Chapter 15. Bank Accounts, Credit Cards, and Petty Cash

You’ve opened your mail, plucked out your customers’ payments, and deposited them in your bank account (Chapter 13); in addition to that, your bills are paid (Chapter 9). Now you can sit back and relax knowing that most of the transactions in your bank and credit card accounts are accounted for. What’s left?

Some stray transactions might pop up—an insurance claim check to deposit, restocking your petty cash drawer, or a fee from your bank for a customer’s bounced check, to name a few. Plus, running a business typically means that money moves between accounts—from interest-bearing accounts to checking accounts or from merchant credit card accounts to savings. If you come across a financial transaction, you can enter it in QuickBooks, whether you prefer the guidance of dialog boxes or the speed of an account register window.

Reconciling your accounts to your bank statements is another key process you don’t want to skip. You and your bank can both make mistakes, and reconciling your accounts is the best way to catch these discrepancies. Once the bane of bookkeepers everywhere, reconciling is practically automatic now that you can download transactions electronically and let QuickBooks handle the math.

In this chapter, the section on reconciling is the only must-read. If you want to learn the fastest way to enter any type of bank account transaction, don’t skip the first section, Entering Transactions in an Account Register on Opening a Register Window. You can read about transferring funds, loans, bounced checks, and other financial arcana covered in this chapter as the need arises.

Entering Transactions in an Account Register

QuickBooks includes windows and dialog boxes for making deposits, writing checks, and transferring funds, but you can also construct these transactions right in a bank account’s register window. Working in a register window has two advantages over the dialog boxes:

Speed. Entering a transaction in a register window is fast, particularly when keyboard shortcuts, like pressing Tab to move between fields, are second nature.

Visibility. Windows, such as Write Checks, keep you focused on the transaction at hand. You can’t see other transactions unless you align the transaction window and the register window side by side. In a register window, you can look at previous transactions for reference and avoid entering duplicate transactions.

Opening a Register Window

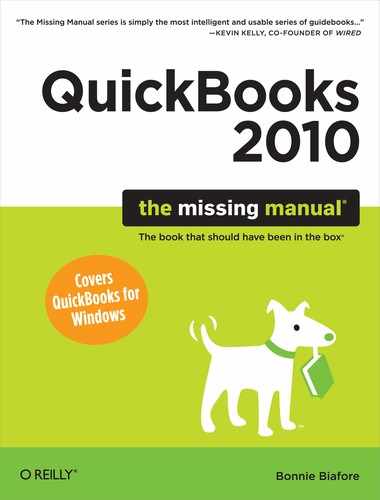

You have to open a register window before you can enter transactions in it. Opening a register window couldn’t be easier. If you want to open a bank account or credit card register, at the top-right of the Home page, under Account Balances, double-click the account you want to see. Here’s how you can open any kind of account:

If the Chart of Accounts window isn’t open, press Ctrl+A (or, on the Home page, click Chart of Accounts).

The window pops open, listing all accounts you’ve set up in QuickBooks.

In the Chart of Accounts window, double-click the bank account whose register window you want to open.

As you can see in Figure 15-1, this method can open register windows for more than just bank accounts. See the box on the next page to learn about different ways to handle credit card accounts.

Creating a Transaction in an Account Register

The steps for creating a check in your checking account register (Adding Checks to an Account Register) work for deposits and transfers, too, with only a few minor adjustments. Here’s how to fill in the cells in the register window to create any kind of bank transaction:

Date. When you first open a bank account register window, QuickBooks automatically puts the current date in the Date cell of the first blank transaction. Tweaking the date by a few days is as easy as pressing + or - until the date is the one you want. To become a master of keyboard shortcuts for dates, read the box on Creating a Transaction in an Account Register.

Figure 15-1. You can open a register window by double-clicking any type of account with a balance, including checking, savings, money market, and petty cash accounts. In fact, double-clicking opens the register for any account on your balance sheet (Accounts Receivable, Accounts Payable, Credit Card, Asset, Liability, and Equity accounts).Number. When you jump to the Number cell (press Tab), QuickBooks automatically fills in the next check number for the bank account. If the number doesn’t match the paper check you want to write, press + or – until the number is correct. (For some types of accounts like credit cards and assets, the register has a Ref field instead of a Number field. You can fill in a reference number for the transaction or leave it blank.)

To make an online payment (see Chapter 22), in the Number cell, type S, which QuickBooks promptly changes to Send.

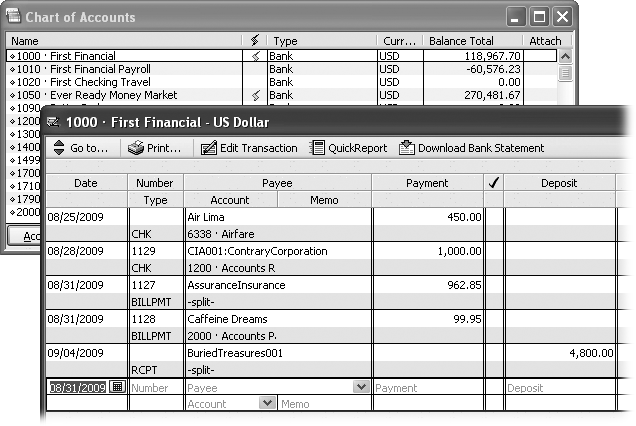

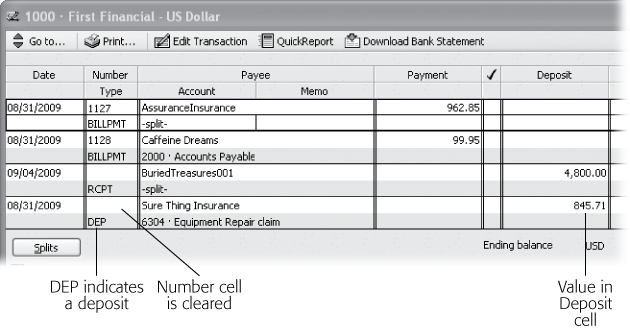

To enter a deposit, you can bypass the Number and Payment cells regardless of what values they have, as you can see in Figure 15-2.

Figure 15-2. You aren’t alone if you frequently type a deposit amount in the Payment cell. Be sure to fill in the value in the Deposit cell. When you move to another cell, QuickBooks springs into action. It automatically clears the check number in the Number cell and the value in the Payment cell. And it replaces the code CHK in the Type cell with DEP for deposit.Note

QuickBooks keeps track of handwritten and printed checks separately. When you use the register window to create a check, QuickBooks fills in the Number cell by incrementing the last handwritten check number. When you choose File → Print Forms → Checks, the program fills in the First Check Number box by incrementing the last printed check number.

Payee. QuickBooks doesn’t require a value in the Payee cell. In fact, for the occasional payee, it’s better to leave that payee name out of the Payee cell for deposits, transfers, or petty cash transactions, so your Vendors list doesn’t fill up with names you rarely use. Instead, type a Payee name like Deposit or Petty Cash and then fill in the Memo cell with a description of the transaction, like Insurance Claim.

Tip

If you want to fill in the Payee cell without filling up the Vendors list, create more general names, like Deposit, Transfer, Petty Cash, and Gasoline. Then you can fill in the Payee cell for every fuel purchase with Gasoline and type the name of the service station in the Memo cell.

As you start typing the name of the payee, QuickBooks scans the names in the various lists in your company file (Vendors, Customers, Other Names, and so on) and selects the first name it finds that matches all the letters you’ve typed so far. As soon as QuickBooks selects the one you want, press Tab to move to the Payment cell.

Payment or Charge. For checks you write, fees that the bank deducts from your account, or petty cash withdrawals, type the amount in the Payment cell. In a credit card register, this field is named Charge for the credit card charges you make.

Deposit. For deposits you make to checking or petty cash, or interest you earned, type the amount in the Deposit cell. In a credit card register, this field is called Payment, because you make payments to a credit card account (instead of making a payment from a checking account).

Account. The Account cell can play many roles. For instance, when you’re creating a check, choose the account for the expense it represents. If you’re making a deposit, choose the income or expense account to which you want to post the deposit. (Depositing an insurance claim check that pays for equipment repair reduces the balance of the expense account for equipment maintenance and repair.) If you’re transferring money from another bank account, choose that account instead.

Tip

If you want to assign a transaction to several accounts, click Splits. Figure 9-2 (Entering Bills) shows how to distribute dollars to different accounts.

Memo. Filling in the Memo cell can jog your memory no matter what type of transaction you create. Enter the bank branch for a deposit (in case your deposit ends up in someone else’s account), the restaurant for a credit card charge, or the items you purchased with petty cash. The transaction reminders just keep coming—the contents of the Memo cell appear in the reports you create.

Note

Remember your accountant’s insistence on an audit trail? If you create a transaction by mistake, don’t delete it. Although QuickBooks’ audit trail keeps track of transactions that you delete, the omission can be confusing to others—or to you after some time has passed.

If you void a transaction instead, the amount (payment or deposit) changes to zero. The voided transaction still appears in your company file, so you know that it happened, but it doesn’t affect any account balances or financial reports. Before you void a transaction, add a note in the Memo field that explains why you’re voiding it. In a register window, right-click a transaction and choose the appropriate Void command (Void Check, Void Deposit, and so on) on the shortcut menu.

Handling Bounced Checks

Bouncing one of your own checks is annoying and embarrassing. And banks charge for each check you bounce (and, often, they craftily pay your larger checks before the smaller ones to rack up as many bounced check charges as possible). Besides depositing more money to cover the shortfall and paying those bank fees, you have to tell people to re-deposit the checks that bounced or write new ones.

When someone pays your company with a rubber check, it’s just as annoying. In addition to the charges your bank might charge for re-depositing a bounced check, you have to do a few things to straighten out your records in QuickBooks when a customer’s check bounces, such as:

Record a new transaction that removes the amount of the bounced check from your checking account, because the money never made it that far.

Record any charges that your bank levies on your account for your customer’s bounced check.

Invoice the customer to recover the original payment, your bounced check charges, and any additional charges you add for your trouble.

Setting Up QuickBooks to Handle Bounced Checks

Before you can re-invoice your customers, you first need to create items for bounced checks and their associated charges.

Bounced check reimbursement item

When a check you deposit bounces, you’ll see two transactions on your next bank statement: the original deposit and a second transaction that removes the amount when the check bounces. You have to do the same thing in your company file, so you don’t overestimate your bank balance and write bad checks of your own. Because the customer hasn’t really paid you, the amount of the check should go back into your Accounts Receivable account.

To create an item that removes the amount of the bounced check from your bank account, create an Other Charge item, such as BadCheck. Here’s how:

Choose Lists → Item List to open the Item List window, and then press Ctrl+N.

The New Item window opens.

In the Type drop-down list, choose Other Charge.

The Other Charge item type is perfect for miscellaneous charges that don’t fit any other category.

In the Item Name/Number box, type the item name, BadCheck in this example. In the Account drop-down list, choose your bank account. Click OK.

The new item appears in the Item List.

Service charges for bounced checks

Companies typically request reimbursement for bounced check charges, but many companies tack on additional service charges for the inconvenience of processing a bounced check. Depending on how you account for these charges, you’ll use one or two Other Charge type items:

Bounced check charge reimbursement. To request reimbursement from a customer for your bank’s bounced check charges, you need an Other Charge item that you can add to an invoice, called something like BadCheck Charge. Be sure to choose a nontaxable code for the item so that QuickBooks doesn’t calculate sales tax.

QuickBooks doesn’t care whether you post this item to an income account or an expense account. For example, you can post reimbursed bounced check charges to the same income account you use for other types of service charges. Although the customer’s reimbursement appears as income, the bank charge you paid is an expense. The effect on your net profit (income minus expenses) is zero.

You can also post bounced check reimbursements directly to the same expense account you use for bank service charges. Then when you pay your bank’s bounced check charge, QuickBooks debits the bank service charge account. When the customer pays you back, QuickBooks credits the bank service charge account. The effect on net profit is still zero.

Bounced check service charge. If you post your bank’s bounced check charges to an income account (such as a Service Charge income account), you can use the same item for any extra service charge you apply for the hassle of handling bounced checks. However, if you post customers’ bounced check charge reimbursements to your bank service charge expense account, you need a separate item for your additional service charge. Create an Other Charge type item for the additional service charge. For the item’s Account, choose your service charge income account. Like the bounced check charge reimbursement item, make this charge nontaxable.

Recording Bank Charges

The easiest place to record a bounced check charge is in the bank account register window. This technique works for any bank charge your bank drops on your account or for service charges and interest your credit card company levies:

Press Ctrl+A to open the Chart of Accounts window.

In the Chart of Accounts window, double-click your bank account to open its register window.

In the Date cell in the first blank transaction, choose the date when the bank assessed the charge.

QuickBooks automatically fills in the Number cell with the next check number. Be sure to delete that number before saving the transaction to keep your QuickBooks check numbers synchronized with your paper checks.

In the Payee cell, type the name of your bank or credit card company.

You can also type a generic payee name like Bank Charge.

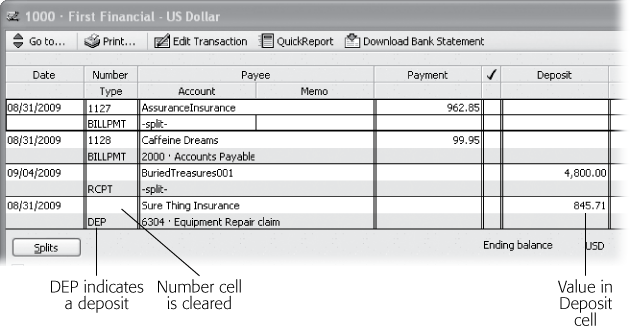

Type the details of the bank charge in the Memo cell, as shown in Figure 15-3.

For a bounced check charge, add the name of the customer, a note that a check bounced, and the number of the check that bounced.

In the Payment cell, type the amount of the bank charge. In the Account cell, choose the account you use to track bank charges or bounced check charges (see previous page).

If you’re recording a bank charge other than a bounced check, choose your expense account for bank service charges in the Account cell. Likewise, choose the service charge expense account if you don’t use statements.

You have to include a bounced check charge item on a new invoice in order to recoup this cost, as described next.

Tip

The Customer:Job cell provides a shortcut to invoicing a customer for bounced check charges. While the transaction is still selected, click Splits to open the Splits table. The Account, Amount, and Memo fields are already filled in with the values you’ve provided so far. To make the bank charge billable to the customer who bounced the check, in the Customer:Job cell, choose the customer. In the Billable? Cell, turn on the checkbox. Then, you can add this billable charge along with any others to the customer’s next invoice (as described in step 5 above).

Click Record.

QuickBooks saves the bank charge in your account.

Re-invoicing for Bounced Checks

With the bounced check items described on Setting Up QuickBooks to Handle Bounced Checks, you can update all the necessary account balances just by re-invoicing the customer for the bounced check. Here’s the short-and-sweet approach:

On the Home page, click Invoices (or press Ctrl+I).

The program opens the Create Invoices window.

In the Customer:Job box, choose the customer who wrote you a bad check.

You don’t have to bother filling in fields like P.O. Number or shipping.

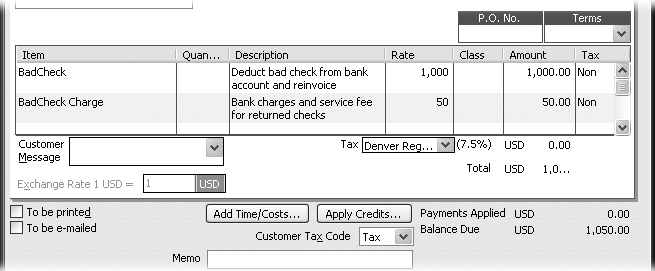

In the item table, add an item for the bounced check itself (“BadCheck” in Figure 15-4).

Figure 15-4. To re-invoice the customer for the amount of the check that bounced, in the first Item cell, choose the item for a bounced check (“BadCheck” in this example). In the Amount cell, type the amount of the bounced check. In the second item cell, choose the item for bounced check charges. The amount covers the bank’s charge for a bounced check and includes any additional service fee you charge.In the Amount cell for the bounced check item, type the amount of the returned check itself.

QuickBooks added any sales tax owed to the original invoice, so include the full amount of the bounced check.

Add a second item to recoup the bounced check fees that your bank charged you. In the Amount cell for the bad check charge item, type the amount you’re charging.

If you really want to deter customers from writing bad checks, in addition to making them pay your bank fees, you can add on a fee for your own trouble. In Figure 15-4, BadCheck Charge covers the bank’s $25 charge plus an additional $25 fee the company collects for itself.

If you recorded the bounced check charge in your bank account as a billable cost to your customer (Re-invoicing for Bounced Checks), the Billable Time/Costs dialog box opens. Keep the “Select the outstanding billable time and costs to add to this invoice” option selected and click OK. In the “Choose Billable Time and Costs” dialog box, click the Expenses tab and select the bank charge. Click OK to add the bank charge to the invoice.

When you save the invoice, QuickBooks updates your bank account and Accounts Receivable account balances, as shown in Figure 15-5.

When you first invoice a customer, the invoice amount gets added on to your Accounts Receivable balance. The customer’s original payment reduced the Accounts Receivable balance, but the bounced check means you have to remove the original payment amount from your records. By re-invoicing the customer, you re-establish the balance as outstanding and add the invoice amount back into Accounts Receivable.

When the customer sends you a check for this new invoice, simply choose Receive Payments to apply that check as a payment for the invoice.

QuickBooks reduces the Accounts Receivable balance by the amount of the payment. If your customer and the money they owe you are gone for good, see the box on Reconciling Accounts to learn what to do next.

Transferring Funds

With the advent of electronic banking services, transferring funds between accounts has become a staple of account maintenance. Companies stash cash in savings and money market accounts to earn interest and then transfer money into checking right before they pay bills.

Fund transfers have nothing to do with income or expenses—they merely move money from one balance sheet account to another. For example, if you keep money in savings until you pay bills, the money moves from your savings bank account (an asset account in your chart of accounts) to your checking bank account (another asset account). Your income, expenses, and, for that matter, your total assets, remain the same before and after the transaction.

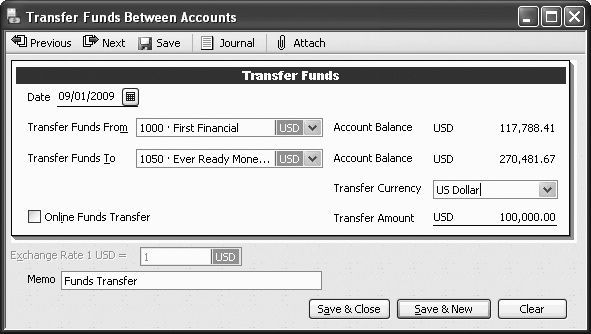

Transferring funds in QuickBooks is easy, whether you use the Transfer Funds dialog box or enter the transaction directly in an account register. The steps for creating a transaction in an account register appear on Opening a Register Window. If you create a transfer in a bank account register (a savings account, for example), in the Account field, choose the bank account to which you’re transferring funds (checking, say). Here’s how to use the Transfer Funds Between Accounts window:

Choose Banking → Transfer Funds.

QuickBooks opens the Transfer Funds Between Accounts window, shown in Figure 15-6.

After you choose the accounts for the transfer, in the Date box, choose the date of the transfer and, on the Transfer Amount line, type the amount you’re transferring from one account to the other.

Typically, you transfer money because you don’t have enough cash in one of your accounts to pay bills. But if you want to record the reason for the transfer, in the Memo box, replace Funds Transfer (which QuickBooks adds automatically) with your reason.

Click Save & Close.

That’s it. Or, if you’ve got more transfers to make, click Save & New. In the account register window for either account in the transfer, QuickBooks identifies the transaction with the code TRANSFR in the Type cell.

Reconciling Accounts

Reconciling a bank statement with a paper check register is tedious and error-prone. Besides checking off items on two different paper documents, the check register and the bank statement never seem to agree—primarily due to arithmetic mistakes you make. With QuickBooks, you can leave your pencils unsharpened and stow your calculator in a drawer.

When all goes well, you can reconcile your account in QuickBooks with a few mouse clicks. Discrepancies crop up less often because QuickBooks does math without mistakes. But problems occasionally happen—transactions might be missing or numbers won’t match. When your bank statement and QuickBooks account don’t agree, QuickBooks helps you find the problems.

Preparing for the First Reconciliation

If you didn’t set the beginning balance for the QuickBooks account to the beginning balance on a bank statement, you might wonder how you can reconcile the bank account the first time around. The best way to resolve this issue is to enter the transactions that happened between your last statement’s end date and the day you started using QuickBooks. Or you can create a journal entry (Creating General Journal Entries) to record the beginning balance. (You’ll select these items as part of the first reconciliation as described on Starting a Reconciliation.)

Warning

Alternatively, the program can align your statement and account the first time you reconcile, as described in the box on Reconciling Transactions. The program generates a transaction that adjusts your account’s opening balance to match the balance on your bank statement. Account opening balances post to your Opening Bal Equity account, so these adjustments affect your Balance Sheet. If you enter an adjustment, let your accountant know that you changed the opening balance so she can address that change while closing your books at the end of the year.

Preparing for Every Reconciliation

QuickBooks lets you create and edit transactions in the middle of a reconciliation, but that doesn’t mean it’s the right way to work. Because bookkeeping in QuickBooks creates an electronic paper trail of forms, you’re better off recording transactions like bills, payments, and deposits first. Reconciling your account flows more smoothly when your transactions are up-to-date.

Take a moment before you reconcile to make sure that you’ve entered all the transactions in your account:

Bills. If you paid bills by writing paper checks and forgot to record the payments in QuickBooks, on the Home page, click Pay Bills and enter those payments (Selecting Bills to Pay).

Checks. Checks missing from your checkbook but not in QuickBooks are a big hint that you wrote a paper check and didn’t record that check in QuickBooks. Create any missing check transactions in the account register (Adding Checks to an Account Register) or choose Banking → Write Checks.

Transfers. Create missing transfers in the account register (Transferring Funds) or choose Banking → Transfer Funds.

Deposits. If you forgot to deposit customer payments in QuickBooks, on the Home page, click Record Deposits to add those deposits to your bank account (Recording Deposits). If a deposit appears on your bank statement but doesn’t show up in the “Payments to Deposit” dialog box, you might have forgotten to receive the payment in QuickBooks. For deposits unrelated to customer payments, create the deposit directly in the account register (Opening a Register Window).

Online transactions. If you use Online Payment or Online Account Access, download online transactions (Online Banking Using Side-by-side Mode) before you start to reconcile your account.

Starting a Reconciliation

Reconciling an account is a two-part process, and QuickBooks has separate dialog boxes for each part. The first part includes choosing the account you want to reconcile, entering the ending balance from your bank statement, and entering service charges and interest earned during the statement period. Here’s how to kick off account reconciliation:

Tip

If your workload gets ahead of you, several months could go by before you have time to reconcile your account. Don’t try to reconcile multiple months at once. Discrepancies are harder to spot, and locating the source of problems will tax your already overworked brain. Put your bank statements in chronological order and then walk through the reconciliation process for each statement.

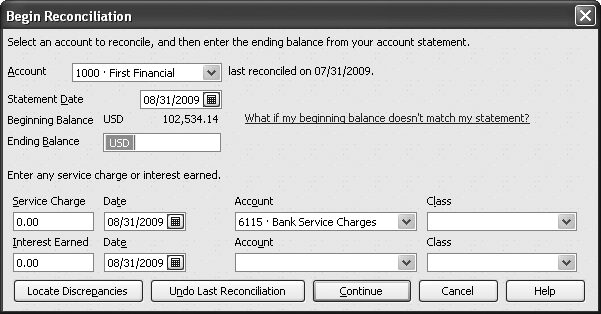

On the Home page, click Reconcile or choose Banking → Reconcile. In the Begin Reconciliation dialog box’s Account drop-down list, choose the account you want to reconcile.

The Begin Reconciliation dialog box displays information about the previous reconciliation, as shown in Figure 15-7.

Figure 15-7. QuickBooks uses the ending balance from the previous reconciliation to fill in the beginning balance for this reconciliation. If the beginning balance in the Begin Reconciliation dialog box doesn’t match the beginning balance on your bank statement, click Cancel and turn to Correcting Discrepancies to learn how to correct the problem.Tip

If the bank account register window is already open, it’s easier to start reconciling by choosing Banking → Reconcile (or right-clicking the register window and choosing Reconcile on the shortcut menu that appears). With this approach, QuickBooks opens the Begin Reconciliation dialog box and automatically selects the active bank account.

The date of the previous reconciliation appears to the right of the Account box. (No date appears if you’re reconciling the account for the first time.) QuickBooks fills in the Statement Date box with a date one month after the previous reconciliation date. If that date doesn’t match your bank statement’s ending date, type the date from you bank statement in the Statement Date box.

In the Ending Balance box, type the ending balance from your bank statement.

If you turned on multiple currencies, the account currency appears to the right of the Beginning Balance and Ending Balance labels. For a foreign currency account, enter the ending balance in the foreign currency, which is the ending balance that appears on your bank statement.

If your bank levies a service charge on your account, in the Service Charge box, type the service charge amount. If you download transactions from your bank, leave this box blank.

In the Date box to the left of the Service Charge box, choose the date that the service charge was assessed. In the Account box, choose the account to which you want to post the charge (usually Bank Service Charges or something similar). QuickBooks creates a transaction for you.

If you’re reconciling an account that pays interest, in the Interest Earned box, type the interest you earned from the bank statement.

As you did for service fees, specify the date and the account that you use to track interest you earn.

Note

If you track service fees and interest earned by class, in the Class boxes, choose the appropriate class. For example, classes might apply if you use them to track performance by region. However, if you use classes to track sales by partner, you don’t have to specify a class for interest earned.

Click Continue to start reconciling individual transactions.

QuickBooks opens the Reconcile window, where you reconcile the individual transactions, as described in the next section.

Reconciling Transactions

The Reconcile window groups payments and charges (items that reduce your balance) on the left side and deposits and other credits on the right side. Marking transactions as cleared is a matter of toggling transaction checkmarks on and off, as you can see in Figure 15-8.

Note

Initially, QuickBooks sorts transactions by date with the earliest transactions first. If you want to sort the transactions by another field (for example, Chk # if you’re trying to find the check that’s preventing you from reconciling successfully), click the column heading for that field. An up arrow indicates that the column is sorted in ascending order (smallest to largest values). Click the column heading again to reverse the order (largest to smallest).

Tip

Initially, the Reconcile window lists all uncleared transactions in the account regardless of when they happened. If transactions after the statement ending date are mixed in, you could select unnecessary transactions by mistake. To filter the list to likely candidates for clearing, turn on the “Hide transactions after the statement’s end date” checkbox (at the top-right corner of the window). If you don’t see transactions that appear on your bank statement, turn the checkbox off. You might have created a transaction with the wrong date.

QuickBooks includes several shortcuts for marking a transaction as cleared. See whether any of these techniques simplify your work:

Mark All. If you usually end up clearing most of the transactions in the list, click Mark All to select all the transactions. Then turn off the checkmarks for the transactions that don’t appear on your bank statement. If you were distracted and selected several transactions by mistake, click Unmark All to start over.

Selecting contiguous transactions. Dragging down the checkmark column selects every transaction you pass. This approach isn’t that helpful if you compare one transaction at a time or if your transactions don’t appear in the same order as those on your bank statement.

Online account access. Click Matched to automatically clear the transactions that you’ve already matched from your QuickStatement (see Chapter 22). Enter the ending date from the printed statement, and then click OK.

When the Difference value changes to 0.00, your reconciliation is a success. To officially complete the reconciliation, click Reconcile Now. The Select Reconciliation Report dialog box opens. If you don’t want to print a reconciliation report, simply click Close.

Reconciliation Reports

After you click Reconcile Now in the Reconcile window, you might notice a short delay while QuickBooks generates your reconciliation reports. These reports come in handy as a benchmark when you try to locate discrepancies in a future reconciliation.

When the Select Reconciliation Report dialog box opens, you can display or print reconciliation reports (or skip them by clicking Close, if you want). Choose the Summary option for a report that provides the totals for the checks and payments you made and also for the deposits and credits you received. To save the reports for future reference, click Print. Click Cancel to close the dialog box without printing or viewing the reports. You can look at them later by choosing Reports → Banking → Previous Reconciliation. Figure 15-9 shows you what a detailed reconciliation report looks like.

Modifying Transactions During Reconciliation

QuickBooks immediately updates the Reconcile window with changes you make in the account register window, so it’s easy to complete a reconciliation. Missing transactions? Incorrect amounts? Other discrepancies? No problem. You can jump to the register window and make your changes. When you click the Reconcile window, the changes are there.

Tip

If you can see the register window and the reconciliation window at the same time, click the one you want to work on. If the Open Windows list appears in the navigation bar on the left side of the QuickBooks window (choose View → Open Window List), you can click names there to change the active window or dialog box.

Here’s how to make changes while reconciling:

Adding transactions. If a transaction appears on your bank statement but isn’t in QuickBooks, switch to the account register window and add the transaction (Opening a Register Window).

Deleting transactions. If you find duplicate transactions, in the account register window, select the transaction and press Ctrl+D. You have to confirm your decision before the program deletes the transaction. The Reconcile window removes the transaction if you delete it.

Editing transactions. If you notice an error in a transaction, in the Reconcile window, double-click the transaction to open the corresponding window (Write Checks for checks, Make Deposits for deposits, Transfer Funds Between Accounts for transfers, and so on). Correct the mistake and save the transaction by clicking Record or Save, depending on the window.

Stopping and Restarting a Reconciliation

If your head hurts and you want to take a break, don’t worry about losing the reconciliation work you’ve already done. Here’s how to stop and restart a reconciliation:

In the Reconcile window, click Leave.

Although QuickBooks closes the window, it remembers what you’ve cleared. In the account register window, you’ll see asterisks in the checkmark column for transactions that you’ve marked, which indicates that your clearing of a transaction is pending.

When you’re re-energized, open the account register window, right-click it, and then choose Reconcile on the shortcut menu.

The Begin Reconciliation dialog box opens with the ending balance, service charge, and interest amounts already filled in.

Click Continue.

The transactions you marked are, happily, still marked. Pick up where you left off by marking the rest of the transactions that cleared on your bank statement.

Correcting Discrepancies

If you modify a transaction that you’ve already reconciled, QuickBooks should freak out and wave a clutch of red flags at you. After all, if you cleared a transaction because it appeared on your bank statement, the transaction is complete, and changing it in QuickBooks doesn’t change it in your bank account. Yet QuickBooks lets you change or delete cleared transactions.

But make no mistake: changing previously cleared transactions is the quickest way to create mayhem when reconciling your accounts. For example, in the account register window, clicking a checkmark cell resets the status of that transaction from reconciled (a checkmark) to cleared (an asterisk), which then removes that transaction’s amount from the Beginning Balance when you try to reconcile the account. And that means that the Beginning Balance won’t match the beginning balance on your bank statement, which is one reason you might be reading this section.

The Discrepancy Report

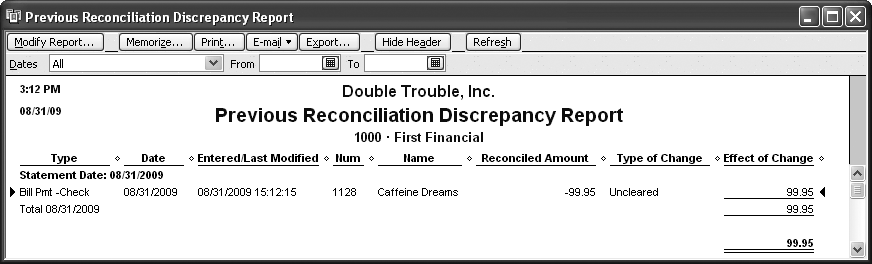

To correct discrepancies created by transaction editing, you have to restore each modified transaction to its original state, and the Discrepancy Report provides the information you need to know to do that. The Discrepancy Report (Figure 15-10) shows you changes that were made to cleared transactions. To create the Discrepancy Report, in the Reconcile window, click Locate Discrepancies, and then, in the Locate Discrepancies window, click Discrepancy Report. You can also choose Reports → Banking → Reconciliation Discrepancy.

Seeing transactions on the Discrepancy Report is a big step toward correcting reconciliation problems. Here’s how you interpret the crucial columns in the report:

Entered/Last Modified. This is the date that the transaction was created or modified, which doesn’t help you restore the transaction, but might help you find the person who’s changing reconciled transactions.

Reconciled Amount. This is the transaction amount when you cleared it during reconciliation. If the transaction amount changed, use this value to restore the transaction amount to its original value. For example, in Figure 15-10, –99.95 represents a check or charge for $99.95.

Type of Change. This indicates the transaction change. For example, “Amount” means that the transaction amount changed. “Deleted” indicates that the transaction was deleted. (The only way to restore a deleted transaction is to recreate it from scratch.) “Uncleared” indicates that someone removed the reconciled checkmark in the account register.

Effect of Change. This value indicates how the change affected the beginning balance for your reconciliation. For example, the $99.95 check that was reset added $99.95 to your bank account. When the Beginning Balance is off and the amount in the “Effect of Change” column matches that discrepancy, you can be sure that restoring these transactions to their original state will fix your problems.

Other ways to find discrepancies

Sometimes, your reconciliation doesn’t match because of subtle errors in transactions or because you’ve missed something in the current reconciliation. Try the following techniques to help spot problems:

Search for a transaction equal to the amount of the discrepancy. Press Ctrl+F to open the Find window. In the Choose Filter list, choose Amount. Select the = option and type the amount in the box, and then click Find to run the search.

Note

Using Find in this way works only if the discrepancy is caused by one transaction that you cleared or uncleared by mistake. If more than one transaction is to blame for the discrepancy, the amount you’re trying to find is the total of all the erroneously cleared transactions, so Find won’t see a matching value.

Look for transactions cleared or uncleared by mistake. Sometimes, the easiest way to find a discrepancy is to start the reconciliation over. In the Reconcile window, click Unmark All to remove the checkmarks from all the transactions. Then, begin checking them off as you compare them to your bank statement. Make sure that every transaction on the bank statement is cleared in the Reconcile window. Also, check that no additional transactions are cleared in the Reconcile window.

Look for duplicate transactions. If you create transactions in QuickBooks and download transactions, it’s easy to end up with duplicates. And when you clear both of the duplicates, the mistake is hard to spot. If that’s the case, you have to scroll through the register window looking for multiple transactions with the same date, payee, and amount.

Tip

Count the number of transactions on your bank statement. Compare that number to the number of cleared transactions displayed on the left side of the Reconcile window, shown in Figure 15-8. Of course, this transaction count won’t help if you enter transactions in QuickBooks differently than they appear on your bank statement. For example, if you deposit every payment individually but your bank shows one deposit for every business day, your transaction counts won’t match.

Look for a deposit entered as a payment or vice versa. To find an error like this, look for transactions whose amounts are half the discrepancy. For example, if a $500 check becomes a $500 deposit by mistake, your reconciliation will be off by $1000 ($500 because a check is missing and another $500 because you have an extra deposit).

Look at each cleared transaction for transposed numbers or other differences between your statement and QuickBooks. It’s easy to type $95.40 when you meant $59.40.

Note

If these techniques don’t uncover the problem, your bank might have made a mistake (When Your Bank Makes a Mistake).

Undoing the Last Reconciliation

If you’re having problems with this month’s reconciliation but suspect that the guilty party is hiding in last month’s reconciliation, you can undo the last reconciliation and start over. When you undo a reconciliation, QuickBooks returns the transactions to an uncleared state.

In the Begin Reconciliation dialog box (choose Banking → Reconcile), click Undo Last Reconciliation. The Undo Previous Reconciliation dialog box opens. Although the button label and the dialog box title don’t match, they both represent the same process. In the Undo Previous Reconciliation dialog box, click Continue. When the Undo Previous Reconciliation message box appears telling you that the previous reconciliation was successfully undone, click OK.

QuickBooks unclears all the transactions back to the beginning of the previous reconciliation and returns to the Begin Reconciliation dialog box. Change the values in the Begin Reconciliation dialog box, and then click Continue to try another reconciliation.

Note

Although QuickBooks removes the cleared status on all the transactions including service charges and interest, it doesn’t remove the service charge and interest transactions that it added. When you restart the reconciliation, in the Begin Reconciliation dialog box, don’t re-enter the service charges or interest.

When Your Bank Makes a Mistake

Banks do make mistakes. Digits get transposed, or amounts are flat wrong. When this happens, you can’t ignore the difference. In QuickBooks, add an adjustment transaction (Reconciling Transactions) to make up the difference, but be sure to tell your bank about the mistake. It’s always a good idea to be polite in case the error turns out to be yours.

When you receive your next statement, check that the bank made an adjustment to correct its mistake. You can delete your adjustment transaction or add a reversing journal entry to remove your adjustment and reconcile as you normally would.

Managing Loans

Unless your business generates cash at an astonishing rate, you’ll probably have to borrow money to purchase big ticket items that you can’t afford to do without, such as a deluxe cat-herder machine. The asset you purchase and the loan you assume are intimately linked—you can’t get the equipment without borrowing the money.

But in QuickBooks, loans and the assets they help purchase aren’t connected in any way. You create an asset account (Creating an Account) to track the value of an asset that you buy. If you take out a loan to pay for that asset, you create a liability account to track the balance of what you owe on the loan. With each payment that you make on your loan, you pay off a little bit of the loan’s principal as well as a chunk of interest.

Note

On your company’s balance sheet, the value of your assets appears in the Assets section, and the balance owed on loans shows up in the Liabilities section. The difference between the asset value and your loan balance is your equity in the asset. Suppose your cat-herder machine is in primo condition and is worth $70,000 on the open market. If you owe $50,000 on the loan, your company has $20,000 in equity for that machine.

Most loans amortize your payoff, which means that each payment represents a different amount of interest and principal. In the beginning of a loan, amortized loan payments are mostly interest and very little principal, which is great for tax deductions. By the end, the payments are almost entirely principal. Making loan payments in which the values change each month would be a nightmare if not for QuickBooks’ Loan Manager, which is a separate program that comes with QuickBooks and can gather information from your company file. This program calculates your loan amortization schedule, posts the principal and interest for each payment to the appropriate accounts, and handles escrow payments and fees associated with your loans.

Note

Loan Manager doesn’t handle loans in which the payment covers only the accrued interest (called interest-only loans). For loans like these, you have to set up payments yourself (Entering Bills) and allocate the payment to principal and interest using the values on your monthly loan statement.

Setting Up a Loan

Whether you use Loan Manager or not, you have to create accounts to keep track of your loan. You probably already know that you need a liability account for the amount of money you owe. But you also need accounts for the interest you pay on the loan and escrow payments (such as insurance or property tax) that you make:

Liability account. Create a liability account (Creating an Account) to track the money you’ve borrowed. For mortgages and other loans whose terms are longer than a year, use the Long Term Liability type. For short-term loans (terms of one year or less), use the Other Current Liability type.

When you create the liability account, add the account number but forego the opening balance. The best way to record money you borrow is with a journal entry (Creating General Journal Entries), which credits the liability account for the loan and debits the bank account where you deposited the money.

Loan interest account. The interest that you pay on loans is an expense, so create an Expense account (or an Other Expense account type if that’s the type of account your company uses for interest paid) called something like Interest Paid. Loan Manager shows Other Expense account types in its account drop-down lists, although the accounts are listed in alphabetical order, not by type.

Escrow account. If you make escrow payments, such as for property taxes and insurance, create an account to track the escrow you’ve paid. Because escrow represents money you’ve paid in advance, use a Current Asset account type.

Fees and finance charge expense account. Chances are you’ll pay some sort of fee or finance charge at some point before you pay off a loan. If you don’t have an account for finance charges yet, set up an Expense account for these fees.

There’s one last QuickBooks setup task to complete before you start Loan Manager: You have to create the lender in your Vendor List (Entering Address Information). The box below tells you what to do if you forgot any of these steps before you started Loan Manager.

Adding a Loan to Loan Manager

Loan Manager makes it so easy to track and make payments on amortized loans, it’s well worth the steps required to set it up. Before you begin, gather your loan documents like chicks to a mother hen, because Loan Manager wants to know every detail of your loan, as you’ll soon see.

Basic setup

With your account and vendor entries complete (see Setting Up a Loan and the box above), follow these steps to describe your loan:

Choose Banking → Loan Manager.

QuickBooks opens the Loan Manager window.

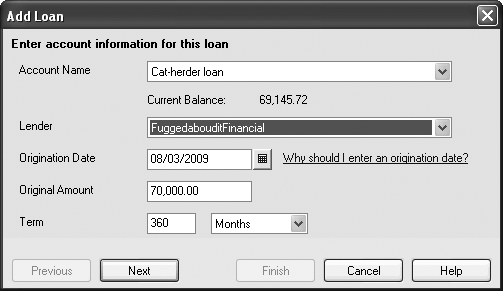

In the Loan Manager window, click “Add a Loan”.

QuickBooks opens the Add Loan dialog box, which has several screens for all the details of your loan. After you fill in a screen, click Next to move to the next one.

In the Account Name drop-down list, choose the liability account you created for the loan.

QuickBooks lists only Current Liability and Long Term Liability accounts.

In the Lender drop-down list, choose the vendor you created for the company you’re borrowing money from.

If you haven’t set up the lender as a vendor in QuickBooks, you have to close Loan Manager. After you’ve created the vendor in QuickBooks, choose Banking → Loan Manager to restart the Loan Manager program, which now shows the lender in the Lender drop-down list.

In the Origination Date box, choose the date that matches the origination date on your loan documents.

Loan Manager uses the loan origination date to calculate the number of remaining payments, the interest you owe, and when you’ll pay off the loan.

In the Original Amount box, type the total amount you borrowed when you first took out the loan.

The Original Amount box is aptly named because it’s always the amount that you originally borrowed. For new loans, the current balance on the loan and the Original Amount are the same. If you’ve paid off a portion of a loan, your current balance (below the Account Name box in Figure 15-11) is lower than the Original Amount.

In the Term boxes, specify the length of the loan. Click Next to advance to the screen for payment information.

The next section tells you how to deal with payment info.

Payment information

When you specify a few details about your loan payments, Loan Manager can calculate a schedule of payments for you. To make sure you don’t forget a loan payment (and incur outrageous late charges), you can tell Loan Manager to create a QuickBooks reminder for your payments. Here’s how:

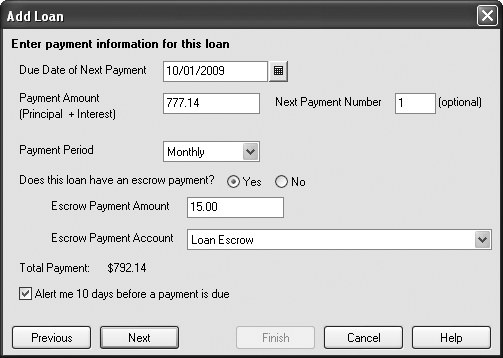

In the “Due Date of Next Payment” box, choose the next payment date.

For a new loan, choose the date for the first payment you’ll make. For an existing loan, choose the date for your next payment, which usually appears on your last loan statement.

In the Payment Amount box, type the total payment for principal and interest.

If you don’t know what your payment is, you can find it in your loan documents. Loan Manager automatically fills in the Next Payment Number box with the number 1. For loans that you’ve made payments on already, type the number for the next payment (this, too, should appear on your last loan statement).

In the Payment Period drop-down list, choose the frequency of your payments.

Loans typically require monthly payments, even when their terms are in years. Regardless of which period you chose on the first Add Loan screen in the Term drop-down list, in the Payment Period drop-down list, choose how often you make loan payments.

If your loan includes an escrow payment, choose the Yes option.

Then specify the amount of escrow you pay each time and the account to which you want to post the escrow, as shown in Figure 15-12.

Figure 15-12. Most mortgages include an escrow payment for property taxes and property insurance. Escrow accounts are asset accounts, because you’re setting aside some money to pay expenses later. When you add an escrow payment, Loan Manager updates the value of the Total Payment to include principal, interest, and escrow.If you want a reminder 10 days before a loan payment is due, turn on the “Alert me 10 days before a payment is due” checkbox.

Loan Manager tells QuickBooks how often and when payments are due, so QuickBooks can create a loan payment reminder in the Reminders List (Reminders).

Click Next to advance to the screen for entering interest rate information.

The next section tells you how to deal with interest rate info.

Interest rate information

For Loan Manager to calculate your amortization schedule (the amount of principal and interest paid with each payment) you have to specify the interest rate. Here’s how:

In the Interest Rate box, type the interest rate for the loan.

Use the interest rate that appears on your loan documents. For example, although you probably make monthly payments, the loan document usually shows the interest rate as an annual rate.

In the Compounding Period box, choose either Monthly or Exact Days, depending on how the lender calculates compounding interest.

If the lender calculates the interest on your loan once a month, choose Monthly. The other option, Exact Days, calculates interest using the annual interest rate divided over a fixed number of days in a year. In the past, many lenders simplified calculations by assuming that a year had 12 months of 30 days each, resulting in the Compute Period choice 365/360. Today, lenders often use the number of days in a year, which is the Compute Period 365/365.

In the Payment Account drop-down list, choose the account from which you make your payments, whether you write checks or pay electronically.

In the Payment Account drop-down list, Loan Manager displays your bank accounts.

In the Interest Expense Account drop-down list, choose the account you use to track the interest you pay. In the Fees/Charges Expense Accounts drop-down list, choose the account you use for fees and late charges you pay.

Expense accounts and Other Expense accounts are co-mingled in these drop-down lists, because accounts appear in alphabetical order, not sorted by account type.

Click Finish.

Loan Manager calculates the payment schedule for the loan and adds it to the list of loans in the Loan Manager window, shown in Figure 15-13.

Note

If Loan Manager shows the loan balance as zero, you aren’t off the hook for paying back the loan. Loan Manager grabs the loan balance from the QuickBooks liability account you created for the loan. The loan balance in Loan Manager is zero if you forgot to create the journal entry to set the liability account’s opening balance.

Modifying Loan Terms

Some loan characteristics change from time to time. For example, if you have an adjustable-rate mortgage, the interest rate changes every so often. And your escrow payment usually increases as your property taxes and insurance go up. To make changes like these, in the Loan Manager window (choose Banking → Loan Manager), select the loan, and then click Edit Loan Details.

Loan Manager takes you through the same screens you saw when you first added the loan. If you change the interest rate, the program recalculates your payment schedule. For a change in escrow, the program updates your payment to include the new escrow amount.

Setting Up Payments

You can set up a loan payment check or bill in Loan Manager, which hands off the payment info to QuickBooks to record in your company file. Although Loan Manager can handle this task one payment at a time, it can’t create recurring payments to send the payment that’s due each month. When you see the QuickBooks reminder for your loan payment, you have to run Loan Manager to generate the payment:

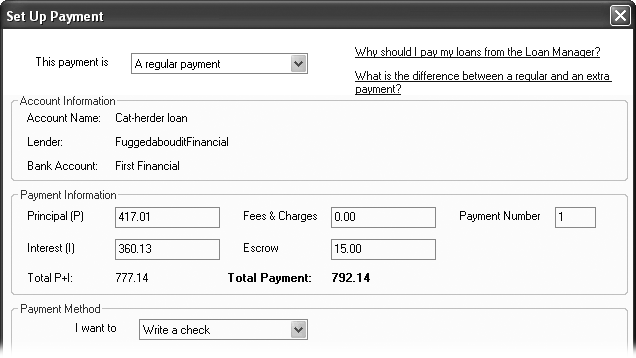

In the Loan Manager window, select the loan you want to pay, and then click Set Up Payment.

Loan Manager opens the Set Up Payment dialog box and fills in the information for the next payment, as you can see in Figure 15-14.

Tip

If you want to make an extra payment, in the “This payment is” drop-down list, choose “An extra payment”. Because extra payments aren’t a part of the loan payment schedule, Loan Manager changes the values in the Principal (P), Interest (I), Fees & Charges, and Escrow boxes to zero. If you want to prepay principal on your loan, type the amount that you want to prepay in the Principal (P) box. Or, if you want to pay an annual fee, fill in the Fees & Charges box.

In the Payment Method drop-down list at the bottom of the window, choose “Write a check” or “Enter a bill”, and then click OK.

Loan Manager opens the QuickBooks Write Checks or Enter Bills window, respectively, and fills in the boxes with the payment information. You can change the payment date or other values if you want.

In the QuickBooks Write Checks or Enter Bills window, click Save & Close.

The window in QuickBooks closes and you’re back in the Loan Manager window. You’ll see the value in the loan’s Balance cell reduced by the amount of principal that the payment paid off. Click Close.

If you want to print the payment schedule for your loan, in the Loan Manager window, click Print. Or, if you pay off a loan and want to remove it from Loan Manager, select the loan, and then click Remove Loan. Removing a loan from Loan Manager doesn’t delete any loan transactions or loan accounts in QuickBooks.

Note

If your loan payments include escrow, each payment deposits the escrow amount into your QuickBooks escrow asset account. When your loan statement shows that the lender paid expenses from escrow—like insurance or property taxes—you can record the corresponding payment in QuickBooks. Open the escrow account register window (Opening a Register Window). In the first blank transaction, choose the date and the payee, such as the insurance company or the tax agency. In the Decrease field, type the payment amount (because the payment reduces the balance in the escrow account). Click Record.

What-If Scenarios

Because economic conditions and interest rates change, loans aren’t necessarily stable things. For example, if you have an adjustable-rate loan, you might want to know what your new payment is. Or, you might want to find out whether it makes sense to refinance an existing loan when interest rates drop. The What-If Scenarios button is your dry-erase board for trying out loan changes before you make up your mind.

When you click What-If Scenarios, Loan Manager opens the What-If Scenarios dialog box. Take your pick from these five scenarios:

Note

The changes you make in the What-If Scenarios dialog box don’t change your existing loans. If you switch to a different scenario or close the dialog box, Loan Manager doesn’t save the information. If you want a record of different scenarios, click the Print button.

What if I change my payment amount? Paying extra principal can shorten the length of your loan and reduce the total interest you pay. Choose this scenario and then, in the Payment Amount box on the right side of the dialog box, type the new amount you plan to pay each month. When you click Calculate, Loan Manager calculates your new maturity date, shows how much you’ll pay overall, and how much you’ll pay in interest.

What if I change my interest rate? If you have an adjustable-rate loan, choose this scenario to preview the changes in payment, interest, and balloon payment for a different rate, higher or lower.

How much will I pay with a new loan? You don’t have to go through the third degree to see what a loan will cost. Choose this scenario to quickly enter the key information for a loan and evaluate the payment, total payments, total interest, and final balloon payment.

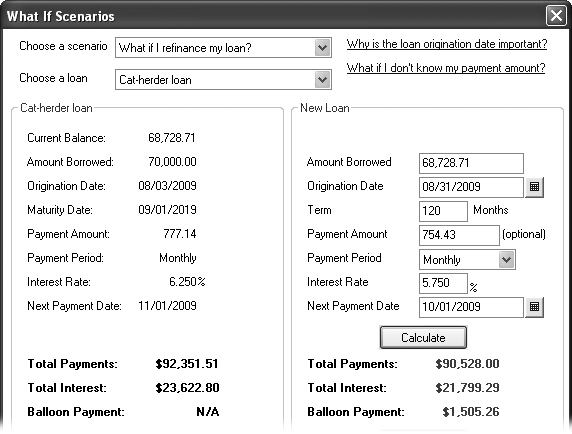

What if I refinance my loan? When interest rates drop, companies and individuals alike consider refinancing their debt to save money on interest. With this scenario, type in a new term, payment, interest rate, and payment date to see whether it’s worth refinancing, as shown in Figure 15-15.

Evaluate two new loans. Type in the details for two loans to see which one is better.

Tracking Petty Cash

Dashing out to buy an extension cord so you can present a pitch to a potential client? Chances are you’ll get money from the petty cash drawer at your office. Petty cash is the familiar term for money spent on small purchases, typically less than $20.

Many companies keep a cash drawer at the office and dole out dollars for small, company-related purchases that employees make. But for the small business owner with a bank card, getting petty cash is as easy as withdrawing money from an ATM. Either way, petty cash is still company money. And that means you have to keep track of it and how it’s spent.

Recording ATM Withdrawals and Deposits to Petty Cash

In QuickBooks, adding money to your petty cash account mirrors the real world transaction. You either write a check made out to Cash (or the trustworthy employee who’s cashing the check), or you withdraw money from an ATM. To write a check for your petty cash account, you can simply open the Write Checks window (choose Banking → Write Checks or, on the Home page, click Write Checks). Withdrawing cash from an ATM requires the Transfer Funds window (choose Banking → Transfer Funds).

If creating transactions in the account register window (Opening a Register Window) is OK with you, you can use the same steps whether you replenish your petty cash with a check or ATM withdrawal:

In the Chart of Accounts window (press Ctrl+A to open it), double-click your checking account to open the register window.

If the current date (which QuickBooks fills in automatically) isn’t the day you added money to petty cash, choose the correct date.

If you’re withdrawing money from an ATM, clear the value in the Number cell.

If you’re writing a check to get petty cash and QuickBooks fills in the Number cell with the correct check number, continue to the Payee cell. Otherwise, type the correct check number in the cell.

Whether you’re writing a check or using an ATM, in the Payee cell, type a name such as Cash or Petty Cash.

If you made a check out to one of your employees, in the Payee cell drop-down list, choose the employee’s name.

In the Payment cell, type the amount that you’re moving from the checking account to petty cash.

If you track classes in QuickBooks, this is one time to ignore the Class cell. You assign classes only when you record purchases made with petty cash.

In the Account cell, choose your petty cash account.

If you don’t have a petty cash account in your chart of accounts, be sure to choose the Bank type when you create the account. When you do so, your petty cash account appears at the top of your balance sheet with your other savings and checking accounts.

Click Record to save the transaction.

That’s it!

Recording Purchases Made with Petty Cash

As long as company cash sits in the petty cash drawer or your wallet, the petty cash account in QuickBooks holds the cash. But when you spend some of the petty cash in your wallet or an employee brings in a sales receipt for purchases, you have to record what that petty cash purchased.

The petty cash account register is as good a place as any to record these purchases. In the Chart of Accounts window, double-click the petty cash account to open its register window. Then, in a blank transaction, follow these guidelines to record your petty cash expenditures:

Number cell. Although petty cash expenditures don’t use check numbers, QuickBooks automatically fills in the Number cell with the next check number anyway. The easiest thing to do is ignore the number and move on to the Payee or Payment cell.

Payee cell. QuickBooks doesn’t require a value in the Payee cell, and for many petty cash transactions, entering a Payee would just clog your lists of names, so leave the Payee cell blank. You can type the vendor name or details of the purchase in the Memo cell if you want a record of it.

Payment cell. In the Payment cell, type the amount that was spent.

Account cell. Choose an account to track the expense.

Note

To distribute the petty cash spent to several accounts, click Splits. In the table that appears, you can specify the account, amount, customer or job, class, and a memo for each split (Entering Bills).