Henry Grand paid off his mortgage on a Monday and retired that Tuesday. True story—I’m not making this up. If you want tips on how to be happy in retirement, Henry’s your man.

I’ve worked with Henry for a long time now, so we know each other pretty well. He worked for 40 years, and his wife, the lovely Ava Grand, worked for 25, starting as soon as the last of the kids got off the parent dole. Henry made between $80,000 and $120,000 per year—not a “1 percenter,” but he did fine.

He had the opportunity to take a retirement package when he was 64, but it required making five extra installments in order to pay off his mortgage concurrently. What was our advice?

Do it, Henry! Do it!

Why do I feel it’s so important to turn your mortgage into ancient history? Sooner or later, every homeowner asks if he should or shouldn’t and is bombarded with a variety of complicated, hedged responses.

Let me offer the simplest possible answer: Yes. If you are anywhere near retirement and can afford to pay off your mortgage, do it.

All the successful retirees I’ve known—the folks who are living their dreams—have eliminated or dramatically reduced their mortgage payment before pressing the retirement button. Paying off a mortgage by the time you retire will bring you enormous peace of mind by dramatically reducing the amount of income your nest egg must produce to create a sunny-side-up retirement.

The data from my survey brooks no objections: happiness levels rise undeniably as mortgages vanish. And why not? A mortgage, at its simplest, is a large amount of debt. Who wouldn’t be happier without that hanging over their heads?

It can be hard for unhappy retirees to see the light at the end of the tunnel when it comes to paying off their homes. Here they are getting close to, or in the middle of, retirement, yet they are still trying to find new ways to pay for the mortgage. This means they aren’t spending money on the things they really want to be buying. It’s all going toward nondiscretionary items and items you have no choice in paying, the mortgage being the largest. It’s easy to see why this would make someone unhappy.

Flying in the Face of Conventional Mortgage Wisdom

While I have a very strong conviction that paying off the mortgage leads to happiness in retirement, not everyone shares my opinion.

Conventional wisdom says that if you can earn a higher rate of return on your investments in the stock market than you are paying in interest cost on your mortgage, then you should keep the mortgage—and not pay it off early. Say you are paying 5 percent on a mortgage and you’re in the 25 percent tax bracket. The net interest cost of your mortgage is about 4 percent. If you can earn 5 or 6 percent or higher through your investments, why pay off the mortgage with funds that could be earning a higher rate of return than you are paying in interest, right?

Ric Edelman is a big proponent of this line of thinking. A New York Times best-selling author, he has written extensively about the financial benefits of keeping a mortgage, and his argument is very compelling. He scrutinizes paying off the mortgage and implores you to invest that money, in order to earn a higher rate of return.

Let’s say you owe $100,000 on your house, and you have that money available in after-tax savings. The bank is charging you 4 percent on your mortgage. Rather than pay it off to avoid the 4 percent, Edelman wants you to put that $100,000 in the stock market and make 8 percent on it. Logical argument.

Simple analogy. Simple terms. If I pay off the $100,000, I make $4,000 by not paying that interest on my mortgage. But if I put it in the market instead, I can make $8,000. Subtract $4,000 from the $8,000 and I’m still up $4,000. Good times, right?

Not so fast, Mr. Edelman.

What if the stock market doesn’t go up for a year or two . . . or three or four or five? What if it ends up being relatively flat for a decade, like it was in the 2000s? You wake up one day and realize you’ve been paying interest on your mortgage but your stock market investments haven’t been holding up their end of the bargain. Where do you come out then? Not $4,000 ahead as the theory would have you believe. The stock market doesn’t kowtow to theory. If it did, a lot more people would be driving Bentleys, believe you me.

The average investor is not making a steady 8 percent per year, so why would we advise people to trust the market rather than paying off their mortgages? Furthermore, in “real life,” most people don’t have 100 percent of their money in stocks, and those who do probably end up timing the stock market poorly. It is widely understood in field of behavioral finance, that over time most individual investors typically end up with returns far less than what a particular average does (i.e., REITs, U.S. stocks, international stocks).

With that in mind, advising people to not pay off something that is costing them a known 4 or 5 percent (and in many times over history, higher than that) and betting on the unknown possibility of 8 percent is an argument that falls on deaf ears for me. I just don’t buy it.

Benefits of Paying Off the Mortgage

Now, here’s what I do buy: that paying off your mortgage will make you a whole lot happier in retirement. Consider the following two benefits, for starters:

• It’s obvious—you are no longer paying interest to the bank. Didn’t the Aflac duck tell us that saving is the same as earning? Or was it Howard the Duck? I’m mixing up my mallards, but that won’t stop me from keeping your mortgage ducks in a row. In fact, in this case saving is even better than earning because at some point you will be making interest on the money you save. Now that’s what I call a golden goose!

• Paying off your mortgage gives you the budgetary freedom to spend more money on finding purpose and happiness in life. I don’t know about you, but I don’t find much purpose in cutting a check to Wells Fargo. Whether it’s travel or volunteering, mountain cycling or Scottish games, you should be spending your money on the things that give you purpose and happiness.

No matter how much you love your home, remember that the mortgage payment is still just money for shelter. And while that turn of phrase sounds like it would be the title of a cool Rolling Stones song, it isn’t.

The One-Third Rule: If It Applies to You, Write a Check Today

If I’m not paying that mortgage note anymore, it lowers my spending tremendously and puts less pressure on my overall financial plan. Think of your retirement assets as an engine. You’re no longer working, so that engine has to function with the finite amount of oil already in it. No more oil changes at the Jiffy Lube. Every thousand dollars you spend revs your retirement engine another thousand RPM. With the mortgage payment being the biggest expense, you’re spending thousands of dollars more a month—and are in danger of redlining the engine.

The more RPM, the more things have to go right in order for your engine not to crack. Yet here you are spending possibly up to nine grand a month. Not even Mr. Goodwrench could keep that engine from cracking. Get rid of that mortgage before it’s too late!

What no one else talks about when giving mortgage advice is the psychological burden that comes along with having a mortgage, and the subsequent release people feel when they’ve paid it off. I can crunch the numbers as well as the next guy, but if you walk into my office or call into my radio show and ask why you should pay off a mortgage with funds that could be earning a higher rate of return than the outflow of interest payments, I look you square in the eye—even if it’s via radio waves—and tell you straight: the happiest retirees care more about happiness than risking engine failure for just a few more shekels.

Of course, the answer to the mortgage question will be different for people in different stages of life and people who have different tolerances to investment risk. But as you think about your mortgage, consider the following rule:

The One-Third Rule: If you can pay off your mortgage using no more than one-third of your nonretirement savings, consider writing that check today. If, for example, you owe $40,000 on your home and have $150,000 in savings, not including your 401(k) and/or IRA funds, eliminating the mortgage lifts a burden and leaves you plenty of cushion for unexpected expenses. Let’s say your mortgage balance is $150,000 and you have $300,000 in nonretirement investments. Now, you could pay off the mortgage in a lump sum. But it would deplete your nonretirement assets by a full 50 percent. And subsequently wipe out a huge portion of your “liquid assets” that can also serve as a cash cushion. That’s too much of a hit, and in this case I would advise against it.

Your mortgage interest rate is inevitably higher than the interest CDs or short-term bonds will give you. This may give comfort to some conservative investors: If you are a very conservative investor who prefers the stability and reliability of CDs and short-term government bonds to the volatile S&P 500 stock index, you may want to drastically accelerate your mortgage payoff. CDs and bonds will almost certainly earn less than the rate you are actually paying on your mortgage. So there is little to no advantage to keeping money in an account earning less than 1 percent when you are paying 5 percent on your mortgage balance.

Disciplined investors can wait. For those who would still prefer putting $200 into a mutual fund each month, rather than paying an extra $200 on the mortgage, that’s okay—as long as you are disciplined about it.

Oftentimes investors who choose not to accelerate their mortgage payments in lieu of investing elsewhere end up failing to invest it elsewhere, putting them right back on track to Unhappy City. I’m all for putting an extra $200 toward your favorite Vanguard dividend-paying stock ETF, but just don’t let it fall through the cracks. As much as I want that mortgage paid off, it’s not a good idea to head into retirement with a house fully paid for at the expense, no pun intended, of having no money in the bank. Last time I checked, you can’t pay for groceries with shingles from the roof.

Paying Off the Mortgage Gives You a Break

For those nearing retirement, paying off the mortgage creates what I call a deflationary moment in their financial planning. Think about all the financial outflow in your life. Are any of those prices going down? Colleges are getting more expensive; healthcare is getting more expensive. Gas, cars, land, daycare, food, milk, eggs, coffee beans are all getting more expensive by the day.

With all this inflation in our lives, when do you get a chance to see any deflation? Give a guy a break, right?

Paying off your mortgage is that break. You’re deflating the amount of money that has to go out the window, and it’s something that lasts forever, which is a very powerful and positive psychological force. Knowing that the bank can’t touch the dwelling in which you hang your hat feels damn good.

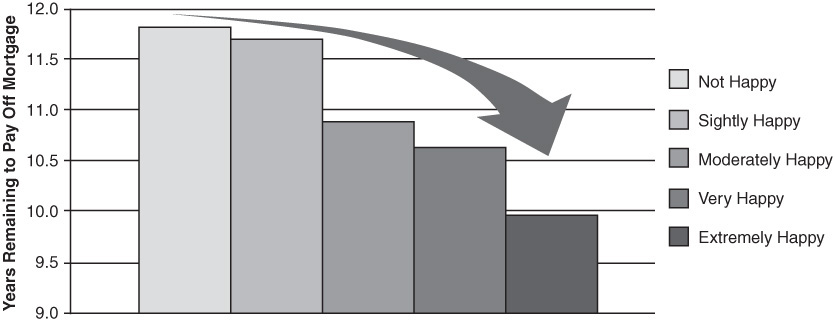

I’ve learned from the happiest retirees that there is a certain amount of calm and security in the cushion of knowing your house is your house, free and clear. If you want to join the ranks of the happy retirees, you’ve got to pay off the mortgage. Look at Illustration 6.1.

Illustration 6.1 Years Until Mortgage Is Paid Off (Mean)

As you can see, the fewer years retirees have left on their mortgage, the happier they tend to be.

I want to reiterate: the number of years to pay off the house goes down as the amount of happiness goes up. On average, happy retirees have their mortgage payoff date within sight—roughly 10 years, and often closer to 5.

In contrast, the unhappiest retirees have somewhere between 11.5 and 12 years left on their mortgage. So, the closer you are to having it paid off, the more likely you are to be happy. Some of the factors are tangible, some aren’t, but from all my years of experience in this field I can tell you that the best move overall is to pay off that mortgage by the time you retire (if you can). The financial and psychological factors both play huge parts.

Morty Shortened His Mortgage Repayment—and So Can You

Let’s take a run at this topic from a slightly different angle. If you can’t afford to pay off your entire mortgage with one (or a few) large payments, then the best way to approach it is to accelerate your payments each month.

This might be the biggest eye-opener and most realistic way to get rid of your mortgage in practice. Many of the families I work with do it this way and they seem to have good results.

A great way to do this is to go to bankrate.com and use its mortgage payoff calculator.3 An example is provided for you in Illustration 6.2. This is a man who decided to accelerate his payments and get rid of his mortgage sooner than he thought he could. Let’s call him “Morty.”

Illustration 6.2 Bankrate Early Mortgage Payoff Calculator

By adding $300 to his monthly payment, Morty shortened his repayment by nine years and four months. He got a whole decade of his life back!

In this example, Morty has just started his 30-year mortgage in the amount of $250,000. His APR, or annual interest rate, is 5.0 percent. His regular monthly scheduled payment is $1,342. If he adds $300 to that payment each month, he will shave 9 years and 4 months off the life of the loan. That will save Morty a grand total of $79,684—not too shabby.

You know when you’re working out and you don’t look at the clock, and so you “accidentally” run five extra minutes on the treadmill? You just burned a bunch of calories without even knowing it. That’s how it is with paying your mortgage. You simply have to forget about the sacrifice, and the good result will be headed your way.

Another option is setting up a payment structure whereby you pay 50 percent of the mortgage every two weeks rather than 100 percent once a month. By virtue of this schedule, you end up paying one extra monthly mortgage payment per year.

So, if your payment amounts to $2,000 per month and you opt for the two-week payment schedule, you’ll pay an extra $2,000 that year. It’s a good way to accelerate payments without feeling too much pain. Again, trick yourself into paying off your house sooner than you think you can.

In the real world, for every 10 happy retirees who have to pay off a mortgage, I’d venture to say 7 of those incorporate the methodology of paying $200 to $500 extra each month. The other three stick to the normally scheduled monthly amount and then do the final chunk at the end. They stay on track until the point at which they can handle paying more.

Money is relative to us all. What is painful to you might not be painful to the rich guy with the big house overlooking the ocean in Santa Barbara. (Or to Oprah, who lives next door to him.) Find what works for you.

Do What the Happy People Do

What I’m trying to do is pass on the secrets of very happy and successful retirees. Let me emphasize that not all are wealthy in the traditional sense. We’re not talking about multi-multimillionaires and billionaires—we’re talking about the happiest retirees.

You might like what I’m saying and you might not, but you can’t argue with the fact that these are behaviors and habits happy retirees have in common. I get my info from my clients, from people who call in to the radio show, and from the answers people gave me in the comprehensive survey I conducted. From all this, it’s clear a majority of these happy people no longer have mortgage payments.

Of course, it’s possible to be happy with a mortgage. But the percentage of possibility is lower, so why take the risk?

Back in 2009, the happiest retirees weren’t as affected by the financial crisis as the unhappy group—and their lack of a mortgage played a big part. In the midst of the financial crisis, with the economy in recession, there was a big fear about real estate, and a tremendous amount of underwater property. Too many people owned “too much house” and had too little equity. Debt was in abundance.

However, retirees in the happy group had a different financial forecast. They would come into my office and say “Oh, we just have one house, and it’s paid off.” Or, “We’ve got $30,000 to $50,000 left and then we’re done. We’re 55 years old and hoping to get this paid off in the next three or four years.”

I heard this over and over again. I thought I just had a funny coincidence on my hands, but it happened so many times that finally I couldn’t ignore it. I realized there had to be some kind of pattern here because these people were happy and comfortable with where they stood in life, despite the fact that we were right in the middle of the financial crisis—a very dark period in our nation’s economic history. The more I researched it, the more I couldn’t deny that paying off the mortgage really did give these people a cushion, offering them greater happiness and overall peace of mind.

Balancing IRA Money and Non-IRA Money in the Mortgage Payoff Game

Let’s say I owe $100,000 on my house. I have $500,000 in my IRA and $200,000 in my after-tax account. I can’t touch my IRA without getting punched in the face by taxes, so I’d be paying my mortgage out of the bucket with $200,000. Should I pay my mortgage or not?

The answer in this case is no. After I pay off the house, I’d only be left with $100,000 in my after-tax account. This means my liquidity is 50 percent less than it was. I don’t want to go into retirement with such a low amount of nonretirement money available to me. Yes, I have $500,000 in my IRA, but to access that money I have to pay taxes. Not fun, right? It gets worse.

You almost never want to take money out of a regular/traditional IRA to pay off a mortgage because every nickel you pull out of that IRA is considered taxable income. It might as well be income from a paycheck because it counts toward your adjustable gross income in the same way.

If I have to pull money out of the IRA to pay off a $100,000 mortgage and I’m in a 20 percent tax bracket, I’m going to end up having to pull $125,000 out to account for the taxes owed ($125,000 – 20% in taxes = $100,000). This is called an income and tax escalation phenomenon.

To net the $100,000 I needed, I had to pull out $125,000 to pay the mortgage, and the oh-so-friendly IRS is happy I did because not only is it taxable; it looks like more income and pushes me into an even higher tax bracket. Now I’m paying taxes on the money and paying a higher tax percentage overall. I got chewed up and spit back out. You can see why it’s so important not to take money out of the retirement fund to pay off the mortgage!

In order to avoid the real-life version of the hypothetical financial black eye I just gave myself, you have to remember to ask yourself this simple question:

Can I take one-third or less of my after tax money to pay off my mortgage?

If the answer is yes, do it.

If the answer is no, don’t. Instead, look at accelerating your monthly payments by a few hundred dollars a month like Morty illustrated in Illustration 6.2.

The Flexibility No Mortgage Affords

There are other important aspects to paying off the mortgage before retirement. First of all, you buy yourself some flexibility. If you need an equity line, you can get it. I’m not recommending a reverse mortgage, but you’d have the opportunity to use it if you had to. You’d also have the flexibility of being able to move somewhere else, rent, or even buy a place and not have to carry two mortgages.

The flexibility in your life skyrockets when you pay off your home. Not being financially beholden or burdened is so important. There’s a lot of utility in that.

Remember Marilyn Noble from Chapter 4? She’s a great example of someone with maximum flexibility. She was able to sell her house and use the money to buy two smaller houses. It’s amazing how much you can afford using the equity from a fully paid off home as you head into retirement. Wouldn’t you want that kind of flexibility? Here’s just a tiny taste of the things I’ve seen happy retirees transition into:

• A new, smaller home with less maintenance and lower utility bills

• A cabin in the mountains and a lakeside cottage

• A cabin in the mountains and a condo in town—a popular choice for those who can afford to avoid traffic in my hometown of Atlanta

• A condo on Lake Michigan and another in the steamy gulf of Florida

• A home near your grandchildren—and another one far away from your grandchildren, for when you need some time away

• An RV to travel across North America

• Enjoying vacations using the vacation rental by owner (VRBO system) described in the next section

Vacation Rentals by Owner: Enjoying a Second Home Without Having to Buy One

There are so many options for vacationing these days, and they allow more opportunity to give up that stressful mortgage payment. My favorite of these is VRBO—vacation rentals by owner, which also operates under the name homeaway.com (so both vrbo.com and homeaway.com will work for you). I’m also a fan of using airbnb.com as well, which also has a vast inventory of homes that you can rent in cities all around the world

Technology and efficiency have led to more affordable lodging and housing in highly valued areas. In today’s world, I’m not sure it’s necessary to have a second home. A lot of the happiest retirees still do, so it’s not a make-or-break situation, but if you want to shed the mortgage payment on that beach or mountain home, VRBO allows you to enjoy vacations without being tied to anything.

There are also vacation clubs, such as Inspirato, where joining allows you access to wonderful properties around the world. There are many options at varying price levels and with different incentive packages, but it’s safe to say that the much maligned and inflexible timeshare model has evolved to give vacationers more desirable options.

Following are five important things to understand when considering higher-end vacation clubs:

• By and large, they are not cheap. They typically involve a one-time, up-front cost of several thousand dollars to more than $15,000, and they can also entail annual membership fees. Make sure you have a list of all fees before giving over your hard-earned money.

• The properties you have to choose from are jaw dropping. If you’re feeling inspired, spend a few minutes on www.inspirato.com. They’re gorgeous!

• The daily cost can range from $500 to more than $1,500 per night—so the costs are jaw dropping, as well. Know that going in.

• Locations range from Aspen to St. Barts to Provence to Tuscany to Thailand to the Turks and Caicos Islands.

• These clubs are about access—the perfect setup for happy retirees who have a larger-than-normal travel budget and never want to be tied to one particular destination. Remember how I’m always saying retirement is freedom? Well, at these clubs, they’d agree.

Buy the “Big Stuff” Now, Before You Retire

Remember the overall concept that your mortgage is most likely your biggest expense—the biggest potential black hole for your finances. And don’t forget that in addition to the mortgage, there is a litany of expensive problems that can go wrong with your home, such as:

• A leaky skylight

• Holes in the roof

• Broken plumbing

• Broken heating or AC

• Warped floors

• An outdated kitchen that “just has to be redone”

• Foundation work (your house needs a new foundation)

All of these are big-ticket items. Your wallet cringes just thinking about them. It would take more than a trip to the local Target or Home Depot to take care of these; you’d have to dust off your yellow pages or get a referral from Kudzu.com to find yourself a handyman or carpenter. And if you think they’re inexpensive, allow me to burst your bubble—they aren’t. They have an amazing ability to turn a two-hour job into a two-day journey.

I recently had a handyman put in new front porch doors. Not only was there a half-inch gap underneath the door so that you could literally see outside, but when the workers painted they opted to sand the actual glass to remove stray paint splatters. Now I have four brand-new French doors with a gap big enough for a groundhog, and brand-new glass where 10 out of the 40 panes have permanent scratches.

So I went out and found a better handyman: Mr. Rex Gillman.

Rex happens to be one of the funniest individuals I’ve ever met, so in addition to his talent, he keeps me laughing. He is clad in overalls, and the rogue hairs on his half-bald head yearn for the comb-over from days of yore. If the nutty professor were tailgating at an SEC college football game, that would be Rex. He’s loaded with every southern proverb in the language. As Rex would put it, he’s got “one foot on the banana peel and the other foot in the grave.”

He’s a great handyman, but at $50 an hour, I think it’s me that has one foot on the banana peel and the other one in the grave. Yet, despite the painful bills I receive, I can handle it because I’m not yet retired. That’s the key.

I’ve had more than one retiree from the happy group tell me that their philosophy is to pay for all the “big stuff” before retirement so it doesn’t hit them when they retire. If this seems like common sense to you, that’s good! Unhappy retirees don’t get it. The bottom line is that if you want to enlist in the army of home repair, you might want to work an extra year and then retire once the deployment is over.

That way, you can have the means to pay off your mortgage on Monday and retire on Tuesday, just like good ol’ Henry and Ava Grand.

Whether you’re employing one of these early payoff strategies or a combination of them, you will be able to shave years or perhaps decades off the life of your mortgage. If these strategies get you mortgage-free in five years or less, you’re well on your way to retiring sooner than you think.