11

Service Costing/Operating Costing

CHAPTER OUTLINE

LEARNING OBJECTIVES

After reading this chapter, you will be able to understand:

- The meaning of operating costing

- The importance of operating costing

- The industries where operating costing is adopted

- Different units used in operating costing

- How the fares and tariff are fixed in transport industries

11.1 INTRODUCTION

It is a method of ascertaining costs of providing or operating a service. This method of costing is applied by those undertakings, which provide services rather than production of commodities. The emphasis under operating costing is on the ascertainment of cost of services rather than on the cost of manufacturing a product. This costing method is usually made use of by transport companies, gas and water works departments, electricity supply companies, canteens, hospitals, theatres and schools.

Operation costing is an advanced form of job-order and process costing. Operation costing uses the methods that are found in either process or job-order costing. Service costing is the cost of providing a service. In other words, service costing is a method of costing applied to determine the cost of rendering service. It is adopted by those businesses, which operate a service rather than produce goods. Service is their final product and this service is sold to consumers. This service may be used within the enterprise as in the case of canteen boiler houses and so on; or may be rendered to the public as in state transport, hospitals, electricity and so on. Service provided within the organization is known as internal service. Service provided outside the organisation is known as external service.

11.1.1 When is operation costing appropriate?

Operation costing is appropriate in businesses that have products that are very similar, yet differentiated in some form from each other. This difference can be in the finishing or in the actual functionality of the product.

For computing the operating cost, it is necessary to decide first, about the unit for which the cost is to be computed.

The cost units usually used in the following service undertakings are as below:

| Transport service Supply service Hospital Canteen Cinema | Passenger kilometre, quintal kilometre, or tonne-kilometre Kilowatt-hour, cubic metre, per kilogram, per litre Patient per day, room per day or per bed, per operation, etc. Per item, per meal, etc. Per ticket. |

11.1.2 Cost units used in service costing

The selection of cost unit is different in service costing. Both simple and composite cost units are used.

| Name of the service | Cost unit |

|---|---|

| (I) Passenger transport (II) Goods transport (III) Hospital (IV) Electricity supply (V) Canteen (VI) Cinema theatre (VII) Lodge | Per passenger kilometre Per tonne-kilometre Per patient bed Per kilowatt-hour Per meal per person Per man show Per room day |

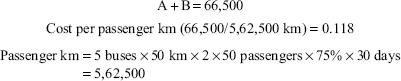

Passenger kilometre = No. of vehicles × No. of. days × No. of. trips × Distance covered × Capacity × Normal passenger travelling

11.1.3 Transport costing

Transport industries include air, water, road and railways. Motor transport includes private cars, buses, taxis, carriers and lorries. The objectives of motor transport costing may be summarized as follows:

- To provide information whereby the efficiency with which the vehicles are rented may be judged.

- To provide an accurate basis for quotation and fixing of rates

- To ensure that all journeys have been carried out in proper time, fuel consumed is not excessive and that tyres are properly maintained

- To provide cost comparison between own transport and alternative, e.g. hiring

- To compare the cost of maintaining of one group of vehicles with another group

- To determine what should be charged against departments using the service

- To decide at what price the use of vehicle can be charged

- To ensure that cost of maintenance and repairs is not excessive

Illustration 1

| Number of buses Days operated Round trips by each bus Distance of route 20 km long one side Capacity of bus Normal passenger travelling 90% of capacity. | 10 25 4 40 seats |

Tonne kilometre = Total capacity (number of vehicles used × tons carried) × average kilometre × number of trips × days of month × percentage of vehicles runs on or average × capacity used.

Solution:

Illustration 2

| Number of Vehicles | Capacity (in tonnes each) |

|---|---|

| 10 05 20 | 02 06 05 |

Each vehicle makes 5 trips a day covering distance of 10 km in each trip. On average 10% of the vehicles are laid up for repairs daily and 80% of capacity of vehicle is actually used. Company operates for 25 days a month.

Solution:

Accounting Procedure for Transport Costing

Preparation of Cost Sheet under Operating Costing

For preparing a cost sheet under operating cost, costs are usually accumulated for a specified period namely a month, a quarter, or a year.

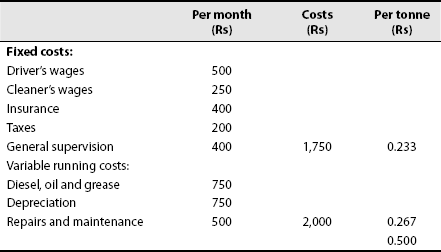

All the accumulated costs should be classified under the following three heads:

- Fixed costs or standing charges,

- Variable costs or running charges,

- Semi-variable costs or maintenance costs.

Note: In the absence of information about semi-variable costs, the costs may be shown under two heads only, i.e. fixed and variable.

Under operating costing, the cost per unit cost of service may be calculated by dividing the total cost for the period by the total units of service in the period.

Treatment of depreciation and interest—depreciation, if related to effluxion of time, may be treated as fixed. If it is related to the activity level, it may be treated as variable.

If information about interest is explicitly given, it may be treated as fixed cost.

| Examples of fixed charges are: | Examples of fixed charges are: | Examples of variable charges are: |

| (a) wages (if passed monthly) | (a) wages (if passed monthly) | (a) petrol and diesel |

| (b) rent | (b) rent | (b) oil |

| (c) licence | (c) licence | (c) repair |

| (d) insurance | (d) insurance | (d) maintenance |

| (e) salary | (e) salary | (e) wages (if based on km run) |

| (f) taxation | (f) taxation | (f) depreciation |

| (g) interest | (g) interest | for calculation of the rate per km/per passenger the following points are essential |

| (h) supervision | (h) supervision | |

| (a) days maintained | ||

| (b) days operated | ||

| (c) days idle | ||

| (d) total hours operated | ||

| (e) total kilometre covered | ||

| (f) total trips made | ||

| (g) total kilometre run |

Illustration 3

| Number of buses | 4 |

| Number of days operated | 30 |

| Number of trips per day per bus | 2 |

| Seating capacity | 60 persons |

| Average passengers traveling | 40 |

| Distance covered on way | 20 km |

Calculate passenger kilometre

Solution:

Illustration 4

| Number of buses | 5 |

| Number of days operated | 25 |

| Number of trips made | 2 |

| Seating capacity | 60 persons |

| Average passengers travelling | 75% |

| Distance covered two way | 48 km |

Calculate passenger kilometre

Solution:

Illustration 5

| Number of lorries | 5 |

| Capacity of a lorry | 8 tonnes |

| Number of days operated | 20 days |

| Kilometre covered each day | 200 km |

| Load carried 80% of capacity | |

| Kilometre run empty | 30% |

Calculate tonne-kilometre

Solution:

Illustration 6

| Number of lorries | 10 |

| Capacity of a lorry | 20 tonnes |

| Number of days operated | 26 days |

| Number of trips per day | 1 |

| Average load carried 70% of capacity | |

| Empty running | 40% |

| Kilometre covered each day | 200 km |

Calculate tonne-kilometre.

Solution: Calculation of total tonne-kilometre

Illustration 7

Operating cost sheet of truck for the year

| p.a. | per km | |

|---|---|---|

| Particulars | Rs P. | Rs P. |

| Fixed charges: | ||

| Road licence | 650 | |

| Insurance | 800 | |

| Garage rent | 700 | |

| Supervision | 1,400 | |

| Interest on vehicle (10% on 30,000) | 3,000 | |

| Total fixed charges | 6,550 | 0.33 |

| Variable charges: | ||

| Petrol | 0.20 | |

| Repairs | 1.80 | |

| Type allocation | 0.40 | |

| Driver's wage | 0.10 | |

| Depreciation | 0.30 | |

| Operating cost per running km | 3.13 |

Illustration 8

| Value of vehicle | Rs 40,000 |

| Road licence (annual) | Rs 2,000 |

| Driver's wages (per month) | Rs 3,000 |

| Insurance (annual) | Rs 3,000 |

| Garage rent (annual) | Rs 4,000 |

| Direct wages (per month) | Rs 3,000 |

| Cost of petrol per litre | Rs 25 |

| Mileage per litre | 30 |

| Estimated life in miles | 1,00,000 |

| Annual mileage runs | 10,000 |

Calculate cost per mile.

Solution: Calculation of cost per mile

| p.a. | per km | |

|---|---|---|

| Particulars | Rs P. | Rs P. |

| Standing charges | ||

| Road licence | 2,000 | |

| Insurance | 3,000 | |

| Garage rent | 4,000 | |

| Total standing charges | 9,000 | 0.90 |

| Variable charges | ||

| Type maintenance | 4.00 | |

| Petrol | 0.83 | |

| Driver's wages | 3.60 | |

| Depreciation | 0.40 | |

| Operating cost per mile | 9.73 |

COST PER EFFECTIVE KILOMETRE

Illustration 9

Anandhan owns a fleet of taxis and the following information is available from the records maintained by him.

| 1. Number of taxis | 10 |

| 2. Cost of each taxi | Rs 54,600 |

| 3. Salary of manager | Rs 700 p.m. |

| 4. Salary of accountant | Rs 500 p.m. |

| 5. Salary of cleaner | Rs 200 p.m. |

| 6. Salary of mechanics | Rs 400 p.m. |

| 7. Garage rent | Rs 600 p.m. |

| 8. Insurance premium | 5% p.a. |

| 9. Annual tax | Rs 900 per taxi |

| 10. Driver's salary | Rs 350 p.m. per taxi |

| 11. Annual repairs | Rs 1,000 per taxi |

Total life of a taxi is about 2,00,000 km. A taxi runs in all 3,000 km in a month and 30% of this distance has to be run without any passenger. Petrol consumption is one litre for every 10 km at 4.41 per litre. Oil and other expenses are Rs 10.50 per 100 km.

Calculate the cost of running a taxi per km.

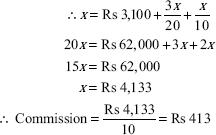

Solution: Cost of running a taxi per km

| per month | per km | |

|---|---|---|

| Particulars | Rs P. | Rs P. |

| Fixed charges: | ||

| Manager's salary | 70 | |

| Accountant salary | 50 | |

| Cleaner's salary | 20 | |

| Mechanics salary | 40 | |

| Garage rent | 60 | |

| Insurance premium | 227.50 | |

| Annual tax | 75 | |

| Driver's salary | 350 | |

| Annual repairs | 83.33 | |

| Total fixed charges | 975.83 | 0.4646 |

| Variable charges: | ||

| Depreciation | 819 | |

| Petrol | 1,323 | |

| Oil and other expenses | 315 | |

| Total variable charges | 2,457 | 1.17 |

| Cost of running a taxi per km | 1.635 |

Illustration 10

Ram owns a fleet of taxies and the following information is available from the records maintained by him.

| 1. Number of taxis | 10 |

| 2. Cost of each taxi | Rs 50,000 |

| 3. Salary of manager | Rs 1,000 p.m. |

| 4. Salary of accountant | Rs 600 p.m. |

| 5. Salary of cleaner | Rs 200 p.m. |

| 6. Salary of mechanics | Rs 400 p.m. |

| 7. Garage rent | Rs 600 p.m. |

| 8. Insurance premium | 5% p.a. |

| 9. Annual tax | Rs 600 per taxi |

| 10. Driver's salary | Rs 500 p.m. per taxi |

| 11. Annual repairs | Rs 1,000 per taxi |

Total life of a taxi is about 2,00,000 km. A taxi runs in all 3,000 km in a month of which 30% of it runs empty. Petrol consumption is one litre for 10 km @ Rs 7 per litre. Oil and other sundries are Rs 10 per 100 kilometres.

Solution: Calculation of effective km run

| Taxi runs in a month | 3,000 | |

| Less: 30% empty | 900 | |

| Effective km run | 2,100 | |

| Fixed charges: | ||

| Manager's salary | 100 | |

| Accountant salary | 60 | |

| Cleaner's salary | 20 | |

| Mechanics salary | 40 | |

| Garage rent | 60 | |

| Insurance premium | 208.33 | |

| Annual tax | 50 | |

| Driver's salary | 500 | |

| Annual repairs | 83.33 | |

| Total fixed charges | 1,121.66 | 0.53 |

| Variable charges: | ||

| Petrol | 2,100 | |

| Oil and other expenses | 300 | |

| Depreciation | 750 | |

| Total variable charges | 3,150 | 1.50 |

| Cost of running a taxi per km | 2.03 |

Illustration 11

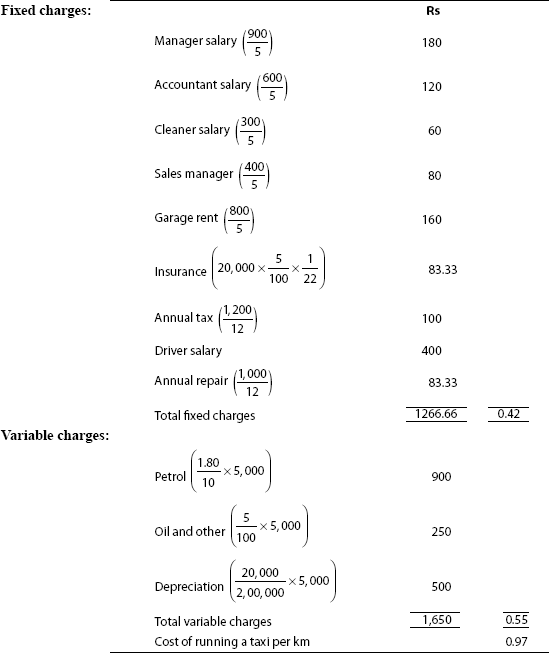

Jawan owns a fleet of taxis and the following information is available from the records maintained by him:

| 1. Number of taxis | 5 |

| 2. Cost of each taxi | Rs 20,000 |

| 3. Salary of manager | Rs 900 p.m. |

| 4. Salary of accountant | Rs 600 p.m. |

| 5. Salary of cleaner | Rs 300 p.m. |

| 6. Salary of mechanics | Rs 400 p.m. |

| 7. Garage rent | Rs 800 p.m. |

| 8. Insurance premium | 5% p.a. |

| 9. Annual tax | Rs 1,200 per taxi |

| 10. Drivers salary | Rs 400 p.m. per taxi |

| 11. Annual repair | Rs 1,000 per taxi |

Total life of a taxi is about 2,00,000 km. A taxi runs in all 5,000 km in a month of which 40% of it runs empty. Petrol consumption is one litre for 10 km @ Rs 1.80 per litre. Oil and other sundries are Rs 5 per 100 km.

Calculate the cost of running a taxi per kilometre.

Solution: Calculate effective km

| Taxi run in a month | 5,000 |

| (Less) 40% empty | 2,000 |

| Effective km run | 3,000 |

Illustration 12

| Staff salary Rs 60,000 per annum | |

| Room attendant's salary is Rs 6 per day. | |

| Room attendants are needed only when the room is occupied. There is one room attendant per room. | |

| Normal lighting expenses for a room for a month is Rs 60 | |

| Power is used only in winter and normal charge per month when occupied for a room is Rs 30 | |

| Repairs to building Rs 12,000 per annum | |

| Linen and cleaning | Rs 5,200 p.a. |

| Other expenses | Rs 4,800 p.a. |

| Interior decoration | Rs 12,000 p.a. |

| Cost of building | Rs 4,20,000 |

| Rate of depreciation | 10% |

| Other equipments | Rs 1,40,000 |

| Depreciation | 10% |

| Investment | Rs 10,00,000 interest 10% |

| There are 100 rooms in the hotel. | |

| 70% of the room are normally occupied in summer. | |

| 70% of the room are normally occupied in winter. | |

| Winter and summer are of six months each. | |

| Normal days in a month is 30 | |

| Profit to be earned | 25% on cost |

Calculate the room to be charged per day.

Solution: Calculation of room days:

Total Rs 1,08,000

Calculation of lighting:

Total Rs 36,000

Calculation of power:

Statement of operating cost

| Particulars | p.a. |

| Staff salary | 60,000 |

| Room attendants | 1,08,000 |

| Lighting | 36,000 |

| Power | 5,400 |

| Repairs | 12,000 |

| Linen and cleaning | 5,200 |

| Other expenses | 4,800 |

| Interior decoration | 12,000 |

| Depreciation on building | 42,000 |

| Depreciation on equipments | 14,000 |

| Interest on investments | 1,00,000 |

| 3,99,400 | |

| Profit (3,99,400 − 1,00,000) × 25% | 74,850 |

| 4,74,250/18,000 | |

| Rs 26.35 |

Power House Costing

It is concerned with the ascertainment of cost per unit of electricity produced. The unit of cost referred here is kilometre per hour. Here, labour is treated as variable charges.

Boiler House Costing

Boiler houses too take to operating costing. Their aim is to ascertain the total and per unit cost of generating steam or electricity so as to fix departmental charges and outside tariffs while the details of constituent elements of cost are furnished by the cost office; technical data is supplied as to steam pressure, evaporation metre—reading, factory heating, turbines, losses. are supplied by the engineering department. Standards of expenditure should be worked out under each major head on the basis of detailed studies.

The main heads of expenditure for an undertaking like boiler house are the following:

- Water—cost of supply, purification and softening.

- Indirect materials—service materials and small tools.

- Fuel—coal or oil, including of course its cartage handling and storage.

- Labour—wage of coal handlers, stockers and ash removers.

- Supervision—wages of foremen and salary of the works manager.

- Maintenance—furnace repairs, renewal of fire bars, replacement of fire iron and so on.

- Overhead costs—rent, rates, depreciation, insurance and interest on capital.

Illustration 13

| Total units generated | 14,00,000 kWh |

| Operating labour | Rs 80,000 |

| Repairs and maintenance | Rs 60,000 |

| Lubricants | Rs 60,000 |

| Plant supervision | Rs 1,40,000 |

| Administration overheads | Rs 1,20,000 |

| Coal consumed per kWh in 4.5 kg | |

| Rate of coal per kg | 0.60 paise |

| Depreciation @ 10% on capital cost of Rs 4,00,000 | |

| Prepare operating cost sheet for kWh. |

Solution: Operating cost sheet

Particulars per kWh

Fixed charges

| Plant supervision | 1,40,000 | |

| Administration overheads | 1,20,000 | |

| Total fixed charges | 2,60,000/14,00,000 | 0.1857 |

Variable charges

| Operating labour | 80,000 |

| Repairs | 60,000 |

| Lubricants | 60,000 |

| Depreciation (4,00,000 × 10%) | 40,000 |

| 2,40,000/14,00,000 | 0.1714 |

| Coal consumed (4.5 kg × 0.60) | 2.70 |

| Cost per kWh | 3.0571 |

Illustration 14

| Operating labour | Rs 24,000 |

| Plant supervision | Rs 64,000 |

| Lubricants | Rs 12,600 |

| Repairs | Rs 22,400 |

| Administration overheads | Rs 1,20,000 |

| Capital cost | Rs 1,60,000 |

| Units produced | Rs 16,00,000 |

| Coal consumed per kWh in 2.5 kg | |

| Depreciation | 10% |

| Rate of coal per kg | 0.80 paisa |

Prepare cost per unit of kWh.

Solution: Operating cost shee

| kWh | |

|---|---|

| Particulars | Rs |

| Fixed charges | |

| Plant supervision | 64,000 |

| Administration overheads | 1,20,000 |

| 1,84,000/16,00,000 | 0.115 |

| Variable charges | |

| Operating labour | 24,000 |

| Repairs | 22,400 |

| Lubricants | 12,600 |

| Depreciation (1,60,000 × 10%) | 16,000 |

| 75,000/16,00,000 | 0.047 |

| Coal consumed (2.5 kg × 0.80) | 2.00 |

| Cost per kWh | 2.162 |

Illustration 15

From the following data relating to two different vehicles A and B, compute the cost per running mile:

| Vehicle A Rs | Vehicle B Rs | |

|---|---|---|

| Mileage run (annual) | 15,000 | 6,000 |

| Cost of vehicle | 30,000 | 20,000 |

| Road licence (annual) | 1,000 | 1,000 |

| Insurance (annual) | 800 | 600 |

| Garage rent (annual) | 1,000 | 500 |

| Supervision and salaries | 1,500 | 1,600 |

| Driver's wage per hour | 3 | 3 |

| Cost of fuel per gallon | 3 | 3 |

| Miles run per gallon | 20 miles | 15 miles |

| Repairs and maintenance per mile | 1.65 | 2.00 |

| Tyre allocation per mile | 0.80 | 0.60 |

| Estimated life of vehicles | 1,00,000 miles | 75,000 miles |

Charge interest at 5% per annum on cost of vehicles. The vehicles run 20 miles per hour on an average.

Solution: Cost sheet (cost per mile running)

| Vehicle A Rs | Vehicle B Rs | |

|---|---|---|

| A. Standing charges: | ||

| | 4,500 | 1,600 |

| Road licence | 1,000 | 1,000 |

| Insurance | 800 | 600 |

| Interest @ 5% | 1,500 | 1,000 |

| Total | 7,800 | 4,200 |

| B. Maintenance charges: | ||

| Garage rent | 1,000 | 500 |

| Supervision and salaries | 1,500 | 1,600 |

| Repairs and maintenance | 24,750 | 12,000 |

| Total | 27,250 | 14,100 |

| C. Running charges: | ||

| Petrol: | 2,250 | 1,200 |

| Driver's wages: miles run × 3/20 | 2,250 | 900 |

| Tyre expenses | 12,000 | 3,600 |

| Total | 16,500 | 5,700 |

| Total operating cost (A + B + C) | 51,550 | 24,000 |

| Total miles run | 15,000 | 6,000 |

| Cost per running mile | 3.44 | 4 |

Problem 1. From the following data relating to two different vehicles A and B, compute the cost per running mile:

| A Rs | B Rs | |

|---|---|---|

| Mileage run (annual) | 15,000 | 6,000 |

| Cost of vehicles | 25,000 | 15,000 |

| Road licence (annual) | 750 | 750 |

| Insurance (annual) | 700 | 400 |

| Garage rent (annual) | 600 | 500 |

| Supervision, salaries, etc. (annual) | 1,200 | 1,200 |

| Driver wage per hour | 8 | 8 |

| Cost of petrol per litre | 10 | 10 |

| Miles run per litre | 20 miles | 15 miles |

| Repair and maintenance charge (per mile) | 0.20 | 0.30 |

| Tyre allocation per mile | 0.80 | 0.60 |

| Estimated life of the vehicle | 1,00,000 miles | 75,000 miles |

You are to charge interest on cost of vehicles at 5% per annum. The vehicles run 20 miles per hour on an average.

(ICWA)

[Ans: Rs 2.45 (Vehicle A); Rs 2.77 (Vehicle B)]

Illustration 16

Work out in appropriate cost sheet form, the unit cost per passenger mile for the year 1968–1969 for a fleet of passenger buses run by a transport company from the following figures extracted from its books:

5 passenger buses costing Rs 50,000, Rs 1,20,000, Rs 45,000, Rs 55,000 and Rs 80,000, respectively. Yearly depreciation of vehicles—20% of the cost. Annual repair, maintenance and spare parts—80% of depreciation.

| Wages of 10 drivers @ Rs 100 each per month |

| Wages of 20 cleaners @ Rs 50 each per month |

| Yearly rate of interest @ 4% on capital |

| Rent of six garages @ Rs 50 each per month |

| Director's fees @ Rs 400 per month |

| Office establishment @ Rs 1,000 per month |

| Licence of taxes @ Rs 1,000 every 6 months |

| Realization by sale of old tyres and tubes @ Rs 3,200 every six months. |

| 900 passengers were carried over 1,600 miles during the year |

(I.C.W.A. Final)

Solution:

| Rs | Cost per passenger mile Re | |

|---|---|---|

| Annual fixed expenses | ||

| Interest @ 4% on capital costs | 14,000 | |

| Rent for six garages @ 50 p.m. | 3,600 | |

| Director's fees | 4,800 | |

| Office establishment | 12,000 | |

| Licence and taxes | 2,000 | |

| Wages of drivers (10 × 12 × 100) | 12,000 | |

| Wages of cleaners (20 × 12 × 50) | 12,000 | |

| Total | 60,400 | 0.042 |

| Annual variable expenses | ||

| Depreciation @ 20% on Rs 3,50,000 | 70,000 | 0.048 |

| Repairs and maintenance charges 80% of Rs 70,000 | 56,000 | 0.039 |

| 0.129 | ||

| Less: Recovery from sale of tyres and tubes | 64,000 | 0.004 |

| Cost per passenger mile | 0.125 |

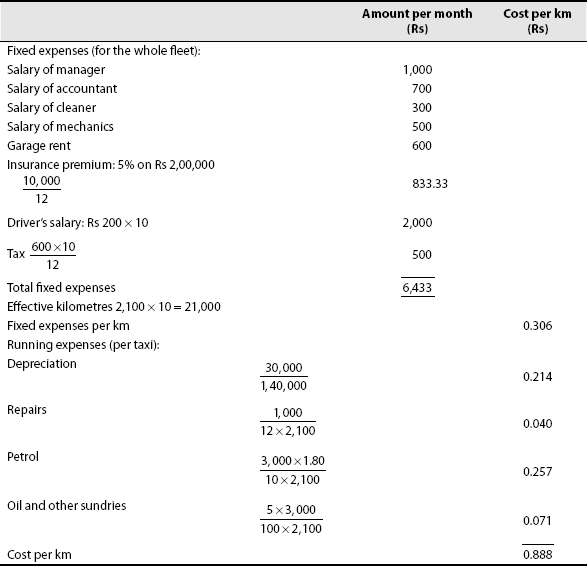

Problem 2. Anandhan owns a fleet of Taxis and the following information is available from the records maintained by him.

| 1. Number of taxis | 10 |

| 2. Cost of each taxi | Rs 54,600 |

| 3. Salary of manager | Rs 700 p.m. |

| 4. Salary of accountant | Rs 500 p.m. |

| 5. Salary of cleaner | Rs 200 p.m. |

| 6. Salary of mechanics | Rs 400 p.m. |

| 7. Garage rent | Rs 600 p.m. |

| 8. Insurance premium | 5% p.a. |

| 9. Annual tax | Rs 900 per taxi |

| 10. Driver's salary | Rs 350 p.m. per taxi |

| 11. Annual repairs | Rs 1,000 per taxi |

Total life of a taxi is about 2,00,000 km. A taxi runs in all 3,000 km in a month and 30% of this distance has to be run without any passenger. Petrol consumption is one litre for every 10 km at 4.41 per litre. Oil and other expenses are Rs 10.50 per 100 km.

Calculate the cost of running a taxi per km.

(Madras, 1995)

[Ans: Cost of running a taxi per km: Rs 1.635; Cost per taxi per month: Rs 3,432.83;

Effective running km per month per taxi: 2,100 km]

Illustration 17

You have been given a permit to run a bus on a route 20 km long. The bus costs you Rs 1,00,000. It has to be insured @ 3% p.a. and the annual tax will be Rs 2,000. Garage rent is Rs 100 p.m. Annual repairs will be Rs 1,000 and the bus is likely to last for 5 years at the end of which the scrap value is likely to be Rs 5,000.

The driver's salary will be Rs 150 p.m. and the conductor's Rs 100 together with 10% of the takings as commission (to be shared equally by both). Stationery will cost Rs 50 p.m. The manager-cum-accountant's salary will be Rs 450 p.m.

Diesel and oil be Rs 25 per 100 km. The bus will make 3 round trips for carrying on the average 40 passengers on each trip. Assuming 15% profit on takings, calculate the bus fare to be charged from each passenger. The bus will work on the average 25 days in a month.

Solution: Operating cost statement

| Bus No. DLP 4179 carrying capacity: 40 | Per annum Rs P. | Per 100 Passenger km. Rs P. |

|---|---|---|

| 1 | 2 | 3 |

| A. Standing charges | ||

| Depreciation (1,00,000 − 5,000) ÷ 5 | 19,000 | |

| Tax | 2,000 | |

| Insurance | 3,000 | |

| Stationery | 600 | |

| Manager's salary | 5,400 | |

| Total | 30,000 | 2.083 |

| B. Maintenance charges | ||

| Garage rent | 1,200 | |

| Repairs | 1,000 | |

| Total | 2,200 | 0.152 |

| C. Operating or running charges | ||

| Diesel and oil | 9,000 | |

| Driver's salary | 1,800 | |

| Conductor's salary | 1,200 | |

| Total | 12,000 | 0.833 |

| Grand total (A + B + C) | 3.068 | |

| Loading @ 25/75 | 1.022 | |

| Fare per passenger km | 4.09 |

Notes:

- Number of km run in a month: 3 × 2 × 20 × 25 = 3,000

- Diesel and oil: 3,000 × 25/100 = Rs 750

- Number of passenger km

per month: 3,000 × 40 = 1,20,000

per annum: 1,20,000 × 12 = 14,40,000

- Loading: If taking is Rs 100, 10 will have to be given as commission and 15 must remain as profit; the cost must therefore be 75. On 75 the loading must be 25 to make the taking equal to 100.

Problem 3. A transport company is running four buses between two towns, which are 50 km apart. Seating capacity of each bus is 40 passengers. The following particulars were obtained from their books for April 1998:

| Rs | |

|---|---|

| Wages of drivers and conductors | 2,400 |

| Salaries to office staff | 1,000 |

| Diesel and other oils | 4,000 |

| Repairs and maintenance | 800 |

| Taxes and insurance | 1,600 |

| Depreciation | 2,600 |

| Interest and other charges | 2,000 |

| 14,400 |

Actual passengers carried were 75% of the seating capacity. All the four buses run on all days of the month. Each bus made one round trip per day. Find out the cost per passenger km.

(Madras, B.Com., (ICE) C & M, May 1999; April 1998; B.Com., Sept. 1988; B.A 1993)

[Ans: Passenger km for the month: 3,60,000; Cost per passenger km = Re 0.038888 (or) 0.04]

Illustration 18

Jaidka owns a fleet of taxis and the following information is available from the records maintained by him:

| 1. Number of taxis | 10 |

| 2. Cost of each taxi | Rs 30,000 |

| 3. Salary of manager | Rs 1,000 p.m. |

| 4. Salary of accountant | Rs 700 p.m. |

| 5. Salary of cleaner | Rs 300 p.m. |

| 6. Salary of mechanics | Rs 500 p.m. |

| 7. Garage rent | Rs 600 p.m. |

| 8. Insurance premium | 5% p.a. |

| 9. Annual tax | 600 per taxi |

| 10. Drivers salary | Rs 200 p.m. per taxi |

| 11. Annual repair | Rs 1,000 per taxi |

Total life of a taxi is about 2,00,000 km. A taxi runs in all 3,000 km in a month of which 30% of it runs empty. Petrol consumption is one litre for 10 km @ Rs 1.80 per litre. Oil and other sundries are Rs 5 per 100 km.

Calculate the cost of running a taxi per kilometre.

Solution: Operating cost sheet

(Effective km 2,100)

Problem 4. Ram owns a fleet of taxies and the following information is available from the records maintained by him.

| 1. Number of taxis | 10 |

| 2. Cost of each taxi | Rs 50,000 |

| 3. Salary of manager | Rs 1,000 p.m. |

| 4. Salary of accountant | Rs 600 p.m. |

| 5. Salary of cleaner | Rs 200 p.m. |

| 6. Salary of mechanics | Rs 400 p.m. |

| 7. Garage rent | Rs 600 p.m. |

| 8. Insurance premium | 5% p.a. |

| 9. Annual tax | Rs 600 per taxi |

| 10. Driver's salary | Rs 500 p.m. per taxi |

| 11. Annual repairs | Rs 1,000 per taxi |

Total life of a taxi is about 2,00,000 k.m. A taxi runs in all 3,000 km in a month of which 30% of it runs empty. Petrol consumption is one litre for 10 km @ Rs 7 per litre. Oil and other sundries are Rs 10 per 100 kilometres.

(CA, ICWA)

[Ans: Rs 2.03]

Illustration 19

An entrepreneur owns a bus, which runs from Delhi to Agra and back for 25 days in a month. The distance from Delhi to Agra is 170 km. The bus completes the trip from Delhi to Agra and back on the same day. Calculate the fare the entrepreneur should charge a passenger if he wants to earn a profit of 33.33% on cost. The following information is further available

| Cost of bus | Rs 3,50,000 |

| Salary of driver per month | Rs 1,200 |

| Salary of conductor per month | Rs 700 |

| Salary of part-time accountant per month | Rs 480 |

| Insurance per annum | Rs 6,720 |

| Diesel consumption 16 km per gallon costing | Rs 26 |

| Local taxes per annum | Rs 1,200 |

| Lubricant oil per 100 km | Rs 25 |

| Repairs and maintenance per annum | Rs 1,000 |

| Licence fee per annum | Rs 3,000 |

| Normal capacity (person) | Rs 50 |

| Depreciation rate per annum | Rs 15 |

The bus usually runs full up to 90% of its capacity both ways. Interest is payable on the cost of bus at 10% per annum.

Solution: Operating cost statement to determine the fare of running a bus from Delhi to Agra per passenger km.

| Particulars | Total cost (Rs) |

| (i) Standing charges | |

| Salary of driver (Rs 1,200 × 12) | 14,400 |

| Salary of conductor (Rs 700 × 12) | 8,400 |

| Salary of part-time (Rs 480 × 12) | 5,760 |

| Insurance | 6,720 |

| Local taxes | 1,200 |

| Licence fee | 3,000 |

| Interest (10% × 3,50,000) | 35,000 |

| (ii) Running charges | 74,480 (i) |

| Depreciation of bus (15% × 3,50,000) | 52,500 |

| Diesel cost per annum (170 × 2 × 25 days × 12 months) × Rs 25 ÷ 16 | 1,59,375 |

| Lubricant oil (1,02,000 km × Rs 20) ÷ 100 | 20,400 |

| Repairs and maintenance per annum | 1,000 |

| 2,33,275 (ii) | |

| (iii) Total charges (I + II) | 3,07,755 |

| (iv) Total passenger km in a year (170 × 2 × 25 days × 12 months × 45 persons) | 45,90,000 |

| (v) Cost per passenger km (III + IV) | 0.067 |

| (vi) Add desire profit (33½% on cost) | 0.022 |

| Fare per passenger km | 0.088 |

| Fare charges (Re 0.089 × 170 km) | 15.13 |

Problem 5. A person owns air condition bus, which runs between Delhi and Chandigarh and back for 10 days in a month. The distance between Delhi and Chandigarh is 150 miles. The bus completes the trip from Delhi and Chandigarh and will be back on the same day.

The bus goes to Agra for another 10 days. The distance between Delhi and Agra is 120 miles. This trip is also completed on the same day. For the rest of the 4 days of its operation, it runs in the local city. Daily distance covered is 40 miles.

Calculate the charge to be made by the person when he wants to earn profit of 33 1/3% on his takings. The other information is:

| Cost of the bus | Rs 1,00,000 |

| Depreciation | 20% p.a. |

| Salary of driver | Rs 650 p.m. |

| Salary of conductor | Rs 650 p.m. |

| Salary of accountant | Rs 360 p.m. |

| Insurance | Rs 1,680 p.a. |

| Diesel consumption 4 miles per litre costing Rs 3 per litre | |

| Road tax | Rs 600 p.a. |

| Lubricant | Rs 20 per 100 miles |

| Repairs and maintenance | Rs 500 p.a. |

| Permit fee | Rs 284 p.m. |

| Normal capacity | 50 per sons |

The bus generally occupies 90% of the capacity when it goes to Chandigarh, 80% when it goes to Agra. It is always full when it runs within the city. Passenger tax is 20% of his net takings.

(B. Com., Bangalore)

[Ans: Cost per passenger per mile Re 0.072; Charges for Chandigarh per passenger:

Rs 10.80; Charges for Agra per passenger: Rs 8.64]

Illustration 20

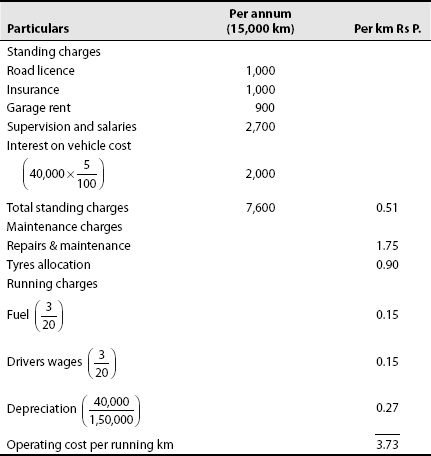

Compute cost per running kilometre from the following data of a truck.

| Estimated life of vehicle | 1,50,000 km |

| Annual running | 15,000 km |

| Rs P. | |

|---|---|

| Cost of vehicle | 40,000 |

| Road licence (annual) | 1,000 |

| Insurance (annual) | 1,000 |

| Garage rent (annual) | 900.00 |

| Supervision and salaries (annual) | 2,700.00 |

| Drivers’ wages per hour | 3.00 |

| Cost of fuel per litre | 3.00 |

| Repairs and maintenance per km | 1.75 |

| Tyre allocation per km | 0.90 |

Charge interest at 5% per annum on cost of vehicle. The vehicle runs 20 km per hour on an average and one litre of fuel gives 20 km.

Solution: Operating cost sheet of truck for the year

Note: Depreciation and driver's wages are running charges because they are related to the distance covered.

Problem 6. From the following data calculate the cost per mile of a vehicle:

| Rs | |

|---|---|

| Value of vehicle | 1,00,000 |

| Garage rent per year | 1,200 |

| Insurance charges per year | 400 |

| Road tax per year | 500 |

| Driver's wages per month | 600 |

| Cost of petrol per litre | 6.40 |

| Tyre maintenance per mile | 0.80 |

| Estimated life—1,50,000 miles | |

| Miles per litre of petrol-8 | |

| Estimated annual mileage-6,000 |

(B. Com., Kerala)

[Ans: Rs 3.82]

Illustration 21

Jayakumar with an inter-state bus permit, has been running a bus of 50 passenger capacity every month as follows:

- Madras–Kolar (150 km apart)—Round Trip, 10 days in a month with 90% passengers.

- Madras–Chittoor (200 km apart)—Round Trip, 10 days in a month with 80% passengers

- Madras–Tirupathi (150 km apart)—Round Trip, 10 days in a month with 70% passengers.

He requests you to fix ‘cost-based’ passenger rates, providing the following information.

- Passenger tax payable to Government 1/6 of gross receipts.

- Commission to conductor and driver at 5% on net receipts.

- Required profit 35% on net receipts.

- Bus purchase price Rs 2,10,000 to be depreciated at 10% p.a.

- Interest on the capital cost of bus at 5% p.a.

- Expenses of the bus were

| Rs | |

|---|---|

| Permit fees per annum | 14,400 |

| Token tax per annum | 5,100 |

| Insurance per annum | 9,000 |

| Office expenses (apportioned per month) | 1,000 |

| Tyres and tubes Re 0.4 per km | |

| Diesel 10 km per litre at Rs 10 per litre | |

| Drivers salary per month | 1,200 |

| Conductors salary per month | 800 |

| Cleaning and repairs charges per month | 1,500 |

| Lubricants and supplies Rs 0.10 per km | |

| Sundry route expenses per month | 500 |

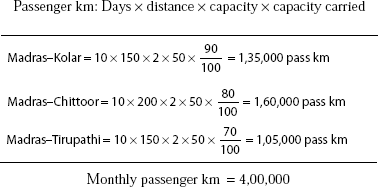

Solution: Statement showing operating cost (4,00,000 pass km)

Particulars | Per month Rs | Per pass km. Rs P. |

|---|---|---|

| Standing charges: | ||

| Permit fees | 1,200 | |

| Token tax | 425 | |

| Insurance | 750 | |

| Office expenses | 1,000 | |

| Driver's salary | 1,200 | |

| Conductor's salary | 800 | |

| Sundry route expenses | 500 | |

| Depreciation | 1,750 | |

| Interest on capital cost | 875 | |

| Total standing charges (A) | 8,500 | 0.02125 |

| Maintenance charges: | ||

| Tyres and tubes (10,000 × 0.4) | 4,000 | |

| Cleaning and repairs | 1,500 | |

| Lubricants and supplies (10,000 × 0.10) | 1,000 | |

| Total maintenance charges (B) | 6,500 | 0.01625 |

| Running charges: | ||

| 10,000 | 0.02500 | |

| Total operating cost (A + B + C) | 25,000 | 0.0625 |

| Add: Commission of conductor and driver (W.N.3) | 2,083 | 0.00500 |

| Add: Required profit (W.N.3) | 14,583 | 0.03500 |

| Net collections | 41,667 | 0.1042 |

| Add: Passenger tax at 1/6 on gross receipts (or) 1/5 on net collections | 8,333 | 0.0208 |

| Gross collections | 50,000 | 0.125 |

Bus charge from Madras to Kolar = 150 km × 0.12 = Rs 18

Bus charge from Madras to Chittoor = 200 × 0.12 = Rs 24

Bus charge from Madras to Tirupathi = 150 km × 0.12 = Rs 18

Working Note (1):

Working Note (2):

Running km: Days × distance

Madras–Kolar = 10 × 150 × 2 = 3,000

Madras–Chittoor = 10 × 200 × 2 = 4,000

Madras–Tirupathi = 10 × 150 × 2 = 3,000

Running km per month = 10,000

Working Note (3):

If net collections are = 100

∴ Driver and conductor's commission

5% on net collections or 5/60 on cost = ![]()

Required profit = 35% on net collections

or 35/60 on cost = ![]()

Problem 7. A transport company is running 4 buses between towns which are 50 km apart. The seating capacity of each bus is 40 passengers. The following particulars were obtained from their books for the month of April.

| Rs | |

|---|---|

| Wages of drivers, conductors and cleaners | 4,000 |

| Salaries to office staff | 2,000 |

| Diesel and other oils | 5,000 |

| Repairs and maintenance | 800 |

| Taxes, insurance, etc. | 1,600 |

| Depreciation | 2,600 |

| Interest and other charges | 2,000 |

Actual passengers carried were 75% of the capacity. All the four buses ran on all the days of the month. Each bus made one trip (up and down) per day. Calculate the cost per passenger km.

(B. Com., Madras)

[Ans: 3,60,000 passenger-km; per passenger-km: Re 0.05]

Illustration 22

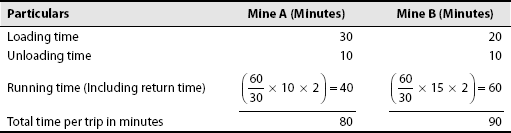

Iron ore is transported from two mines ‘A’ and ‘B’ and unloaded at plots in a railway station. ‘A’ is at a distance of 10 km and ‘B’ is at a distance of 15 km, from the rail head plots. A fleet of lorries of 6 tonne capacity is used for transport from mines. The lorries average a speed of 30 km per hour when running and consume 10 minutes to unload at the railhead. At mine ‘A’ loading time averages 30 minutes while at mine ‘B’ it is 20 minutes per load.

Driver's wages, depreciation, insurance and taxes are found to cost Rs 12 per hour operated. Fuel, oil, tyres, repairs and maintenance cost Rs 1.50 per km. Draw up a statement showing the cost per ton-km of carrying iron ore from each mine.

Solution: Statement showing operating cost

Particulars | Mine A (50 ton-km) | Mine B (75 ton-km) |

|---|---|---|

| Standing charges per trip | Rs 16 | Rs 18 |

| Running charges per trip | Rs 30 | Rs 45 |

| Total cost per trip | Rs 46 | Rs 63 |

| Cost per ton-km (total cost/ton-km) | 46/60 | 63/90 |

| Re 0.77 | Re 0.7 |

Working Note (1):

| Tonne kilometre: | Mine A | Mine B |

|---|---|---|

| Vehicle capacity | 6 tonnes | 6 tonnes |

| Distance to be travelled | 10 km | 15 km |

| ∴ Tonne kilometres | = 6 × 10 = 60 | 6 × 15 = 90 |

Working Note (2):

Schedule of trip times

Working Note (3):

Costs

| Particulars | Mine A (Minutes) | Mine B (Minutes) |

|---|---|---|

| Driver's wages, etc. per trip | ||

| Fuel, oil, etc. per trip | (1.50 × 20) = Rs 30 | (1.50 × 30) = Rs 45.00 |

Illustration 23

Delhi Transport Company has been given a route of 20 km long to run a bus. The bus costs the company a sum of Rs 70,000. It has been insured at 3% p.a. and the annual tax will amount to Rs 1,500. Garage rent is Rs 100 p.m. Actual repairs will be Rs 1,500 and the bus is likely to last for 5 years.

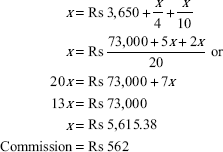

The driver's salary will be Rs 150 per month and the conductor's salary will be Rs 100 per month in addition to 10% of the takings as commission (to be shared by the driver and the conductor equally). Cost of stationery will be Rs 50 p.m. Manager-cum-accountant's salary is Rs 400 p.m.

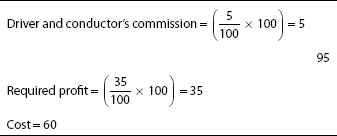

Petrol and oil will be Rs 25 per 100 km. The bus will make 3 round trips carrying on the average 40 passengers on each trip. Assuming 15% profit on takings, calculate the bus fare to be charged from each passenger. The bus will run on an average 25 days in a month.

Solution: Statement showing the fare to be charged from a passenger for one km

*In order to calculate the amount of commission payable to the driver and the conductor, total takings will have to be calculated.

Let total takings = x

Profit to be changed = ![]()

Total cost per month without including commission = Rs 3,100

Problem 8. Pallavan Transport Corporation runs the following fleet of buses in a particular area of Madras for 30 days in a month: 25 buses of 50 passenger capacity, On an average, each bus makes 10 trips a day covering a distance of 8 km in each trip with 75% of seats occupied. Generally, 10% of buses are kept away from the roads for repairs.

| Rs | |

|---|---|

| Monthly expenses: | |

| Rent | 2,500 |

| Road tax | 500 |

| Salary of chief operating manager | 1,500 |

| Salary of three assistant managers | 800 each |

| Salary of four supervisors | 400 each |

| Wages of 30 cleaners | 100 each |

| Wages of 25 drivers | 240 each |

| Wages of 25 conductors | 200 each |

| Consumable stores | 4,500 |

| Diesel | 34,000 |

| Lubricants | 5,500 |

| Replacement of tyres | 1,750 |

| Miscellaneous | 2,750 |

| Depreciation | 6,500 |

| Work shop expenses | 3,500 |

Calculate the cost per passenger km of operating the service.

(Madras, 1987)

[Ans: Cost per passenger km = Re 0.04; Total passenger km = 20,25,000 per month;

Total expenses per month = Rs 81,000]

Illustration 24

A Transport Company has been given a 20 km long route to run a bus. The bus costs Rs 70,000 and has been insured @ 6% p.a. while annual taxes amount to Rs 2,000. Garage rent is Rs 100 p.m. yearly repairs will be Rs 2,000 and the bus is likely to last for five years.

The driver's salary will be Rs 4,000 p.a. and that of conductor's Rs 2,000 p.a. in addition to 10% of the taking as commission (to be shared by the driver and the conductor equally). Cost of stationery will be Rs 600 p.a. Manager's salary is Rs 400 p.m. who also looks after accounts.

Petrol and oil will be Rs 25 per 100 km. The bus will make 3 round trips carrying on the average 40 passengers on each trip. Assuming 25% profit on taking, calculate the bus fare to be charged from the each passenger. The bus runs on an average 25 days in a month.

Solution: Statement showing the fare to be charged for a passenger km

| Annual exp. Rs | Monthly exp. Rs | |

|---|---|---|

| Fixed expenses: | ||

| Insurance | 4,200 | |

| Taxes | 2,000 | |

| Garage rent | 1,200 | |

| Driver's salary | 4,000 | |

| Conductor's salary | 2,000 | |

| Cost of stationery | 600 | |

| Manager's salary | 4,800 | |

| 18,800 | 1,566.67 | |

| Variable expenses: | ||

| Depreciation | 14,000 | |

| Repairs | 2,000 | 1,333.33 |

| Petrol | 7,50.00 | |

| Commission | 562 | |

| Total cost p.m. | 4,212 | |

| Profit 25% on takings | 1,404 | |

| Total takings | 5,616 |

Note: Calculation of commission:

Let total takings be ‘x’

Commission will be ![]()

Profit charged is ![]()

Total expenses without commission are Rs 3,650

Problem 9. Laxmi Transport Company is running 4 buses between two towns, which are 100 km apart. Seating capacity of each bus is 40 passengers.

The following particulars were obtained from their books for April:

| Rs | |

|---|---|

| Wages of drivers, conductors and cleaners | 4,800 |

| Salaries of office and supervisory staff | 2,000 |

| Diesel oil and other oil | 8,000 |

| Repairs and maintenance | 1,600 |

| Taxation, insurance, etc. | 3,200 |

| Depreciation | 5,200 |

| Interest and other charges | 4,000 |

| 28,800 |

Actual passengers carried were 75% of the seating capacity. All the four buses ran on all the days of the month. Each bus made one round trip per day. Find out the cost per passenger-km.

(M.Com., Bhopal)

[Ans: Re 0.04]

Illustration 25

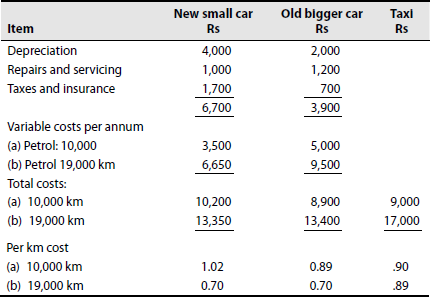

A practising Chartered Accountant now spends Re 0.90 per kilometre on taxi fares for his clients, 5 works. He is considering two other alternatives, the purposes of a new small can or an old bigger car. The estimated cost figures are:

Items | New small car Rs | Old bigger car Rs |

|---|---|---|

| Purchase price | 40,000 | 25,000 |

| Sale price of the car after five years | 20,000 | 15,000 |

| Repairs and servicing, per annum | 1,000 | 1,200 |

| Taxes and insurance per annum | 1,700 | 700 |

| Petrol price, per litre | 3.50 | 3.50 |

| Petrol consumption per litre | 10 km | 7 km |

He estimates that he does 10,000 km annually, which of the three alternatives will be cheaper? If his practice expends and he has to do 19,000 km per annum, what should be his decision? At how many km per annum, will the cost of the two cars break even and why? Ignore interest and income tax.

Solution: Statement showing comparative cost of alternative modes of conveyance

For his present practice, an old bigger car is the cheapest. But at his practice expends, a new small car will be the cheapest.

The difference in the variable costs of running the two cars is 15 paise. The difference of fixed costs is Rs 2,800. Hence, the break-even point between the two cars is calculated as:

At 18,667 km per annum, the cost of the two cars will break even as verified below.

| New car Rs | Old car Rs | |

|---|---|---|

| Fixed costs | 6,700 | 3,900 |

| Variable costs | 5,600 | 8,000 |

| 12,300 | 11,900 |

Illustration 26

XY & Company Limited owns a fleet of ten trucks each costing Rs 75,000. The company has employed one manager to whom it pays Rs 450 p.m. an accountant who gets Rs 250 p.m. and a peon who gets Rs 100 p.m. The company has got its trucks insured @ 2% per annum. The annual total tax is Rs 1,200 per truck. The other expenses are as follows:

| Driver's salary | Rs 300 per month |

| Cleaner's salary | Rs 100 per month |

| Mechanic's salary | Rs 400 per month |

| Repairs and maintenance | Rs 1,200 per year for one truck |

| 3 km per litre at Re 90 per litre | |

| The estimated life of the truck is five years. |

Other information:

| Distance travelled by each truck per day 200 km. | |

| Normal loading capacity | 100 quintals |

| Wastage in loading capacity | 10% |

| Percentage of truck laid up for repair | 5% |

| Effective days in a month | 25 |

Calculate (a) cost per quintal kilometre and (b) cost per kilometre of running a truck.

Solution:

Operating cost per quintal km and per km.

| Fixed expenses per month | Rs |

|---|---|

| Manager's salary | 450 |

| Accountant's salary | 250 |

| Peon's salary | 100 |

| Mechanic's salary | 400 |

| Total for 10 trucks per month for one truck | 1,200 |

| Rs | |

| Salary for one truck | 120.00 |

| Driver's salary per truck | 300.00 |

| Cleaner's salary | 100.00 |

| Repair and maintenance | 100.00 |

| Insurance | 125.00 |

| Annual tax | 100.00 |

| Depreciation | 1,250 |

| 2,095 |

Effective quintal km per month 4,750 for one truck

| Effective km per month 4,750 for one truck | per km paise | per quintal km paise |

|---|---|---|

| Fixed expenses | 0.44 | 0.049 |

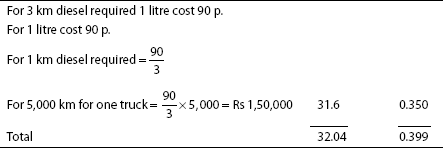

Note: Diesel consumption value has been taken for 5,000 km per truck because it has been assumed that during the time of repairs there will be consumption of diesel. Hence 5,000 km for truck has been calculated as follows:

Problem 10. A transport company supplies the following details in respect of a truck of five ton capacity:

| Cost of truck | Rs 1,20,000 |

| Estimated life | 10 years |

| Scrap value at the end of life | Rs 6,000 |

| Diesel, oil, grease | Rs 25 per trip each way |

| Repairs and maintenance | Rs 500 p.m. |

| Driver's wage | Rs 600 p.m. |

| Cleaner's wage | Rs 250 p.m. |

| Insurance | Rs 4,800 p.a. |

| Tax | Rs 2,400 |

| General supervision charges | Rs 6,000 p.a. |

The truck carries goods to and from the city covering a distance of 50 miles each way.

On outward trip freight is available to the extent of full capacity and on return 20% of capacity.

Assuming that the truck runs on an average 25 days a month, work out:

- Operating cost per tonne-mile

- Rate per tonne per trip that the company should charge if a profit of 50% on freightage is to be earned.

[Ans: Cost per tonne-mile: Re 0.63; Profit 50% of freightage: Re 0.63; That is freight per

tonne-mile: Re 1.26; Freight per trip: 250 ë Rs 1.26 + 50 ë Rs 1.26 = Rs 378]

Illustration 27

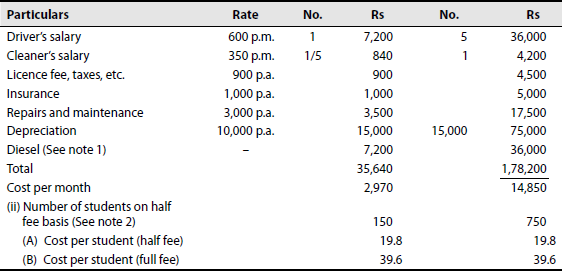

SMC is a public school having five buses each plying in different directions for the transport of its school students. In view of a larger number of students availing of the bus service the buses work two shifts daily both in the morning and in the afternoon. The buses are garaged in school. The workload of the students has been so arranged that in the morning the first trip picks up senior students and the second trip plying an hour later picks up the junior students. Similarly in the afternoon the first trip takes the junior students and an hour later the second trip takes the senior students home.

The distance travelled by each bus one way is 8 km. The school works 25 days in a month and remains closed for vacation in May, June and December, Bus fee however, is payable by the students for all 12 months in a year.

The details of expenses for a year as under

| Driver's salary | Rs 600 per month per driver |

| Cleaner's salary | Rs 350 per month |

| (Salary payable for all 12 months) | |

| (One cleaner employed for all the five buses) | |

| Licence fee, taxes, etc. | Rs 900 per bus per annum |

| Insurance | Rs 1,000 per bus per annum |

| Repairs and maintenance | Rs 3,500 per bus per annum |

| Purchase price of the bus | Rs 2,00,000 each |

| Life 12 years | |

| Scrap value | Rs 20,000 |

| Diesel cost | Rs 2.00 per litre |

| Each bus gives an average mileage of 4 km per litre of diesel | |

| Seating capacity of each bus is 50 students. | |

| The seating capacity is fully occupied during the whole year. |

Students picked up and dropped within a range up to 4 km of distance from the school are charged half fare. 50% of the students travelling in each trip in this category ignore interest. Since the charges are to be based on average cost, you are required to:

- Prepare a statement showing the expenses of operating a single bus and the fleet of five buses for a year.

- Work out the average cost per student per month in respect of

- Students coming from a distance of up to 4 km from the school and

- Students coming from a distance beyond 4 km from the school.

Solution: SMC Public School

Operating cost statement

Working Note:

- Calculation of diesel cost per bus:

Number of trips of 8 km each/day: 8 Distance travelled per day by a bus: 8 × 8 km/trip = 64 km Distance travelled during a month: 64 × 25 = 1,600 km Distance travelled p.a. (May, June: 1,600 × 9 = 14,400 km and December being vacation) Mileage: 4 km/litres Diesel required: 14,400/4 = 3,600 litres. Cost of diesel: 3,600 litres × Rs 2 per litre = Rs 7,200 p.a. per bus. - Calculation of number of students per bus:

Bus capacity 50 students Half fare 50%, i.e. 25 students Full fare 50%, i.e. 25 students Full fare students as equivalent to half fare students i.e. 50 students Total number of half fare students per trip 75 students Total number of half fare students in two trips 150 students On full fare basis number of students in two trips 75 students

Problem 11. From the following information, calculate total kilometres and total passenger kilometres:

| No. of buses: 5 |

| Days operated in the month: 25 |

| Trips made by each bus: 4 |

| Distance of route: 20 km, long (one side) |

| Capacity of bus: 50 passengers |

| Normal passenger travelling: 90% of capacity |

(B. Com.)

[Ans: Total km: 20,000; Total passenger-km: 9,00,000]

Illustration 28

A state transport corporation has been in serious financial and operational difficulty due to the high prices of spares, rising fuel cost and high wages.

The running operational expenses have been worked out for a single deck bus and are reproduced below:

Total fleet—500 buses single—deck

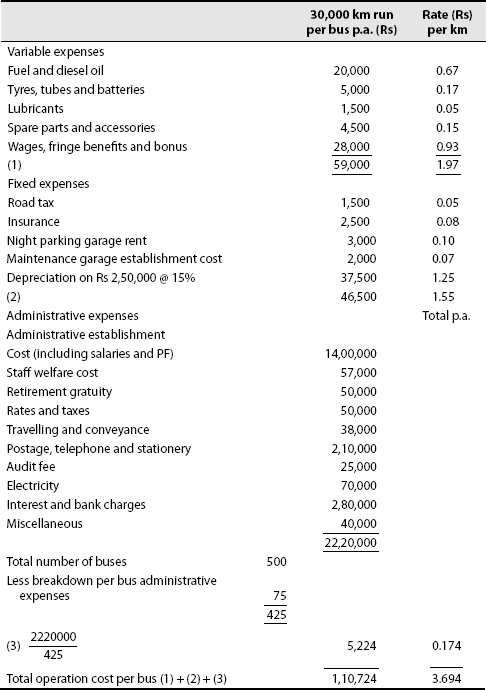

Average passengers occupying each trip—40

List of expenses for one-year period ending 31-12-197

| Variable expenses | Table for 30,000 km per bus per year (Rs) |

|---|---|

| (i) Fuel diesel oil | 20,000 |

| (ii) Tyres, tubes and batteries | 5,000 |

| (iii) Lubricants | 1,500 |

| (iv) Spare parts and accessories | 4,500 |

| (v) Wages, fringe benefits and bonus | 28,000 |

| Fixed expenses | |

| (i) Road tax | 1,500 |

| (ii) Insurance | 2,500 |

| (iii) Rent for night parking garage | 3,000 |

| (iv) Maintenance garage establishment cost | 2,000 |

| (v) Original cost per bus Depreciation @ 15% straight line basis | 2,50,000 |

| Administrative expenses | |

| (i) Administrative establishment cost (including salaries and PF) | 14,00,000 |

| (ii) Staff welfare cost | 57,000 |

| (iii) Retirement gratuity | 50,000 |

| (iv) Rates and taxes | 50,000 |

| (v) Travelling and conveyance | 38,000 |

| (vi) Postage, telephone and stationery | 2,10,000 |

| (vii) Audit fee | 25,000 |

| (viii) Electricity | 70,000 |

| (ix) Interest and bank charges | 2,80,000 |

| (x) Miscellaneous | 40,000 |

Administrative overhead is to be absorbed in the operating cost on the basis of available number of budgeted operable fleet (calculated on the basis of total fleet less 15% breakdown).

You are required to advise management regarding the fare structure on cost plus 10% basis for the following stages of travel, assuming that the fare is charged in proportion to kilometres travelled.

| Minimum fare on | |

| 1st stage of travel | 5 km (Rounded of |

| 2nd stage of travel | 10 km to nearest |

| 3rd stage of travel | 15 km paise) |

Suggest suitable statistical data to be collected on a weekly basis for management information for effective operational control.

Solution:

State transport corporation operational expenses for the period ending 31-12-1978

Average passenger per bus—40

| Cost per passenger per km | Rs 3.694/40 = 0.09235 paise |

| Cost per km | Rs 0.09235 |

| Margin | 0.009235 |

| Fare per km | 0.101 paise |

The fare structure will be as follows:

| Stage I | 5 km × 0.101 p | = 0.505 paise |

| Stage II | 10 km × 0.101 p | = 1.01 |

In order to have effective operational control, the following statistical data should be collected on a weekly basis for management.

- Number of buses run per-day and kilometres covered per day budgeted figure of 40 passengers per bus.

- Road breakdown

Problem 12. A transport company has been given a 10 km long route to run a bus. The bus costs Rs 50,000 and has been insured at 6% p.a., while annual taxes amount to Rs 2,000. Garage rent is Rs 100 p.m. Yearly repairs will be Rs 2,000 and the bus is likely to last for 5 years.

The driver's salary will be Rs 3,000 p.a. and that of conductor's Rs 1,800 p.a. in addition to 10% of the takings as commission (to be shared by the driver and the conductor equally). Cost of stationery will be Rs 600 p.a. Manager's salary is Rs 400 p.m. who also looks after accounts.

Petrol and oil will be Rs 25 per 100 km. The bus will make 5 round trips each day carrying on the average 40 passengers on each trip. Assuming 25% profit on takings, calculate the bus fare to be charged from each passenger. The bus runs on an average 25 days in a month.

(Madras, 1985)

[Ans: Bus fare to be charged: Re 0.046 or 4.6 paise per passenger km; Passenger km per month:

1,00,000; Total cost per month excluding commission: Rs 2,992; Petrol: Rs 625;

Commission: Rs 460; Profit: Rs 1,151; Total takings per month: Rs 4,603]

Illustration 29

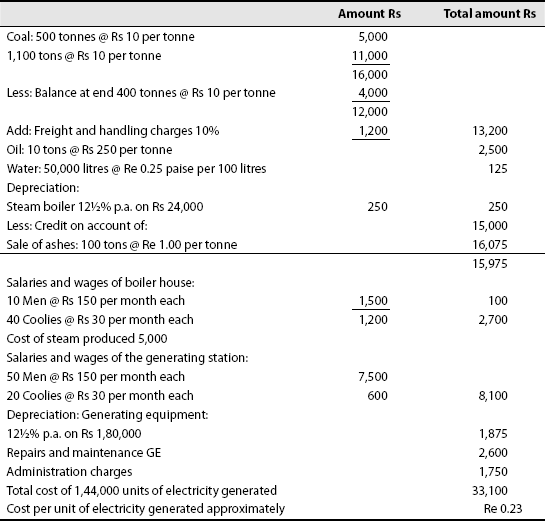

The new thermal power generating plant gives you the following data; find out in an appropriate cost sheet, cost of electricity per unit produced during the month of August 1978.

- Fuel:

Coal at the beginning of the month 500 tonnes.

Supply during the month 1,100 tonnes

Balance at the end of the month 400 tonnes.

Annual contract for supply of coal for colliery at Rs 10 per tonne.

Add: 10% to cover freight and handling charges.

- Oil: 10 tonnes at Rs 250 per tonne.

- Water: 50,000 litres. Pumping charges at 25 paise 100 per litre.

- Depreciation of steam boiler: Capital value Rs 24,000 and the rate of depreciation 12½% per annum.

- Salaries and wages of the boiler house:

10 men at Rs 150 per month each.

40 coolies at Rs 30 per month each.

- Recovery on account of sale of ashes: 100 tonnes at Re 1 per tonne.

- Salaries and wages of the generating station:

50 men at Rs 150 per month each.

20 coolies at Rs 30 per month each.

- Repairs and maintenance of the generating equipment: Rs 2,600.

Depreciation of generating equipment: Capital value:

Rs 1,80,000 and the rate of depreciation 12½% p.a.

- Share of administration charges: Rs 1,750

- Number of units generated: 1,46,000.

- Loss in the process 2,000 units generated.

Solution: Cost sheet (electricity generated

Illustration 30

Progressive Enterprises Limited runs a canteen for the benefit of its workmen and provides necessary subsidy to the canteen.

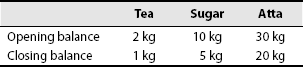

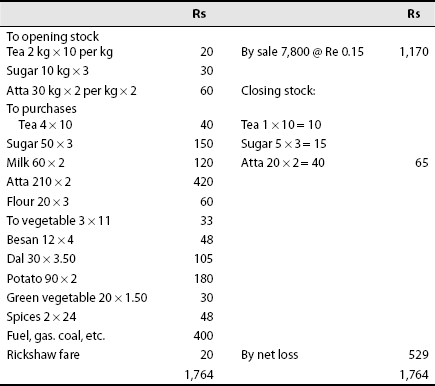

During month of August 1981, the following purchases were made:

Commodity | Quantity kg | Rate per kg Rs |

|---|---|---|

| 1. Tea | 4 | 10 |

| 2. Sugar | 50 | 3 |

| 3. Milk | 60 | 2 |

| 4. Atta | 210 | 2 |

| 5. Flour | 20 | 3 |

| 6. Vegetable ghee | 30 | 11 |

| 7. Besan | 12 | 4 |

| 8. Dal | 30 | 3.50 |

| 9. Potato | 90 | 2 |

| 10. Green vegetable | 20 | 1.50 |

| 11. Spices | 2 | 24 |

The other expenses for the month were : Rickshaw fare Rs 20 salary to cook (1) Rs 250 per month each. Wages to waiters (2) Rs 150 per month each. Supervisor's salary Rs 300 per month

Fuel, gas, coal, etc. Rs 400. Miscellaneous expenses crockery and glassware Rs 100. Depreciation of utensils and furniture Rs 50.

Sale of coupons 7,800 @ Re 0.15 per coupon.

Prepare trading and profit and loss account of the canteen for the month of August and find out the amount of subsidy paid by the company.

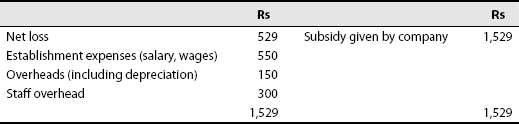

Solution: Trading and profit and loss account for the month of August 1981.

Canteen subsidy during the month of August 1981

Note: Cost sheet for the month of August 1981 to the above canteen can be prepared.

Illustration 31

The following cost data pertaining to the year 1964–1965 are collected from the books of ABC Power Company Limited

Coal consumed per kWh for the year is 1.5 lb and the cost of cool delivered to the power station is Rs 33.06 per metric ton. Depreciation rate chargeable is 4% per annum and interest on capital is to be taken at 1% higher than Reserve bank rate of 6% per annum.

Solution: Operating cost sheet of ABC Power Company Limited

Note: Cost of one tonne (2,205 1b) = Rs 33.06

Illustration 32

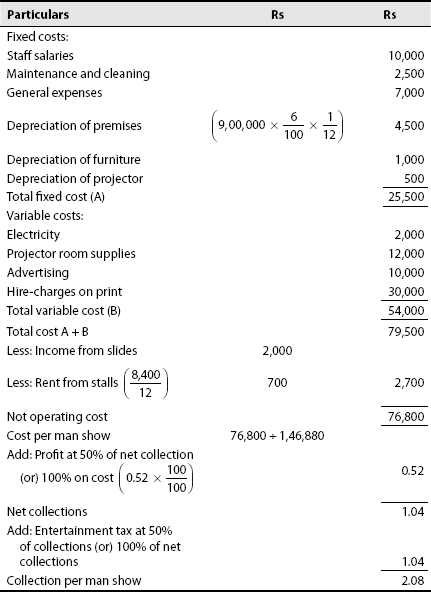

'Amitabh’ theatre in Bombay seeks your assistance in price determination. From the following data relating to April 1998, you are requested to

- Compute cost per ‘Man Show'

- Ascertain rates to be charged for each class of seating accommodation.

| Rs | |

|---|---|

| Staff salaries per month | 10,000 |

| Monthly maintenance and cleaning | 2,500 |

| Electricity charges per month | 2,000 |

| Projector room supplies per month | 12,000 |

| Advertising expenditure per month | 10,000 |

| Hire-charges of print per month | 30,000 |

| General expenses | 7,000 |

| Revenue from slides shown per month | 2,000 |

The theatre premises and building are valued at Rs 9,00,000. 6% on the capital cost per annum should be charged as depreciation. Rents collected from stalls in the theatre are Rs 8,400 per year. Depreciation of furniture & projector per month respectively are Rs 1,000 and Rs 500.

During April 1998, four shows with average attendance of 80% were run daily. Out of the seats occupied, 10% represent free passes and owner's connections.

Entertainment tax 50% of collections

Profit required 50% of net collections

The theatre contains 200 balcony, 300 first class and 500 second class seats. The weightage given is 3, 2, 1 respectively in terms of worth.

Solution: (1) Statement showing operating cost for April 1988

(2) Rates to be charged for each class of seating

Second class = 2.08 × 1 = Rs 2.08

First class = 2.08 × 2 = Rs 4.16

Balcony = 2.08 × 3 = Rs 6.24

Working Note (1):

Man Shows = Seats × weightage × days × shows × occupancy × paid occupancy

Second class = ![]()

First class = ![]()

Balcony = ![]()

Total Man Shows for the month = 1,46,880

Working Note (2):

Computation of profit and tax per man show

| If collections are | 100 |

| Less: Entertainment tax | 50 |

| Net collections | 50 |

| Less: Profit at 50% of net collections | 25 |

| Cost | 25 |

Note: Entertainment tax is on ticket price. Profit is on net collections, which is ticket price less tax.

Problem 13. The data given relates to ‘Vasanth Talkies’ a mini theatre, for the year ending 31-3-1976.

| Salaries: | Rs |

|---|---|

| One manager | 800 p.m. |

| 10 gate keepers | 200 p.m. each |

| two operators | 400 p.m. each |

| four clerks | 250 p.m. each |

| Electricity and oil | 11,655 |

| Carbon | 7,235 |

| Sundry expenses | 5,425 |

| Advertising | 34,710 |

| Office expenses | 18,000 |

| Hire for prints | 1,40,700 |

The theatre premises are valued at Rs 6,00,000 and the estimated life is 15 years. Projector costs Rs 3,20,000 on which 10% per annum depreciation is to be charged. Three shows are run daily throughout the year. The total capacity is 625 seats, which are divided into three classes as follows:

Janata circle 250 seats

Sanman circle 250 seats

Lords circle 125 seats

Ascertain cost per man show if

- 20% of the seats remain vacant

- Weightage for the classes is 1 : 2 : 3 respectively.

Determine the rates for each class if profit required is 30% on collections.

(Madras, 1983)

[Ans: Man shows 9,85,500 rate per man show = Re 0.50;

Rates: Janata: Re 0.50; Sanman: Re 1.00; Lords: Rs 1.50]

11.1.4 Hospital costing

The main purpose of hospital costing is to ascertain the cost of providing medical services. There are different departments in a hospital, which are generally formed on the basis of functions performed by them. The following are the main departments in a hospital:

- Out-Patient Department (OPD)

- Wards

- Medical Service Departments as diagnostic X-ray, radiotherapy, pathology, and so on

- General Service Department as boiler house, if any, power, heating, lighting, and so on: Catering, laundry, medical records, works maintenance, administration, and so on

- Miscellaneous service departments as transport, dispensary, cleaning, and so on

Cost of department 5 will have to be apportioned to the other departments on equitable basis. Cost of departments 1–4 above can be determined separately with reference to the units of cost, which are given below:

| OPD | Per out-patient attended |

| Wards | Per new out-patient attended or per case |

| Radiotherapy | Per course of treatment per day |

| Diagnostic X-ray | Per 100 units weighted points value. |

| Pathology | Per 100 requests |

| Boiler house | Per 1,000 lbs, steam raised |

| Power, heating and lighting, etc. | Per 1,000 cubic feet |

| Catering | Per person fed per week |

| Laundry | Per 100 articles laundered |

| Medical records | Per weighted unit |

| Works and maintenance | Per 1,000 cubic feet |

| Administration | Suitable percentage of turnover |

Cost Statement

The expenses of a hospital can be broadly divided into two categories: (1) capital expenditure and (2) Maintenance expenditure—This includes salaries and wages, provisions, staff uniforms and clothing, patients’ clothing, medical and surgical appliances and equipments, fuel, light and power, laundry and water.

11.1.5 Hotel costing

Hotel industry is a service industry and covers various activities as provision for food and accommodation and providing other comforts like recreation, business facilities, shopping areas for shopping facilities. In order to provide the service, hotel industry is required to incur various expenses. Expenses may be fixed or variable. Fixed expenses comprise staff salaries, repairs and renovations, interior decoration, laundry contract cost, sundries and depreciation on fixed assets, variable expenses include lighting charges, attendants salaries and power charges.

In order to calculate the room rent to be charged per person, notional profit is added in the total operating cost and divided by the number of rooms available. The numbers of rooms available are calculated after taking into consideration various categories of suite, various seasons and occupancy percentage.

Room rents may be different during season and off-season. Sometimes besides accommodation, food facilities are also provided. Then cost of meals, direct wages (restaurant and kitchen, housekeeping & general) and direct expenses (of house keeping and restaurant) are taken into consideration. Indirect expenses are apportioned on equitable basis among the different concerned departments.

11.1.6 Canteen costing

Hotel, motels, restaurants and cafeterias also employ operating costing. The aim obviously is to find out the total cost of running the business and then on that basis to fix the tariff. How much to charge per customer, per room, per bed, per meal, per dish, and so on can be determined only when these establishments maintain a complete set of record pertaining to each element of cost. After-all hotelling is a business and has to be conducted with minimum of cost and maximum of profit. The hotel manager has to ensure this. However, the point not to be missed is that most of the factory canteens are subsidised. The main heads of expenditure here are:

- Provision—vegetables, fruits, meat, flour, oil, milk, sugar, cream, tea, coffee and soft drinks

- Labour cooks, waitresses, kitchen assistants, supervision and porters

- Services—steam, gas, electricity, power and light water

- Consumable stores—cutlery, crockery, glassware, table linen, mops and washing-up clothes, dying up clothes, cleaning materials, dustpans and brushes

- Miscellaneous overhead—rent, rates, depreciation and insurance

- Credit—charges for meals, tea and other sales

Illustration 33

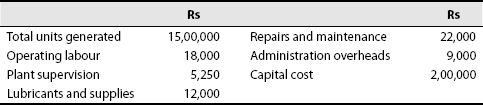

The following cost data is available from the books of ABC Power Company, Limited for 1995. Prepare cost sheet showing cost of power generation per unit of kWh.

| Rs | |

|---|---|

| Operating labour | 16,500 |

| Plant supervision | 7,000 |

| Lubricants and supplies | 10,500 |

| Repairs | 21,000 |

| Administration overheads | 10,000 |

| Capital cost | 2,00,000 |

Total units of power generated 15,00,000. Coal consumed per kWh for the year is 1.5 pounds and the cost of coal purchased is Rs 33.06 per metric tonne. Depreciation is at 4% per annum and the interest on capital is to be taken at 7% per annum.

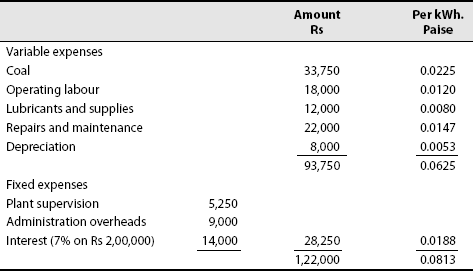

Solution: Operating cost sheet of ABC Power Company Limited for the year ended 1965

(15,00,000 kWh)

Particulars | Total Rs | Per kWh. Rs P. |

|---|---|---|

| Fixed charges: | ||

| Depreciation | 8,000 | |

| Administration overheads | 10,000 | |

| Interest on capital cost | 14,000 | |

| Plant supervision | 7,000 | |

| Total fixed charges (A) | 39,000 | 0.026 |

| Variable costs | ||

| Coal | 33,735 | 0.0225 |

| Operating labour | 16,500 | 0.0110 |

| Lubricants and supplies | 10,500 | 0.0070 |

| Repairs | 21,000 | 0.0140 |

| Total variable cost (B) | 81,735 | 0.0545 |

| Total cost (A + B) | 1,20,735 | 0.0805 |

Working Note:

| Coal consumed | |

|---|---|

| A metric tonne | = 2.205 pounds |

| Coal per kWh. | = 1.5 pounds |

| kWh produced | = 15,00,000 |

| Total coal required (15,00,000 × 1.5) | = 22,50,000 pounds |

| Metric tons of coal | = 1,020.4081 |

Illustration 34

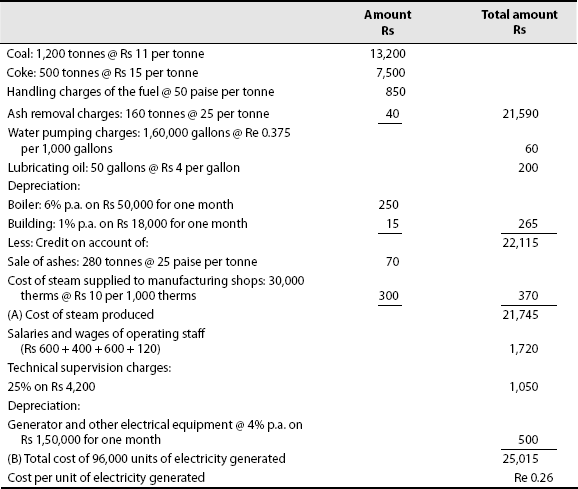

Find out the cost per unit of electricity generated in the powerhouse located in Eagle Engineering Works for the month of November 2001, with references to the following data extracted from the accounts books of works. The cost-sheet must be drawn up in the appropriation form:

Fuel:

| Coal 1,200 tons @ Rs 11 per tonne |

| Coke 500 ton @ Rs 15 per tonne |

| Handling charges of the fuel at 50 P. per tonne |

| Ash removal charges—160 tonnes @ 25 P. per tonne |

| Cost of water pumped from the river—160 thousand gallons |

| @ 37 ½ P. per thousand gallon |

| Lubricating oil—50 gallons @ Rs 4 per gallon |

Credit on account of

- Sale of ashes—280 tonnes @ 25 P. per tonne

- Cost of steam supplied to the manufacturing shops—30,000 therms @ Rs 10 per 1,000 therms

Salaries and wages of operating staff in the power house:

| Foreman | 1 @ Rs 600 per month |

| Assistant foremen | 2 @ Rs 200 per month |

| Mechanics | 4 @ Rs 150 per month |

| Coolie | 1 @ Rs 4 per day for 30 days |

Depreciation | Capital cost Rs | Rate of depreciation per annum |

|---|---|---|

| Boiler | 50,000 | 6% |

| Generator and other electrical equipment | 1,50,000 | 4% |

| Building | 18,000 | 1% |

| 25% share of monthly Total technical supervision charge | 4,200 | |

| Total gross units generated | 97,000 units | |

| Loss during the month due to leakage in course of generation due to defective equipments | 1,000 units |

Solution

11.2 ADVANCED-TYPE SOLVED PROBLEMS

Illustration 35

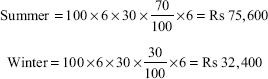

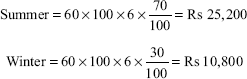

Fast roadways runs 10 buses between two suburban centres which are 25 km apart seating capacity at each bus in 30 passengers. The expenses for the month of November 1994 were as under:

| Rs | |

|---|---|

| Salaries of drivers and conductors | 30,000 |

| Salaries of mechanical staff | 3,000 |

| Diesel oil and lubricants | 20,000 |

| Taxes, insurance etc. | 2,600 |

| Repairs and maintenance | 4,000 |

| Depreciation | 16,000 |

Seating capacity utilized was 60%.

All the buses ran 25 days at the month.

Each bus made four round trips daily.

- Find out the cost per passenger-kilometre and the cost per round trip per passenger

- What would have been the cost per passenger, if the seating capacity utilization were to go up to 80%.

- What would have been the cost per round trip per passenger, if all the expenses (other than depreciation) were to go up by 20% at a seating capacity utilization of 80%?

Solution:

-

- Passenger km = 10 × 25 × 30 × 4 × 2 × 25 × 60/100

= 9,00,000

- Total cost = Rs 75,600

- Cost per passenger km = 75,600/9,00,000

= Rs 0.084

- Cost per round trip passenger = 50 × 0.084

= Rs 4.20

- Passenger km = 10 × 25 × 30 × 4 × 2 × 25 × 60/100

- Cost per round trip per passenger, if the seating capacity utilized were 80%

- Passenger km = 10 × 25 × 30 × 4 × 2 × 25 × 80/100

= Rs 12,00,000

- Total cost = Rs 75,600

- Cost per passenger km = 75,600/12,00,000

= Rs 0.063

- Cost per round trip passenger = 50 × 0.063

= Rs 3.15

- Passenger km = 10 × 25 × 30 × 4 × 2 × 25 × 80/100

- Cost per round trip passenger if all the expenses (other than depreciation) were to go up by 20% at seating capacity utilization of 80%

- Total cost = 16,000 + (71,520)

= Rs 87,520

- Passenger kilometre = Rs 12,00,000

- Cost per passenger kilometre = 0.0729

- Cost per round trip to passenger = 50 × 0.072

= 3.60

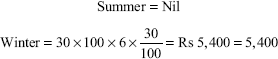

- Total cost = 16,000 + (71,520)

Illustration 36

Raja runs a fleet of taxis and the following information is available from the rewards maintained by Rim.

| 1. Number of taxis | 10 |

| 2. Cost of each taxi | Rs 20,000 |

| 3. Salary of manager | Rs 600 p.m. |

| 4. Salary of accountant | Rs 500 p.m. |

| 5. Salary of cleaner | Rs 200 p.m. |

| 6. Salary of mechanics | Rs 400 p.m. |

| 7. Garage rent | 600 p.m. |

| 8. Insurance premium | 5% p.a. |

| 9. Annual tax | Rs 600 per taxi |

| 10. Driver's salary | Rs 200 p.m. per taxi |

| 11. Annual repairs | Rs 1,000 per taxi |

Total life of a taxi is about 2,00,000 km. A taxi runs in all 3,000 km in a month at which 30% of it runs empty. Petrol consumption is one litre for 10 km @ Rs 1.80 per litre. Old and other sundries are Rs 5 per 100 km.

Calculate the cost of running a taxi per km.

Solution:

Fixed expenses:

| Amount p.m. Rs | Cost per km | |

|---|---|---|

| Salary of manager | 600 | |

| Salary of accountant | 500 | |

| Salary of cleaner | 200 | |

| Salary of mechanics | 400 | |

| Garage rent | 600 | |

| Insurance premium 5% on 2,00,000 | 833.33 | |

| Driver's salary 200 × 10 | 2,000 | |

| Tax 600 × 10/12 | 500 | |

| Total fixed expenses | 5,633.33 | |

| Effective kilometre 2,100 × 100 = 21,000 Fixed expenses per km | 0.268 |

Running expenses:

| Depreciation | 20,000/1,40,000 | 0.143 |

| Repairs | 0.040 | |

| Petrol | 0.257 | |

| Oil and other sundries | 0.071 | |

| Cost per km | 0.779 |

Illustration 37

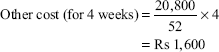

Raja automobiles distributes its good to a regional dealer using a single lorry. The dealer's premises are 40 km away by road. The lorry has a capacity of 10 tonnes and makes the journey twice a day fully loaded on the outward journeys and empty on return journeys. The following information is available for a four-weekly period during the year 1991.

| Petrol consumption | 8 km per km |

| Petrol cost | Rs 6.50 per litre |

| Oil | Rs 50 per week |

| Driver's wages | Rs 200 per week |

| Repairs | Rs 50 per week |

| Garage rent | Rs 75 per week |

| Cost of lorry | 80,000 km |

| Insurance | Rs 3,250 p.a. |

| Cost of tyres | Rs 3,125 |

| Life of tyres | 25,000 km |

Estimated sale value of Rs 25,000 lorry at end of its life. Vehicle licence cost Rs 650 p.a. Other overhead rate Rs 20,800 p.a. The lorry operates on a five-day week.

Required:

- A statement to show the total cost of operating the vehicle for a four-weekly period analysed into running costs and fixed costs.

- Calculate vehicle cost per km and per ton-km

Solution

| Running costs (Rs): | |

|---|---|

| Petrol cost | 2,600 |

| Oil expenses | 200 |

| Driver's wages | 800 |

| Repairs | 200 |

| Tyre cost | 400 |

| Depreciation | 8,000 |

| Total running cost (A) | Rs 12,200 |

| Fixed costs (Rs): | |

| Garage rent | 300 |

| Insurance | 250 |

| Licence cost | 50 |

| Other overhead cost | 1,600 |

| Total fixed cost (B) | 2,200 |

| Total cost (A) + (B) | Rs 14,400 |

(b) Cost per kilometre:

Cost per ton kilometre:

Working Notes:

Illustration 38

Raja has been promised a contract to run a tourist car on a 20 km long rate for the chief executive of a multinational firm. He buys a car costing Rs 1,50,000. The annual cost of insurance and taxes are Rs 4,500 and Rs 900, respectively. He has to pay Rs 12,500 p.m. for a garage where he keeps the car when it is not in use. The annual repair are estimated at Rs 4,000. The car is estimated to have a life at 10 years, at the end of which the scrap value is likely to be Rs 50,000.

He hires a driver who is to be paid Rs 300 p.m. plus 10% of the takings ads commission. Other incidental expenses are estimated at Rs 200 p.m. Petrol and oil will cost Rs 100 per 100 km. The car will make four round trips each day. Assuming that a profit of 15% on taking is desired and that the car will be on the road for 25 days on an average per month, what should be charge per round trip?

Solution

| Per annum (Rs) | Per month (Rs) | |

|---|---|---|

| Standing charges: | ||

| Insurance | 4,500 | |

| Taxes | 900 | |

| Garage rent (500 × 12) | 6,000 | |

| Driver's salary (300 × 12) | 3,600 | |

| Incidental expenses (200 × 12) | 2,400 | |

| 17,400 | 1,450 | |

| Running expenses: | ||