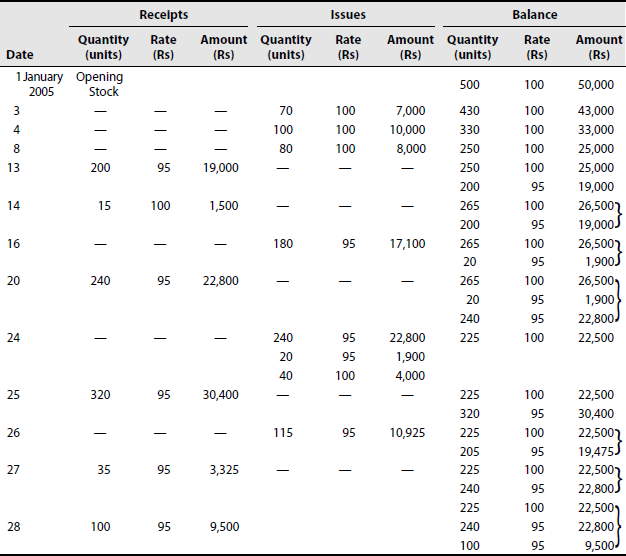

5

Pricing of Materials

CHAPTER OUTLINE

LEARNING OBJECTIVES

After reading this chapter, you will be able to understand:

Different methods of pricing of materials

The advantages and disadvantages of different methods of pricing

The various adjustments involved in different methods of pricing

5.1 INTRODUCTION

Materials are purchased at different times and at different prices. Now the question arises: At what price should materials be issued to production? Frequent changes in the prices of materials, and fluctuation in business cycle and frequency at which materials are issued to production make things complicated. However, in order to price the materials that are to be sent to production, some methods are adopted. The important methods for pricing materials are as follows

| I Actual cost methods | II Average cost methods | III Other methods |

|---|---|---|

| 1. First in first out (FIFO) | 1. Simple average | 1. Standard price |

| 2. Last in first out (LIFO) | 2. Weighted average | 2. Inflated price |

| 3. Base stock | 3. Periodic simple average | 3. Market price |

| 4. Periodic weighted average |

5.2 FIFO (FIRST IN FIRST OUT)

FIFO assumes that the first items placed in an inventory are the first ones sold. Thus, the inventory at the end of a year consists of the goods most recently placed in the inventory. The FIFO method follows the principle that materials used should carry the actual cost of the specific units used. The methods assume that materials are issued from the oldest supply.

According to the FIFO method, the goods that are entered first into the inventory are the ones that are disposed of first. This means that as newer goods start entering the inventory list, they are put at the end of the line. The items that have been in the inventory the longest are the ones that are sold immediately. This necessarily means that at the end of the financial year, the items that are left on the inventory list are those that have been introduced into the list most recently.

The formula used to calculate the inventory cost is as follows:

Inventory at the start of a year + net purchases − cost of goods sold = inventory at the end of the year

Under FIFO, the cost of goods sold is based upon the cost of material bought earliest in a given period, whereas the cost of inventory is based upon the cost of material bought later in the year. This results in the inventory being valued close to current replacement cost.

FIFO method is suitable under the following situations:

- The size and cost of units are large.

- Materials are identified as belonging to a particular purchased lot.

- Not more than two or three different receipts of materials are on a materials’ card at one time.

Under this method, materials received first are issued first. Materials are charged at actual cost in their chronological order. This method is suitable when prices fall because the price of materials issued is high but the price of material replaced is low. Some terms used in a store ledger account are as follows:

GRN—goods received note

MRN—materials returned note

MTN—materials transfer note

SRN—store requisition note

Advantages of FIFO:

- Simple to understand and easy to operate

- Closing stock reflects current price

- Suitable for slow-moving materials

- Suitable when prices fall

- Wastage and spoilage can be avoided

- Material cost charged to production represents the actual cost with which the cost of production should be charged.

Disadvantages of FIFO:

- Issue prices do not reflect current prices.

- When prices fluctuate, calculation becomes difficult.

- When materials are returned to the store, they are treated as new purchases.

- If the prices fluctuate frequently, this method may lead to clerical error.

- Since each issue of material to production is related to a specific purchase price, the costs charged to the same job are likely to show a variation from period to period.

- When prices rise, the real profits of a concern, being low, may be inadequate to meet the concern's demand to purchase raw materials at the ruling price.

5.3 LIFO (LAST IN FIRST OUT)

LIFO is an asset-management and valuation method that assumes assets produced or acquired last are the ones that are used, sold or disposed of first. LIFO assumes disposal of the newest inventory first. There is a possibility of inventory being sold for less than it was acquired for; then, the difference is considered a capital loss. If the inventory is sold for more than it was acquired for, the difference is considered a capital gain.

The LIFO method of costing materials issued is based on the assumption that material units issued should carry the cost of the most recent purchase, although the physical flow may actually be different. The method assumes that the most recent cost is most significant in matching cost with revenue in the income determination procedure.

Under LIFO the objective is to charge the cost of current purchases to work in process and to leave the oldest costs in the inventory. Under LIFO the cost of goods sold is based upon the cost of material bought towards the end of the period, resulting in costs that closely approximate current costs. The inventory, however, is valued on the basis of the cost of materials bought earlier in a year.

The advantages of the LIFO method are as follows:

- Materials consumed are priced in a systematic and realistic manner.

- It is argued that current acquisition costs are incurred for the purpose of meeting current production and sales requirements.

- The most recent costs are charged against current production and sales.

- Unrealized inventory gains and losses are minimized.

Disadvantages of the LIFO costing method are as follows:

- This is a ‘cost only’ method with no intention of lowering the cost.

- Record keeping requirements under this method are substantially greater than those of pricing methods.

- Inventories may be depleted due to inventories priced at older or perhaps the oldest prices.

- The Cost Accounting Standards Board (CASB) precludes the use of LIFO except when applied currently on a specific identification basis.

5.4 SIMPLE AVERAGE METHOD

In the simple average method, issue price of materials are fixed at the average unit price. Simple average is an average of price without considering the quantities involved. The average price is calculated by dividing the total of the rates of the materials in the stores by the number of rates of prices.

The advantages of simple average method are as follows:

- Simple average method is suitable when materials are received in uniform lot quantities.

- Simple average method is very easy to operate.

- Simple average method reduces clerical work.

The disadvantages of simple average method are as follows:

- If the quantity in each lot varies, the average price will be inaccurate.

- Costs are not fully recovered.

- Closing stock is not valued at the current assets.

5.5 WEIGHTED AVERAGE METHOD

This method uses the weighted average value for all issues. This is done by dividing the total cost of materials by their quantities. A new issue price is calculated each time a new material is received.

Under the weighted average method, both inventory and the cost of goods sold are based upon the average cost of all units currently in stock at the time of reporting.

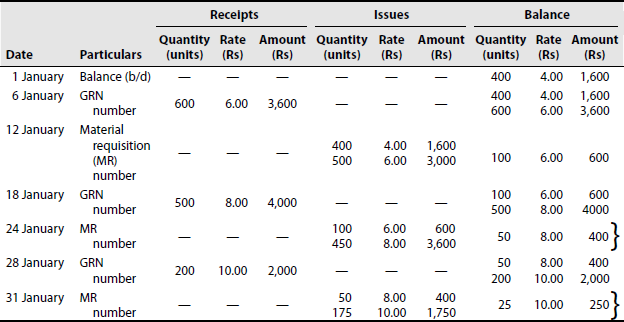

Illustration 1

Prepare a stores ledger on FIFO method:

| 2005 | |

|---|---|

| 1 January | Opening balance is 400 units at Rs 4 per unit |

| 6 | Purchased 600 units at Rs 6 per unit |

| 12 | Issued 900 units |

| 18 | Purchased 500 units at Rs 8 per unit |

| 24 | Issued 550 units |

| 28 | Purchased 200 units at Rs 10 per unit |

| 31 | Issued 225 units |

Solution: Stores ledger account (FIFO method):

Stock at the end is 25 units valued at Rs 250.

Problem 1. Prepare a stores ledger on FIFO method

| 2005 | |

|---|---|

| 1 January | Opening balance is 400 units at Rs 6 per unit |

| 6 | Purchased 600 units at Rs 8 per unit |

| 12 | Issued 900 units |

| 18 | Purchased 500 units at Rs 10 per unit |

| 24 | Issued 550 units |

| 28 | Purchased 200 units at Rs 12 per unit |

| 31 | Issued 225 units |

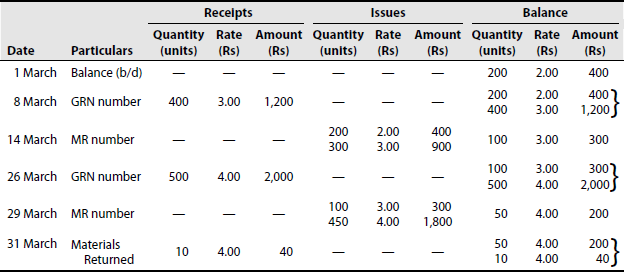

Illustration 2

Prepare a stores ledger on FIFO method:

| 2005 | |

|---|---|

| 1 March | Opening balance is 200 units at Rs 2 per unit |

| 8 | Purchased 400 units at Rs 3 per unit |

| 14 | Issued 500 units |

| 26 | Purchased 500 units at Rs 4 per unit |

| 29 | Issued 550 units |

| 31 | Received back 10 units issued on 29 March |

Solution: Stores ledger account (FIFO method):

Stock at the end is 60 units valued at Rs 240.

Problem 2. Prepare a stores ledger on FIFO method

| 2005 | |

|---|---|

| 1 March | Opening balance is 200 units at Rs 4 per unit |

| 8 | Purchased 400 units at Rs 6 per unit |

| 14 | Issued 500 units |

| 26 | Purchased 500 units at Rs 8 per unit |

| 29 | Issued 550 units |

| 31 | Received back 10 units issued on 29 March |

Illustration 3

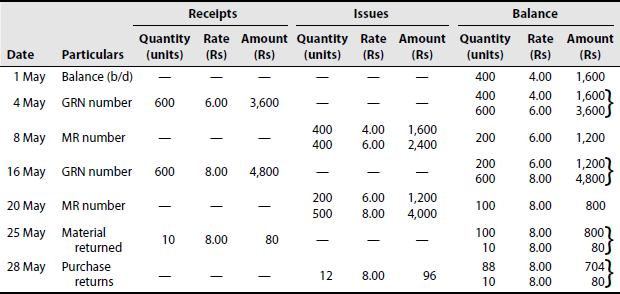

Prepare a stores ledger on FIFO method:

| 2005 | |

|---|---|

| 1 May | Opening stock is 400 units at Rs 4 per unit |

| 4 | Purchased 600 units at Rs 6 per unit |

| 8 | Issued 800 units |

| 16 | Purchased 600 units at Rs 8 per unit |

| 20 | Issued 700 units |

| 25 | Returned from factory 10 units issued on 20 May |

| 28 | Returned to vendors 12 units purchased on 16 May |

Solution: Stores ledger account (FIFO method):

Stock at the end is 98 units valued at Rs 784.

Problem 3. Prepare a stores ledger on FIFO method

| 2005 | |

|---|---|

| 1 May | Opening stock is 400 units at Rs 7 per unit |

| 4 | Purchased 600 units at Rs 9 per unit |

| 8 | Issued 800 units |

| 16 | Purchased 600 units at Rs 11 per unit |

| 20 | Issued 700 units |

| 25 | Returned from factory 10 units issued on 20 May |

| 28 | Returned to vendors 12 units purchased on 16 May |

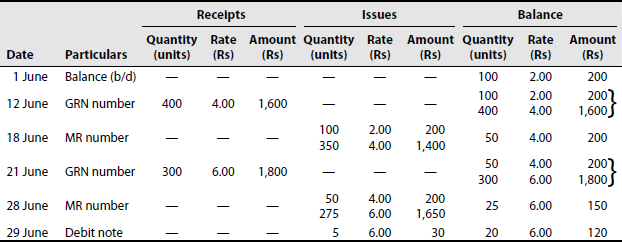

Illustration 4

Prepare a stores ledger on FIFO method:

| 2005 | |

|---|---|

| 1 June | Opening stock is 100 units at Rs 2 per unit |

| 12 | Purchased 400 units at Rs 4 per unit |

| 18 | Issued 450 units |

| 21 | Purchased 300 units at Rs 6 per unit |

| 28 | Issued 325 units |

| 29 | Shortage of 5 units |

Solution: Stores ledger account (FIFO method)

Stock at the end is 20 units valued at Rs 120.

Problem 4. Prepare a stores ledger under FIFO method

| 2005 | |

|---|---|

| 1 June | Opening stock is 100 units at Rs 5 per unit |

| 12 | Purchased 400 units at Rs 7 per unit |

| 18 | Issued 450 units |

| 21 | Purchased 300 units at Rs 9 per unit |

| 28 | Issued 325 units |

| 29 | Shortage of 5 units |

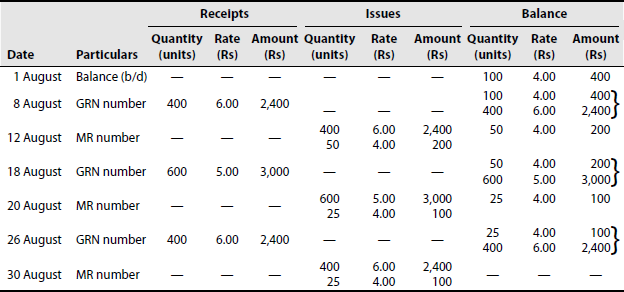

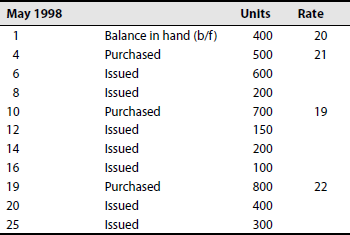

Illustration 5

Prepare a stores ledger under LIFO method:

| 2005 | |

|---|---|

| 1 August | Opening stock is 100 units at Rs 4 per unit |

| 8 | Purchased 400 units at Rs 6 per unit |

| 12 | Issued 450 units |

| 18 | Purchased 600 units at Rs 5 per unit |

| 20 | Issued 625 units |

| 26 | Purchased 400 units at Rs 6 per unit |

| 30 | Issued 425 units |

Solution: Stores ledger account (LIFO method)

Problem 5. Prepare a stores ledger under LIFO method

| 2005 | |

|---|---|

| 1 August | Opening stock is 100 units at Rs 8 per unit |

| 8 | Purchased 400 units at Rs 12 per unit |

| 12 | Issued 450 units |

| 18 | Purchased 600 units at Rs 10 per unit |

| 20 | Issued 625 units |

| 26 | Purchased 400 units at Rs 12 per unit |

| 30 | Issued 425 units |

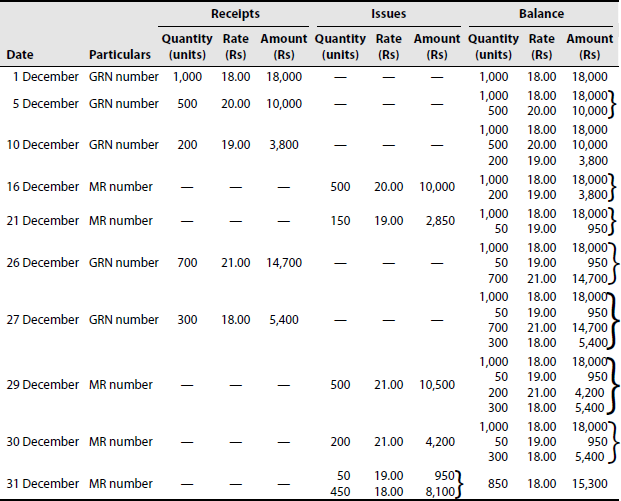

Illustration 6

Prepare a stores ledger under highest in first out (HIFO) method:

| 2005 | |

|---|---|

| 1 December | Purchased 1,000 units at Rs 18 per unit |

| 5 | Purchased 500 units at Rs 20 per unit |

| 10 | Purchased 200 units at Rs 19 per unit |

| 16 | Issued 500 units |

| 21 | Issued 150 units |

| 26 | Purchased 700 units at Rs 21 per unit |

| 27 | Purchased 300 units at Rs 18 per unit |

| 29 | Issued 500 units |

| 30 | Issued 200 units |

| 31 | Issued 500 units |

Solution: Stores ledger account (HIFO method)

Stock at the end is 850 units valued at Rs 15,300.

Problem 6. Prepare a stores ledger under HIFO method

| 2005 | |

|---|---|

| 1 December | Purchased 1,000 units at Rs 21 per unit |

| 5 | Purchased 500 units at Rs 23 per unit |

| 10 | Purchased 200 units at Rs 22 per unit |

| 16 | Issued 500 units |

| 21 | Issued 150 units |

| 26 | Purchased 700 units at Rs 24 per unit |

| 27 | Purchased 300 units at Rs 21 per unit |

| 29 | Issued 500 units |

| 30 | Issued 200 units |

| 31 | Issued 500 units |

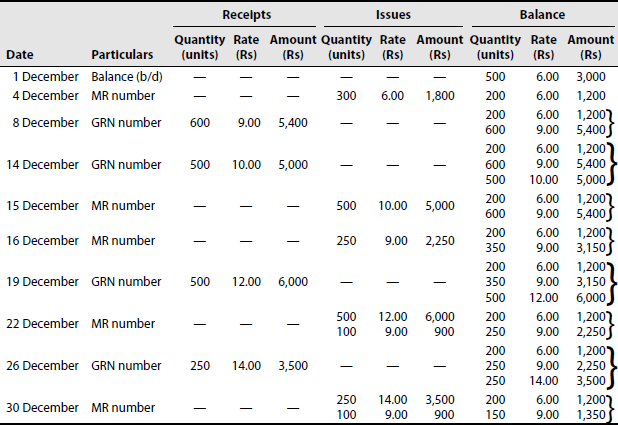

Illustration 7

Prepare a stores ledger under LIFO method:

| 2005 | |

|---|---|

| 1 December | Opening stock is 500 units at Rs 6 per unit |

| 4 | Issued 300 units |

| 8 | Purchased 600 units at Rs 9 per unit |

| 14 | Purchased 500 units at Rs 10 for a specific job to be issued on 15 December |

| 16 | Issued 250 units |

| 19 | Purchased 500 units at Rs 12 per unit |

| 22 | Issued 600 units |

| 26 | Purchased 250 units at Rs 14 per unit |

| 30 | Issued 350 units |

Solution: Stores ledger account (specific price method)

Stock at the end is 350 units valued at Rs 2,550.

Problem 7. Prepare a stores ledger under LIFO method

| 2005 | |

|---|---|

| 1 December | Opening stock is 500 units at Rs 10 per unit |

| 4 | Issued 300 units |

| 8 | Purchased 600 units at Rs 13 per unit |

| 14 | Purchased 500 units at Rs 14 for a specific job to be issued on 15 December |

| 16 | Issued 250 units |

| 19 | Purchased 500 units at Rs 16 per unit |

| 22 | Issued 600 units |

| 26 | Purchased 250 units at Rs 18 per unit |

| 30 | Issued 350 units |

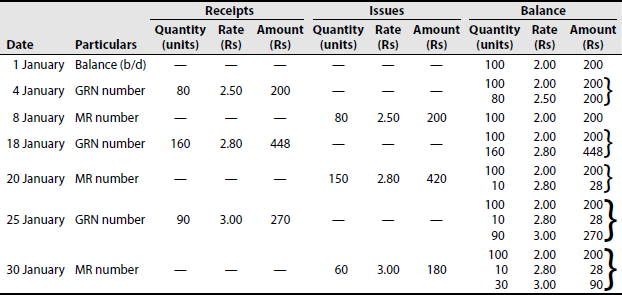

Illustration 8

Prepare a stores ledger under LIFO method, with a base stock of 100 units:

| 2005 | |

|---|---|

| 1 January | Opening stock is 100 units at Rs 2 per unit |

| 4 | Purchased 80 units at Rs 2.50 per unit |

| 8 | Issued 80 units |

| 18 | Purchased 160 units at Rs 2.80 per unit |

| 20 | Issued 150 units |

| 25 | Purchased 90 units at Rs 3 per unit |

| 30 | Issued 60 units |

Solution: Stores ledger account (base stock with LIFO):

Stock at the end is 140 units valued at Rs 318.

Problem 8. Prepare a stores ledger under FIFO method, with a base stock of 100 units

| 2005 | |

|---|---|

| 1 January | Opening stock is 100 units at Rs 4 per unit |

| 4 | Purchased 80 units at Rs 4.50 per unit |

| 8 | Issued 80 units |

| 18 | Purchased 160 units at Rs 4.80 per unit |

| 20 | Issued 150 units |

| 25 | Purchased 90 units at Rs 6 per unit |

| 30 | Issued 60 units |

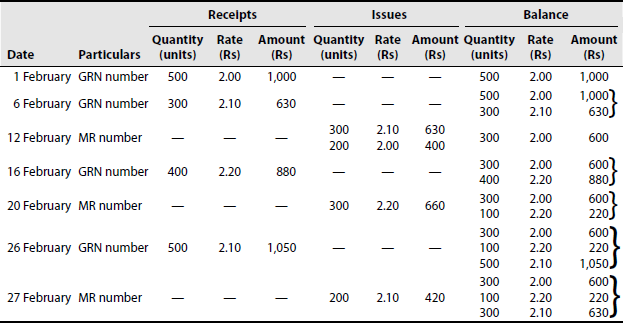

Illustration 9

Prepare a stores ledger under LIFO method and maintain 200 units as base stock:

| 2005 | |

|---|---|

| 1 February | Purchased 500 units at Rs 2 per unit |

| 6 | Purchased 300 units at Rs 2.10 per unit |

| 12 | Issued 500 units |

| 16 | Purchased 400 units at Rs 2.20 per unit |

| 20 | Issued 300 units |

| 26 | Purchased 500 units at Rs 2.10 per unit |

| 27 | Issued 200 units |

Solution: Stores ledger account (base stock with LIFO):

Stock at the end is 700 units valued at Rs 1,450.

Problem 9. Prepare a stores ledger under LIFO method and maintain 200 units as base stock

| 2005 | |

|---|---|

| 1 February | Purchased 500 units at Rs 5 per unit |

| 6 | Purchased 300 units at Rs 5.10 per unit |

| 12 | Issued 500 units |

| 16 | Purchased 400 units at Rs 5.20 per unit |

| 20 | Issued 300 units |

| 26 | Purchased 500 units at Rs 5.10 per unit |

| 27 | Issued 200 units |

Illustration 10

Prepare a stores ledger using simple average method:

| 1995 | ||

|---|---|---|

| 1 February | Opening balance | 50 units at Rs 3 per unit |

| 5 | Issued | 20 units |

| 7 | Purchased | 50 units at Rs 4 per unit |

| 9 | Issued | 35 units |

| 19 | Purchased | 75 units at Rs 5 per unit |

| 20 | Issued | 20 units |

| 21 | Received back | 10 units out of units issued on 9 February |

| 26 | Issued | 60 units |

Solution: Stores ledger account (simple average method):

Stock at the end is 50 units valued at Rs 237.30.

Problem 10. Prepare a stores ledger using simple average method

| 1995 | ||

|---|---|---|

| 1 February | Opening balance | 50 units at Rs 5 per unit |

| 5 | Issued | 20 units |

| 7 | Purchased | 50 units at Rs 6 per unit |

| 9 | Issued | 35 units |

| 19 | Purchased | 75 units at Rs 7 per unit |

| 20 | Issued | 20 units |

| 21 | Received back | 10 units out of units issued on 9 February |

| 26 | Issued | 60 units |

Illustration 11

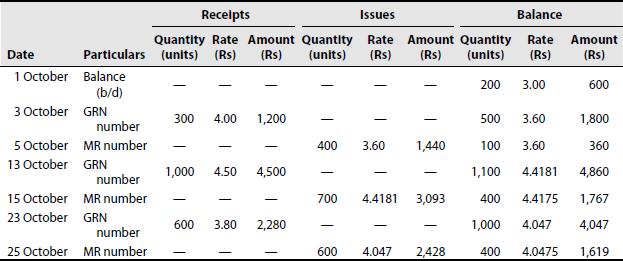

Prepare a stores ledger using weighted average method:

| Date | Particular unit | Rate |

|---|---|---|

| 1 October 1994, opening stock | 200 units | Rs 3.00 per unit |

| 3 October 1994, purchased | 300 units | Rs 4.00 per unit |

| 13 October 1994, purchased | 1000 units | Rs 4.50 per unit |

| 23 October 1994, purchased | 600 units | Rs 3.80 per unit |

Issues:

| 5 October 1994, issued | 400 units |

| 15 October 1994, issued | 700 units |

| 25 October 1994, issued | 600 units |

Solution: Stores ledger account (weighted average method):

Stock at the end is 400 units valued at Rs 1,619.

Problem 11. Prepare a stores ledger using weighted average method

| Date | Particular unit | Rate |

|---|---|---|

| 1 October 1994, opening stock | 200 units | Rs 7.00 per unit |

| 3 October 1994, purchased | 300 units | Rs 8.00 per unit |

| 13 October 1994, purchased | 1,000 units | Rs 8.50 per unit |

| 23 October 1994, purchased | 600 units | Rs 7.80 per unit |

Issues:

| 5 October 1994, issued | 400 units |

| 15 October 1994, issued | 700 units |

| 25 October 1994, issued | 600 units |

Illustration 12

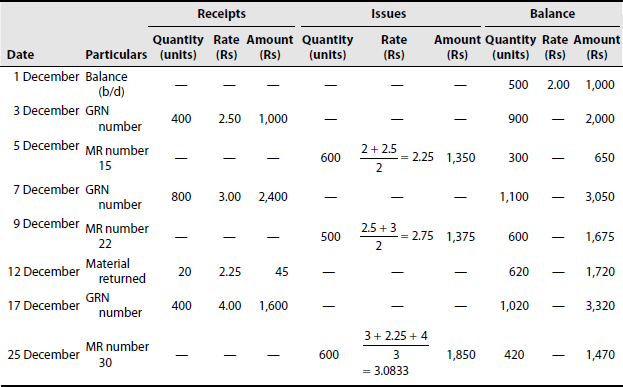

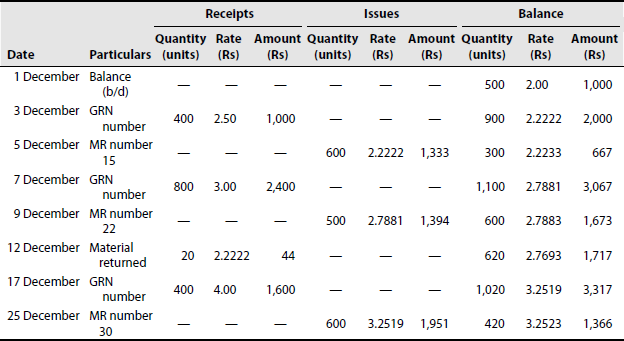

Prepare stores ledger using (a) simple average and (b) weighted average methods:

| 1994 | |

|---|---|

| 1 December | Opening stock is 500 units at Rs 2 each |

| 3 | Purchased 400 units at Rs 2.50 each |

| 5 | Issued 600 units, vide MR number 15 |

| 7 | Purchased 800 units at Rs 3.00 each |

| 9 | Issued 500 units, vide MR number 22 |

| 12 | Returned from issue on 5 December, 20 units |

| 17 | Purchased 400 units at Rs 4.00 each |

| 25 | Issued 600 units, vide MR number 30 |

Solution:

- Stores ledger account (simple average method):

Stock at the end is 420 units valued at Rs 1,470.

- Stores ledger account (weighted average method):

Stock at the end is 420 units valued at Rs 1,366.

Problem 12. Prepare stores ledger using simple average and weighted average methods

| 1994 | |

|---|---|

| 1 December | Opening stock is 500 units at Rs 5 each |

| 3 | Purchased 400 units at Rs 5.50 each |

| 5 | Issued 600 units, vide MR number 15 |

| 7 | Purchased 800 units at Rs 6.00 each |

| 9 | Issued 500 units, vide MR number 22 |

| 12 | Returned 20 units from issue on 5 December |

| 17 | Purchased 400 units at Rs 7.00 each |

| 25 | Issued 600 units, vide MR number 30 |

Illustration 13

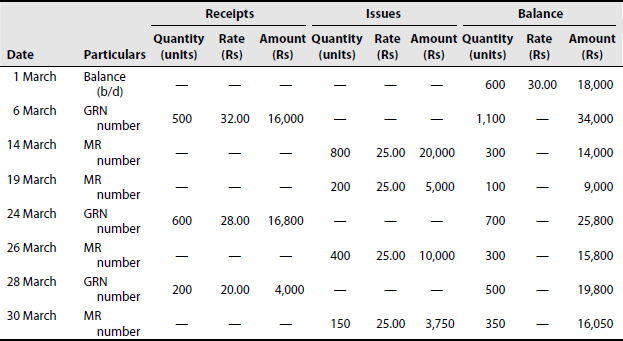

Prepare stores ledger using standard price method, with standard price Rs 25:

| 2005 | |

|---|---|

| 1 March | Opening balance is 600 units at Rs 30 per unit |

| 6 | Purchased 500 units at Rs 32 per unit |

| 14 | Issued 800 units |

| 19 | Issued 200 units |

| 24 | Purchased 600 units at Rs 28 per unit |

| 26 | Issued 400 units |

| 28 | Purchased 200 units at Rs 20 per unit |

| 30 | Issued 150 units |

Solution: Stores ledger account (standard price)

Material price variancelosing balance = (closing balance in×standard price) – closing balance in value

= (350 × 25) – 16,050

= 8,750 – 16,050

= 7,300 (adverse)

Problem 13. Prepare stores ledger using standard price method, with standard price Rs 25

| 2005 | |

|---|---|

| 1 March | Opening balance is 600 units at Rs 50 per unit |

| 6 | Purchased 500 units at Rs 52 per unit |

| 14 | Issued 800 units |

| 19 | Issued 200 units |

| 24 | Purchased 600 units at Rs 48 per unit |

| 26 | Issued 400 units |

| 28 | Purchased 200 units at Rs 40 per unit |

| 30 | Issued 150 units |

Illustration 14

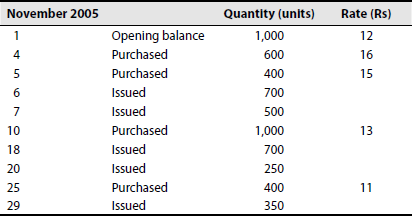

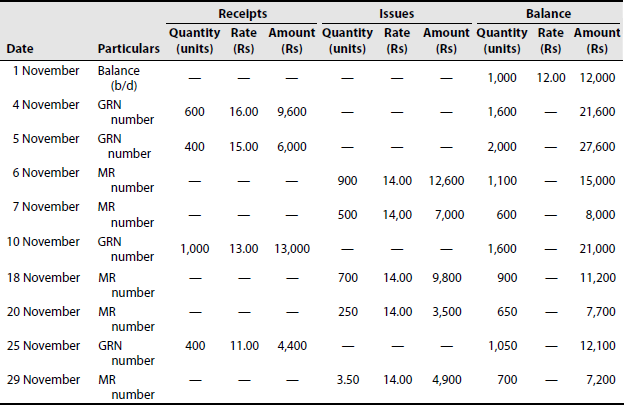

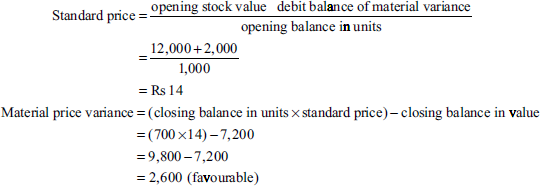

Prepare the stores ledger account showing how issues and closing stock balance are recorded under the standard price method. The debit balance of material variance was 2,000 on 1 November 2005. The following are the purchases and issues made during November 2005:

Calculate the material price variance at the end of November 2005.

Solution: Stores ledger account (standard price method):

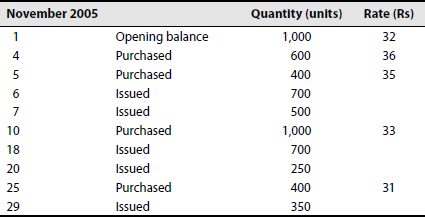

Problem 14. Prepare the stores ledger account showing how issues and closing stock balance are recorded under the standard price method. The debit balance of material variance was 2,000 on 1 November 2005. The following are the purchases and issues made during November 2005:

Calculate the material price variance at the end of November 2005.

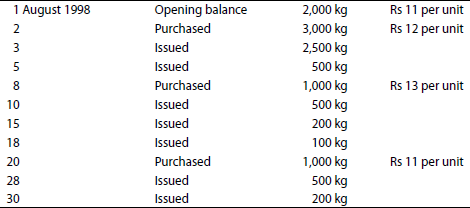

Illustration 15

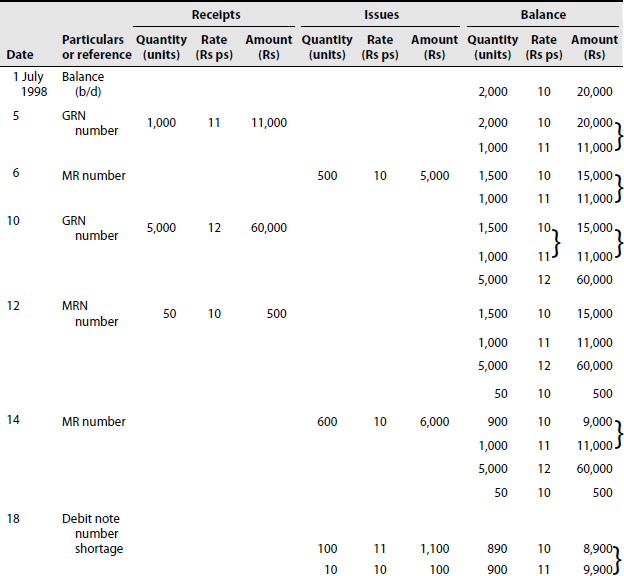

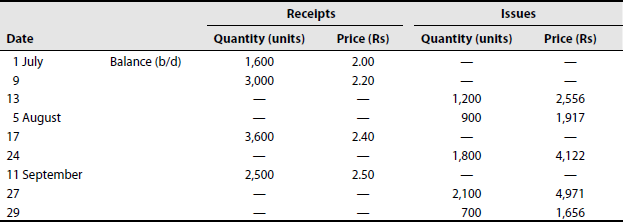

Draw a stores ledger card recording the following transactions under (a) FIFO method and (b) LIFO method:

| 1998 | |

|---|---|

| 1 July | Opening stock is 2,000 units at Rs 10 each |

| 5 | Received 1,000 units at Rs 11 each |

| 6 | Issued 500 units |

| 10 | Received 5,000 units at Rs 12 each |

| 12 | Received back 50 units out of the issue made on 6 July |

| 14 | Issued 600 units |

| 18 | Returned to supplier 100 units out of the goods received on 5 July |

| 19 | Received back 100 units out of the issue made on 14 July |

| 20 | Issued 150 units |

| 25 | Received 500 units at Rs 14 each |

| 28 | Issued 300 units |

The stock verification report reveals that there was a shortage of 10 units on 18 July and another shortage of 15 units on 26 July.

Solution:

Closing stock = 6,975 units, valued at Rs 82,650

(425 × 10 + 900 × 11 + 5,000 × 12 + 50 × 10 + 100 × 10 + 500 × 14)

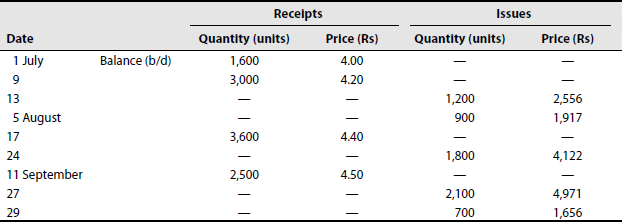

Problem 15. Draw a stores ledger card recording the following transactions under (a) FIFO method and (b) LIFO method

| 1998 | |

|---|---|

| 1 July | Opening stock is 2,000 units at Rs 20 each |

| 5 | Received 1,000 units at Rs 21 each |

| 6 | Issued 500 units |

| 10 | Received 5,000 units at Rs 22 each |

| 12 | Received back 50 units out of the issue made on 6 July |

| 14 | Issued 600 units |

| 18 | Returned to supplier 100 units out of the goods received on 5 July |

| 19 | Received back 100 units out of the issue made on 14 July |

| 20 | Issued 150 units |

| 25 | Received 500 units at Rs 24 each |

| 28 | Issued 300 units |

The stock verification report reveals that there was a shortage of 10 units on 18 July and another shortage of 15 units on 26 July.

Illustration 16

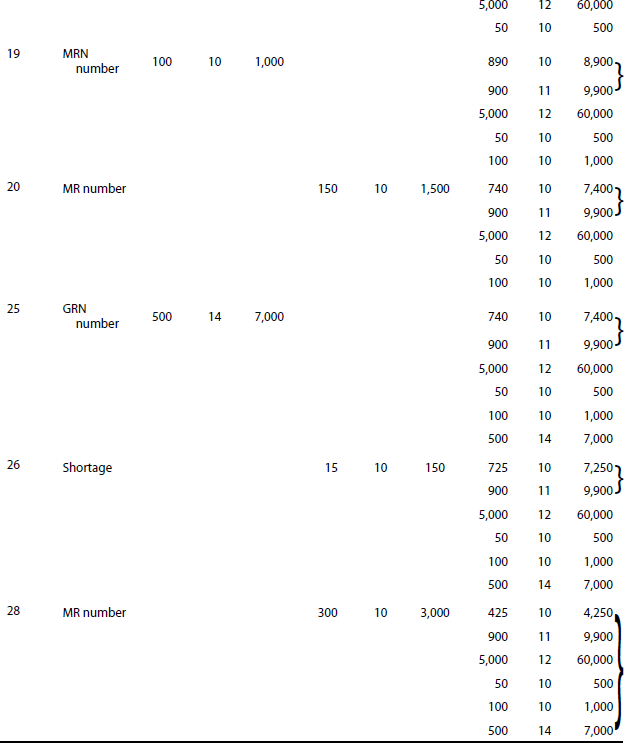

From the following particulars, write the stores ledger card:

| 1998 | ||

|---|---|---|

| 1 January | Opening stock | 1,000 units at Rs 26.00 each |

| 5 | Purchased | 500 units at Rs 24.50 each |

| 7 | Issued | 750 units |

| 10 | Purchased | 1,500 units at Rs 24.00 each |

| 12 | Issued | 1,100 units |

| 15 | Purchased | 1,000 units at Rs 25.00 each |

| 17 | Issued | 500 units |

| 18 | Issued | 300 units |

| 25 | Purchased | 1,500 units at Rs 26 each |

| 29 | Issued | 1,500 units |

Adopt the FIFO method of issue and ascertain the value of closing stock.

Solution: Stores ledger account by FIFO method:

Closing stock is 1,350 units at Rs 26 each = Rs 35,100.

Problem 16. From the following particulars, write the stores ledger card

| 1998 | ||

|---|---|---|

| 1 January | Opening stock | 1,000 units at Rs 36.00 each |

| 5 | Purchased | 500 units at Rs 34.50 each |

| 7 | Issued | 750 units |

| 10 | Purchased | 1,500 units at Rs 34.00 each |

| 12 | Issued | 1,100 units |

| 15 | Purchased | 1,000 units at Rs 35.00 each |

| 17 | Issued | 500 units |

| 18 | Issued | 300 units |

| 25 | Purchased | 1,500 units at Rs 36.00 each |

| 29 | Issued | 1,500 units |

Adopt the FIFO method of issue and ascertain the value of closing stock.

Illustration 17

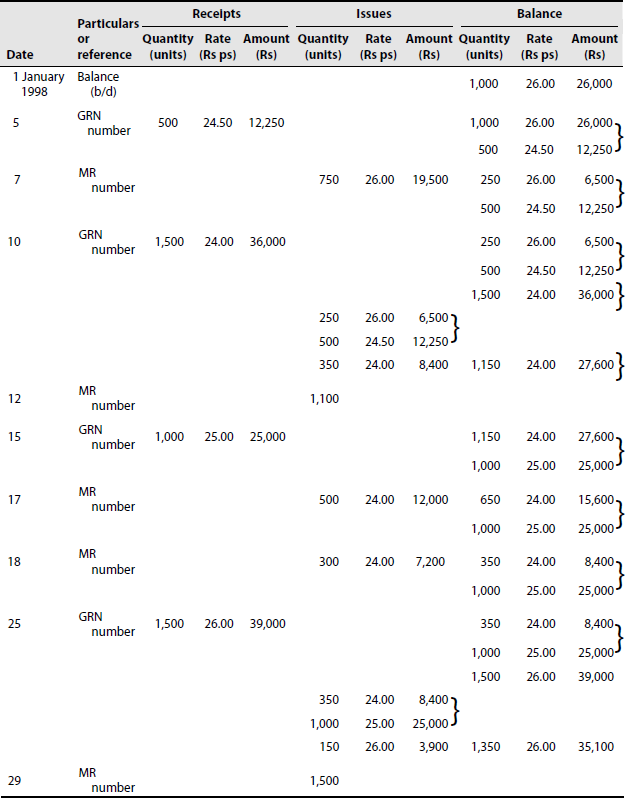

From the following particulars, prepare the stores ledger account showing the pricing of materials issue by adopting the FIFO method, with a base stock of 400 units out of the opening stock

| 1990 | |

|---|---|

| 1 December | Opening stock 1,000 units at Rs 2.00 each |

| 3 | Purchased 800 units at Rs 2.10 |

| 5 | Issued 800 units |

| 12 | Purchased 1,600 units at Rs 2.10 each |

| 17 | Issued 1,500 units |

| 20 | Purchased 900 units at Rs 2.50 each |

| 25 | Issued 600 units |

Solution: Storage ledger account (LIFO method):

Closing stock is 1,400 units valued at Rs 2,960 (1,000 × 2 + 100 × 2.10 + 300 × 2.50).

Problem 17. From the following particulars, prepare the stores ledger account showing the pricing of materials issue by adopting the FIFO method, with a base stock of 400 units out of the opening stock

| 1990 | |

|---|---|

| 1 December | Opening stock is 1,000 units at Rs 5.00 each |

| 3 | Purchased 800 units at Rs 5.10 |

| 5 | Issued 800 units |

| 12 | Purchased 1,600 units at Rs 5.10 each |

| 17 | Issued 1,500 units |

| 20 | Purchased 900 units at Rs 5.50 each |

| 25 | Issued 600 units |

Illustration 18

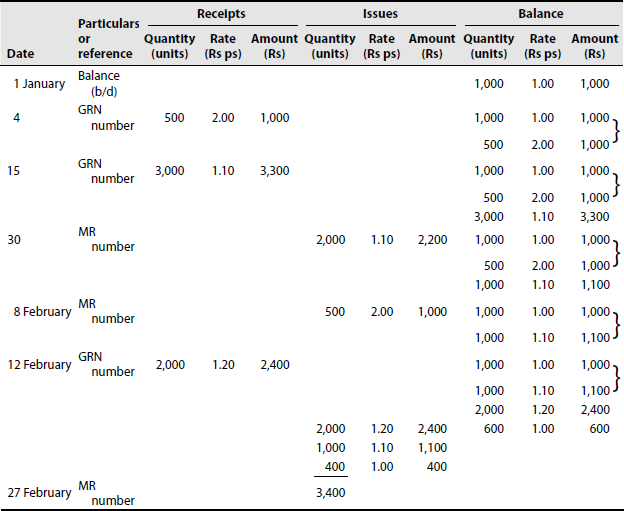

Using the following information, write the stores ledger account showing quantities and value of receipts, issues and balance in hand under the LIFO method of pricing stores issues:

| 1 January | Balance in hand is 1,000 units at Re 1 each |

| 4 January | Received 500 units to be issued on request from department X, at the rate of Rs 2 each |

| 15 January | Received 3,000 units costing Rs 3,300 |

| 30 January | Issued 2,000 units |

| 8 February | Issued 500 units (received on 4 January) to department X |

| 12 February | Received 2,000 units costing Rs 2,400 |

| 27 February | Issued 3,400 units |

Solution: Stores ledger account (specific price with LIFO method):

Closing stock = 600 units valued at Rs 600 (600 × 1)

Problem 18. Using the following information, draft the stores ledger account showing quantities and value of receipts, issues and balance in hand under the LIFO method of pricing stores issues

| 1 January | Balance in hand is 1,000 units at Re 1 each |

| 4 January | Received 500 units to be issued on request from department X, at the rate of Rs 2 each |

| 15 January | Received 3,000 units costing Rs 3,300 |

| 30 January | Issued 2,000 units |

| 8 February | Issued 500 units (received on 4 January) to department X |

| 12 February | Received 2,000 units costing Rs 2,400 |

| 27 February | Issued 3,400 units |

Illustration 19

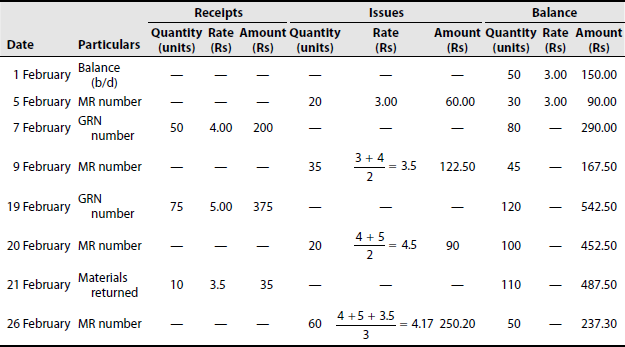

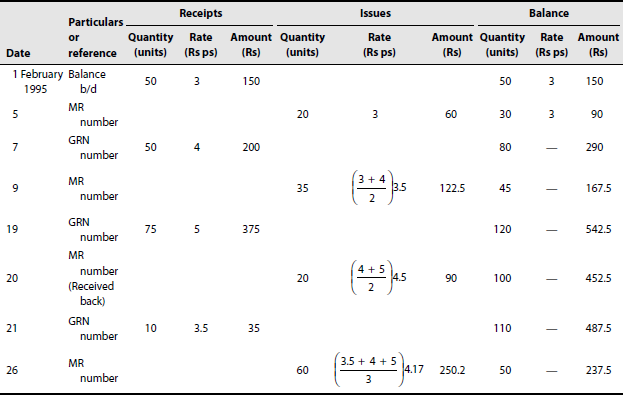

Prepare a stores ledger account and enter the following transactions adopting the simple average method of pricing issues:

| 1995 | ||

|---|---|---|

| 1 February | Opening balance | 50 units at Rs 3 per unit |

| 5 | Issued | 20 units |

| 7 | Purchased | 50 units at Rs 4 per unit |

| 9 | Issued | 35 units |

| 19 | Purchased | 75 units at Rs 5 per unit |

| 20 | Issued | 20 units |

| 21 | Received back | 10 units out of the units issued on 9 February |

| 26 | Issued | 60 units |

Solution: Stores ledger account (simple average method):

Closing stock = 50 units valued at Rs 237.50.

Problem 19. Prepare a stores ledger account and enter the following transactions adopting the simple average method of pricing issues

| 1995 | ||

|---|---|---|

| 1 February | Opening balance | 50 units at Rs 7 per unit |

| 5 | Issued | 20 units |

| 7 | Purchased | 50 units at Rs 8 per unit |

| 9 | Issued | 35 units |

| 19 | Purchased | 75 units at Rs 9 per unit |

| 20 | Issued | 20 units |

| 21 | Received back | 10 units out of the units issued on 9 February |

| 26 | Issued | 60 units |

Illustration 20

The store ledger account for material X in a manufacturing concern reveals the following data for the quarter ending on 30 September:

Physical verification on 30 September revealed an actual stock of 3,800 units. You are required to (a) indicate the method of pricing employed in the aforementioned account. (b) Prepare store ledger under weighted average method.

Solution:

- On observation of the pricing of issues in the problem, it is clear that weighted average rate method is adopted.

- Stores ledger account (weighted average method):

Problem 20. The store ledger account for material X in a manufacturing concern reveals the following data for the quarter ending on September 30:

Physical verification on 30 September revealed an actual stock of 3,800 units. You are required to (a) indicate the method of pricing employed in the aforementioned account.

5.6 ADVANCED-TYPE SOLVED PROBLEMS

- A.T. Ltd. furnishes the following store transactions for September 1992

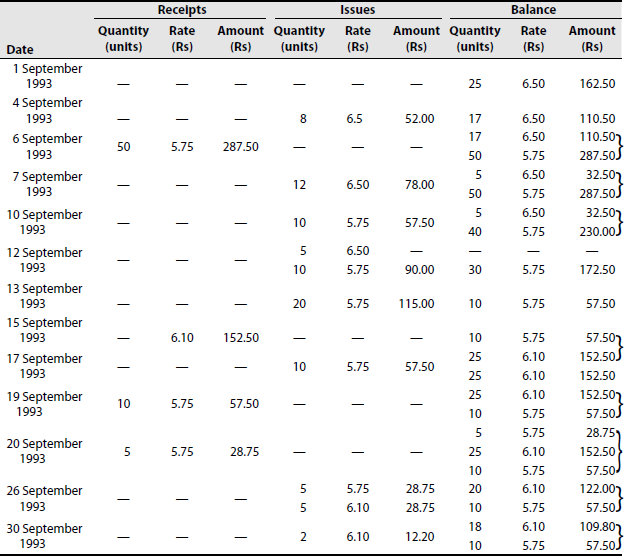

1 September 1993 Opening balance 25 units at Rs 162.50 4 September 1993 Issue register number 85 8 units 6 September 1993 Receipts from B&W GRN number 26 50 units at Rs 5.75 7 September 1993 Issue register number 97 12 units 10 September 1993 Returns to B&W 10 units 12 September 1993 Issues 15 units 13 September 1993 Issues 20 units 15 September 1993 Receipts from M&W 25 units at Rs 6.10 17 September 1993 Issues 10 units 19 September 1993 Received replacement from B&W 10 units 20 September 1993 Return from department material at M&W 5 units 22 September 1993 Transfer from job 182 to job 187 in the department MTR 6 5 units 26 September 1993 Issues 10 units 29 September 1993 Transfer from department A to department B 5 units 30 September 1993 Shortage in stocktaking 2 units Write the priced stores ledger on FIFO method and discuss how you would treat the shortage in stocktaking

Working Notes:

- The material received as replacement from vendor has been treated as fresh supply.

- In the absence of information, the price of the material received from within on 20 September 1993 has been taken as the price of the earlier issue made on 17 September 1992. In FIFO, physical flow of material is irrelevant for pricing the issues.

- The issue of material on 26 September 1993 has been made first out of the material received from within.

- The entries for transfer from one job and department to another on 22 September 2000 are book entries for adjusting the loss of respective jobs and as such they have not been shown in the stores ledger account.

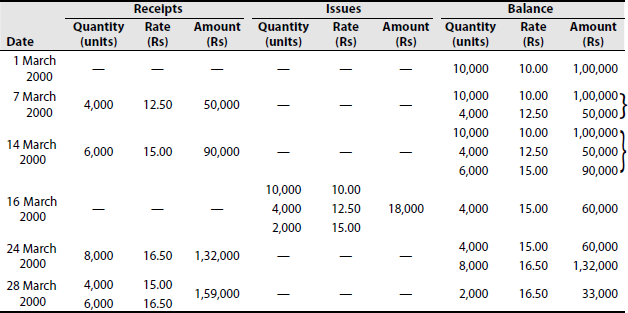

- In the beginning of March 2000, Ram and company had in stock 10,000 brushes valued at Rs 10 each. Further purchases were made during the month as follows:

7 March 4,000 brushes at Rs 12.50 14 March 6,000 brushes at Rs 15.00 24 March 8,000 brushes at Rs 16.50 Issues to the shop were as follows:

16 March 16,000 brushes 28 March 10,000 brushes You are required to prepare a stores ledger card for the month of March 2000 on the assumption that materials were issued on the FIFO principle.

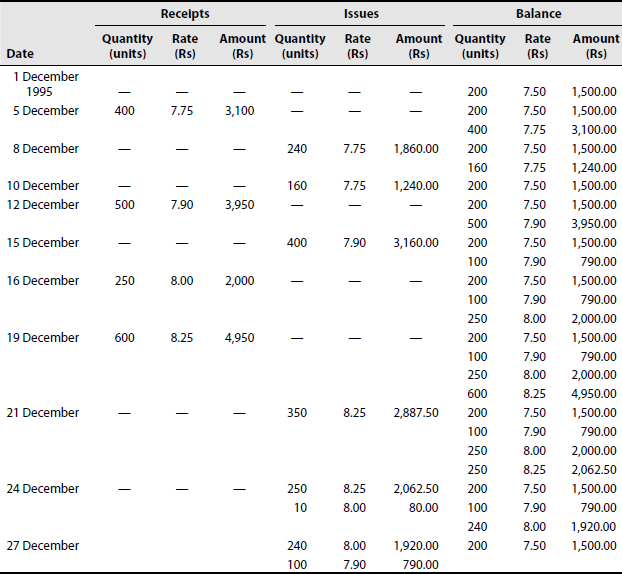

- The stores ledger account of material C in the book of Chemical Process Ltd. shows the following transactions for the month of December 1995.

1995 1 December Opening stock is 200 kg at Rs 7.50 per kg 5 Received from supplier 5,400 kg at Rs 7.75 per kg 8 Issued to production department 240 kg 10 Issued 160 kg 12 Received from supplier 500 kg at Rs 7.90 per kg 15 Issued to production department 400 kg 16 Received from supplier 250 kg at Rs 8.00 per kg 19 Received from supplier 600 kg at Rs 8.25 per kg 21 Issued to department 350 kg 24 Issued to production department 260 kg 27 Issued 340 kg All are required to price the issues and draw out the closing balances in the form of stores ledger account under the pricing method of LIFO.

- The following is an extract of the record of receipts and issues of sulphur in a factory during November 2005:

1 January Opening balance is 500 tonne at Rs 100 per tonne 3 Issue: 70 tonne 4 Issue: 100 tonne 8 Issue: 80 tonne 13 Received 200 tonne at Rs 95 per tonne 14 Return from department 15 tonne 16 Issue: 180 tonne 20 Received from supplier 240 tonne at Rs 95 per tonne 24 Issue: 300 tonne 25 Received from supplier 320 tonne at Rs 95 per tonne 26 Issue: 115 tonne 27 Return from department 35 tonne 28 Received from supplier 100 tonne at Rs 95 per tonne Issues are to be priced on the LIFO principle.

- Indian Oil is a bulk distributor of high-octane petrol. A periodic inventory of petrol at hand is made when the books are closed at the end of each month. The following summary of information is available for the month of June.

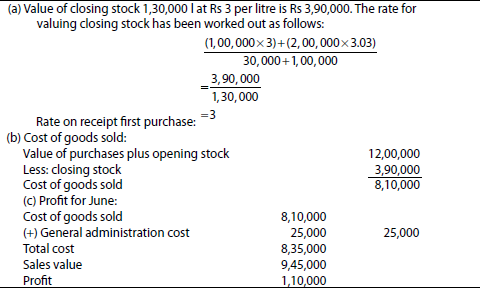

Sales Rs 9,45,000 General administration cost Rs 25,000 Opening stock: 1,00,000 l at Rs 3 per litre Rs 3,00,000 Purchases (including freight inwards): 1 June 2,00,000 l at Rs 2.85 per litre 30 June 1,00,000 l at Rs 3.03 per litre 30 June Closing stock is 1,30,000 l Compute the following data by the weighted average method of inventory costing:

- Value of inventory on 30 June

- Amount of the cost of goods sold in June

- Profit or loss for June

Weighted average method:

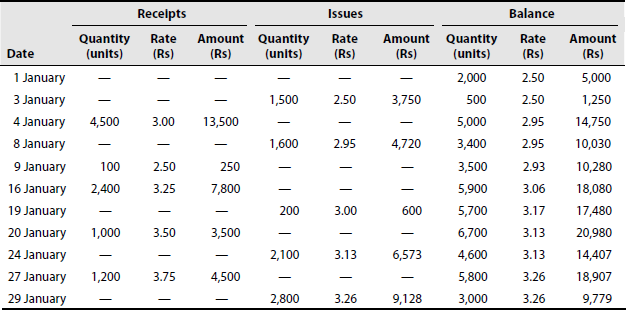

- From the following details of stores receipts and issues of material ABC in a manufacturing unit, prepare the stock ledger using the weighted average method of valuing the issues:

1 January Opening stock is 2,000 units at Rs 2.50 each 3 January Issued 1,500 units to production 4 January Received 4,500 units at Rs 3 each 8 January Issued 1,600 units to production 9 January Returned to stores 100 units by production department (from the issue of 3 January) 16 January Received 2,400 units at Rs 3.25 each 19 January Returned to the supplier 200 units out of the quantity received on 4 January 20 January Received 1,000 units at Rs 3.50 each 24 January Issued to production 2,100 units 27 January Received 1,200 units at Rs 3.75 each 29 January Issued to production 2,800 units

CHAPTER SUMMARY

After reading this chapter, you should have understood the different methods of pricing of materials, adjust-ments involved in these methods, and merits and demerits of each method. It should be noted that material should be controlled to reduce the cost of production.

EXERCISE FOR YOUR PRACTICE

Objective-Type Questions

- State whether the following statements are true or false:

- In standard price method, issue of materials is priced at a predetermined rate.

- When material prices fluctuate widely, the method of pricing that gives absurd result is simple average price. 3. When prices fluctuate widely, the method that will smooth out the effects of fluctuations is the weighted average method.

- Price fluctuation is not an important criterion in fixing pricing methods.

- Under replacement price method, issues are priced at the market rate.

- In LIFO, issues are close to current economic values.

- Weighted average method is adding all the different prices and dividing the sum by the number of such prices.

- FIFO is suitable in times of rising prices.

- Material should be issued against material requisition.

- Market price method is suitable when quotations have to be sent.

[Ans: 1—true, 2—true, 3—true, 4—false, 5—true, 6—true, 7—false, 8—false, 9—true, 10—true]

- Choose the correct answer:

- Reordering quantity may be measured in

- LIFO

- FIFO

- Standard cost

- Weighted average cost

Ans: (a)

- Which of the following methods of stock control aims at concentrating efforts on selected items of materials?

- Level setting

- Material turnover

- ABC analysis

- Perpetual inventory system

Ans: (c)

- Under which method issue of materials is priced at the latest purchase price?

- Simple average

- Weighted average

- LIFO

- FIFO

Ans: (c)

- In the base stock method of pricing material issues, the term base stock represents the

- Maximum stock

- Minimum stock

- Stock in balance

- Quantity of stock being issued

Ans: (b)

- When prices fluctuate widely, the method of pricing that smoothes out the effects of fluctuations is

- FIFO

- LIFO

- Weighted average

- Simple average

Ans: (c)

- In which of the following methods are issues of materials priced at a predetermined rate?

- Specific price method

- Inflated price method

- Replacement price method

- Standard price method

Ans: (d)

- The method of pricing where cost lag behind the current economic values is

- LIFO

- Weighted average price

- Simple average

- Replacement cost

Ans: (b)

- A method of stock valuation seldom used by companies is

- Standard cost

- FIFO

- LIFO

- Weighted average cost

Ans: (c)

- Materials are issued at the price prevailing at the time of issue in

- Specific price method

- Replacement price method

- Inflated price method

- Standard price method

Ans: (b)

- A purchase requisition is prepared by

- Storekeeper

- Supplier

- Foremen

- Purchase manager

Ans: (a)

- Reordering quantity may be measured in

DISCUSSION QUESTIONS

Short Answer-Type Questions

- Write short notes on LIFO and FIFO methods.

- What do you mean by standard price?

- Write a short note on average cost method.

- What is base stock?

Essay-Type Questions

- Write the advantages and disadvantages of LIFO method.

- Explain the merits and demerits of average cost method.

- Indicate the different methods used for pricing materials.

- Which of the pricing methods would you recommend under conditions of rising prices and why?

- What are the conditions that favour the adoption of FIFO and LIFO methods?

PROBLEMS

- The following information is extracted from the stores ledger:

1 January Opening balance 500 units at Rs 4 each 5 Purchases 200 units at Rs 4.25 each 12 Purchases 150 units at Rs 4.10 each 20 Purchases 300 units at Rs 4.50 each 25 Purchases 400 units at Rs 4.00 each Issues of materials were as follows: 4 January 200 units 10 400 units 15 100 units 19 100 units 26 200 units 30 250 units Issues are to be priced on the principle of FIFO. Write the stores ledger account.

(Madras, 1996)

[Ans: closing stock = 300 units at Rs 4 per unit = Rs 1,200]

- Write a stores ledger card in the proper form making use of the following particulars, pricing issues on the principle of FIFO:

The stock verifier found a shortage of 10 units on 30 January and left a note.

(B.Com., Kerala)

[Ans: stocks = 190 units at Rs 28 each = Rs 5,320]

- The following transactions are recorded in respect of materials used in a factory during April 1984:

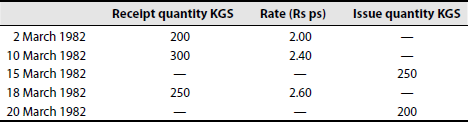

1 April Opening balance 500 tonne at Rs 25 2 Issue 70 tonne 4 Issue 100 tonne 7 Issue 80 tonne 12 Received from vendor 200 tonne at Rs 26 14 Return of surplus from a work order 15 tonne at Rs 25 16 Issue 180 tonne 20 Received from vendor 240 tonne at Rs 25 24 Issue 300 tonne 25 Received from vendor 320 tonne at Rs 28 26 Issue 112 tonne 27 Refund of surplus from a work order 12 tonne at Rs 27 28 Received from vendor 100 tonne at Rs 29 Issues are to be priced on the principle of FIFO. The stock verifier noted that on 15 April he found a shortage of 5 tonne and on 27 April another shortage of 8 tonne. Write the stores ledger account.

(Madras, 1986)

[Ans: closing stock = 532 units, valued at Rs 14,684 (100 × 25 + 320 × 28 + 12 × 27 + 100 × 29)]

- The following is the record of receipts and issues for a certain material in a factory during a week:

1 January Opening balance is 50 tonne at Rs 10.00 per tonne 1 Issued 30 tonne 2 Received 60 tonne at Rs 10.20 per tonne 3 Issued 25 tonne 3 Stock verification revealed a loss of 1 tonne 4 Received back from work orders 10 tonne (previously issued at Rs 9.15 per tonne) 5 Issued 40 tonne 6 Received 22 tonne at Rs 10.30 per tonne 7 Issued 38 tonne At what prices will you issue the materials? Use two important methods for this purpose and show the comparative results.

(B. Com. Bangalore)

[Ans: value of stocks: 8 tonne at Rs 10.30 = Rs 82.40 (FIFO);

8 tonne at Rs 10.00 = Rs 80.00 (LIFO)]

- A clothing manufacturer commenced business on 1 January 1989. Textile materials used by the manufacturer include two types: M and N. During the six months till 30 June 1989, purchases were as follows:

4 January 1,000 m of type M Rs 10.00 per metre 6 January 1,600 m of type N Rs 15.00 per metre 18 March 2,300 m of type M Rs 12.00 per metre 16 April 3,000 m of type N Rs 16.00 per metre 26 May 800 m of type M Rs 9.50 per metre Issues from the storeroom to the factory were as follows:

7 January 700 m of M 12 January 1,200 m of N 28 March 1,420 m of M 22 April 2,860 m of N 1 June 1,580 m of M Materials were charged to the factory at cost on the FIFO principle. Prepare stores ledger account.

(Madras, 1990)

[Ans: closing stock = type M 400 m at Rs 9.50 each; type N 540 m at Rs 16.00 each]

- From the following particulars, write the stores ledger card:

1 January Opening stock is 1,000 units at Rs 26.00 each 5 Purchased 500 units at Rs 24.50 each 7 Issued 750 units 10 Purchased 1,500 units at Rs 24.00 each 12 Issued 1,100 units 15 Purchased 1,000 units at Rs 25.00 each 17 Issued 500 units 18 Issued 300 units 25 Purchased 1,500 units at Rs 26.00 each 29 Issued 1,500 units Adopt the FIFO method of issue and ascertain the value of closing stock.

(B. Com., Bangalore)

[Ans: stocks = 1,350 units at Rs 26 = Rs 35,100]

- From the following particulars, prepare a stores ledger by adopting the LIFO method:

Date Receipts Issues 1 January 1990 300 units at Rs 10 per unit 10 200 units at Rs 12 per unit 15 250 units 18 200 units at Rs 14 per unit 20 300 units 25 100 units at Rs 16 per unit 31 100 units (Madras, 1992)

[Ans: closing stock = 150 units at Rs 10 per unit = Rs 1,500]

- The following information is provided by Coorg Coffee manufacturing unit for the fortnight of April 1996:

Material A Stock on 1 April 1996 100 units at Rs 5 per unit Purchases: 5 April 1996 300 units at Rs 6 8 April 1996 500 units at Rs 7 12 April 1996 600 units at Rs 8 Issues: 6 April 1996 250 units 10 April 1996 400 units 14 April 1996 500 units Calculate the value of material consumed during the period under LIFO method.

(Madras, 1997)

[Ans: closing stock = 350 units valued at Rs 2,300 (100 × 5 + 50 × 6 + 100 × 7 + 100 × 8)]

- The following are the receipts and issues of coal in a factory during March 1994:

1 March Opening stock is 200 tonne at Rs 460 per tonne 4 Issued 140 tonne 6 Purchased 350 tonne at Rs 450 per tonne 8 Condemned due to deterioration in quality and transferred to scrap, 30 tonne 9 Issued 80 tonne 14 Issued 210 tonne 17 Purchased 200 tonne at Rs 480 per tonne 20 Issued 120 tonne 25 Purchased 180 tonne at Rs 470 per tonne 28 Issued 280 tonne 31 Excess found in stock, 43 tonne, due to wrong weighing during the month The maximum level fixed is 400 tonne, the minimum is 75 tonne and the reorder level is 100 tonne. Show the stores ledger under LIFO system.

(B.Com, Madurai)

[Ans: value of stocks = 113 tonne (60 × Rs 460 + 10 × Rs 450 + 43 × Rs 470) = Rs 52,310]

- Enter the following transactions in the stores ledger of material Y using the (i) FIFO and (ii) LIFO methods:

May 1980 1 Balance of 250 units at Re 1 per unit 3 Issued 50 units on MR number 61 6 Received 800 units, vide goods received [note number 13] at Rs 1.10 per unit 7 Issued 300 units on MR number 63 8 Returned to stores 20 units issued on MR number 61 12 Received 300 units as per GRN number 15 at Rs 1.20 per unit 15 Issued 320 units [MR number 83] 18 Received 100 units, vide GRN number 77 at 1.20 per unit 20 Issued 80 units [MR number 102] 23 Returned to vendors 20 units from GRN number 77 received on 18 May 26 Received 200 units on GRN number 96 at Re 1 per unit 28 Freight paid on purchase [vide GRN number 96] Rs 50 30 Issued 250 units on MR number 113 (Madras, 1983)

[Ans: closing stock = LIFO—650 units valued at Rs 695 (200 × 1 + 450 × 1.10),

FIFO—650 units valued at Rs 781 (50 × 1.10 + 20 × 1 + 300 × 1.20 + 80 ×

1.20 + 200 × 1 + 50)]

Note:

- ‘Returned to store’ is treated like a fresh receipt and issue is as per the method used.

- 'Return to supplier’ is like an issue, but at the original purchase price.

- 'Freight paid should be added to the cost of a specific purchase.

- From the following transaction, prepare separately the stores ledger accounts, using the (i) FIFO and (ii) LIFO pricing methods:

January 1 Opening balance is 100 units at Rs 5 each January 5 Received 500 units at Rs 6 each January 20 Issued 300 units February 5 Issued 200 units February 6 Received 600 units at Rs 5 each March 10 Issued 300 units March 12 Issued 250 units (I.C.W.A. Inter)

[Ans: value of stocks: (i) 150 units at Rs 5 = Rs 750 and (ii) 150 units at Rs 5 = Rs 750]

- From the following transactions, prepare separately the stores ledger account, using the (i) FIFO and (ii) LIFO methods:

1 January Opening balance 100 units at Rs 5 each 5 Received 500 units at Rs 6 each 20 Issued 300 units 5 February Issued 200 units 6 February Received back from work order 10 units Issued on 5 February 7 February Received 600 units at Rs 5 each 20 February Issued 300 units 25 February Returned to supplier 50 units purchased on 7 February 26 February Issued 200 units 10 March Received 500 units at Rs 7 per unit 15 March Issued 300 units Stock verification on 15 March revealed a shortage of 10 units.

[Ans: closing stock = FIFO—350 units valued at Rs 7 each = Rs 2,450;

LIFO—350 units valued at Rs 2,140 (100 × 5 + 10 × 6 + 50 × 5 + 190 × 7)]

- In the beginning of October 1994, Bangalore Tin Co. had 10,000 lb of tin at Rs 2 per lb. Further purchases were made during the month as follows:

4 October 2,000 lb at Rs 2.50 per lb 10 October 6,000 lb, at Rs 2.00 per lb 20 October 10,000 lb at Rs 3.50 per lb The issues to manufacture were as follows:

12 October 16,000 lb 22 October 10,000 lb Write the stores ledger cards with the aforementioned transactions based on both the FIFO and LIFO methods. What will be the value of closing stock in each case?

(B. Com., Bangalore)

[Ans: value of stocks = FIFO: 2,000 units—Rs 7,000; LIFO: 2,000 units—Rs 4,000]

- Prepare a stores ledger account from the following transactions assuming that the issue of stores has been priced on the LIFO principle:

January 1 Received 1,000 units at Rs 20 per unit January 10 Received 260 units at Rs 21 per unit January 20 Issued 700 units February 4 Received 400 units at Rs 23 per unit February 21 Received 300 units at Rs 25 per unit March 16 Issued 620 units April 12 Issued 240 units May 10 Received 500 units at Rs 22 per unit May 25 Issued 380 units (B. Com., Delhi)

[Ans: value of stocks = 520 units—Rs 10,640]

- From the following information, prepare a store ledger account under specific pricing with FIFO:

1 April Opening balance 50 kg at Rs 10 2 April Issued 30 kg 4 April Purchased 60 kg at Rs 11 5 April Purchased 50 kg at Rs 12 for a specific job to be issued on 15 April 6 April Issued 25 kg 10 April Purchased 50 kg at Rs 10 16 April Issued 60 kg 25 April Purchased 25 kg at Rs 12 30 April Issued 35 kg (Madras, 1993)

[Ans: closing stock = 35 units valued at Rs 400 (10 × 10 + 25 × 12)]

Hint: The lot purchased on 5 April was reserved and issued to the specific job on 15 April.

- From the following particulars, write the stores ledger card:

1990 1 January Purchased 500 ton at Rs 2 per ton 10 Purchased 300 ton at Rs 2.10 per ton 13 Issued 500 ton 20 Purchased 400 ton at Rs 2.20 per ton 25 Issued 300 ton 27 Purchased 500 ton at Rs 2.10 per ton 31 Issued 200 ton Adopt base stock method with LIFO. Base stock is 200 ton out of the 1 January purchase.

(Bharathidasan, 1992)

[Ans: closing stock = base stock is 200 ton at Rs 2 each = Rs 400;

other stock is 500 ton valued at Rs 1,050 (100 × 2 + 100 × 2.2 + 300 × 2.10)]

- Explain the following two methods of pricing of material issues and also the circumstances under which these methods are used: FIFO and LIFO

Draw a stores ledger card recording the following transactions that took place in a month under the aforementioned two methods:

(I.C.W.A. Inter)

[Ans: value of stocks using LIFO = 50 units at Rs 2.00 + 30 units

at Rs 2.40 = Rs 172; value of stocks using

FIFO = 80 units at Rs 2.50 = Rs 200]

- The following transactions took place for an item of a material:

Record the aforementioned transactions in the stores ledger, pricing issues at simple average rate.

(Madras, 1995)

Ans: closing stock = 300 units valued at Rs 720]

- The following transactions took place for a material item:

Prepare a priced ledger sheet, pricing the issues at weighted average rate.

(Madras, 1994)

[Ans: closing stock = 300 units at Rs 242 = Rs 726]

- XY Ltd. purchased and issued materials in the following order:

March 1985 1 Purchased 300 units at Rs 3 per unit 5 Purchased 500 units at Rs 4 per unit 10 Issued 500 units 12 Purchased 700 units at Rs 4.50 per unit 15 Issued 700 units 20 Purchased 300 units at Rs 5 per unit 30 Issued 150 units Ascertain the quantity of closing stock as on 31 March and state its value under the weighted average cost method.

(Madras, 1986)

[Ans: closing stock = 450 units at Rs 4.61875 = Rs 2,078]

- From the following particulars, prepare stores ledger account showing the pricing of material issues under (i) simple average and (ii) weighted average methods:

2 August 1983 Opening stock 800 units at Rs 4.20 3 August 1983 Purchased 800 units at Rs 4.20 4 August 1983 Issued 1,200 units 6 August 1983 Purchased 1,600 units at Rs 4.80 7 August 1983 Issued 1,000 units 9 August 1983 Purchased 400 units at Rs 6.00 11 August 1983 Issued 800 units 13 August 1983 Issued 100 units 15 August 1983 Purchased 500 units at Rs 8.00 (Madras,. 1987)

[Ans: closing stock: (i) 1,000 units valued at Rs 6,400;

(ii) 1,000 units valued at Rs 6.529 = Rs 6,529]

- The following transactions occur in the purchase and issue of a material:

2 January Purchased 4,000 units at Rs 4.00 per unit 20 Purchased 500 units at Rs 5.00 per unit 5 February Issued 2,000 units 10 Purchased 6,000 units at Rs 6.00 per unit 12 Issued 4,000 units 2 March Issued 1,000 units 5 Issued 2,000 units 15 Purchased 4,500 units at Rs 5.50 per unit 20 Issued 3,000 units Prepare stores ledger account using the (a) simple average method and (b) weighted average method.

(Madras,. 1996)

[Ans: closing stock: (a) 3,000 units valued at Rs 18,000;

(b) 3,000 units at Rs 54,863 per unit = Rs 16,475]

- Show the stores ledger entries as they would appear when using the (a) weighted average method and (b) LIFO method of pricing issues in connection with the following transactions:

In a period of rising prices such as above, what are the effects of each method?

(I.C.W.A.)

[Ans: value of stocks: 150 units at Rs 2.28 Rs 342.00

(weighted average) and 150 units at Rs 2.00 Rs 300.00 (LIFO)]

- The following were the receipts and issues of a material during March:

1 March Opening balance is 1,000 units at Rs 50 per unit 3 Issued 140 units 4 Issued 200 units 8 Issued 160 units 13 Received from vendor 400 units at Rs 48 per unit 14 Refund of surplus from a work order, 30 units at Rs 48 per unit 16 Issued 360 units 20 Received from vendor 480 units at Rs 52 per unit 24 Issued 608 units 25 Received from vendor 640 units at Rs 50 per unit 26 Issued 524 units 28 Refund of surplus from a work order, 24 units (issued on 3 March) 31 Received from vendor 200 units at Rs 54 per unit From the aforementioned details, write the stores ledger account on simple average basis following the FIFO method.

(B. Com., Mysore)

[Ans: value of stocks = 782 units Rs 39,788]

EXAMINATION PROBLEMS

- The following information is extracted from the stores ledger:

1 September Opening balance 500 units at Rs 10 6 Purchases 100 units at Rs 11 20 Purchases 700 units at Rs 12 27 Purchases 400 units at Rs 13 13 October Purchases 1,000 units at Rs 14 20 Purchases 500 units at Rs 15 17 November Purchases 400 units at Rs 16 Issues of materials: 9 September 500 units 22 500 units 30 500 units 15 October 500 units 22 500 units 11 November 500 units Issues are to be priced on the principle of FIFO. Write the stores ledger account.

(Madras, 1999)

[Ans: closing stock 600 units at Rs 9,400 (200 × 15 + 400 × 16)]

- From the following particulars, prepare the stores ledger account under the FIFO method of pricing issues:

1992 1 January Opening balance 50 units at Rs 30 per unit 5 Issued 20 units 7 Purchased 48 units at Rs 40 per unit 9 Issued 20 units 19 Purchased 36 units at Rs 35 per unit 24 Received back 10 units out of the units issued on 9 January 27 Issued 15 units (Madras,1995)

[Ans: closing stock is 89 units; value is Rs 3,280 (43 × 40 + 36 × 35 + 10 × 30)]

Hint: Returned material of 10 units is shown like a fresh receipt at the original issue price of Rs 30.

- Prepare a store ledger account from the following information adopting the FIFO method of pricing of issues of materials:

1 March Opening balance 500 tonne at Rs 200 3 Issued 70 tonne 4 Issued 100 tonne 8 Issued 80 tonne 13 Received from supplier 200 tonne at Rs 190 14 Returned from department A 15 tonne 16 Issued 180 tonne 20 Received from supplier 240 tonne at Rs 195 24 Issued 300 tonne 25 Received from supplier 320 tonne at Rs 200 26 Issued 115 tonne 27 Returned from department B 35 tonne 28 Received from supplier 100 tonne at Rs 200 (Madras, 1989)

[Ans: closing stock– is 565 tonne, valued at Rs 1,12,275

(110 × 195 + 320 × 200 + 35 × 195 + 100 × 200)]

Hint: Returns from departments on 14 and 27 March are to be assumed out of the immediate preceding issue since no details are given.

- From the following transactions, prepare stores ledger account (using the FIFO method):

October 1 Opening balance is 100 units at Rs 5 each 2 Received 500 units at Rs 6 each 20 Issued 300 units November 5 Issued 200 units 6 Received 500 units at Rs 5 each December 10 Issued 300 units 12 Issued 250 units (B. Com., Madurai)

[Ans: value of stock is 50 units at Rs 5 each = Rs 250]

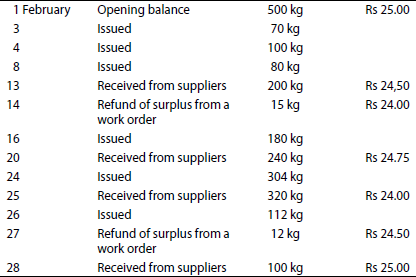

- The following is the summary of the receipts and issues of materials in a factory during February:

Issues are to be priced on the principle of FIFO. The stock verifier of the factory noticed that on 15 February there was a shortage of 5 kg and on 27 February there was another shortage of 8 kg. Write the stores ledger account, recording the aforementioned transactions.

(B. Com., Tirupati)

[Ans: stocks = 528 units 96 × Rs 24.75 + 320 × 24 + 12 × 24.50 + 100 × 25 = Rs 12,850]

- The following receipts and issues were made for a material during the month of May 1993:

Receipts 1 May 1993 Balance of stock 500 units at Rs 4.50 per unit 7 May 1993 Purchases 400 units at Rs 5.00 per unit 15 May 1993 Purchases 1,000 units at Rs 5.50 per unit 23 May 1993 Purchases 700 units at Rs 4.80 per unit Issues 3 May 1993 Issued 200 units 8 May 1993 Issued 100 units 17 May 1993 Issued 700 units 26 May 1993 Issued 700 units Assume that base stock is 200 units out of the opening stock; use FIFO method.

(Madras, 1994)

[Ans: closing stock: base stock is 200 units at Rs 4.50 = Rs 900; other stock is 700 units at Rs 4.8 = Rs 3,360; and total stock is 900 units, valued at Rs 4,260]

Hint: Base stock of 200 units at Rs 4.50 out of the opening stock should always be a part of the stock and should not be issued.

- From the following particulars, prepare the stores ledger under the LIFO method:

1 December Stock in hand 500 units at Rs 20 2 December Issued 200 units 3 December Purchased 150 units at Rs 22 4 December Issued 100 units 5 December Purchased 200 units at Rs 25 (Madras, 1998)

[Ans: closing stock is 550 units valued at Rs 12,100 (300 × 20 + 50 × 22 + 200 × 25)]

- The ‘Receipts’ side of the stores ledger account shows the following particulars:

1 January Opening balance of 500 units at Rs 4 per unit 5 January Received 200 units at Rs 4.25 per unit 12 January Received 150 units at Rs 4.10 per unit 20 January Received 300 units at Rs 4.50 per unit 25 January Received 400 units at Rs 4.00 per unit Issues of the materials are as follows:

4 January Issued 200 units 10 January Issued 400 units 15 January Issued 100 units 19 January Issued 100 units 26 January Issued 200 units 30 January Issued 250 units Write the stores ledger account pricing the issues on the principle of FIFO and LIFO.

(B. Com., Tirupati)

[Ans: value of stocks—(a) 300 units at Rs 4 = Rs 1,200 and (b) 300 units (300 × 4 = 1,200)]

- Prepare a statement showing how the issues would be priced under LIFO method:

1998 1 February Opening balance 100 units at Rs 10 each 1 February Received 200 units at Rs 10.50 each 2 February Received 300 units at Rs 10.60 each 4 February Issued 400 units to job A 6 February Issued 120 units to job K 7 February Received 400 units at Rs 11 each 10 February Issued 200 units at job B 12 February Received 400 units at Rs 11.50 each 17 February Issued 300 units to job D (Madras, 1998)

[Ans: Closing stock is 380 units valued at Rs 4,150 (80 × 10 + 200 × 11 + 100 × 11.5)]

- Prepare a store ledger account and enter the following transactions adopting the simple average method of pricing issues:

1985 1 February Opening balance 50 units at Rs 3 per unit 5 Issued 20 units 7 Purchased 40 units at Rs 4 per unit 9 Issued 25 units 19 Purchased 75 units at Rs 5 per unit 20 Issued 15 units 21 Received back 10 units out of the 9 February issue 26 Issued 60 units (Madras, 1986)

[Ans: Closing stock is 55 units valued at Rs 262.50]

- The following particulars have been extracted for material X. Prepare a store ledger account showing the receipts and issues, pricing the materials issued on the basis of (a) simple average and (b) weighted average methods:

Receipts

1 October 1994, opening stock 200 units Rs 3.50 per unit 3 October 1994, purchased 300 units Rs 4.00 per unit 13 October 1994, purchased 900 units Rs 4.30 per unit 23 October 1994, purchased 600 units Rs 3.80 per unit Issues

5 October 1994, issued 400 units 15 October 1994, issued 600 units 25 October 1994, issued 600 units (B. Com., Poona)

[Ans: Issue price rate 5, 15 and 25 October: closing stock—(a) 3.75, 4.15, 4.05, 400 units,

Rs 1,630; (b) 3.80, 4.25, 3.98, 400 units, Rs 1,592]

- From the following particulars, prepare the store ledger account showing the pricing of material issue under (a) simple average and (b) weighted average:

December 1994 1 Opening stock is 500 units at Rs 2 each 3 Purchased 400 units at Rs 2.10 each 5 Issued 600 units, vide MR number 15 7 Purchased 800 units at Rs 2.40 each 9 Issued 501 units, vide MR number 22 12 Returned from issue on 5 December, 12 units 17 Purchased 400 units at Rs 2.50 each 25 Issued 600 units, vide MR number 30 (B. Com. Calicut)

[Ans: value of stocks—(a) 422 units, Rs 1,058 returns at Rs 2.05;

(b) 422 at Rs 2.38 = Rs 1,004.36]

- Prepare a store ledger account by adopting the weighted average method of pricing.

1 September 1997 Opening balance 50 units at Rs 3 per unit 4 Issued 2 units 8 Purchased 48 units at Rs 4 per unit 9 Issued 20 units 15 Purchased 76 units at Rs 3 per unit 22 Received back into stores 19 units out of the 20 units issued on 9 September 30 Issued 10 units to production (Madras, 1998)

[Ans: closing stock = 161 units at Rs 3.27778 = Rs 527.72]

- Prepare a store ledger account assuming that issues are priced on the principle of HIFO:

1 December Received 1,000 units at Rs 20 per unit 10 Received 500 units at Rs 22 per unit 11 Received 200 units at Rs 21 per unit 15 Issued 500 units 20 Issued 150 units 22 Received 700 units at Rs 23 per unit 24 Received 300 units at Rs 19 per unit 28 Issued 500 units 30 Received 200 units at Rs 18 per unit 31 Issued 300 units [Ans: closing stock = 1,450 units, valued at Rs 28,300

(950 × 20 + 300 × 19 + 200 × 18)]

- The standard price of a material is fixed at Rs 20 per unit. Show the store ledger entries as they would appear when using the standard price method.

Calculate the material price variance.

[Ans: closing balance = 450 units valued at Rs 10,400;

material price variance = Rs 1,400 (adverse)]

- (Computation of standard price and variance) With the help of the following information, prepare the store ledger card based on the standard price method:

The credit balance of material price variance was Rs 1,000 on 1 August 1998.