I live in Atlanta—home of the 1996 Summer Olympics and headquarters of Coca-Cola, Home Depot, the Atlanta Braves, and one of the largest airports in the world. It’s a city of roughly 6 million people, and it makes the list of the top 10 worst cities for traffic.

One big beltline draws a 64-mile circle around the city—Buckhead, midtown, downtown, and hundreds of “in town” neighborhoods. The majority of the population lives outside the perimeter (OTP) and must commute to inside the perimeter (ITP) each morning.

This is where the traffic nightmare comes to life.

My office is only 12 miles from my home, but it routinely takes anywhere from 25 minutes to an hour to get there. While on the road I see car after car of zombie-eyed individuals making the trek, battling urban sprawl. Every day I get the sense there are millions of hamsters on this wheel—home to work to home to work and then back to home and work again.

The shame is that so many of these working Americans can’t see the light at the end of the tunnel. They can’t visualize the promise of what was once a traditional retirement. It has been replaced by a sense that the hamster wheel spins for eternity, day in, day out.

It’s the same in other cities. Whether it’s a carpool in San Francisco or a subway ride in New York City, this sense of a never-ending cycle, of running in place, is destroying the hope of one day retiring like grandma and grandpa did—with a decent monthly pension, a “safe and sound” social security payment, and a nice chunk of savings.

These commuters, for whom the hamster wheel spins, are wondering if they’ll ever be able to retire. They’re 30, 40, 50 years old, teeming with envy for that nice couple down the street who retired at 56 and now spends every summer at the beach or in the mountains. We all know people like this, and we think: Can that ever be me?

Sure it can. In this chapter, I’ll show you how.

But know this: whether you’re retiring today or 20 years from today, the economic climate has changed drastically over the last few decades. The sooner you understand how and why, the sooner you can adapt.

How Not to Be Another Scary Statistic

Our parents and grandparents didn’t have to worry about retirement: they had a juicy pension waiting for them the moment they left the cubicle where they’d been slaving away for the last 40 years. I probably don’t have to tell you times are different now.

In a 2012 article for the investment site The Motley Fool, John Reeves points out some scary facts about retirement savings in America.1 He sources a study from the Employee Benefit Research Institute (EBRI) in which only 42 percent of private sector workers between the ages of 25 and 64 had any pension coverage in their current job. And anyone under the age of 50 who still does have a pension program in place will most likely find it far less lucrative than the plans of 30 years ago.

Only 14 percent of American workers reported being “very confident” that they would have enough money to live comfortably in retirement. Only 16 percent of American workers claimed to feel “very confident” about their investments growing in value. Another EBRI study from 2013 revealed:2

• 43 percent of all workers think they need to accumulate between $250,000 and $999,999 by the time they retire to live comfortably in retirement.

• 21 percent feel they need between $250,000 and $499,999.

Do these expectations mirror the realities? Not according to the study.

• 57 percent of workers reported that they and/or their spouse had less than $25,000 in total savings and investments (excluding their home and defined benefit plans). This includes 28 percent who had less than $1,000 (up from 20 percent in 2009).

Sound bad? The EBRI study found that nearly half of workers age 45 and older have not even tried to calculate how much money they will need to have saved by the time they retire if they want to live comfortably during that retirement.

Planning to let social security carry you into the good life during retirement? Think again. Reeves tells us that for a low earner retiring at 62, social security only replaces 40 percent of preretirement earnings.

Alarmingly, Reeves points out that nearly 75 percent of retirees have not saved enough and would save more if they could do it all over again. It seems like having the ability to find enough financial freedom for retirement at any age would be a modern miracle, right?

Actually, it’s not a miracle. But it does require making the right choices and persevering, even when times are tough. It means refusing to become another statistic and being proactive with your money instead. I’ve been privileged to work with hundreds of people whom you might think of as “that rich couple down the street”—who, by the way, probably have less money than you think. They just know what to do with it!

The happy retirees I work with aren’t scared by the statistics. They know they’re living in trying times, but they also know there are plenty of things under their control—like how much they save, how much they spend, and how they define their life’s purpose. They have the five money secrets at the heart of their financial philosophy, and thanks to those secrets, they’ve established comfort and cushion for themselves. Most important: they’re living happy lives.

Here’s one fascinating finding from my survey: the people who are happy with their money retire earlier than those who aren’t. The people who are unhappy? Many of them are still working. I get dozens and dozens of phone calls on my radio show from people who are 66, 68, even 70 years old—and they’re still punching a time clock. The other day I had a caller on my radio show who was 82 years old and still working!

I don’t want you to be one of them. I want you to be able to retire at 62, 60, 55—maybe even 50. And I’m betting you want the same. You don’t have to be rich. You just have to sit up and pay attention. If you want to get from point A to B, you have to be ready to fill the gap.

Adopt My Fill the Gap Strategy

The fill the gap strategy (FTG) is at the core of the work I do. But before I explain what it is, let’s cover some basics about money and investing.

You can make money in two ways. The first is through appreciation. As an example, I buy a stock at $10, it appreciates over 10 years to $20. I double my money in 10 years—great. The second is through income. I can buy a stock at $10 that pays me a dividend of $1 a year, and I can reinvest that dividend and, 10 years later, I’m at $20 as well.

Both work. Both appreciation and income got me to $20. What my firm does is tell retirees: “We’re going to get you a 4 percent yield on your investment.” That’s just a cash flow. Dividends, interest—all the things that come regularly from owning a dividend specific ETF (exchange traded fund), or Johnson & Johnson stock. Or a pipeline company. Or a bond. With just that part of the equation, you can get to a 3.5, 4, or 4.5 percent yield (alone), which is just the actual cash flow percentage that is paid out to you (or added to your account).

The other part of the equation is growth. How much in overall growth (also known as appreciation) should you expect over time? That part is less predictable, and will rely to some extent on how well the stock market and economy fare in any given year. In a year like 2013 when the U.S. stock market was up more than 30 percent, the growth part of your overall equation (perhaps half of your overall investments) should be up a similar amount, ultimately adding 10 or 15 percent in growth to the overall pie.

However, years like 2013 in the stock market are a somewhat rare occurrence—and not the kind of return you should come to expect or count on. So, on average, I am aiming to gain an additional 2 to 4 percent a year from this part of the equation.

Ultimately, we’re trying to get to 6.5 to 7.5 percent a year when you combine those two numbers. Remember, this is with a balanced portfolio of stocks, bonds, and other income-producing investments.

Considering everything we hear about the less-than-stellar rate of return the stock market has shown over the last 12 to 13 years, you may think these numbers sound unrealistic. Not so. Starting from 1926, long-term S&P 500 averages still come in at slightly north of 9 percent per annum. Think of everything that’s happened in the world during that span—the Great Depression, multiple wars, assassinations, terror attacks, natural disasters, and the recent Great Recession. Despite all that, the market still averaged a higher return than what we’re attempting to get for the people we serve. Feeling optimistic? Good. You should be.

When people are in their twenties, they think, “I don’t need dividends, I don’t need interest. I just want to buy stocks like Google and watch them go up.” That’s normal, and smart at that age. You have time to wait and room to maneuver. But as people get older, the strategy changes, and they naturally become more risk-averse. Think of it as a side effect of aging.

The fear most people have about retirement is, “Will I run out of money?” They say, “Wes, I want to get some income, and I don’t want my money to run out. Can you do that for me?” They’re all trying to fill the gap.

Can I help? Absolutely. It’s my job to help them fill the gap (FTG) to ensure their retirement income never runs out.

How do I do it? By structuring their nest egg to generate enough steady income to fill the gap. That way they’re only eating what’s in the fridge. And they never (or rarely) have to dip into the freezer and thaw out their principal.

Here are some initial steps to get your FTG planning underway:

1. Figure out your income. It’s simple: First, add up all of your guaranteed income streams (pension 1 + pension 2 + social security 1 + social security 2, etc.). This number is your steady monthly stream: it won’t change much and is in little danger of fluctuation. Let’s say that number is $3,500 a month (after taxes) for you. This is your “take-home income.”*

2. Now, figure out what your monthly spending need is. An Excel spreadsheet will work, Quicken will work, or just use a good old-fashioned pencil and paper. We have also put one on our website you can use free at http://yourwealth.com/resources-5/retirement-calculator.html. Let’s say your monthly expenditures come out to $5,000 a month.

3. Find your gap. Subtract your steady income sources from your spending need. $5,000 – $3,500 = a gap of $1,500 a month. That’s the perpetual gap you will need to fill—and also an amount that will need to be adjusted higher over time due to inflation.

Looks easy, right? Honestly, if your money is being invested the way it should be, it is. Retirees in the happy group make money work for them, not the other way around. Let it slowly and steadily grow over time, enjoy the additional income it produces on a monthly or annual basis, and have a blast during retirement. Piece of cake.

Your Financial Situation Is Unique—but Finding the Right Game Plan Will Be Easier than You Think

“But my situation is unique, Wes,” you say. “I’m not like those other people. I’ve got debts and obligations and a big fat mortgage. There’s no way I’ll ever be able to retire early—I’ll never be one of the lucky ones.”

Sure, your financial situation is unique, but so is everyone else’s. Each weekend, the Money Matters team and I field dozens of calls from radio listeners who are dealing with everything under the sun. During the week, I work at an investment planning and tax practice firm alongside 10 other financial advisors, CPAs, and Certified Financial Planner professionals whose job is to help people, no matter what they’re dealing with. Every day we respond to a never-ending combination of new financial situations and problems—and we still find ways to help.

Here are just a few of the variations we see:

• Difference in age between spouses

• Married, not married, widowed, and divorced

• Pension versus no pension

• The amount of social security

• The amount of savings

• The number of years until retirement

• The amount of risk and volatility you’re willing to take

• Fear of stocks, or love of stocks

• Love of bonds, or fear of bonds

• Business backgrounds

• Medical backgrounds

• Financial discipline

• Addicted to spending, or addicted to saving

• Kids versus no kids

• Grandkids versus no grandkids

• Healthy versus not healthy

• Great healthcare insurance coverage versus minimal healthcare coverage

• Employee versus business owner

• Great retirement plan at work versus absolutely no retirement benefits at work

The list goes on and on. But we’ve never been thrown by any of these variables. We’re still able to help every person who comes through that door.

Why am I telling you this? To assure you that happiness is possible for you, too. Every person has a unique combination of variables, but if you adopt the strategies in this book, you may still be able to retire happy and—with sound planning and hard work—earlier than you thought.

If You Want to Retire Early, Ditch the VIP Mentality

I’ll let you in on a secret: I’ve noticed a distinct difference between the happy retirees I work with today and the people I worked with during my time as vice president of investments at a very well-known Wall Street investment firm. (Without naming names, let’s call the firm a global financial juggernaut.) Interestingly, many clients of the firm had a “VIP mentally.” They yearned for celebrity treatment. They had money, but many of them weren’t at peace with it.

This is different for the families I work with today at my fee-only RIA (registered investment advisor) firm. They are just as wealthy but don’t demand extra special treatment. They’re more like the inconspicuous millionaires Thomas J. Stanley talks about in The Millionaire Next Door. They live in the suburbs of Atlanta, where the houses are between $200,000 and $500,000; they don’t live in Buckhead where the houses are $800,000 to $3 million. Think back to Nick and Katie Benjamin and how they took this similar track in order to build an early course toward financial freedom.

For these people, financial planning is less about being a millionaire, or what Stanley would call a PAW (Prodigious Accumulator of Wealth). They march to a different tune, a tune that says, “I’ve got enough money to be pretty damn comfortable and do what I want to do.”

If a happy retiree wants to play golf every day, she can. She doesn’t necessarily belong to an ultra-high-end country club that costs $100,000 to join, but she does belong to the Affinity Group of Golf, where she pays a really low monthly fee that allows her to play more than 15 courses across the state of Georgia. Sure, they aren’t private clubs with golden mermaids spouting rose-scented water, but they offer a solid consortium of well-maintained courses.

Needless to say, these non-VIP happy retirees really started to catch my eye. Their money provided them with a vehicle to drive toward the things they really wanted to do. As individuals or couples left my office, I’d notice they seemed satisfied with their positions in life. By and large they were having the time of their lives. Here are some examples:

• Marc and Candice love their RV and have hit about half of the states in the United States—they plan on RVing through the rest—including Alaska and Hawaii.

• Emily and Henry love to travel, but have never been to Asia—they are planning a trip there this year.

• Susan and Peter love to watch their granddaughter Brianna, who is in second grade. Brianna’s dad and mom both work, but fortunately for the entire family, Susan and Peter are ultra-active grandparents.

• Barney and Dotty are in their early to midsixties and are athletically active. They make it a point each and every day to either go for a walk, take a bike ride, play a round of golf, or play tennis.

All in all, these retirees are simply a much happier group, maybe because they’re happier living “in the middle.” That doesn’t mean they skimp on luxuries—after all, Barney and Dotty go to a nice steak house at least once a week and Emily and Henry love Korean BBQ—but it does mean they know how to put those luxuries in perspective. They’re also not interested in “keeping up with the Joneses,” because they understand the plateau effect: after a certain degree of wealth, happiness comes in diminishing returns.

Keep the Plateau Effect in Mind

Remember the “plateau effect,” where after a certain level of wealth is achieved, people experience a diminishing return of happiness? The plateau effect doesn’t just show up in regard to income, as we saw in the Preface. The exact same thing happens with spending: happiness tapers off after a certain point.

• Average spending from the unhappy group of retirees jumps 25 percent to reach the next level (the slightly happy retirees). But then spending levels begin to level out and rise at a much slower pace, eventually becoming remarkably similar.

• Median spending jumps by 60 percent from the unhappiest retirees to the next level of retiree. But then, once we’re into the happy retiree categories, it levels off significantly.

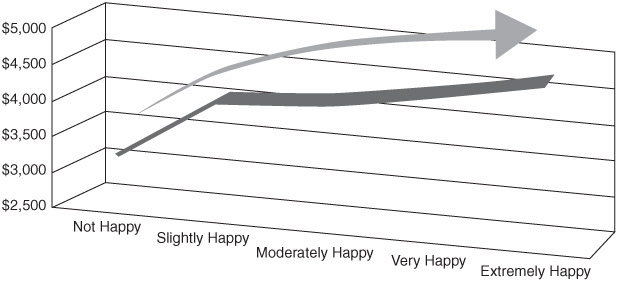

You might expect spending levels to shoot way up as happiness levels rise, but look at the graphs from my proprietary money and happiness survey in Illustration 3.1. The results might surprise you.

Illustration 3.1 Happiness by Spending Level (Mean)

As you can see from the graph, the plateau effect is on full display here. After a certain point, spending more does little to increase happiness levels.

Look at the mean (or average) data for each group. From the not happy to slightly happy group, spending jumps a noticeable 25 percent. But between the next four gradations of happy—slightly, moderately, very, extremely—spending only jumps 2 percent, 5 percent, and 6 percent respectively. Yes, the “average level of spending per month” rises, but not significantly. Slightly happy retirees spend $4,000 a month on average, while very happy retirees spend not much more.

What kind of income would it take to be able to spend $4,000 to $4,100 a month? A family would have to generate about $58,800 in pretax income to net $50,000 ($4,100 × 12 months = $49,200, rounded to $50,000).

Netting $50,000 at a 15 percent overall tax rate would require a family to have a pretax income of $58,822. Thus, up to a certain point, more spending means more happiness, but once a family reaches a median level of around $50,000 a year, there’s a decreasing amount of additional happiness with each dollar spent.

The plateau effect strikes again, serving as further evidence that more income and more spending only lead to more happiness up to a point. That point is very attainable to most Americans. (Note: This means you!)

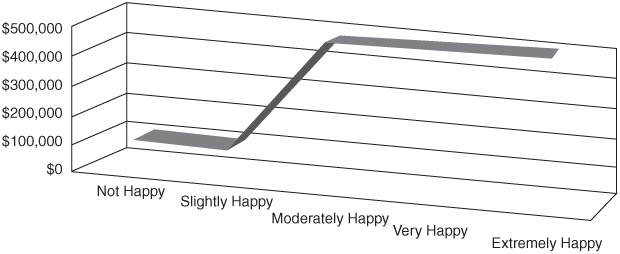

What about liquid net worth? Is there a plateau effect with your stocks, bonds, mutual funds, and cash? Take a look at Illustration 3.2.

Illustration 3.2 Happiness by Liquid Net Worth (Median)

You can see that $500,000 is an important inflection point for moving from the unhappy group to the happy group, but after that, not much changes.

The unhappy and slightly happy retirees have a liquid net worth slightly north of $100,000. If you move up the graph to the moderately happy retirees, you’ll see liquid net worth jumps all the way to $500,000. Looking at the data in this way shows that $500,000 in liquid net worth is an important inflection point.

Want to Retire Early? Be Like the Happy Retirees

Marc and Carol Hobbs are a prototypical happy retiree family. They’re one of those couples who seem to be having fun all the time. Hard to find a day of the week Marc isn’t playing golf, and Carol’s the same way—always relaxed, always headed somewhere to play tennis or help with the grandkids. And that’s when they’re not vacationing in exotic sunny locales.

How do they accomplish this lifestyle without being “super rich”? Marc and Carol live their lives by the five money secrets—and they were able to retire at 61 and 58, respectively.

Or take James and Wendy Camp. The Camps love working part-time, hiking Stone Mountain weekly, cycling for exercise, and going on cycling tours with large groups—Tuscany, Colorado, Washington State, you name it. They stay very fit, and Wendy retired early (at 62) to enjoy her many pursuits. If you think this is out of range for you, you’re wrong.

They say it’s never a good idea to compare yourself to others, but I disagree. If you see someone standing where you want to be standing, study that person! Figure out how he or she got there and what you need to do or change to arrive at the same place. As you read, I want you to start comparing yourself to the happy retirees in these pages. Take a look at the ways they’ve made the right choices financially—and figure out how you can do the same.

I’ve done the research for you. Those 1,350 retirees I surveyed? They’re featured in this book, spilling their secrets—about their core pursuits, lack of a mortgage, multiple income sources, savings, and the ways they became income investors.

Can you really retire sooner than you think? Sure you can. In this book, you’ll learn from the best.

Next on the Docket: Five Money Secrets

Purpose, Savings, Mortgage, Income, and Income Investing: these five money secrets are at the core of any happy retirement. In the chapters that follow, we’ll discuss each of these in greater depth.

Purpose

Money Secret #1: Determine What You Want and Need Your Retirement Money For

What do you want to do with your life when you retire? Happy retirees all have passions and at least three core pursuits they yearn to accomplish. In Chapter 4 we’ll see that core pursuits are the key drivers of the entire happy retiree journey.

Savings

Money Secret #2: Figure Out How Much Money You Need to Save Before You Retire

For every $240,000 you have saved for retirement, you can expect to have $1,000 a month at your disposal, provided you don’t retire before you hit your sixties. If you have more than $240,000, great. I like working with multiples of that number: $480,000, $720,000, $960,000, $1,200,000, $1,440,000, and so on. In Chapter 5 we’ll talk about how to translate these numbers into happiness.

Mortgage

Money Secret #3: Pay Off Your Mortgage in as Little as Five Years

Sooner or later, every homeowner asks the simple question, “Should I pay off my mortgage?” and immediately is bombarded with a variety of complicated, hedged responses. Here is the simplest possible answer: Yes. If you are anywhere near retirement and can afford to pay off your mortgage, you should. I’ll dedicate all of Chapter 6 to showing you how to make it happen.

Income

Money Secret #4: Develop an Income Stream from Three or Four Sources, Not Just One

We get used to receiving a W-2 paycheck or paying ourselves (as business owners) while we’re in our yeoman working years—one big paycheck to rule them all. This mentality has to change as we head into retirement, if not before. We have to go from one big income stream to a bunch of little ones. In Chapter 7, we’ll discuss the following income sources and more:

• Part-time work

• Part-time consulting

• Rental income

• Investment income (various types—Chapter 8 is dedicated to this)

• Social security (if you get it)

• Pension income (if you have it)

Income Investing

Money Secret #5: Become an Income Investor

In Chapter 8, I will submit my very own “bucket” approach, which is going to shift your whole investment paradigm. The bucket approach takes a very complex world of investing and simplifies it tremendously by helping you visualize your investments as money dropped into one of four easy-to-understand buckets.

This bucket diagram that I will walk you through is at the very heart of my “be happy in retirement” financial philosophy. It’s something that really resonates with our radio listeners and the families we work with direclty. I believe in trying to generate steady levels of income through dividends, interest, and distributions. Those three areas add up to a portfolio yield—something predictable in an otherwise unpredictable market.

Sound good to you? Read on.