Heterogeneous Expectations and Micro-Foundations in Macroeconomics✶

William A. Branch⁎,1; Bruce McGough† ⁎University of California, Irvine, CA, United States

†University of Oregon, Eugene, OR, United States

1Corresponding author. email address: [email protected]

Abstract

This chapter provides an overview of recent models of heterogeneous expectations in macroeconomics. We begin with a description of household behavior in an environment with features common to many models in asset pricing, monetary theory, and New Keynesian macroeconomics. We demonstrate issues facing modelers when agents are boundedly rational and have (possibly) heterogeneous beliefs about the future evolution of endogenous state variables. These issues can be summed up in three broad categories: boundedly rational decision making, aggregation of decision rules, and the appropriate equilibrium concept. After having laid out the basic underlying theories we present several applications that illustrate the non-trivial implications of heterogeneous expectations for economic outcomes. Our applications include asset-pricing and bubbles, trading inefficiencies in monetary economies, and monetary policy design.

Keywords

Heterogeneous expectations; DSGE models; Bounded rationality; Asset pricing; Monetary theory; Monetary policy

1 Introduction

Modern macroeconomic models are built on micro-foundations: households and firms are dynamic optimizers in uncertain environments who interact in markets that clear in general equilibrium. Because decision-making is intertemporal, and the future is uncertain, macroeconomic models impart an important role to households' and firms' expectations about future states of the economy. Despite the importance of expectations, the benchmark approach is to assume homogeneous rational expectations, where all agents in the economy hold similar and correct views about the dynamic evolution of economic variables. Even in models of adaptive learning, e.g. Evans and Honkapohja (2001), individuals and firms are typically assumed to forecast using the same econometric model.

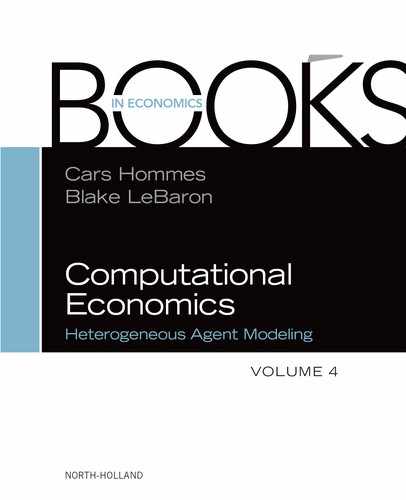

Nevertheless, there is substantial empirical and experimental evidence that individuals and firms have heterogeneous expectations. For example, Fig. 1 plots the interquartile range from individual inflation probability forecasts published by the Survey of Professional Forecasters (SPF) over the period 1992.1–2010.4. The IQR gives a good measure of the range of views in the SPF. The left plot is the histogram of the IQR in the sample, while the right plot is the time-series of the median IQR in each quarterly survey. Evidently, there is substantial heterogeneity among professional forecasters and, importantly, the degree of heterogeneity evolves over time.

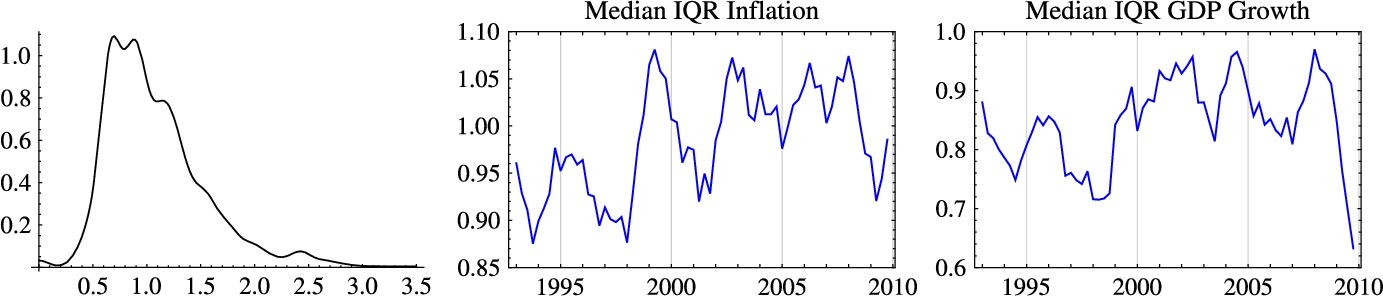

Fig. 2 plots an estimated time-series of likely forecasting methods used by respondents in the Michigan Survey of Consumers' inflation expectation series. This figure comes from Branch (2004) who estimates a model of expectation formation where households select from a set of standard statistical forecasting models, each differing in complexity and parsimony, in such a way that people favor predictors with lower forecast errors net of complexity costs. In this figure, and a substantial body of other research, there is strong evidence of time-varying expectational heterogeneity. Finally, in a series of learning-to-forecast experiments, Hommes (2013) shows strong evidence of heterogeneous expectations even in simple, controlled laboratory environments.1

A burgeoning literature studies the implications of heterogeneous expectations for dynamic, stochastic, general equilibrium (DSGE) models. This literature, motivated by these empirical facts, introduce agents with different beliefs into micro-founded models. This step of bringing bounded rationality into models with micro-foundations brings certain challenges to modelers. In particular, we begin with a discussion of the following three key questions about how to model heterogeneous beliefs in DSGE models:

- 1. How to model individual behavior given the available forecasting models?

- 2. Given a distribution of individuals across forecasting models, how are endogenous variables determined?

- 3. How are individuals distributed across forecasting models?

To address these questions we adopt a stylized DSGE environment that nests benchmark models in monetary theory, asset-pricing, and New Keynesian business cycles. The framework, which is outlined in Section 2.2, is a simplified version of Rocheteau and Wright (2011) which combines the New Monetarist monetary model with search frictions by Lagos and Wright (2005) with a Lucas asset-pricing model. By turning the search frictions off, the model reduces to a standard asset-pricing model. If we set the dividend flow to zero, the model is isomorphic to a pure monetary economy. This simple framework is able to demonstrate many of the important implications of heterogeneous expectations for the macroeconomy and asset-pricing.

We then turn to address the first question, namely, how to model the decision making of boundedly rational agents. A substantial segment of the literature follows a reduced-form approach, where the conditional expectations in the equations derived under rational expectations are replaced with a convex combination of heterogeneous expectations operators. More recently, the frontier of the adaptive learning literature adopts an “agent-level” approach that takes as given a set of behavioral primitives for individual decision-making. These behavioral primitives are based on two observations. First, agents who make boundedly rational forecasts may also make boundedly optimal decisions. Second, aggregation into equilibrium equations should follow a temporary equilibrium approach where aggregation occurs after imposing boundedly rational decision-making. The literature has proposed a variety of behavioral primitives, some based on anticipated utility maximization and others based on internal rationality. In Section 2.3 we review these approaches while discussing strengths and drawbacks of each alternative.

The link between individual decisions and aggregate outcomes is provided by temporary equilibrium: individual-level decision rules and the distribution of agents across forecasting rules are coordinated through market clearing. With properly specified forecasting rules, this leads to a temporary equilibrium law of motion that can be written entirely in terms of aggregate state variables. Section 2.4 briefly discusses this analysis in the context of our simple environment, and also discusses some potential impediments.

Our analysis is complete by specifying how the distribution of agents across forecasting models is determined as an equilibrium object. Most of the literature follows the seminal Brock and Hommes (1997) by modeling expectation formation as agents rationally choosing a predictor from a finite set of forecasting models. That is, expectation formation is a discrete choice in a random utility setting, where the distribution of agents across models is given by a multinomial logit (MNL) mapping. There have been two ways in which agents might not have rational expectations and select heterogeneous predictors. The first, called rationally heterogeneous expectations, is when rational expectations is available to agents, as well as other predictors such as adaptive and naive expectations, but they must pay a higher cost to do so. This cost is meant to proxy for computational and cognitive costs in forming rational expectations. If the utility associated with predictor choice is subject to an idiosyncratic preference shock, then heterogeneous beliefs can arise as an equilibrium object of the model. The second approach, based on Branch and Evans (2006), rules out that agents are able to form rational expectations and instead they must select from a set of parsimonious forecasting models. Branch and Evans (2006) define a Misspecification Equilibrium as occurring when individuals only select the best performing models from a restricted set.2 Of course, which models are best performing is an equilibrium property and we demonstrate a variety of environments where Intrinsic Heterogeneity can arise.

Having laid out the key theoretical issues with incorporating, and deriving, heterogeneous expectations, the rest of the chapter focuses on applications. Section 4 focuses on asset-pricing applications. Here we show that asset-pricing models with heterogeneous expectations are able to explain key empirical regularities such as bubbles/crashes, regime-switching returns and volatilities, and excess volatility. We then, in Section 5, turn to a pure monetary economy and show how heterogeneous beliefs can alter the nature of trade in economies with over-the-counter frictions. An important result here is that trading between agents with heterogeneous beliefs must also specify higher-order beliefs and these may lead to a failure for buyers and sellers to successfully execute a trade. That is, there can be an extensive margin of trade that arises from heterogeneous expectations. However, these higher order beliefs also induce people to make more cautious offers, hoping to avoid times when their offers are rejected, and so affect the intensive margin of trade as well. We show that heterogeneous expectations can have important welfare implications and can also explain puzzling experimental results.

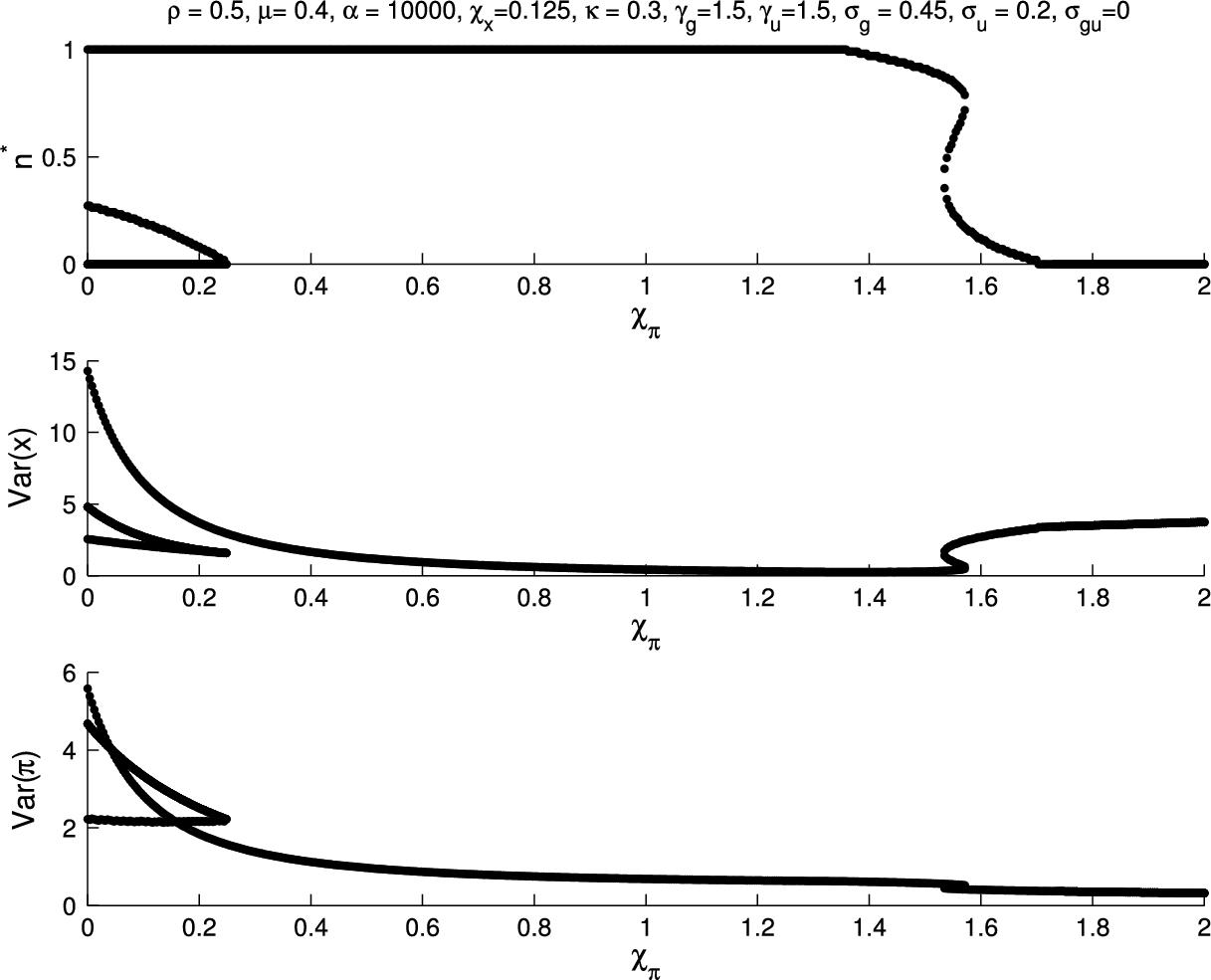

We then extend the basic framework to the New Keynesian model. Here we show how a basic property of heterogeneous expectations models, “stability reversal,” can have important implications for the design of monetary policy. A general principle of heterogeneous expectations is the tension between forward-looking rational expectations and backward-looking adaptive expectations and learning models. Homogeneous rational expectations models that are determinate (dynamically unstable) can be indeterminate (dynamically stable) with homogeneous adaptive expectations: adaptive beliefs can reverse the stability properties of rational expectations models. Thus, there is a tension between the repelling and attracting forces inherent to heterogeneous expectations. Brock and Hommes (1997) demonstrated, with masterful force, how these attracting/repelling forces can lead to periodic and complex dynamics. An important factor for the existence of complex belief dynamics is the self-referential property of the model, and, in New Keynesian models the policy rule followed by the central bank can alter the strength of expectational feedback. We demonstrate how a policy designed to adhere to the Taylor principle under rational expectations can destabilize an economy with even just a small amount of steady-state equilibrium fraction of adaptive agents. We also show that policy rules can affect that steady-state equilibrium fraction and potentially lead to hysteresis effects for plausibly strong inflation reaction coefficients in Taylor-type rules. Finally, we show how heterogeneous expectations can lead to multiple stable equilibria including the possibility of recurring collapses to a (stable under learning) liquidity trap.

This chapter proceeds as follows. Section 2 defines the notion of an expectations operator, introduces the model, and discusses the micro-foundations and aggregation of heterogeneous beliefs. Section 3 introduces the two types of equilibria considered in this chapter: rationally heterogeneous expectations and misspecification equilibria. The stability reversal principle is introduced in this section. Section 4 presents applications to asset-pricing models, while Section 5 focuses on pure monetary economies. Section 6 presents results for DSGE models.

2 Expectations Operators and Bounded Rationality

In macroeconomic models, economic agents make decisions in dynamic, uncertain environments and, thereby, confront two related, but conceptually distinct, issues: how to make forecasts given the available information; and, how to make decisions given the available forecasts. The rational expectations hypothesis joins these two aspects of agent-level behavior through the cross-equation restrictions imposed by the equilibrium, i.e. optimal forecasts depend on actions and optimal actions depend on forecasts. This chapter focuses on bounded rationality and heterogeneous expectations, an environment where the strict nature of the link is broken, and the agents' forecasting and decision-making problems may be treated separately. Before discussing the forecasting problem, the ways in which heterogeneous beliefs can arise in equilibrium, and the resulting applications, we begin with a review of boundedly rational decision-making.

In order to motivate an equilibrium with heterogeneous expectations, we follow the adaptive learning literature that has recently turned towards a more careful modeling of the decision-making process made by individuals given that forecasts are not fully rational. This “agent-level approach” is distinguished from reduced-form learning – where the conditional expectations in the equilibrium equations derived under rational expectations are replaced with a heterogeneous expectations operator – in two important ways: first, it is reasonable to assume that agents who make boundedly rational forecasts may also make boundedly optimal decisions; and second, aggregation into equilibrium equations should take place after boundedly-rational behavior has been imposed. The first point, the possibility of boundedly optimal decision-making, requires that we take a stand on – i.e. specify behavioral primitives governing – how agents make decisions given their forecasts; and the second point, concerning the aggregation of boundedly rational behavior, demands a temporary equilibrium approach. This section reviews several approaches pursued in the literature and shows how to aggregate the agent-level decision rules.

2.1 Expectations Operators

The literature on heterogeneous expectation formation is influenced, in part, by the adaptive learning literature (e.g. Evans and Honkapohja, 2001). In this class of models, fully rational expectations are replaced by linear forecasting rules with parameters that are updated by recursive least squares. In this chapter, we imagine different sets of agents who engage in economic forecasting while recognizing there may exist heterogeneity in forecasting rules. Some examples of heterogeneity consistent with our framework include the following: some agents may be rational while others adaptive, as has been examined in a cobweb model by Brock and Hommes (1997) and found empirically relevant in the data in Branch (2004); agents may have different information sets (e.g. Branch, 2007); or, they may use structurally different learning rules as in Honkapohja and Mitra (2006). Our goal is to extend this notion of agents as forecasters to the agents' primitive problem, and to characterize a set of admissible beliefs that facilitates aggregation.

Denote by ˆEτt![]() a (subjective) expectations operator; that is, ˆEτt(xt+k)

a (subjective) expectations operator; that is, ˆEτt(xt+k)![]() is the time t expectation of xt+k

is the time t expectation of xt+k![]() formed by an agent of type τ. We require that

formed by an agent of type τ. We require that

- A1. Expectations operators fix observables.

- A2. If x is a variable forecasted by agents and has steady state ˉx

then ˆEτˉx=ˉx

then ˆEτˉx=ˉx .

. - A3. If x, y, x+y

and αx are variables forecasted by agents then ˆEτt(x+y)=ˆEτt(x)+ˆEτt(y)

and αx are variables forecasted by agents then ˆEτt(x+y)=ˆEτt(x)+ˆEτt(y) and ˆEτt(αx)=αˆEτt(x)

and ˆEτt(αx)=αˆEτt(x) .

. - A4. If for all k≥0

, xt+k

, xt+k and ∑kβt+kxt+k

and ∑kβt+kxt+k are forecasted by agents then

are forecasted by agents then

ˆEτt(∑k≥0βt+kxt+k)=∑k≥0βt+kˆEτt(xt+k).

- A5. ˆEτt

satisfies the law of iterated expectations (L.I.E.): If x is a variable forecasted by agents at time t and time t+k

satisfies the law of iterated expectations (L.I.E.): If x is a variable forecasted by agents at time t and time t+k then ˆEτt∘ˆEτt+k(x)=ˆEτt(x)

then ˆEτt∘ˆEτt+k(x)=ˆEτt(x) .

.

These assumptions impose regularity conditions consistent with the literature on bounded rationality and they facilitate aggregation in a linear, or linearized environment. Assumption A1 is consistent with reasonable specifications of agent behavior (the forecast of a known quantity should be the known quantity). Assumption A2 requires some continuity in beliefs in the sense that, in a steady state, agents' beliefs will coincide. Assumptions A3 and A4 require expectations to possess some linearity properties. Essentially, linear expectations require agents to incorporate some economic structure into their forecasting model rather than, say, mechanically applying a lag operator to every random variable.

Assumptions A5 restricts agents' expectations so that they satisfy the law of iterated expectations at an individual level. The L.I.E. at the individual level is a reasonable and intuitive assumption: agents should not expect to systematically alter their expectations. In deriving the New Keynesian IS curve, with heterogeneous expectations, Branch and McGough (2009) imposed an additional assumption of the L.I.E. at the aggregate level, essentially ruling out higher order beliefs. In other applications, such as the New Monetarist search model, we explicitly model higher-order beliefs by assuming that an expectation operator consists of two components, a point estimate given by Eτt![]() and an uncertainty measure Fτt(⋅,Σ)

and an uncertainty measure Fτt(⋅,Σ)![]() .

.

2.2 The Economic Environment

Before turning to a discussion of bounded optimality and aggregation of heterogeneous expectations, it is useful to describe a general economic environment that forms the basis for many of the applications in this chapter. The environment is based on a Lucas (1978) asset-pricing model with consumption risk in the form of a frictional goods market characterized by bilateral trading and a limited commitment problem. By opening and closing the frictional market we are able to nest a standard asset-pricing model or a search-based New Monetarist type model, depending on the desired application. We turn to a brief description of the environment, and then develop the analysis as the chapter progresses.

Time is discrete, and each time period is divided into two sub-periods. There are two types of non-storable goods: specialized goods, denoted q, that are produced and consumed in a market that opens during the first sub-period (“DM”); and general goods, denoted x, that are produced and consumed in a competitive market (“CM”) during the second sub-period. There are two types of agents: “buyers” and “sellers”. All agents produce the general good using the same technology that is linear in labor. We assume that labor is traded in the competitive market at a real wage of wt![]() , which, in equilibrium, will equal the real wage in terms of the numeraire good. When we develop results for a standard Lucas asset-pricing model, we assume a perfectly inelastic labor supply so that the model reduces, essentially, to an endowment economy. Thus, the competitive market represents the part of the environment that is standard in macro DSGE models like the New Keynesian model or the Lucas asset-pricing model. In the specialized goods market, though, buyers can consume but not produce the specialized good while sellers can produce but cannot consume. Moreover, trade in these markets is characterized by a limited commitment friction where buyers are unable to commit to repay unsecured debt using their proceeds from producing in the competitive market. Thus, this part of the model captures environments with frictional goods markets where assets such as fiat money, stocks or bonds are used as payment instruments. Some of the most interesting, and recent, applications of heterogeneous expectations occur in such markets. We assume that with probability σ buyers will have preferences for the specialized goods. By setting σ=0

, which, in equilibrium, will equal the real wage in terms of the numeraire good. When we develop results for a standard Lucas asset-pricing model, we assume a perfectly inelastic labor supply so that the model reduces, essentially, to an endowment economy. Thus, the competitive market represents the part of the environment that is standard in macro DSGE models like the New Keynesian model or the Lucas asset-pricing model. In the specialized goods market, though, buyers can consume but not produce the specialized good while sellers can produce but cannot consume. Moreover, trade in these markets is characterized by a limited commitment friction where buyers are unable to commit to repay unsecured debt using their proceeds from producing in the competitive market. Thus, this part of the model captures environments with frictional goods markets where assets such as fiat money, stocks or bonds are used as payment instruments. Some of the most interesting, and recent, applications of heterogeneous expectations occur in such markets. We assume that with probability σ buyers will have preferences for the specialized goods. By setting σ=0![]() , the economic environment collapses into a standard environment without any real frictions.

, the economic environment collapses into a standard environment without any real frictions.

There exists a single storable good, an asset a that yields a stochastic payoff yt![]() . This asset could be fiat money, with yt=0

. This asset could be fiat money, with yt=0![]() , a Lucas tree with a stochastic dividend, or a risk-free bond with a known payoff. Depending on the frictions in the specialized goods market, the asset can be used to smooth consumption or as a liquid asset used in quid pro quo trade in the specialized goods market. That is, the frictional goods market gives a precautionary savings motive to hold the asset to insure against random consumption opportunities for the specialized good. Assume that households have separable preferences over the general good, the specialized good, and leisure.

, a Lucas tree with a stochastic dividend, or a risk-free bond with a known payoff. Depending on the frictions in the specialized goods market, the asset can be used to smooth consumption or as a liquid asset used in quid pro quo trade in the specialized goods market. That is, the frictional goods market gives a precautionary savings motive to hold the asset to insure against random consumption opportunities for the specialized good. Assume that households have separable preferences over the general good, the specialized good, and leisure.

2.3 Bounded Optimality

We now turn to agent-level decision-making taking the expectations operators as given. To best illustrate the ideas reviewed here, we develop them within the context of a very simple asset-pricing model. We, therefore, take the economic environment described above and shut-down the frictional goods market.

2.3.1 Rational Expectations

Assume that there is a fixed quantity (unit mass) of the asset (Lucas trees) each of which yields per-period non-storable stochastic dividend yt=y+εt![]() , where εt

, where εt![]() is zero mean, i.i.d. and has small support (so that yt>0

is zero mean, i.i.d. and has small support (so that yt>0![]() ). Each agent is initially endowed with a unit of assets, discounts the future at rate β, and receives per-period utility from consuming the dividend, as measured by the function u. Note that agents are assumed identical, except possibly in the way they form forecasts and make decisions.

). Each agent is initially endowed with a unit of assets, discounts the future at rate β, and receives per-period utility from consuming the dividend, as measured by the function u. Note that agents are assumed identical, except possibly in the way they form forecasts and make decisions.

Under the rational expectations hypothesis (REH), it is sufficient to consider the behavior of a representative agent. This agent solves the following problem:

(1) maxat+1≥0E∑t≥0u(ct)ptat+1=(pt+yt)at−ct,

where at![]() is the quantity of the asset held at the beginning of time t, ct

is the quantity of the asset held at the beginning of time t, ct![]() is consumption in time t, and pt

is consumption in time t, and pt![]() is the asset's (ex dividend) price in time t in terms of consumption goods.

is the asset's (ex dividend) price in time t in terms of consumption goods.

Because in a rational expectations equilibrium agents are identical, ct=yt![]() , the representative agent's Euler equation must be satisfied:

, the representative agent's Euler equation must be satisfied:

u′(yt)=βEt(pt+1+yt+1pt)u′(yt+1).

Thus the non-stochastic steady state of this model (or the perfect-foresight REE in case income is non-stochastic) is given by

(2) p=(β1−β)y,

which is the present value of the expected dividend flow.

The analysis of the model under the REH is quite straightforward from a modeler's perspective, but agents themselves are unrealistically sophisticated: they are assumed to know the endogenous distribution of pt![]() , fully solve their dynamic programming problem given this knowledge, and further, this knowledge must be common among agents.

, fully solve their dynamic programming problem given this knowledge, and further, this knowledge must be common among agents.

In the following subsections we provide various models of decision-making that do not require these assumptions. Once departing from the rational expectations hypothesis, the modeler is confronted with whether to require that boundedly rational agents take the evolution of their beliefs as a constraint on their decision-making. Or, should they satisfy behavioral primitives that (mistakenly) take their beliefs as having come from a completed learning process? The latter approach – called the anticipated utility approach – is the benchmark in the literature and forms the basis for the discussion in the next several sections. Below, we discuss alternative implementations of the anticipated utility approach as well as some of the associated drawbacks.

2.3.2 The Shadow-Price Approach

The first approach to boundedly rational decision making that we consider is shadow price learning, developed by Evans et al. (2016) as a general approach to boundedly-optimal decision making. We now relax the representative agent assumption and consider agents who are identical except for expectations, indexed by type-j. Shadow-price learning is based on two simple assumptions: agents make linear forecasts and make decisions by contemplating trade-offs as measured by shadow prices.

Within the context of the current asset-pricing model, let λjt![]() be the perceived time-t value of an additional unit of the asset for an agent of expectations-type j. To make a time t consumption decision, the agent employs a variational thought experiment about the savings/consumption tradeoff: by reducing consumption by one unit today and increasing asset holdings tomorrow by 1/pt

be the perceived time-t value of an additional unit of the asset for an agent of expectations-type j. To make a time t consumption decision, the agent employs a variational thought experiment about the savings/consumption tradeoff: by reducing consumption by one unit today and increasing asset holdings tomorrow by 1/pt![]() an agent will equate

an agent will equate

(3) u′(cjt)=βptˆEjtλjt+1.

To determine consumption, the modeler must take a stand on how ˆEjtλjt+1![]() is formed, as well as a forecasting rule for pt

is formed, as well as a forecasting rule for pt![]() . Given a specification for the forecasting models, the modeler can solve for the consumption rule by combining the budget constraint (1) and Eq. (3). Plugging the consumption rule into the budget constraint determines the agent's asset demand as a function of price, dividend, asset holdings and beliefs:

. Given a specification for the forecasting models, the modeler can solve for the consumption rule by combining the budget constraint (1) and Eq. (3). Plugging the consumption rule into the budget constraint determines the agent's asset demand as a function of price, dividend, asset holdings and beliefs:

(4) ajt+1=aSP(pt,yt,ajt,ˆEjtλjt+1).

In the literature, and the examples presented below, boundedly rational beliefs are typically modeled as functions of past data. To update beliefs over time as new data become available some proxy data for λt![]() must be computed, and for this the agent again employs another variational thought experiment: given the consumption choice, the benefit from an additional unit of the state today is

must be computed, and for this the agent again employs another variational thought experiment: given the consumption choice, the benefit from an additional unit of the state today is

(5) λjt=(pt+yt)u′(cjt).

More generally, the envelope condition provides a way to compute the observed value for the shadow price. Thus, the shadow price approach provides a set of behavioral primitives consistent with optimization but does not require the full sophistication required of the agent in order to solve the complete dynamic programming problem.

2.3.3 The Shadow-Price Approach in the Linearized Model

A particularly nice feature of the shadow price approach is that it is easily employed in non-linear environments: no linearization was needed to determine demand (4). Further, note that this approach is amenable to any expectations operator satisfying the axioms (and based on linear forecasting models).3 Most other implementations of boundedly-rational decision-making are developed in a linearized environment, and for comparison purposes, we consider a linearized version of shadow-price learning here.

Log-linearizing (3) and (5) around the non-stochastic steady state (2) (and using c=y![]() , which follows from the axioms) provides

, which follows from the axioms) provides

(6) cjt=υ−1(pt−ˆEjtλjt+1)λjt=−υcjt+βpt+βyyt,

where now all variables are written in proportional deviation from steady state form, and υ=−cu″(c)/u′(c)![]() . Eq. (6) is consistent with general expectations operators, but as above, it is standard to cast Ejtλjt+1

. Eq. (6) is consistent with general expectations operators, but as above, it is standard to cast Ejtλjt+1![]() as a linear function of state variables. These equations can be coupled with the linearized budget constraint to compute the linearized asset demand equation

as a linear function of state variables. These equations can be coupled with the linearized budget constraint to compute the linearized asset demand equation

(7) ajt+1=aSPlin(pt,yt,ajt,ˆEjtλjt+1).

As long as beliefs are linear functions of prices and dividends, then asset-demand is a function only of state variables. Importantly, aSPlin![]() is linear, which allows for tractable equilibrium analysis.

is linear, which allows for tractable equilibrium analysis.

2.3.4 The Euler Equation Approach in the Linearized Model

Under shadow-price learning, the behavioral primitive is that agents make decisions based on tradeoffs measured by shadow prices. Here we take a different perspective, Euler-equation learning as advanced by Honkapohja et al. (2013): agents make decisions based on their perceived Euler equation. We continue to work within the linearized model.

The linearized Euler equation is given by

(8) cjt=υ−1pt+ˆEjtcjt+1−βυ−1ˆEjtpt+1−βyυ−1ˆEjtyt+1.

Note that (8) identifies the agent's decision in terms of a general expectations operator, but as in the shadow-price approach, it is common to assume agents use linear forecasting models to form expectations; however, rather than their shadow-value this time agents are required to forecast their own consumption plan. Coupled with the linearized budget constraint and perceived Euler equation, we can compute asset demand:

(9) ajt+1=aELlin(pt,yt,ajt,ˆEjtcjt+1,ˆEjtpt+1),

which, as before, depends on beliefs, and is linear in prices. As before, provided that beliefs are linear functions of prices and dividends, the demand function can be written entirely in terms of state variables.

2.3.5 The Finite Horizon Approach in the Linearized Model

The shadow price and Euler equation approaches, as developed above, are based on one-step-ahead forecasts. When longer planning horizons are relevant, e.g. in case of anticipated structural change, a modification is in order. In this section we consider the implementation developed in Branch et al. (2012). The idea is simple: agents forecast their terminal asset position to solve their N-period consumption-savings problem. This finite-horizon learning approach places forecaster – who typically forecasts over a finite horizon – on equal footing with decision-makers.

While the model remains the same, it is convenient to change notation. First, go back to levels. Let ˆat=pt−1at![]() be the goods-value of the asset held at time t and let Rt=p−1t−1(pt+yt)

be the goods-value of the asset held at time t and let Rt=p−1t−1(pt+yt)![]() be the return. The flow constraint may be written

be the return. The flow constraint may be written

cjt=Rtˆajt−ˆajt+1.

Now let Dt+k=∏kn=1R−1t+n![]() , with Dt=1

, with Dt=1![]() , be the cumulative discount factor. The N-period budget constraint is then given by

, be the cumulative discount factor. The N-period budget constraint is then given by

(10) N∑k=0Dt+kct+k=Rtˆat−Dt+Nˆat+N+1.

In differential form, we have

yN∑k=1dDt+k+N∑k=0βkdcjt+k=ˆadRt+β−1dajt−βNdajt+N+1−ˆadDt+N,

where we have used that in steady state, y=c![]() and R=β−1

and R=β−1![]() . Simplifying, using that dDt+k=−βk+1∑kn=1dRt+n

. Simplifying, using that dDt+k=−βk+1∑kn=1dRt+n![]() and returning to log-deviation form, we arrive at

and returning to log-deviation form, we arrive at

(11) yN∑k=0βkcjt+k=ˆaβ−1Rt+β−1ˆaˆajt−βNˆaˆajt+N+1+ˆaβNk∑n=1Rt+k+yN∑k=1βkk∑n=1Rt+n,

which is the agent's linearized budget constraint with planning horizon N.

The linearized Euler equation yields

(12) ˆEjtcjt+k=cjt+υ−1k∑n=1ˆEjtRt+n.

Taking expectations of (11) (relying on the axioms), and using (12) to eliminate ˆEjtcjt+k![]() , we may write current consumption as linear in ajt,Rt,ˆEjtajt+N+1

, we may write current consumption as linear in ajt,Rt,ˆEjtajt+N+1![]() , and ˆEjtRt+n

, and ˆEjtRt+n![]() , for n=1,…,N

, for n=1,…,N![]() . By providing the agent with linear forecasting models for asset holdings and returns, the current consumption and savings decisions may be determined in terms of beliefs and observable state variables.

. By providing the agent with linear forecasting models for asset holdings and returns, the current consumption and savings decisions may be determined in terms of beliefs and observable state variables.

2.3.6 The Infinite Horizon Approach in the Linearized Model

Letting the planning horizon N go to infinity and imposing the transversality condition provides the infinite horizon approach. Eq. (11) becomes the usual lifetime budget constraint, which is particularly simple in our case:

(13) y∞∑k=0βkEτtcjt+k=(1−β)−1Rt+(1−β)−1ajt+y(1−β)−1∞∑k=1βkRt+k,

which, when coupled to the linearized Euler equation (12), yields

(14) cjt=y−1Rt+y−1ajt+υ−1υ∞∑k=1βkEjtRt+k.

By providing the agent with linear forecasting models for returns, the current consumption and savings decisions may be determined in terms of beliefs and observables. Notice, unlike the previous approaches, with infinite-horizon learning they only need to forecast state variables beyond their own control.

The infinite horizon approach has advantages over the Euler equation in that the agents are behaving as optimizing anticipated utility maximizers. Thus, although the agents have non-rational and possibly heterogeneous expectations, they optimize given their subjective expectations. We show below that infinite horizon learning – by emphasizing decision rules that depend on expectations of state variables beyond an agent's control – can help aggregate decision rules across agents with heterogeneous expectations. From (14), the approach leads to a key result that long-run expectations play an important role in household consumption decisions. The infinite-horizon approach has been employed extensively by Preston (2005, 2006), Eusepi and Preston (2011), Woodford (2013), and recently surveyed in Eusepi and Preston (2018).

However, there are drawbacks as well. First, as a model of bounded rationality it seems unlikely that consumers hold such long-horizon expectations. Second, solving the infinite horizon problem can be technically challenging without log-linearizing the behavioral equations. While this may be appropriate in some environments such as the New Keynesian model which also is usually solved only after log-linearizing even when agents hold rational expectations, it is not a good approximation in other environments such as asset-pricing, pure monetary theory, and models with search and matching frictions. Finally, if the motivation for learning models is to place economist and economic agent on equal footing, it seems natural to model agents as finite-horizon learners who have a more limited horizon as most econometricians only forecast for so many periods into the future.

2.3.7 A Nod to Value Functions

As an alternative to the shadow-price approach, Evans et al. (2016) consider “value-function learning” within a linear-quadratic framework. Under this approach, agents estimate the value function based on a quadratic form specification and then make decisions conditional on the estimated value function. They show that asymptotic optimality obtains under the same conditions as for the shadow-price approach.

Value-function learning in the current environment is less natural: the analog to the linearized model would be to compute a second order approximation to the objective (after substituting in the non-linear budget constraint). On the other hand, the value-function approach is especially natural in discrete choice environments: Evans et al. (2016) develop a value-function learning analysis of the McCall (1970) search model where the agent must decide whether to accept an offer. They provide conditions under which a learning agent will behave optimally asymptotically.

The value function approach is also particularly convenient when special assumptions make it natural for the agent to know the value function's form. The LQ-environment considered by Evans et al. (2016) provides one framework, and the quasi-linear utility environment in many incarnations of the Lagos–Wright model provide another: Branch and McGough (2016) and Branch (2016) use precisely this approach, which is discussed below.

2.3.8 A Defense of Anticipated Utility

In models of learning and heterogeneous (non-rational) expectations, beliefs evolve over time. Households and firms solve intertemporal optimization problems that require expectations about future variables that are relevant to their decision making. Under rational expectations, an agent holds a well-specified probability distribution that, in equilibrium, is time invariant. Under learning, there is the issue of whether, and to what extent, agents explicitly account for the evolution of their beliefs when deciding on their optimal decision rules. That is, should an agent's beliefs be a state variable in their value functions?

The anticipated utility approach dictates that agents take their current beliefs as fixed when solving for their optimal plans. Given an expectation operator dated at time t, an agent is able to formulate expectations about variables relevant to their decision making over their particular planning horizon. They then solve for their optimal plan – consumption, labor hours, and asset holdings in the present environment – while assuming that their beliefs will not change in the future. As their beliefs change, they will discard their plan and formulate a new one. In a sense, an anticipated utility maximizing agent is dogmatic about their current beliefs. Conversely, a Bayesian agent would acknowledge that their beliefs evolve and treat those beliefs as a state variable with an associated law of motion. The literature on learning and heterogeneous expectations typically maintains the anticipated utility assumption for technical convenience: solving intertemporal optimization problems as a fully Bayesian agent is analytically and computationally challenging. Moreover, as we argue here the anticipated utility assumption is appealing from a bounded rationality perspective.

Cogley and Sargent (2008) directly address the inconsistency inherent to anticipated utility maximization. Each period the agent holds beliefs about all payoff-relevant variables over the planning horizon. Then when making decisions they act as if they will never change those beliefs again, that is, until the learning process has ended. In the next period they update beliefs and again pretend that they will not learn anymore. A fully Bayesian agent, however, would acknowledge their uncertainty, include their beliefs as a state variable, and assign posterior probabilities to all of the possible future paths, choosing the consumption plan that maximizes their expected utility, where expectations are taken with respect to their posterior distribution. Cogley and Sargent (2008) compare how anticipated utility consumption decisions compare to the fully Bayesian plan. They find that anticipated utility can be seen as a good approximation to fully Bayesian optimization.

This subsection briefly comments on their results, placing the discussion in the context of our present environment, and relating it to recent models of “Internal Rationality.”4 Cogley and Sargent's approach could be mapped into the present environment by assuming that the dividend growth process follows a two-state Markov chain and the agents know that the pricing function depends on the current realization of dividend growth. Cogley and Sargent's learning model imposes that the agents know that dividend growth, hence prices, follow the two-state process but they don't know the transition probabilities. Instead, they learn about these transition probabilities using past data and by updating their estimates using Bayes' rule. The Bayesian agents solve a dynamic programming problem including their beliefs about the transition probabilities in the state vector and, so, their learning rule becomes a part of the state transition equation. An anticipated utility maximizer, on the other hand, does not include the evolution of their beliefs in the state transition equation, and solves a standard dynamic programming problem assuming their beliefs are fixed.

Cogley and Sargent show that in this simple environment that the number of times that dividend growth is in a particular state is a sufficient statistic for agents' learning model. They focus on a model with finitely-lived agents. The agent considers each possible node which consists of a particular state at time t, and the number of times that it has been in a state, assigns probabilities to these nodes, and then chooses the consumption plan that maximizes expected utility. This can be done recursively using dynamic programming methods. As time advances, the number of nodes expands and the solution to the dynamic programming problem can run into the curse of dimensionality. If the agent has an infinite planning horizon, as is typical in macroeconomic and asset-pricing models, then the state space is unbounded and standard results for dynamic programming do not apply. Cogley and Sargent discuss an approximation, where since the agents are learning about an exogenous process, with no feedback from beliefs, the estimated probabilities eventually converge to their true values. So agents can take as given the value function that they will eventually converge to, and then recursively solve a finite horizon problem.

Adam et al. (2017) consider an asset-pricing model where agents are “internally rational.” Like Cogley and Sargent they expand the state vector to include agents' beliefs. However, internally rational agents do not know the pricing function and so also forecast price-growth. With a continuous Markov process for dividend growth, and other restrictions on beliefs, they are able to numerically solve for the policy function. They find that such a model can explain key asset pricing and survey data empirical regularities.

This chapter focuses on bounded rationality and heterogeneous expectations. We do not present results on internal rationality because we do not find it a realistic model of individual behavior. The motivation for heterogeneous expectations and learning models is that forming rational expectations is complex and costly. The fully Bayesian model of decision making is, in essence, a hyper-rational model of agent decision-making. Besides considering what prices and other exogenous variables might be in the future, they also take into account how their beliefs might evolve along any history of shocks. Loosely speaking, an agent who is optimistic today has to forecast how they will behave in a few years if they become pessimistic and, continuing this internal thought experiment, will they switch to being optimistic in, say, another 10 years, and so on. Given the complexity for the modeler to solve such a dynamic programming problem, the potential for the curse of dimensionality, and the possibility that standard recursive tools are not available, it strikes us as not the most compelling way to describe real-life behavior.5 The advantage of the internal rationality approach is to focus attention on the role of learning, without other assumptions about boundedly rational decision-making, and, as a benchmark like rational expectations, we agree that it is a useful theoretical approach. We are heartened that models with Euler equation learning and internal rationality produce similar asset-pricing implications.

However, the focus of this article is the extent to which bringing more realistic models of agent behavior can lead to distinct implications and provide explanations for real-world phenomena. Thus, we advocate for, and focus on, models of anticipated utility maximization.

2.4 Aggregating Household Decision Rules

Having derived the individual boundedly rational optimizing behavior of heterogeneous agents, equilibrium requires computing aggregate, or market-clearing consumption/output from which assets can then be priced. Many applications derive an aggregate asset-pricing equation that depends on the aggregate expectations operator. This section illustrates how to aggregate decision rules, while briefly discussing some challenges.

To illustrate, we adopt the Euler equation learning approach. Recall that the behavioral primitives, in the log-linearized economy, are

cjt=βRˆEjtcjt+1−βRυ−1ˆEjtRt+1cjt=ˆaR(ˆajt+Rt)−ˆaˆajt+1≡Ωjt

where Ωj![]() denotes (end of period) real-wealth. Iterating on the Euler equation, we have

denotes (end of period) real-wealth. Iterating on the Euler equation, we have

Ωjt=Ωj∞−βRυ−1ˆEjt∞∑k=1(βR)k−1Rt+k

where Ωj∞=limT→∞(βR)TˆEjtcT![]() . In the asset-pricing application, βR=1

. In the asset-pricing application, βR=1![]() and so the Euler equation iterated forward depends on expected limiting wealth. In a model where there is a precautionary savings motivate, for instance in the version of the model with the specialized goods market and a limited commitment friction, it is possible that R<β−1

and so the Euler equation iterated forward depends on expected limiting wealth. In a model where there is a precautionary savings motivate, for instance in the version of the model with the specialized goods market and a limited commitment friction, it is possible that R<β−1![]() and Ωj∞=0

and Ωj∞=0![]() . In this case, aggregation proceeds without any difficulty.

. In this case, aggregation proceeds without any difficulty.

When βR=1![]() , then additional assumptions on higher-order beliefs are necessary for aggregation. To illustrate this, assume that there are two expectation-types, j=1,2

, then additional assumptions on higher-order beliefs are necessary for aggregation. To illustrate this, assume that there are two expectation-types, j=1,2![]() . Then, nΩ1t+(1−n)Ω2t=(1−β)−1Rt

. Then, nΩ1t+(1−n)Ω2t=(1−β)−1Rt![]() in this linearized economy. Then

in this linearized economy. Then

(1−β)−1Rt=nΩ1t+(1−n)Ω2t=nΩ1∞+(1−n)Ω2∞−υ−1ˆEt∑k⩾1Rt+k=[1−υ−1(1−β)]ˆEtRt+1+nΩ1∞+(1−n)Ω2∞−ˆE[nΩ1∞+(1−n)Ω2∞]

where ˆE=nˆE1+(1−n)ˆE2![]() . Thus, to have a (linearized) asset-pricing equation that depends on the aggregate expectations operator – i.e. a weighted average of heterogeneous expectations – requires that all agents agree on limiting wealth, an axiom needed for aggregation in the New Keynesian model as shown by Branch and McGough (2009). Alternatively, a model with βR<1

. Thus, to have a (linearized) asset-pricing equation that depends on the aggregate expectations operator – i.e. a weighted average of heterogeneous expectations – requires that all agents agree on limiting wealth, an axiom needed for aggregation in the New Keynesian model as shown by Branch and McGough (2009). Alternatively, a model with βR<1![]() also facilitates aggregation without difficulty.

also facilitates aggregation without difficulty.

3 Equilibria with Heterogeneous Expectations

Having developed both a general framework for non-rational expectations operators as well as a corresponding decision theory, we now turn to equilibrium considerations. There are two questions to address:

- 1. Given the distribution of agents across expectations operators, how are endogenous variables determined?

- 2. How are agents distributed across expectations operators?

The first question is straightforward to address: under the reduced form approach, a convex combination of expectations operators is imposed directly into the reduced-form expectational difference equations; while under a micro-founded approach, a temporary equilibrium is constructed by aggregating individual rules and imposing market clearing.

Three different broad mechanisms have been proposed to address the second question. Many, especially early, applications of heterogeneous expectations in macroeconomic models imposed the degree of heterogeneity exogenously, which we describe as extrinsic heterogeneity. Beginning with the seminal work by Brock and Hommes (1997), much of the literature has the distribution of agents across models as an equilibrium object. Here we review two ways in which heterogeneity can arise endogenously: first, where there is a cost to using certain types of predictors, i.e. rationally heterogeneous expectations; second, where forecasters miss-specify their models in different ways, but in equilibrium they only choose the best performing models, that is, intrinsic heterogeneity.

3.1 Extrinsic Heterogeneity

An equilibrium with extrinsic heterogeneity takes the distribution of agents across models as fixed and computes equilibrium prices and quantities. In particular, in the asset-pricing application developed in the previous section, each agent of type j, solves for their optimal consumption and asset holdings given their behavioral primitives (e.g. SP-learning, etc.), and then the temporary equilibrium pins down the price. For example, suppose J is a finite index set of types of SP-learning agents who differ only in their time-t beliefs. The asset demand of an agent of type j∈J![]() is then given by

is then given by

ajt+1=aSP(pt,yt,ajt,ˆEjtλjt+1)

Let nj![]() be the measure of type j agents. Given yt

be the measure of type j agents. Given yt![]() , beliefs {ˆEjtλjt+1}j∈J

, beliefs {ˆEjtλjt+1}j∈J![]() , and asset holdings {ajt}j∈J

, and asset holdings {ajt}j∈J![]() , the equilibrium price is determined by

, the equilibrium price is determined by

1=∑j∈Jnj⋅aSP(pt,yt,ajt,ˆEjtλjt+1)

Note that here we are using the non-linear version of SP-learning. The linearized market-clearing condition would set the sum to zero. Note also that, in this linearized case, an analytic expression for pt![]() in terms of beliefs, exogenous variables, and the distribution of asset holdings, is available.

in terms of beliefs, exogenous variables, and the distribution of asset holdings, is available.

3.2 Rationally Heterogeneous Expectations

The theory of rationally heterogeneous expectations, as formulated by Brock and Hommes (1997), holds that expectation formation is a discrete choice from a finite set of predictors.

3.2.1 Predictor Selection

In order to illustrate how the approach works in the present environment, for ease of exposition, we assume the shadow value learning formulation, and risk-neutral preferences. In this case,

(15) pt=βy+βˆEtpt+1

where ˆEt![]() is a convex combination of expectations operators:

is a convex combination of expectations operators:

ˆEtpt+1=N∑j=1njpet+1(j)

where pet+1(j)![]() is the forecast provided by predictor j, and nj

is the forecast provided by predictor j, and nj![]() is the proportion of agents using that forecast.

is the proportion of agents using that forecast.

Each individual i is assumed to select their predictor j by solving the following problem:

jt+1=argmaxj=1,...,J{Ωi(j,pet(j),pt)}

where

Ωi(j,pet,pt)=−(pt−pet(j))2−Cit(j)

The objective function Ωi![]() can be thought of as consisting of two components: −(pt−pet(j))2

can be thought of as consisting of two components: −(pt−pet(j))2![]() captures the preference for predictors that forecast well; and, Cit(j)

captures the preference for predictors that forecast well; and, Cit(j)![]() is an idiosyncratic preference shock measuring individual i's relative ease of using predictor j, i.e. it is a “cost” to using the predictor.

is an idiosyncratic preference shock measuring individual i's relative ease of using predictor j, i.e. it is a “cost” to using the predictor.

The cross-sectional distribution of the preference shock determines the distribution of agents across the predictors. We follow the discrete choice approach of Brock and Hommes (1997) and assume that Cit(j)=C(j)+ηit(j)![]() . Provided that the ηit

. Provided that the ηit![]() are i.i.d. across time and individuals and, further, have the extreme value distribution, then the fraction of individuals using predictor j, denoted nt(j)

are i.i.d. across time and individuals and, further, have the extreme value distribution, then the fraction of individuals using predictor j, denoted nt(j)![]() is given by the multinomial logit (MNL) map:

is given by the multinomial logit (MNL) map:

(16) nt(j)=nt(j,pt−1,{pet−1(τ)}Jτ=1)=exp{ω×Ω(j,pt−1,pet−1(j))}∑Nτ=1exp{ω×Ω(τ,pt−1,pet−1(τ))}

The MNL map has a long and venerable history in discrete choice decision making. It is a natural way of introducing randomness in forecasting and has a similar interpretation as mixed strategies in actions as a mechanism for remaining robust to forecast model uncertainty. The coefficient ω is referred to as the ‘intensity of choice’ and is inversely related to the variance of the idiosyncratic preference shock ηit![]() . Finite values of ω, the intensity of choice, imply less than full utility maximization. The neoclassical case is when ω→+∞

. Finite values of ω, the intensity of choice, imply less than full utility maximization. The neoclassical case is when ω→+∞![]() .

.

One note about the formulation in (16). Here nt(j)![]() is the fraction of agents holding predictor j at time t, i.e. it is the distribution at the time when markets clear and pt

is the fraction of agents holding predictor j at time t, i.e. it is the distribution at the time when markets clear and pt![]() is realized. We follow much of the adaptive learning literature in assuming a (t−1)

is realized. We follow much of the adaptive learning literature in assuming a (t−1)![]() -timing structure of information known to agents when they select predictors. Since these individuals are boundedly rational it is natural to assume that predictor choice and market outcomes are not determined simultaneously. Thus, when selecting the predictor to take into the market in time t the most recently observed data point is pt−1

-timing structure of information known to agents when they select predictors. Since these individuals are boundedly rational it is natural to assume that predictor choice and market outcomes are not determined simultaneously. Thus, when selecting the predictor to take into the market in time t the most recently observed data point is pt−1![]() .

.

3.2.2 Heterogeneous Beliefs and Economic Dynamics: Stability Reversal

Coupling predictor choice as in (16) with the pricing equation (15) can lead to interesting non-linear dynamics that exploit the mutual feedback between the pricing process – which is self-referential – and the choice of predictors. We illustrate these implications in this subsection.

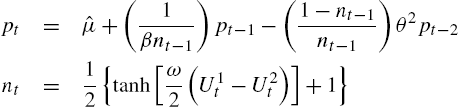

Continue to assume that price is determined by (15). We will consider a simple example, as in Branch and McGough (2016), where individuals select from either a perfect foresight predictor, with a cost C>0![]() , or a simple adaptive predictor at no cost. That is, the predictors are

, or a simple adaptive predictor at no cost. That is, the predictors are

ˆE1tpt+1=pt+1ˆE2tpt+1=ˉp+θ(pt−1−ˉp)

where ˉp=ˉy/(1−β)![]() is the steady-state price. Without loss of generality, set ˉy=0

is the steady-state price. Without loss of generality, set ˉy=0![]() . Then the actual law of motion is

. Then the actual law of motion is

pt=(1βnt−1)pt−1−(1−nt−1nt−1)θpt−2nt=12{tanh[ω2((pt−1−θpt−2)2−C)]+1}

Predictor selection can lead to an endogenous attracting/repelling dynamic that can lead to periodic and complex fluctuations in price. The key intuition for complex dynamics is the stability reversal property of heterogeneous expectations:

Proposition 1

Consider the case of rational versus adaptive expectations and (15) with extrinsic heterogeneity.

- a. Let n=1

. The steady state is dynamically unstable and there exists a unique non-explosive perfect foresight equilibrium path.

. The steady state is dynamically unstable and there exists a unique non-explosive perfect foresight equilibrium path. - b. Let n=0

. The steady state is dynamically stable provided that βθ<1

. The steady state is dynamically stable provided that βθ<1 .

.

When n=1![]() , and all agents are rational, there is a unique rational expectations equilibrium that coincides with the steady-state. That is, the steady state is the only non-explosive solution to the forward expectational difference equation (15). The equilibrium is unique because the steady-state is dynamically unstable. Conversely, so long as θ is not too large – for example, 0<θ<1

, and all agents are rational, there is a unique rational expectations equilibrium that coincides with the steady-state. That is, the steady state is the only non-explosive solution to the forward expectational difference equation (15). The equilibrium is unique because the steady-state is dynamically unstable. Conversely, so long as θ is not too large – for example, 0<θ<1![]() would be sufficient – then the steady-state is dynamically stable and all paths from an initial condition on beliefs will converge to the steady-state.

would be sufficient – then the steady-state is dynamically stable and all paths from an initial condition on beliefs will converge to the steady-state.

The stability reversal property arises intuitively because perfect foresight requires forward-looking behavior and adaptive beliefs are backward-looking. This is most easily seen by noting that the expectational difference equation (15) reverses direction when, for instance, ˆEtpt+1=pt−1![]() . Therefore, forward stability implies backward stability, and vice versa. The possibility of stability reversal plays a prominent role in explaining the dynamic behavior of models with heterogeneous expectations. In subsequent sections, we present examples where stability reversal implies complex attracting/repelling dynamics.

. Therefore, forward stability implies backward stability, and vice versa. The possibility of stability reversal plays a prominent role in explaining the dynamic behavior of models with heterogeneous expectations. In subsequent sections, we present examples where stability reversal implies complex attracting/repelling dynamics.

3.3 Intrinsic Heterogeneity

In the rationally heterogeneous expectations approach, heterogeneity arises because of a cost to using a particular predictor, and for finite intensities of choice, ω, i.e. because of the idiosyncratic preference shocks. In Branch and Evans (2006) an environment is presented where heterogeneity can arise even in the neoclassical case of ω→+∞![]() . The framework developed by Branch and Evans is an extension of Brock and Hommes to a stochastic environment where agents select among a set of misspecified forecasting models. In a Misspecification Equilibrium the parameters of the forecasting models, and the distribution of agents across models, are determined jointly as equilibrium objects. Intrinsic Heterogeneity arises if agents are distributed across more than one model even as ω→∞

. The framework developed by Branch and Evans is an extension of Brock and Hommes to a stochastic environment where agents select among a set of misspecified forecasting models. In a Misspecification Equilibrium the parameters of the forecasting models, and the distribution of agents across models, are determined jointly as equilibrium objects. Intrinsic Heterogeneity arises if agents are distributed across more than one model even as ω→∞![]() . Branch and Evans (2006) developed their results within the context of a cobweb model, though Branch and Evans (2010) extend to an asset-pricing model, and Branch and Evans (2011) show existence of Intrinsic Heterogeneity in a New Keynesian model.

. Branch and Evans (2006) developed their results within the context of a cobweb model, though Branch and Evans (2010) extend to an asset-pricing model, and Branch and Evans (2011) show existence of Intrinsic Heterogeneity in a New Keynesian model.

To illustrate the approach, we extend the basic modeling environment to include two different serially correlated shocks, a dividend shock and a share-supply shock. In Branch and Evans (2010) the share-supply shock arises in an OLG model through random variations in population growth, which affects the supply of trees per person. In Branch (2016) variations in the supply can arise in the search-based asset-pricing model outlined in the previous section. Here we will illustrate the approach in the context of the search-based asset-pricing model that, with large enough liquidity services role for the asset in facilitating specialized good consumption, can feature negative feedback as in the Cobweb and New Keynesian economies.

A log-linearization to the asset-pricing equation extended to include a liquidity premium can be written as

ˆpt=α0ˆEtˆyt+1+α1ˆEtˆpt+1+α2ˆAt

for appropriately defined αk,k=0,1,2![]() .6 The stochastic process At

.6 The stochastic process At![]() is the supply of shares in the Lucas tree, which can be interpreted as asset float resulting from new share issuances, repurchases, and stock splits. Assume that the stochastic processes for dividends and share supply are stationary AR(1) processes, given by

is the supply of shares in the Lucas tree, which can be interpreted as asset float resulting from new share issuances, repurchases, and stock splits. Assume that the stochastic processes for dividends and share supply are stationary AR(1) processes, given by

ˆyt=ρˆyt−1+εtˆAt=ϕˆAt−1+νt

where ε,ν![]() are uncorrelated across time but are potentially correlated with each other. If there is sufficient curvature of the utility function over the specialized good then α1<0

are uncorrelated across time but are potentially correlated with each other. If there is sufficient curvature of the utility function over the specialized good then α1<0![]() and the model exhibits negative feedback. This arises when the liquidity premium is high: if the expected price of the asset is high then it will relax the liquidity constraint and individuals do not need to hold as much of the asset to facilitate specialized-goods consumption, demand for the asset goes down, and price decreases. Alternatively, for smaller liquidity premia then α1>0

and the model exhibits negative feedback. This arises when the liquidity premium is high: if the expected price of the asset is high then it will relax the liquidity constraint and individuals do not need to hold as much of the asset to facilitate specialized-goods consumption, demand for the asset goes down, and price decreases. Alternatively, for smaller liquidity premia then α1>0![]() .

.

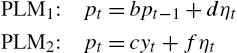

In a rational expectations equilibrium, agents would include in their forecasting model, or perceived law of motion (PLM), both dividends and share supply. In Branch and Evans (2006), agents were assumed to select from a set of underparameterized forecasting models. In the present application, the set of forecasting models are:

ˆpt=b1ˆyt+ϵ1t⇒ˆE1tˆpt+1=b1ρˆytˆpt=b2ˆAt+ϵ2t⇒ˆE2tˆpt+1=b2ϕˆAt

Underparameterization is motivated by real life decisions encountered by professional forecasters. Often, degrees of freedom limitations lead forecasters to adopt parsimonious models.7

Denote by n the fraction of agents who adopt the dividend-only forecasting model, i.e. “model 1”. Plugging in expectations, the actual law of motion can be written as

ˆpt=ξ0(b1,n)ˆyt+ξ1(b2,n)ˆAt

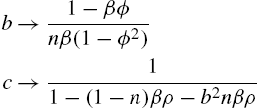

In a Misspecification Equilibrium, agents only select the best-forming statistical models. Thus, in equilibrium we require that the coefficients of the forecasting models are determined by the least-squares projection of price onto the restricted set of regressors, i.e. b1,b2![]() satisfy the least-squares orthogonality conditions

satisfy the least-squares orthogonality conditions

(17) Eˆyt(pt−b1ˆyt)=0

(18) EˆAt(pt−b2ˆAt)=0

A Restricted Perceptions Equilibrium is a stochastic process for pt![]() , given n, such that b1,b2

, given n, such that b1,b2![]() satisfy (17)–(18). In a restricted perceptions equilibrium the agents forecasting models are misspecified but, within the context of their forecasting model, they do not recognize the misspecification. A restricted perceptions equilibrium can be justified in environments where data is slow to reveal the misspecification, a property shared by most time series data.

satisfy (17)–(18). In a restricted perceptions equilibrium the agents forecasting models are misspecified but, within the context of their forecasting model, they do not recognize the misspecification. A restricted perceptions equilibrium can be justified in environments where data is slow to reveal the misspecification, a property shared by most time series data.

A Misspecification Equilibrium requires that the agents only select their best performing statistical model. Branch and Evans (2006) endogenize the distribution of agents across forecasting models, as in Brock–Hommes, by assuming they make a discrete choice and the distribution is determined by the MNL-map:

n=12{tanh[ω2F(n)]+1}≡Tω(n)

where F(n)![]() is the relative mean-squared error between predictor 1 and predictor 2 within a restricted perceptions equilibrium for a given n. Notice that the T-map: Tω:[0,1]→[0,1]

is the relative mean-squared error between predictor 1 and predictor 2 within a restricted perceptions equilibrium for a given n. Notice that the T-map: Tω:[0,1]→[0,1]![]() is continuous and so the set of equilibria is indexed by the intensity of choice ω and the properties of the function F.

is continuous and so the set of equilibria is indexed by the intensity of choice ω and the properties of the function F.

Definition 2

A Misspecification Equilibrium is a fixed point, n⁎![]() , of Tω

, of Tω![]() .

.

The set of equilibria depend on the properties of F, and can be characterized in the following way.

Proposition 3

The set of Misspecification Equilibria has one of the following properties.

- 1. If F(0)>0

and F(1)<0

and F(1)<0 , then as ω→∞

, then as ω→∞ , n⁎→˜n

, n⁎→˜n where F(˜n)=0

where F(˜n)=0 . That is, the model exhibits Intrinsic Heterogeneity.

. That is, the model exhibits Intrinsic Heterogeneity. - 2. If F(0)>0 and F(1)>0

, then as ω→∞, n⁎→1

, then as ω→∞, n⁎→1 .

. - 3. If F(0)<0

and F(1)<0, then as ω→∞, n⁎→0

and F(1)<0, then as ω→∞, n⁎→0 .

. - 4. If F(0)<0 and F(1)>0, then as ω→∞, the model has multiple Misspecification equilibrium with n⁎→∈{0,˜n,1}

and F(˜n)=0.

and F(˜n)=0.

Intrinsic Heterogeneity arises when agents do not want to mass on one or the other predictors, which occurs when F(0)>0,F(1)<0![]() , i.e. there is always an incentive to deviate from expectations homogeneity. In the Branch–Evans papers it was shown that Intrinsic Heterogeneity requires negative feedback, α1<0

, i.e. there is always an incentive to deviate from expectations homogeneity. In the Branch–Evans papers it was shown that Intrinsic Heterogeneity requires negative feedback, α1<0![]() , which can occur for large liquidity premia in the present environment. In the monetary policy application, negative feedback can arise when the central bank sets its policy rate according to an expectations-based Taylor-type rule with an aggressive response to expectations. Negative feedback implies that the asset pricing model features strategic substitution effects. There can also be multiple equilibria when there are sufficiently strong strategic complementarities, i.e. with α1>0

, which can occur for large liquidity premia in the present environment. In the monetary policy application, negative feedback can arise when the central bank sets its policy rate according to an expectations-based Taylor-type rule with an aggressive response to expectations. Negative feedback implies that the asset pricing model features strategic substitution effects. There can also be multiple equilibria when there are sufficiently strong strategic complementarities, i.e. with α1>0![]() . In this case, there are misspecification equilibria with all agents massed onto one model or the other, and a third misspecification equilibria that exhibits Intrinsic Heterogeneity.8

. In this case, there are misspecification equilibria with all agents massed onto one model or the other, and a third misspecification equilibria that exhibits Intrinsic Heterogeneity.8

4 Asset-Pricing Applications

Heterogeneous expectations provide a promising avenue for generating more realistic movements in asset prices than what is capable with the representative agent counterpart. This section illustrates three mechanisms for generating empirical features of asset prices. First, we present a Misspecification Equilibrium, when combined with learning, that is able to generate regime-switching returns and volatilities consistent with the data. Second, we highlight two ways in which heterogeneous expectations can lead to the endogenous emergence of bubbles and crashes.

4.1 Regime-Switching Returns

Branch and Evans (2010) construct a mean-variance asset-pricing model where stock prices are driven by expected returns, which depend directly on dividends and asset share supply, and indirectly via the self-referential feature of the pricing Euler equation. As in the previous section, it was assumed that traders are distributed across underparameterized forecasting models that depend only on dividends or share supply. It was shown that multiple Misspecification Equilibria exist and a real-time adaptive learning version of the model generates regime-switching returns and volatilities.

The asset-pricing equation in Branch and Evans (2010) was derived from an overlapping generations model with mean-variance preferences. The dynamic structure of OLG models is quite similar to the sub-periods of the Lagos–Wright based model developed in Section 2. The CARA preferences underlying the mean-variance structure lead to a downward sloping demand curve, similar to what emerges in the search-based model where the limited demand is based on the liquidity properties of the asset. Thus, the results in Branch and Evans (2010) are robust to the version of the model with liquidity considerations provided that there are log preferences over the specialized good: see Branch (2016). For ease of exposition, this subsection deviates from the model derived in this chapter and presents the asset-pricing equation derived by Branch and Evans (2010).

The mean-variance asset-pricing model, with stochastic processes for dividends and share supply, has asset demand represented by equations of the form, for an agent with expectations-type j,

ajt=1γˆσ2ˆEjt(pt+1+yt+1−Rpt)

where γ is the coefficient of absolute risk aversion and ˆσ2![]() is the (perceived) conditional variance of excess returns. The risk parameter ˆσ

is the (perceived) conditional variance of excess returns. The risk parameter ˆσ![]() is pinned down as an equilibrium object of the model. As in the previous section, assume that there are two-types of agents who differ based on whether they forecast with a dividends-based or share supply-based model. Then market equilibrium requires that

is pinned down as an equilibrium object of the model. As in the previous section, assume that there are two-types of agents who differ based on whether they forecast with a dividends-based or share supply-based model. Then market equilibrium requires that

na1t+(1−n)a2t=At

where, again, At![]() represents asset share supply (or, float). The equilibrium process for price is, then, given by

represents asset share supply (or, float). The equilibrium process for price is, then, given by

(19) pt=β[nˆE1tpt+1+(1−n)ˆE2tpt+1]+βρyt−βaˆσ2At

where β=1/R![]() . As before, assume that dividends and share supply are represented as stationary AR(1) processes, written in deviation-from-mean form:

. As before, assume that dividends and share supply are represented as stationary AR(1) processes, written in deviation-from-mean form:

yt=(1−ρ)y0+ρyt−1+εtAt=(1−ϕ)A0+ϕAt−1+νt

Traders are assumed to form their forecasts by selecting from one of the following misspecified models:

PLM1:pt=b10+b1yt+ηtPLM1:pt=b20+b2At+ηt

where ηt![]() is a perceived white noise error. As before, the distribution of agents, after selecting their predictor, is given by the MNL map:

is a perceived white noise error. As before, the distribution of agents, after selecting their predictor, is given by the MNL map:

Tω(n)=12{tanh[ω2F(n)]+1}

A Misspecification Equilibrium is a fixed point n⁎![]() to the T-map, i.e. n⁎=Tω(n⁎)

to the T-map, i.e. n⁎=Tω(n⁎)![]() .

.

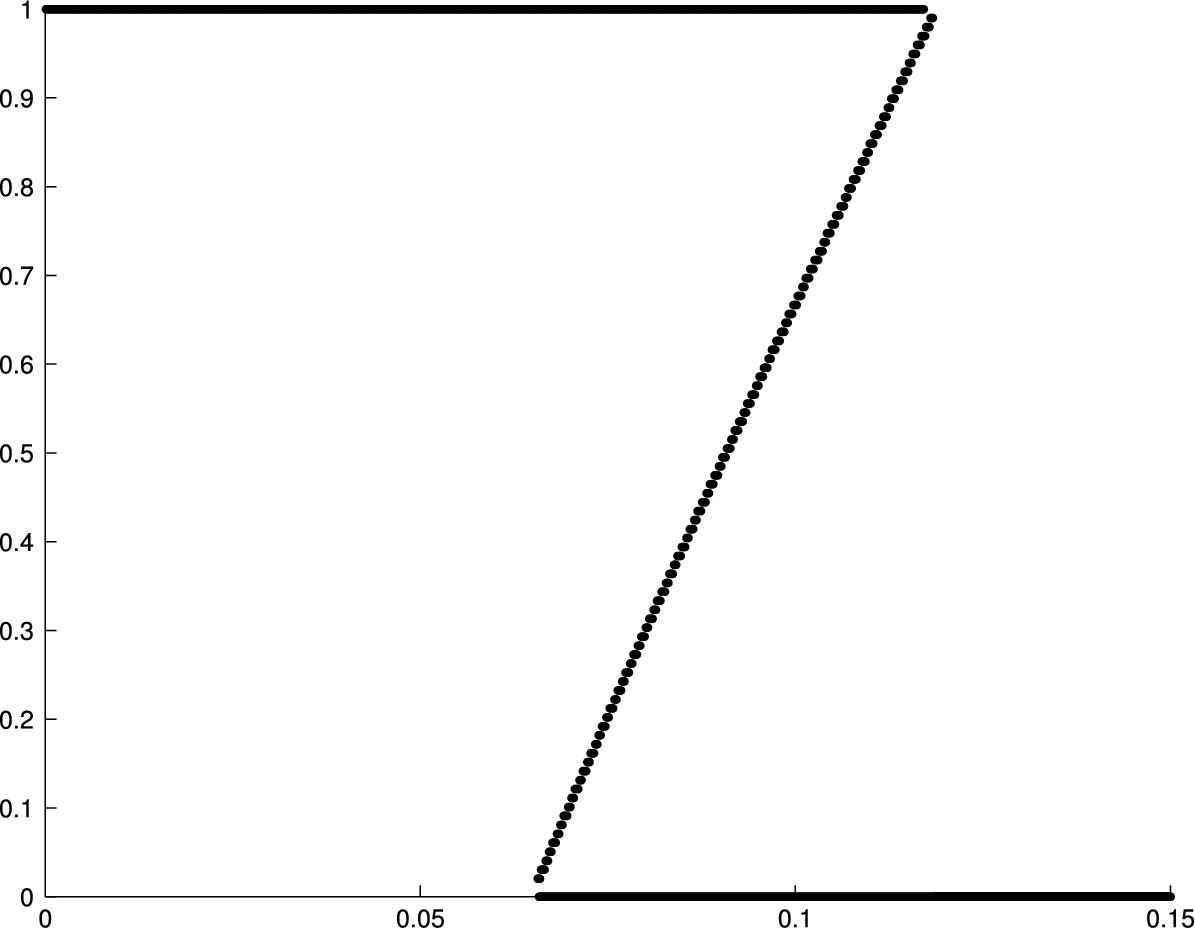

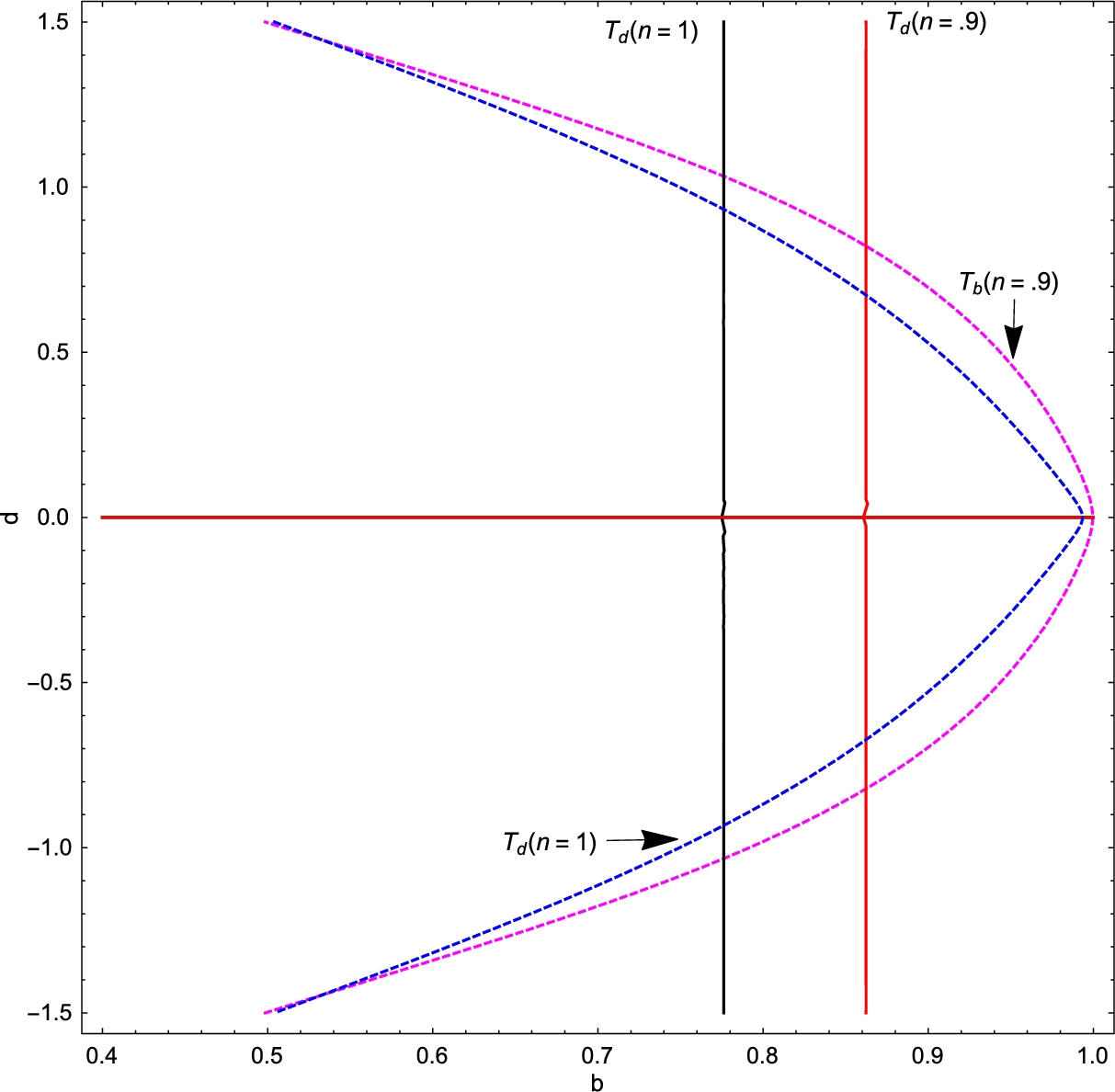

Branch and Evans (2010) show theoretically that there can exist multiple misspecification equilibria. An example is given in Fig. 3, which is based on a calibrated version of the model with ω→∞![]() . Fig. 3 plots the T-map and F(n)

. Fig. 3 plots the T-map and F(n)![]() functions, where the T-map crosses the 45∘

functions, where the T-map crosses the 45∘![]() line is a Misspecification Equilibrium. In the calibrated version of the model, there are multiple misspecification equilibria. When all agents use forecast model 1, then it is a best-response for an agent to use forecast model 1 as it delivers a lower mean-square forecast error. Similarly, for model 2. Notice that there is also an interior equilibrium exhibiting Intrinsic Heterogeneity. The right hand panels compute the volatility of returns for a given n. These figures reveal that there exist multiple misspecification equilibria, that differ in mean returns and volatilities. In particular, there exists a low return-low volatility and a high return-high volatility equilibrium.

line is a Misspecification Equilibrium. In the calibrated version of the model, there are multiple misspecification equilibria. When all agents use forecast model 1, then it is a best-response for an agent to use forecast model 1 as it delivers a lower mean-square forecast error. Similarly, for model 2. Notice that there is also an interior equilibrium exhibiting Intrinsic Heterogeneity. The right hand panels compute the volatility of returns for a given n. These figures reveal that there exist multiple misspecification equilibria, that differ in mean returns and volatilities. In particular, there exists a low return-low volatility and a high return-high volatility equilibrium.

The set of Misspecification Equilibria depends on the structural parameters of the model. In particular, the degree of risk-aversion – analogously, in the search-based model, the preferences for the differentiated good – plays an important role in determining whether multiple equilibria and whether Intrinsic Heterogeneity can exist. In Fig. 4, Branch and Evans (2010) compute the misspecification equilibria treating the degree of risk-aversion, a, as a bifurcation parameter. For low and high risk aversion there exist unique equilibria with homogeneous expectations. For moderate, and empirically realistic, degrees of risk-aversion there are multiple equilibria, including ones with Intrinsic Heterogeneity.

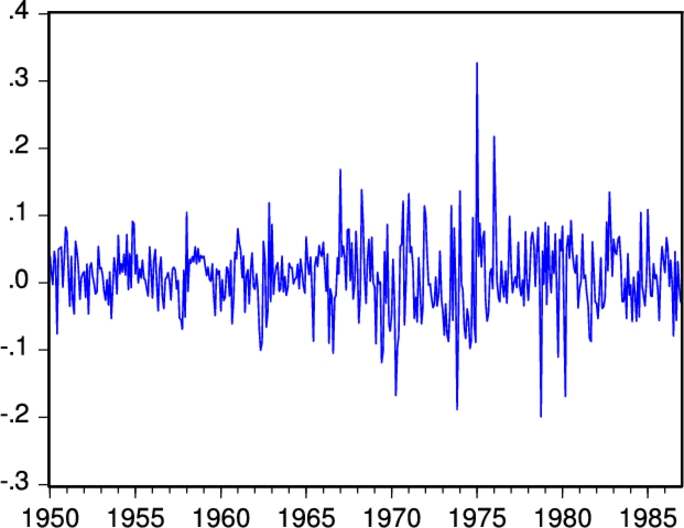

Branch and Evans (2010) exploited the existence of multiple misspecification equilibria to generate regime-switching returns and volatilities that match those estimated in the data by Guidolin and Timmermann (2007). To generate plausible dynamics, the Misspecification Equilibrium values for the belief parameters bj![]() , and the mean-square errors, were replaced by real-time recursive econometric estimators. Branch and Evans also specified a recursive estimator for the conditional variance ˆσ2