Agent-Based Models for Market Impact and Volatility

Jean-Philippe Bouchaud Capital Fund Management, Paris, France, [email protected]

Abstract

Financial markets display a host of universal “stylized facts” begging for a scientific explanation: Excess volatility, fat tails, and clustered activity are well known and have been studied for many years. More microstructural stylized facts have recently emerged, for example the long memory of the order flow or the square-root dependence of impact on the volume of metaorders. Agent-based models are attempts to account for these stylized facts in a unified manner. Devising faithful microstructural ABMs would allow one to answer crucial questions, such as those related to market stability. Can large orders destabilize markets? Is HFT activity detrimental? Can destabilizing feedback loops be mitigated by adequate regulation? The present review paper summarizes recent work in that direction. We discuss in particular the Santa-Fe zero-intelligence model, which provides a very interesting benchmark, but suffers from important drawbacks as well, such as strong mean-reversion effects. One can enrich the Santa-Fe model as to reproduce both diffusive prices, and the square-root impact law. The underlying mechanism can be well understood in terms of a generic “reaction–diffusion” model for the dynamics of the liquidity, which can be solved analytically. Finally, we argue that the role of “information” is probably overstated in classical theories, while a picture based on a self-reflexive price-impacting order flow has many merits. The recent accumulation of microstructural stylized facts, allowing one to focus on the price formation mechanism, all but confirm that fundamental information plays a relatively minor role in the dynamics of financial markets, at least on short to medium time scales.

Keywords

Microstructure; Order flow; Impact; Agent-based models; Market stability

1 Introduction

Understanding why and how prices move is arguably one of the most important problems in financial economics. The “why” question is intimately related to the information content of prices and the efficiency of markets, and the “how” question is related to the issue of price impact, that has become one of the main theme of research in the recent years, both in academic circles and in trading houses. From a theoretical standpoint, price impact is the transmission belt that allows private information to be reflected by prices. But by the same token, it is also the very mechanism by which prices can be distorted, or even crash, under the influence of uninformed trades and/or fire-sale deleveraging. Price impact is also a cost for trading firms – in fact the dominant one when assets under management become substantial.

Now, the simplest guess is that price impact should be linear, i.e. proportional to the (signed) volume of a transaction. This is in fact the central result of the seminal microstructure model proposed by Kyle in 1985 (Kyle, 1985). This paper has had a profound influence on the field, with over 9500 citations as of November 2017. A linear impact model is at the core of many different studies, concerning for example optimal execution strategies, liquidity estimators, agent-based models, volatility models, etc.

Quite surprisingly, however, the last 20 years have witnessed mounting empirical evidence invalidating classical assumptions. For example, the order flow is found to have long-range autocorrelations, in apparent contradiction with the (nearly) unpredictable nature of price changes. How can this be if order flow impact prices? More strikingly still, empirical results suggest a square-root like growth of impact with traded volume Q, often dubbed the “square-root impact law”, see Section 3.2 below for precise statements and references. This finding is in our opinion truly remarkable, on several counts. First, it is to a large extent universal, across time, markets (including the options markets or the Bitcoin), and execution strategies, suggesting to call it a “law” akin to physical laws. Second, a square-root dependence entails that the last Q/2![]() trades have an impact that is only ∼40% of the first Q/2

trades have an impact that is only ∼40% of the first Q/2![]() . The only possibility for such a strange behavior to hold is that there must exist some memory in the market that extends over a time scale longer than the typical time needed to complete an order (see below for more on this). The second ingredient needed to explain the concavity of the square-root impact is that the last Q/2

. The only possibility for such a strange behavior to hold is that there must exist some memory in the market that extends over a time scale longer than the typical time needed to complete an order (see below for more on this). The second ingredient needed to explain the concavity of the square-root impact is that the last Q/2![]() must experience more resistance than the first Q/2

must experience more resistance than the first Q/2![]() . In other words, after having executed the first half of the order, the liquidity opposing further moves must somehow increase. Still, it is quite a quandary to understand how such non-linear effects can appear, even when the bias in the order flow is very small.

. In other words, after having executed the first half of the order, the liquidity opposing further moves must somehow increase. Still, it is quite a quandary to understand how such non-linear effects can appear, even when the bias in the order flow is very small.

In several recent publications, simple Agent-Based Models (ABM) have been proposed to rationalize the universal square-root dependence of the impact. The argument relies on the existence of slow “latent” order book, i.e. orders to buy/sell that are not necessarily placed in the visible order book but that only reveal themselves as the transaction price moves closer to their limit price. Using both analytical arguments and numerical simulations of an artificial market, one finds that the liquidity profile is V-shaped, with a minimum around the current price and a linear growth of the latent volume as one moves away from that price. This explains why the resistance to further moves increases with the executed volume, and provides a simple explanation – borne out by numerical simulations – for the square-root impact. By the same token, a vanishing expected volume available around the mid-price leads to very small trades having anomalously large impact, as indeed reflected by the singular behavior of the square-root function near the origin.

The aim of the present chapter is to review the recent progress in Agent-Based Microstructure models that attempt to account for the various emergent “stylized facts” of financial markets, in particular the square-root impact just described. We show in particular that zero-intelligence models of order flow fail in general at reproducing the most basic property of prices, namely a random walk like behavior. Interestingly, models must be poised at a “critical point” separating a super-diffusive (trending) market and a sub-diffusive (mean-reverting) market, in such a way that the long range correlation of order flow is precisely balanced by the inertia of the (latent) order book. While all the necessary ingredients seem to be present to understand how fat-tailed distributions and clustered activity effects may emerge within such artificial markets, the final steps needed to complete this program are still not convincingly established, and is an important research objective for the future.

While the literature on ABM for financial markets is extremely abundant (see LeBaron, 2000; Chiarella et al., 2009b; Cristelli et al., 2011 for recent reviews), such models often start from the “mesoscale” (say minutes to days). Agent-Based Models at “microscale” (trades and quotes) have however been considered as well, see Sections 4, 5 and, among others, Bak et al. (1997), Chiarella and Iori (2002), Challet and Stinchcombe (2003), Chiarella et al. (2009a), Preis et al. (2006).

2 The Statistics of Price Changes: A Short Overview

2.1 Bachelier's First Law

The simplest property of financial prices, dating back to Bachelier's thesis (Bachelier, 1900), states that typical price variations grow like the square root of time. More formally, under the assumption that price changes have zero mean (which is a good approximation on short time scales), then the price variogram

(1) V(τ):=E[(pt+τ−pt)2]

grows linearly with time lag τ, such that V(τ)=Dτ![]() .

.

Subsequent to Bachelier's time, many empirical studies noted that the typical size of a given stock's price change tends to be proportional to the stock's price itself. This suggests that price changes should be regarded as multiplicative rather than additive, which, in turn, suggests the use of geometric Brownian motion for price-series modeling. However, over short time horizons – say intraday – there is empirical evidence that price changes are closer to being additive than multiplicative, so we will assume throughout this chapter an additive model of price changes. Still, given the prevalence of multiplicative models for price changes on longer time scales, it has become customary to define the volatility σ in relative terms (even for short timescales), according to the equation

(2) D=σ2p20,

where p0![]() is either the current price or some medium-term average.

is either the current price or some medium-term average.

2.2 Signature Plots

Assume now that a price series is described by

(3) pt=p0[1+t∑t′=1rt′],

where the return series rt![]() is covariance-stationary with zero mean and covariance

is covariance-stationary with zero mean and covariance

(4) Cov(rt′,rt″)=σ20Cr(|t′−t″|).

The case of a random walk with uncorrelated price returns corresponds to Cr(u)=δu,0![]() , where δu,0

, where δu,0![]() is the Kronecker delta function. A trending random walk has Cr(u)>0

is the Kronecker delta function. A trending random walk has Cr(u)>0![]() and a mean-reverting random walk has Cr(u)<0

and a mean-reverting random walk has Cr(u)<0![]() . How does this affect Bachelier's first law?

. How does this affect Bachelier's first law?

One important implication is that the volatility observed by sampling price series on a given time scale τ is itself dependent on that time scale. More precisely, the volatility at scale τ is given by

(5) σ2(τ):=V(τ)p20τ=σ20[1+2τ∑u=1(1−uτ)Cr(u)].

A plot of σ(τ)![]() versus τ is called a volatility signature plot. The case of an uncorrelated random walk leads to a flat signature plot. Positive correlations (which correspond to trends) lead to an increase in σ(τ)

versus τ is called a volatility signature plot. The case of an uncorrelated random walk leads to a flat signature plot. Positive correlations (which correspond to trends) lead to an increase in σ(τ)![]() with increasing τ. Negative correlations (which correspond to mean reversion) lead to a decrease in σ(τ)

with increasing τ. Negative correlations (which correspond to mean reversion) lead to a decrease in σ(τ)![]() with increasing τ.

with increasing τ.

2.3 High-Frequency Noise

Another interesting case occurs when the price pt![]() is soiled by some high-frequency noise, coming e.g. from price discretization effects or from pricing errors. Consider the case where rather than being given by Eq. (3), pt

is soiled by some high-frequency noise, coming e.g. from price discretization effects or from pricing errors. Consider the case where rather than being given by Eq. (3), pt![]() is instead assumed to be governed by

is instead assumed to be governed by

(6) pt=p0[1+t∑t′=1rt′]+ηt,

where ηt![]() is a mean zero, variance σ2η

is a mean zero, variance σ2η![]() noise, uncorrelated with rt

noise, uncorrelated with rt![]() , but is autocorrelated as

, but is autocorrelated as

(7) Cη(τ)=e−τ/τη,

where τη![]() is a short time scale time over which the high-frequency noise is correlated. Eq. (6) is standard in the microstructure (Hasbrouck, 2007), where the observed price is decomposed into a “fundamental” price plus microstructural noise.

is a short time scale time over which the high-frequency noise is correlated. Eq. (6) is standard in the microstructure (Hasbrouck, 2007), where the observed price is decomposed into a “fundamental” price plus microstructural noise.

How does this noise affect the observed volatility? By replacing Cr(τ)![]() in Eq. (5) with Cη(τ)

in Eq. (5) with Cη(τ)![]() , we see that compared to the volatility observed in a price series without noise, the addition of the ηt

, we see that compared to the volatility observed in a price series without noise, the addition of the ηt![]() term in Eq. (6) serves to increase the lag-τ volatility by 2σ2η(1−e−τ/τη)/τ

term in Eq. (6) serves to increase the lag-τ volatility by 2σ2η(1−e−τ/τη)/τ![]() . This additional noise term decays from 2σ2η/τη

. This additional noise term decays from 2σ2η/τη![]() for τ→0

for τ→0![]() , to 0 for τ→∞

, to 0 for τ→∞![]() . The effect of this high-frequency noise on a volatility signature plot is thus akin to mean-reversion, in the sense that it creates a higher short-term volatility than long-term volatility. Note that small pricing errors of ση=0.01%

. The effect of this high-frequency noise on a volatility signature plot is thus akin to mean-reversion, in the sense that it creates a higher short-term volatility than long-term volatility. Note that small pricing errors of ση=0.01%![]() with a one minute life-time would contribute to a very significant excess short-term volatility of 0.3% (daily), to be compared with a typical volatility of 1% for stock indexes.

with a one minute life-time would contribute to a very significant excess short-term volatility of 0.3% (daily), to be compared with a typical volatility of 1% for stock indexes.

2.4 Volatility Signature Plots for Real Price Series

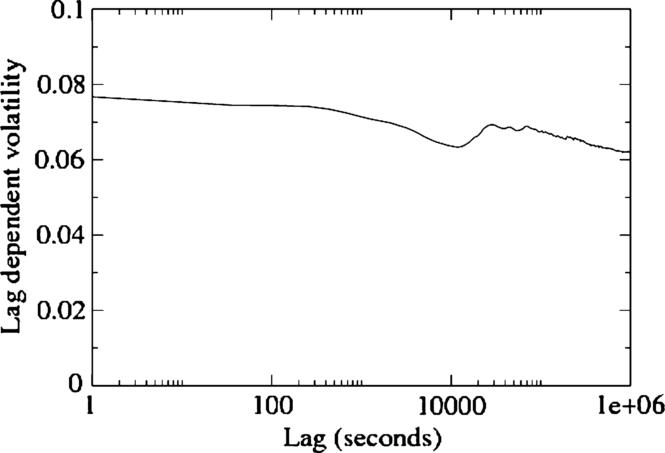

Quite remarkably, the volatility signature plots of most liquid assets (stocks, futures, FX, ...) are nowadays almost flat for values of τ ranging from a few seconds to a few months (beyond which it becomes dubious whether the statistical assumption of stationarity still holds). For example, for the S&P500 E-mini futures contract, which is one of the most liquid contracts in the world, σ(τ)![]() only decreases by about 20% from short time scales (seconds) to long time scales (weeks) – see Fig. 1. The exact form of a volatility signature plot depends on the microstructural details of the underlying asset, but most liquid contracts in this market have a similar volatility signature plot.

only decreases by about 20% from short time scales (seconds) to long time scales (weeks) – see Fig. 1. The exact form of a volatility signature plot depends on the microstructural details of the underlying asset, but most liquid contracts in this market have a similar volatility signature plot.

The important conclusion from this empirical result is that long-term volatility is almost entirely determined by the short-term price formation process. Depending on how one views this result, it is either trivial (a simple random walk has this property) or extremely non-intuitive. In fact, one should expect a rather large fundamental uncertainty about the price of an asset, which would translate into substantially larger high-frequency volatility. Although empirical data shows that high-frequency volatility is larger than low-frequency volatility, the size of this effect is small (∼20%![]() ). In a nutshell, long-term volatility seems is closely related to short-term volatility, itself determined by the high-frequency mechanisms of price formation.

). In a nutshell, long-term volatility seems is closely related to short-term volatility, itself determined by the high-frequency mechanisms of price formation.

2.5 Heavy Tails

An overwhelming body of empirical evidence from a vast array of financial instruments (including stocks, currencies, interest rates, commodities, and even implied volatility) show that unconditional distribution of returns has fat tails, which decay as a power law for large arguments and are much heavier than the corresponding tails of the Gaussian distribution, see e.g. Plerou et al. (1999), Gopikrishnan et al. (1999), Gabaix et al. (2006), Cont (2001), Bouchaud and Potters (2003).

On short time scales (between about a minute and a few hours), the empirical density function of returns r can be fit reasonably well by a Student's t distribution, with a distribution f(r)![]() decaying for large r as |r|−1−μ

decaying for large r as |r|−1−μ![]() , is the tail exponent. Empirically, the tail parameter μ is consistently found to be around 3 for a wide variety of different markets, which suggests some kind of universality in the mechanism leading to extreme returns. This universality hints at the fact that fundamental factors are probably unimportant in determining the amplitude of most large price jumps. Interestingly, many studies indeed suggest that large price moves are often not associated to an identifiable piece of news that would rationally explain wild valuation swings (Cutler et al., 1989; Fair, 2002; Joulin et al., 2008).

, is the tail exponent. Empirically, the tail parameter μ is consistently found to be around 3 for a wide variety of different markets, which suggests some kind of universality in the mechanism leading to extreme returns. This universality hints at the fact that fundamental factors are probably unimportant in determining the amplitude of most large price jumps. Interestingly, many studies indeed suggest that large price moves are often not associated to an identifiable piece of news that would rationally explain wild valuation swings (Cutler et al., 1989; Fair, 2002; Joulin et al., 2008).

2.6 Volatility Clustering

Although considering the unconditional distribution of returns is informative, it is also somewhat misleading. Returns are in fact very far from being IID random variables – although they are indeed nearly uncorrelated, as their flat signature plots demonstrate. Therefore, returns are not simply independent random variables drawn from the Student's t distribution. Such an IID model would predict that upon time aggregation, the distribution of returns would quickly converge to a Gaussian distribution on longer time scales. Empirical data indicates that this is not the case, and that returns remain substantially non-Gaussian on time scales up to weeks or even months (Bouchaud and Potters, 2003).

The dynamics of financial markets is in fact highly intermittent, with periods of intense activity intertwined with periods of relative calm. In intuitive terms, the volatility of financial returns is itself a dynamic variable that changes over time with a broad distribution of characteristic frequencies. In more formal terms, returns can be represented by the product of a time-dependent volatility component σt![]() and a directional component ξt

and a directional component ξt![]() ,

,

(8) rt:=σtξt.

In this representation, ξt![]() are IID (but not necessarily Gaussian) random variables of unit variance and σt

are IID (but not necessarily Gaussian) random variables of unit variance and σt![]() are positive random variables with long memory (Cont, 2001; Bollerslev et al., 1994; Muzy et al., 2000; Calvet and Fisher, 2002; Lux, 2008; Chicheportiche and Bouchaud, 2014).

are positive random variables with long memory (Cont, 2001; Bollerslev et al., 1994; Muzy et al., 2000; Calvet and Fisher, 2002; Lux, 2008; Chicheportiche and Bouchaud, 2014).

It is worth pointing out that volatilities σ and scaled returns ξ are not independent random variables. It is well-documented that positive past returns tend to decrease future volatilities and that negative past returns tend to increase future volatilities (i.e., 〈ξtσt+τ〉<0![]() for τ>0

for τ>0![]() ). This is called the leverage effect (Bouchaud et al., 2001). Importantly, however, past volatilities do not give much information on the sign of future returns (i.e., 〈ξtσt+τ〉≈0

). This is called the leverage effect (Bouchaud et al., 2001). Importantly, however, past volatilities do not give much information on the sign of future returns (i.e., 〈ξtσt+τ〉≈0![]() for τ<0

for τ<0![]() ).

).

2.7 Activity Clustering

In view of the long-range correlations of the volatility discussed in the last section, it is interesting to study the temporal fluctuations of market activity itself. Even a cursory look at the time series of mid-point changes suggests a strong degree of clustering in the activity as well.

A more precise way of characterizing this clustering property is to choose a time t and a small dt![]() , and count the number dNt

, and count the number dNt![]() of price changes that occur during the time interval [t,t+dt]

of price changes that occur during the time interval [t,t+dt]![]() (i.e., count dNt=1

(i.e., count dNt=1![]() if the mid-point changed or dNt=0

if the mid-point changed or dNt=0![]() if it did not). The empirical average of dNt

if it did not). The empirical average of dNt![]() provides a way to define the average market activity ‾λ

provides a way to define the average market activity ‾λ![]() , while the covariance Cov[dNt,dNt+τ]

, while the covariance Cov[dNt,dNt+τ]![]() characterizes the temporal structure of the fluctuations in market activity.

characterizes the temporal structure of the fluctuations in market activity.

An increased activity at time t appears to trigger more activity at time t+τ![]() , much like earthquakes are followed by aftershocks. For example, a large jump is usually followed by an increased frequency of smaller price moves. More generally, some kind of “self-excitation” seem to be present in financial markets. This contagion takes place either in the time direction (some events trigger more events in the future) or across different assets (the activity of one stock spills over to other correlated stocks, or even from one market to another). Hawkes processes are mathematical models that capture (part) of these contagion effects, see Bacry et al. (2015) for a review, and Blanc et al. (2016) for some recent extensions.

, much like earthquakes are followed by aftershocks. For example, a large jump is usually followed by an increased frequency of smaller price moves. More generally, some kind of “self-excitation” seem to be present in financial markets. This contagion takes place either in the time direction (some events trigger more events in the future) or across different assets (the activity of one stock spills over to other correlated stocks, or even from one market to another). Hawkes processes are mathematical models that capture (part) of these contagion effects, see Bacry et al. (2015) for a review, and Blanc et al. (2016) for some recent extensions.

2.8 Long Memory in the Order Flow

Another striking stylized fact of financial markets is the persistence in the sign of the order flow. More formally, let εt![]() denote the sign of the tth market order, with εt=+1

denote the sign of the tth market order, with εt=+1![]() for a buy market order and εt=−1

for a buy market order and εt=−1![]() for a sell market order, where t is discrete and counts the number of market orders. In this event-time framework, one can introduce the sign autocorrelation function

for a sell market order, where t is discrete and counts the number of market orders. In this event-time framework, one can introduce the sign autocorrelation function

(9) C(ℓ):=Cov[εt,εt+ℓ],

The surprising empirical result – that holds for many different asset classes (stocks, FX, futures, ...) – is that C(ℓ)![]() decays extremely slowly with ℓ (see Bouchaud et al., 2004, 2006; Lillo and Farmer, 2004; Bouchaud et al., 2009 for a review). Its long time behavior is well-approximated by a power-law ℓ−γ

decays extremely slowly with ℓ (see Bouchaud et al., 2004, 2006; Lillo and Farmer, 2004; Bouchaud et al., 2009 for a review). Its long time behavior is well-approximated by a power-law ℓ−γ![]() with γ<1

with γ<1![]() , corresponding to a so-called long-memory process (Beran, 1994). Typically, γ≈0.5

, corresponding to a so-called long-memory process (Beran, 1994). Typically, γ≈0.5![]() for stock markets and γ≈0.8

for stock markets and γ≈0.8![]() for futures markets (see for example Bouchaud et al., 2004, 2006, 2009; Lillo and Farmer, 2004; and, for futures markets, Mastromatteo et al., 2014a). The origin of this long-memory has been argued to be chiefly due to order splitting (LeBaron and Yamamoto, 2010; Tóth et al., 2015) rather than direct herding. Importantly, the long memory of order signs and long-memory in activity fluctuations are distinct phenomena, with no logical relation to one another (it is easy to build models that have one type of long memory, but not the other).

for futures markets (see for example Bouchaud et al., 2004, 2006, 2009; Lillo and Farmer, 2004; and, for futures markets, Mastromatteo et al., 2014a). The origin of this long-memory has been argued to be chiefly due to order splitting (LeBaron and Yamamoto, 2010; Tóth et al., 2015) rather than direct herding. Importantly, the long memory of order signs and long-memory in activity fluctuations are distinct phenomena, with no logical relation to one another (it is easy to build models that have one type of long memory, but not the other).

The persistence in the sign of the order flow leads to an apparent “efficiency paradox”, which asks the question of how prices can remain unpredictable when order flow (which impacts the price directly) is so predictable. We will come back on this issue in Section 5.

2.9 Summary

The above short review of the statistical properties of prices has left aside a host of other interesting regularities, in particular concerning inter-asset correlations, long-term behavioral anomalies, trend following effects and other “factor” dynamics, etc. The main message of this section is that price changes are remarkably uncorrelated over a large range of frequencies, with little signs of price adjustments or tâtonnement at high frequencies. The long-term volatility appears to be determined by the short-term, high frequency movements of the price.

In fact, the frequency of news that would affect the fundamental value of financial assets is much lower than the frequency of price changes themselves. As Cutler, Poterba, and Summers state it: The evidence that large market moves often occur on days without any identifiable major news releases, casts doubt on the view that stock price movements are fully explicable by news. It is as if price changes themselves are the main source of news, and feedback as to create self-induced excess volatility and, most probably, price jumps that occur without any news at all. Interestingly, all quantitative volatility/activity feedback models (such as ARCH/GARCH models and the like, or Hawkes processes; see Bollerslev et al., 1994; Chicheportiche and Bouchaud, 2014; Bacry et al., 2015; Hardiman et al., 2013) suggest that at least 80% of the price variance is induced by self-referential effects. This adds credence to the idea that a lion's share of the short to medium term activity of financial markets is unrelated to any fundamental information or economic effects.

From a scientific point of view, this is extremely interesting, since it opens the path to building a theory of price moves that is mostly based on modeling the endogenous, self-exciting dynamics of markets, and not on long-term fundamental effects. One particularly important question is to understand the origin and the mechanisms leading to price jumps, which seem to have a similar structure on all traded, liquid markets (again indicating that fundamental factors are probably unimportant at short time scales).

3 The Square-Root Impact Law

3.1 Introduction

Assume that following a decision to trade (whatever the underlying reason might be) one has to buy (or sell) some quantity Q on the market. Ideally, one would like to execute it immediately, “at the market price”. However, unless the quantity Q is smaller than the available volume at the best quote, this is simply not possible. There is no such thing as a “market price”. The market price is not only different for buy trades and sell trades, it really only makes sense for infinitesimal volumes, when the trade can be executed in one shot, such that impact on later trades can be neglected. For volumes typical of large financial institutions – say 1% of the market capitalization of a given stock – there is just not enough liquidity in the whole Limit Order Book (LOB) to match the required quantity Q.

Large trades should thus be split in small chunks. This incremental execution aims at allowing the latent liquidity to reveal itself and refill the LOB with previously undisclosed orders (what we call later the “latent” order book). This should, in principle, considerably improve the price obtained compared to an immediate execution with market orders that would otherwise penetrate deep into the book and possibly even destabilize the market.

The sequence of trades that comes from a single investment decision is known as a metaorder. How does a metaorder of size Q impact the price? From the point of view of investors: what is the true cost of trading? How does it depend on market conditions, execution strategies, and time horizon, etc.? From the point of view of regulators: can large metaorders destabilize markets? Is marked-to-market accounting wise when, as emphasized above, the market price is at best meaningful for infinitesimal volumes, but not for large investment portfolios that would substantially impact the price upon unwinding?

3.2 Empirical Evidence

Naively, one expects the impact of a metaorder to be linear in its volume Q. It is also what standard theoretical models of impact predict, such as the famous Kyle model (Kyle, 1985). However, there is now overwhelming empirical evidence ruling out the simple linear impact law, and suggesting instead a concave, square-root-like growth of impact with volume, often dubbed the “square-root impact law”. The impact of a metaorder is surprisingly universal: the square-root law has been reported in many different studies, both academic and professional, since the early eighties (Loeb, 1983). It appears to hold for completely different markets (equities, futures, FX, options (Tóth et al., 2016), or even the Bitcoin; Donier and Bonart, 2015), epochs (pre-2005, when liquidity was mostly provided by market makers, and post-2005, with electronic markets dominated by HFT), types of microstructure (small ticks versus large ticks), market participants and underlying trading strategies (fundamental, technical, etc.), and styles of execution (using limit or market orders). In all these cases, the impact of a meta-order of volume Q is well described by (Torre and Ferrari, 1997; Grinold and Kahn, 1999; Almgren et al., 2005; Moro et al., 2009; Tóth et al., 2011; Mastromatteo et al., 2014a; Gomes and Waelbroeck, 2014; Bershova and Rakhlin, 2013; Brokmann et al., 2015)1

(10) I(Q,T)≈YσT(QVT)δ(Q≪VT)

where δ is an exponent in the range 0.4–0.7, Y is a numerical coefficient of order unity (Y≈0.5![]() for US stocks), and σT

for US stocks), and σT![]() and VT

and VT![]() are, respectively, the average contemporaneous volatility on the time horizon T and the average contemporaneous traded volume over time T. Note that Eq. (10) is dimensionally correct (in the sense that the dimension of Q and VT

are, respectively, the average contemporaneous volatility on the time horizon T and the average contemporaneous traded volume over time T. Note that Eq. (10) is dimensionally correct (in the sense that the dimension of Q and VT![]() cancel out, while impact and volatility are indeed expressed as price percentage). Kyle's model instead leads to δ=1

cancel out, while impact and volatility are indeed expressed as price percentage). Kyle's model instead leads to δ=1![]() , with a Kyle “lambda” parameter equal to YσT/VT

, with a Kyle “lambda” parameter equal to YσT/VT![]() .

.

3.3 A Very Surprising Law

This square-root impact law is extremely well established empirically but extremely surprising theoretically. As mentioned in the introduction, one finds that the second half of a metaorder of size impacts the price much less than the first half, in fact, a square-root impact gives √2−1=0.4142...![]() times less. How can this be? Surely if one traded the second half a very long time after the first half, impact should be additive again, as the memory of the first trade would evaporate. This clearly shows that there must be some kind of “memory time” Tm

times less. How can this be? Surely if one traded the second half a very long time after the first half, impact should be additive again, as the memory of the first trade would evaporate. This clearly shows that there must be some kind of “memory time” Tm![]() in financial markets, such that impact is square root for T≪Tm

in financial markets, such that impact is square root for T≪Tm![]() but additivity is recovered for T≫Tm

but additivity is recovered for T≫Tm![]() , when all memory of past trades is lost. We will hypothesize in Sections 5, 6 that this memory is in fact imprinted in the “latent” order book alluded to above, that stores the outstanding liquidity that cannot be executed immediately.

, when all memory of past trades is lost. We will hypothesize in Sections 5, 6 that this memory is in fact imprinted in the “latent” order book alluded to above, that stores the outstanding liquidity that cannot be executed immediately.

Note that the relevant ratio here is the volume of the metaorder Q to the market volume VT![]() over the execution time, and not, as could have been naively anticipated, the ratio of Q over total the market capitalization M

over the execution time, and not, as could have been naively anticipated, the ratio of Q over total the market capitalization M![]() of the asset. That one should trade 1% of the market capitalization M

of the asset. That one should trade 1% of the market capitalization M![]() of a stock to move its price by 1% would look reasonable at first sight. It was in fact common lore in the 80's, when impact was deemed totally irrelevant for quantities representing a few basis points of M

of a stock to move its price by 1% would look reasonable at first sight. It was in fact common lore in the 80's, when impact was deemed totally irrelevant for quantities representing a few basis points of M![]() . But M

. But M![]() is (for stocks) 200 times larger than VT

is (for stocks) 200 times larger than VT![]() itself, so that Q/M≪Q/VT

itself, so that Q/M≪Q/VT![]() . Therefore a Q/M

. Therefore a Q/M![]() scaling would have meant a much smaller impact than the one observed in practice. The non-linear square-root behavior for Q≪VT

scaling would have meant a much smaller impact than the one observed in practice. The non-linear square-root behavior for Q≪VT![]() furthermore substantially amplifies the impact of small metaorders: executing 1% of the daily volume moves the price (on average) by √1%=10%

furthermore substantially amplifies the impact of small metaorders: executing 1% of the daily volume moves the price (on average) by √1%=10%![]() of its daily volatility. The main conclusion here is that impact, even of relatively small metaorders, is a surprisingly large effect.

of its daily volatility. The main conclusion here is that impact, even of relatively small metaorders, is a surprisingly large effect.

Let us highlight another remarkable property of the strict square-root impact, which that I(Q,T)![]() is approximately independent of the execution time horizon T, and only determined by the total exchanged volume Q. This follows from the fact that σT∝√T

is approximately independent of the execution time horizon T, and only determined by the total exchanged volume Q. This follows from the fact that σT∝√T![]() whereas VT∝T

whereas VT∝T![]() , so that the T dependence cancels out in Eq. (10). In economics term, this makes sense: the market price has to adapt to a certain change of global supply/demand εQ, quite independently on how this volume is actually executed. A more detailed, “Walrasian” view of this highly non-trivial statement is provided in Section 6.

, so that the T dependence cancels out in Eq. (10). In economics term, this makes sense: the market price has to adapt to a certain change of global supply/demand εQ, quite independently on how this volume is actually executed. A more detailed, “Walrasian” view of this highly non-trivial statement is provided in Section 6.

Let us note however that the square-root impact law (10) is only approximately valid in a certain domain of parameters, as with any empirical law. For example, as we have mentioned already, the execution time T should not be longer than a certain “memory time” Tm![]() of the market. The second obvious limitation is that the ratio Q/VT

of the market. The second obvious limitation is that the ratio Q/VT![]() should be small, such that the metaorder remains a small fraction of the total volume VT

should be small, such that the metaorder remains a small fraction of the total volume VT![]() and that the impact itself is small compared to the volatility. In the case where Q/VT

and that the impact itself is small compared to the volatility. In the case where Q/VT![]() becomes substantial, one must enter a different regime as the metaorder becomes a large perturbation to the normal course of the market.

becomes substantial, one must enter a different regime as the metaorder becomes a large perturbation to the normal course of the market.

Finally, let us discuss some recurrent misconceptions or confusions that exist in the literature concerning the impact of metaorders:

- • First, we emphasize that the impact of a metaorder of volume Q is not equal to the aggregate impact of order imbalance ΔV=Q

, which is in fact linear for small ΔV, and not square-root like (Bouchaud et al., 2009; Patzelt and Bouchaud, 2018). One cannot measure the impact of metaorders without being able to identify the origin of the trades, and correctly ascribe them to a given investor executing an order.

, which is in fact linear for small ΔV, and not square-root like (Bouchaud et al., 2009; Patzelt and Bouchaud, 2018). One cannot measure the impact of metaorders without being able to identify the origin of the trades, and correctly ascribe them to a given investor executing an order. - • The square-root impact law applies to slow metaorders composed of several individual trades, but not to these individual trades themselves. Universality, if it holds, can only result from some “mesoscopic” properties of the supply and demand in financial markets, that are insensitive to the way markets are organized at the microscale. This would explain, for example, why the square-root law holds equally well in the pre-HFT era (say before 2005) and since the explosion of electronic, high frequency market making (after 2005).

- • Conversely, at the single trade level, one expects that microstructure effects (tick size, continuous markets vs. batch auctions, etc.) play a strong role. In particular, the impact of a single market order of size q does not behave like a square-root, although it behaves as a concave function of q (Bouchaud et al., 2009). But this concavity has no immediate relation with the concavity of the impact of metaorders.

3.4 Theoretical Ideas

The square-root law was not anticipated by financial economists: classical models, such as the Kyle model, all suggested or posited a linear behavior. It is an interesting case where empirical data compelled the finance community to accept that reality was fundamentally different from theory. Several stories have been proposed since the mid-nineties to account for the square-root impact law.

The first attempt, due to the Barra group (Torre and Ferrari, 1997) and Grinold and Kahn (1999), argues that the square-root behavior is a consequence of market-markers getting compensated for their inventory risk. Assume that the metaorder of volume Q is absorbed by market-makers who will need to slowly offload their position later on. The amplitude of an adverse move of the price during this unwinding phase is given by ∼σ√Toff.![]() , where Toff.

, where Toff.![]() is the time needed to offload an inventory of size Q. It is reasonable to assume that Toff.

is the time needed to offload an inventory of size Q. It is reasonable to assume that Toff.![]() is proportional to Q and inversely proportional to the trading rate of the market V. If market-makers respond to the metaorder by moving the price in such a way that their profit is of the same order as the risk they take, then indeed I∝σ√Q/V

is proportional to Q and inversely proportional to the trading rate of the market V. If market-makers respond to the metaorder by moving the price in such a way that their profit is of the same order as the risk they take, then indeed I∝σ√Q/V![]() , as found empirically. However, this story assumes no competition between market-makers. Indeed, inventory risk is diversifiable over time and on the long run averages to zero. Charging an impact cost compensating for the inventory risk of each metaorder would lead to formidable profits and necessarily attract competing liquidity providers.

, as found empirically. However, this story assumes no competition between market-makers. Indeed, inventory risk is diversifiable over time and on the long run averages to zero. Charging an impact cost compensating for the inventory risk of each metaorder would lead to formidable profits and necessarily attract competing liquidity providers.

Another story, proposed by Gabaix et al. (2003, 2006), ascribes the square-root impact law to the fact that the optimal execution horizon T⁎![]() for “informed” metaorders of size Q grows like T⁎∼√Q

for “informed” metaorders of size Q grows like T⁎∼√Q![]() . Since during that time the price is expected to move linearly in the direction of the trade as information gets slowly revealed, the apparent peak impact behaves as √Q

. Since during that time the price is expected to move linearly in the direction of the trade as information gets slowly revealed, the apparent peak impact behaves as √Q![]() . However, this scenario would imply that the impact during the metaorder is linear in the executed quantity q, at variance with empirical data: the impact path itself behaves as a square-root of q, at least when the execution schedule is flat.

. However, this scenario would imply that the impact during the metaorder is linear in the executed quantity q, at variance with empirical data: the impact path itself behaves as a square-root of q, at least when the execution schedule is flat.

Recently, Farmer et al. (2013) have proposed yet another theory which is very reminiscent of the Glosten–Milgrom model (Glosten and Milgrom, 1985) that competitively sets the size of the bid–ask spread. One assumes metaorders with a power-law distributed volume Q come one after the other. Market-makers attempt to guess whether the metaorder will continue or stop at the next time step, and set the price such that (a) it is a martingale and (b) the average execution price compensates for the information contained in the metaorder (“fair pricing”). Provided the distribution of metaorder sizes behaves as Q−5/2![]() , these two conditions lead to a square-root impact law. Although enticing, this theory has difficulty explaining why the square-root law holds even when the average impact is smaller than, or of the same order as the bid–ask spread and/or the trading fees – which should in principle strongly affect the market-makers' fair pricing condition. Furthermore, the square-root impact law appears to be much more universal than the distribution of the size of metaorders. In the case of Bitcoin, for example, the square-root law holds very precisely while the distribution of metaorders behaves as Q−2

, these two conditions lead to a square-root impact law. Although enticing, this theory has difficulty explaining why the square-root law holds even when the average impact is smaller than, or of the same order as the bid–ask spread and/or the trading fees – which should in principle strongly affect the market-makers' fair pricing condition. Furthermore, the square-root impact law appears to be much more universal than the distribution of the size of metaorders. In the case of Bitcoin, for example, the square-root law holds very precisely while the distribution of metaorders behaves as Q−2![]() rather than Q−5/2

rather than Q−5/2![]() (Donier and Bonart, 2015).

(Donier and Bonart, 2015).

The universality of the square-root law suggests that its explanation should rely on minimal, robust ingredients that would account for its validity is different markets (from stocks to Bitcoin) and different epochs (from pit markets to electronic platforms). We will present in Sections 5 and 6 a minimal agent-based model of the dynamics of supply and demand. This framework, originally put forth by Tóth et al. (2011) and much developed since, provides a natural interpretation of the square-root law and its apparent universality.

4 The Santa-Fe “Zero-Intelligence” Model

In this section, we introduce a (over-)simplified framework for describing the co-evolution of liquidity and prices, at the level of the Limit Order Book.2 This model was initially proposed and developed by a group of scientists then working at the Santa Fe Institute, see Daniels et al. (2003), Smith et al. (2003), Farmer et al. (2005).3 After describing the Santa-Fe model and the price dynamics it generates, we will discuss some of its limitations. (Note that what we call here the Santa-Fe model is not the stock market agent-based model (Palmer et al., 1994) but rather the more recent particle-based limit order book model.)

4.1 Model Definition

Consider the continuous-time temporal evolution of a set of particles on a one-dimensional lattice of mesh size equal to one tick ϑ. Each location on the lattice corresponds to a specified price level in the LOB. Each particle is either of type A, which corresponds to a sell order, or of type B, which corresponds to a buy order. Each particle corresponds to an order of a fixed size υ0![]() which we can arbitrarily set to unity. Whenever two particles of opposite type occupy the same point on the pricing grid, an annihilation A+B→∅

which we can arbitrarily set to unity. Whenever two particles of opposite type occupy the same point on the pricing grid, an annihilation A+B→∅![]() occurs, to represent the matching of a buy order and a sell order. Particles can also “evaporate”, to represent the cancellation of an order by its owner. The position of the leftmost A particle defines the ask price a(t)

occurs, to represent the matching of a buy order and a sell order. Particles can also “evaporate”, to represent the cancellation of an order by its owner. The position of the leftmost A particle defines the ask price a(t)![]() , and he position of the rightmost B particle defines the bid price b(t)

, and he position of the rightmost B particle defines the bid price b(t)![]() . The mid-price is m(t)=(b(t)+a(t))/2

. The mid-price is m(t)=(b(t)+a(t))/2![]() , and the bid–ask spread s(t)

, and the bid–ask spread s(t)![]() is a(t)−b(t)

is a(t)−b(t)![]() .

.

In the Santa-Fe “Zero-Intelligence” model, order flows are completely random and assumed to be governed by the following stochastic processes,4 where all orders have size υ0=1![]() :

:

- • At each price level p⩽m(t)

(resp. p⩾m(t)

(resp. p⩾m(t) ), buy (resp. sell) limit orders arrive as a Poisson process with rate λ, independently of p.

), buy (resp. sell) limit orders arrive as a Poisson process with rate λ, independently of p. - • Buy/Sell market orders arrive as Poisson processes, each with rate μ.

- • Each outstanding buy (resp. sell) limit order is canceled according to a Poisson process with rate ν.

- • All event types are mutually independent.

The first two rules mean that the mid-price m(t)![]() is the reference price around which the order flow organizes. Whenever a buy (respectively, sell) market order x arrives at time tx

is the reference price around which the order flow organizes. Whenever a buy (respectively, sell) market order x arrives at time tx![]() , it annihilates a sell limit order at the price a(tx)

, it annihilates a sell limit order at the price a(tx)![]() (respectively, buy limit order at the price b(tx)

(respectively, buy limit order at the price b(tx)![]() ), and thereby causes a transaction. Therefore, the interacting flows of market order arrivals, limit order arrivals, and limit order cancellations together fully specify the temporal evolution of the LOB, and in particular the mid-price m(t)

), and thereby causes a transaction. Therefore, the interacting flows of market order arrivals, limit order arrivals, and limit order cancellations together fully specify the temporal evolution of the LOB, and in particular the mid-price m(t)![]() .

.

4.2 Basic Intuition

Before investigating the model in detail, we first appeal to intuition to discuss some of its more straightforward properties. First, each of the parameters λ, μ, and ν are rate parameters, with units of inverse time. Therefore, any observable related to the equilibrium distribution of volumes, spreads, or gaps between filled prices can only depend on ratios of λ, μ, and ν, to cause the units to cancel out.

Second, the approximate distributions of queue sizes can be derived by considering the interactions of the different types of order flows at different prices. Because market order arrivals only influence activity at the best quotes, it follows that very deep into the LOB, the distribution of queue sizes V reaches a stationary state that is independent of the distance from m(t)![]() , given by

, given by

(11) Pst.(V)=e−V⁎V⁎VV!,V⁎=λν.

Two extreme cases are possible:

- • A sparse LOB, corresponding to V⁎≪υ0=1

, where most price levels are empty while some are only weakly populated. This case corresponds to very small-tick assets.

, where most price levels are empty while some are only weakly populated. This case corresponds to very small-tick assets. - • A dense LOB, corresponding to V⁎≫υ0=1

, where all price levels are populated with a large number of orders. This corresponds to large-tick assets, at least close enough to the mid-point so that the assumption that λ is constant is reasonable.

, where all price levels are populated with a large number of orders. This corresponds to large-tick assets, at least close enough to the mid-point so that the assumption that λ is constant is reasonable.

In reality, one observes that λ decreases with increasing distance from m(t)![]() . Therefore, even in the case of large-tick stocks, we expect a cross-over between a densely populated LOB close to the best quotes and a sparse LOB far away from them. This does not, however, imply that there are no buyers or sellers who wish to trade at prices far away from the current mid-point. As we will argue in Sections 5, 6, the potential number of buyers (respectively, sellers) is expected to grow with increasing distance from m(t)

. Therefore, even in the case of large-tick stocks, we expect a cross-over between a densely populated LOB close to the best quotes and a sparse LOB far away from them. This does not, however, imply that there are no buyers or sellers who wish to trade at prices far away from the current mid-point. As we will argue in Sections 5, 6, the potential number of buyers (respectively, sellers) is expected to grow with increasing distance from m(t)![]() , but most of the corresponding liquidity is latent, and only becomes revealed as m(t)

, but most of the corresponding liquidity is latent, and only becomes revealed as m(t)![]() decreases (respectively, increases).

decreases (respectively, increases).

The above distribution of queue sizes is not accurate for prices close to m(t)![]() . If d denotes the distance between a given price and m(t)

. If d denotes the distance between a given price and m(t)![]() , then for smaller values of d, it becomes increasingly likely that a given price was actually the best price in the recent past. Correspondingly, limit orders are depleted not only because of cancellations but also because of market orders that may have hit that queue. Heuristically, one expects that the average size of the queues is given by

, then for smaller values of d, it becomes increasingly likely that a given price was actually the best price in the recent past. Correspondingly, limit orders are depleted not only because of cancellations but also because of market orders that may have hit that queue. Heuristically, one expects that the average size of the queues is given by

V⁎≈λ−μϕeff(d)ν,

where ϕeff(d)![]() is the fraction of time during which the corresponding price level was the best quote in the recent past (of duration ν−1

is the fraction of time during which the corresponding price level was the best quote in the recent past (of duration ν−1![]() , beyond which all memory is lost). This formula says that queues tend to be smaller on average close to the mid-point, simply because the market order flow plays a greater role in removing outstanding limit orders. One therefore expects that the average depth profile is an increasing function of d, at least close to d=0

, beyond which all memory is lost). This formula says that queues tend to be smaller on average close to the mid-point, simply because the market order flow plays a greater role in removing outstanding limit orders. One therefore expects that the average depth profile is an increasing function of d, at least close to d=0![]() where λ can be considered as a constant. This is indeed what is observed in empirical data of LOB volume profiles, see Bouchaud et al. (2002, 2009), where a simple theory describing the shape of an LOB's volume profile is also given.

where λ can be considered as a constant. This is indeed what is observed in empirical data of LOB volume profiles, see Bouchaud et al. (2002, 2009), where a simple theory describing the shape of an LOB's volume profile is also given.

Next, we consider the size of the spread s(t)![]() . For large-tick stocks, the bid and ask queues will both typically be long and s(t)

. For large-tick stocks, the bid and ask queues will both typically be long and s(t)![]() will spend most of the time equal to its smallest possible value of one tick, s(t)=ϑ

will spend most of the time equal to its smallest possible value of one tick, s(t)=ϑ![]() . For small-tick stocks, however, the spread may become larger. In this case, the probability per unit time that a new limit order arrives inside the spread is given by (ˆs−1)λ

. For small-tick stocks, however, the spread may become larger. In this case, the probability per unit time that a new limit order arrives inside the spread is given by (ˆs−1)λ![]() (because both buy and sell limit orders can fall on the ˆs−1

(because both buy and sell limit orders can fall on the ˆs−1![]() available intervals inside the spread s=ˆsϑ

available intervals inside the spread s=ˆsϑ![]() ), and the probability per unit time that an order at the best quotes is removed by cancellation or by an incoming market order is given by 2(μ+ν)

), and the probability per unit time that an order at the best quotes is removed by cancellation or by an incoming market order is given by 2(μ+ν)![]() . The equilibrium spread size is such that these two effects compensate,

. The equilibrium spread size is such that these two effects compensate,

seq.≈ϑ[1+2μ+νλ].

Although hand-waving, this argument gives a good first approximation of the average spread. In particular, the result that a large flux of market orders μ opens up the spread sounds reasonable.

4.3 Simulation Results

Deriving analytical results about the behavior of the Santa Fe model is deceptively difficult (Smith et al., 2003). By contrast, simulating the model is relatively straightforward. The Santa Fe model is extremely rich, so many output observables can be studied in this way. We restrict here to three particularly relevant topics:

- 1. The ratio between the mean first gap behind the best quote (i.e., the price difference between the best and second-best quotes) and the mean spread s;

- 2. The volatility and signature plot of the mid-price;

- 3. The mean impact of a market order and the mean profit of market-making.

Numerical results show that the model does a good job of capturing some of these properties, but a less good job at capturing others, due to the many simplifying assumptions that it makes. For example, when λ,μ,ν![]() are calibrated on real data, the model makes good predictions of the mean bid–ask spread, as first emphasized by Farmer et al. (2005). However, the price series that it generates show significant mean-reverting behavior, except when the memory time Tm=ν−1

are calibrated on real data, the model makes good predictions of the mean bid–ask spread, as first emphasized by Farmer et al. (2005). However, the price series that it generates show significant mean-reverting behavior, except when the memory time Tm=ν−1![]() is very short (Daniels et al., 2003; Smith et al., 2003). As noticed in Section 2.4, such mean-reversion is usually not observed in real markets. Moreover, the model predicts volatility to be too small for large-tick stocks and too large for small-tick stocks, and furthermore creates strong arbitrage opportunities for market-making strategies that do not exist in real markets. These weaknesses of the model provide insight into how it might be improved, by including additional effects such as the long-range correlations of order flow or some simple strategic behaviors from market participants (see Section 5).

is very short (Daniels et al., 2003; Smith et al., 2003). As noticed in Section 2.4, such mean-reversion is usually not observed in real markets. Moreover, the model predicts volatility to be too small for large-tick stocks and too large for small-tick stocks, and furthermore creates strong arbitrage opportunities for market-making strategies that do not exist in real markets. These weaknesses of the model provide insight into how it might be improved, by including additional effects such as the long-range correlations of order flow or some simple strategic behaviors from market participants (see Section 5).

4.3.1 The Gap-to-Spread Ratio

Let us consider the mean gap between the second-best quote and the best quote, compared to the mean spread itself. We call this ratio the gap-to-spread ratio. The gap-to-spread ratio is interesting since it is to a large extent insensitive to the problem of calibrating the parameters correctly (and of reproducing the mean bid–ask spread exactly).

Fig. 2 shows the empirical gap-to-spread ratio versus the gap-to-spread ratio generated by simulating the Santa Fe model, for a selection of 13 US stocks with different tick sizes (Bouchaud et al., 2018). For large-tick stocks, the model predicts that both the spread and the gap between the second-best and best quotes are nearly always locked to 1 tick, so the ratio is itself simply equal to 1. In reality, however, the dynamics is more subtle. The bid–ask spread actually widens more frequently than the Santa Fe model predicts, such that the empirical gap-to-spread ratio is in fact in the range 0.8–0.95. This discrepancy becomes even more pronounced for small-tick stocks, for which the empirical gap-to-spread ratio typically takes values around 0.15–0.2, but for which the Santa Fe model predicts a gap-to-spread ratio as high as 0.4. In other words, when the spread is large, the second best price tends to be much closer to the best quote in reality than it is in the model. As we will see in below this turns out to have an important consequence for the impact of market orders in the model.

This analysis of the gap-to-spread ratio reveals that an important ingredient is missing from the Santa Fe model. When the spread is large, real liquidity providers tend to place new limit orders inside the spread, but still close to the best quotes, and thereby typically only improve the quote price by one tick at a time. This leads to gaps between the best and second-best quotes that are much smaller than those predicted by the assumption of uniform arrivals of limit orders at all prices beyond the mid-price. One could indeed modify the Santa Fe specification to account for this empirically observed phenomenon of smaller gaps for limit orders that arrive inside the spread, but doing so comes at the expense of adding extra parameters, see Mike and Farmer (2008).

4.3.2 The Signature Plot

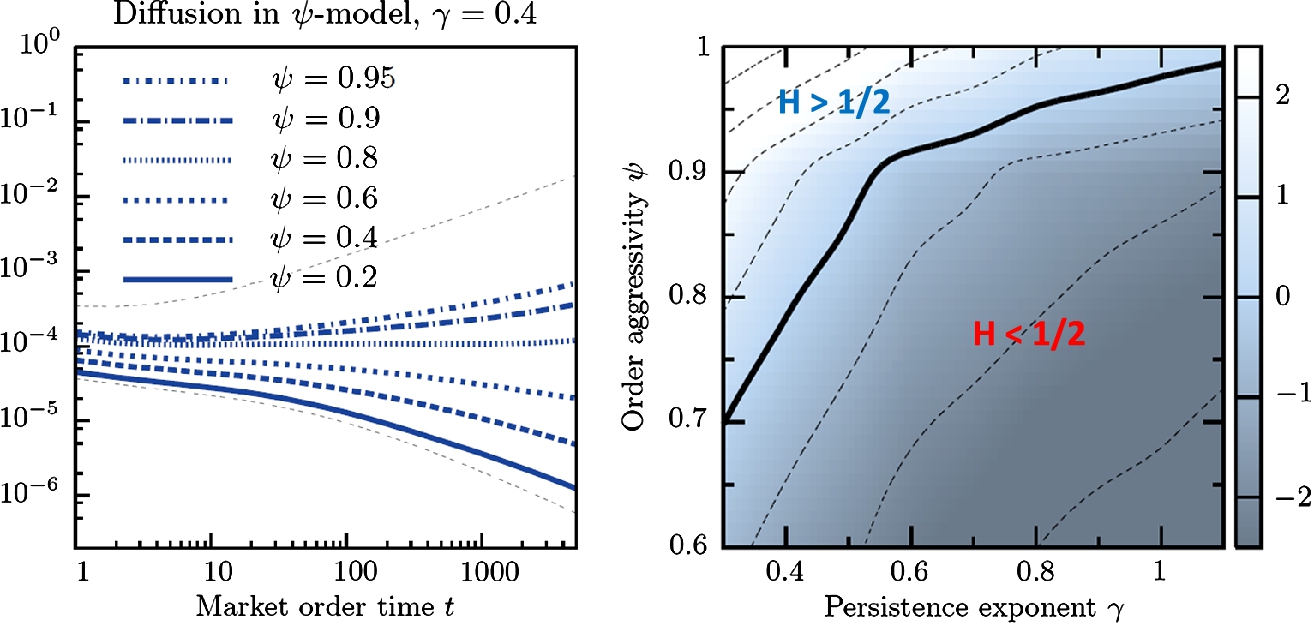

When simulating the Santa Fe model, the lag-dependent volatility σ(τ)![]() of the mid-price, and the corresponding signature plot (see Section 2.4), both reveal that the model exhibits some excess volatility at small values of τ, particularly when the cancellation rate ν is small. Put another way, the slow temporal evolution of the LOB leads to a substantial mean-reversion in the mid price. This was already noted in the papers published by the Santa-Fe group (Daniels et al., 2003; Smith et al., 2003), and can be observed in the left graph of Fig. 3 in the case ψ=0

of the mid-price, and the corresponding signature plot (see Section 2.4), both reveal that the model exhibits some excess volatility at small values of τ, particularly when the cancellation rate ν is small. Put another way, the slow temporal evolution of the LOB leads to a substantial mean-reversion in the mid price. This was already noted in the papers published by the Santa-Fe group (Daniels et al., 2003; Smith et al., 2003), and can be observed in the left graph of Fig. 3 in the case ψ=0![]() that corresponds to the Santa-Fe limit. Intuitively, this strong mean-reverting behavior is explained by the following argument: imagine that the price has been drifting upwards for a while. The buy side of the book, below the current price, has had little time to refill yet, whereas the sell side of the book is full and creates a barrier resisting further increases. Subsequent sell market orders will therefore have a larger impact than buy orders, pushing the price back down.

that corresponds to the Santa-Fe limit. Intuitively, this strong mean-reverting behavior is explained by the following argument: imagine that the price has been drifting upwards for a while. The buy side of the book, below the current price, has had little time to refill yet, whereas the sell side of the book is full and creates a barrier resisting further increases. Subsequent sell market orders will therefore have a larger impact than buy orders, pushing the price back down.

Empirically, one observes some mean reversion for large-tick stocks, but very little – or even weak trending effects – for small-tick stocks (see e.g. Eisler et al., 2012; Taranto et al., 2016). Strong short term mean-reversion, and the consequent failure to reproduce realistic signature plots, is one of the main drawbacks of the Santa-Fe model. The problem manifests in many different ways. For example, the model predicts long-term volatility to be much too small for large-tick stocks and somewhat too large for small-tick stocks, and incorrectly predicts a negative correlation between the ratio of long-term volatility and short-term volatility and tick size.

For the parameter value estimates for large-tick stocks, the model in fact predicts that the queues almost never empty, and the mid-price almost never moves. In real markets, these extremely long emptying times are tempered, in part through the dynamical coupling between the bid queue and the ask queue, and in part because of the existence of large market orders that consume a substantial fraction the queue at once. Both of these important empirical effects are absent from the Santa Fe model.

For small-tick stocks, the model predicts values of volatility higher than those observed empirically. The main reason for this weakness is because of the absence of a mechanism that accurately describes how order flows adapt when prices change. In the model, once the best quote has disappeared, the order flow immediately adapts around the new mid-price, irrespective of whether the price change was caused by a cancellation, a market order arrival, or a limit order arrival inside the spread. In other words, the permanent impact of all of these events are identical, whereas in reality the permanent impact of a market order arrival is much larger than that of cancellations, as shown in Eisler et al. (2012).

4.3.3 Impact of Market Orders and Market-Making

Let us now analyze in more detail the lag-dependent impact of market orders in the Santa-Fe model. We define this impact as

(12) R(τ):=〈εt⋅(mt+τ−mt)〉t,

where εt![]() denotes the sign of the market order at event-time t, where t increases by one unit for each market order arrival, and the brackets mean an empirical average over t. In real markets the impact function R(τ)

denotes the sign of the market order at event-time t, where t increases by one unit for each market order arrival, and the brackets mean an empirical average over t. In real markets the impact function R(τ)![]() is positive and grows with τ before saturating for large τs, see e.g. Bouchaud et al. (2004, 2006) and Wyart et al. (2008). In the Santa Fe model, however, R(τ)

is positive and grows with τ before saturating for large τs, see e.g. Bouchaud et al. (2004, 2006) and Wyart et al. (2008). In the Santa Fe model, however, R(τ)![]() is strictly constant, independent of τ, and is well approximated by

is strictly constant, independent of τ, and is well approximated by

(13) R(τ)≈P(Vbest=1)×12〈first gap〉,

where P(Vbest=1)![]() is the probability that the best queue is of length 1. This approximation holds because a market order of size unity impacts the price if and only if it completely consumes the volume at the opposite-side best quote, and if it does so, it moves that quote by the size of the first gap, and thus moves the mid-price by half this amount. Since order flow in the Santa Fe model is uncorrelated and is always centered around the current mid-price, the impact of a market order is instantaneous and permanent. Therefore, the model predicts that R(τ)

is the probability that the best queue is of length 1. This approximation holds because a market order of size unity impacts the price if and only if it completely consumes the volume at the opposite-side best quote, and if it does so, it moves that quote by the size of the first gap, and thus moves the mid-price by half this amount. Since order flow in the Santa Fe model is uncorrelated and is always centered around the current mid-price, the impact of a market order is instantaneous and permanent. Therefore, the model predicts that R(τ)![]() is constant in τ. In real markets, by contrast, the signs of market orders show strong positive autocorrelation, which causes R(τ)

is constant in τ. In real markets, by contrast, the signs of market orders show strong positive autocorrelation, which causes R(τ)![]() to increase with τ (Bouchaud et al., 2004, 2006; Wyart et al., 2008).

to increase with τ (Bouchaud et al., 2004, 2006; Wyart et al., 2008).

This simple observation has an important immediate consequence: The Santa Fe model specification leads to profitable market-making strategies. It is plain to see that market-making is profitable if the mean bid–ask spread is larger than twice the long-term impact R∞![]() (Wyart et al., 2008). In the Santa Fe model, the mean first gap is found to be smaller than the bid–ask spread (see Fig. 2). Therefore, from Eq. (13), one necessarily has R∞<〈s〉/2

(Wyart et al., 2008). In the Santa Fe model, the mean first gap is found to be smaller than the bid–ask spread (see Fig. 2). Therefore, from Eq. (13), one necessarily has R∞<〈s〉/2![]() , so market-making is “easy” within this framework. If we want to avoid the existence of such opportunities, which are absent in real markets, we need to find a way to extend the Santa Fe model. One possible route for doing so is incorporating some strategic behavior into the model, such as introducing agents that specifically seek out and capitalize on any simple market-making opportunities that arise. Another route is to modify the model's assumptions regarding order flow to better reflect the empirical properties observed in real markets. For example, introducing the empirically observed autocorrelation in market order signs would increase the long-term impact R∞

, so market-making is “easy” within this framework. If we want to avoid the existence of such opportunities, which are absent in real markets, we need to find a way to extend the Santa Fe model. One possible route for doing so is incorporating some strategic behavior into the model, such as introducing agents that specifically seek out and capitalize on any simple market-making opportunities that arise. Another route is to modify the model's assumptions regarding order flow to better reflect the empirical properties observed in real markets. For example, introducing the empirically observed autocorrelation in market order signs would increase the long-term impact R∞![]() and thereby reduce the profitability of market-making. This is the direction taken in the next section.

and thereby reduce the profitability of market-making. This is the direction taken in the next section.

5 An Improved Model for the Dynamics of Liquidity

5.1 Introduction

The Santa-Fe model was originally proposed as a model of the visible LOB. However, most of the liquidity in financial markets remains latent, and only gets revealed when execution is highly probable. This latent order book is where the “true” liquidity of the market lies, at variance with the real order book where only a very small fraction of this liquidity is revealed, and that evolves on very fast time scales (i.e. large values of ν). In particular, market making/high frequency trading contributes heavily to the latter but only very thinly to the former, which corresponds to much smaller values of ν.5 The vast majority of the daily traded volume in fact progressively reveals itself as trading proceeds: liquidity is a dynamical process – see Bouchaud et al. (2004, 2006, 2009), Weber and Rosenow (2005), and for an early study carrying a similar message, Sandas (2001). When one wants understand the impact of long metaorders – and in particular the square-root law, see Section 3.2 – it is clearly more important to model this latent liquidity, not seen in the LOB, than the LOB itself. We therefore need a modeling strategy that is able to describe the dynamics of the latent liquidity, and how it is perturbed by a metaorder. This is what we will pursue in the following sections.

In order to describe prices movements on medium to long time scales, one should therefore understand the dynamics of the “latent liquidity” (LL). The simplest model for the LL is again the Santa-Fe model, now interpreted in terms of latent intentions – rather than visible limit orders. We imagine that the volume in the latent order book materializes in the real order book with a probability that increases sharply when the distance between the traded price and the limit price decreases.

As we have seen in the previous section, one of the main drawback of the Santa-Fe model is the strong mean-reversion effects on time scales small compared to the renewal time of the LL Tm=ν−1![]() , assumed to be large (hours or days – see below). Some additional features must be introduced to allow the price to be diffusive, with a “flat” signature plot (Tóth et al., 2011; Mastromatteo et al., 2014a). In the present extension of the Santa-Fe model, we still assume the deposition rate λ of limit orders and the cancellation rate ν to be constants, independent of the price level. The sign of market orders, on the other hand, is determined by a non-trivial process, such as to generate long-range correlations, in agreement with empirical findings (Bouchaud et al., 2009). More precisely, the sign εt

, assumed to be large (hours or days – see below). Some additional features must be introduced to allow the price to be diffusive, with a “flat” signature plot (Tóth et al., 2011; Mastromatteo et al., 2014a). In the present extension of the Santa-Fe model, we still assume the deposition rate λ of limit orders and the cancellation rate ν to be constants, independent of the price level. The sign of market orders, on the other hand, is determined by a non-trivial process, such as to generate long-range correlations, in agreement with empirical findings (Bouchaud et al., 2009). More precisely, the sign εt![]() of market order at (event) time t has zero mean, 〈εt〉=0

of market order at (event) time t has zero mean, 〈εt〉=0![]() , but is characterized by a power-law decaying autocorrelation function C(ℓ)∝ℓ−γ

, but is characterized by a power-law decaying autocorrelation function C(ℓ)∝ℓ−γ![]() with γ<1

with γ<1![]() , see Section 2.8. A way to do this in practice is to use the Lillo–Mike–Farmer model (Lillo et al., 2005), or the so-called DAR(p) model (see e.g. Taranto et al., 2016).

, see Section 2.8. A way to do this in practice is to use the Lillo–Mike–Farmer model (Lillo et al., 2005), or the so-called DAR(p) model (see e.g. Taranto et al., 2016).

Another ingredient of the model is the statistics of the volume consumed by each single market order. In the Santa-Fe model, each market order is of unit volume υ0![]() . However, this is unrealistic, since more volume at the best is a clear incentive to send larger market orders, in order to accelerate trading without immediately impacting the price. It is more reasonable to assume selective liquidity taking, i.e. that the size of market order VMO

. However, this is unrealistic, since more volume at the best is a clear incentive to send larger market orders, in order to accelerate trading without immediately impacting the price. It is more reasonable to assume selective liquidity taking, i.e. that the size of market order VMO![]() is an increasing function of the prevailing volume at the best Vbest

is an increasing function of the prevailing volume at the best Vbest![]() . A simple specification is the following (Mastromatteo et al., 2014a):

. A simple specification is the following (Mastromatteo et al., 2014a):

(14) VMO=υ1−ψ0Vψbest

with ψ∈[0,1]![]() , so that υ0⩽VMO⩽Vbest

, so that υ0⩽VMO⩽Vbest![]() . Clearly, larger values of ψ correspond to more aggressive orders, so that ψ=1

. Clearly, larger values of ψ correspond to more aggressive orders, so that ψ=1![]() corresponds to eating the all the available liquidity at the best price and ψ=0

corresponds to eating the all the available liquidity at the best price and ψ=0![]() corresponds to unit size execution. In fact, the model with ψ=0

corresponds to unit size execution. In fact, the model with ψ=0![]() and γ→∞

and γ→∞![]() (no correlation of the order flow) precisely recovers the Santa-Fe specification of the previous section.

(no correlation of the order flow) precisely recovers the Santa-Fe specification of the previous section.

As already emphasized, the cancellation rate defines a time scale Tm=ν−1![]() which is of crucial importance for the model, since this is the memory time of the market. For times much larger than Tm

which is of crucial importance for the model, since this is the memory time of the market. For times much larger than Tm![]() , all limit orders have been canceled and replaced elsewhere, so that no memory of the initial (latent) order book can remain. Now, as we emphasized in Section 3.3, a concave (non-additive) impact law can only appear if some kind of memory is present. Therefore, we will study the dynamics of the system in a regime where times are small compared to Tm

, all limit orders have been canceled and replaced elsewhere, so that no memory of the initial (latent) order book can remain. Now, as we emphasized in Section 3.3, a concave (non-additive) impact law can only appear if some kind of memory is present. Therefore, we will study the dynamics of the system in a regime where times are small compared to Tm![]() . From a mathematical point of view, rigorous statements about the diffusive nature of the price, and the non-additive nature of the impact, can only be achieved in the limit where ν/μ→0

. From a mathematical point of view, rigorous statements about the diffusive nature of the price, and the non-additive nature of the impact, can only be achieved in the limit where ν/μ→0![]() , i.e. in markets where the latent liquidity profile changes on a time scale very much longer than the inverse trading frequency. Although Tm

, i.e. in markets where the latent liquidity profile changes on a time scale very much longer than the inverse trading frequency. Although Tm![]() is very hard to estimate directly using market data,6 it is reasonable to think that trading decisions only change when the transaction price changes by a few percent, which leads to Tm

is very hard to estimate directly using market data,6 it is reasonable to think that trading decisions only change when the transaction price changes by a few percent, which leads to Tm![]() ∼ a few days in stocks and futures markets. Hence, we expect the ratio ν/μ

∼ a few days in stocks and futures markets. Hence, we expect the ratio ν/μ![]() to be indeed very small, on the order of 10−5

to be indeed very small, on the order of 10−5![]() , in these markets. (In other words, 10,000 to 100,000 trades take place before the memory of the latent liquidity is lost.)

, in these markets. (In other words, 10,000 to 100,000 trades take place before the memory of the latent liquidity is lost.)

5.2 Super-Diffusion vs. Sub-Diffusion