Heterogeneous Agent Models in Finance✶

Roberto Dieci⁎; Xue-Zhong He†,1 ⁎University of Bologna, Bologna, Italy

†University of Technology Sydney, Sydney, NSW, Australia

1Corresponding author. email address: [email protected]

Abstract

This chapter surveys the state-of-art of heterogeneous agent models (HAMs) in finance using a jointly theoretical and empirical analysis, combined with numerical analysis from the latest development in computational finance. It provides supporting evidence on the explanatory power of HAMs to various stylized facts and market anomalies through model calibration, estimation, and economic mechanisms analysis. It presents HAMs with the mainstream finance a unified framework in continuous time to study the impact of historical price information on price dynamics, profitability and optimality of fundamental and momentum trading. It demonstrates how HAMs can help to understand stock price co-movements and evolutionary CAPM. It also introduces a new HAMs perspective on house price dynamics and an integrate approach to study dynamics of limit order markets. The survey provides further insights into the complexity and efficiency of financial markets and policy implications.

Keywords

Heterogeneity; Bounded rationality; Heterogeneous agent-based models; Stylized facts; Asset pricing; Housing bubbles; Limit order markets; Information efficiency; Comovement

1 Introduction

Economic and finance theory is witnessing a paradigm shift from a representative agent with rational expectations to boundedly rational agents with heterogeneous expectations. This shift reflects a growing evidence on the theoretical limitations and empirical challenges in the traditional view of homogeneity and perfect rationality in finance and economics.

The existence of limitations to fully rational behavior and the roles of psychological phenomena and behavioral factors in individuals' decision making have been emphasized and discussed from a variety of different standpoints in the economics and finance literature (see, e.g. Simon, 1982, Sargent, 1993, Arthur, 1994, Conlisk, 1996, Rubinstein, 1998, and Shefrin, 2005). Due to endogenous uncertainty about the state of the world and limits to information and computational ability, agents are prevented from forming rational forecasts and solving life-time optimization problems. Rather, agents favor simple reasoning and ‘rules of thumb’, such as the well documented technical analysis and active trading from financial market professionals.1 In addition, empirical investigations of financial time series show a number of market phenomena (including bubbles, crashes, short-run momentum and long-run mean reverting in asset prices) and some common features, the so-called stylized facts,2 which are difficult to accommodate and explain within the standard paradigm based on homogeneous agents and rational expectations.

Moreover, agents are heterogeneous in their beliefs and behavioral rules, which may change over time due to social interaction and evolutionary selection (see Lux, 1995, Arthur et al., 1997b, and Brock and Hommes, 1998). Such heterogeneity and diversity in individual behavior in economics, along with social interaction among individuals, can hardly be captured by a ‘representative’ agent at the aggregate level (see Kirman, 1992, 2010 for extensive discussions). For instance, as Heckman (2001), the 2000 Nobel Laureate in Economics, points out (concerning the contribution of microeconometrics to economic theory), “the most important discovery was the evidence on pervasiveness of heterogeneity and diversity in economic life. When a full analysis was made of heterogeneity in response, a variety of candidate averages emerged to describe the average person, and the longstanding edifice of the representative consumer was shown to lack empirical support.” Regarding agents' behavior during crisis periods and the role of policy makers, the former ECB president Jean-Claude Trichet writes “We need to deal better with heterogeneity across agents and the interaction among those heterogeneous agents”, highlighting the potential of alternative approaches such as behavioral economics and agent-based modeling.

Over the last three decades, empirical evidence, unconvincing justification of the assumption of unbounded rationality, and role of investor psychology have led to an incorporation of heterogeneity in beliefs and bounded rationality of agents into financial market modeling and asset pricing theory. This has changed the landscape of finance theory dramatically and led to fruitful development in financial economics, empirical finance, and market practice. In this chapter, we focus on the state-of-the-art of this expanding research field, denoted as Heterogeneous Agent Models (HAMs) in finance.

HAMs start from the contributions of Day and Huang (1990), Chiarella (1992), de Grauwe et al. (1993), Lux (1995), Brock and Hommes (1998), inspired by the pioneering work of Zeeman (1974) and Beja and Goldman (1980). This modeling framework views financial market dynamics as a result of the interaction of heterogeneous investors with different behavioral rules, such as fundamental and technical trading rules. One of the key aspects of these models is the expectation feedback mechanism. Namely, agents' decisions are based upon the predictions of endogenous variables whose actual values are determined by the expectations of agents. This results in the co-evolution of beliefs and asset prices over time. Earlier HAMs develop various nonlinear models to characterize various endogenous mechanisms of market fluctuations and financial crisis resulting from the interaction of heterogeneous agents rather than exogenous shocks or news. Overall, such models demonstrate that asset price fluctuations can be caused endogenously. We refer to Hommes (2006), LeBaron (2006), Chiarella et al. (2009a), Hommes and Wagener (2009), Westerhoff (2009), Chen et al. (2012), Hommes (2013), and He (2014) for surveys of these developments in the literature.

HAMs have strong connections with a broader area of Agent-Based Models (ABMs) and Agent-based Computational Economics (ACE). In fact, HAMs can be regarded as particular types of ABMs. However, generally speaking, ABMs are by nature very computationally oriented and allow for a large number of interacting agents, network structures, many parameters, and thorough descriptions of the underlying market microstructures. As such, they turn out to be extremely flexible and powerful, suitable for simulation, scenario analysis and regulation of real-world dynamic systems (see, e.g. Tesfatsion and Judd, 2006, LeBaron and Tesfatsion, 2008). By contrast, HAMs are typically characterized by substantial simplifications at the modeling level (few belief-types or behavioral rules, simplified interaction structures and reduced number of parameters). This makes HAMs analytically tractable to some extent, mostly within the theoretical framework of nonlinear dynamical systems. However, unlike computationally oriented ABMs, HAMs allow a deeper understanding of the basic dynamic mechanisms and driving forces at work, making it possible to identify different and clear-cut ‘types’ of macro outcomes in connection to specific agents' behavior.

Among the large number of HAMs in finance, this chapter is mostly concerned with analytically tractable models based on the interplay of two broad types of beliefs: extrapolative vs. regressive (or technical vs. fundamental rules, or chartists vs. fundamentalists). Since chartists rely on extrapolative rules to forecast future prices and to take their position in the market, they tend to sustain and reinforce current price trends or to amplify the deviations from the ‘fundamental price’. By contrast, fundamentalists place their orders in view of a mean reversion of asset price to its fundamental in long-run. The interplay between such forces is able to capture, albeit in a simplified manner, a basic mechanism of price fluctuations in financial markets. Support to this kind of behavioral heterogeneity comes from survey evidence (Menkhoff and Taylor, 2007, Menkhoff, 2010), experimental evidence (Hommes et al., 2005, Heemeijer et al., 2009), and empirically grounded discussion on the profitability of momentum and mean reversion strategies in financial markets (e.g. Lakonishok et al., 1994, Jegadeesh and Titman, 2001, Moskowitz et al., 2012).

In this chapter, we focus on the state-of-the-art of HAMs in finance from five main strands of the literature developed approximately over the last ten years since the appearance of the previous contributions in Volume II of this Handbook series. This development can have profound consequences for the interpretation of empirical evidence and the formulation of economic policy.

The first strand of research (Section 2) emphasizes the lasting potential of stylized HAMs in discrete time (in particular, chartist-fundamentalist models) to address key issues in finance. Such models have been largely investigated in the past in a wide range of versions incorporating heterogeneity, adaptation, evolution, and even learning (Hommes, 2001, Chiarella and He, 2002, 2003, and Chiarella et al., 2002, 2006b). They have successfully explained various market behavior, such as the long-term swing of market prices from fundamental price, asset bubbles, and market crashes, showing a potential to characterize and explain the stylized facts (Alfarano et al., 2005, Gaunersdorfer and Hommes, 2007) and various power law behavior (He and Li, 2008 and Lux and Alfarano, 2016) observed in financial markets. In addition, the chartist-fundamentalist framework can still provide insight into various stylized facts and market anomalies, and relate them to the economic mechanisms, parameters and scenarios of the underlying nonlinear deterministic systems. Such promising perspectives have motivated further empirical studies, leading to a growing literature on the calibration and estimation of the HAMs. In particular, in Sections 2.1 and 2.2, we focus on a simple HAM of Dieci et al. (2006) to illustrate its explanatory power to volatility clustering through calibration and empirical estimation, and relate the results to the underlying mechanisms and bifurcations of the nonlinear deterministic ‘skeleton’. Moreover, by considering an integrated approach of HAMs and incomplete information about the fundamental value, we provide a micro-foundation to the endogenous trading heterogeneity and switching behavior wildly characterized in HAMs (Section 2.3). We also survey fund flow effect among competing and evolving investment strategies (Section 2.4).

The second strand (Section 3) is on the development of a general framework in continuous time HAMs to incorporate historical price information in the HAMs. It provides a plausible way to deal with a variety of expectation rules formed from historical prices via moving averages over different time horizons, through a parsimonious system of stochastic delay differential equations. We introduce a time delay parameter to measure the effect of historical price information. Besides being consistent with continuous-time finance, this framework appears promising to understand the impact on market stability of lagged information (incorporated in different moving average rules and in realized profits recorded over different time horizons) and to explain a number of phenomena, particularly the long-range dependence in financial markets. We illustrate this approach and the main results in Section 3.1 by surveying the model in He and Li (2012). We emphasize the similarities to and differences from discrete-time HAMs. Moreover, Sections 3.2 and 3.3 demonstrate how useful the continuous-time HAMs can be in addressing the profitability of momentum and contrarian strategies and the optimal allocation with time series momentum and reversal, two of the most dominating financial market anomalies.

The third strand (Section 4) is on the impact of heterogeneous beliefs, expectations feedback and portfolio diversification on the joint dynamics of prices and returns of multiple risky assets. A related issue concerns the joint dynamics of international asset markets, driven by heterogeneous speculators who switch across markets depending on relative profit opportunities. In such models, often described by dynamical systems of large dimension, the typical nonlinear features of baseline HAMs interact with additional nonlinearities that arise naturally within a multi-asset setting, such as the beliefs about second moments and correlations. Section 4 surveys such models, starting from the basic setup developed by Westerhoff (2004), in which investors can switch not only across strategies but across markets (Section 4.1). Such models are not only able to reproduce various stylized facts, but also to offer some explanations to price comovements and cross-correlations of volatilities reported empirically (Schmitt and Westerhoff, 2014), as well as to address some key regulatory issues (Westerhoff and Dieci, 2006). Further research deals with asset comovements and changes in correlations from a different perspective. Based on models of evolving beliefs and (mean-variance) portfolios of heterogeneous investors, Section 4.2 is devoted to the multi-asset HAM of Chiarella et al. (2013b). This approach appears quite promising to address the issue of ‘time-varying betas’ within an evolutionary CAPM framework. It establishes a link between investors' behavior and changes in risk-return relationships at the aggregate level. Finally, Section 4.3 applies HAMs to illustrate the potentially destabilizing impact of the interlinkages between stock and foreign exchange markets (Dieci and Westerhoff, 2010, 2013b).

The fourth strand (Section 5) investigates the dynamics of house prices from the perspective of HAMs. Similar to financial markets, housing markets have long been characterized by boom-bust cycles and other phenomena apparently unrelated to changes in economic fundamentals, such as short-term positive autocorrelation and long-term mean-reversion, which are at odds with the predictions of the rational representative agent framework. Moreover, peculiar features of the housing market (such as the ‘twofold’ nature of housing, illiquidity, and supply-side elasticity) may interact with investors' demand influenced by behavioral factors. Section 5.1 surveys two recent HAMs of the housing market (Bolt et al., 2014 and Dieci and Westerhoff, 2016) which are based on mean-variance preferences and standard equilibrium conditions, with the fundamental price being regarded as the present value of future expected rental payments. However, within this framework, investors form heterogeneous expectations about future house prices, according to (evolving) regressive and extrapolative beliefs. Estimation of similar models supports the assumption of behavioral heterogeneity changing over time, based on the relative performance of the competing prediction rules. It highlights how such heterogeneity can produce endogenous house price bubbles and crashes (disconnected from the dynamics of the fundamental price). Moreover, the nonlinear dynamic analysis of such models can provide a simple behavioral explanation for the observed role of supply elasticity in ‘shaping’ housing bubbles and crashes, as widely reported and discussed in empirical and theoretical literature (see, e.g. Glaeser et al., 2008). Further ‘disequilibrium’ models, illustrated in Section 5.2, confirm the main findings about the impact of behavioral heterogeneity on housing price dynamics.

The fifth strand (Section 6) is on an integrated approach combining HAMs with traditional market microstructure literature to examine the joint impact of information asymmetry, heterogeneous expectations, and adaptive learning in limit order markets. As shown in Section 6.1, these HAMs are very helpful in examining complexity in market microstructure, providing insight into the impact of heterogeneous trading rules on limit order book and order flows (Chiarella and Iori, 2002, Chiarella et al., 2009b, 2012b, Kovaleva and Iori, 2014), and replicating the stylized facts in limit order markets (Chiarella et al., 2017). Earlier HAMs mainly examine the endogenous mechanism of interaction of heterogeneous agents, less so about information asymmetry, which is the focus of traditional market microstructure literature under rational expectations. Moreover, while the current microstructure literature focuses on informed traders by simplifying the behavior of uninformed traders substantially, a thorough modeling of the learning behavior of uninformed traders appears crucial for trading and market liquidity (O'Hara, 2001). Section 6.2 surveys a contribution in this direction by Chiarella et al. (2015a). By integrating HAMs with asymmetric information and Genetic Algorithm (GA) learning into microstructure literature, they examine the impact of learning on order submission, market liquidity, and price discovery. Finally, very recent contributions (in Sections 6.3 and 6.4) further examine the impact of high frequency trading (Arifovic et al., 2016) and different regulations (Lensberg et al., 2015) on market in a GA learning environment.

Most of the development surveyed in this chapter is based on a jointly theoretical and empirical analysis, combined with numerical simulations and Monte Carlo analysis from the latest development in computational finance. It provides very rich approaches to deal with various issues in equity market, housing market, and market microstructure. The results provide some insights into our understanding of the complexity and efficiency of financial market and policy implications.

2 HAMs of Single Asset Market in Discrete-Time

Empirical evidence of various stylized facts and anomalies in financial markets, such as fat tails in return distribution, long-range dependence in volatility, and time series momentum and reversal, has stimulated increasing research interest in financial market modeling. By focusing on endogenous heterogeneity of investor behavior, HAMs play a very important role in providing insights into the importance of investor heterogeneity and explaining stylized facts and marker anomalies observed in financial time series. Early HAMs consider two types of traders, typically fundamentalists and chartists. Beja and Goldman (1980), Day and Huang (1990), Chiarella (1992), Lux (1995), and Brock and Hommes (1997, 1998) are amongst the first to have shown that interaction of agents with heterogeneous expectations can lead to market instability. These HAMs have successfully explained market booms, crashes, and the deviations of market price from fundamental price and replicated some of the stylized facts, which are nicely surveyed in Hommes (2006), LeBaron (2006), and Chiarella et al. (2009a). The promising perspectives of HAMs have stimulated further studies on empirical testing in different markets, including commodity markets (Baak, 1999, Chavas, 2000), stock markets (Boswijk et al., 2007; Franke, 2009; Franke and Westerhoff, 2011, 2012; Chiarella et al., 2012a, 2014; He and Li, 2015a, 2015b), foreign exchange markets (Westerhoff and Reitz, 2003; de Jong et al., 2010; ter Ellen et al., 2013), mutual funds (Gomes and Michaelides, 2008), option markets (Frijns et al., 2010), oil markets (ter Ellen and Zwinkels, 2010), and CDS markets (Chiarella et al., 2015b). HAMs have also been estimated with contagious interpersonal communication by Gilli and Winker (2003), Alfarano et al. (2005), Lux (2009a, 2012), and other works reviewed in Chen et al. (2012).

This development has spurred recent attempts at theoretical explanations and the underlying economic mechanism analysis, which is nicely summarized in a recent survey of Lux and Alfarano (2016). Several behavioral mechanisms on volatility clustering have been proposed based on the underlying deterministic dynamics (He and Li, 2007, 2015b, 2017, Gaunersdorfer et al., 2008, He et al., 2016b), stochastic herding (Alfarano et al., 2005), and stochastic demand (Franke and Westerhoff, 2011, 2012).

In this section, we use the simple HAM of Dieci et al. (2006) to illustrate the explanatory power of the model to investor behavior and provide some of the underlying mathematical and economic mechanisms to volatility clustering and long-range dependence in volatility. We first introduce the model of boundedly rational and adaptive switching behavior of investors in financial markets in Section 2.1. We then provide two particular mechanisms to explain volatility clustering and long memory in return volatility based on the underlying deterministic dynamics in Section 2.2. Mathematically, the first is based on the local stability and Hopf bifurcation, explored in He and Li (2007), while the second is characterized by the coexistence of two locally stable attractors with different size, proposed initially in Gaunersdorfer et al. (2008) and further developed theoretically in He et al. (2016b). Economically, it demonstrates that the dominance of trend chasing behavior when investors cannot change their strategies or the intensive switching behavior of investors to switch to more profitable strategy can explain volatility clustering and long memory in return volatility, while the noise traders also play a very important role.

In Section 2.3, we briefly discuss He and Zheng (2016) about the emergence of trading heterogeneity due to information uncertainty and strategic trading of agents. Through an integrated approach of HAMs and incomplete information about the fundamental value, He and Zheng (2016) provide an endogenous self-correction mechanism of the market. This mechanism is very different from the HAMs with complete information, in which mean-reverting is channeled through some kind of nonlinear assumptions on the demand or order flow of risky asset and market stability depends exogenously on balanced activities from fundamental and momentum trading. The approach provides a micro-foundation to endogenous trading heterogeneity and switching behavior wildly characterized in HAMs. We complete the section with a discussion about an evolutionary finance framework in Section 2.4 to examine the effect of the flows of funds among competing and evolving investment styles on investment performance.

2.1 Market Mood and Adaptive Behavior

Empirical evidence in foreign exchange markets (Allen and Taylor, 1990, Taylor and Allen, 1992, Menkhoff, 1998, and Cheung et al., 2004) and managing fund industrial (Menkhoff, 2010) suggests that agents have different information and/or beliefs about market processes. They use not only fundamental but also technical analyses, which are consistent with short-run momentum and long-run reversal behavior in financial markets. In addition, although some agents do not change their particular trading strategies, there are agents who may switch to more profitable strategies over time. Recent laboratory experiments in Hommes et al. (2005), Anufriev and Hommes (2012), and Hommes and in't Veld (2015) also show that agents using simple “rule of thumb” trading strategies are able to coordinate on a common prediction rule. Therefore heterogeneity in expectations and adaptive behavior are crucial to describe individual forecasting and aggregate price behavior.

Motivated by the empirical and experiment evidence, Dieci et al. (2006) introduce a simple financial market of fundamentalists and trend followers. Some agents switch between different strategies over time according to their performance, characterizing the adaptively rational behavior of agents. Others are confident and stay with their strategies over time, representing market mood. It turns out that this simple model is rich enough to illustrating the complicated price dynamics and to exploring different mechanisms in generating volatility clustering and long memory in volatility. In the following, we first outline the model, discuss calibration and empirical estimation of the model, and then provide an analysis on the two underlying mechanisms (see Dieci et al., 2006 and He and Li, 2008, 2017 for the detail).

Consider a financial market with one risky asset and one risk free asset. Let r be the constant risk free rate, pt![]() the price, and dt

the price, and dt![]() the dividend of the risky asset at time t. Assume that there are four types of investors, fundamental traders (or fundamentalists), trend followers (or chartists) and noise traders, and one market maker. Let n3

the dividend of the risky asset at time t. Assume that there are four types of investors, fundamental traders (or fundamentalists), trend followers (or chartists) and noise traders, and one market maker. Let n3![]() be the population fraction of the noise traders. Among 1−n3

be the population fraction of the noise traders. Among 1−n3![]() , the fractions of the fundamentalists and trend followers have fixed, n1

, the fractions of the fundamentalists and trend followers have fixed, n1![]() and n2

and n2![]() , and switching, n1,t

, and switching, n1,t![]() and n2,t=1−n1,t

and n2,t=1−n1,t![]() , components respectively. Denote n0=n1+n2,m0=(n1−n2)/n0

, components respectively. Denote n0=n1+n2,m0=(n1−n2)/n0![]() and mt=n1,t−n2,t

and mt=n1,t−n2,t![]() . Then the market fractions Qh,t

. Then the market fractions Qh,t![]() (h=1,2,3

(h=1,2,3![]() ) of the fundamentalists, trend followers, and noise traders at time t can be rewritten as, respectively,

) of the fundamentalists, trend followers, and noise traders at time t can be rewritten as, respectively,

(1) {Q1,t=12(1−n3)[n0(1+m0)+(1−n0)(1+mt)],Q2,t=12(1−n3)[n0(1−m0)+(1−n0)(1−mt)],Q3,t=n3.

Let Rt+1=pt+1+dt+1−Rpt![]() be the excess return and R=1+r

be the excess return and R=1+r![]() . We model the order flow3 zh,t

. We model the order flow3 zh,t![]() of type-h investors from t to t+1

of type-h investors from t to t+1![]() by zh,t=Eh,t(Rt+1)/(ahVh,t(Rt+1))

by zh,t=Eh,t(Rt+1)/(ahVh,t(Rt+1))![]() , where Eh,t

, where Eh,t![]() and Vh,t

and Vh,t![]() are the conditional expectation and variance at time t and ah

are the conditional expectation and variance at time t and ah![]() is the risk aversion coefficient of type h traders. The order flow of the noise traders ξt∼N(0,σ2ξ)

is the risk aversion coefficient of type h traders. The order flow of the noise traders ξt∼N(0,σ2ξ)![]() is an i.i.d. random variable. Then the population weighted average order flow is given by Ze,t=Q1,tz1,t+Q2,tz2,t+n3ξt.

is an i.i.d. random variable. Then the population weighted average order flow is given by Ze,t=Q1,tz1,t+Q2,tz2,t+n3ξt.![]() To determine the market price, we follow Chiarella and He (2003) and assume that the market price is determined by the market maker as follows,

To determine the market price, we follow Chiarella and He (2003) and assume that the market price is determined by the market maker as follows,

(2) pt+1=pt+λZe,t=pt+μze,t+δt,

where ze,t=q1,tz1,t+q2,tz2,t![]() , qh,t=Qh,t/(1−n3)

, qh,t=Qh,t/(1−n3)![]() for h=1,2

for h=1,2![]() , λ denotes the speed of price adjustment of the market maker, μ=(1−n3)λ

, λ denotes the speed of price adjustment of the market maker, μ=(1−n3)λ![]() and δt∼N(0,σ2δ)

and δt∼N(0,σ2δ)![]() with σδ=λn3σξ

with σδ=λn3σξ![]() .

.

We now describe briefly the heterogeneous beliefs of the fundamentalists and trend followers and the adaptive switching mechanism. The conditional mean and variance for the fundamental traders are assumed to follow

(3) E1,t(pt+1)=pt+(1−α)[Et(p⁎t+1)−pt],V1,t(pt+1)=σ21,

where p⁎t![]() is the fundamental value of the risky asset following a random walk,

is the fundamental value of the risky asset following a random walk,

(4) p⁎t+1=p⁎texp(−σ2ε2+σεεt+1),εt∼N(0,1),σε≥0,p⁎0=p⁎>0,

εt![]() is independent of the noise process δt

is independent of the noise process δt![]() , σ21

, σ21![]() is constant, and hence Et(p⁎t+1)=p⁎t

is constant, and hence Et(p⁎t+1)=p⁎t![]() . Here (1−α)

. Here (1−α)![]() measures the speed of price adjustment towards the fundamental price with 0<α<1

measures the speed of price adjustment towards the fundamental price with 0<α<1![]() . A high α indicates less confidence on the convergence to the fundamental price, leading to a slower adjustment of the market price to the fundamental. For the trend followers, we assume

. A high α indicates less confidence on the convergence to the fundamental price, leading to a slower adjustment of the market price to the fundamental. For the trend followers, we assume

(5) E2,t(pt+1)=pt+γ(pt−ut),V2,t(pt+1)=σ21+b2vt,

where γ⩾0![]() measures the extrapolation of the trend, ut

measures the extrapolation of the trend, ut![]() and vt

and vt![]() are sample mean and variance, respectively. We assume that ut=δut−1+(1−δ)pt

are sample mean and variance, respectively. We assume that ut=δut−1+(1−δ)pt![]() and vt=δvt−1+δ(1−δ)(pt−ut−1)2

and vt=δvt−1+δ(1−δ)(pt−ut−1)2![]() , representing limiting mean and variance of the geometric decay processes when the memory lag tends to infinity. Here δ∈(0,1)

, representing limiting mean and variance of the geometric decay processes when the memory lag tends to infinity. Here δ∈(0,1)![]() measures the geometric decay rate and b2≥0

measures the geometric decay rate and b2≥0![]() measures the sensitivity to the sample variance. For simplicity we assume that investors share a homogeneous belief about the dividend process dt

measures the sensitivity to the sample variance. For simplicity we assume that investors share a homogeneous belief about the dividend process dt![]() , which is i.i.d. and normally distributed with mean ˉd

, which is i.i.d. and normally distributed with mean ˉd![]() and variance σ2d

and variance σ2d![]() . Denote by p⁎=p⁎o=ˉd/r

. Denote by p⁎=p⁎o=ˉd/r![]() the long-run fundamental price.

the long-run fundamental price.

Let πh,t+1![]() be the realized profit between t and t+1

be the realized profit between t and t+1![]() of type-h investors, πh,t+1=zh,t(pt+1+dt+1−Rpt)

of type-h investors, πh,t+1=zh,t(pt+1+dt+1−Rpt)![]() for h=1,2

for h=1,2![]() . Following Brock and Hommes (1997, 1998), the market fraction of investors choosing strategy h at time t+1

. Following Brock and Hommes (1997, 1998), the market fraction of investors choosing strategy h at time t+1![]() is determined by

is determined by

nh,t+1=exp[β(πh,t+1−Ch)]∑iexp[β(πi,t+1−Ci)],h=1,2,

where β measures the intensity of the choice and Ch≥0![]() the cost. Together with (1) the market fractions and asset price dynamics are determined by the following random dynamic system in discrete-time,

the cost. Together with (1) the market fractions and asset price dynamics are determined by the following random dynamic system in discrete-time,

(6) {pt+1=pt+μ(q1,tz1,t+q2,tz2,t)+δt,δt∼N(0,σ2δ),ut=δut−1+(1−δ)pt,vt=δvt−1+δ(1−δ)(pt−ut−1)2,mt=tanh[β2(z1,t−1−z2,t−1−(C1−C2))(pt+dt−Rpt−1)].

2.2 Volatility Clustering: Calibration and Mechanisms

By conducting econometric analysis via Monte Carlo simulations, He and Li (2015b, 2017) show that the autocorrelations of returns, absolute returns and squared returns of the model developed above share the same pattern as those of the DAX 30. They further characterize the power-law behavior of the DAX 30 and find that the estimates of the power-law decay indices, the (FI)GARCH parameters, and the tail index of the model closely match those of the DAX 30. In the following we first report the calibrated results of the model developed in the previous subsection and then provide some insights into investor behavior and two underlying mechanisms of the volatility clustering.

When there is no switching between the two strategies, the above model reduces to the no-switching model in He and Li (2007), showing that the no-switching model is able to replicate the power-law behavior in return volatility. Based on the daily price index data of the DAX 30 from 11 August, 1975 to 29 June, 2007, He and Li (2015b, 2017) calibrate three scenarios of the above model: the no-switching (N) model with β=0![]() , pure-switching (S) model with n0=0

, pure-switching (S) model with n0=0![]() , and full (F) model of (6). The results are collected in Table 1 (with fixed r=5%p.a

, and full (F) model of (6). The results are collected in Table 1 (with fixed r=5%p.a![]() . and C1=C2=0

. and C1=C2=0![]() ). By conducting econometric analysis via Monte Carlo simulations based on the calibrated models, He and Li (2015b, 2017) find that, for all three scenarios, the estimates of the power-law decay indices d, the (FI)GARCH parameters, and the tail index of the calibrated model closely match those of the DAX 30. By conducting a Wald test Ho:dDAX=d

). By conducting econometric analysis via Monte Carlo simulations based on the calibrated models, He and Li (2015b, 2017) find that, for all three scenarios, the estimates of the power-law decay indices d, the (FI)GARCH parameters, and the tail index of the calibrated model closely match those of the DAX 30. By conducting a Wald test Ho:dDAX=d![]() at 5% and 1% significant levels (with the critical values of 3.842 and 6.635, respectively), He and Li (2017) show that switching model fits the data better than the no-switching and pure-switching models.

at 5% and 1% significant levels (with the critical values of 3.842 and 6.635, respectively), He and Li (2017) show that switching model fits the data better than the no-switching and pure-switching models.

Table 1

Calibrated parameters of the no-switching (N), pure-switching (S), and full (F) models

| α | γ | a 1 | a 2 | μ | n 0 | m 0 | δ | b | σ | σ δ | β | Wald | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | 0.858 | 8.464 | 6.024 | 0.383 | 0.946 | 1 | −0.200 | 0.292 | 6.763 | 0.24 | 3.473 | 0 | 112 |

| S | 0.513 | 0.764 | 7.972 | 0.231 | 2.004 | 0 | – | 0.983 | 3.692 | 0.231 | 3.268 | 0.745 | 108 |

| F | 0.488 | 1.978 | 7.298 | 0.320 | 1.866 | 0.313 | −0.024 | 0.983 | 3.537 | 0.231 | 3.205 | 0.954 | 106 |

Comparing the estimates of the three scenarios leads to different investor behavior. The estimated annual return volatility σ is close to the annual return volatility of the DAX 30. Higher a1![]() than a2

than a2![]() implies that the fundamentalists are more risk averse compared to the trend followers. For the no-switching scenario, a higher value of α indicates a slow price adjustment of the fundamentalists toward the fundamental value, while a higher value of γ indicates that the trend followers extrapolate the price trend actively. Without switching, mo=−0.2

implies that the fundamentalists are more risk averse compared to the trend followers. For the no-switching scenario, a higher value of α indicates a slow price adjustment of the fundamentalists toward the fundamental value, while a higher value of γ indicates that the trend followers extrapolate the price trend actively. Without switching, mo=−0.2![]() indicates that both the fundamentalists and trend followers are active in the market, which is however dominated by the trend followers (about 60%). On the full model, the market is dominated by investors (about 70%) who constantly switch between the fundamental and trend following strategies, although some investors (about 30%) never change their strategies over the time. This is consistent with the empirical findings discussed at the beginning of this section.

indicates that both the fundamentalists and trend followers are active in the market, which is however dominated by the trend followers (about 60%). On the full model, the market is dominated by investors (about 70%) who constantly switch between the fundamental and trend following strategies, although some investors (about 30%) never change their strategies over the time. This is consistent with the empirical findings discussed at the beginning of this section.

We now provide two mechanisms based on the underlying deterministic dynamics. The first one is on the local stability and periodic oscillation due to Hopf bifurcation, explored in He and Li (2007). Essentially, on the parameter space of the deterministic model, near the Hopf bifurcation boundary, the fundamental steady state can be locally stable but globally unstable. Due to the nature of Hopf bifurcation, such global instability leads to switching between the locally stable fundamental price and the periodic oscillations around the fundamental price. Then triggered by the fundamental and market noises, He and Li (2007) show that the interaction of the fundamental, risk-adjusted trend chasing from the trend followers, and the interplay of the noises and the underlying deterministic dynamics can be the source of power-law behavior in return volatility. Mathematically, the calibrated no-switching and switching models share the same underlying deterministic mechanism. Economically, however, they provide different behavioral mechanisms. With no-switching, it is the dominance of the trend followers (about 60%) that drives the power-law behavior. However, with both switching and no-switching investors, dominated by these traders (about 70%) who constantly switch between the two strategies. It is therefore the adaptive behavior of investors that generates the power-law behavior. This is also in line with Franke and Westerhoff (2012, 2016) who estimate various HAMs and show that herding behavior plays a key role in matching the stylized facts. More importantly, the noise traders play an important role in generating insignificant ACs on the returns, while the significantly decayed AC patterns of the absolute returns and squared returns are more influenced by the fundamental noise. As pointed out in Lux and Alfarano (2016), noise traders is probably a central ingredient of these models.

The second mechanism proposed initially in Gaunersdorfer et al. (2008) is characterized by the coexistence of two locally stable attractors with different size, while such coexistence is not required in the previous mechanism. Dieci et al. (2006) show that the above model can display such co-existence of locally stable fundamental steady state and periodic cycle. The interaction of the coexistence of the deterministic dynamics and the noise processes then triggers the switching among the two attractors and endogenously generates volatility clustering. More recently, by applying normal form analysis and center manifold theory, He et al. (2016b) provide the following theoretical result on the coexistence of the locally stable steady state and invariant circle of the underlying deterministic model (we refer to He et al., 2016b for the details).

Proposition 2.1

The underlying deterministic system of (6) has a unique fundamental steady state (p,u,v,m)=(ˉp,ˉp,0,ˉm)![]() with ˉm=tanhβ(C2−C1)2

with ˉm=tanhβ(C2−C1)2![]() . The fundamental steady state is locally asymptotically stable for γ∈(0,γ⁎⁎)

. The fundamental steady state is locally asymptotically stable for γ∈(0,γ⁎⁎)![]() , and it undergoes a Neimark–Sacker bifurcation at γ=γ⁎⁎

, and it undergoes a Neimark–Sacker bifurcation at γ=γ⁎⁎![]() , that is, there is an invariant curve near the fundamental steady state. Moreover, the bifurcated closed invariant curve is forward and stable when a(0)<0

, that is, there is an invariant curve near the fundamental steady state. Moreover, the bifurcated closed invariant curve is forward and stable when a(0)<0![]() and backward and unstable when a(0)>0

and backward and unstable when a(0)>0![]() , and a Chenciner (generalized Neimark–Sacker) bifurcation takes place when a(0)=0

, and a Chenciner (generalized Neimark–Sacker) bifurcation takes place when a(0)=0![]() . Here a(0)

. Here a(0)![]() is the first Lyapunov coefficient.

is the first Lyapunov coefficient.

Note that the market fractions of the fundamentalists and trend followers at the fundamental steady state are given by q1=(1+mq)/2![]() and q2=(1−mq)/2

and q2=(1−mq)/2![]() with mq=n0m0+(1−n0)ˉm

with mq=n0m0+(1−n0)ˉm![]() , respectively. When the cost of the fundamental strategy C1

, respectively. When the cost of the fundamental strategy C1![]() is higher than the cost of the trend following strategy C2

is higher than the cost of the trend following strategy C2![]() , an increase in the switching intensity β leads to a decrease in γ⁎⁎

, an increase in the switching intensity β leads to a decrease in γ⁎⁎![]() , meaning that the fundamental price becomes less stable when traders switch their strategies more often. This is essentially the rational routes to randomness of Brock and Hommes (1997, 1998).

, meaning that the fundamental price becomes less stable when traders switch their strategies more often. This is essentially the rational routes to randomness of Brock and Hommes (1997, 1998).

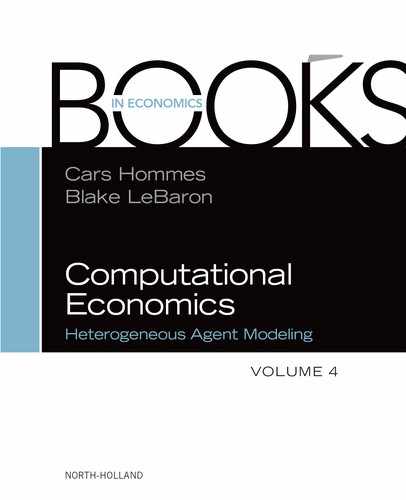

Fig. 1 illustrates two different types of Neimark–Sacker bifurcation. It is the sign of the first Lyapunov coefficient a(0)![]() that determines the bifurcation direction, either forward or backward, and the stability of the bifurcated invariant circles, leading to different bifurcation dynamics. When a(0)<0

that determines the bifurcation direction, either forward or backward, and the stability of the bifurcated invariant circles, leading to different bifurcation dynamics. When a(0)<0![]() , the bifurcation is forward and stable, meaning that the bifurcated invariant circle occurring for γ>γ⁎⁎

, the bifurcation is forward and stable, meaning that the bifurcated invariant circle occurring for γ>γ⁎⁎![]() is locally stable. In this case, as γ increases and passes γ⁎⁎

is locally stable. In this case, as γ increases and passes γ⁎⁎![]() , the fundamental steady state becomes unstable and the trajectory converges to an invariant circle bifurcating from the fundamental steady state. As γ increases further, the trajectory converges to invariant circles with different sizes. This is illustrated in Fig. 1A with γ⁎⁎≈0.93

, the fundamental steady state becomes unstable and the trajectory converges to an invariant circle bifurcating from the fundamental steady state. As γ increases further, the trajectory converges to invariant circles with different sizes. This is illustrated in Fig. 1A with γ⁎⁎≈0.93![]() where the two bifurcating curves for γ>γ⁎⁎

where the two bifurcating curves for γ>γ⁎⁎![]() indicate the minimum and maximum value boundaries of the bifurcating invariant circles as γ increases.

indicate the minimum and maximum value boundaries of the bifurcating invariant circles as γ increases.

However, when a(0)>0![]() , the bifurcation is backward and unstable, meaning that the bifurcated invariant circle occurring at γ=γ⁎⁎

, the bifurcation is backward and unstable, meaning that the bifurcated invariant circle occurring at γ=γ⁎⁎![]() is unstable, illustrated in Fig. 1B (with γ⁎⁎≈0.88

is unstable, illustrated in Fig. 1B (with γ⁎⁎≈0.88![]() ). There is a continuation of the unstable bifurcated circles as γ decreases initially until it reaches a critical value ˆγ

). There is a continuation of the unstable bifurcated circles as γ decreases initially until it reaches a critical value ˆγ![]() , which is indicated by the two (red) dotted curves of the bifurcating circles for ˆγ<γ<γ⁎⁎

, which is indicated by the two (red) dotted curves of the bifurcating circles for ˆγ<γ<γ⁎⁎![]() . Then as γ increases from the critical value ˆγ

. Then as γ increases from the critical value ˆγ![]() , the bifurcated circles become forward and stable. This is illustrated by the two (blue) solid curves, which are the boundaries of the bifurcating circles, for γ>ˆγ

, the bifurcated circles become forward and stable. This is illustrated by the two (blue) solid curves, which are the boundaries of the bifurcating circles, for γ>ˆγ![]() in Fig. 1B. Therefore, the locally stable steady state coexists with the locally stable ‘forward extended’ circles for ˆγ<γ<γ⁎⁎

in Fig. 1B. Therefore, the locally stable steady state coexists with the locally stable ‘forward extended’ circles for ˆγ<γ<γ⁎⁎![]() , in between there are backward extended unstable circles. For ˆγ<γ<γ⁎⁎

, in between there are backward extended unstable circles. For ˆγ<γ<γ⁎⁎![]() , even when the fundamental steady state is locally stable, prices need not converge to the fundamental value, while may settle down to a stable limit circle. We call ˆγ<γ<γ⁎⁎

, even when the fundamental steady state is locally stable, prices need not converge to the fundamental value, while may settle down to a stable limit circle. We call ˆγ<γ<γ⁎⁎![]() the ‘volatility clustering region’. In addition, a Chenciner (generalized Neimark–Sacker) bifurcation takes place when a(0)=0

the ‘volatility clustering region’. In addition, a Chenciner (generalized Neimark–Sacker) bifurcation takes place when a(0)=0![]() . Based on the above analysis, a necessary condition on the coexistence is that a(0)>0

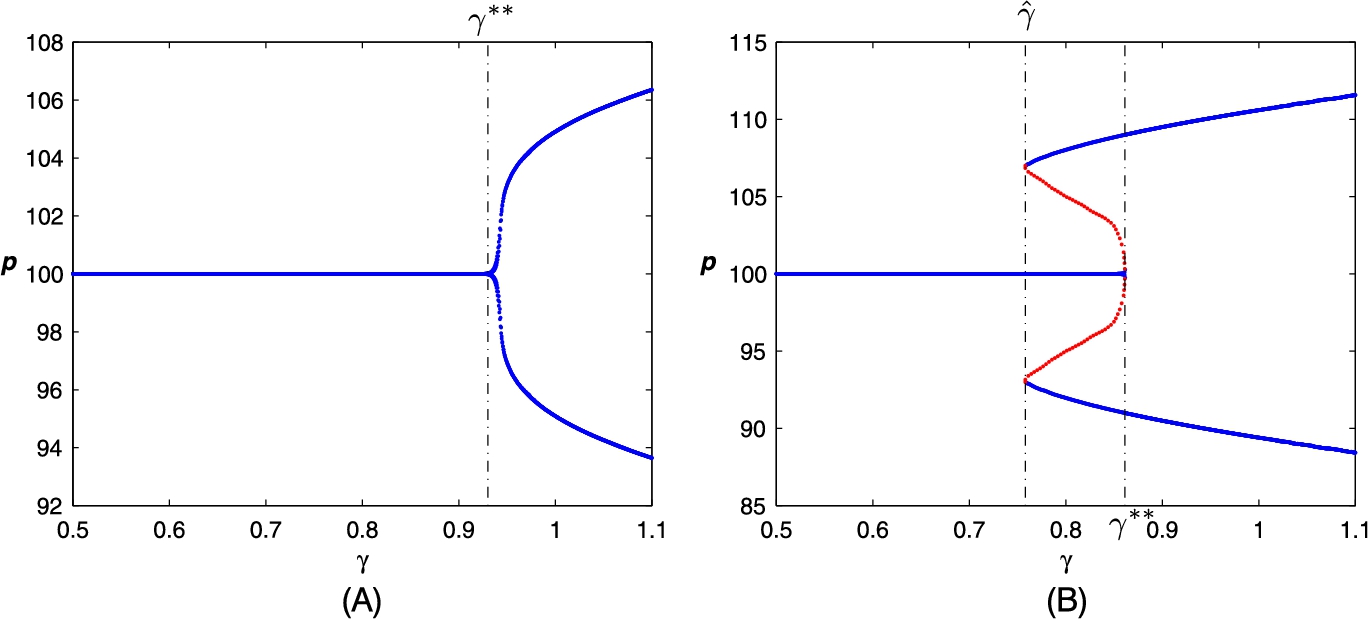

. Based on the above analysis, a necessary condition on the coexistence is that a(0)>0![]() . The coexistence of the locally stable steady state and invariant circle illustrated in Fig. 2 shows that the price dynamics depends on the initial values.

. The coexistence of the locally stable steady state and invariant circle illustrated in Fig. 2 shows that the price dynamics depends on the initial values.

in (A) and (p0,u0,v0,m0)=(ˉp+1,ˉp−1,0,ˉm)

in (A) and (p0,u0,v0,m0)=(ˉp+1,ˉp−1,0,ˉm) in (B) and the phase plot of (p,u) in (C). Here the parameter values are the same as in Fig. 1 and n0 = 0.5. (A) Price time series; (B) price time series; (C) phase plot.

in (B) and the phase plot of (p,u) in (C). Here the parameter values are the same as in Fig. 1 and n0 = 0.5. (A) Price time series; (B) price time series; (C) phase plot.When buffeted with noises, the stochastic model can endogenously generate volatility clustering and long range dependence in volatility, illustrated in Fig. 3. Economically, with strong trading activities of either the fundamental investors or the trend followers, market price fluctuates around either the fundamental value with low volatility or a cyclical price movement with high volatility, depending on market conditions. When the activities of the fundamentalists and trend followers are balanced (to be in the volatility clustering region), the interaction of the fundamental noise and noise traders and the underlying co-existence dynamics then triggers an irregular switching between the two volatility regimes, leading to volatility clustering. In particular, volatility clustering becomes more significant when neither the fundamental nor the trend following traders dominate the market and traders switch their strategies more often. The results verify the endogenous mechanism on volatility clustering proposed by Gaunersdorfer et al. (2008) and provide a behavioral explanation on the volatility clustering.

2.3 Information Uncertainty and Trading Heterogeneity

Traditional finance literature mainly explore the role of asymmetric information and information uncertainty. Most HAMs however mainly focus on endogenous market mechanism through the interaction among heterogeneous agents by assuming a complete information about the fundamental value of risky assets. An integration of HAMs and asymmetric and/or uncertain information would provide a micro-foundation on behavioral heterogeneity and a more broad framework to better explaining various puzzles and anomalies in financial markets. Instead of heuristical heterogeneity assumption of agents' behavior, He and Zheng (2016) model the trading heterogeneity by introducing information uncertainty about the fundamental value to a HAM. Agents are homogeneous ex ante. Conditional on their private information about the fundamental value, agents choose optimally among different trading strategies when optimizing their expected utilities. This approach provides a micro-foundation to trading and behavioral heterogeneity among agents. It also offers a different switching behavior of agents from the current HAMs. In the following, we brief this approach.

Consider a continuum [0,1]![]() of agents trading one risky asset and one risk-free asset in discrete-time. For simplicity, the risk-free rate is normalized to be zero. The fundamental value of the risky asset μ∼N(ˉμ,σ2μ)

of agents trading one risky asset and one risk-free asset in discrete-time. For simplicity, the risk-free rate is normalized to be zero. The fundamental value of the risky asset μ∼N(ˉμ,σ2μ)![]() is not known publicly. Denote αμ=1/σ2μ

is not known publicly. Denote αμ=1/σ2μ![]() the precision of the fundamental value μ. In each time period, agent i receives a private signal about the fundamental value μ, given by xi,t=μ+εi,t

the precision of the fundamental value μ. In each time period, agent i receives a private signal about the fundamental value μ, given by xi,t=μ+εi,t![]() , where εi,t∼N(0,σ2x)

, where εi,t∼N(0,σ2x)![]() is i.i.d. normal across agents and over time. Let αx=1/σ2x

is i.i.d. normal across agents and over time. Let αx=1/σ2x![]() be the precision of the signal. Agents maximize CARA utility function U(Wi,t)=−exp(−aWi,t),

be the precision of the signal. Agents maximize CARA utility function U(Wi,t)=−exp(−aWi,t),![]() with the same risk aversion coefficient a, in which Wi,t

with the same risk aversion coefficient a, in which Wi,t![]() is the wealth of agent i at time t. Let pt

is the wealth of agent i at time t. Let pt![]() be the (cum-)market price of the risky asset and denote It={pt,pt−1,⋯}

be the (cum-)market price of the risky asset and denote It={pt,pt−1,⋯}![]() the public information of historical price. Conditional on the public information It−1

the public information of historical price. Conditional on the public information It−1![]() and her private signal xi,t

and her private signal xi,t![]() , agent i seeks to maximize her expected utility, leading to the optimal demand qi,t=[E(pt|xi,t,It−1)−pt−1]/[aVar(pt|xi,t,It−1)]

, agent i seeks to maximize her expected utility, leading to the optimal demand qi,t=[E(pt|xi,t,It−1)−pt−1]/[aVar(pt|xi,t,It−1)]![]() , conditional on the public information It−1

, conditional on the public information It−1![]() and her signal xi,t

and her signal xi,t![]() .

.

Facing the information uncertainty on the fundamental value, the agent considers both fundamental and momentum trading strategies based on the public information of the history price and her private signal about the fundamental value. More explicitly, the fundamental trading strategy is based on

(7) Ef(pt|xi,t,It−1)=(1−γ)pt−1+γαμˉμ+αxxi,tαμ+αx,

(8) Varf(pt|xi,t,It−1)=γ2Var(μ|xi,t,It−1)=γ2αμ+αx,

where γ∈(0,1]![]() is a constant, measuring the convergence speed of the market price to the expected fundamental value. Note that αμˉμ+αxxi,tαμ+αx

is a constant, measuring the convergence speed of the market price to the expected fundamental value. Note that αμˉμ+αxxi,tαμ+αx![]() and 1αμ+αx

and 1αμ+αx![]() are agent i's posterior updating of the mean and variance, respectively, of the fundamental value of the risky asset conditional on her signal xi,t

are agent i's posterior updating of the mean and variance, respectively, of the fundamental value of the risky asset conditional on her signal xi,t![]() . Condition (7) means that the predicted price is a weighted average of the latest market price and the posterior updating of the fundamental value conditional on her private signal xi,t

. Condition (7) means that the predicted price is a weighted average of the latest market price and the posterior updating of the fundamental value conditional on her private signal xi,t![]() ; while (8) means that the conditional variance is proportional to the posterior variance conditional on the private signal xi,t

; while (8) means that the conditional variance is proportional to the posterior variance conditional on the private signal xi,t![]() . In particular, when γ=1

. In particular, when γ=1![]() , the conditional mean and variance (7)–(8) are reduced to the posterior mean and variance, respectively. Therefore the fundamental trading strategy reflects agent's belief that the future price is expected to converge to the expected fundamental value. Though the private signals xi,t

, the conditional mean and variance (7)–(8) are reduced to the posterior mean and variance, respectively. Therefore the fundamental trading strategy reflects agent's belief that the future price is expected to converge to the expected fundamental value. Though the private signals xi,t![]() are i.i.d. across agents and over time, they are partially incorporated through the current market price pt

are i.i.d. across agents and over time, they are partially incorporated through the current market price pt![]() and hence reflected in the prediction of the future prices. Consequently, the optimal demand based on the fundamental analysis becomes qfi,t=[αμˉμ+αxxi,t−(αμ+αx)pt−1]/(aγ)

and hence reflected in the prediction of the future prices. Consequently, the optimal demand based on the fundamental analysis becomes qfi,t=[αμˉμ+αxxi,t−(αμ+αx)pt−1]/(aγ)![]() , which is called the fundamental trading strategy f.

, which is called the fundamental trading strategy f.

The momentum trading is however independent of the private signal xi,t![]() , but depends on a price trend,

, but depends on a price trend,

(9) Ec(pt|xi,t,It−1)=pt−1+β(pt−1−vt),Varc(pt|xi,t,It−1)=σ2t−1,

where vt![]() is a reference price or price trend (can be a moving average, a supporting/resistance price level, or any index derived from technical analysis), β measures the extrapolation of the price deviation from the trend, and σ2t−1

is a reference price or price trend (can be a moving average, a supporting/resistance price level, or any index derived from technical analysis), β measures the extrapolation of the price deviation from the trend, and σ2t−1![]() is a heuristic prediction on the variance of the asset price. Then the optimal demand becomes qci,t=β(pt−1−vt)/(aσ2t−1)

is a heuristic prediction on the variance of the asset price. Then the optimal demand becomes qci,t=β(pt−1−vt)/(aσ2t−1)![]() , which is called momentum strategy c. In particular, when vt

, which is called momentum strategy c. In particular, when vt![]() is a moving average of the historical prices and β>(<)0

is a moving average of the historical prices and β>(<)0![]() , strategy c is essentially a time-series momentum (contrarian) strategy (Moskowitz et al., 2012).

, strategy c is essentially a time-series momentum (contrarian) strategy (Moskowitz et al., 2012).

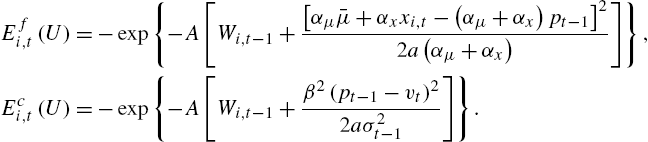

Given the information uncertainty, the agent compares the expected value functions based on the two optimal trading strategies and chooses the one with relative higher value. More explicitly, the agent firstly calculates the respective value functions based on strategy f and c,

Efi,t(U)=−exp{−A[Wi,t−1+[αμˉμ+αxxi,t−(αμ+αx)pt−1]22a(αμ+αx)]},Eci,t(U)=−exp{−A[Wi,t−1+β2(pt−1−vt)22aσ2t−1]}.

The agent then compares the value functions and selects the one that yields a higher value. Note that Efi,t![]() is an increasing function of the absolute value of the signal |xi,t|

is an increasing function of the absolute value of the signal |xi,t|![]() , while Eci

, while Eci![]() is independent of xi,t

is independent of xi,t![]() . Therefore there exists threshold signal values ˉxt

. Therefore there exists threshold signal values ˉxt![]() for the private signal such that Efi,t=Eci,t

for the private signal such that Efi,t=Eci,t![]() , that is,

, that is,

Efi,t(U)Eci,t(U)=exp{−[[αμˉμ+αxˉxt−(αμ+αx)pt−1]22(αμ+αx)−β2(pt−1−vt)22σ2t−1]}=1.

Solving for ˉxt![]() yields

yields

(10) x±t=1αx[(αμ+αx)pt−1−αμˉμ±β√αμ+αxσt−1(pt−1−vt)].

Therefore, when vt=pt−1![]() , the agent chooses strategy f. When vt≠pt−1

, the agent chooses strategy f. When vt≠pt−1![]() , the agent chooses strategy c if her signal is less informative, falling into the interval (xmt,xMt)

, the agent chooses strategy c if her signal is less informative, falling into the interval (xmt,xMt)![]() , and strategy f otherwise, where xmt=min(x±t)

, and strategy f otherwise, where xmt=min(x±t)![]() and xMt=max(x±t)

and xMt=max(x±t)![]() . Therefore, the optimal demand of agent i is given by qi,t=qfi,t

. Therefore, the optimal demand of agent i is given by qi,t=qfi,t![]() for xi,t⩽xmt

for xi,t⩽xmt![]() or xi,t⩾xMt

or xi,t⩾xMt![]() ; otherwise qi,t=qci,t

; otherwise qi,t=qci,t![]() when xi,t∈(xmt,xMt)

when xi,t∈(xmt,xMt)![]() . Intuitively, when agent's private signal is near the mean fundamental value, the private information becomes less valuable. However, when agent's private signal is far away from the mean fundamental value, the private information becomes more valuable and hence the agent favors the fundamental trading strategy.

. Intuitively, when agent's private signal is near the mean fundamental value, the private information becomes less valuable. However, when agent's private signal is far away from the mean fundamental value, the private information becomes more valuable and hence the agent favors the fundamental trading strategy.

The choice between the two strategies due to the informativeness of the private information about the fundamental value leads to endogenous heterogeneity and switching behavior of agents' choices. More explicitly, by aggregating the demand Dt![]() in a closed form and considering noisy supply St

in a closed form and considering noisy supply St![]() , the market price is determined through a market maker scenario via pt=pt−1+λ(Dt+St)

, the market price is determined through a market maker scenario via pt=pt−1+λ(Dt+St)![]() with λ>0

with λ>0![]() . He and Zheng (2016) first conduct an analysis on the underlying deterministic model when σ2t−1=σ2

. He and Zheng (2016) first conduct an analysis on the underlying deterministic model when σ2t−1=σ2![]() is a constant and vt=pt−2

is a constant and vt=pt−2![]() (corresponding to a simple momentum trading based on the change in the last price). They show that the fundamental price is locally stable with small precisions of the fundamental information noise. That is, the fundamental price becomes unstable when the level of the fundamental information noise is small, leading to high price volatility. Intuitively, in this case, the fundamental information become more accurate and hence less valuable. Therefore the fundamental strategy becomes less profitable, while the momentum trading strategy becomes more popular. This is consistent with the literature on coordination game with imperfect information (see Angeletos and Werning, 2006).

(corresponding to a simple momentum trading based on the change in the last price). They show that the fundamental price is locally stable with small precisions of the fundamental information noise. That is, the fundamental price becomes unstable when the level of the fundamental information noise is small, leading to high price volatility. Intuitively, in this case, the fundamental information become more accurate and hence less valuable. Therefore the fundamental strategy becomes less profitable, while the momentum trading strategy becomes more popular. This is consistent with the literature on coordination game with imperfect information (see Angeletos and Werning, 2006).

When the fundamental price becomes unstable, the price dynamics can become very complicated. On the stochastic model, they have shown that the market fraction of the agents choosing the momentum (fundamental) strategy decreases (increases) as the mis-pricing increases. This underlies mean-reverting of market price to its fundamental price when mis-pricing becomes significant, burst of a bubble, and recover of a recession. This mechanism, together with the destabilizing role of the momentum trading and the stabilizing role of the fundamental trading, provides an endogenous self-correction mechanism of the market. This mechanism is very different from the HAMs with complete information, in which the mean-reverting is channeled through some nonlinear assumptions on the demand or order flow of risky asset. The market stability depends exogenously on balanced activities from fundamental and momentum trading. This integrated approach of HAMs and incomplete information about the fundamental value therefore provides a micro-foundation to endogenous trading heterogeneity and switching behavior wildly characterized in HAMs. Furthermore, He and Zheng (2016) conduct a time series analysis on the stylized facts and demonstrate that the model is able to match the S&P 500 in terms of power-law distribution in returns, volatility clustering, long memory in volatility, and leverage effect.

2.4 Switching of Agents, Fund Flows, and Leverage

Similar to Dieci et al. (2006), most HAMs employ the discrete-choice framework4 to capture the way investors switch across different competing strategies/behavioral rules. However, since this approach models the changes of investors' proportions, not directly the flows of funds, it is not very suitable to capture the long-run performance of investment strategies (or ‘styles’) in terms of accumulated wealth, nor the impact of fund flows on the price dynamics. For this reason, LeBaron (2011) defines such forms of switching between strategies as active learning, capturing investors' tendency to adopt the best-performing rule, in contrast to passive learning, by which investors' wealth naturally accumulates on strategies that have been relatively successful. This second form of learning is closely related to the issue of survival and long-run dominance of strategies and to the evolutionary finance approach (see Blume and Easley, 1992, 2006, Sandroni, 2000, Hens and Schenk-Hoppé, 2005, as well as Evstigneev et al., 2009 for a comprehensive survey of early results and recent research in this field).5

LeBaron (2011) argues that the dynamics of real-world markets are likely to be affected by some combinations of active and passive learning, and that exploring their interaction may improve our understanding of the dynamics of asset prices. Moreover, LeBaron (2012) proposes a simple framework that can simultaneously account for wealth dynamics and active search for new strategies, based on performance comparison. Besides reproducing the basic stylized facts of asset returns and trading volume, the model yields some insight into the dynamics of agents' strategies and their impact on market stability.

A further recent contribution on the interplay of active and passive learning is provided by Palczewski et al. (2016). They build an evolutionary finance framework in discrete time with fundamental, trend-following and noise trading strategies. Such strategies are interpreted as portfolio managers with different investment ‘styles’. Individual investors can move (part of) their funds between portfolio managers. The total amount of freely flowing capital is a model parameter, capturing the clients' degree of impatience (similar to the proportion of switching investors in Dieci et al., 2006). Funds are reallocated based on the relative performance of competing fund managers, according to the discrete choice principle. Therefore, portfolio managers may experience an exogenous growth of their wealth, in addition to the endogenous growth due to returns on the employed capital. The model framework appears promising to investigate the market impact of the fund flows and to incorporate different types of ‘behavioral biases’ into HAMs. In particular, Palczewski et al. (2016) show that even a small amount of freely flowing capital can have a large impact on price movements if investors exhibit ‘recency bias’ in evaluating fund performance.

In a somewhat related framework with heterogeneous investment funds using ‘value investing’, Thurner et al. (2012) explore the joint impact of wealth dynamics and the flows of capital among competing investment funds. Evolutionary pressure generated by short-run competition forces fund managers to make leveraged asset purchases with margin calls. Simulation results highlight a new mechanism to fat tails and clustered volatility, which is linked to wealth dynamics and leverage-induced crashes. Moreover, this framework appears promising to test different credit regulation policies (Poledna et al., 2014) and to investigate the impact of bank leverage management on the stability properties of the financial system (Aymanns and Farmer, 2015).

3 HAMs of Single Asset Market in Continuous-Time

Historical information plays a very important role in testing efficient market hypothesis in financial markets. In particular, it is crucial to understand how quickly market prices reflect fundamental shocks and how much information is contained in the historical prices. Empirical evidence shows that stock markets react with a delay to information on fundamentals and that information diffuses gradually across markets (Hou and Moskowitz, 2005, Hong et al., 2007). Based on market underreaction and overreaction hypotheses, momentum and contrarian strategies are widely used by financial market practitioners and their profitability has been extensively investigated by academics. De Bondt and Thaler (1985) and Lakonishok et al. (1994) find supporting evidence on the profitability of contrarian strategies for a holding period of 3–5 years based on the past 3–5 years' returns. In contrast, Jegadeesh and Titman (1993, 2001) among many others, find supporting evidence on the profitability of momentum strategies for holding periods of 3–12 months based on the returns over the past 3–12 months. Time series momentum investigated recently in Moskowitz et al. (2012) characterizes a strong positive predictability of a security's own past returns. It becomes clear that the time horizons of historical prices play crucial roles in the performance of contrarian and momentum strategies. Many theoretical studies have tried to explain the momentum,6 however, as argued in Griffin et al. (2003), “the comparison is in some sense unfair since no time horizon is specified in most behavioral models”.

In the literature of HAMs, the heterogeneous expectations of agents, in particular of chartists, are formed based on price trends such as moving average of historical prices. In discrete-time models, with different time horizon, the dimension of the model is different. To examine the effect of time horizon analytically, we need to study the model with different dimension separately. Also, as the time horizon increases, it becomes more difficult analytically in dealing with high dimensional nonlinear dynamic system. This challenge is illustrated in Chiarella et al. (2006b) when examining the effect of different moving averages on market stability. Therefore, how different time horizons of historical prices affect price dynamics becomes a challenging issue in the current HAMs.

This section introduces some of the recent developments of HAMs of a single risky asset (and a riskless asset) in continuous time to deal with the price delay problems in behavioral finance and HAMs literature. In continuous-time HAMs, the time horizon of historical price information is simply captured by a time delay parameter. Such models are characterized mathematically by a system of stochastic delay differential equations, which provide a more broad framework to investigate the joint effect of adaptive behavior of heterogeneous agents and the impact of historical prices.

Development of deterministic delay differential equation models to characterize fluctuation of commodity prices and cyclic economic behavior has a long history,7 however the application to asset pricing and financial markets is relatively new. This section bridges HAMs with traditional approaches in continuous-time finance to investigate the impact of moving average rules over different time horizon (He and Li, 2012) in Section 3.1, the profitability of fundamental and momentum strategies (He and Li, 2015a) in Section 3.2, and optimal asset allocation with time series momentum and reversal (He et al., 2018) in Section 3.3.

3.1 A Continuous-Time HAM with Time Delay

We now introduce the continuous-time model of He and Li (2012) and demonstrate first that the result of Brock and Hommes on rational routes to market instability in discrete-time also holds in continuous time. That is, adaptive switching behavior of agents can lead to market instability as the switching intensity increases. We then show a double edged effect of an increase in the time horizon of historical price information on market stability. An initial increase in time delay can destabilize the market, leading to price fluctuations. However, as the time delay increases further, the market is stabilized. This double edged effect is a very different feature of continuous-time HAMs from discrete-time HAMs. With noisy fundamental value and liquidity traders, the continuous-time model is able to generate long deviations of market price from the fundamental price, bubbles, crashes, and volatility clustering.

Consider a financial market with a risky asset and let P(t)![]() denote the (cum) price per share of the risky asset at time t. The market consists of fundamentalists, chartists, liquidity traders, and a market maker. The fundamentalists believe that the market price P(t)

denote the (cum) price per share of the risky asset at time t. The market consists of fundamentalists, chartists, liquidity traders, and a market maker. The fundamentalists believe that the market price P(t)![]() is mean-reverting to the fundamental price F(t)

is mean-reverting to the fundamental price F(t)![]() , and their demand is given by Zf(t)=βf[F(t)−P(t)]

, and their demand is given by Zf(t)=βf[F(t)−P(t)]![]() , with βf>0

, with βf>0![]() measuring the mean-reverting speed of the market price to the fundamental price. The chartists are modeled as trend followers, believing that the future market price follows a price trend u(t)

measuring the mean-reverting speed of the market price to the fundamental price. The chartists are modeled as trend followers, believing that the future market price follows a price trend u(t)![]() , and their demand is given by8 Zc(t)=tanh(βc[P(t)−u(t)])

, and their demand is given by8 Zc(t)=tanh(βc[P(t)−u(t)])![]() with βc>0

with βc>0![]() measuring the extrapolation of the trend followers to the price trend. Among various price trends used in practice, we consider u(t)

measuring the extrapolation of the trend followers to the price trend. Among various price trends used in practice, we consider u(t)![]() as a normalized exponentially decaying weighted average of historical prices over a time interval [t−τ,t]

as a normalized exponentially decaying weighted average of historical prices over a time interval [t−τ,t]![]() ,

,

(11) u(t)=k1−e−kτ∫tt−τe−k(t−s)P(s)ds,

where time delay τ∈(0,∞)![]() represents time horizon of historical prices, k>0

represents time horizon of historical prices, k>0![]() measures the decay rate of the weights on the historical prices. In particular, when k→0

measures the decay rate of the weights on the historical prices. In particular, when k→0![]() , the weights are equal and the price trend u(t)

, the weights are equal and the price trend u(t)![]() in (11) is simply given by the standard moving average (MA) with equal weights, u(t)=1τ∫tt−τP(s)ds

in (11) is simply given by the standard moving average (MA) with equal weights, u(t)=1τ∫tt−τP(s)ds![]() . When k→∞

. When k→∞![]() , all the weights go to the current price so that u(t)→P(t)

, all the weights go to the current price so that u(t)→P(t)![]() . For the time delay, when τ→0

. For the time delay, when τ→0![]() , the trend followers regard the current price as the price trend. When τ→∞

, the trend followers regard the current price as the price trend. When τ→∞![]() , the trend followers use all the historical prices to form the price trend, u(t)=k∫t−∞e−k(t−s)P(s)ds

, the trend followers use all the historical prices to form the price trend, u(t)=k∫t−∞e−k(t−s)P(s)ds![]() . In general, for 0<k<∞

. In general, for 0<k<∞![]() , Eq. (11) can be expressed as a delay differential equation with time delay τ

, Eq. (11) can be expressed as a delay differential equation with time delay τ

du(t)=k1−e−kτ[P(t)−e−kτP(t−τ)−(1−e−kτ)u(t)]dt.

The demand of liquidity traders is i.i.d. normally distributed with mean of zero and standard deviation of σM(>0)![]() .

.

Let nf(t)![]() and nc(t)

and nc(t)![]() represent the market fractions of agents who use the fundamental and trend following strategies, respectively. Their net profits over a short time interval [t,t+dt]

represent the market fractions of agents who use the fundamental and trend following strategies, respectively. Their net profits over a short time interval [t,t+dt]![]() can be measured, respectively, by πf(t)dt=Zf(t)dP(t)−Cfdt

can be measured, respectively, by πf(t)dt=Zf(t)dP(t)−Cfdt![]() and πc(t)dt=Zc(t)dP(t)−Ccdt

and πc(t)dt=Zc(t)dP(t)−Ccdt![]() , where Cf,Cc⩾0

, where Cf,Cc⩾0![]() are constant costs of the strategies. To measure strategy performance, we introduce a cumulated profit over the time interval [t−τ,t]

are constant costs of the strategies. To measure strategy performance, we introduce a cumulated profit over the time interval [t−τ,t]![]() by Ui(t)=η1−e−ητ∫tt−τe−η(t−s)πi(s)ds,i=f,c

by Ui(t)=η1−e−ητ∫tt−τe−η(t−s)πi(s)ds,i=f,c![]() , where η>0

, where η>0![]() measures the decay of the historical profits. Consequently, dUi(t)=η[πi(t)−e−ητπi(t−τ)1−e−ητ−Ui(t)]dt

measures the decay of the historical profits. Consequently, dUi(t)=η[πi(t)−e−ητπi(t−τ)1−e−ητ−Ui(t)]dt![]() for i=f,c

for i=f,c![]() . Following Hofbauer and Sigmund (1998, Chapter 7), the evolution dynamics of the market populations are governed by

. Following Hofbauer and Sigmund (1998, Chapter 7), the evolution dynamics of the market populations are governed by

dni(t)=βni(t)[dUi(t)−dˉU(t)], for i=f,c,

where dˉU(t)=nf(t)dUf(t)+nc(t)dUc(t)![]() is the average performance of the two strategies and β>0

is the average performance of the two strategies and β>0![]() measures the intensity of choice. The switching mechanism in the continuous-time setup is consistent with the one used in discrete-time HAMs. In fact, it can be verified that the dynamics of the market fraction nf(t)

measures the intensity of choice. The switching mechanism in the continuous-time setup is consistent with the one used in discrete-time HAMs. In fact, it can be verified that the dynamics of the market fraction nf(t)![]() satisfy dnf(t)=βnf(t)(1−nf(t))[dUf(t)−dUc(t)]

satisfy dnf(t)=βnf(t)(1−nf(t))[dUf(t)−dUc(t)]![]() , leading to nf(t)=eβUf(t)/(eβUf(t)+eβUc(t))

, leading to nf(t)=eβUf(t)/(eβUf(t)+eβUc(t))![]() , which is the discrete choice model used in Brock and Hommes (1998).

, which is the discrete choice model used in Brock and Hommes (1998).

Finally, the price P(t)![]() is adjusted by the market maker according to dP(t)=μ[nf(t)Zf(t)+nc(t)Zc(t)]dt+σMdWM(t)

is adjusted by the market maker according to dP(t)=μ[nf(t)Zf(t)+nc(t)Zc(t)]dt+σMdWM(t)![]() , where μ>0

, where μ>0![]() represents the speed of the price adjustment of the market maker, WM(t)

represents the speed of the price adjustment of the market maker, WM(t)![]() is a standard Wiener process capturing the random excess demand process either driven by unexpected market news or liquidity traders, and σM>0

is a standard Wiener process capturing the random excess demand process either driven by unexpected market news or liquidity traders, and σM>0![]() is a constant. To sum up, the market price of the risky asset is determined according to the stochastic delay differential system

is a constant. To sum up, the market price of the risky asset is determined according to the stochastic delay differential system

(12) {dP(t)=μ[nf(t)Zf(t)+(1−nf(t))Zc(t)]dt+σMdWM(t),du(t)=k1−e−kτ[P(t)−e−kτP(t−τ)−(1−e−kτ)u(t)]dt,dU(t)=η1−e−ητ[π(t)−e−ητπ(t−τ)−(1−e−ητ)U(t)]dt,

where U(t)=Uf(t)−Uc(t)![]() , nf(t)=1/(1+e−βU(t))

, nf(t)=1/(1+e−βU(t))![]() , Zf(t)=βf(F(t)−P(t))

, Zf(t)=βf(F(t)−P(t))![]() , Zc(t)=tanh[βc(P(t)−u(t))]

, Zc(t)=tanh[βc(P(t)−u(t))]![]() , C=Cf−Cc

, C=Cf−Cc![]() , and

, and

π(t)=πf(t)−πc(t)=μ[nf(t)Zf(t)+(1−nf(t))Zc(t)][Zf(t)−Zc(t)]−C.

By assuming that the fundamental price is a constant F(t)≡ˉF![]() and there is no market noise σM=0

and there is no market noise σM=0![]() , system (12) becomes a deterministic delay differential system with (P,u,U)=(ˉF,ˉF,−C)

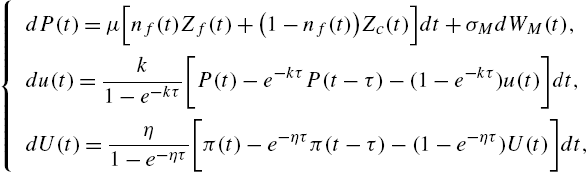

, system (12) becomes a deterministic delay differential system with (P,u,U)=(ˉF,ˉF,−C)![]() as the unique fundamental steady state. He and Li (2012) show that the steady state is locally stable for either small or large time delay τ when the market is dominated by the fundamentalists. Otherwise, the steady state becomes unstable through Hopf bifurcations as the time delay increases. This result is in line with the results obtained in discrete-time HAMs. However, different from discrete-time HAMs, the continuous-time model shows that the fundamental steady state becomes locally stable again when the time delay is large enough. This is illustrated by the bifurcation diagram of the market price with respect to τ in Fig. 4A.9 It shows that there are two Hopf bifurcation values 0<τo<τ1

as the unique fundamental steady state. He and Li (2012) show that the steady state is locally stable for either small or large time delay τ when the market is dominated by the fundamentalists. Otherwise, the steady state becomes unstable through Hopf bifurcations as the time delay increases. This result is in line with the results obtained in discrete-time HAMs. However, different from discrete-time HAMs, the continuous-time model shows that the fundamental steady state becomes locally stable again when the time delay is large enough. This is illustrated by the bifurcation diagram of the market price with respect to τ in Fig. 4A.9 It shows that there are two Hopf bifurcation values 0<τo<τ1![]() occurring at τ=τ0(≈8)

occurring at τ=τ0(≈8)![]() and τ=τ1(≈28)

and τ=τ1(≈28)![]() . The fundamental steady state is locally stable when the time delay is small, τ∈[0,τ0)

. The fundamental steady state is locally stable when the time delay is small, τ∈[0,τ0)![]() , then becomes unstable for τ∈(τo,τ1)