INTRODUCTION

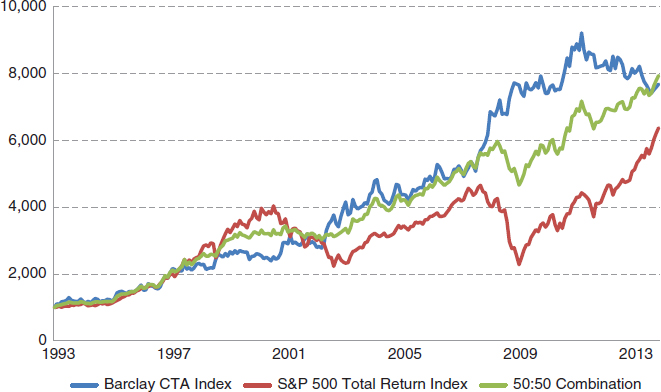

Trend following is one of the classic investment styles. “Find a trend and follow it” is a common adage that has been passed on throughout the centuries. The concept of trend following is simple. When there is a trend, follow it; when things move against you or when the trend isn’t really there, cut your losses. Despite the simplicity of the concept, the strategy has roused substantial criticism among neoclassical economists. For decades, trend following has been shunned as the black sheep of investment styles. In the classroom, in research, and even in the popular press, many have preached the word of efficient markets, touted the value of the equity premium, and asserted the importance of buying and holding for the long term. Figure I.1 presents the performance for trend following and equity markets. Figure I.2 presents the drawdown profile for trend following and equity markets. Over the past two decades, equity markets have experienced rather severe boom and bust cycles. Although trend followers follow trends across markets, the approach is seemingly uncorrelated with this dramatic boom and bust cycle. The drawdown profile for equity markets is akin to a high-speed roller-coaster ride. Although there are many benefits to long-term investing, this simple example demonstrates that the ride may be a bumpy one. In comparison, trend followers have a rather persistent drawdown profile. Despite a history of criticism, there is clearly something to following the trend.1

FIGURE I.1 The cumulative performance for trend following (using the Barclay CTA index) and equity markets (using the S&P 500 Total Return Index). The sample period is 1993 to 2013.

Data source: Bloomberg.

FIGURE I.2 The drawdown profile for trend following (using the Barclay CTA Index) and equity markets (using the S&P 500 Total Return Index). The sample period is 1993 to 2013.

Data source: Bloomberg.

The rather stable performance of trend following over a turbulent period for equity markets gives rise to several questions. What would happen if the trend following index had the same volatility? Or even more interesting—what would happen if equity markets and trend following were combined 50/50?

Figure I.3 plots the cumulative performance for equity markets, trend following at the same volatility, and a 50/50 combination of the two. The combination of trend following and equity markets seems to provide the most stable return series over time. Table I.1 lists the performance statistics for equity markets, trend following, and a 50/50 combination of the two. Both equity markets and trend following have similar Sharpe ratios, but an equal combination of the two increases the Sharpe ratio for equity markets by 66 percent. The maximum drawdown for the combined portfolio reduces the maximum drawdown for equity markets from 51 percent to 22 percent. Despite the simplicity of this example, there is clearly something unique and complementary to a trend following approach that deserves further analysis and inspection.

FIGURE I.3 The cumulative performance for equity markets (S&P 500 Total Return Index), trend following with the same volatility as equity markets (Barclay CTA Index), and 50/50 equities and trend following (S&P 500 Total Return Index, Barclay CTA Index). The sample period is 1993 to 2013.

Data source: Bloomberg.

TABLE I.1 Performance statistics for equity markets (S&P 500 Total Return Index), trend following at equity volatility (Barclay CTA Index), and a 50/50 combination of equity markets and trend following (S&P 500 Total Return Index, Barclay CTA Index). The sample period is 1993 to 2013.

Barclay CTA Index (at equity volatility) |

S&P 500 Total Return Index |

50:50 Combination |

|

| Average Return (annual) | 10.19% |

9.22% |

10.37% |

| Standard Deviation (annual) | 14.94% |

14.94% |

10.10% |

| Sharpe Ratio (annual) | 0.68 |

0.62 |

1.03 |

| Max Drawdown | 19.53% |

50.95% |

21.89% |

Modern-day trend following strategies are about systematically finding trends in market prices, riding them, and getting out before they revert. For this type of momentum strategy, there is both an art and a science to execution. The science of modern systematic trend following is facilitated by computational power and trading automation. Subjective (or discretionary) rules of thumb and heuristics have been replaced by structured systems of trading rules creating autonomous trading systems, the notorious “black boxes.” A modern systematic trend following system has become more like a finely tuned and engineered machine. These machines adjust their outputs (trading positions) as a function of price movements (inputs). Each system includes internal components (risk management systems) to regulate stressors and shocks.2 The design of these systems is structurally simple, efficient, and transparent. Simplicity and robustness is essential, as these trading systems manage hundreds to thousands of positions simultaneously.

The art of modern day trend following is in signal processing and trading execution. Trend followers use signals to determine when a trend is beginning or ending. These signals must be quantified, processed, and combined with other signals. Creating a connection between the signal processing and the corresponding trading execution for implementation is a skill that requires eloquence, experience, and a fine attention to detail.3

As with any comprehensive and arduous endeavor, this book begins with history by taking a philosophical and historical look at the concept of trend following over the centuries. The remainder of this book has the noble goal of demystifying both the art and the science of trend following from the perspective of the end user, the institutional investor.

■ A Foreword for the Remainder of the Book

The book begins by telling the tale of trend following throughout the ages. A multicentennial view of the strategy from a historical perspective sets the stage for the deeper more detailed analysis of modern systematic trend following in the remainder of the book. The book is divided into six core sections:

Using a unique 800-year dataset, trend following is examined from a multicentury perspective.

The goal of this section is to explain trend following system construction and the mechanics of trading in futures markets. Futures markets, futures trading, and the managed futures industry are reviewed. The basic building blocks of a modern systematic trend following system are discussed.

This section provides theoretical motivation for understanding why trend following works. The Adaptive Markets Hypothesis (AMH) is introduced and applied to derive and clarify the concept of crisis alpha. The concepts of divergent and convergent risk-taking strategies are introduced. This section explains the concept of market divergence and its role in trend following performance. Given that trend following is applied in futures markets, the role of interest rates and the roll yield are also discussed.

Trend following is discussed as an alternative asset class. The key properties of trend following returns are discussed, including performance measures, crisis alpha, crisis beta, drawdowns, correlation, and volatility. The concept of hidden and unhidden risks, leverage risk with dynamic leveraging, and macro environments are explained.

This section discusses return dispersion, benchmarking, and style analysis. The idiosyncratic effects of parameter selection are linked to return dispersion in trend following. A divergent trend following index and three construction style factors are introduced. The divergent trend following index and style factors are used to demonstrate the applications of return based style analysis. Performance attribution, monitoring, appropriate benchmarking, manager selection, and manager allocation are applications of style analysis.

This section discusses trend following from the investor’s perspective and advanced topics based on common themes earlier in the book. Topics include the role of equity markets in crisis alpha, the role of mark-to-market on inter-manager correlation, aspects of size, liquidity, and capacity, as well as the move from pure trend following to multistrategy. Finally dynamic allocation, or the question of when to invest in trend following, is discussed.

1 Market efficiency, equity premiums, and buy and hold are all important notions in finance. The point to be made here is that they do not negate the value of trend following. In fact, trend following is a natural complement to these concepts. The goal of this book is to demonstrate and motivate this point.

2 A cellular phone (or any mobile device) provides a good, practical example. Mobile devices have structured methodology for processing external inputs from a user. The functionality of a mobile device is organized by a network of systems coupled together with rules and instructions. These rules and instructions are initiated by external inputs. External inputs are processed, and an action takes place if the proper parameters of that action create a sequence of actions by the device. If there are actions that stress the system, there are internal blocks similar to circuit breakers and controls that deal with external inputs that are not within the bands acceptable for the device.

3 Returning to the analogy of a mobile phone, the structure and operation system of a mobile device must be functional. The art is in the external user interface and the eloquence in which it processes external inputs.