Models of Financial Stability and Their Application in Stress Tests✶

Christoph Aymanns⁎; J. Doyne Farmer†,‡,§,¶,1; Alissa M. Kleinnijenhuis†,‡,∥; Thom Wetzer†,∥,⁎⁎ ⁎Swiss Institute of Banking and Finance, University of St. Gallen, St. Gallen, Switzerland

†Institute for New Economic Thinking at the Oxford Martin School, University of Oxford, Oxford, United Kingdom

‡Mathematical Institute, University of Oxford, Oxford, United Kingdom

§Department of Computer Science, University of Oxford, Oxford, United Kingdom

¶Santa-Fe Institute, Santa Fe, NM, United States

∥Oxford-Man Institute of Quantitative Finance, University of Oxford, Oxford, United Kingdom

⁎⁎Faculty of Law, University of Oxford, Oxford, United Kingdom

1Corresponding author. email address: [email protected]

Abstract

We review heterogeneous agent models of financial stability and their application in stress tests. In contrast to the mainstream approach, which relies heavily on the rational expectations assumption and focuses on situations where it is possible to compute an equilibrium, this approach typically uses stylized behavioral assumptions and relies more on simulation. This makes it possible to include more actors and more realistic institutional constraints, and to explain phenomena that are driven by out of equilibrium behavior, such as clustered volatility and fat tails. We argue that traditional equilibrium models and agent-based models are complements rather than substitutes, and review how the interaction between these two approaches has enriched our understanding of systemic financial risk. After presenting a brief summary of key terminology, we review models for leverage and endogenous risk dynamics. We then review the network aspects of systemic risk, including models for the three main channels of contagion: counterparty loss, overlapping portfolios, and funding liquidity. We give an overview of applications to stress testing, including both microprudential and macroprudential stress tests. Finally, we discuss future directions. These include a better understanding of dynamics on networks and interacting channels of contagion, models with learning and limited deductive reasoning that can survive the Lucas critique, and practical applications to risk monitoring using models estimated with the massive data bases currently being assembled by the leading central banks.

Keywords

Stress testing; Systemic risk; Contagion; Leverage cycles; Multi-layered networks; Heterogeneous agent models; Financial systems; Financial stability; Computational economics; Complex systems; Banks; Non-banks; Microprudential; Macroprudential; System-wide stress tests

1 Introduction

The financial system is a classic example of a complex system. It consists of many diverse actors, including banks, mutual funds, hedge funds, insurance companies, pension funds and shadow banks. All of them interact with each other, as well as interacting directly with the real economy (which is undeniably a complex system in and of itself). The financial crisis of 2008 provided a perfect example of an emergent phenomenon, which is the hallmark of a complex system.

While the causes of the crisis remain controversial, a standard view goes like this: A financial market innovation called mortgage-backed securities made lenders feel more secure, causing them to extend more credit to households and purchase large quantities of securities on credit. Liberalized lending fueled a housing bubble; when it crashed, the fact that the portfolios of most major financial institutions had significant holdings of mortgage backed securities caused large losses. This in turn caused a credit freeze, cutting off funding for important activities in the real economy. This generated a global recession that cost the world an amount that has been estimated to be as high as fifty trillion dollars, the order of half a year of global GDP. Here we will present an alternative hypothesis, suggesting the possibility that the housing bubble was only the spark that lit the fire, and a deeper underlying cause might have been the build up of systemic risk over time. As we will discuss below, a substantial part of this systemic risk may have been due to backward looking, procyclical risk management of leveraged financial institutions.2 In either case, the crisis provides a clear example of an emergent phenomenon.

The crisis has made everyone aware of the complex nature of the interactions and feedback loops in the economy, and has driven an explosive amount of research attempting to better understand the financial system from a systemic point of view. It has also underlined the policy relevance of the complex systems approach. Systemic risk occurs when the decisions of individuals, which might be prudent if considered in isolation, combine to create risks at the level of the whole system that may be qualitatively different from the simple combination of their individual risks. By its very nature systemic risk is an emergent phenomenon that comes about due to the nonlinear interaction of individual agents. To understand systemic risk we need to understand the collective dynamics of the system that gives rise to it.

The financial system is sufficiently complicated that it is not yet possible to model it realistically. Existing models only attempt a stylized view, trying to elucidate the underlying mechanisms driving financial stability. There are currently two basic approaches. The mainstream approach has been to focus on situations where it is possible to compute an equilibrium. This generally requires making very strong simplifications, e.g. studying only a few actors and interactions at a time. The equilibrium approach has been useful to clarify some of the key mechanisms driving financial instabilities and financial contagion, but it comes at the expense of simplifications that limit the realism of the conclusions. There is also a concern that, particularly during a crisis, the assumptions of rationality and equilibrium are too strong.

The alternative approach abandons equilibrium and rationality and replaces them with behavioral assumptions.3 This approach often relies on simulation, which has the advantage that it is easier to study more complicated situations, e.g. with more actors and more realistic institutional constraints. It also makes it possible to study multiple channels of interaction; even though research in this direction is still in its early stages, it is clear that this plays an important role.

The use of behavioral assumptions as an alternative to utility maximization is controversial. Unlike utility, behavioral assumptions have the advantage of being directly observable, and in many cases the degree to which they are followed can be confirmed empirically. The disadvantage of this approach is that behavior may be context dependent, and as a result, such models typically fail the Lucas critique. We will show examples here where models based on behavioral assumptions are nonetheless very useful because they make it possible to directly investigate the consequences of a given set of behaviors. We will show examples where it leads to simple models that make clear predictions, at the same time that it can potentially be extended to complex real world situations.

This review will focus primarily on the simulation approach, though we will attempt to discuss key influences and interactions with the more traditional equilibrium approach. Our view is that the two approaches are complements rather than substitutes. The most appropriate approach depends on the context and the goals of the modeling exercise. We predict that the simulation approach will become increasingly important with time, for several reasons. One is that this approach can be easier to bring to the data, and data is becoming more readily available. Many central banks are beginning to collect comprehensive data sets that make it possible to monitor the key parts of the financial system. This makes it easier to test the realism of behavioral assumptions, making such models less ad hoc. With such models it is potentially feasible to match the models to the data in a literal, one-to-one manner. This has not yet been done, but it is on the horizon, and if successful such models may become valuable tools for assessing and monitoring financial stability, and for policy testing. In addition, computational power is always improving. This is a new area of pursuit and the computational techniques and software are rapidly improving.

The actors in the financial system are highly interconnected, and as a consequence network dynamics plays a key role in determining financial stability. The distress of one institution can propagate to other institutions, a process that is often called contagion, based on the analogy to disease. There are multiple channels of contagion, including counterparty risk, funding risk, and common assets holdings. Counterparty risk is caused by the web of bilateral contracts, which make one institution's assets another's liabilities. When a borrower is unable to pay, the lender's balance sheet is affected, and the resulting financial distress may in turn be transmitted to other parties, causing them to come under stress or default. Funding risk occurs when a lender comes under stress, which may create problems for parties that routinely borrow from this lender because loans that they would normally expect to receive fail to be extended. Institutions are also connected in many indirect ways, e.g. by common asset holdings, also called overlapping portfolios. If an institution comes under stress and sells assets, this depresses prices, which can cause further selling, etc. There are of course other channels of contagion, such as common information, that can affect expectations and interact with the more mechanical channels described above.

These channels of contagion cause nonlinear interactions that can create positive feedback loops that amplify external shocks or even generate purely endogenous dynamics, such as booms and busts. Nonlinear feedback loops can also be amplified by behavioral and institutional constraints and by bounded rationality (often in the context of incomplete information and learning).

Behavioral and institutional constraints force agents to take actions that they would prefer to avoid in the absence of the constraint. Such behavioral constraints can be imposed by a regulator but they can also result from bilateral contracts between private institutions. In principle, regulatory constraints, such as capital or liquidity coverage ratios, are designed to increase financial stability. In many cases however, these constraints are designed to increase the resilience of an individual financial institution to idiosyncratic shocks rather than the resilience of the system as a whole. Take the example of a leverage constraint. If a financial institution has high leverage, a small shock may be enough to push it into insolvency. Hence, from a regulatory perspective, a cap on leverage seems like a good idea. However, as we will discuss below, a leverage constraint may have the adverse side effect that it forces distressed institutions to sell into falling asset markets, causing prices to fall further and amplifying a crisis. Of course, leverage constraints are needed, but the point is that their effects can go far beyond the failure of individual institutions, and the way in which they are enforced can make a big difference. Similar positive feedback can result from other behavioral constraints as well.

This brings up the distinction between microprudential regulation, which is designed to benefit individual institutions without considering the effect on the system as a whole, vs. macroprudential regulation, which is designed to take systemic effects into account. These can come into dramatic conflict. For example, we will discuss the base of Basel II, which provided perfectly sensible rules for risk management from a microprudential point of view, but which likely caused substantial systemic risk from a macroprudential point of view, and indeed may have been a major driver of the crisis of 2008. It is ironic that prudent behavior of an individual can cause such significant problems for society as a whole.

Rational agents with complete information might be able to navigate the risks inherent to the financial system. Indeed, optimal behavior might well mitigate the positive feedback resulting from interconnectedness and behavioral constraints. However, we believe that optimal behavior in the financial system is rare. Instead, agents are restricted by bounded rationality. Their limited understanding of the system in which they operate forces agents to rely on simple rules as well as biased methods to learn about the state of the system and form expectations about its future states (Farmer, 2002; Lo, 2005). Suboptimal decisions and biased expectations can exacerbate the destabilizing effects of interconnectedness and behavioral constraints but can also lead to financial instability on their own.

The remainder of this paper is organized as follows: In Section 2 we briefly contrast and compare traditional equilibrium models with agent-based models. In Section 3 we introduce the dynamical systems perspective on the financial system that will underlie many of the models of financial stability that we discuss in subsequent sections. In Sections 4 and 5 we discuss models of systemic risk resulting from leverage constraints and models of financial contagion due to interconnectedness, respectively. Sections 6 to 9 consider various different stress tests. In particular, Section 6 gives a brief conceptual overview of stress tests; Section 7 introduces and critically evaluates standard, micro-prudential stress tests; Section 8 discusses examples of macroprudential stress tests and how to bring them to data; finally Section 9 outlines a vision for the next generation of system-wide stress tests.

2 Two Approaches to Modeling Systemic Risk

As mentioned in the introduction, traditionally finance has focused on modeling systemic risk in highly stylized models that are analytically tractable. These efforts have improved our understanding of a wide range of phenomena related to systemic risk ranging from bank runs (Diamond and Dybvig, 1983; Morris and Shin, 2001), credit cycles (Kiyotaki and Moore, 1997; Brunnermeier and Sannikov, 2014), balance sheet (Allen and Gale, 2000), and information contagion (Acharya and Yorulmazer, 2008) over fire sales (Shleifer and Vishny, 1992), to the feedback between market and funding liquidity (Brunnermeier and Pedersen, 2009). A comprehensive review that does justice to this literature is beyond the scope of this paper. However, we would like to make a few observations in regard to the traditional modeling approach and contrast it with the agent-based approach.

Traditional models place great emphasis on the incentives and information structure of agents in a financial market. Given those, agents behave strategically, taking into account their beliefs about the state of the world, and other agents' strategies. The objects of interest are then the game theoretic equilibria of this interaction. This allows for studying the effects of properties such as asymmetric information, uncertainty or moral hazard on the stability of the financial system. While these models provide valuable qualitative insights, they are typically only tractable in very stylized settings. Models are usually restricted to a small number or a continuum of agents, a few time periods and a drastically simplified institutional and market set up. This can make it difficult to draw quantitative conclusions from such models.

Agent-based models typically place less emphasis on incentives and information, and instead focus on how the dynamic interactions of behaviorally simple agents can lead to complex aggregate phenomena, such as financial crises, and how outcomes are shaped by the structure of this interaction and the heterogeneity of agents. From this perspective, the key drivers of systemic risk are the amplification of dynamic instabilities and contagion processes in financial markets. Complicated strategic interactions and incentives are often ignored in favor of simple, empirically motivated behavioral rules and a more realistic institutional and market set up. Since these models can easily be simulated numerically, they can in principle be scaled to a large number of agents and, if appropriately calibrated, can yield quantitative insights.

Two common criticisms leveled against heterogeneous agent-based models are the lack of strategic interactions and the reliance on computer simulations. The first criticism is fair and, in many cases, highlights an important shortcoming of this approach. Hard wired behavioral rules need to be carefully calibrated against real data, and even when they are, they can fail in new situations where the behavior of agents may change. For computer simulations to be credible, their parameters need to be calibrated and the sensitivity of outcomes to those parameters needs to be understood. The latter in particular is more challenging in computational models than in tractable analytical models.

In our view, what is not fair is to regard computer simulations as inherently inferior to analytic results. Analytic models have the benefit of the relative ease with which they can be used to understand the concepts driving structural cause-and-effect relationships. But many aspects of the economic world are not simple, and in most realistic situations computer simulations are the only possibility. Good practice is to make code freely available and well documented, so that results are easily reproducible.

Traditional and heterogeneous agent-based models are complements rather than substitutes. Some heterogeneous agent-based models already use myopic optimization, and in the future the line between the two may become increasingly blurred.4 As methods such as computational game theory or multi-agent reinforcement learning mature, it may become possible to increasingly introduce strategic interactions into computational heterogeneous agent-based models. Furthermore, as computational resources and large volumes of data on the financial system become more accessible, parameter exploration and calibration should become increasingly feasible. Therefore, we are optimistic that, provided technology progresses as expected,5 in the future heterogeneous agent-based models will be able to overcome some of the shortcomings discussed above. And as we demonstrate here, they have already led to important new results in this field, that were not obtainable via analytic methods.

3 A View of the Financial System

At a high level, it is useful to think of the financial system as a dynamical system that consists of a collection of institutions that interact via centralized and bilateral markets. An institution can be represented by its balance sheet, i.e. its assets and liabilities, together with a set of decision rules that it deploys to control the state of its balance sheet in order to achieve a certain goal. Within this framework, a market can be thought of as a mechanism that takes actions from institutions as inputs and changes the state of their balance sheets based on its internal dynamics. Anyone wishing to construct an agent model of the financial system therefore has to answer three fundamental questions: (i) what comprises the institutions' balance sheets, (ii) what determines their actions conditional on the state of the world, and (iii) how do markets respond to these actions? In the following, we will sketch the balance sheet of a generic leveraged investor, which will serve as the fundamental building block of the models of financial stability that we will discuss in this review. We will also briefly touch on (ii) and (iii) when discussing the important channels through which leveraged investors interact. In the subsequent sections we will then discuss concrete models of financial stability that fall within this general framework.

3.1 Balance Sheet Composition

When developing a model of a financial system, it is useful to distinguish between two types of agents which we refer to as “active” and “passive” agents. Active agents are the objects of interest and their internal state and interactions are carefully modeled. Passive agents represent parts of the financial system that interact with active agents but are not the focus of the model, and are therefore typically represented by simple stochastic processes. For the remainder of this review, consider a financial system that consists of a set ![]() of active leveraged investors and a set of passive agents which will remain unspecified for now. We are particularly interested in systemic risk that is driven by borrowing, and thus we focus on agents that use leverage (defined as purchasing assets with borrowed funds). However, the setup below is sufficiently general to accommodate unleveraged investors as a special case with leverage equal to one.

of active leveraged investors and a set of passive agents which will remain unspecified for now. We are particularly interested in systemic risk that is driven by borrowing, and thus we focus on agents that use leverage (defined as purchasing assets with borrowed funds). However, the setup below is sufficiently general to accommodate unleveraged investors as a special case with leverage equal to one.

Leveraged investors need not be homogeneous and may differ, among other aspects, in their balance sheet composition, strategies or counterparties. In practice, a leveraged investor might be a bank or a leveraged hedge fund and other active investors might include unleveraged mutual funds. Passive agents could be depositors, noise traders, fund investors that generate investment flows or banks that lend to hedge funds. The choice of active vs. passive investors of course varies from model to model.

The balance sheet of an investor ![]() is composed of assets

is composed of assets ![]() , liabilities

, liabilities ![]() , and equity

, and equity ![]() , such that

, such that ![]() . The investor's leverage is simply the ratio of assets to equity

. The investor's leverage is simply the ratio of assets to equity ![]() . It is useful to decompose the investor's assets into three classes: bilateral contracts

. It is useful to decompose the investor's assets into three classes: bilateral contracts ![]() between investors, such as loans or derivative exposures; traded securities

between investors, such as loans or derivative exposures; traded securities ![]() , such as stocks; and external assets

, such as stocks; and external assets ![]() , whose value is assumed exogenous. Throughout this review, we assume that the value

, whose value is assumed exogenous. Throughout this review, we assume that the value ![]() of traded securities is marked to market.6 That is, the value of a traded security on the investor's balance sheet will be determined by its current market price. Of course we must have that

of traded securities is marked to market.6 That is, the value of a traded security on the investor's balance sheet will be determined by its current market price. Of course we must have that ![]() . Each asset class can be further decomposed into individual loan contracts, stock holdings and so on.

. Each asset class can be further decomposed into individual loan contracts, stock holdings and so on.

The investor's liabilities can be decomposed in a similar fashion. For now, let us decompose the investor's liabilities simply into bilateral contracts ![]() between investors, such as loans or derivative exposures, and external liabilities

between investors, such as loans or derivative exposures, and external liabilities ![]() which can be assumed exogenous. In the case of a bank, these external liabilities might be deposits. Again we must have that

which can be assumed exogenous. In the case of a bank, these external liabilities might be deposits. Again we must have that ![]() , and bilateral liabilities can be further decomposed into individual bilateral contracts. Bilateral assets and liabilities might be secured, such as repurchase agreements, or unsecured such as interbank loans. Naturally, bilateral liabilities are just the flip side of bilateral assets such that summing over all investors we must have

, and bilateral liabilities can be further decomposed into individual bilateral contracts. Bilateral assets and liabilities might be secured, such as repurchase agreements, or unsecured such as interbank loans. Naturally, bilateral liabilities are just the flip side of bilateral assets such that summing over all investors we must have ![]() .

.

3.2 Balance Sheet Dynamics

Of all the factors that affect the dynamics of the investors' balance sheets, three are of particular importance for financial stability: leverage, liquidity, and interconnectedness. Below, we discuss each factor in turn.

Leverage: Leverage amplifies returns, both positive and negative. Therefore, investors typically face a leverage constraint to limit the investors' risk.7 However, at the level of the financial system, binding leverage constraints can lead to substantial instabilities. On short time scales, a leveraged investor may be forced to sell into falling markets when she exceeds her leverage constraint. Her sales will in turn depress prices further as we explain in the next paragraph on market liquidity. Leverage constraints can thus lead to an unstable feedback loop between falling prices and forced sales. On longer time scales dynamic leverage constraints that depend on backward looking risk estimates can lead to entirely endogenous volatility – so called leverage cycles.8

Liquidity: Broadly speaking, one can distinguish between two types of liquidity: market liquidity and funding liquidity.

Market liquidity can be understood as the inverse to price impact. When market liquidity is high, the market can absorb large sell orders without large changes in the price. If markets were perfectly liquid it would always be possible to sell assets without affecting prices and most forms of systemic risk would not exist.9 Leverage is dangerous both because it directly increases risk, amplifying gains and losses proportionally, but also because the market impact of liquidating a portfolio to achieve a certain leverage increases with leverage. This point was stressed by Caccioli et al. (2012a), who showed how, due to her own market impact, an investor with a large leveraged position can easily drive herself bankrupt by liquidating her position. They showed that this can be a serious problem even under normal market conditions, and recommended taking market impact into account when valuing portfolios in order to reduce this problem. The problem can become even worse if investors are forced to sell too quickly, inducing fire sales in which a market is overloaded with sell orders, causing a dramatic decrease in liquidity for sellers.10 Fire sales can be induced when investors hit leverage constraints, forcing them to sell, which in turn causes leverage constraints to be more strongly broken, inducing more selling.

Funding liquidity refers to the ease with which investors can borrow to fund their balance sheets. When funding liquidity is high, investors can easily roll over their existing liabilities by borrowing again, or even expand their balance sheets. In times of crises, funding liquidity can drop dramatically. If investors rely on short term liabilities they may be forced to liquidate a large part of their assets to pay back their liabilities. This forced sale can trigger fire sales by other investors.

Interconnectedness: Investors are connected via their balance sheets and so are not isolated agents. Connections can result from direct exposures due to bilateral loan contracts, or from indirect exposures due to investments into the same assets. Interconnectedness together with feedback loops resulting from binding leverage constraints and endogenous liquidity can lead to financial contagion. In analogy to epidemiology, financial contagion refers to the process by which “distress” may spread from one investor to another, where distress can be broadly understood as an investor becoming uncomfortably close to insolvency or illiquidity. Typically financial contagion arises when, via some mechanism or channel, a distressed investor's actions negatively affect some subset of other investors. This subset of investors is said to be connected to the distressed investor. A simple example of such connections are the bilateral liabilities between investors. Taken together, the set of all such connections form a network over which financial contagion can spread. For an in-depth review of financial networks see Iori and Mantegna (2018).

The aim of the subsequent sections is to introduce the reader to a number of models that tackle the effect of leverage, liquidity and interconnectedness on financial stability in isolation. These models then form the building blocks of more comprehensive models discussed in Section 6. Below, in Section 4, we first focus on the potentially destabilizing effects of leverage as they form the basis of fire sale models discussed later, and because they are thought to have contributed to the build up of risk prior to the great financial crisis. In Section 5 we then proceed to models of financial contagion as they form the scientific bedrock of the stress testing models that will be discussed in Section 6 and beyond. While liquidity is of great importance, we will only discuss it implicitly in Sections 4 and 5, rather than dedicating a separate section to it. This is because, unfortunately, there are currently only few dedicated models on this topic, see Bookstaber and Paddrik (2015) for an example. We will not be able to provide a complete overview of the agent-based modeling literature devoted to various aspects of financial stability. Important topics that we will not be able to discuss include the role of heterogeneous expectations or time scales in the dynamics of financial markets, see for example Hommes (2006), LeBaron (2006) for early surveys, and Dieci and He (2018) for a recent overview.

4 Leverage and Endogenous Dynamics in a Financial System

4.1 Leverage and Balance Sheet Mechanics

Many financial institutions borrow and invest the borrowed funds into risky assets. Three simple properties of leverage are worth noting at this point. First, ceteris paribus, leverage determines the size of the investor's balance sheet. Second, leverage boosts asset returns. Third, leverage increases when the investor incurs losses, again ceteris paribus. In the following, we discuss each property in turn. For a fixed amount of equity, an investor can only increase the size of its balance sheet by increasing its leverage. Further, it is easy to show that, if ![]() is the asset return, the equity return is

is the asset return, the equity return is ![]() , where, as above, λ is the investor's leverage. In good times, leverage thus allows an investor to boost its return. In bad times however, even small negative asset returns can drive the investor into bankruptcy provided leverage is sufficiently high. Given the potential risks associated with high leverage, an investor typically faces a leverage limit which may be imposed by a regulator, as is the case for banks, or by creditors via a haircut11 on collateralized debt. Finally, why does leverage increase when the investor incurs losses? Suppose the investor holds S units of a risky asset at price p such that

, where, as above, λ is the investor's leverage. In good times, leverage thus allows an investor to boost its return. In bad times however, even small negative asset returns can drive the investor into bankruptcy provided leverage is sufficiently high. Given the potential risks associated with high leverage, an investor typically faces a leverage limit which may be imposed by a regulator, as is the case for banks, or by creditors via a haircut11 on collateralized debt. Finally, why does leverage increase when the investor incurs losses? Suppose the investor holds S units of a risky asset at price p such that ![]() . Holding the investor's liabilities fixed, it is easy to see that

. Holding the investor's liabilities fixed, it is easy to see that ![]() implies

implies ![]() . In other words, whenever an investor is leveraged (

. In other words, whenever an investor is leveraged (![]() ), a decrease (increase) in asset prices leads to an increase (decrease) in its leverage.

), a decrease (increase) in asset prices leads to an increase (decrease) in its leverage.

In what follows, we discuss how these three properties of leverage, in combination with reasonable assumptions about investor behavior, can lead to financial instability. We begin by discussing how leverage constraints can force investors to sell into falling markets even if they would prefer to buy in the absence of leverage constraints. We then show how a leverage constraint based on a backward looking estimator of market risk can lead to endogenous volatility and leverage cycles.

4.2 Leverage Constraints and Margin Calls

Consider again the simple investor discussed above. Suppose the investor faces a leverage constraint ![]() and has leverage

and has leverage ![]() .12 The investor has to decide on an action at time

.12 The investor has to decide on an action at time ![]() to ensure that it does not violate its leverage constraint at time t. Suppose the investor expects the price of the risky asset to drop sufficiently from one period to the next, such that its leverage is pushed beyond its limit, i.e.

to ensure that it does not violate its leverage constraint at time t. Suppose the investor expects the price of the risky asset to drop sufficiently from one period to the next, such that its leverage is pushed beyond its limit, i.e. ![]() . In this situation the investor has two options to decrease its leverage: raise equity or reduce its assets (or some combination of the two). Raising equity can be time consuming or even impossible during a financial crisis. Therefore, if the leverage constraint has to be satisfied quickly or if new equity is not available and no assets are maturing in the next period, the investor has to sell at least

. In this situation the investor has two options to decrease its leverage: raise equity or reduce its assets (or some combination of the two). Raising equity can be time consuming or even impossible during a financial crisis. Therefore, if the leverage constraint has to be satisfied quickly or if new equity is not available and no assets are maturing in the next period, the investor has to sell at least ![]() of its assets to satisfy its leverage constraint, where

of its assets to satisfy its leverage constraint, where ![]() is the conditional expectation at time t. In the following we will set

is the conditional expectation at time t. In the following we will set ![]() and

and ![]() . This can be done for simplicity or because a contract forces the investor to make adjustments based on current rather than expected values. In this case we have simply

. This can be done for simplicity or because a contract forces the investor to make adjustments based on current rather than expected values. In this case we have simply ![]() . If

. If ![]() exceeds the leverage limit due to a drop in prices, the investor will sell into falling markets which may lead to a feedback loop between leverage and falling prices as outlined in the previous section.

exceeds the leverage limit due to a drop in prices, the investor will sell into falling markets which may lead to a feedback loop between leverage and falling prices as outlined in the previous section.

This simple mechanism has been discussed by a number of authors, see for example Gennotte and Leland (1990), Geanakoplos (2010), Thurner et al. (2012), Shleifer and Vishny (1997), Gromb and Vayanos (2002), Fostel and Geanakoplos (2008). Gorton and Metrick (2012) study the effect of haircuts on repo markets during the financial crisis empirically. Thurner et al. (2012) incorporate this mechanism in a heterogeneous agent model of leverage-constrained value investors. In the remainder of this section we will introduce their model and discuss some of the quantitative results they obtain for the effect of leverage constraints on asset returns.

Consider our set ![]() of leveraged investors introduced in Section 3. Suppose that investors have no bilateral assets or liabilities and only invest into a single traded security, i.e.

of leveraged investors introduced in Section 3. Suppose that investors have no bilateral assets or liabilities and only invest into a single traded security, i.e. ![]() . Furthermore, assume that the investor has access to a credit line from an unmodeled bank such that

. Furthermore, assume that the investor has access to a credit line from an unmodeled bank such that ![]() . For brevity and to guide intuition, we will refer to these leveraged investors as funds for the remainder of this section. In addition to the funds, there is a representative noise trader and a representative “fund investor” that allocates capital to the funds. There is an asset of supply N with fundamental value V that is traded by the funds and the noise trader at discrete points in time

. For brevity and to guide intuition, we will refer to these leveraged investors as funds for the remainder of this section. In addition to the funds, there is a representative noise trader and a representative “fund investor” that allocates capital to the funds. There is an asset of supply N with fundamental value V that is traded by the funds and the noise trader at discrete points in time ![]() . Every period a fund i takes a long position

. Every period a fund i takes a long position ![]() provided its equity satisfies

provided its equity satisfies ![]() . The fund's leverage is given by the heuristic

. The fund's leverage is given by the heuristic

where ![]() is the mispricing signal and

is the mispricing signal and ![]() is the fund's aggressiveness. In other words, the fund goes long in the asset if the asset is underpriced relative to its fundamental value V. The noise trader's long position follows a transformed AR(1) process with normally distributed innovations. The price of the asset is determined by market clearing. Every period, the fund investor adjusts its capital allocation to the funds, withdrawing capital from poorly performing funds and investing into successful funds relative to an exogenous benchmark return.

is the fund's aggressiveness. In other words, the fund goes long in the asset if the asset is underpriced relative to its fundamental value V. The noise trader's long position follows a transformed AR(1) process with normally distributed innovations. The price of the asset is determined by market clearing. Every period, the fund investor adjusts its capital allocation to the funds, withdrawing capital from poorly performing funds and investing into successful funds relative to an exogenous benchmark return.

Before considering the dynamics of the full model, let us briefly discuss the limit where the funds are small, i.e. ![]() . In this case, in the absence of any significant effect of the funds, log price returns will be approximately iid normal due to the action of the noise trader. This serves as a benchmark. The authors then calibrate the parameters of the model such that funds are significant in size and prices may deviate substantially from fundamentals. This corresponds to a regime where arbitrage is limited as in Shleifer and Vishny (1997). The authors also assume that funds differ substantially in their aggressiveness

. In this case, in the absence of any significant effect of the funds, log price returns will be approximately iid normal due to the action of the noise trader. This serves as a benchmark. The authors then calibrate the parameters of the model such that funds are significant in size and prices may deviate substantially from fundamentals. This corresponds to a regime where arbitrage is limited as in Shleifer and Vishny (1997). The authors also assume that funds differ substantially in their aggressiveness ![]() but share the same leverage constraint

but share the same leverage constraint ![]() and initial equity

and initial equity ![]() .

.

In this setting the funds' leverage and wealth dynamics can lead to a number of interesting phenomena. When the noise trader's demand drives the price below the asset's fundamental value, funds will enter the market in proportion to their aggressiveness ![]() . Due to the built-in tendency of the price to revert to its fundamental value due to the action of the noise traders, these trades will be profitable for the funds on average and even more profitable for more aggressive funds. Hence, the equity of aggressive funds grows quicker due to a combination of profits and capital reallocation of the fund investor. Importantly, as the equity of funds grows, their influence on prices increases and the volatility of the price decreases, due to the fact that they buy into falling markets and sell into rising markets.

. Due to the built-in tendency of the price to revert to its fundamental value due to the action of the noise traders, these trades will be profitable for the funds on average and even more profitable for more aggressive funds. Hence, the equity of aggressive funds grows quicker due to a combination of profits and capital reallocation of the fund investor. Importantly, as the equity of funds grows, their influence on prices increases and the volatility of the price decreases, due to the fact that they buy into falling markets and sell into rising markets.

Aggressive funds are also more likely to leverage to their maximum. Consider an aggressive fund i that has chosen ![]() . Now suppose the price drops such that

. Now suppose the price drops such that ![]() . In response the fund sells parts of its assets as outlined above. Thurner et al. (2012) refer to this forced selling as a margin call, as they interpret the leverage constraint as arising from a haircut on a collateralized loan. Recall that the amount the fund will sell is

. In response the fund sells parts of its assets as outlined above. Thurner et al. (2012) refer to this forced selling as a margin call, as they interpret the leverage constraint as arising from a haircut on a collateralized loan. Recall that the amount the fund will sell is ![]() , i.e. it is proportional to the fund's equity. As the aggressive fund is likely also the most wealthy fund, its selling can be expected to lead to a significant drop in prices. This drop may push other, less aggressive funds past their leverage limits. A margin spiral ensues in which more and more funds are forced to sell into falling markets. In an extreme outcome, most funds will exit or will have lost most of their equity in the price crash. As a result, their impact on prices is limited and the price is dominated by the noise trader. Thus following a margin spiral, price volatility increases due to two forces. First, it spikes due to the immediate impact of the price collapse. But then, it remains at an elevated level due to lack of value investors that push the price toward its fundamental value. These dynamics, which are illustrated in Fig. 1, reproduce some important features of financial time series in a reasonably quantitative way, in particular fat tails in the distribution of returns and clustered volatility (cf. Cont, 2001), as well as a realistic volatility dynamics profile before and after shocks (Poledna et al., 2014). These are difficult to reproduce in standard models.

, i.e. it is proportional to the fund's equity. As the aggressive fund is likely also the most wealthy fund, its selling can be expected to lead to a significant drop in prices. This drop may push other, less aggressive funds past their leverage limits. A margin spiral ensues in which more and more funds are forced to sell into falling markets. In an extreme outcome, most funds will exit or will have lost most of their equity in the price crash. As a result, their impact on prices is limited and the price is dominated by the noise trader. Thus following a margin spiral, price volatility increases due to two forces. First, it spikes due to the immediate impact of the price collapse. But then, it remains at an elevated level due to lack of value investors that push the price toward its fundamental value. These dynamics, which are illustrated in Fig. 1, reproduce some important features of financial time series in a reasonably quantitative way, in particular fat tails in the distribution of returns and clustered volatility (cf. Cont, 2001), as well as a realistic volatility dynamics profile before and after shocks (Poledna et al., 2014). These are difficult to reproduce in standard models.

One would expect these dynamics to be less drastic if funds took precautions against margin calls and stayed some ![]() below their maximum leverage allowing them to more smoothly adjust to price shocks. However, it is important to note that a single “renegade” fund that pushes its leverage limit while all other funds remain well below it can be sufficient to cause a margin spiral.

below their maximum leverage allowing them to more smoothly adjust to price shocks. However, it is important to note that a single “renegade” fund that pushes its leverage limit while all other funds remain well below it can be sufficient to cause a margin spiral.

It should be noted that the deleveraging schedule ![]() that a fund follows can depend on how the leverage constraint is implemented. In Thurner et al. (2012), the leverage constraint results from a haircut applied to a collateralized loan, i.e. the fund obtains a short term loan from a bank, purchases the asset with the loan and its equity and then posts the asset as collateral for the loan. The haircut is equivalent to leverage and determines how much of its assets the fund can finance via borrowing. When the value of the asset drops, the bank will make a margin call as outlined above and the fund will have to sell assets immediately. However, a leverage constraint can, for example, also be imposed by a regulator. In this case, the fund may be allowed to violate the leverage constraint for a few time steps while smoothly adjusting to satisfy the constraint in later periods. Such an implementation will increase the stability of the system. Finally, the schedule

that a fund follows can depend on how the leverage constraint is implemented. In Thurner et al. (2012), the leverage constraint results from a haircut applied to a collateralized loan, i.e. the fund obtains a short term loan from a bank, purchases the asset with the loan and its equity and then posts the asset as collateral for the loan. The haircut is equivalent to leverage and determines how much of its assets the fund can finance via borrowing. When the value of the asset drops, the bank will make a margin call as outlined above and the fund will have to sell assets immediately. However, a leverage constraint can, for example, also be imposed by a regulator. In this case, the fund may be allowed to violate the leverage constraint for a few time steps while smoothly adjusting to satisfy the constraint in later periods. Such an implementation will increase the stability of the system. Finally, the schedule ![]() assumes the price remains unchanged from the current to the next period. A more sophisticated fund might take its own price impact into account when determining the deleveraging schedule.

assumes the price remains unchanged from the current to the next period. A more sophisticated fund might take its own price impact into account when determining the deleveraging schedule.

4.3 Procyclical Leverage and Leverage Cycles

In the model presented in the previous section, funds actively increase their leverage when the price falls until they reach a leverage limit. Of course, a variety of other leverage management policies are possible. In an effort to study leverage management policies, Adrian and Shin (2010) analyze how changes in leverage ![]() relate to changes in total assets

relate to changes in total assets ![]() (at mark-to-market prices) during the period 1963–2006 for three types of investors: households, commercial banks and security broker dealers (such as Goldman Sachs). Below we focus on households on one extreme and broker dealers on the other.

(at mark-to-market prices) during the period 1963–2006 for three types of investors: households, commercial banks and security broker dealers (such as Goldman Sachs). Below we focus on households on one extreme and broker dealers on the other.

For households and broker-dealers the authors find a distinct correlation between leverage and asset changes, see Fig. 2. For households, changes in leverage are negatively correlated to changes in assets: ![]() . For broker dealers they find a positive correlation

. For broker dealers they find a positive correlation ![]() . This points toward at least two distinct leverage management policies.

. This points toward at least two distinct leverage management policies.

Households appear to be passive investors since leverage decreases when assets appreciate, ceteris paribus. Broker-dealers however, appear to follow a state-contingent target leverage which they try to reach through balance sheet adjustments. To see this, suppose an investor has a leverage target which is high in good times and low in bad times. Let us say that good times are identified by increasing asset prices while bad times are identified by falling asset prices (there are other ways of identifying the state of the world as we will discuss below). In this case, in response to an increase (decrease) in the price of the asset, the investor will increase (decrease) its target leverage and adjust its balance sheet accordingly. Importantly, the leverage adjustment often occurs via debt and asset adjustment rather than equity adjustment. Adrian and Shin (2010) call this a procyclical leverage policy. With such a leverage policy we expect ![]() . Hence, it appears that broker-dealers follow a procyclical leverage policy.

. Hence, it appears that broker-dealers follow a procyclical leverage policy.

A procyclical leverage policy could arise if the broker-dealers face a time varying leverage constraint and choose to leverage maximally. In fact, Adrian and Shin (2010), Danıelsson et al. (2004), and others show that a time varying leverage constraint arises when the investor faces a Value-at-Risk (VaR) constraint as was required under the Basel II regulatory framework. As we will show below, the effect of a VaR constraint is that the investor faces a leverage constraint that is inversely proportional to market risk. Thus, when market risk is high (low), the leverage constraint is low (high). In this setting the level of risk identifies the state of the world: in good times risk is low, while in bad times risk is high.

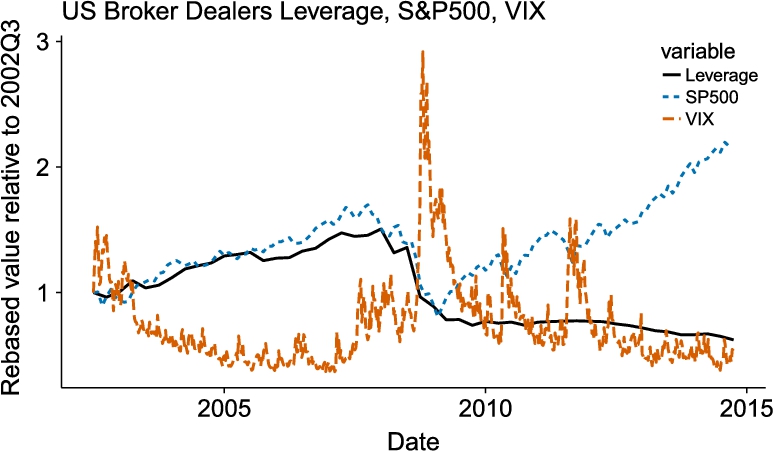

In summary, two leverage management policies are borne out by the data: passive leverage and procyclical target leverage. The type of leverage management policy used by the investor can have significant implications for financial stability. Indeed, at least anecdotally, the time series of broker-dealer leverage,13 perceived risk (as measured by the VIX) and asset prices (as measured by the S&P500) in Fig. 3 suggests a relationship between these three variables that is potentially induced by the dealers' procyclical leverage policy. In the following, we will introduce a model developed by Aymanns and Farmer (2015) that links leverage, perceived risk and asset prices in order to illustrate the effect of procyclical leverage and VaR constraints on the dynamics of asset prices.

Consider again our set ![]() of leveraged investors (banks for short) and a representative noise trader. As above, we assume that there are no bilateral assets or liabilities. There is a risk free asset (cash) and a set

of leveraged investors (banks for short) and a representative noise trader. As above, we assume that there are no bilateral assets or liabilities. There is a risk free asset (cash) and a set ![]() of risky assets that are traded by banks and the noise trader at discrete points in time

of risky assets that are traded by banks and the noise trader at discrete points in time ![]() . At the beginning of every period, the banks and the noise trader determine their demand for the assets. For this, each bank i picks a vector

. At the beginning of every period, the banks and the noise trader determine their demand for the assets. For this, each bank i picks a vector ![]() of portfolio weights and is assigned a target leverage

of portfolio weights and is assigned a target leverage ![]() . The noise trader is not leveraged and therefore only picks a vector

. The noise trader is not leveraged and therefore only picks a vector ![]() of portfolio weights. Once the agent's demand functions have been fixed, the markets for the risky assets clear which fixes prices. Given the new prices, banks choose their next period's balance sheet adjustment (buying or selling of assets) in order to hit their target leverage. We refer the reader to Aymanns and Farmer (2015) for a detailed description of the model.

of portfolio weights. Once the agent's demand functions have been fixed, the markets for the risky assets clear which fixes prices. Given the new prices, banks choose their next period's balance sheet adjustment (buying or selling of assets) in order to hit their target leverage. We refer the reader to Aymanns and Farmer (2015) for a detailed description of the model.

As mentioned above, banks are subject to a Value-at-Risk constraint.14 Here, a bank's VaR is the loss in market value of its portfolio over one period that is exceeded with probability ![]() , where a is the associated confidence level. The VaR constraint then requires that bank holds equity to cover these losses, i.e.

, where a is the associated confidence level. The VaR constraint then requires that bank holds equity to cover these losses, i.e. ![]() . We approximate the Value-at-Risk by

. We approximate the Value-at-Risk by ![]() , where

, where ![]() is the estimated portfolio variance of bank i and α is a parameter. This relation becomes exact for normal asset returns and an appropriately chosen α. Rearranging the VaR constraint yields the bank's leverage constraint

is the estimated portfolio variance of bank i and α is a parameter. This relation becomes exact for normal asset returns and an appropriately chosen α. Rearranging the VaR constraint yields the bank's leverage constraint ![]() . We assume that the bank chooses to be maximally leveraged, e.g. for profit motives. The leverage constraint is therefore equivalent to the target leverage we discussed above. To evaluate their VaR, banks compute their portfolio variance as an exponentially weighted moving average of past log returns.

. We assume that the bank chooses to be maximally leveraged, e.g. for profit motives. The leverage constraint is therefore equivalent to the target leverage we discussed above. To evaluate their VaR, banks compute their portfolio variance as an exponentially weighted moving average of past log returns.

Let us briefly discuss the implications of this set up. As mentioned at the outset of this section, banks follow a procyclical leverage policy. In particular, the banks' VaR constraint, together with its choice to be maximally leveraged at all times, imply a target leverage that is inversely proportional to the banks' perceived risk as measured by an exponentially weighted moving average of past squared returns. Why is such a leverage policy procyclical? Suppose a random drop in an asset's price causes an increase in the level of perceived risk of bank i. As a result the bank's target leverage will decrease (while its actual leverage simultaneously increases) and it will have to sell some of its assets, similar to the funds in the previous section.15 The banks selling may lead to a further drop in prices and a further increase in perceived risk. In other words, the bank's leverage policy together with its perception of risk can lead to an unstable feedback loop. It is in this sense that the leverage policy is procyclical.

Banks in this model have a very simple, yet realistic, method of computing perceived (or expected) risk. Similar backward looking methods are well established in practice, see for example Andersen et al. (2006). It is important to note that perceived risk ![]() and realized volatility over the next time step can be very different. Since banks have only bounded rationality and follow a simple backward looking rule in this model, their expectations about volatility are not necessarily correct on average and tend to lag behind realizations.

and realized volatility over the next time step can be very different. Since banks have only bounded rationality and follow a simple backward looking rule in this model, their expectations about volatility are not necessarily correct on average and tend to lag behind realizations.

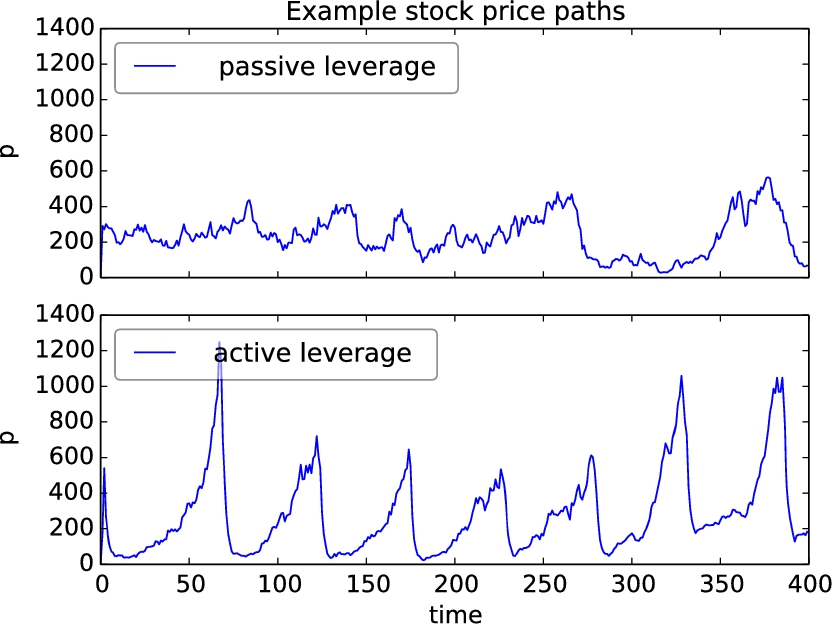

Let us now consider the dynamics of the model in more detail. In Fig. 4 we show two simulation paths (with the same random seed) of the price of a single risky asset for two leverage policy rules. In the top panel, banks behave like the households in Adrian and Shin (2010) – they are passive and do not adjust their leverage to changes in asset prices or perceived risk. In the bottom panel, banks follow the procyclical leverage policy outlined above. The difference between the two price paths is striking. In the case of passive banks, the price follows what appears to be a simple mean reverting random walk. However, when banks follow the procyclical leverage policy, the price trajectory shows stochastic, irregular cycles with a period of roughly 100 time steps. These complex, endogenous dynamics are the result of the unstable feedback loop outlined above.

Aymanns and Farmer (2015) refer to these cycles as leverage cycles. Leverage cycles are an example of endogenous volatility – volatility that arises not because of the arrival of exogenous information but due to the endogenous dynamics of the agents in the financial system. To better understand these dynamics, consider the state of the system just after a crash has occurred, e.g. at time ![]() . Following the crash, banks' perceived risk is high, their leverage is low and prices are stable. Over time, perceived risk declines and banks increase their leverage. As they increase their leverage, they buy more of the risky assets and push up their prices. At some point leverage is sufficiently high and perceived risk sufficiently low, so that a relatively small drop of the price of an asset leads to large downward correction in leverage. A crash follows and prices fall until the noise trader's action stops the crash and the cycle begins anew. Naturally, these dynamics depend on the choice of parameters. In particular, when the banks are small relative to the noise trader, banks' trading has no significant impact on asset prices and leverage cycles do not occur. For a detailed discussion of the sensitivity of the results to parameters see Aymanns and Farmer (2015), and for a more realistic model that is better calibrated to the data, see Aymanns et al. (2016).

. Following the crash, banks' perceived risk is high, their leverage is low and prices are stable. Over time, perceived risk declines and banks increase their leverage. As they increase their leverage, they buy more of the risky assets and push up their prices. At some point leverage is sufficiently high and perceived risk sufficiently low, so that a relatively small drop of the price of an asset leads to large downward correction in leverage. A crash follows and prices fall until the noise trader's action stops the crash and the cycle begins anew. Naturally, these dynamics depend on the choice of parameters. In particular, when the banks are small relative to the noise trader, banks' trading has no significant impact on asset prices and leverage cycles do not occur. For a detailed discussion of the sensitivity of the results to parameters see Aymanns and Farmer (2015), and for a more realistic model that is better calibrated to the data, see Aymanns et al. (2016).

These results show that simple behavioral rules, grounded in empirical evidence of bank behavior (Adrian and Shin, 2010; Andersen et al., 2006), can lead to remarkable and unexpected dynamics which bear some resemblance to the run up to and crash following the 2008 financial crises. The results originate from the agents' bounded rationality and their reliance on past returns to estimate their Value-at-Risk. These features would be absent in a traditional economic models in which agents are fully rational. Indeed, rational models rarely display the dynamic instabilities that Aymanns and Farmer (2015) observe. If we believe that real economic actors are rarely fully rational, we should take note of this result. Of course, the agents in this model are really quite dumb. For example, they do not adjust to the strong cyclical pattern in the time series. However, they also live in an economy that is significantly simpler than the real world. Thus, their level of rationality in relation to the complexity of the world they inhabit might not be too far off from real economic agents' level of rationality.

The model discussed above can also yield insights for policy makers on how bank risk management might be modified in order to mitigate the effects of the leverage cycle. Aymanns et al. (2016) present a reduced form version of the model outlined above in order to investigate the implications of alternative leverage policies on financial stability. They show that, depending on the size of the banking sector and the properties of the exogenous volatility process, either a constant leverage policy or a Value-at-Risk based leverage policy is optimal from the perspective of a social planner. This finding lends support to the use of macroprudential leverage ratios as discussed in ESRB (2015). The authors also show that the timescale for the bubbles and crashes observed in the model is around 10–15 years, roughly corresponding to the run-up to the 2008 crash. Another important insight from Aymanns et al. (2016) is that the time scale on which investors need to achieve their leverage constraint plays a crucial role in the stability of the financial system: slower adjustment toward the constraint (corresponding to more slackness) increases stability.

The effect of leverage targeting on asset price dynamics has also been studied by other others in the multi-asset case. For example, Capponi and Larsson (2015) show that the deleveraging of banks may amplify asset return shocks and lead to large fluctuations in realized returns which in turn can cause spillover effects between different assets.

5 Contagion in Financial Networks

5.1 Financial Linkages and Channels of Contagion

A channel of contagion is a mechanism by which distress can spread from one financial institution to another.16 Often the channel of contagion is such that distress can only spread from one institution to a subset of all institutions in the system. These susceptible institutions are said to be linked to the stressed institution. The set of all links then forms a financial network associated with the channel of contagion.17 Depending on the channel, links in this network may arise directly from bilateral contracts between banks, such as loans, or indirectly via the markets in which the banks operate. In the literature, one typically distinguishes between three key channels of contagion: counterparty loss, overlapping portfolios, and funding liquidity contagion.18 Counterparty loss and overlapping portfolio contagion affect the value of the assets on the investors' balance sheet while funding liquidity contagion affects the availability of funding for the investors' balance sheets. In the following we will first introduce the investor's balance sheet relevant for this section. We will then give a brief overview of the channels of contagion before discussing each in more detail.

Balance sheet: Throughout this chapter we will consider a set ![]() of leveraged investors (banks for short) whose assets can be decomposed into three classes: bilateral interbank contracts

of leveraged investors (banks for short) whose assets can be decomposed into three classes: bilateral interbank contracts ![]() , traded securities

, traded securities ![]() that are marked to market and external, unmodeled assets

that are marked to market and external, unmodeled assets ![]() . Furthermore bank liabilities can be decomposed into bilateral interbank contracts

. Furthermore bank liabilities can be decomposed into bilateral interbank contracts ![]() , and external, unmodeled liabilities

, and external, unmodeled liabilities ![]() such that

such that ![]() . Note that bilateral interbank contracts need not be loans, they can also be derivative contracts for example. For simplicity however, we will think of bilateral interbank contracts as loans for the remainder of this section.

. Note that bilateral interbank contracts need not be loans, they can also be derivative contracts for example. For simplicity however, we will think of bilateral interbank contracts as loans for the remainder of this section.

Counterparty loss: Suppose bank i has lent an amount C to bank j such that ![]() . Now suppose the value of bank j's external assets

. Now suppose the value of bank j's external assets ![]() drops due to an exogenous shock. As a result the probability of default of bank j is likely to increase, which will affect the value of the claim

drops due to an exogenous shock. As a result the probability of default of bank j is likely to increase, which will affect the value of the claim ![]() that bank i holds on bank j. If bank i's interbank assets are marked to market, a change in bank j's probability of default will affect the market value of

that bank i holds on bank j. If bank i's interbank assets are marked to market, a change in bank j's probability of default will affect the market value of ![]() . In the worst case, if bank j defaults, bank i will only recover some fraction

. In the worst case, if bank j defaults, bank i will only recover some fraction ![]() of its initial claim

of its initial claim ![]() . If the loss of bank i exceeds its equity, i.e.

. If the loss of bank i exceeds its equity, i.e. ![]() , bank i will default as well.19 Now, how can this lead to financial contagion? To elaborate on the above stylized example, suppose that bank i in turn borrowed an amount C from another bank k such that

, bank i will default as well.19 Now, how can this lead to financial contagion? To elaborate on the above stylized example, suppose that bank i in turn borrowed an amount C from another bank k such that ![]() .20 In this scenario, it can be plausibly argued that an increase in the probability of default of j increases the probability of default of i which in turn increases the probability of default of k. If all banks mark their books to market, an initial shock to j can therefore end up affecting the value of the claim that bank k holds on bank i. Again, in the extreme scenario, the default of bank j may cause bank i to default which may cause bank k to default. This is the essence of counterparty loss contagion. Naturally, in a real financial system the structure of interbank liabilities will be much more complex than in the stylized example outlined above. However, the conceptual insights carry over: the financial network associated with the counterparty loss contagion channel is the network induced by the set of interbank liabilities.

.20 In this scenario, it can be plausibly argued that an increase in the probability of default of j increases the probability of default of i which in turn increases the probability of default of k. If all banks mark their books to market, an initial shock to j can therefore end up affecting the value of the claim that bank k holds on bank i. Again, in the extreme scenario, the default of bank j may cause bank i to default which may cause bank k to default. This is the essence of counterparty loss contagion. Naturally, in a real financial system the structure of interbank liabilities will be much more complex than in the stylized example outlined above. However, the conceptual insights carry over: the financial network associated with the counterparty loss contagion channel is the network induced by the set of interbank liabilities.

Overlapping portfolios: The overlapping portfolio channel is slightly more subtle. Suppose bank i and bank j have both invested an amount C in the same security l such that ![]() , where we have introduced the additional index to reference the security.21 Now, suppose the value of bank j's external assets

, where we have introduced the additional index to reference the security.21 Now, suppose the value of bank j's external assets ![]() drops due to some exogenous shock. How will bank j respond to this loss? In the extreme case, when the exogenous shock causes bank j's bankruptcy (

drops due to some exogenous shock. How will bank j respond to this loss? In the extreme case, when the exogenous shock causes bank j's bankruptcy (![]() ), the bank will liquidate its entire investment in the security in a fire sale. However, even if the bank does not go bankrupt, it may wish to liquidate some of its investment. This can occur for example when the bank faces a leverage constraint as discussed in Section 4. Bank j's selling is likely to have price impact. As a result, the market value of

), the bank will liquidate its entire investment in the security in a fire sale. However, even if the bank does not go bankrupt, it may wish to liquidate some of its investment. This can occur for example when the bank faces a leverage constraint as discussed in Section 4. Bank j's selling is likely to have price impact. As a result, the market value of ![]() will fall. If bank i also faces a leverage constraint, or even goes bankrupt following the fall in prices, it will liquidate part of its securities portfolio in response. How will this lead to contagion? Suppose that bank i also has invested an amount C into another security m and that another bank k has also invested into the same security, such that

will fall. If bank i also faces a leverage constraint, or even goes bankrupt following the fall in prices, it will liquidate part of its securities portfolio in response. How will this lead to contagion? Suppose that bank i also has invested an amount C into another security m and that another bank k has also invested into the same security, such that ![]() . If bank i liquidates across its entire portfolio, it will sell some of security m following a fall in the price of security l. The resulting price impact will then affect the balance sheet of bank k which was not connected to bank j via an interbank contract or a shared security. This is the essence of overlapping portfolio contagion. Banks are linked by the securities that they co-own and the fact that they liquidate with market impact across their entire portfolios. Empirical evidence from the 2007 Quant meltdown for this contagion channel has been provided in Khandani and Lo (2011).

. If bank i liquidates across its entire portfolio, it will sell some of security m following a fall in the price of security l. The resulting price impact will then affect the balance sheet of bank k which was not connected to bank j via an interbank contract or a shared security. This is the essence of overlapping portfolio contagion. Banks are linked by the securities that they co-own and the fact that they liquidate with market impact across their entire portfolios. Empirical evidence from the 2007 Quant meltdown for this contagion channel has been provided in Khandani and Lo (2011).

Funding liquidity contagion often occurs when a lender is stressed, and so often occurs in conjunction with overlapping portfolio contagion and counterparty loss contagion. To see this, let us reconsider the scenario we discussed for counterparty loss contagion. Suppose bank i has lent an amount C to bank j such that ![]() . As before, suppose the value of bank j's external assets

. As before, suppose the value of bank j's external assets ![]() drops due to some exogenous shock and as a result, the probability of default of bank j increases. Now, suppose that every T periods bank i can decide whether to roll over its loan to bank j. Further assume that bank i is bank j's only source of interbank funding and

drops due to some exogenous shock and as a result, the probability of default of bank j increases. Now, suppose that every T periods bank i can decide whether to roll over its loan to bank j. Further assume that bank i is bank j's only source of interbank funding and ![]() is fixed. Given bank j's increased default probability, bank i may choose not to roll over the loan at the next opportunity. Ignoring interest payments, if bank i does not roll over the loan, bank j will have to deliver an amount C to bank i. In the simplest case, bank j may choose not to roll over its own loans to other banks which in turn may decide against rolling over their loans. This is the essence of funding liquidity contagion. As for counterparty loss contagion, the associated financial network is induced by the set of interbank loans. Empirical evidence on the fragility of funding markets during the past financial crisis has been provided for example by Afonso et al. (2011) and Iyer and Peydro (2011). In a further complication, bank j may also choose to liquidate part of its securities portfolio in order to pay back its loan. Funding liquidity contagion can therefore lead to fire sales and overlapping portfolio contagion and vice versa. This interdependence of contagion channels makes the funding liquidity and overlapping portfolio contagion processes the most challenging from a modeling perspective.

is fixed. Given bank j's increased default probability, bank i may choose not to roll over the loan at the next opportunity. Ignoring interest payments, if bank i does not roll over the loan, bank j will have to deliver an amount C to bank i. In the simplest case, bank j may choose not to roll over its own loans to other banks which in turn may decide against rolling over their loans. This is the essence of funding liquidity contagion. As for counterparty loss contagion, the associated financial network is induced by the set of interbank loans. Empirical evidence on the fragility of funding markets during the past financial crisis has been provided for example by Afonso et al. (2011) and Iyer and Peydro (2011). In a further complication, bank j may also choose to liquidate part of its securities portfolio in order to pay back its loan. Funding liquidity contagion can therefore lead to fire sales and overlapping portfolio contagion and vice versa. This interdependence of contagion channels makes the funding liquidity and overlapping portfolio contagion processes the most challenging from a modeling perspective.

In the remainder of this section, we will discuss models for counterparty loss, overlapping portfolio and funding liquidity contagion, as well as models for the interaction of all three contagion channels.

5.2 Counterparty Loss Contagion

Let P denote the matrix of nominal interbank liabilities such that banks hold interbank assets ![]() , where T denotes the matrix transpose. In addition, banks hold external assets

, where T denotes the matrix transpose. In addition, banks hold external assets ![]() which can be liquidated at no cost. Banks have interbank liabilities

which can be liquidated at no cost. Banks have interbank liabilities ![]() only. Assume all interbank liabilities mature at the same time and have the same seniority. We further assume that all banks are solvent initially. There is only one time period. At the end of that period all liabilities mature, external assets are liquidated and banks pay back their loans if possible. Now suppose banks are subject to a shock

only. Assume all interbank liabilities mature at the same time and have the same seniority. We further assume that all banks are solvent initially. There is only one time period. At the end of that period all liabilities mature, external assets are liquidated and banks pay back their loans if possible. Now suppose banks are subject to a shock ![]() to the value of their external assets such that

to the value of their external assets such that ![]() . Given an exogenous shock, we can ask a number of questions. First, which loan payments are feasible given the exogenous shock? Second, which banks will default on their liabilities? And finally, how do the answers to the first two questions depend on the structure of the interbank liabilities P? There is a large literature that studies counterparty loss contagion in a set up similar to the above, including Eisenberg and Noe (2001), Gai and Kapadia (2010), May and Arinaminpathy (2010), Elliott et al. (2014), Acemoglu et al. (2015), Battiston et al. (2012), Amini et al. (2016), and Capponi et al. (2015). In the following, we will briefly introduce the seminal contribution by Eisenberg and Noe (2001), who provide a solution to the first two questions. We will then consider a number of extensions of Eisenberg and Noe (2001) and alternative approaches to addressing the above questions.

. Given an exogenous shock, we can ask a number of questions. First, which loan payments are feasible given the exogenous shock? Second, which banks will default on their liabilities? And finally, how do the answers to the first two questions depend on the structure of the interbank liabilities P? There is a large literature that studies counterparty loss contagion in a set up similar to the above, including Eisenberg and Noe (2001), Gai and Kapadia (2010), May and Arinaminpathy (2010), Elliott et al. (2014), Acemoglu et al. (2015), Battiston et al. (2012), Amini et al. (2016), and Capponi et al. (2015). In the following, we will briefly introduce the seminal contribution by Eisenberg and Noe (2001), who provide a solution to the first two questions. We will then consider a number of extensions of Eisenberg and Noe (2001) and alternative approaches to addressing the above questions.