral” health from “physical” health in terms of access, coverage, and service delivery. This occurs despite the fact that prevalent chronic conditions, like diabetes, often first present in the mouth and require dental care as part of an ongoing care management program. This fragmentation is costly and wasteful. Lost productivity due to dental conditions costs employers over $6 billion each year. Over 2 million consumers visited emergency departments (ED) in 2012 for preventable dental conditions.

ED visits are the proverbial tip of the iceberg with dental care. Overall, 74 million Americans don’t have access to dental care services. These individuals are 29 percent more likely to have diabetes, 50 percent more likely to have osteoporosis, and an alarming 67 percent more likely to have heart disease.

DentaQuest president and CEO Steve Pollock says, “The current oral health system is broken. Too many people lack access to quality care or cannot afford the care they do get, and the industry overall is in dire need of innovative solutions.”

DentaQuest designed its ambitious “Preventistry” platform to fundamentally change the delivery of and payment for better oral health. The company has invested over $200 million to transform the oral health care system of delivery. Pollock gleams with optimism when discussing Preventistry:

Everyone can get a fair shot at oral health if we focus on prevention. The idea that we will prevent the problem before it occurs will lead to better outcomes for millions of people.

The company’s strategic emphasis is on implementing value-based oral healthcare as a component of holistic, systematic care. It’s pioneering this approach through Medicaid programs throughout the country. For example, DentaQuest has partnered with Advantage Dental in Oregon and the state’s Medicaid program to create patient-centered health homes and accountable care organizations (ACOs) that integrate physical, oral, and behavioral health.

The results speak for themselves. In 2016, over 11,000 children in Oregon received dental care in the community from DentaQuest, which is 10 times more than in 2012. Further, the Medicaid dental costs for children served by DentaQuest decreased by 10 percent compared to a national increase of 41 percent over this time period. Its Westborough, Massachusetts, center serves all types of patients. In that center, DentaQuest has reduced the percentage of patients requiring oral surgery from 22 percent to 9 percent.

DentaQuest has revolutionary spirit and intentions. Its Preventistry campaign features a clear call to action, “Revolutionizing Oral Health for Everyone.” Sound familiar? The Health Revolution will continue until all Americans receive whole-person care that encompasses physical, mental, spiritual, and oral care.

A Better Healthcare Steward11

In April 2008, CEO Ralph de la Torre took the helm of Caritas Christi Health Care, New England’s second-largest health system. At that time, Caritas Christi Health Care was among the United States’ worst-performing health systems. As a surgeon, engineer, and self-described “evangelist for integrated delivery,” de la Torre knew continuing the current approach would not solve Caritas Christi’s strategic and operating dilemmas. To add complication, the Catholic, not-for-profit system needed papal dispensation before selling its assets. With its sale to Cerberus Capital Management in 2010, the Caritas Christi converted to for-profit status and changed its name to Steward Health Care.

Changing ownership changed everything. As de la Torre observes, “Steward was founded as a business plan for a vertically integrated healthcare delivery, and Caritas Christi became its first acquisition.” De la Torre and his team set to the task of reinventing Steward as a competitively priced “integrated, community-based Accountable Care Organization (ACO).”

What a difference a decade makes. Now, de la Torre describes Steward as “a glorified managed care” company. It strives for global, capitated payments with financial rewards for achieving high-quality outcomes. Empowered primary care physicians “own their patients” and quarterback care.

In a landmark 2016 transaction, Steward sold its 9 hospital facilities and a small equity stake to the Birmingham, Alabama, REIT Medical Properties Trust (MPT) for $1.2 billion. Subsequently, MPT served as Steward’s capital partner in acquiring 8 CHS hospitals and all of Iasis, which included 18 hospitals and an insurance company. Today, Steward is an $8 billion health company operating in 10 states with a new corporate headquarters in Dallas.

Steward’s operating-company business model focuses on aggregating consumers into its care networks by being customer-centric. It affords greater flexibility without the heavy burden of facility ownership. It facilitates consumer connection.

Consumers want easy, mobile-friendly solutions for making appointments, getting directions, and finding physicians. Steward listened and delivered. Steward has revamped its digital and mobile platforms to ease, customize, and personalize patient/customer communication. The new platform mimics digital media for major online retailers like Amazon and Airbnb. Mobile traffic is skyrocketing.

Once an underperforming hospital-centric health system with limited capital access, Steward has become a dynamic for-profit health company with a national footprint, high-performing ACO, and expansive capital access. With its care management expertise and efficient operating platform, Steward is moving aggressively into Medicaid managed care programs.

Giving customers the services they want is a recipe for success in any business. As healthcare shifts toward value-based payments and consumerism, de la Torre believes health companies must engage and align with their patients/consumers. In a September 2016 interview with the Boston Globe, de la Torre stressed that Steward “will seek partners with a focus on wellness and prevention services.”12 In this way, Steward’s integrated and accountable care model provides solutions for all three of consumers’ health and healthcare jobs-to-be-done.

Having risen from the ashes of Caritas Christi by embracing customer-centric delivery, Steward sees abundant opportunity to bring accountable care into other US markets. Revolutions disrupt the status quo and create winners and losers. Like American patriots in 1776, Steward has marched outward from Boston with a revolutionary agenda. It’s bringing Revolutionary Healthcare to towns, hamlets, and cities throughout the land!

Selecting Care That Matters13

In 2014, Utah-based Intermountain Healthcare changed its mission statement to “Helping people live the healthiest lives possible.” A commentary accompanying the announcement demonstrates the power of organizational purpose:

We are now focusing even more strongly on prevention and wellness, on shared-decision making with our patients, and on using our resources and technology to help patients enjoy their lives without needing our hospitals and clinics, if possible. Our new Mission reflects that expanded role—it describes “why we exist.”14

Wow! Who wouldn’t want to receive healthcare services from a company that lives this mission?

Of course, rhetoric is cheap. Intermountain Healthcare put its lofty brand ambitions into practice when it launched a “shared accountability” insurance product for 2016. SelectHealth Share operates on the premise that providers, insurers, employers, and employees must collaborate to create affordable healthcare that delivers necessary medical services, promotes well-being, and engages all participants.

To participate, employers, employees, providers, and SelectHealth agree in writing to comply with provisions that support “predictable premiums, greater affordability and healthier lives.” SelectHealth Share excludes no one, but participation requires commitment and accountability. This can be particularly difficult for physicians and subscribers who cherish independence. The offsetting benefits, however, are wonderful—healthier workplaces, communities, and individuals.

People are flocking to SelectHealth Share not for what it does, but for why it does it. Customers connect with Intermountain Healthcare’s values because they make them feel better about themselves. These values burnish the image customers wish to project to others. Shared values create powerful company-consumer connection. It’s brand love in the making.

Bert Zimmerli, Intermountain Healthcare’s chief financial officer, repeatedly makes the statement, “Healthcare is personal. It touches our teams, family and friends.” Intermountain Healthcare lives its values. It truly cares about its community and its customers. Nothing is more important in winning customers’ trust and loyalty.

Not only does SelectHealth Share practice Revolutionary Healthcare, the company has embraced the terminology. Their website asks the question, “Ready to experience revolutionary healthcare?” How great is that! We couldn’t have said it better ourselves.

CONCLUSION: PUTTING MISSION FIRST15

During the 1992 vice presidential debate, Admiral James Stockdale, Ross Perot’s running mate, opened with these two questions: “Who am I? Why am I here?” That line generated a huge laugh, but its purpose was deadly serious—to establish rapport with the audience, share the Perot-Stockdale vision for the country’s future, and earn trust for a shared journey toward a better America. Health companies can benefit from similar introspection and connection. In Asheville, North Carolina, Mission Health did exactly that.

Mission is a highly regarded health company with six hospitals and $2 billion in annual revenues. At its biannual strategic retreat, Mission’s CEO Ron Paulus always asks his board a version of Admiral Stockdale’s existential questions: “Are we still best positioned as an independent not-for-profit (NFP) company to fulfill our organizational mission?” In 2017, the answer came back “No.” Paulus and the board concluded that Mission needed to be part of a larger health system to best serve its community.

Paulus then led a process to evaluate potential strategic partners. In March 2018, Mission announced its intention to sell to HCA Healthcare, the nation’s largest for-profit healthcare system. This was a landmark transaction. For the first time in recent history, a strong not-for-profit health system chose to sell to an for-profit system to achieve scale, rather than acquire or merge with another NFP health system.

In the wake of the announcement, many questioned the proper role of the profit motive in healthcare delivery. Yet, focusing primarily on profits and ownership transfer obscures whether NFP health system conversions advance community health and wellness.

In Mission’s case, there is more to the transaction than the HCA sale. Residual proceeds from the transaction will flow into an independent nonprofit foundation, the Dogwood Foundation. This new foundation will be among North Carolina’s largest, with assets higher than $5 billion. It will invest between $50 million and $75 million annually to improve health in Western North Carolina. Mission Health describes this new foundation as “transformational.”

As a for-profit company, HCA also must pay sales, property, income, excise, and other applicable state and local taxes. Early estimates suggest new property taxes will add roughly $15 million to the city of Asheville’s coffers. This represents a substantial increase, the equivalent of adding 8,000 new homes valued at $200,000 each. Mission’s board weighed all these factors before unanimously approving the sale to HCA.

The Mission-HCA transaction is part of a broader, disruptive trend confronting established health companies as they position to compete in a revolutionizing marketplace that emphasizes transparency, outcomes, efficiency, consumerism, and growth.

HCA is highly proficient at back-office operations. Its investment in artificial intelligence (AI) and the sophistication of its supply chain operations particularly impressed the Mission team. According to Paulus, HCA’s scale and operating efficiency make it “one of the lowest, if not the lowest-cost operators in the country.” For example, HCA makes a small margin on Medicare patients, while Mission loses 4–5 percent. While there is naturally grieving for lost independence, Paulus and the Mission board believed that their circumstances required a radical rather than an incremental solution.

Market dynamics are forcing many health companies to consider relinquishing local ownership and operating control. Ultimately, ownership and tax status are tactical decisions that do not define, in and of themselves, organizational mission. True measures of health system performance and community benefit relate to care access, care quality, operational efficiency, customer experience, and health status.

On these measures, a reconstituted Mission Health delivers. Selling to HCA enables Mission Health to contribute millions in local tax revenues, invest more in community health, operate nimbly, and innovate strategically. This means Mission Health is truly putting its community health mission first and sustaining it for the future.

Mission Health’s board chair, Dr. John R. Ball, made this point persuasively in describing the board’s decision-making process during an interview with the Citizen Times’ editorial board after the sale announcement:

The basic measure was what our mission is, which is to improve the health of people in Western North Carolina and the surrounding regions. That was the measure. Does any deal do that and do it better than we could independently down the line?

This is the type of game-changing strategic move that is transforming US healthcare for the better. Health companies across America would do well to heed Mission’s example of asking the tough existential questions honestly and evaluating the benefits and drawbacks of potential strategic transactions.

Revolutionary clarity and resolve are evident in Mission’s strategic repositioning. Paraphrasing SelectHealth Share’s provocative question, “Was Mission ready for Revolutionary Healthcare?” The answer is a resounding yes!