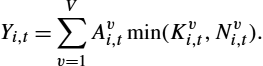

Agent-Based Macroeconomics✶

Herbert Dawid⁎,1; Domenico Delli Gatti†,‡ ⁎Department of Business Administration and Economics and Center for Mathematical Economics, Bielefeld University, Bielefeld, Germany

†Complexity Lab in Economics (CLE), Department of Economics and Finance, Università Cattolica del Sacro Cuore, Italy

‡CESifo Group Munich, Germany

1Corresponding author. email address: [email protected]

Abstract

This chapter surveys work dedicated to macroeconomic analysis using an agent-based modeling approach. After a short review of the origins and general characteristics of this approach a systemic comparison of the structure and modeling assumptions of a set of important (families of) agent-based macroeconomic models is provided. The comparison highlights substantial similarities between the different models, thereby identifying what could be considered an emerging common core of macroeconomic agent-based modeling. In the second part of the chapter agent-based macroeconomic research in different domains of economic policy is reviewed.

Keywords

Agent-based macroeconomics; Aggregation; Heterogeneity; Behavioral rules; Business fluctuations; Economic policy

1 Introduction

Starting from the early years of the availability of digital computers, the analysis of macroeconomic phenomena through the simulation of appropriate micro-founded models of the economy has been seen as a promising approach for Economic research. In an article in the American Economic Review in 1959 Herbert Simon argued that

“The very complexity that has made a theory of the decision-making process essential has made its construction exceedingly difficult. Most approaches have been piecemeal-now focused on the criteria of choice, now on conflict of interest, now on the formation of expectations. It seemed almost utopian to suppose that we could put together a model of adaptive man that would compare in completeness with the simple model of classical economic man. The sketchiness and incompleteness of the newer proposals has been urged as a compelling reason for clinging to the older theories, however inadequate they are admitted to be. The modern digital computer has changed the situation radically. It provides us with a tool of research—for formulating and testing theories—whose power is commensurate with the complexity of the phenomena we seek to understand. [...] As economics finds it more and more necessary to understand and explain disequilibrium as well as equilibrium, it will find an increasing use for this new tool and for communication with its sister sciences of psychology and sociology.” (Simon, 1959, p. 280).

This quote, which calls for an encompassing macroeconomic modeling approach building on the interaction of (heterogeneous) agents whose expectation formation and decision making processes are based on empirical and psychological insights, might be seen as the first formulation of a research agenda, which is now referred to as “Agent-Based Macroeconomics.” Cohen (1960) provides a very insightful discussion of the potential and the challenges of the use of computer simulations for the development of a behavioral theory of the firm, as well as for the analysis of aggregate economic models. An early example of an actual simulation-based macroeconomic model is the evolutionary model of economic growth discussed in Nelson and Winter (1974) and Nelson et al. (1976). In the 1970s micro-founded simulation models of the Swedish economy (the MOSES model, see Eliason, 1977, 1984) and the US economy (the “Transactions Model”, see Bergman, 1974; Bennett and Bergmann, 1986) have been developed as a tool for the analysis of certain economic policy measures. Although calibrated for specific countries, the structure of these models was rather general and as such they can be seen as very early agent-based macroeconomic models.

At the same time, starting in the 1970s the attention of the mainstream of macroeconomic research has shifted towards (dynamic) equilibrium models as a framework for macroeconomic studies and policy analyses. At least in their original form these models are built on assumptions of representative agents, rational expectations, and equilibrium based on inter-temporally optimal behavior of all agents. The clear conceptual basis, as well as the relatively parsimonious structure of these models, and the fact that they address the Lucas critique has strongly contributed to their appeal and has resulted in a large body of work dedicated to this approach. In particular, these models have become the workhorse for macroeconomic policy analysis.

Nevertheless, already early in this development different authors have pointed out numerous problematic aspects associated with using such models, in particular Dynamic Stochastic General Equilibrium (DSGE) models, for economic analysis and policy studies. Kirman (1992) nicely summarizes results, showing that in general aggregate behavior of a heterogeneous set of (optimizing) agents cannot be interpreted as the optimal decision of a representative agent and that, even in cases where it can, the sign of effects of policy changes on the utility of that representative agent might be different from the sign of the induced utility changes of all agents in the underlying population, which makes the interpretation of welfare analysis in representative agent models problematic. Furthermore, an extensive stream of literature has shown that under reasonable informational assumptions no adjustment processes ensuring general convergence to equilibrium can be constructed (see Kirman, 2016). Hence, the assumption of coordination of all agents in an equilibrium is very strong, even if a unique equilibrium exists, which in many classes of models is not guaranteed. As argued, e.g., in Howitt (2012) this assumption also avoids addressing coordination issues in the economy, which are essential for understanding the phenomena like the emergence of crises and also the impact of policies. Similarly, the assumption that all agents have rational expectations about the future dynamics of the economy has been criticized as being rather unrealistic, and indeed there is little experimental or empirical evidence suggesting that the evolution of expectations of agents is consistent with the rational expectations assumption (see, e.g., Carroll, 2003 or Hommes et al., 2005).

From a more technical perspective, studies in the DSGE literature typically rely on local approximations of the model dynamics around a steady state (e.g., log-linearization) and thereby do not capture the full global dynamics of the underlying model. This makes it problematic to properly capture global phenomena like regime changes or large fluctuations in such a framework. Business cycles and fluctuations are driven by shocks to fundamentals or expectations, whose structure is calibrated in a way to match empirical targets. Hence, the mechanisms actually generating these fluctuations are outside the scope of the model and therefore the model can only be used to study propagation of shocks, but is silent about which mechanisms generate such phenomena and which measures might reduce the risk of the emergence of cycles and downturns in the first place.

In the aftermath of the crises developing after 2007, policy makers, as well as economists, have acknowledged that several of the properties mentioned above substantially reduce the ability of standard DSGE models to inform policy makers about suitable responses to the unfolding economic downturn. New generations of DSGE-type models have been developed addressing several of these issues, in particular introducing more heterogeneity (see Ragot, 2018 in this handbook), heterogeneous non-rational expectations (see Branch and McGough, 2018 in this handbook) or the feedback between real and financial dynamics (e.g., Benes et al., 2014); however, also in each of these extensions several of the points discussed above, which seem intrinsic associated with this approach, still apply.1

Related to these new developments also a stream of literature has emerged, which, although relying on the backbone of a standard DSGE-type model, in certain parts of the model incorporates explicit micro-level representations of the (local) interaction of agents and relies on (agent-based) simulation of the emerging dynamics. Although these contributions (e.g., Anufriev et al., 2013; Arifovic et al., 2013; Assenza and Delli Gatti, 2013, 2017; Lengnick and Wohltmann, 2016) can be considered to be part of the agent-based macroeconomic literature, they are more hybrid in nature and this literature is treated in the chapter by Branch and McGough (2018) in this handbook, rather than in this chapter.2

The agent-based approach to macroeconomic modeling, which has started to attract increasing attention from the early 2000s onwards, is similar in spirit to Simon's quote above and hence differs in several ways from mainstream dynamic equilibrium models. In agent-based macroeconomic models, different types of heterogeneous agents endowed with behavioral and expectational rules interact through explicitly represented market protocols and meso- as well as macroeconomic variables are determined by actual aggregation of the output in this population of agents. They are mainly driven by the desire to provide empirically appealing representations of individual behavior and interaction patterns at the micro level and at the same time to validate the models by comparing the characteristics of their aggregate level output with empirical data. The global dynamics of the models are studied relying on (batches of) simulation runs and typically no ex-ante assumptions about the coordination of individual behavior are made.

Already early contributions to this stream of literature have shown that such models can endogenously generate fluctuations resembling actual business cycles without relying on external shocks (e.g., Dosi et al., 2006) and have highlighted, before the outbreak of the crises of 2007, mechanisms by which contagion (e.g., through credit networks) and feedback between the real and financial side of the economy can induce instability and sudden downturns (see Battiston et al., 2007). These properties, together with the ability to incorporate a wide range of behavioral assumptions and to represent institutional characteristics, which might be relevant for the analysis of actual policy proposals, have fostered interest of policy makers for agent-based macroeconomic modeling3 and resulted in a vast increase in research in this area in general, and in agent-based policy analysis in particular. As has to be expected from a new emerging paradigm, the evolution of the field has progressed in several weakly coordinated streams, and in light of the large body of work that has been produced so far, a systematic review of the progress that has been made seems to be in order. This chapter is an attempt to provide such a review.

1.1 Complexity and Macroeconomics

The notion of complexity is general enough to encompass a broad class of phenomena and models in nature and society. We interpret complexity as an attribute of a system. In particular, following the approach pioneered at the Santa Fe Institute by an interdisciplinary group of prominent scientists, complex adaptive systems (CAS) are systems consisting of a large number of “coupled elements the properties of which are modifiable as a result of environmental interactions. [...] In general complex adaptive systems are highly non-linear and are organized on many spatial and temporal scales” (cited from Cowan and Feldmann in Fontana, 2010, p. 173).

Macroeconomic dynamics are characterized by the interaction of a large number of heterogeneous individuals who take a plethora of decisions of different kinds to produce and exchange a large variety of goods, as well as information. These transactions are governed by institutional rules which might vary significantly between different regions, industries, time periods, and other contexts. Based on this, economic systems must certainly be seen as very complex adaptive systems. This makes it extremely challenging to develop appropriate models for studying economic systems and to derive any insights of general validity about the (future) dynamics of key economic variables or the effect of certain economic policy measures.

In order to study CAS, a natural tool is an Agent Based Model (ABM), i.e., a model in which a multitude of (heterogeneous) elements or objects interact with each other and the environment. The single most important feature of an ABM is the autonomy of the elements, i.e., the absence of a centralized (“top down”) coordinating or controlling mechanism. ABMs are, by construction, computationally intensive. The output of the model typically cannot be determined analytically but must be computed and consists of simulated time series. A key feature of CAS is that it often gives rise to emerging properties, i.e., stable, orderly aggregate structures resulting from the interaction of the agents' behavior. A phenomenon is emergent whenever the whole achieves properties which its elements, if taken in isolation, do not have.

1.2 The Agent-Based Approach to Macroeconomic Modeling

Agent-based Computational Economics (ACE) is the application of AB modeling to economics or: “The computational study of economic processes modeled as dynamic systems of interacting agents.” (Tesfatsion, 2006). Surveys of the ample literature on ACE work in different areas of Economics are provided in the second volume of the Handbook of Computational Economics (Tesfatsion and Judd, 2006). It is worthwhile noting that in this handbook no separate chapter on agent-based macroeconomics was included, which is a signal of the limited work in this area that has been completed before 2006.

A defining feature of macroeconomic ABMs (MABMs) is that although concerned with the dynamics of aggregate economic variables, such as GDP, consumption, etc., they explicitly capture the micro-level interaction of different types of heterogeneous economic agents and allow computing the aggregate variables “from the bottom up”, i.e., summing individual quantities across agents. The bottom-up approach to macroeconomics consists therefore in deducing the macroscopic patterns and phenomena in terms of a multitude of elementary microscopic objects (microeconomic variables) interacting according to certain rules and protocols.

Developing and using an MABM typically requires a number of steps:

- • Model Design and Theory:

- ∘ determine the type of agents included to be in the model (households, firms, banks, etc.);

- ∘ for each agent of each type define the set of decisions to be taken, the set of internal states (e.g., wealth, skills, savings, etc.), structure of each decision rule (inputs, how is decision made), the potential information exchange with other agents and the potential dynamic adjustment of internal states and decision rules; decide on the theoretical, empirical or experimental foundations on which these choices are based;

- ∘ define interaction protocols for all potential interactions.

- • Codification: translate the rules into computer code, do proper testing of the code (e.g., unit testing) to ensure proper implementation of the model.

- • Parameter Choice and Validation: estimate and calibrate the parameters; run simulations; analyze the emerging properties of the simulated data, both at the cross-sectional level (e.g., firms' size distribution) and at the macroeconomic level (GDP growth and fluctuations, inflation/unemployment trade-off); compare these properties with real world “stylized facts.”

- • Model Analysis: study the effects of changes in key model parameters (e.g., policy parameters) based on proper statistical analysis of the output of batch runs across different parameter settings; use micro-level simulation data to highlight the mechanisms responsible for the observed findings and to foster economic intuition for the findings.

Several properties are common to MABMs and have been encountered in many agent-based models in Economics, among them several of the models reviewed in this chapter. First and foremost, in MABMs GDP tends to self-organize towards a growth path with endogenously generated fluctuations, such that business cycles are driven by the mechanics of the model rather than by properties of exogenous shocks. Furthermore, these models typically generate persistent heterogeneity of agents, giving rise to stable population distributions of firm size, productivity, profitability, growth rate or household income and thereby can reproduce also empirical patterns with respect to distributions of such variables. In particular, distributions with fat tails, which are observed for many real world variables (see, e.g., Axtell, 2018 in this handbook), have been reproduced in many instances by MABMs. Being able to jointly reproduce empirical stylized facts with respect to time series properties and distributional properties at different levels of aggregation is certainly a very appealing feature of MABMs, which is hard to obtain in the framework of alternative macroeconomic modeling approaches.

Many MABMs are characterized by externalities and nonlinearities (due to interaction), which generate dynamic processes with positive feedbacks. Due to the presence of such feedbacks path dependencies might arise such that initial conditions or random events in the transient phase can have decisive impact on the long run dynamics. These properties of MABMs are also the basis for endogenously generating extreme events, like crashes and economic crises, as well as fast transitions between different quasi-stable regimes. MABMs capture the actual dynamic mechanisms generating such potential fast economic transitions and therefore are natural tools to study how to prevent or mollify economic crises, e.g., through appropriate institutional designs or policy measures. Generally speaking, the fact that agent-based models allow for global analysis of macroeconomic dynamics in frameworks which endogenously generate dynamic and cross-sectoral patterns, which closely resemble empirical data, arguably is a main reason for the appeal of this approach.

1.3 Behavior, Expectations, and Interaction Protocols

In dynamic equilibrium models, individual behavior is typically determined by the optimal solution of some (dynamic) optimization problem an agent with rational expectations faces. Quite differently, in agent-based macroeconomic models it is not assumed that the economy is in equilibrium and that individuals have rational expectations. Hence, the agents in the model, similarly to real-world decision makers, are “necessarily limited to locally constructive actions, that is, to actions constrained by their interaction networks, information, beliefs, and physical states.” (Sinitskaya and Tesfatsion, 2015, p. 152). The design of behavioral rules determining such locally constructive actions is a crucial aspect of developing an agent-based macroeconomic model. The lack of an accepted precise common conceptual or axiomatic basis for the modeling of bounded rational behavior has raised concerns about the “wilderness of bounded rationality” (Sims, 1980); however, agent-based modelers have become increasingly aware of this issue, providing different foundations for their approaches to model individual behavior.

Generally speaking, in many MABMs the design of the behavioral rules builds on the extensive psychological and empirical literature showing the prevalence of relatively simple heuristics and rules of thumb for making decisions, including economic decisions in complex environments (see, e.g., Gigerenzer and Gaissmaier, 2011; Artinger and Gigerenzer, 2016). Such rules might be derived from optimization within the framework of a simplified internal model of the surrounding environment, or might evolve over time based on adjustment dynamics that take into account which types of rules generate desirable results for the decision maker.4 In a number of agent-based models the chosen behavioral rules are strongly motivated by experimental5 or empirical observations of how actual decision makers behave in certain types of decision problems.6 As will become clear in our survey below, the literature shows substantial heterogeneity with respect to the approach that underlies the design of the behavioral rules. Similar statements apply to the expectation formation of agents. The absence of the assumption of rational expectations typically gives rise to models with evolving heterogeneous expectations and also in this domain different approaches have been followed.

Given the heterogeneity in the way decision making and expectation formation are modeled, it would be desirable to have a clear understanding of how robust results obtained in the framework of a certain model are with respect to the use of alternative plausible behavioral rules. A step in this direction is taken by Sinitskaya and Tesfatsion (2015), who compare in a simple macroeconomic framework how key outcomes of the model compare across settings with different types of decision rules; however, in particular in large macroeconomic models such robustness tests are not feasible and the chosen design of the behavioral rules might therefore be an important determinant of the model output.

In most macroeconomic agent-based models the interaction of the different agents in markets or other interaction structures are governed by explicit protocols that represent the institutional design of the considered economic system. This allows capturing details of the institutional setting and also allows representing in a natural way potential rationing of both market sides, as well as the occurrence of frictions in a market. The degree of detail with which the interactions structures in different markets are described, of course, varies substantially across the agent-based macroeconomic models that have been developed and is strongly influenced by the main focus of the model.

1.4 Outline of the Chapter

In this chapter we discuss the main developments in Agent-Based Macroeconomics during the last decade. The treatment is essentially split into two parts. In the first part, consisting of Sections 2 and 3, we focus on the design of macroeconomic agent-based models. In particular, in Section 2 we address in some detail several main challenges of macroeconomic agent-based modeling, in particular the design of the behavioral rules of different types of agents for several of the most crucial decisions to be taken. We illustrate how these challenges were treated in eight macroeconomic agent-based models that have been well perceived in the literature. In Section 3, we provide more of a bird's-eye view on these model by summarizing the detailed discussion of Section 2 and providing a systematic comparison of these eight MABMs along a larger number of modeling dimensions. Section 3 also contains a discussion of the way these models have been linked to empirical data. The discussion in Section 3 is based on Tables A1 and A2, provided in Appendix A, in which a short summary of the main features of all eight models is given. Overall, we hope that Sections 2 and 3 of the chapter do not only provide a survey of the literature, but are also helpful in identifying what could be considered a common core of macroeconomic agent-based modeling. The second part of the chapter, essentially Section 4, provides an overview of macroeconomic policy analyses that have been carried out using agent-based models. Although the eight models discussed in Sections 2 and 3 are the basis for a considerable fraction of this policy oriented work, numerous studies reviewed in Section 4 do not fall into this category. This highlights the breadth of work in agent-based macroeconomics during the last years and the fact that a chapter like this, due to space constraints, cannot properly capture the full status of the literature. The chapter concludes with some remarks about challenges for the future development of this line of research and about areas in which, in our opinion, the potential for agent-based analysis is particularly high.

2 Design of Agent-Based Macroeconomic Models

2.1 Families of MABMs

Macroeconomic Agent-Based Models (MABMs) can be classified according to different criteria. First of all, we can distinguish between large, medium sized, and small MABMs.

Medium sized and large MABMs feature at least three agent types – households, firms, and banks – interacting at least on five markets: consumption goods (C-goods hereafter), capital or investment goods (K-goods), labor, credit, deposits. Small MABMs generally feature just two types of agents – households and firms – interacting on two markets: C-goods and labor.

Some MABMs are able to replicate growth, i.e., a long-run exponential trend around which actual GDP irregularly fluctuates, some other focus only on the short run, i.e., they can replicate only business fluctuations.

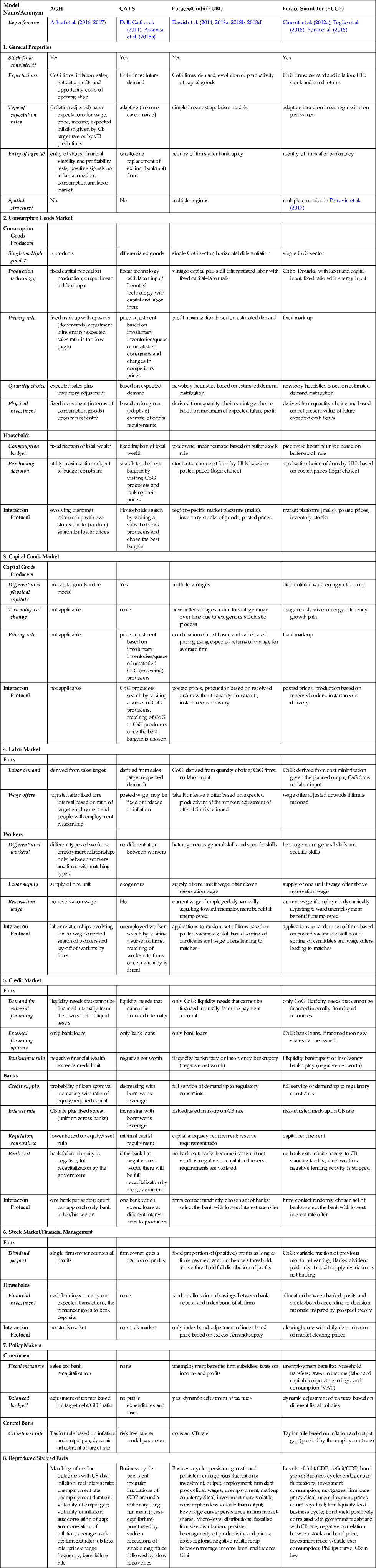

In this section and the next, we will focus on medium-sized MABMs, grouping them into seven families:

- 1. The framework developed by Ashraf, Gershman, and Howitt (AGH hereafter)7;

- 2. The family of models proposed by Delli Gatti, Gallegati, and coauthors in Ancona and Milan exploiting the notion of Complex Adaptive Trivial Systems (CATS)8;

- 3. The framework developed by Dawid and coauthors in Bielefeld as an offspring of the EURACE project,9 known as Eurace@Unibi (EUBI)10;

- 4. The EURACE framework maintained by Cincotti and coauthors in Genoa (EUGE)11;

- 5. The Java Agent based MacroEconomic Laboratory developed by Salle and Seppecher (JAMEL)12;

- 6. The family of models developed by Dosi, Fagiolo, Roventini, and coauthors in Pisa, known as the “Keynes meeting Schumpeter” framework (KS)13;

- 7. The LAGOM model developed by Jaeger and coauthors.14

We will also present the relatively simple small model developed by Lengnick (LEN) for comparison.15 Key references for these models are given in Tables A1 and A2.

By selecting these eight families of models, on the one hand, we tried to pick those that seem to have had the strongest impact on the literature and have been used as the basis for interesting economic analyses and policy experiments, and, on the other hand, also present some variety to show the range of approaches that have been developed to deal with the challenges of agent-based macroeconomic modeling. Clearly, any such selection is highly subjective and, as will also become clear in the discussion of agent-based policy analyses in Section 4, the selection made here misses a substantial number of important contributions to this area. Nevertheless, we believe that presenting such a survey is not only useful for newcomers to the field, but also helps to provide transparency about the status of the field of agent-based macroeconomics. Due to the rather complex structure of many models in this field, which often makes a full model description rather lengthy, such transparency is not easy to obtain.

The interested reader who ventures for the first time into this literature may feel the excitement of exploring a new world and, at the same time, the disorientation and discouragement of getting lost in the wilderness. At first sight, in fact, these models look very different from one another so that it's extremely difficult for the beginner to “see the forest” above and beyond a wide variety of trees. In our opinion, however, there are common denominators, both in the basic architecture of the models and in the underlying theory of the way in which agents form behavioral rules and interact on markets.

2.2 A Map of this Section

Let us set the stage by considering the architecture of an MABM. The economy is populated, at a minimum, by households and firms (as in LEN). Medium-sized MABMs are populated also by banks.

Households supply labor and demand C-goods. In most MABMs, households are “surplus units”, i.e., net savers. Savings are used to accumulate financial wealth.

The corporate sector consists, at a minimum, of producers of C-goods (C-firms). Most MABMs, however, are now incorporating also producers of K-goods (K-firms). C-firms demand labor and K-goods in order to produce and sell C-goods to households. K-firms supply K-goods to C-firms.

In most MABMs firms are “deficit units”, i.e., firms' internal funds may not be sufficient to finance costs. Therefore they resort to external finance to fill the financing gap. In most MABMs, external finance coincides with bank loans. Banks receive deposits from households and extend loans to firms.

In small MABMs, such as LEN, there are markets for C-goods and labor. In medium-sized MABMs, there are typically markets for C-goods, K-goods, labor, credit, and deposits.16 Given this architecture, we can allocate agents in markets according to the grid shown in Table 1. Each column of the table represents a group of agents, each row a market. For instance, H/C/d represents Households acting on the market for C-goods on the side of demand.

Table 1

H stands for households; F denotes firms; B stands for banks; N denotes the labor market; L denotes the market for loans; and A denotes the market for assets

| Households | Firms | Banks | |

|---|---|---|---|

| C-goods | H/C/d | F/C/s | |

| K-goods | F/K/d,s | ||

| Labor | H/N/s | F/N/d | |

| Credit | F/L/d | B/L/s | |

| Assets | H/A/d | F/A/s |

Instead of reviewing the models one after another, in each of the following subsections we will discuss the characterizations that the proponents of different MABMs adopt to describe the behavioral rules that each type of agent (on the columns) follows in each of the different markets the agent is active (on the rows). We will also devote some space to the description of the interaction of buyers and sellers on markets (market protocols) which Tesfatsion labels “procurement process.”17

We aim at bringing to the fore the similarities among different MABMs. As mentioned above, assumptions and modeling choices come from a variety of sources, first and foremost from the empirical and experimental evidence. It is worth noting, moreover, that these assumptions have a varying degree of kinship with the current macroeconomic literature. MABMs are not developed in a vacuum, the shapes of their building blocks come also from the theoretical debate in macroeconomics. For this reason, at the beginning of each subsection, we will succinctly present the microeconomic backbone of a standard New Keynesian DSGE (NK-DSGE) model (the standard model hereafter) pertaining to that class of agents,18 then present the behavioral rules and market protocols of MABMs concerning the same class. In this way we can discuss similarities and differences (i) between the standard model and the MABMs, and (ii) among MABMs. In order to make the comparison easier, we will adopt our own notation, which will be uniform across different MABMs. We will also slightly simplify the analytical apparatus of a specific MABM under review to make the modeling choices starker in the eyes of the reader. Notice finally that we will consider each MABM as the result of a collective effort (with the exception of LEN). Hence we will conjugate a verb describing the action of the group behind the label of each MABM in the third person plural. To foster readability, we provide in Appendix B a list of symbols with their meaning that are used in this section.

In our presentation of MABMs, due to space limitations, we will not discuss three relevant features.

The first concerns the sequence of events, which may differ from one model to another. By construction, MABMs are recursive sequential models. Agents decide on the desired level of their choice variables (planned level) following behavioral rules and then enter markets one after another in order to implement those decisions by suitable transactions. Search of trading opportunities and matching of supply and demand occur in fully decentralized markets, i.e., in the absence of a top-down mechanism to enforce equilibrium. Therefore, transactions typically occur at prices which do not clear the market. This may cause a disruption of plans, which must be revised accordingly.

Consider, for instance, a C-firm. Once the quantity to be produced has been established, the firm determines desired employment. If desired employment is greater than the current workforce, the firm tries to hire new workers by posting vacancies. It may not be able to fill the vacancies, however, because not enough workers will visit the firm or accept the position.19 In this case, the firm has to downsize its production plans. Generally, due to unexploited trading opportunities, three constraints may limit the implementation of decisions, e.g., firms may be unable to (i) find enough external funds to fill the financing gap and/or (ii) hire enough workers and/or (iii) acquire enough capital to implement the desired level of production.

The second feature concerns time discretization. By construction, in MABMs time is discrete. MABMs can differ, however, as far as the minimal time unit is considered (a day, a week, a month, a quarter). Moreover, transactions can occur at different time scales. For instance, in LEN C-goods are traded every day but labor services are traded on a monthly basis. In the following, for simplicity we will not be specific on the time unit which will be referred to with the generic term “a period.”

The third feature concerns the characterization of interaction. A few MABMs are networked, i.e., they have an explicit network structure: agents are linked by means of trading relationships which take the form of persistent partnerships. In LEN, for instance, each household trades with a finite set of firms.20 Most of the MABMs we will consider below, however, do not assume a fixed network of trading relationships. Partners in a trade today may not trade again tomorrow. In a sense, trading relationships de facto connect people in a network which is systematically reshuffled every period.21

2.3 Households

In the following, we will consider a population of H households. Variables pertaining to the hth household will be denoted with the suffix h. Households may be active or inactive on the labor market. If active, they supply labor (in most MABMs, labor supply is exogenous). In some MABMs, households searching the labor market have a reservation wage, which may be constant or decreasing with the length of the unemployment spell. If employed, the household earns a wage. In some MABMs, if unemployed, the household receives an unemployment subsidy, which amounts to a fraction of the wage of employed households.

Households are also firm owners. Firm ownership may be limited to a fraction of inactive households or spread somehow also to active households. As a firm owner, the household receives dividends. Current income is the sum of the wage bill and dividends. Households purchase C-goods. Generally, households are surplus units, i.e., they do not get into debt. Unspent income is saved and generates financial wealth. In most MABMs, financial wealth consists of bank deposits only.

In LEN, households are linked in a network of trading relationships to a finite set of firms from which they buy C-goods and firms for which they work. Since there are no banks, households hold wealth in liquid form (money holding).

In AGH, each household (“person”) is denoted by the type (i,j)![]() where i is the household's labor/product type and j are the types of goods the household wants to consume. By assumption the household consumes only two goods, different from the good it can produce. The product type is isomorphic to the labor type.22 A household of type i can be a worker if employed by a firm (“shop”) of the same type. If a worker, she earns a wage. Otherwise, the household can be a firm owner.

where i is the household's labor/product type and j are the types of goods the household wants to consume. By assumption the household consumes only two goods, different from the good it can produce. The product type is isomorphic to the labor type.22 A household of type i can be a worker if employed by a firm (“shop”) of the same type. If a worker, she earns a wage. Otherwise, the household can be a firm owner.

In the CATS framework, households can be either workers or “capitalists.” Workers supply labor, earn a wage (if employed), consume, and save. Capitalists are the owners of firms. For simplicity there is one capitalist per firm. Capitalists earn dividends (if the firm is profitable), consume, and save (therefore they behave as rentiers). Both workers and capitalists accumulate their savings in the form of deposits at banks. If the firm goes bankrupt, the owner of the bankrupt firm employs his personal wealth to provide equity to the entrant firm. In other words, the capitalist is de facto recapitalizing the defaulting firm to make it survive.

In KS, EUBI, EUGE, and LAGOM, each household supplies labor and owns firms at the same time. This alternative approach poses the problem of attributing ownership rights, dividends, and recapitalization commitments to heterogeneous households. For instance, in EUBI, the household holds financial wealth in the form of deposits at banks and an index of stocks which define property rights and the distribution of dividends.

In JAMEL, some of the households (chosen at random) are firm owners and remain firm owners for a certain time period (typically a run of a simulation).

2.3.1 The Demand for Consumption Goods

In this section we will first recall the basic tenets of the standard model of household's consumption/saving decisions, which we will refer to as the Life Cycle/Permanent Income (LCPI) benchmark. We will then present the most general specification of the consumption behavioral rule which we can extract from the MABM literature. The specific behavioral rules adopted by different MABMs can be conceived as special cases of this general specification.

The Life Cycle/Permanent Income Benchmark

The standard approach to households' behavior (incorporated in NK-DSGE models) is based on “two-stage budgeting.” In the first stage, the representative infinitely lived household maximizes expected lifetime utility subject to the intertemporal budget constraint, determining the optimal size of consumption expenditure Ch,t![]() , which we will sometimes refer to hereafter as the consumption budget.

, which we will sometimes refer to hereafter as the consumption budget.

In the second stage the household determines the composition of Ch,t![]() , i.e., the fraction Ci,h,t/Ch,t

, i.e., the fraction Ci,h,t/Ch,t![]() for each variety i=1,2,…,Fc

for each variety i=1,2,…,Fc![]() where Fc

where Fc![]() is the cardinality of the set of C-goods (and of C-firms).23

is the cardinality of the set of C-goods (and of C-firms).23

As far as the first stage is concerned, optimal consumption turns out to be a function of expected future consumption EtCh,t+1![]() and the real interest rate r (consumption Euler equation).

and the real interest rate r (consumption Euler equation).

Notice now that consumption expenditure is equal by definition to permanent income, Ch,t=Yph,t![]() . Hence, after some algebra, we get

. Hence, after some algebra, we get

(1) Ch,t=ˆr(Whh,t+Wfh,t)

where ˆr=ˆR−1![]() is the (net, real) interest rate, Whh,t

is the (net, real) interest rate, Whh,t![]() is human capital, and Wfh,t

is human capital, and Wfh,t![]() is financial wealth. Eq. (1) can be interpreted as a benchmark Life Cycle/Permanent Income (LCPI) consumption function. In this framework, by construction, the consumption budget is equal to the annuity value of total (financial and human) wealth.

is financial wealth. Eq. (1) can be interpreted as a benchmark Life Cycle/Permanent Income (LCPI) consumption function. In this framework, by construction, the consumption budget is equal to the annuity value of total (financial and human) wealth.

Human capital, in turn, is defined as the discounted sum of current income and expected future incomes accruing to the household:

(2) Whh,t=1ˆR∞∑s=0(1ˆR)sEtYh,t+s=1ˆRYh,t+1ˆR∞∑s=1(1ˆR)sEtYh,t+s.

Substituting (2) into (1), the LCPI consumption function becomes

(3) Ch,t=ˆrˆRYh,t+ˆrˆR∞∑s=1(1ˆR)sEtYh,t+s+rWfh,t.

In words, consumption is a linear function of current and expected future incomes and of financial wealth.

By definition, in the LCPI benchmark, Wfh,t+1=ˆRWfh,t+Yh,t−Ch,t![]() . Therefore savings, i.e., the change in financial wealth Sh,t=Wfh,t+1−Wfh,t

. Therefore savings, i.e., the change in financial wealth Sh,t=Wfh,t+1−Wfh,t![]() , turns out to be equal to Sh,t=ˆrWfh,t+Yh,t−Ch,t

, turns out to be equal to Sh,t=ˆrWfh,t+Yh,t−Ch,t![]() . Since consumption is equal to permanent income, savings can be specified as follows:

. Since consumption is equal to permanent income, savings can be specified as follows:

(4) Sh,t=ˆrWfh,t+(Yh,t−Yph,t)

where the expression in parentheses is transitory income. All the income in excess of permanent income will be saved and added to financial wealth. If, on the other hand, current income falls short of permanent income, the household will stabilize consumption by decumulating financial wealth.

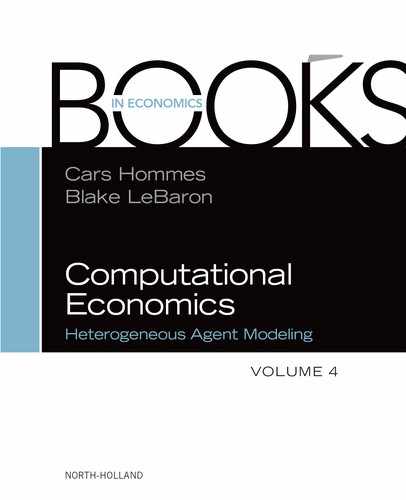

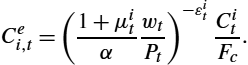

As far as the second stage is concerned, it is easy to show that in a Dixit–Stiglitz framework the (optimal) fraction of each good in the bundle is

(5) Ci,h,tCh,t=(Pi,tPt)−ε

where Pi,t![]() is the price of the ith variety, Pt

is the price of the ith variety, Pt![]() is the general price level,24 and ε is the absolute value of the price elasticity of demand. In words, the fraction of the consumption budget allocated to each variety is a decreasing function of the relative price Pi,tPt

is the general price level,24 and ε is the absolute value of the price elasticity of demand. In words, the fraction of the consumption budget allocated to each variety is a decreasing function of the relative price Pi,tPt![]() .

.

Generally, households are assumed to be identical. If household members are heterogeneous (for instance, because of the employment status, or the level and the source of income), in standard models complete markets are assumed so that idiosyncratic risk can always be insured. Within the household, “full consumption insurance” follows from the assumption that household members pool together their incomes (wages, unemployment subsidies, dividends) and consume the same amount in the same proportions. Thanks to this assumption, heterogeneity, albeit present, is irrelevant because the household may still be dealt with as a unique (representative) agent. If idiosyncratic income risk is uninsurable, then heterogeneity cannot be assumed away.25

The Agent Based Approach to Consumption/Saving Decisions

A two stage procedure is also generally adopted in MABMs. In the first stage household h determines the consumption budget Ch,t![]() , i.e., the amount of resources (income, wealth) to be allocated to consumption expenditure. In the second stage the household determines the composition of the bundle of consumption goods, i.e., the quantities Ci,h,t

, i.e., the amount of resources (income, wealth) to be allocated to consumption expenditure. In the second stage the household determines the composition of the bundle of consumption goods, i.e., the quantities Ci,h,t![]() , i=1,2,…,Fc

, i=1,2,…,Fc![]() of the goods which enter the consumption bundle. Notice, however, that in general agents do not follow explicit optimization procedures. Markets are generally incomplete and within-household consumption insurance is ruled out.

of the goods which enter the consumption bundle. Notice, however, that in general agents do not follow explicit optimization procedures. Markets are generally incomplete and within-household consumption insurance is ruled out.

The Choice of the Consumption Budget

As far as the first stage is concerned, the most general behavioral rule adopted to set the consumption budget in the MABM literature can be specified as follows:

(6) Ch,t=chWhh,t+cfWfh,t

where Wfh,t![]() is the household's financial wealth (deposited at the bank and/or invested in financial assets), Whh,t

is the household's financial wealth (deposited at the bank and/or invested in financial assets), Whh,t![]() is human capital, ch

is human capital, ch![]() and cf

and cf![]() are propensities to consume, both positive and smaller than one. In words, consumption is a linear function of human and financial wealth.

are propensities to consume, both positive and smaller than one. In words, consumption is a linear function of human and financial wealth.

By definition, Wfh,t=ˆRWfh,t−1+Yh,t−Ch,t![]() and Sh,t=Wfh,t−Wfh,t−1

and Sh,t=Wfh,t−Wfh,t−1![]() . Consumption is defined as in (6). Hence, in a generic MABM savings turn out to be

. Consumption is defined as in (6). Hence, in a generic MABM savings turn out to be

(7) Sh,t=Yh,t+(ˆr−cf)Wfh,t−1−chWhh,t.

If positive, savings increase financial wealth. In some MABMs saving can be involuntary: it may happen that the household cannot find enough consumption goods at the limited number of firms it visits. Savings will turn negative, i.e., the household will decumulate financial wealth, if the consumer does not receive income, for instance, because a worker becomes unemployed and/or financial income (interest payments on financial wealth) is too low. In most MABMs, household do not get into debt so that consumption smoothing is limited or absent (in the jargon of NK-DSGE models, asset market participation is limited).

Specifications of the general rule (6) differ from one MABM to another.

AGH set ch=cf=c![]() . Moreover, they define human capital as the capitalized value of permanent income Whh,t=khYph,t

. Moreover, they define human capital as the capitalized value of permanent income Whh,t=khYph,t![]() where kh

where kh![]() is a capitalization factor.26 Permanent income Yph,t

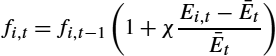

is a capitalization factor.26 Permanent income Yph,t![]() is computed by means of an adaptive algorithm, Yph,t−Yph,t−1=(1−ξ)(Yh,t−1−Yph,t−1)

is computed by means of an adaptive algorithm, Yph,t−Yph,t−1=(1−ξ)(Yh,t−1−Yph,t−1)![]() where ξ∈(0,1)

where ξ∈(0,1)![]() is a memory parameter. By iterating, it is easy to see that permanent income (and therefore human capital) turns out to be a weighted sum of past incomes only, Yph,t=(1−ξ)∑−∞s=0ξsYh,t−s−1

is a memory parameter. By iterating, it is easy to see that permanent income (and therefore human capital) turns out to be a weighted sum of past incomes only, Yph,t=(1−ξ)∑−∞s=0ξsYh,t−s−1![]() . Hence the AGH behavioral rule for consumption expenditure is

. Hence the AGH behavioral rule for consumption expenditure is

(8) Ch,t=ckh(1−ξ)−∞∑s=0ξsYh,t−s−1+cWfh,t.

In words, consumption is a linear function of past incomes and financial wealth.

In the CATS/ADG framework, human capital is defined by the following adaptive algorithm: Whh,t=ξWhh,t−1+(1−ξ)Yh,t![]() . By iterating, one gets Whh,t=(1−ξ)Yh,t+(1−ξ)∑−∞s=1ξsYh,t−s

. By iterating, one gets Whh,t=(1−ξ)Yh,t+(1−ξ)∑−∞s=1ξsYh,t−s![]() , i.e., human capital is a weighted average of current and past incomes.27 Substituting this definition into (6), the behavioral rule specializes to

, i.e., human capital is a weighted average of current and past incomes.27 Substituting this definition into (6), the behavioral rule specializes to

(9) Ch,t=ch(1−ξ)Yh,t+ch(1−ξ)−∞∑s=1ξsYh,t−s+cfWfh,t.

While human capital in the neoclassical approach is a linear combination of current and expected future incomes, and therefore is formed in a forward looking way, the proxy for human capital in AGH and CATS/ADG is a linear combination of current and past incomes, i.e., it is determined by a backward looking algorithm.28

Setting ξ=0![]() , i.e., assuming that there is no memory, human capital boils down to current income, so that (9) specializes to

, i.e., assuming that there is no memory, human capital boils down to current income, so that (9) specializes to

(10) Ch,t=cyYh,t+cfWfh,t

where cy![]() is the propensity to consume out of income.29

is the propensity to consume out of income.29

Setting cf=0![]() , from (10) we get a specification of the consumption function sometimes adopted in MABMs of a strictly Keynesian flavor

, from (10) we get a specification of the consumption function sometimes adopted in MABMs of a strictly Keynesian flavor

(11)

In many models of the KS family, the behavioral rule is (11) with ![]() :

:

(12)

This specification describes the behavior of “hand-to-mouth” consumers.30

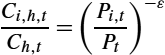

LAGOM adopts a rule such as (10) with ![]() . Moreover, since financial wealth coincides with money holding (

. Moreover, since financial wealth coincides with money holding (![]() ), the consumption budget turns out to be an increasing linear function of real money balances31

), the consumption budget turns out to be an increasing linear function of real money balances31

(13)

In CATS/DD, consumption is a special case of (10) obtained by setting ![]() . Therefore

. Therefore

(14)

The expression in parentheses is one of the possible specifications of “cash-on-hand”, which can be defined in the most general way as liquid assets which can be used to carry on transactions. In small MABMs which do not feature banks such as LEN, cash-on-hand coincides with currency. In a setting with banks such as CATS/DD, cash-on-hand coincides with new deposits, which in turn amount to the sum of income and old deposits. This is in line with Deaton (1991), who defines cash-on-hand as the sum of income and financial assets.

In EUBI and EUGE, saving behavior aims at achieving a target for wealth, namely ![]() where

where ![]() is the target wealth-to-income ratio and ν is the velocity of adjustment of wealth to targeted wealth. Since by definition

is the target wealth-to-income ratio and ν is the velocity of adjustment of wealth to targeted wealth. Since by definition ![]() , simple algebra shows that under this assumption the consumption budget can be written as

, simple algebra shows that under this assumption the consumption budget can be written as

(15)

which is a special case of (10) with ![]() and

and ![]() .

.

Carroll has shown that in an uncertain world consumption is a concave function of cash-on-hand which he defines as the sum of human capital and beginning of period wealth.32 In Carroll's framework, for low values of wealth, the propensity to consume (out of wealth) is high due to the precautionary motive: a reduction of wealth would in fact lead to a sizable reduction of consumption to rebuild wealth (buffer stock rule). In some MABMs the consumption function is adjusted to mimic Carroll's precautionary motive, i.e., to reproduce the nonlinearity of the relationship between consumption and wealth. This theoretical setting has been corroborated by a number of empirical studies (see Carroll and Summers, 1991; Carroll, 1997), such that using this approach in MABMs is consistent with the agenda to rely on behavioral rules which have strong empirical foundations.

For instance, in EUBI the specification of the consumption function discussed above gives rise to a piecewise linear heuristic based on the buffer-stock rule. Also EUGE adopt a specification of the consumption budget which adopts Carroll's rule.

In the CATS/MBU framework, consumption is specified as in (11) but ![]() is a nonlinear function of wealth. This allows capturing the interaction between income and wealth in the determination of consumption.

is a nonlinear function of wealth. This allows capturing the interaction between income and wealth in the determination of consumption.

LEN explicitly models the consumption budget as an increasing concave function of money holdings by

(16)

where ![]() .33

.33

JAMEL presents a variant of Carroll's framework. The household computes “average income” (which can be considered a proxy of permanent income) as the mean of incomes received over a certain time span occurred in the past, ![]() .34 Moreover, JAMEL define desired or targeted cash on hand as a fraction of average income,

.34 Moreover, JAMEL define desired or targeted cash on hand as a fraction of average income, ![]() , where

, where ![]() are real money balances and

are real money balances and ![]() is the desired propensity to save (out of average income). The consumption budget is defined as follows:

is the desired propensity to save (out of average income). The consumption budget is defined as follows:

(17)

where ![]() and

and ![]() is the propensity to consume. In words, if liquid assets are (relatively) “low”, the household spends a fraction c of average income. If liquidity is “high”, the household consumes the entire average income and a fraction

is the propensity to consume. In words, if liquid assets are (relatively) “low”, the household spends a fraction c of average income. If liquidity is “high”, the household consumes the entire average income and a fraction ![]() of excess money balances, defined as the difference between the current and targeted money holding.

of excess money balances, defined as the difference between the current and targeted money holding.

With the help of some algebra, the behavioral rule above can be written as follows:

(18)

where ![]() is the cut-off value of average income and

is the cut-off value of average income and ![]() . Notice that

. Notice that ![]() . The cut-off value of average income is a multiple of current money holdings. The specification above highlights the basic tenets of Carroll's buffer stock theory in a very simple piecewise linear setting. When average income is below the threshold, i.e., when the threshold is relatively high because the household is wealthy/liquid, the marginal propensity to consume is

. The cut-off value of average income is a multiple of current money holdings. The specification above highlights the basic tenets of Carroll's buffer stock theory in a very simple piecewise linear setting. When average income is below the threshold, i.e., when the threshold is relatively high because the household is wealthy/liquid, the marginal propensity to consume is ![]() , i.e., it is relatively high. When average income surpasses the threshold, the marginal propensity drops to c.

, i.e., it is relatively high. When average income surpasses the threshold, the marginal propensity drops to c.

JAMEL also incorporates consumer sentiment and opinion dynamics in the consumption function. The propensity to save, s, can take on two values. When “optimistic”, the household is characterized by ![]() while if “pessimistic” it sets s to

while if “pessimistic” it sets s to ![]() , with

, with ![]() . Pessimism leads to a reduction of the propensity to consume: households save more for rainy days.

. Pessimism leads to a reduction of the propensity to consume: households save more for rainy days.

Each household switches from a low to a high propensity to save (and vice versa) depending on its employment status. The household turns pessimistic if unemployed. In each period, the household observes the consumer sentiment (proxied by the employment status) of a finite subset of other households (a neighborhood, for short). With probability ![]() it adopts the majority opinion, i.e., the prevailing consumer sentiment, of the neighborhood; with probability

it adopts the majority opinion, i.e., the prevailing consumer sentiment, of the neighborhood; with probability ![]() the household relies on its own situation: if it is unemployed (employed), it will be pessimistic (optimistic) and will choose

the household relies on its own situation: if it is unemployed (employed), it will be pessimistic (optimistic) and will choose ![]() (

(![]() ). The probability of adopting the sentiment of the majority can be interpreted as the strength of the households' “animal spirits.”

). The probability of adopting the sentiment of the majority can be interpreted as the strength of the households' “animal spirits.”

The Choice of the Goods to Buy

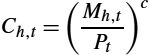

As to the second stage, the choice of the goods to buy is generally influenced by the relative price. EUBI and EUGE introduce a multinomial logit model, CATS posit a search mechanism.

In LEN each household is linked to a fixed number of firms from which it can buy. The network can change over time. Each period, with a certain probability, the household chooses at random a firm in the neighborhood of current trading partners and a firm outside it, compares the prices, and switches to the new firm if the price of the price set by the current partner exceeds the price of the new firm by at least a certain margin. In the end, therefore, the household searches for better trading opportunities based on relative price.35

AGH posit that the household can buy only from two firms (“stores”, i.e., shops where the household purchases its consumption goods). Hence it has to choose the quantity to be demanded from each firm. AGH derives behavioral rules by solving a simple optimization problem. The household maximizes ![]() subject to

subject to ![]() where

where ![]() ,

, ![]() . Hence the quantity demanded for each variety turns out to be

. Hence the quantity demanded for each variety turns out to be

(19)

which can be easily compared with (22). The household explores the goods market looking for stores supplying the goods it wants to consume. The household buys from store j only if the posted price ![]() is smaller than a reservation price equal to the price paid by the household in the past

is smaller than a reservation price equal to the price paid by the household in the past ![]() (appropriately indexed):

(appropriately indexed): ![]() where

where ![]() is expected inflation, anchored to the inflation target of the central bank.36

is expected inflation, anchored to the inflation target of the central bank.36

In the CATS framework, households collect information and pick goods by visiting firms chosen at random. The hth household visits ![]() randomly selected firms, ranks them according to the price they charge and purchases C-goods starting from the firm charging the lowest price. If it does not spend the entire consumption budget at the first firm, it will move up to the second firm in the ranking, and so on. If it has not spent all the consumption budget after visiting

randomly selected firms, ranks them according to the price they charge and purchases C-goods starting from the firm charging the lowest price. If it does not spend the entire consumption budget at the first firm, it will move up to the second firm in the ranking, and so on. If it has not spent all the consumption budget after visiting ![]() firms, it will save involuntarily. This implies that the demand for the good produced by the ith C-firm is implicitly decreasing with the relative price

firms, it will save involuntarily. This implies that the demand for the good produced by the ith C-firm is implicitly decreasing with the relative price ![]() . Notice, however, that the implicit demand curve that the ith firm is facing is shifting over time. A given firm may be visited by different sets of consumers on subsequent days. The search and matching mechanism leads to the coexistence of queues of unsatisfied consumers (involuntary savers) at some firms and involuntary inventories of unsold goods at some other firms.

. Notice, however, that the implicit demand curve that the ith firm is facing is shifting over time. A given firm may be visited by different sets of consumers on subsequent days. The search and matching mechanism leads to the coexistence of queues of unsatisfied consumers (involuntary savers) at some firms and involuntary inventories of unsold goods at some other firms.

LAGOM adopts a similar market protocol as CATS for the market for C-goods. In the LAGOM model also firms enter the market for C-goods as they use circulating capital together with fixed capital for production.

EUBI and EUGE assume that the consumer receives information about the range of products, their prices, and their availability at (local) malls. The choice of the good to buy is random and the probability of buying a certain product is determined by a multinomial logit model:

(20)

where the sum in the denominator includes all products for which the consumer has received information.37 As has been discussed in Dawid et al. (2018d), this formulation can also be interpreted as a representation of a situation in which the product offered by the different C-firms are horizontally differentiated along dimensions not explicitly captured in the model. The parameter γ governs the intensity of (price) competition between the C-firms and typically has strong influence on the emerging economic dynamics on the aggregate level. Dawid et al. (2018d) also point out that the use of logit-choice models for the representation of consumer choice has strong empirical foundations, e.g., in the Marketing literature.38

2.3.2 Labor Supply

On the labor market, households are suppliers of labor. The hth worker supplies inelastically one unit of labor.

LEN assumes that each household has a reservation wage, denoted with ![]() . It supplies its labor only to a finite subset of the population of firms, a neighborhood of potential employers. However, the network can be rewired. If the household is employed, say, at firm i, and its current wage is higher than the reservation wage (

. It supplies its labor only to a finite subset of the population of firms, a neighborhood of potential employers. However, the network can be rewired. If the household is employed, say, at firm i, and its current wage is higher than the reservation wage (![]() ), it will search for a better position infrequently, i.e., with probability less than one. When searching, it will visit only one new firm chosen at random. If at this new firm, say j, it finds

), it will search for a better position infrequently, i.e., with probability less than one. When searching, it will visit only one new firm chosen at random. If at this new firm, say j, it finds ![]() , so it will quit the current job and move to the jth firm. If, for any reasons, its current wage falls below the reservation wage (

, so it will quit the current job and move to the jth firm. If, for any reasons, its current wage falls below the reservation wage (![]() ),39 it will intensify the quest for a better position by exploring a new firm every period (i.e., with certainty). If the household is unemployed, it will search for a job every period by visiting a fixed number

),39 it will intensify the quest for a better position by exploring a new firm every period (i.e., with certainty). If the household is unemployed, it will search for a job every period by visiting a fixed number ![]() of firms chosen at random. If the household switches to a new employer, the former employer drops out of the set of employers of the households and is replaced by the new one.

of firms chosen at random. If the household switches to a new employer, the former employer drops out of the set of employers of the households and is replaced by the new one.

Also in LAGOM each household has a reservation wage. If the household is employed, say, at firm i, and its current wage is lower than the reservation wage (![]() ), so it will quit the job and search for a better position at a finite set of firms chosen at random.

), so it will quit the job and search for a better position at a finite set of firms chosen at random.

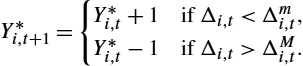

In AGH, as we saw above, a household type is defined by the production good it can produce with its labor type. If employed, the household is working in the same firm which produces its production good. If unemployed, the household engages in job search with a given probability ![]() . It explores the labor market looking for a firm (with the same product type) posting a vacancy. The household accepts the job offer if the previous wage

. It explores the labor market looking for a firm (with the same product type) posting a vacancy. The household accepts the job offer if the previous wage ![]() (appropriately indexed) is smaller than the posted wage

(appropriately indexed) is smaller than the posted wage ![]() , i.e., if

, i.e., if ![]() .

.

In CATS/MBU and CATS/ADG, the hth household, if unemployed, looks for a job by visiting ![]() firms chosen at random and applying to those with open vacancies. In CATS/MBU the posted wage is firm-specific and cannot drop below a lower bound represented by a minimum wage, which is changing over time due to indexation. The unemployed worker will accept a job from the firm with open vacancies which pays the highest wage. For simplicity in CATS/ADG the posted wage is given and is uniform across firms so that the unemployed worker accepts the job at the first chance of finding an open vacancy. If it doesn't find an open vacancy, the household remains unemployed and funds consumption by dissaving, i.e., consuming out of accumulated wealth. For simplicity CATS assume that there are neither hiring nor firing costs. If a firm wants to scale down activity in a certain period, it can fire workers at no cost. Fired workers become unemployed and start searching for a job in the same period.

firms chosen at random and applying to those with open vacancies. In CATS/MBU the posted wage is firm-specific and cannot drop below a lower bound represented by a minimum wage, which is changing over time due to indexation. The unemployed worker will accept a job from the firm with open vacancies which pays the highest wage. For simplicity in CATS/ADG the posted wage is given and is uniform across firms so that the unemployed worker accepts the job at the first chance of finding an open vacancy. If it doesn't find an open vacancy, the household remains unemployed and funds consumption by dissaving, i.e., consuming out of accumulated wealth. For simplicity CATS assume that there are neither hiring nor firing costs. If a firm wants to scale down activity in a certain period, it can fire workers at no cost. Fired workers become unemployed and start searching for a job in the same period.

In EUBI the household is characterized by a specific skill and has a reservation wage. If unemployed, it explores the labor market with a given probability. Firms post vacancies and wages. The unemployed household ranks the wage offers and applies only to firms that make a wage offer (for the worker's skill group) which is higher than its reservation wage. If the unemployed job searcher receives several acceptable job offers he/she accepts the offer with the highest wage. The reservation wage of the worker is adjusted downwards during periods of unemployment.

In JAMEL the household's reservation wage is stochastically reduced if the unemployment spell is greater than an exogenous upper bound. In symbols,

(21)

where ![]() is a random draw from a uniform distribution,

is a random draw from a uniform distribution, ![]() is the duration of the unemployment spell and

is the duration of the unemployment spell and ![]() is the threshold value of this spell.

is the threshold value of this spell.

2.3.3 The Demand for Financial Assets

In a small MABM such as LEN, households can hold wealth only in the most liquid form (cash). Most medium-sized MABMs assume that there is at least one other financial asset such as deposits at banks. For CATS, KS, JAMEL, and LAGOM, households' wealth consists only of deposits. In AGH, households can hold cash, deposits, and government bonds. In EUBI and EUGE the household can hold wealth as liquidity (deposits at banks), as a portfolio of shares issued by firms and banks, and in EUGE also as government bonds. Households therefore receive dividends according to the composition of their portfolio of shares. For simplicity, in EUBI the allocation of households' savings to bank deposits and shares is random. Modeling the portfolio choice for each household, however, may be quite complex. For instance, the preference structure of “investors” in EUGE, i.e., households trading in financial markets, takes into account insights from behavioral finance, namely myopic loss aversion. Transactions on financial markets occur at higher frequency than on real markets (daily as against monthly). Prices are determined in equilibrium through a clearinghouse mechanism. In CATS households can be of two types, workers and capitalists. Assuming that there is one capitalist per firm, each firm distributes part of its profits to the firm owner as dividends. KS adopt the extreme assumption that all the profits are retained within the firm and used to accumulate net worth. In this case, by assumption there will be no dividends. In JAMEL some households (chosen at random) are firm owners and therefore receive dividends which will be distributed only if the firm's net worth is higher than a threshold (defined by a target level for leverage). Opinion dynamics play a role in dividend distribution. Firms switch from “optimistic” (characterized by high target leverage and high dividends) to “pessimistic” (low target leverage and low dividends). Also in LAGOM households are firm owners and receive both wages and dividends.

2.4 Firms

In this section we will consider a population of F firms, which produce either consumption goods (C-firms) or capital goods (K-firms). Variables pertaining to the ith C-firm will be denoted with the index ![]() . Variables pertaining to the kth K-firm will be denoted with the index

. Variables pertaining to the kth K-firm will be denoted with the index ![]() . In most MABMs, C-firms demand labor and K-goods in order to produce and sell C-goods to households; K-firms demand labor in order to produce and sell K-goods to C-firms.40

. In most MABMs, C-firms demand labor and K-goods in order to produce and sell C-goods to households; K-firms demand labor in order to produce and sell K-goods to C-firms.40

Firms have market power, hence they set the quantity and the price of the goods they produce and sell. Generally, market power is rooted in transaction costs. Due to uncertainty and the costs of exploring market conditions, in fact, buyers do not have enough information on the prices and quantities set by all the sellers so that they purchase goods from a limited set of suppliers. Each supplier, therefore, operates in condition of monopolistic competition or oligopoly on the market for its own good.

The planned (or desired) scale of activity is the main determinant of the demand for inputs, namely the demand for capital and the demand for labor.

On the market for K-goods, demand comes from C-firms and supply comes from K-firms. The ith C-firm's demand for K-goods, i.e. investment, is driven mainly by production requirements. If production planned at period t for period ![]() can be carried out with the capital stock inherited from the past (after depreciation), the firm simply adjusts capacity utilization. If capital inherited from the past is insufficient to undertake planned production, the ith firm should expand capacity by purchasing new K-goods (sometimes referred to as “machine tools”). In some MABMs, this is feasible. In other MABMs, investment at period t is driven by long-run production requirements and cannot be used to face short-run peaks of demand. Hence the firm will be constrained to produce at full capacity but less than desired.

can be carried out with the capital stock inherited from the past (after depreciation), the firm simply adjusts capacity utilization. If capital inherited from the past is insufficient to undertake planned production, the ith firm should expand capacity by purchasing new K-goods (sometimes referred to as “machine tools”). In some MABMs, this is feasible. In other MABMs, investment at period t is driven by long-run production requirements and cannot be used to face short-run peaks of demand. Hence the firm will be constrained to produce at full capacity but less than desired.

On the market for labor, demand comes from all the firms and supply comes from households. Firms whose workforce is insufficient to undertake planned production will post vacancies and a wage offer (which may be firm-specific or uniform across firms, constant or time-varying because of indexation and/or because of labor market conditions.)

Firms may have a financing gap, i.e., a positive difference between operating costs and internally generated funds. They generally ask for a loan to fill this gap. The quantity and price of credit are set by banks.

Firms may be unable to achieve the desired scale of activity for lack of funds (if they are rationed on the credit market), of capital (if investment is disconnected from short-run production need and/or if they don't find enough machine tools to buy) or of labor (if they don't find enough workers to hire).

2.4.1 The Supply of Consumption Goods

The Dixit–Stiglitz Benchmark

As far as the corporate sector is concerned, NK DSGE models are based on monopolistic competition: each firm behaves as a monopolist on its own market. The firm's market power is due to product heterogeneity. Products may be different in the eyes of consumers for a number of reasons: spatial dispersion, product differentiation, or transaction costs which may generate captive markets.

In the Dixit–Stiglitz benchmark, the demand of the hth household for the ith good is represented by Eq. (5). Summing across H households and rearranging, one gets the demand function for the ith good:

(22)

where ![]() is total consumption (economywide).41

is total consumption (economywide).41

With a linear technology and only the labor input, the marginal cost will be ![]() where

where ![]() is the wage and α is the marginal productivity of labor. Optimal pricing yields

is the wage and α is the marginal productivity of labor. Optimal pricing yields

(23)

where ![]() is the mark-up.

is the mark-up.

Substituting (23) into (22), one gets the optimal scale of production

(24)

Since the manager of the firm knows the production function and input costs, and therefore can compute the marginal cost, if she knows also the demand curve she will choose an optimal mark-up (i.e., ratio of the individual price to marginal cost) and an optimal scale of activity. In other words, in the absence of uncertainty on market demand, the firm will choose a point on the demand curve in such a way as to maximize profits. In this case supply will always be equal to demand: the firm will neither accumulate involuntary inventories of unsold goods nor face queues of unsatisfied consumers; output will always be sold and no potential customer will leave the firm's premises empty handed.

Moreover, in the absence of frictions on the labor market, the firm will always be able to carry out planned production. In the end therefore, planned output will be equal to actual output and actual output will be equal to sales.

From (23) and (24) we can predict the following: the firm will react to (i) an increase of elasticity of demand by reducing the mark up and therefore the individual price and increasing production; (ii) an increase of the real wage by increasing the price and reducing production; (iii) an increase in productivity by reducing the price and increasing production; (iv) an increase in total consumption by increasing production.

Since firms have the same technology, incur the same labor cost, and face the same demand function, a symmetric equilibrium in which all firms charge the same price, is considered: ![]() , so that the real wage will be equal to

, so that the real wage will be equal to ![]() . At that wage, employment is determined by labor supply, the labor market clears, and there is full employment.42 Total output is equal to the full employment level of GDP.43 In the absence of investment, output is equal to consumption. Each firm therefore will produce the same quantity, i.e., a fraction

. At that wage, employment is determined by labor supply, the labor market clears, and there is full employment.42 Total output is equal to the full employment level of GDP.43 In the absence of investment, output is equal to consumption. Each firm therefore will produce the same quantity, i.e., a fraction ![]() of total consumption, which is equal to total full employment output. In the presence of nominal rigidities (e.g., Calvo pricing), this level of output is unattainable, at least in the short run.

of total consumption, which is equal to total full employment output. In the presence of nominal rigidities (e.g., Calvo pricing), this level of output is unattainable, at least in the short run.

Price/Quantity Decisions when Demand Is Unknown

In order to understand the price/quantity strategies of firms in MABMs and compare them with firms' decisions in the standard model, in this “intermezzo” we will keep the basic structure of the Dixit–Stiglitz framework, but will relax the assumption of perfect information as far as market demand is concerned. We will assume instead that, at the moment decisions on price and quantity must be made, the firm does not know the position of the demand curve on the price/quantity space.

Uncertainty on market demand may be due to the fact that transactions do not occur at the same time on all markets. There is a sequence of events which take place at different times on different markets. For instance, we can envisage the following 4 steps: (1) At the beginning of period t (before the market for C-goods opens), the firm decides the price and the quantity. On the basis of the production plan, it decides whether to hire or fire workers. Suppose the workforce must be expanded to fulfill the production plan. (2) The firm enters the labor market by posting vacancies at a certain wage. These vacancies may or may not be filled depending on the number of matches between demand (job offers) and supply (unemployed workers) of labor. Suppose all the vacancies are filled. (3) The firm can therefore implement the desired production plan. (4) The quantity produced is then sold on the market of C-goods. Production must be decided in step (1) but actual demand will be revealed to the firm only in step (4).