3

Cost Sheet/Statement of Cost

CHAPTER OUTLINE

3. Items Not Included in Total Costs (Non-cost Items)

4. Format of a Simple Cost Sheet

LEARNING OBJECTIVES

After reading this chapter, you will be able to understand:

- The meaning of cost sheet

- The features of cost sheet

- Items that are not considered in the cost sheet

- Format of a simple cost sheet

- Format of an advanced cost sheet

3.1 INTRODUCTION

Cost sheet is a statement prepared to show the various elements of costs, like prime cost, factory cost of production and total cost. It is prepared at regular intervals, for example, weekly, monthly quarterly, yearly, etc. In some cases comparative figures of various periods are also shown in the cost sheet so that assessment can be made about the progress of a business.

Cost sheet is a statement of cost showing cost per unit of any product at every level of production. It is important to know at what stage of production we are and what price the particular production stage has.

Cost sheet is a statement of cost. In other words, when costing information is set out in the form of a statement it is called a cost sheet. It is usually adopted when only one product is produced and all costs are incurred for that product only. Cost sheet may be prepared for a week, for a month, quarterly or yearly indicating various components of cost such as prime cost, works cost, cost of production, cost of goods sold, total cost and also profitability of production.

Cost sheet is a statement containing the detailed costs of output during a period.

Cost sheet is a statement of total costs under different headings.

Cost sheet is a tabulated statement of total costs under various classifications.

3.2 FEATURES OF A COST SHEET

The major features of a cost sheet are as follows:

- Cost sheet reveals total costs and the cost per unit of units produced.

- Cost sheet reveals total costs under different classifications.

- Cost sheet helps in the preparation of tender and quotation.

- Cost sheet helps in fixing the selling price.

The advantages of cost sheet are as follows:

- It discloses the total cost and the cost per unit of the units produced during a given period.

- It enables a manufacturer to keep a close watch on and control over the cost of production.

- It helps in eliminating costs that go towards increasing the cost of a product.

- It acts as a guide to the manufacturer and helps him or her in formulating a definite, useful production policy.

- It helps in fixing the selling price more accurately.

- It helps businesses to minimize the cost of production when there is cut-throat competition.

3.3 ITEMS NOT INCLUDED IN TOTAL COSTS (NON-COST ITEMS)

Following are the expenses that should not be included in a cost sheet:

- Income tax

- Reserves

- Dividends

- Bonus

- Cash discount

- Rents received

- Donations

- Charity

- Commission

- Abnormal losses

- Purchases of assets

- Loss on account of sale of fixed assets

- Preliminary expenses that are written off

The preparation of cost sheets depends on the cost data provided by cost accounting. Due to differences in the nature of cost data, different cost sheet formats may be used.

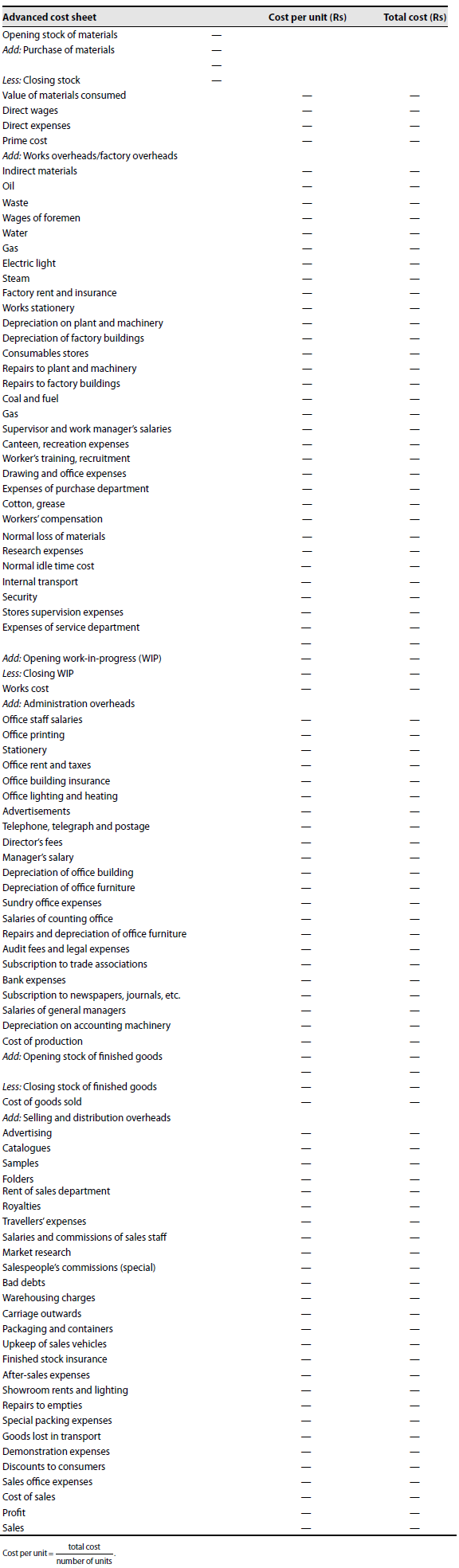

3.4 FORMAT OF A SIMPLE COST SHEET

The format of a simple cost sheet is as follows:

Table 3.1

| Cost sheet | Amount |

|---|---|

| Direct material | — |

| Direct labour | — |

| Direct expenses | — |

| Prime cost | — |

| (+) Factory overheads | — |

| * Factory cost | — |

| (+) Administration overheads | — |

| * Cost of production | — |

| (+) Selling and distribution overheads | — |

| Cost of sales | — |

| (+) Profit | — |

| Sales | — |

* Factory overheads are otherwise known as works overheads.

* Factory cost is otherwise known as works cost.

* Cost of production is known as the stage of finished goods.

Table 3.2

Format of a cost sheet with stocks of raw material WIP and finished goods:

Table 3.3

| Opening stock of raw material | — | |

| (+) Purchases of raw material | — | |

| — | ||

| (−) Closing stock of raw material | — | |

| Direct material consumed | — | |

| Direct labour | — | |

| Direct expenses | — | |

| Prime cost | — | |

| (+) Factory overheads | — | |

| (+) Opening WIP | — | |

| — | ||

| (−) Closing WIP | — | — |

| Factory cost | — | |

| (+) Administration overheads | — | |

| Cost of production/finished goods | — | |

| Finished goods | — | |

| (+) Opening stock of finished goods | — | |

| (−) Closing stock of finished goods | — | — |

| Cost of goods sold | — | |

| (+) Selling and distribution overheads | — | |

| Cost of sales | — | |

| Profit | — | |

| Sales | — |

Illustration 1

Calculate prime cost from the following information:

| Particulars | Rs | Rs |

| Direct material | 20,000 | |

| Direct labour | 12,000 | |

| Direct expenses | 6,000 | |

| Indirect materials | 10,000 | |

| Indirect expenses | 3,000 | |

| Indirect labour | 6,000 | |

| Carriage inwards | 1,000 | |

| Carriage outwards | 500 |

Solution: Calculation of prime cost

| Particulars | Rs |

| Direct material | 20,000 |

| Direct labour | 12,000 |

| Direct expenses | 6,000 |

| Carriage inwards | 1,000 |

| Prime cost | 39,000 |

Problem 1. Calculate prime cost from the following information

| Particulars | Rs | Rs |

|---|---|---|

| Direct material | 40,000 | |

| Direct labour | 24,000 | |

| Direct expenses | 12,000 | |

| Indirect materials | 15,000 | |

| Indirect expenses | 4,500 | |

| Indirect labour | 9,000 | |

| Carriage inwards | 1,500 | |

| Carriage outwards | 750 |

Illustration 2

Prepare a cost sheet from the following information:

| Rs | Rs | |

|---|---|---|

| Direct materials | 80,000 | |

| Direct expenses | 20,000 | |

| Direct labour | 30,000 | |

| Factory overheads | 10,000 | |

| Office overheads | 5,000 | |

| Selling overheads | 3,000 | |

| Sales | 1,60,000 |

Solution: Statement of cost and profit

| Particulars | Rs | |

|---|---|---|

| Direct materials | 80,000 | |

| Direct labour | 30,000 | |

| Direct expenses | 20,000 | |

| Prime cost | 1,30,000 | |

| Add: | Factory overheads: | 10,000 |

| Factory cost | 1,40,000 | |

| Add: | Office overheads: | 5,000 |

| Cost of production | 1,45,000 | |

| Add: | Selling overheads: | 3,000 |

| Cost of sales | 1,48,000 | |

| Profit (b/f) | 12,000 | |

| Sales | 1,60,000 |

Problem 2. Prepare a cost sheet from the following information

| Rs | Rs | |

|---|---|---|

| Direct materials | 80,000 | |

| Direct expenses | 40,000 | |

| Direct labour | 60,000 | |

| Factory overheads | 15,000 | |

| Office overheads | 7,500 | |

| Selling overheads | 4,500 | |

| Sales | 3,20,000 |

Illustration 3

Prepare a cost sheet from the following information:

| Rs | |

|---|---|

| Prime cost | 40,000 |

| Factory cost | 60,000 |

| Cost of production | 80,000 |

| Cost of sales | 1,00,000 |

| Sales | 2,00,000 |

Solution: Statement of cost and profit

| Particulars | Rs | |

|---|---|---|

| Prime cost | 40,000 | |

| Add: | Factory overheads (b/f) | 20,000 |

| Factory cost | 60,000 | |

| Add: | Administration overheads (b/f) | 20,000 |

| Cost of production | 80,000 | |

| Add: | Selling and distribution overheads (b/f) | 20,000 |

| Cost of sales | 1,00,000 | |

| Profit (b/f) | 1,00,000 | |

| Sales | 2,00,000 |

Problem 3. Prepare a cost sheet from the following information

| Rs | |

|---|---|

| Prime cost | 80,000 |

| Factory cost | 1,20,000 |

| Cost of production | 1,60,000 |

| Cost of sales | 1,50,000 |

| Sales | 4,00,000 |

Illustration 4

A factory produces 100 units of a commodity. The cost of production is as follows:

| Rs | Rs | |

|---|---|---|

| Direct material | 80,000 | |

| Direct wages | 30,000 | |

| Direct expenses | 15,000 | |

| Factory overheads | 120% on wages | |

| Office overheads | 40% on works cost | |

| Expected profit: 20% on sales | ||

Prepare a cost sheet and the price to be fixed per unit.

Note: Profit is 1/3 on cost.

Solution: Statement of cost and profit

| Particulars | Rs | |

|---|---|---|

| Direct material | 80,000 | |

| Direct wages | 30,000 | |

| Direct expenses | 15,000 | |

| Prime cost | 1,25,000 | |

| Add: | Factory overheads (120% on wages) | 36,000 |

| Works cost | 1,61,000 | |

| Add: | Office overheads (40% on works cost) | 64,400 |

| Cost of sales | 2,25,400 | |

| Profit (1/4 on cost or 1/5 on sales) | 56,350 | |

| Sales (b/f) | 2,81,750 |

Price to be fixed per unit= Rs 2,817.50

Problem 4. A factory produces 100 units of a commodity. The cost of production is as follows

| Rs | Rs | |

|---|---|---|

| Direct material | 1,60,000 | |

| Direct wages | 60,000 | |

| Direct expenses | 15,000 | |

| Factory overheads | 120% on wages | |

| Office overheads | 40% on works cost | |

| Expected profit: 20% on sales |

Prepare a cost sheet and the price to be fixed per unit.

Note: Profit is 1/3 on cost.

Illustration 5

A factory produces 100 units of a commodity. The cost of production is as follows:

| Rs | Rs | |

|---|---|---|

| Direct material | 60,000 | |

| Direct labour | 40,000 | |

| Direct expenses | 20,000 | |

| Factory overheads | 7,500 | |

| Administrative overheads | 2,500 |

Profit margin is 20% on sales.

Prepare a cost sheet and the price per unit.

Solution: Statement of cost and profit

| Particulars | Rs | |

|---|---|---|

| Direct material | 60,000 | |

| Direct labour | 40,000 | |

| Direct expenses | 20,000 | |

| Prime cost | 1,20,000 | |

| Add: | Factory overheads | 7,500 |

| Works cost | 1,27,500 | |

| Add: | Administration overheads | 2,500 |

| Cost of sales | 1,30,000 | |

| Profit (25% on cost (or) 20% on sales) | 32,500 | |

| Sales | 1,62,500 |

Price per unit = 90,000/100 = Rs 900

Problem 5.

| Rs | Rs | |

|---|---|---|

| Direct material | 1,20,000 | |

| Direct labour | 49,000 | |

| Direct expenses | 25,000 | |

| Factory overheads | 9,500 | |

| Administrative overheads | 4,500 |

Profit margin is 25% on sales.

Prepare a cost sheet and the price per unit.

Illustration 6

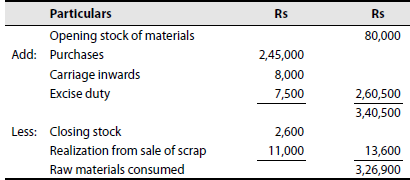

Calculate the raw material consumed for the period ending on 31 March 2005:

| Rs | Rs | |

|---|---|---|

| Materials purchased | 2,45,000 | |

| Opening stock of material | 80,000 | |

| Carriage inwards | 8,000 | |

| Closing stock of material | 2,600 | |

| Realization from sale of scrap | 11,000 | |

| Excise duty on material purchased | 7,500 |

Note: Realization from scrap is deducted.

Solution: Calculation of raw materials consumed:

Problem 6. Calculate the raw material consumed for the period ending on 31 March 2005

| Rs | Rs | |

|---|---|---|

| Materials purchased | 4,50,000 | |

| Opening stock of material | 1,00,000 | |

| Carriage inwards | 16,000 | |

| Closing stock of material | 4,600 | |

| Realization from sale of scrap | 15,000 | |

| Excise duty on material purchased | 10,000 |

Note: Realization from scrap is deducted.

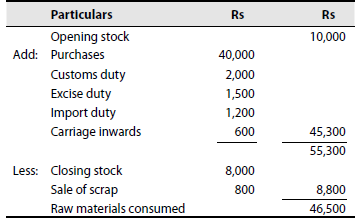

Illustration 7

The following details have been obtained from the cost records of Comet Paints Limited:

| Rs | Rs | |

|---|---|---|

| Material purchased | 40,000 | |

| Opening stock of material | 10,000 | |

| Closing stock of material | 8,000 | |

| Customs duty on purchase | 2,000 | |

| Excise duty on purchase | 1,500 | |

| Import duty on purchase | 1,200 | |

| Sale of scrap | 800 | |

| Carriage inwards | 600 | |

| Carriage outwards | 400 |

Note: Scrap and carriage outwards deducted.

Solution: Calculation of raw materials consumed:

Problem 7. The following details have been obtained from the cost records of Comet Paints Limited

| Rs | Rs | |

|---|---|---|

| Material purchased | 80,000 | |

| Opening stock of material | 20,000 | |

| Closing stock of material | 16,000 | |

| Customs duty on purchase | 4,000 | |

| Excise duty on purchase | 3,000 | |

| Import duty on purchase | 2,000 | |

| Sale of scrap | 1,000 | |

| Carriage inwards | 800 | |

| Carriage outwards | 600 |

Note: Scrap and carriage outwards deducted.

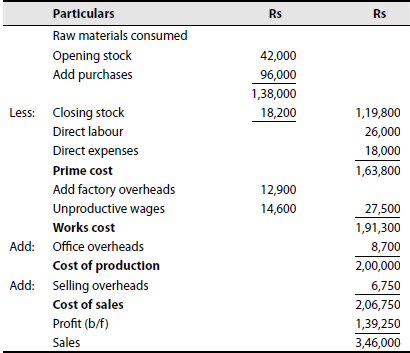

Illustration 8

Prepare a cost sheet.

| Rs | Rs | |

|---|---|---|

| Opening stock of material | 42,000 | |

| Purchase | 96,000 | |

| Closing stock of material | 18,200 | |

| Direct labour | 26,000 | |

| Direct expenses | 18,000 | |

| Unproductive wages | 14,600 | |

| Factory overheads | 12,900 | |

| Office overheads | 8,700 | |

| Selling overheads | 6,750 | |

| Sales | 3,46,000 |

Note: Unproductive wages is put under factory overheads.

Solution: Statement of cost and profit

Problem 8. Prepare a cost sheet

| Rs | Rs | |

|---|---|---|

| Opening stock of material | 84,000 | |

| Closing stock of material | 36,200 | |

| Direct labour | 46,000 | |

| Direct expenses | 28,000 | |

| Unproductive wages | 28,600 | |

| Factory overheads | 24,900 | |

| Office overheads | 16,700 | |

| Selling overheads | 16,750 | |

| Sales | 6,92,000 |

Note: Unproductive wages is put under factory overheads.

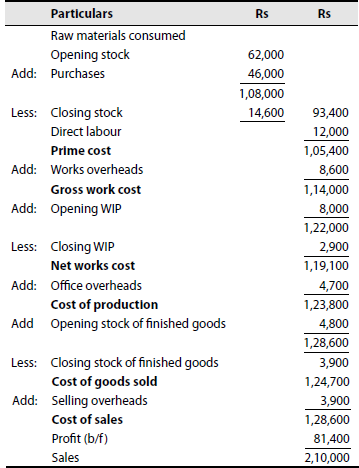

Illustration 9

Prepare a cost sheet.

| Rs | Rs | |

|---|---|---|

| Opening stock of material | 62,000 | |

| Closing stock of material | 14,600 | |

| Opening stock of WIP | 8,000 | |

| Closing stock of WIP | 2,900 | |

| Opening stock of finished goods | 4,800 | |

| Closing stock of finished goods | 3,900 | |

| Direct material purchases | 46,000 | |

| Direct labour | 12,000 | |

| Works overheads | 8,600 | |

| Office overheads | 4,700 | |

| Selling overheads | 3,900 | |

| Sales | 2,10,000 |

Solution: Statement of cost and profit

Problem 9. Prepare a cost sheet

| Rs | Rs | |

|---|---|---|

| Opening stock of material | 92,000 | |

| Closing stock of material | 28,600 | |

| Opening stock of WIP | 16,000 | |

| Closing stock of WIP | 4,900 | |

| Opening stock of finished goods | 8,800 | |

| Closing stock of finished goods | 5,900 | |

| Direct material purchased | 50,000 | |

| Direct labour | 24,000 | |

| Works overheads | 9,800 | |

| Office overheads | 7,700 | |

| Selling overheads | 5,900 | |

| Sales | 4,20,000 |

Illustration 10

Prepare a cost sheet from the following information:

| Rs | Rs | |

|---|---|---|

| Raw material consumed | 20,000 | |

| Direct wages | 20,000 | |

| Machine hours worked | 1,800 hours | |

| Machine hour rate | Rs 2 | |

| Selling overheads | 6,000 | |

| Office overheads | 9,500 | |

| Units produced | 26,550 | |

| Units sold | 21,225 | |

| Selling price per unit | Rs 3 |

Note: Closing stock is missing. We have to calculate it.

Solution: Statement of cost and profit:

| Particulars | Rs | |

|---|---|---|

| Raw materials consumed | 20,000 | |

| Direct wages | 20,000 | |

| Prime cost | 40,000 | |

| Add: | Factory overheads (machine hours × rate per unit) | 3,600 |

| Factory cost | 43,600 | |

| Add: | Office overheads | 9,500 |

| Cost of production at Rs 2 | 53,100 | |

| Less: | Closing stock of finished goods | 10,650 |

| Cost of goods sold | 42,450 | |

| Add: | Selling overheads | 6,000 |

| Cost of sales | 48,450 | |

| Profit (b/f) | 15,225 | |

| Sales | 63,675 |

Hint: Closing stock = units produced – units sold = 26,550 – 21,225 = 5,325

Problem 10. Prepare a cost sheet from the following information

| Rs | Rs | |

|---|---|---|

| Raw material consumed | 40,000 | |

| Direct wages | 50,000 | |

| Machine hours worked | 1,800 hours | |

| Machine hour rate | Rs 4 | |

| Selling overheads | 9,000 | |

| Office overheads | 38,500 | |

| Units produced | 46,550 | |

| Units sold | 41,225 | |

| Selling price per unit | Rs 6 |

Note: Closing stock is missing. We have to calculate it.

Illustration 11

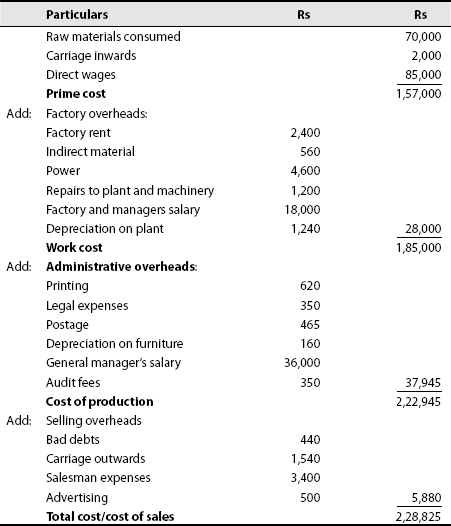

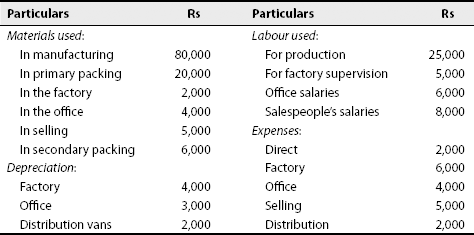

A manufacturer presents the following details about the various expenses incurred in manufacturing:

| Rs | |

|---|---|

| Raw materials consumed | 70,000 |

| Carriage inwards | 2,000 |

| Factory rent | 2,400 |

| Bad debts | 440 |

| Printing and stationery | 620 |

| Legal expenses | 350 |

| Carriage outwards | 1,540 |

| Indirect material | 560 |

| Power | 4,600 |

| Depreciation on furniture | 160 |

| Postage expenses | 465 |

| Repairs to plant and machinery | 1,200 |

| Salesmen's expense | 3,400 |

| Advertising | 500 |

| Direct wages | 85,000 |

| General manager's salary | 36,000 |

| Factory manager's salary | 18,000 |

| Depreciation on plant and machinery | 1,240 |

| Audit fees | 350 |

Classify the aforementioned expenses under the various elements of cost showing separately the total expenditure under each element.

Solution: Statement of cost sheet:

Problem 11. A manufacturer presents the following details about the various expenses incurred

| Rs | |

|---|---|

| Raw materials consumed | 1,40,000 |

| Carriage inwards | 4,000 |

| Factory rent | 4,400 |

| Bad debts | 840 |

| Printing and stationery | 820 |

| Legal expenses | 550 |

| Carriage outwards | 2,540 |

| Indirect material | 960 |

| Power | 5,600 |

| Depreciation on furniture | 560 |

| Postage expenses | 865 |

| Repairs to plant and machinery | 2,200 |

| Salespeople's expenses | 5,400 |

| Advertising | 900 |

| Direct wages | 95,000 |

| General manager's salary | 56,000 |

| Factory manager's salary | 38,000 |

| Depreciation on plant and machinery | 2,240 |

| Audit fees | 650 |

Classify the aforementioned expenses under the various elements of cost showing separately the total expenditure under each element.

Illustration 12

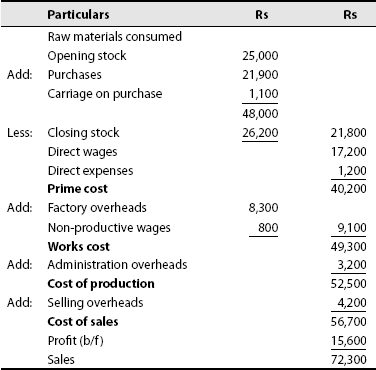

From the following information, prepare a cost sheet for the month of January:

| Rs | Rs | |

|---|---|---|

| Stock of raw materials on 1 January | 25,000 | |

| Stock of raw materials on 31 January | 26,200 | |

| Purchase of raw materials | 21,900 | |

| Carriage on purchases | 1,100 | |

| Sale of finished goods | 72,300 | |

| Direct wages | 17,200 | |

| Non-productive wages | 800 | |

| Direct expenses | 1,200 | |

| Factory overheads | 8,300 | |

| Administrative overheads | 3,200 | |

| Selling overheads | 4,200 |

Solution: Statement of cost and profit:

Problem 12. From the following information, prepare a cost sheet for the month of January

| Rs | Rs | |

|---|---|---|

| Stock of raw materials on 1 January | 45,000 | |

| Stock of raw materials on 31 January | 46,200 | |

| Purchase of raw materials | 41,900 | |

| Carriage on purchases | 3,100 | |

| Sale of finished goods | 1,44,600 | |

| Direct wages | 27,200 | |

| Non-productive wages | 900 | |

| Direct expenses | 3,200 | |

| Factory overheads | 9,300 | |

| Administrative overheads | 5,200 | |

| Selling overheads | 4,900 |

Illustration 13

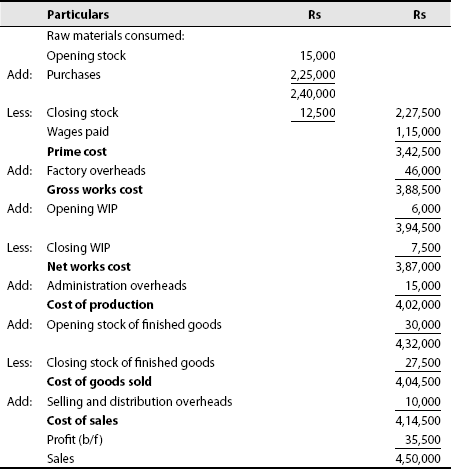

The following information has been obtained from the records of a factory for the period from 1 June to 30 June:

| Rs | |

|---|---|

| Opening balance of raw materials on 1 June | 15,000 |

| Purchases of raw materials during the month of June | 2,25,000 |

| Wages paid | 1,15,000 |

| Factory overheads | 46,000 |

| Opening balance of WIP on 1 June | 6,000 |

| Closing balance of WIP on 30 June | 7,500 |

| Closing balance of raw materials on 30 June | 12,500 |

| Opening balance of finished goods manufactured on 1 June | 30,000 |

| Closing balance of finished goods manufactured on 30 June | 27,500 |

| Selling and distribution overheads | 10,000 |

| Administration overheads | 15,000 |

| Sales | 4,50,000 |

Prepare

- Statement of cost of production of goods manufactured

- Statement of cost of production of goods sold and

- Statement of profit on sales.

Solution: Statement of cost and profit:

Problem 13. The following information has been obtained from the records of a factory for the period from 1 June to 30 June

| Rs | |

|---|---|

| Opening balance of raw materials on 1 June | 25,000 |

| Purchase of raw materials during the month of June | 2,45,000 |

| Wages paid | 1,35,000 |

| Factory overheads | 86,000 |

| Opening balance of WIP on 1 June | 9,000 |

| Closing balance of WIP on 30 June | 9,500 |

| Closing balance of raw materials on 30 June | 15,500 |

| Opening balance of finished goods manufactured on 1 June | 50,000 |

| Closing balance of finished goods manufactured on 30 June | 47,500 |

| Selling and distribution overheads | 20,000 |

| Administration overheads | 35,000 |

| Sales | 9,00,000 |

Prepare

- Statement of cost of production of goods manufactured

- Statement of cost of production of goods sold

- Statement of profit on sales

Illustration 14

A modern manufacturing company submits the following information on 31 March 1993

| Rs | |

|---|---|

| Sales for the year | 2,75,000 |

| Inventories at the beginning of the year: | |

| Finished goods | 7,000 |

| WIP | 4,000 |

| Purchase of materials | 1,10,000 |

| Materials inventory: | |

| At the beginning of the year | 3,000 |

| At the end of the year | 4,000 |

| Direct labour | 65,000 |

| Factory overheads were 60% of direct labour cost | |

| Inventories at the end of the year: | |

| WIP | 6,000 |

| Finished goods | 8,000 |

| Other expenses for the year: | |

| Selling expenses | |

| Administration expenses | 10% of sales |

| Prepare a statement of cost | 5% of sales |

Solution: Statement of cost and profit:

Problem 14. A modern manufacturing company submits the following information on 31 March 1993

| Rs | |

|---|---|

| Sales for the year | 5,50,000 |

| Inventories at the beginning of the year: | |

| Finished goods | 9,000 |

| WIP | 8,000 |

| Purchase of materials | 2,10,000 |

| Materials inventory: At the beginning of the year | 6,000 |

| At the end of the year | 6,000 |

| Direct labour | 85,000 |

| Factory overheads were 60% of direct labour cost | |

| Inventories at the end of the year: | |

| WIP | 8,000 |

| Finished goods | 9,000 |

| Other expenses for the year: | |

| Selling expenses | |

| Administration expenses | 10% of sales |

| Prepare a statement of cost | 5% of sales |

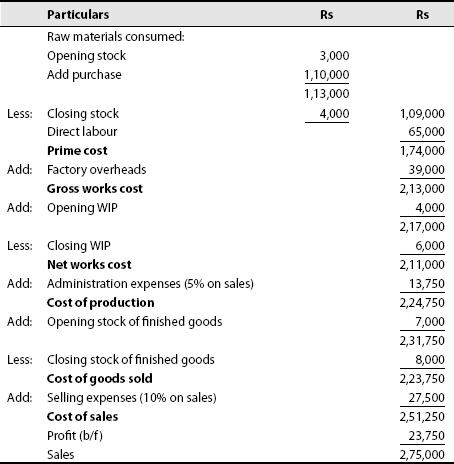

Illustration 15

The following extracts of costing information related to commodity A for the half-year ending on 31 December 1993:

| Rs | |

|---|---|

| Purchase of raw materials | 1,20,000 |

| Works overheads | 48,000 |

| Direct wages | 1,00,000 |

| Carriage on purchases Stock (1 July 1993): | 1,440 |

| Raw materials | 20,000 |

| Finished products (1,000 tons) | 16,000 |

| Stock (31 December 1993) | |

| Raw materials | 22,240 |

| Finished products (2,000 tons) | 32,000 |

| WIP (1 July 1993) | 4,800 |

| WIP (31 December 1993) | 16,000 |

| Sales—finished products | 3,00,000 |

Selling and distribution overheads are Re 1 per ton sold. During the period, 16,000 tons of commodities were produced.

You are to ascertain (a) cost of raw materials used, (b) cost of output for the period, (c) cost of sales, (d) net profit for the period and (e) net profit per ton of the commodity.

Solution: Statement of cost and profit:

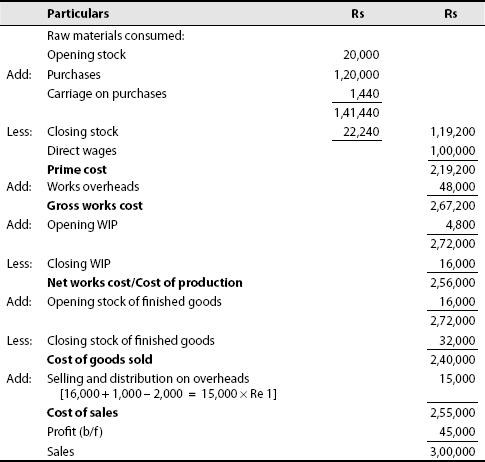

Problem 15. The following extracts of costing information related to commodity A for the half-year ending on 31 December 1993:

| Rs | |

|---|---|

| Purchase of raw materials | 2,20,000 |

| Works overheads | 88,000 |

| Direct wages | 2,00,000 |

| Carriage on purchases | 2,440 |

| Stock (1 July 1993) | |

| Raw materials | 40,000 |

| Finished products (1,000 tons) | 26,000 |

| Stock (31 December 1993): | |

| Raw materials | 32,240 |

| Finished products (2,000 tons) | 42,000 |

| WIP (1 July 1993) | 6,800 |

| WIP (31 December 1993) | 26,000 |

| Sales—finished products | 6,00,000 |

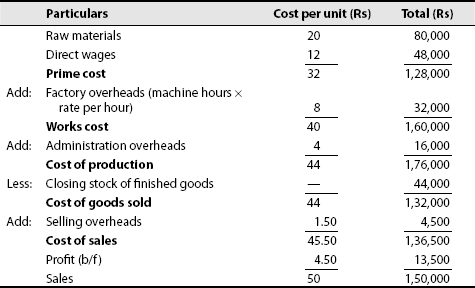

Illustration 16

The following data were collected related to the manufacture of a standard product during the month of April 1984:

| Raw material | Rs 80,000 |

| Direct wages | Rs 48,000 |

| Machine hours worked | 8,000 hours |

| Machine hour rate | Rs 4 |

| Administration overheads | 10% of works cost |

| Selling overheads | Rs 1.50 per unit |

| Units produced | 4,000 |

| Units sold | 3,000 |

| Selling price | Rs 50 per unit |

You are required to prepare a cost sheet in respect of the aforementioned data showing (a) cost per unit and (b) profit for the month of April 1984.

Solution: Statement of cost and profit:

Hint: Closing stock = produced – sold = 4,000 – 3,000 = 1,000

Problem 16. The following data were collected related to the manufacture of a standard product during the month of April 1984

| Raw material | Rs 90,000 |

| Direct wages | Rs 68,000 |

| Machine hours worked | 8,000 hours |

| Machine hour rate | Rs 8 |

| Administration overheads | 10% of works cost |

| Selling overheads | Rs 3.50 per unit |

| Units produced | 5,000 |

| Units sold | 7,000 |

| Selling price | Rs 100 per unit |

Illustration 17

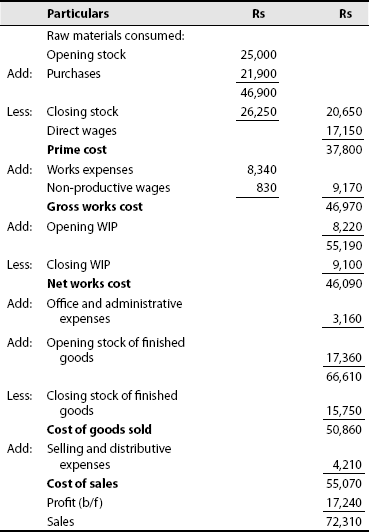

The directors of a manufacturing business require a statement showing the production results of a business for the month of March 1994. The cost accounts reveal the following information:

| Rs | |

|---|---|

| Stock on hand, 1 March 1994: | |

| Raw materials | 25,000 |

| Finished goods | 17,360 |

| Stock on hand, 31 March 1994: | |

| Raw materials | 26,250 |

| Finished goods | 15,750 |

| Purchase of raw materials | 21,900 |

| WIP, 1March 1994 | 8,220 |

| WIP, 31 March 1994 | 9,100 |

| Sale of finished goods | 72,310 |

| Direct wages | 17,150 |

| Non-productive wages | 830 |

| Works expenses | 8,340 |

| Office and administrative expenses | 3,160 |

| Selling and distributive expenses | 4,210 |

You are required to construct the statement so as to show (a) the value of material consumed, (b) total cost of production, (c) cost of goods sold, (d) profit on goods sold and (e) net profit for the month of March 1994.

Solution: Statement of cost and profit:

Problem 17. The directors of a manufacturing business require a statement showing the production results of the business for the month of March 1994. The cost accounts reveal the following information

| Rs | |

|---|---|

| Stock on hand, 1 March 1994: | |

| Raw materials | 45,000 |

| Finished goods | 27,360 |

| Stock on hand, 31 March 1994 | |

| Raw materials | 46,250 |

| Finished goods | 25,750 |

| Purchase of raw materials | 31,900 |

| WIP, 1 March 1994 | 9,320 |

| WIP, 31 March 1994 | 9,900 |

| Sale of finished goods | 92,310 |

| Direct wages | 37,150 |

| Non-productive wages | 950 |

| Works expenses | 9,640 |

| Office and administrative expenses | 5,160 |

| Selling and distributive expenses | 7,210 |

You are required to construct the statement so as to show (a) the value of material consumed, (b) total cost of production, (c) cost of goods sold, (d) profit on the goods sold and (e) net profit for the month.

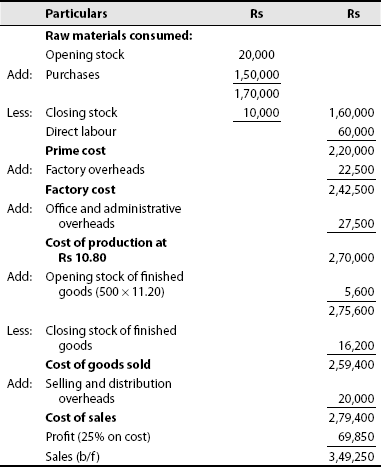

Illustration 18

From the following particulars for product X, compile the cost sheet for the month of March 1991

| Rs | |

|---|---|

| Raw material: | |

| Opening stock | 20,000 |

| Purchases | 1,50,000 |

| Closing stock | 10,000 |

| Direct labour | 60,000 |

| Factory overheads | 22,500 |

| Office and administrative overheads | 27,500 |

| Finished stock: | |

| Opening stock: 500 units at Rs 11.20 per unit | |

| Closing stock: 1,500 units at the current cost price | |

| Profit on sales: 20% | |

| Selling and distribution overheads: 20,000 | |

| Units produced: 25,000 units |

Solution: Statement of cost and profit:

Problem 18. From the following particulars of product X, compile cost sheet for the month of March 1991

| Rs | |

|---|---|

| Raw material: | |

| Opening stock | 40,000 |

| Purchases | 2,50,000 |

| Closing stock | 30,000 |

| Direct labour | 90,000 |

| Factory overheads | 42,500 |

| Office and administrative overheads | 47,500 |

| Finished stock: | |

| Opening stock: 500 units at Rs 21.20 per unit | |

| Closing stock: 1,500 units at the current cost price | |

| Profit on sales: 20% | |

| Selling and distribution overheads: 40,000 | |

| Units produced: 45,000 units |

Illustration 19

From the following data relating to the manufacture of a standard product during the month of September 1983, prepare a statement showing the cost and profit per unit:

| Raw material used | Rs 40,000 |

| Direct wages | Rs 24,000 |

| Manhours worked | 9,500 (hours) |

| Manhour rate | Rs 4 per hour |

| Office overheads | 20% on works cost |

| Selling overheads | Re 1 per unit |

| Units produced | 20,000 units |

| Units sold | 18,000 at Rs 10 per unit |

Solution: Statement of cost and profit

| Particulars | Rs | |

|---|---|---|

| Raw materials consumed: | 40,000 | |

| Direct wages | 24,000 | |

| Prime cost | 64,000 | |

| Add: | Factory overheads (Machine hours worked × rate) | 38,000 |

| Works cost | 1,02,000 | |

| Add: | Office overheads | 20,400 |

| Cost of production at Rs 6.12 | 1,22,400 | |

| Less: | Closing stock of finished goods (20,000 − 18,000) × Rs 6.12 | 12,240 |

| Cost of goods sold | 1,10,160 | |

| Add: | Selling overheads | 18,000 |

| Cost of sales | 1,28,160 | |

| Profit | 51,840 | |

| Sales | 1,80,000 |

Problem 19. From the following data relating to the manufacture of a standard product during the month of September 1983, prepare a statement showing the cost and profit per unit

| Raw material used | Rs 80,000 |

| Direct wages | Rs 44,000 |

| Manhours worked | 9,500 (hours) |

| Manhour rate | Rs 8 per hour |

| Office overheads | 20% on works cost |

| Selling overheads | Rs 2 per unit |

| Units produced | 30,000 units |

| Units sold | 38,000 at Rs 10 per unit |

Illustration 20

Prepare cost sheet for the year 1986 from the following showing the total cost and cost per unit. Number of units produced is 2,000.

| Rs | |

|---|---|

| Opening stock of raw materials | 10,000 |

| Purchases | 1,80,000 |

| Direct wages | 56,000 |

| Indirect wages | 48,000 |

| Closing stock of raw materials | 12,000 |

| WIP on 1 January 1986 | 5,000 |

| WIP on 31 December 1986 | 6,000 |

| Factory overheads | 26,000 |

| Office overheads | 45,000 |

| Selling overheads | 16,000 |

| Opening stock of finished goods (100 units) | 20,000 |

The closing stock of finished goods is 120 units. Profit is 10% on sales.

During the year 1987, it was decided to increase the production to 2,400 units. It was anticipated that

- Material prices would increase by 10%.

- Wages would reduce by 20%.

- Other expenses would remain constant per unit.

- Expected profit would become 20% of sales.

Prepare cost sheet and ascertain selling price to be fixed per unit.

Solution: Cost sheet for the year 1986 (output 2,000 units):

Estimated cost statement for the year and 1987 [output is 2,400 units]:

Problem 20. Prepare cost sheet for the year 1986 from the following data showing the total cost and cost per unit. The number of units produced is 2,000

| Rs | |

|---|---|

| Opening stock of raw materials | 30,000 |

| Purchases | 2,80,000 |

| Direct wages | 76,000 |

| Indirect wages | 68,000 |

| Closing stock of raw materials | 32,000 |

| WIP on 1 January 1986 | 9,000 |

| WIP on 31 December 1986 | 8,000 |

| Factory overheads | 36,000 |

| Office overheads | 55,000 |

| Selling overheads | 26,000 |

| Opening stock of finished goods (100 units) | 30,000 |

The closing stock of finished goods is 120 units. Profit is 10% of sales.

During the year 1987, it was decided to increase the production to 2,400 units. It was anticipated that

- Material prices would increase by 10%.

- Wages would reduce by 20%.

- Other expenses would remain constant per unit.

- Expected profit would become 20% on sales.

Ascertain the selling price to be fixed per unit.

3.5 ADVANCED-TYPE SOLVED PROBLEMS

- The following figures are extracted from the trial balance of Gogetter company on 30 September 1998:

- Inventories:

Finished stock 40,000 Raw materials 70,000 WIP 1,00,000 Office appliances 8,700 Plant and machinery 2,30,250 Buildings 1,00,000 Sales 3,84,000 Sales return and rebates 7,000 Material purchased 1,60,000 Freight incurred on materials 8,000 Purchase returns 2,400 Direct labour 80,000 Indirect labour 9,000 Factory supervision 5,000 Repairs and upkeep of factory 7,000 Heat, light and power 32,500 Rates and taxes 3,150 Sales travelling 5,500 Miscellaneous factory expenses 9,350 Sales commission 16,800 Sales promotion 11,250 Distribution department salaries and expenses 9,000 - Office salaries and expenses:

Office salaries and expenses 4,300 Interest on borrowed funds 1,000

Further details are available as follows:

- Closing inventories:

Finished goods 57,500 Raw materials 90,000 Work-in-process 96,000 - Accrued expenses on

Direct labour 4,000 Indirect labour 600 Interest on borrowed funds 1,000 - Depreciation to be provided on

Office appliances 5% Plant and machinery 10% Buildings 4% - Distribution of the following costs:

Heat, light and power to factory, office and selling in the ratio 8:1:1.

Rates and taxes two thirds of factory and one third of office.

Depreciation on buildings to factory, office and selling in the ratio 8:1:1.

Prepare

- Administration ratio

- Selling and distribution expenses

- Cost of sales

- Profit and sales statement

Solution: Office overheads

Heat, light and power 3,250 Rates and taxes 1,050 Office salaries and expenses 4,300 Depreciation on building 400 Depreciation on office appliances 435 Total 9,435 Selling and distribution overheads:

Heat, light and power 3,250 Sales commission 16,800 Sales travelling 5,500 Sales promotion 11,250 Distribution department salaries and expenses 9,000 Depreciation on building 400 46,200 Cost of sales:

Opening stock of raw materials 70,000 (+) Purchase of raw materials 1,60,000 2,30,000 (−) Closing stock of raw materials 90,000 1,40,000 (+) Freight incurred on materials 8,000 1,48,000 (−) Purchase returns 2,400 Raw materials consumed 1,45,600 (+) Direct labour 84,000 Prime cost 2,29,600 (+) Factory overheads: Indirect labour 9,600 Factory supervision 5,000 Repairs and upkeep 7,000 Heat, light and power 26,000 Rates and taxes 2,100 Miscellaneous factory expenses 9,350 Depreciation on plant and machinery 23,025 Depreciation on building 3,200 Gross works cost 3,14,875 (+) Opening WIP 1,00,000 4,14,875 (−) Closing WIP 96,000 Factory cost 3,18,875 (+) Office expenses 9,435 Cost of production 3,28,310 (+) Opening stock of finished goods 40,000 3,68,310 (−) Closing stock of finished goods 57,500 Cost of goods sold 3,10,810 (+) Selling and distribution overheads 46,200 Cost of sales 3,57,010 Profit and loss statement:

Sales 3,84,000 (−) Sales return and rebates 7,000 3,77,000 Cost of sales 3,57,010 Operating profit 19,990 (−) Interest on borrowed funds 2,000 Profit 17,990 - Inventories:

- The books of Adarsh manufacturing company present the following data for the month of June 2005:

Direct labour cost is Rs 35,000 being 17.5% of works overheads.

Cost of goods sold excluding administration expenses is Rs 1,12,000.

Inventory account showed the following opening and closing balances:

1 June 30 June Raw materials 16,000 21,200 WIP 21,000 29,000 Finished goods 35,200 38,000 Other data: Selling expenses 7,000 General and administration expenses 5,000 Sales for the month 1,50,000 You are required to compute the value of materials purchased.

Solution:

Rs Opening stock of raw material 16,000 (+) Purchase of raw materials 73,000 89,000 (−) Closing stock of raw material 21,200 Raw material consumed 67,800 (+) Direct labour 35,000 Prime cost 1,02,800 (+) Works overheads 20,000 Gross works cost 1,22,800 (+) Opening WIP 21,000 1,43,800 (−) Closing WIP 29,000 Works cost 1,14,800 (+) Opening stock of finished goods 35,200 1,55,000 (−) Closing stock of finished goods 38,000 Cost of goods sold 1,17,000 (+) Selling expenses 7,000 Cost of sales 1,24,000 Sales 1,50,000 Profit 26,000 Note: Cost of goods sold also includes administrative overheads. So we should include administration overheads to the given cost of goods sold because it excludes administrative overheads.

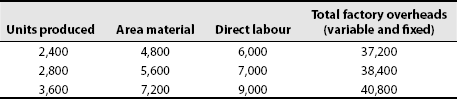

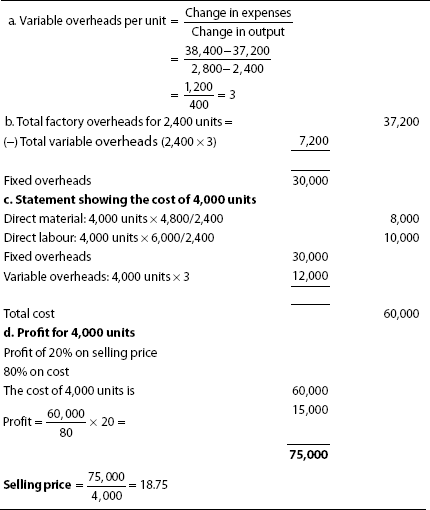

- Meera Industries Ltd. is a single-product organization having a manufacturing capacity of 6,000 units per week at 48 hours. The output data vis-a-vis different elements of cost for three consecutive weeks are given as follows:

As a cost accountant, you are asked by the company management to work out the selling price assuming an activity level of 4,000 units per week and a profit of 20% on selling price.

Solution:

- Ravi manufacturing company submits the following information on 31 March 1999:

Sales for the year 1,37,500 Inventories at beginning of the year: Finished goods 3,500 WIP 2,000 Purchase of material 55,000 Material inventory: At the beginning f the year 1,500 At the end of the year 2,000 Direct labour 32,500 Factory overheads were 60% of direct labour cost Inventories at the end of the year: WIP 3,000 Finished goods 4,000 Other expenses for the year: Selling expenses: 10% of sales Administrative expenses: 5% of sales Solution:

Rs Opening stock of raw material 1,500 (+) Purchase of raw materials 55,000 56,500 (−) Closing stock of raw material 2,000 Raw material used 54,500 (+) Direct labour 32,500 Prime cost 87,000 (+) Factory overheads 19,500 Gross works cost 1,06,500 (+) Opening stock of WIP 2,000 1,08,500 (−) Closing stock of WIP 3,000 Works cost 1,05,500 (+) Administration overheads 6,875 Cost of production 1,12,375 Profit or loss statement

Rs Cost of production 1,12,375 (+) Opening stock of finished goods 3,500 1,15,875 (−) Closing stock of finished goods 4,000 Cost of goods sold 1,18,875 (+) Selling overheads 13,750 Cost of sales 1,25,625 Sales 1,37,500 Profit 11,875 - The following is the manufacturing and profit and loss accounts of Ramya Ltd. for the year ending on 30 June 2004:

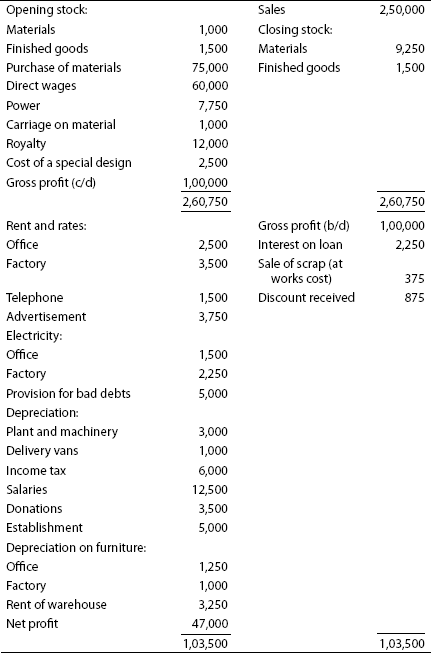

You are required to prepare a statement showing the classification of cost under different components from the aforementioned information after giving due consideration to the following facts:

- 60% of telephone expenses relate to office and 40% to sales department.

- 25% of salaries relate to factory, 50% to office and 25% to sales department

- 50% of the establishment expenses relate to office and 50% to sales department.

Statement of cost:

Rs Opening stock of raw material 1,000 (+) Purchase of raw materials 75,000 76,000 (−) Closing stock of raw material 9,250 66,750 (+) Carriage on material 1,000 Materials consumed 67,750 (+) Direct wages 60,000 Royalty 12,000 Cost of a special design 2,500 Prime costs 1,42,250 (+) Factory overheads: Power 7,750 Rent and rates 3,500 Electricity 2,250 Depreciation on plant and machinery 3,000 Salaries 3,125 Depreciation on furniture 1,000 1,62,875 (−) Sale of scrap 375 Works costs 1,62,500 (+) Administration overheads: Rent and taxes 2,500 Telephone 900 Electricity—office 1,500 Salaries 6,250 Establishment 2,500 Depreciation on furniture 1,250 Cost of production 1,77,400 (+) Opening stock of finished goods 1,500 1,78,900 (−) Closing stock of finished goods 1,500 Cost of goods sold 1,77,400 (+) Selling and administration overheads: Telephone 600 Advertisement 3,750 Depreciation on delivery vans 1,000 Salaries 3,125 Rent of warehouse 3,250 Establishment 2,500 Cost of sales 1,91,625 Sales 2,50,000 Profit 58,375 - The books and records of Ajith manufacturing company present the following data for the month of January 2000:

Direct labour 32,000 (160% of factory overheads) Cost of goods sold 1,12,000 Administration overhead 5,200 Selling overhead 6,800 Sales 1,50,000 Inventory accounts showed the following opening and closing balances:

1 January 31 January Raw materials 16,000 17,200 WIP 16,000 24,000 Finished goods 28,000 36,000 You are required to prepare a statement showing the cost of goods manufactured and sold and the profit earned.

Raw materials consumed:

Rs Cost of goods sold 1,12,000 (+) Closing stock of finished goods 36,000 1,48,000 (−) Opening stock of finished goods 28,000 Cost of production 1,20,000 (−) Administration overheads 5,200 Works costs 1,14,800 (−) Closing WIP 24,000 1,38,800 (−) Opening WIP 16,000 Gross work costs 1,22,800 (−) Factory overheads 20,000 Prime costs 1,02,800 (−) Direct labour 32,000 Raw materials consumed 70,800 Raw material consumed: = Opening stock + Raw material purchase – Closing stock raw material

77,800 = 16,000 + Purchase – 17,200

Purchase = 72,000

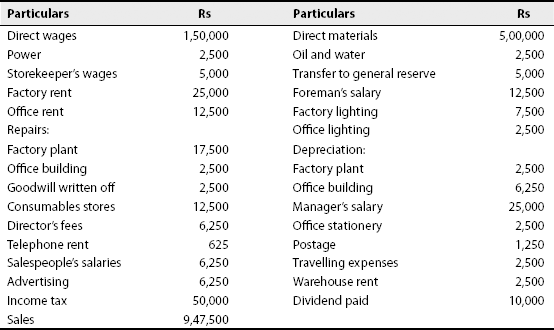

Rs Opening stock of raw material 16,000 (+) Purchase of raw materials 72,000 88,000 (−) Closing stock of raw material 17,200 Raw materials consumed 70,800 (+) Direct labour 32,000 Prime costs 1,02,800 (+) Factory overheads 20,000 Gross works costs 1,22,800 (+) Opening stock of WIP 16,000 1,38,800 (−) Closing stock of WIP 24,000 Works costs 1,14,800 (+) Administration overheads 5,200 Cost of production 1,20,000 (+) Opening stock of finished goods 28,000 1,48,000 (−) Closing stock of finished goods 36,000 1,12,000 (+) Selling overheads 6,800 Cost of sales 1,18,800 Sales 1,50,000 Profit 31,200 - From the account books of M/s. Aryan Enterprises, the following details are extracted for the year ending on 31 March 2006:

Stock of material—opening 94,000 Stock of material—closing 1,00,000 Direct wages 1,19,200 Material purchases during the year 4,16,000 Indirect wages 8,000 Salaries to administrative staff 20,000 Freights inwards 16,000 Freights outwards 10,000 Cash discounts allowed 7,000 Bad debts written off 9,400 Repairs to plant and machinery 21,200 Rent rates and taxes—factory 6,000 Rent rates and taxes—office 3,200 Travelling expenses 6,200 Salespeople's salaries and commissions 16,800 Depreciation written off—plant and machinery 14,200 Depreciation written off—furniture 1,200 Directors' fees 12,000 Electricity charges (factory) 24,000 Fuel (for boiler) 32,000 General chargers 12,400 Manager's salary 24,000 The manager's time is shared between the factory and the office in the ratio 20:80. For the aforementioned details, you are required to prepare (a) prime cost, (b) factory cost, (c) factory overheads, (d) general overheads and (e) total cost.

Cost statement:

Rs Opening stock of raw material 94,000 (+) Purchase of raw materials 4,16,000 5,10,000 (+) Freight inwards 16,000 5,26,000 (−) Closing stock of raw material 1,00,000 Raw material consumed 4,26,000 (+) Direct wages 1,19,200 Prime costs 5,45,200 (+) Factory overheads: Indirect wages 8,000 Repairs to plant and machinery 21,200 Rent, rates and taxes 6,000 Depreciation—plant and machinery 14,200 Electricity 24,000 Fuel 32,000 Manager's salary 4,800 Factory overheads 1,10,200 Factory cost 6,55,400 (+) General overheads: Salaries to administrative staff 20,000 Freight outwards 10,000 Bad debts written off 9,400 Rent, rates and taxes 3,200 Travelling expenses 6,200 Salespeople's salaries and commissions 16,800 Depreciation on furniture 1,200 Directors' fees 12,000 General charges 12,400 Manager's salary 19,200 General overheads 1,10,400 Total 7,65,800

CHAPTER SUMMARY

After reading this chapter, you should be able to understand the concept of cost sheet and its break-up of costs. You should also understand that cost sheet is only a memorandum statement and does not involve standard accounting principles. Further, you should understand the advantages and disadvantages of a cost sheet along with its various related adjustments.

EXERCISE FOR YOUR PRACTICE

Objective-Type Questions

I. State whether the following statements are true or false:

- Prime cost = direct wages + direct material + production overheads.

- Cost of production stage can be called as finished goods stage.

- Cost of sales and cost of goods sold are the same.

- Secondary packing is a part of direct material.

- Cost sheet is also known as statement of cost.

- Cost of goods sold is a stage between cost of production and cost of sales.

- Works cost is otherwise known as factory cost.

- Cost sheet is a memorandum statement.

- Income tax is included in the cost sheet.

- Reserve is an example of non-cost items.

[Ans: 1—false, 2—true, 3—false, 4—false, 5—true, 6—true, 7—true, 8—true, 9—false, 10—true]

II. Choose the correct answer:

- _____ is not included in cost sheet.

- Research expenses

- Security

- Stores supervision expenses

- Commission

- Premises comes under

- Factory overheads

- Administrative overheads

- Selling and distribution

- None of the above

- Depreciation of factory plant is a

- Factory overhead

- Administrative overhead

- Selling overhead

- None of the above

- Twenty per cent of profit on a cost of Rs 25,350 is

- 5,070

- 8,607

- 5,860

- 2,060

- The cost of production stage can be called as

- Semi-finished goods stage

- Finished goods stage

- Both a and b

- None of above

- Cost sheet is also known as

- Statement of production

- Statement of selling

- Statement of cost

- None of the above

- Reserve is an example of

- Cost item

- Non-cost item

- Selling item

- None of the above

- Cost of goods sold is the stage between

- Cost of production and sales

- Factory cost and cost of production

- Prime cost and factory cost

- None of above

- Works cost is otherwise known as

- Prime cost

- Production cost

- Factory cost

- None of the above

- WIP comes under

- Factory overheads

- Prime cost

- Administrative overheads

- None of the above

[Ans: 1—(d), 2—(b), 3—(a), 4—(a), 5—(b), 6—(c), 7—(b), 8—(a), 9—(c), 10—(a)]

DISCUSSION QUESTIONS

Short Answer-Type Questions

- What is cost sheet?

- What are the important features of a cost sheet?

- What is the formula for computing cost per unit?

- Give a few examples for items of appropriation of profit.

Essay-Type Questions

- Mention the non-cost items.

- Write a note on the various overheads.

- Explain the purposes of a cost sheet.

- Explain the difference between works overhead and works cost.

- Explain the terms cost of goods sold and cost of sales.

- Explain the term prime cost with examples.

PROBLEMS

- Ascertain prime cost from the following data:

Rs Direct wages 50,000 Chargeable expenses 5,000 Opening stock of raw materials 10,000 Raw materials bought during the period 60,000 Closing stock of raw materials 20,000 Carriage inwards 1,500 Carriage outwards 2,000 Raw materials returned to the supplier 1,500 (Osmania, 1995)

[Ans: prime cost = Rs 1,05,000]

- The following cost data are available for a firm from its books for the year ending on 31 December 1995:

Rs Direct material 9,00,000 Direct wages 7,50,000 Profit 6,09,000 Selling and distribution overheads 5,25,000 Administrative overheads 4,20,000 Factory overheads 4,50,000 Prepare a cost sheet indicating the prime cost, works cost, production cost, cost of sales and sales value.

(Madras, 1997)

[Ans: prime cost = Rs 16,50,000; works cost = Rs 21,00,000; production cost = Rs 25,20,000; cost of sales = Rs 30,45,000; and sales value = Rs 36,54,000]

- Calculate (a) prime cost, (b) factory cost, (c) cost of production, (d) cost of sales and (e) profit from the following particulars:

Rs Direct materials 1,00,000 Direct wages 25,000 Direct expenses 5,000 Wages of foremen 2,500 Electric power 500 Lighting: Factory 1,500 Office 500 Rent: Factory 5,000 Office 500 Salaries to salespeople 1,250 Advertising 1,250 Income tax 10,000 Sales 1,89,500 (Bharathidasan, 1993)

[Ans: (a) Rs 1,30,000; (b) Rs 1,39,500; (c) Rs 1,40,500; (d) Rs 1,43,000; (e) Rs 46,500]

- A manufacturing company submits to you the following details about the various expenses incurred by it during the year ending on 31 December 1985:

Rs Cost of raw materials consumed 25,000 Advertising 1,000 Depreciation on plant and machinery 1,500 Factory office salaries 6,000 Legal expenses 300 Supervisor's salary 5,500 Factory rates and insurance 1,000 Carriage outwards 1,500 Direct labour 20,000 Bad debts 300 Office stationery 200 Rent of factory buildings 2,500 Office salary 10,000 Commission on sales 4,000 Audit fees 300 Income tax 1,500 Donation to charitable institutions 500 Purchase of new plant 10,000 Classify the aforementioned expenses under various heads of cost, showing separately the total expenditure under each head. Also show separately the expenses that shall not be included in calculating the cost.

(Madras, 1987)

[Ans: prime cost = Rs 45,000; factory overhead = Rs 16,500; works cost = Rs 61,500; administrative overhead = Rs 10,800; cost of production = Rs 72,300; selling and distribution overheads = Rs 6,800; total cost = Rs 79,100; expenses that shall not be included = (1) income tax, (2) donation and (3) purchase of plant]

- A manufacturer presents the following details about the various expenses incurred by him:

Rs Raw materials consumed 70,000 Carriage inwards 2,000 Factory rent 2,400 Bad debts 440 Printing and stationery 620 Legal expenses 350 Carriage outwards 1,540 Indirect material 560 Power 4,600 Depreciation on furniture 160 Postage expenses 465 Repairs to plant and machinery 1,200 Salespeople's expenses 3,400 Advertising 500 Direct wages 85,000 General manager's salary 36,000 Factory manager's salary 18,000 Depreciation on plant and machinery 1,240 Audit fees 350 Classify the aforementioned expenses under the various elements of cost, showing separately the total expenditure under each element.

(Madras, 1998)

[Ans: prime cost = Rs 1,57,000; factory cost = Rs 1,85,000; cost of production = Rs 2,22,945; total cost = Rs 2,28,825; factory overheads = Rs 28,000; administrative overheads = Rs 37,945; Selling and distribution overheads = Rs 5,880]

- The following particulars relating to the year 1994 have been taken from the books of a chemical works, manufacturing and selling a chemical mixture:

Stock on 1 January 1994 Kg Rs Raw materials 2,000 2,000 Finished mixture 500 1,750 Factory stores 7,250 Purchases Raw materials 1,60,000 1,80,000 Factory stores 24,250 Sales Finished mixture 1,53,050 9,18,000 Factory scrap 8,170 Factory wages 178,650 Power 30,400 Depreciation of machinery 18,000 Salaries Factory 72,220 Office 37,220 Selling 41,500 Expenses Direct 18,500 Office 18,200 Selling 18,000 Stock on 31 December 1994 Raw materials 1,200 Finished mixture 450 Factory stores 5,550 The stock of finished mixture at the end of 1994 is to be valued at the factory cost of the mixture for that year. The purchase price of raw materials remained unchanged throughout 1994.

Prepare a statement giving the maximum possible information on cost and its break-up for 1994.

(B.Com., Delhi)

Rs 3,77,800; sales of factory scrap (7,800 kg); works cost (15,300 kg) =Rs 8,170, Rs 5,16,200; cost of sales (1,53,050 kg) = Rs 6,31,189; profit = Rs 2,86,811]

- The following data are extracted from the books of M/s. Moonshine Industries Ltd. for the calendar year 1994:

Rs Opening stock of raw material 25,000 Purchases of raw material 85,000 Closing stock of raw material 40,000 Carriage inwards 5,000 Wages—direct 75,000 Wages—indirect 10,000 Other direct charges 15,000 Rent and rates—factory 5,000 Rent and rates—office 500 Indirect consumption of material 500 Depreciation—plant, etc. 1,500 Depreciation—office furniture 100 Salary—office 2,500 Salary—salespeople 2,000 Other factory expenses 5,700 Other office expenses 900 Managing director's remuneration 12,000 Other selling expenses 1,000 Travelling expenses of salespeople 1,100 Carriage and freight outwards 1,000 Sales 2,50,000 Advance income tax paid 15,000 Advertisement 2,000 Managing director's remuneration is to be allocated as follows: Rs 4,000 to factory, Rs 2,000 to office and Rs 6,000 to selling departments. From the aforementioned information, prepare (a) prime cost, (b) works cost, (c) cost of production, (d) cost of sales and (e) net profit.

(B.Com., Delhi)

[Ans: (a) Rs 1,65,000; (b) Rs 1,91,700; (c) Rs 1,97,700; (d) Rs 2,10,800; (e) Rs 39,200]

- The following particulars are extracted from the books of a manufacturing company:

Rs Stock of material on 1 January 1994 47,000 Stock of material on 31 December 1994 50,000 Materials purchased 2,08,000 Office salaries (drawing) 9,600 Counting house salaries 14,000 Carriage inwards 8,200 Carriage outwards 5,100 Cash discount allowed 3,400 Bad debts written off 4,700 Repairs to plant and machinery 10,600 Rent, rates, etc.—factory 3,000 Rent, rates, etc.—office 1,600 Travelling expenses 3,100 Travelling commission 8,400 Production wages 1,40,000 Depreciation on plant and machinery 7,100 Depreciation on office furniture 600 Directors' fees 6,000 Gas and water charges—factory 1,500 Gas and water charges—office 300 General charges 5,000 Manager's salary 12,000 Out of 48 hours in a week, time devoted by the manager to the factory and the office was on average 40 hours and 8 hours, respectively, throughout the accounting year. Prepare a statement giving the following information: (a) prime cost, (b) factory cost as a percentage of production wages, (c) factory cost, (d) general on cost as a percentage factory cost and (e) total cost.

(B.Com., Delhi)

[Ans: (a) Rs 3,53,200; (b) 33%; (c) 3,99,400; (d) 13.42%; (e) Rs 4,49,200]

- The following details are obtained from the cost records of Comet Paints Limited:

Rs Stock of raw materials on 1 December 1994 75,000 Stock of raw materials on 31 December 1994 91,500 Direct wages 52,500 Indirect wages 2,750 Sales 2,11,000 WIP, 1 December 1994 28,000 WIP, 31 December 1994 35,000 Purchases of raw materials 66,000 Factory rent, rates and powers 15,000 Depreciation of plant and machinery 3,500 Expenses on purchases 1,500 Carriage outwards 2,500 Advertising 3,500 Office rent and taxes 2,500 Travellers' wages and commission 6,500 Stock of finished goods, 1 December 1994 54,000 Stock of finished goods, 31 December 1994 31,000 Prepare a production account giving the maximum possible break-up of costs and profit.

(B.Com., Delhi)

[Ans: prime cost = Rs 1,03,500; works cost = Rs 1,17,750; cost of production = Rs 1,20,250; cost of goods sold = Rs 1,43,250; cost of sales = Rs 1,55,750; profit = Rs 55,250]

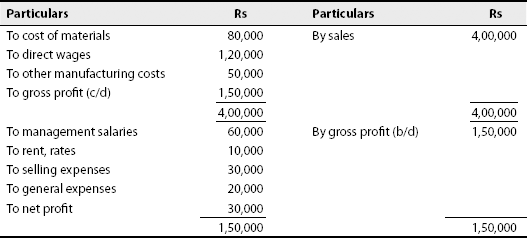

- Prepare a statement showing cost and profit from the following details, clearly showing (a) prime cost, (b) works cost, (c) cost of production, (d) cost of sales and (e) profit:

[Ans: (a) Rs 6,50,000; (b) Rs 7,37,500 – factory OH = Rs 87,500; (c) cost of production =Rs 7,96,875; administrative OH = Rs 59,375; (d) cost of sales = Rs 8,14,375; selling and distribution overheads = Rs 17,500; (e) profit = Rs 1,33,125]

- The following data are extracted from Pavan Kishore for the year 1991:

Rs Opening stock of raw materials 25,000 Closing stock of raw materials 40,000 Purchase of raw materials 85,000 Carriage inwards 5,000 Wages direct 75,000 Wages indirect 10,000 Other direct charges 15,000 Rent and rates: Factory 5,000 Office 500 Indirect consumption of material 500 Depreciation on plant 1,500 Depreciation on office furniture 100 Salary—office 2,500 Salary—salesmen 2,000 Other office expenses 900 Other factory expenses 5,700 Managing director's remuneration 12,000 Other selling expenses 1,000 Travelling expenses 1,100 Carriage outwards 1,000 Sales 2,50,000 Advance income tax paid 15,000 Advertisement 2,000 Managing director's remuneration is allocated as follows: Rs 4,000 to the factory, Rs 2,000 to the office and Rs 6,000 to the selling departments.

From the aforementioned information, calculate (a) prime cost, (b) works cost, (c) cost of production (d) cost of sales and (e) net profit.

(Andhra, 1992)

[Ans: (a) Rs 1,65,000; (b) Rs 1,91,700; (c) Rs 1,97,700; (d) Rs 2,10,800; (e) Rs 39,200]

- The following details relating to a factory are available for the month of March 1999:

It is customary to fix the selling price by adding 20% to the total cost. Prepare a cost sheet showing the profit for the month.

[Ans: prime cost = Rs 1,27,000; works cost = Rs 1,44,000; cost of production = Rs 1,61,000; cost of sales = Rs 1,89,000; profit = Rs 37,800]

- From the following particulars of a manufacturing company, prepare a statement showing (a) cost of materials used, (b) prime cost, (c) works cost, (d) percentage of works overheads to productive wages, (e) cost of production, (f) percentage of general overheads to works cost and (g) net profit:

Rs Stock of materials on 1 January 1985 20,000 Purchase of materials in January 5,50,000 Stock of finished goods on 1 January 1985 25,000 Productive wages 2,50,000 Finished goods sold 12,00,000 Works overhead charges 75,000 Office and general expenses 50,000 Stock of materials on 31 January 1985 70,000 Stock of finished goods on 31 January 1985 30,000 (Madras, 1985)

[Ans: (a) Rs 5,00,000; (b) Rs 7,50,000; (c) Rs 8,25,000; (d) 30%; (e) Rs 8,75,000; (f) 6.06%; (g) Rs 3,30,000]

- Draw a statement of cost from the following particulars:

Rs Opening stock: Materials 2,00,000 Work-in-progress 60,000 Finished goods 5,000 Closing stock: Materials 1,80,000 WIP 50,000 Finished goods 15,000 Materials purchased 5,00,000 Direct wages 1,50,000 Manufacturing expenses 1,00,000 Sales 8,00,000 Selling and distribution expenses 20,000 (Madras, 2001; Madras,)

[Ans: materials consumed = Rs 5,20,000; prime cost: Rs 6,70,000; works cost = Rs 7,80,000; cost of production of goods sold = Rs 7,70,000; cost of sales = Rs 7,90,000; profit = Rs 10,000]

- From the following particulars, prepare a cost sheet showing the components of total cost and profit for the year ended 31 December 1994.

Rs Stocks on 1 January 1994: Raw materials 2,500 WIP 822 Finished goods 1,736 Stock on 31 December 1994: Raw materials 2,625 WIP 910 Finished goods 1,575 Purchase of raw materials 2,190 Direct wages 1,715 Non-productive wages 83 Office expenses 316 Works expenses 834 Selling and distribution expenses 421 Sale of finished goods 7,331 (Bangalore, 1995)

[Ans: raw materials consumed = Rs 2,065; prime cost = Rs 3,780; works cost = Rs 4,609; cost of production = Rs 4,921; cost of production of goods sold = Rs 5,086; cost of sales = Rs 5,507; profit = Rs 1,824]

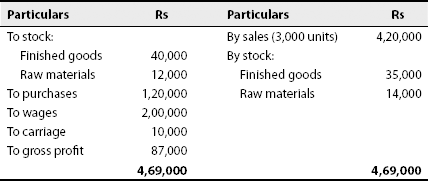

- From the trading account of a concern, prepare a cost sheet showing the cost of materials, used prime cost, cost of goods sold and profit per unit.

Trading account for the year ending on 31 December 1994:

(Bangalore, 1995)

[Ans: cost of materials used = Rs 1,28,000; prime cost = Rs 3,28,000; cost of goods sold = Rs 3,33,000; profit per unit sold = Rs 29]

- From the following information, prepare a cost sheet for the month of December 1989:

Rs Stock on hand—1 December 1989: Raw materials 25,000 Finished goods 17,300 Stock on hand—31 December 1989: Raw materials 26,200 Finished goods 15,700 Purchase of raw materials 21,900 Carriage on purchases 1,100 WIP, 1 December 1989 at works cost 8,200 WIP, 31 December 1989 at works cost 9,100 Sale of finished goods 72,300 Direct wages 17,200 Non-productive wages 800 Direct expenses 1,200 Factory overheads 8,300 Administration overheads 3,200 Selling and distribution overheads 4,200 (Madurai Kamaraj, 1991)

[Ans: raw materials consumed = Rs 21,800; prime cost = Rs 40,200; works cost = Rs 48,400; cost of production of goods produced = Rs 51,600; cost of production of goods sold = Rs 53,200; cost of sales = Rs 57,400; profit = Rs 14,900]

- From the following particulars, prepare a statement showing (a) prime cost, (b) works cost, (c) cost of production and (d) cost of sales:

Rs Opening stock of finished goods 9,750 Closing stock of finished goods 11,100 Raw materials purchased 35,250 Carriage on materials purchased 850 Direct wages 18,450 Factory expenses 2,750 Selling expenses 2,450 Office cost 1,850 Sales 75,000 Sales of scrap 250 Also show by what percentage the average selling price in the aforementioned case should be increased in order to double the net profit.

(Kerala, B.Com.)

[Ans: (a) Rs 54,550; (b) Rs 57,050; (c) Rs 58,900; (d) Rs 60,000; present profit = Rs 15,000; doubled profit = Rs 30,000; required sales = 60,000 + 30,000 = Rs 90,000;

Sale of scrap is taken as indirect material scrap and is reduced from factory expenses.

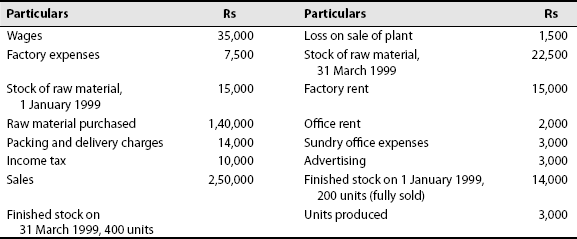

- From the following details relating to Kannan Ltd. for the quarter ending on 31 March 1999, prepare a cost sheet showing profit or loss for the quarter:

[Ans: prime cost = Rs 1,67,500; works cost = Rs 1,90,000; cost of production of goods produced = Rs 1,95,000; closing stock of finished goods = Rs 26,000; cost of production of goods sold =Rs 1,83,000; cost of sales = Rs 2,00,000; profit = Rs 50,000]

(Exclude income tax and loss on sale of plant.)

- From the following particulars, prepare a statement showing the components of total sales and the profit for the year ending on 31 December.

Rs Stock of finished goods (1 January) 6,000 Stock of raw materials (1 January) 40,000 WIP (1 January) 15,000 Purchase of raw materials 4,75,000 Carriage inwards 12,500 Factory rent, taxes 7,250 Other production expenses 43,000 Stock of finished goods (31 December) 15,000 Wages 1,75,000 Works manager's salary 30,000 Factory employees' salary 60,000 Power expenses 9,500 General expenses 32,500 Sales for the year 8,60,000 Stock of raw materials (31 December) 50,000 WIP (31 December) 10,000 (Andhra, B.Com.)

[Ans: material consumed = Rs 4,77,500; prime cost = Rs 6,52,500; works cost = Rs 8,07,250; cost of production = Rs 8,39,750; cost of production of goods sold = Rs 8,30,750; profit = Rs 29,250]

- A company received an enquiry for the supply of 10,000 steel folding chairs. The costs are estimated as follows:

Raw materials 1,00,000 kg at Re 1 per kg Direct wages 10,000 hours at Rs 4 per hour Variable overheads: Factory Rs 2.40 per labour hour Selling and distribution Rs 16,000 Fixed overheads: Factory Rs 6,000 Selling and distribution Rs 14,000 Prepare a statement showing the price to be fixed that will result in a profit of 20% on the selling price.

(C.A. Inter)

[Ans: total cost = Rs 2,00,000; profit = Rs 50,000; price to be fixed = Rs 2,50,000]

- The following information was obtained from the cost records of Aditya Chemicals Ltd. for 1998:

Rs Finished goods on 1 January 1998 50,000 Raw materials, 1 January 1988 10,000 WIP, 1 January 1988 14,000 Direct labour 1,60,000 Purchase of raw materials 98,000 Indirect labour 40,000 Heat, light and power 20,000 Factory insurance and taxes 5,000 Repairs to plant 3,000 Factory supplies 5,000 Depreciation—factory building 6,000 Depreciation—plant 10,000 Other information made available is Factory cost of goods produced in 1988 2,80,000 Raw materials consumed in 1988 95,000 Cost of goods sold in 1988 1,60,000 No office and administration expenses were incurred during 1988. Prepare a statement of cost for the year ending on 1988 giving the maximum possible information and the detailed break-up of cost.

(Madras, 1989)

[Ans: closing stock of raw material = Rs 13,000; prime cost = Rs 2,55,000; works cost excluding WIP = Rs 3,44,000; closing WIP = Rs 78,000; closing stock of finished goods = Rs 1,70,000]

EXAMINATION PROBLEMS

- From the following information, prepare a cost sheet for the month of January:

Rs Rs Stock of raw materials on 1 January 25,000 Stock of raw materials on 31 January 26,200 Purchase of raw materials 21,900 Carriage on purchases 1,100 Sale of finished goods 72,300 Direct wages 17,200 Non-productive wages 800 Direct expenses 1,200 Factory overheads 8,300 Administrative overheads 3,200 Selling overheads 4,200 (Madras, 1998)

[Ans: raw materials consumed = Rs 21,800; prime cost = Rs 40,200; works cost = Rs 49,300; cost of production = Rs 52,500; cost of sales = Rs 56,700; profit = Rs 15,600]

- A manufacturer presents the following details about the various expenses incurred by him:

Rs Raw materials consumed 70,000 Carriage inwards 2,000 Factory rent 2,400 Bad debts 440 Printing and stationery 620 Legal expenses 350 Carriage outwards 1,540 Indirect material 560 Power 4,600 Depreciation on furniture 160 Postage expenses 465 Repairs to plant and machinery 1,200 Salespeople's expense 3,400 Advertising 500 Direct wages 85,000 General manager's salary 36,000 Factory manager's salary 18,000 Depreciation on plant and machinery 1,240 Audit fees 350 Classify the aforementioned expenses under the various elements of cost, showing separately the total expenditure under each element.

(B.Com., Delhi)

[Ans: prime cost = Rs 1,57,000; factory cost = Rs 1,85,000; cost of production = Rs 2,22,945; total cost = Rs 2,28,825]

- Gopal furnishes the following data relating to the manufacture of a standard product during the month of April:

Rs Raw materials consumed 15,000 Direct labour charges 9,000 Machine hours worked 900 Machine hour rate Rs 5 Administrative overheads 20% on works cost Selling overheads Rs 0.50 per unit Units produced: 17,100 Units sold: 18,000 at Rs 4 per unit You are required to prepare a cost sheet from the aforementioned data showing(a) the cost per unit and (b) profit per unit sold and profit for the period.

[Ans: (a) Rs 2; (b) Rs 1.50; profit = Rs 27,000]

4a. A factory produces 100 units of a commodity. The cost of production is as follows:

Rs Materials 10,000 Wages 5,000 Direct expenses 1,000 Factory overheads are 125% on wages, and office overheads are 20% on works cost. Expected profit is 25% on sales.

Calculate the price to be fixed per unit.

(Madras1987)

[Ans: Price to be fixed per unit = Rs 356; prime cost = Rs 16,000; profit = Rs 8,900; sales = Rs 35,600; profit is 25% on sales or 1/3 on cost]

- A factory produces 100 units of a commodity. The cost of production is as follows:

Rs Direct materials 10,000 Direct wages 5,000 Direct expenses 1,000 Factory overheads 6,500 Administrative overheads 3,480 If a profit of 25% on sales is to be realized, what would be the selling price of each unit of the commodity? Prepare the cost sheet.

(Madras, 1997)

[Ans: selling price per unit = Rs 346.40; prime cost = Rs 16,000; works cost = Rs 22,500; cost of production = Rs 25,980; sales = Rs 34,640; profit = Rs 8,660; profit is 25% on sales or

on cost]

on cost] - The following information is obtained from the records of a factory for the period from 1 June to 30 June:

Rs Opening balance of raw materials on 1 June 15,000 Purchases of raw materials during the month 2,25,000 Wages paid 1,15,000 Factory overheads 46,000 Opening balance of WIP on 1 June 6,000 Opening balance of WIP on 30 June 7,500 Closing balance of raw materials on 30 June 12,500 Opening balance of finished goods manufactured on 1 June 30,000 Closing balance of finished goods manufactured on 30 June 27,500 Selling and distribution overheads 10,000 Administration overheads 15,000 Sales 4,50,000 Prepare statement on cost of production of goods manufactured, statement of cost of production of goods sold and statement of profit on sales.

(B.Com., Karnataka)

[Ans: cost of production of goods manufactured = Rs 4,02,000; cost of goods sold = Rs 4,04,500; gross profit = Rs 45,500; net profit = Rs 35,500]

- The Modern manufacturing company submitted the following information on 31 March 1993:

Rs Sales for the year 2,75,000 Inventories at the beginning of the year: Finished goods 7,000 WIP 4,000 Purchase of materials 1,10,000 Materials inventory: At the beginning of the year 3,000 At the end of the year 4,000 Direct labour 65,000 Factory overheads were 60% of direct labour cost Inventories at the end of the year: WIP 6,000 Finished goods 8,000 Other expenses for the year: Selling expenses Administration expenses 10% of sales Prepare a statement of cost 5% of sales (Calicut, 1994)

[Ans: material consumed = Rs 1,09,000; prime cost = Rs 1,74,000; works cost = Rs 2,11,000; cost of production of goods produced = Rs 2,24,750; cost of production of goods sold = Rs 2,23,750; cost of sales = Rs 2,51,250; profit = Rs 23,750]

- The following extracts of costing information related to commodity A for the half-year ending on 31 December 1993:

Rs Purchase of raw materials 1,20,000 Works overheads 48,000 Direct wages 1,00,000 Carriage on purchases 1,440 Stock (1 July 1993) Raw materials 20,000 Finished products (1,000 tons) 16,000 Stock (31 December 1993) Raw materials 22,240 Finished products (2,000 tons) 32,000 WIP (1 July 1993) 4,800 WIP (31 December 1993) 16,000 Sales—finished products 3,00,000 Selling and distribution overheads are Re 1 per ton sold. A total of 16,000 tons of commodities were produced during the period.

You are to ascertain (a) cost of raw materials used, (b) cost of output for the period, (c) cost of sales, (d) net profit for the period and (e) net profit per ton of the commodity.

(Madras, 1995)

[Ans: (a) Rs 1,19,200; (b) Rs 2,56,000; (c) Rs 2,55,000; (d) Rs 45,000; (e) Rs 3 per ton sold; selling overheads = Rs 15,000]

- From the following particulars, you are required to prepare a statement showing (a) the cost of materials consumed, (b) prime cost, (c) works cost, (d) total cost and (e) cost of sales and profit

Rs Stock of finished goods on 31 December 1993 73,000 Stock of raw materials on 31 December 1993 35,000 Purchase of raw materials 7,60,000 Productive wages 5,20,000 Stock of finished goods on 31 December 1994 82,500 Stock of raw materials on 31 December 1994 37,500 Sales of finished goods 15,45,800 Works overhead charges 1,30,200 Office and general charges 69,700 (B.Com., Karnataka)

[Ans: (a) Rs 7,57,500; (b) Rs 12,77,500; (c) Rs 14,07,700; (d) 14,77,400;(e) cost of sales = Rs 14,67,900 and profit = Rs 77,900]

- The following data are related to the manufacture of a standard product during the month of April 1984:

Raw material Rs 80,000 Direct wages Rs 48,000 Machine hours worked 8,000 hours Machine hour rate Rs 4 Administration overheads 10% of works cost Selling overheads Rs 1.50 per unit Units produced 4,000 Units sold 3,000 Selling price Rs 50 per unit You are required to prepare a cost sheet with respect to the preceding data showing (a) cost per unit and (b) profit for the month.

(Madras, 1986)

[Ans: (a) prime cost = Rs 1,28,000; Rs 32 per unit; works cost = Rs 1,60,000; Rs 40 per unit; cost of production = Rs 1,76,000; Rs 44 per unit; closing stock of finished goods = Rs 44,000; cost of sales = Rs 1,36,500 at Rs 45.5 per unit; profit = Rs 13,500 at Rs 4.5 per unit; sales = Rs 1,50,000]

- The directors of a manufacturing business require a statement showing the production results of the business for the month of March 1994. The cost accounts reveal the following information:

Rs Stock on hand, 1 March 1994: Raw materials 25,000 Finished goods 17,360 Stock on hand, 31 March 1994 Raw materials 26,250 Finished goods 15,750 Purchase of raw materials 21,900 WIP, 1 March 1994 8,220 WIP, 31 March 1994 9,100 Sale of finished goods 72,310 Direct wages 17,150 Non-productive wages 830 Works expenses 8,340 Office and administrative expenses 3,160 Selling and distributive expenses 4,210 You are required to construct the statement so as to show (a) value of the material consumed, (b) total cost of production, (c) cost of goods sold, (d) profit on goods sold and (e) net profit for the month.

(M.Com., Sugar)

[Ans: (a) Rs 20,650; (b) Rs 49,250; (c) Rs 50,860; (d) Rs 21,450; (e) 17,240]

- From the following particulars of product X, compile the cost sheet for the month of March 1991:

Rs Raw material: Opening stock 20,000 Purchases 1,50,000 Closing stock 10,000 Direct labour 60,000 Factory overheads 22,500 Office and administrative overheads 27,500 Finished stock: Opening stock: 500 units at Rs 11.20 per unit Closing stock: 1,500 units at current cost price Profit on sales: 20% Selling and distribution overheads: 20,000 Units produced: 25,000 units (Madras, 1991)

[Ans: prime cost = Rs 2,20,000; works cost = Rs 2,42,500; cost of production = Rs 2,70,000; closing stock of finished goods = Rs 16,200 at Rs 10.8 per unit; cost of production of goods sold = Rs 2,59,400; cost of sales = Rs 2,79,400; profit = Rs 69,850]

- From the following data relating to the manufacture of a standard product during the month of September 1983, prepare a statement showing the cost and profit per unit:

Raw material used Rs 40,000 Direct wages Rs 24,000 Manhours worked 9,500 (hours) Manhour rate Rs 4 per hour Office overheads 20% on works cost Selling overheads Re 1 per unit Units produced 20,000 units Units sold 18,000 at Rs 10 per unit (Madras, 1984)

[Ans: prime cost = Rs 64,000; works cost = Rs 1,02,000; cost of production = Rs 1,22,400 at Rs 6.12 per unit; closing stock of finished goods = Rs 12,240; cost of production of goods sold = Rs 1,10,160; cost of sales = Rs 1,28,160 at Rs 7.12 per unit; profit = Rs 51,840 at Rs 2.88 per unit; sales = Rs 1,80,000]

- Gopal furnishes the following data relating to the manufacture of a standard product during the month of April 1984:

Raw materials consumed Rs 15,000 Direct labour charges Rs 9,000 Machine hours worked 900 Machine hour rate Rs 5 Administrative overheads 20% on works cost Selling overheads Re 0.50 per unit Units produced 17,100 Units sold 16,000 at Rs 4 per unit You are required to prepare a cost sheet from the aforementioned data showing (a) the cost per unit and (b) profit per unit sold and profit for the period.

(Madras, 1989)

[Ans: prime cost = Rs 24,000, Rs 1.40 per unit; works cost: Rs 26,833 per unit; cost of production = Rs 34,200 at Rs 2 per unit; closing stock of finished goods = Rs 2,200; cost of production of goods sold = Rs 32,000; cost of sales = Rs 40,000 at Rs 2.5 per unit; profit = Rs 24,000 at Rs 1.5 per unit; sales: Rs 64,000]

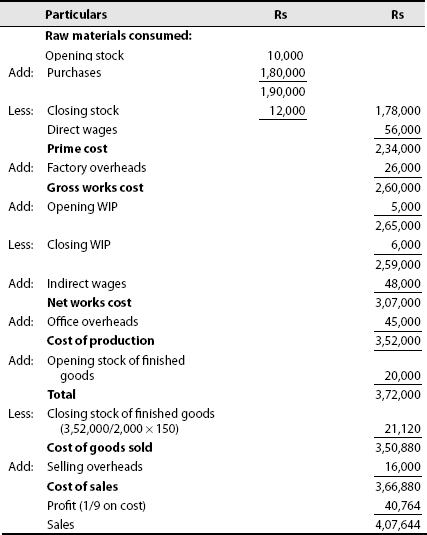

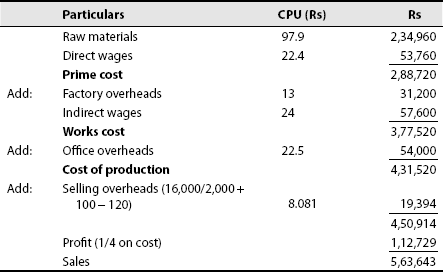

- Prepare a cost sheet for 1986 from the following details showing the total cost and cost per unit. The number of units produced is 2,000:

Rs Opening stock of raw materials 10,000 Purchases 1,80,000 Direct wages 56,000 Indirect wages 48,000 Closing stock of raw materials 12,000 WIP on 1 January 1986 5,000 WIP on 31 December 1986 6,000 Factory overheads 26,000 Office overheads 45,000 Selling overheads 16,000 Opening stock of finished goods (100 units) 20,000 The closing stock of finished goods is 120 units. Profit is 10% on sales. During 1987, it was decided to increase the production to 2,400 units. It was anticipated that

(a) Material prices would increase by 10%. (b) Wages would reduce by 20%. (c) Other expenses would remain constant per unit. (d) Expected profit would become 20% of sales.

Ascertain the selling price to be fixed per unit.

(Madras, 1987)

[Ans: For 1986, prime cost = Rs 2,34,000; works cost = Rs 3,07,000; cost of production = Rs 3,52,000; closing stock of finished goods = Rs 21,120; cost of production of goods sold = Rs 3,50,880; cost of sales = Rs 3,66,880; profit = Rs 40,764; sales = Rs 4,07,644. For 1987, prime cost = Rs 2,88,720; works cost = Rs 3,77,520; cost of production = Rs 4,31,520; cost of sales = Rs 4,50,912; profit = Rs 1,12,728; sales = Rs 5,63,640]

- The company Cooling Limited manufactured and sold 1,000 refrigerators in the year ending on 31 December 1997. The summarized trading, profit and loss account is as follows:

For the year ending on 31 December 1998, it was estimated that

- Output and sales would be 1,200 refrigerators.

- Prices of materials would go up by 20% on the level of the previous year.

- Wages would increase by 5%.

- Manufacturing cost would rise in proportion to the combined cost of materials and wages.

- Selling costs per unit would remain unchanged.

- Other expenses would also remain constant.