Module 38: Corporate Taxation

Overview

This module covers corporate taxation and reviews the rules that apply throughout the life cycle of a corporation. The tax consequences of corporate formation are covered first, followed by a review of some of the special rules that apply to the income and deductions of a corporation, including the charitable contributions deduction and the dividends received deduction. The Schedule M-1 reconciliation of book income to taxable income, and the tax concepts of affiliated and controlled groups are next reviewed. This is followed by a review of the tax treatment of corporate distributions to shareholders and their taxability as dividends. Next reviewed are the tax consequences of a complete liquidation, as well as the accumulated earnings and personal holding company penalty taxes. The module then continues with a review of the special rules that apply to S corporations and their shareholders, and the tax effects of corporate reorganizations. The module concludes with a comparison of C corporations, S corporations, and partnerships.

I. Corporations

A. Transfers to a Controlled Corporation (Sec. 351)

B. Section 1244–Small Business Corporation (SBC) Stock

C. Variations from Individual Taxation

D. Affiliated and Controlled Corporations

E. Dividends and Distributions

F. Personal Holding Company and Accumulated Earnings Taxes

G. S Corporations

H. Corporate Reorganizations

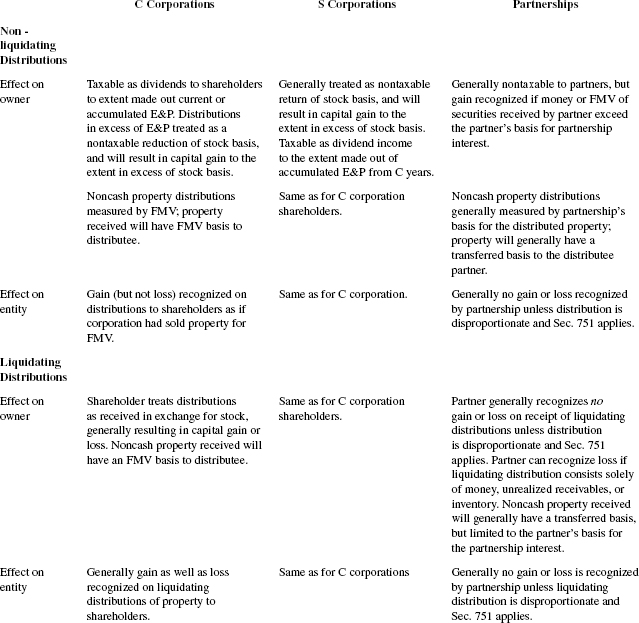

II. Comparison of C Corporations, S Corporations, and Partnerships

Key Terms

Multiple-Choice Questions

Multiple-Choice Answers and Explanations

Simulations

Simulation Solutions

I. CORPORATIONS

Corporations are separate taxable entities, organized under state law. Although corporations may have many of the same income and deduction items as individuals, corporations are taxed at different rates and some tax rules are applied differently. There also are special provisions applicable to transfers of property to a corporation, and issuance of stock.

A. Transfers to a Controlled Corporation (Sec. 351)

1.

No gain or loss is recognized if property is transferred to a corporation solely in exchange for stock and immediately after the exchange those persons transferring property control the corporation.

a. Property includes everything but services.

b. Control means ownership of at least 80% of the total combined voting power and 80% of each class of nonvoting stock.

c.

Receipt of boot (e.g., cash, short-term notes, securities, etc.) will cause recognition of gain (but not loss).

(1) Corporation’s assumption of liabilities is treated as boot only if there is a tax avoidance purpose, or no business purpose.

(2) Shareholder recognizes gain if liabilities assumed by corporation exceed the total basis of property transferred by the shareholder.

2.

Shareholder’s basis for stock = Adjusted basis of property transferred

a. + Gain recognized

b. − Boot received (assumption of liability always treated as boot for purposes of determining stock basis)

3.

Corporation’s basis for property = Transferor’s adjusted basis + Gain recognized to transferor.

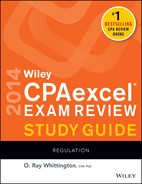

EXAMPLE

Individuals A, B, & C form ABC Corp. and make the following transfer to their corporation:

a. If the aggregate adjusted basis of transferred property exceeds its aggregate FMV, the corporate transferee’s aggregate basis for the property is generally limited to its aggregate FMV immediately after the transaction. Any required basis reduction is allocated among the transferred properties in proportion to their built-in loss immediately before the transaction.

b. Alternatively, the transferor and the corporate transferee are allowed to make an irrevocable election to limit the basis in the stock received by the transferor to the aggregate FMV of the transferred property.

EXAMPLE

Amy transferred Lossacre with a basis of $6,000 (FMV of $2,000) and Gainacre with a basis of $4,000 (FMV of $5,000) to ABE Corp. in exchange for stock in a Sec. 351 transaction. Since the aggregate adjusted basis of the transferred property ($10,000) exceeds its aggregate FMV ($7,000), ABE’s aggregate basis for the property is limited to $7,000. The required basis reduction of $3,000 would reduce ABE’s basis for Lossacre to $3,000 ($6,000 − $3,000). Amy’s basis for her stock would equal the total basis of the transferred property, $10,000.

Alternatively, if Amy and ABE elect, ABE’s basis for the transferred property will be $6,000 for Lossacre and $4,000 for Gainacre, and Amy’s basis for her stock will be limited to its FMV of $7,000.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 1 THROUGH 7

B. Section 1244–Small Business Corporation (SBC) Stock

1. Sec. 1244 stock permits shareholders to deduct an

ordinary loss on sale or worthlessness of stock.

a. Shareholder must be the original holder of stock, and an individual or partnership.

b. Stock can be common or preferred, voting or nonvoting, and must have been issued for money or property (other than stock or securities)

c. Ordinary loss limited to $50,000 ($100,000 on joint return); any excess is treated as a capital loss.

d. The corporation during the five-year period before the year of loss, received less than 50% of its total gross receipts from royalties, rents, dividends, interest, annuities, and gains from sales or exchanges of stock or securities.

EXAMPLE

Jim (married and filing a joint return) incurred a loss of $120,000 from the sale of Sec. 1244 stock during 2013. $100,000 of Jim’s loss is deductible as an ordinary loss, with the remaining $20,000 treated as a capital loss.

2. If Sec. 1244 stock is received in exchange for property whose FMV is less than its adjusted basis, the stock’s basis is reduced to the FMV of the property to determine the amount of ordinary loss.

EXAMPLE

Joe made a Sec. 351 transfer of property with an adjusted basis of $20,000 and an FMV of $16,000 in exchange for Sec. 1244 stock. The basis of Joe’s stock is $20,000, but solely for purposes of Sec. 1244 the stock’s basis is reduced to $16,000. If Joe subsequently sold his stock for $15,000, $1,000 of his loss would be treated as an ordinary loss under Sec. 1244, with the remaining $4,000 treated as a capital loss.

3. For purposes of determining the amount of ordinary loss, increases in basis through capital contributions or otherwise are treated as allocable to stock which is not Sec. 1244 stock.

EXAMPLE

Jill acquired 100 shares of Sec. 1244 stock for $10,000. Jill later made a $2,000 contribution to the capital of the corporation, increasing her stock basis to $12,000. Jill subsequently sold the 100 shares for $9,000. Of Jill’s $3,000 loss, ($10,000 ÷ $12,000) × $3,000 = $2,500 qualifies as an ordinary loss under Sec. 1244, with the remaining ($2,000 ÷ $12,000) × $3,000 = $500 treated as a capital loss.

4. SBC is any domestic corporation whose aggregate amount of money and adjusted basis of other property received for stock, as a contribution to capital, and as paid-in surplus, does not exceed $1,000,000. If more than $1 million of stock is issued, up to $1 million of qualifying stock can be designated as Sec. 1244 stock.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 8 THROUGH 11

C. Variations from Individual Taxation

1. Filing and payment of tax

a. A corporation generally must file a Form 1120 every year even though it has no taxable income. A short-form Form 1120-A may be filed if gross receipts, total income, and total assets are each less than $500,000.

b. The return must be filed by the fifteenth day of the third month following the close of its taxable year (e.g., March 15 for calendar-year corporation).

(1) An automatic six-month extension may be obtained by filing Form 7004.

(2) Any balance due on the corporation’s tax liability must be paid with the request for extension.

c. Estimated tax payments must be made by every corporation whose estimated tax is expected to be $500 or more. A corporation’s estimated tax is its expected tax liability (including alternative minimum tax) less its allowable tax credits.

(1) Quarterly payments are due on the fifteenth day of the fourth, sixth, ninth, and twelfth months of its taxable year (April 15, June 15, September 15, and December 15 for a calendar-year corporation). Any balance due must be paid by the due date of the return.

(2) No penalty for underpayment of estimated tax will be imposed if payments at least equal the lesser of

(a) 100% of the current year’s tax (determined on the basis of actual income or annualized income), or

(b) 100% of the preceding year’s tax (if the preceding year was a full twelve months and showed a tax liability).

(3) A corporation with $1 million or more of taxable income in any of its three preceding tax years (i.e., large corporation) can use its preceding year’s tax only for its first installment and must base its estimated payments on 100% of its current year’s tax to avoid penalty.

(4) If any amount of tax is not paid by the original due date, interest must be paid from the due date until the tax is paid.

(5) A failure-to-pay tax delinquency penalty will be owed if the amount of tax paid by the original due date of the return is less than 90% of the tax shown on the return. The failure-to-pay penalty is imposed at a rate of 0.5% per month (or fraction thereof), with a maximum penalty of 25%.

2. Corporations are subject to

a.

Regular tax rates

|

Taxable income |

Rate |

| (1) |

$0–$50,000 |

15% |

| (2) |

$50,001–$75,000 |

25 |

| (3) |

$75,001–$10 million |

34 |

| (4) |

Over $10 million |

35 |

(5) The less-than-34% brackets are phased out by adding an additional tax of 5% of the excess of taxable income over $100,000, up to a maximum additional tax of $11,750.

(6) The 34% bracket is phased out for corporations with taxable income in excess of $15 million by adding an additional 3% of the excess of taxable income over $15 million, up to a maximum additional tax of $100,000.

b. Certain personal service corporations are not eligible to use the less-than-35% brackets and their taxable income is taxed at a flat 35% rate.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 12 THROUGH 20

c.

Alternative minimum tax (AMT)

(1) Computation. The AMT is generally the amount by which 20% of alternative minimum taxable income (AMTI) as reduced by an exemption and the alternative minimum tax foreign tax credit, exceeds the regular tax (i.e., regular tax liability reduced by the regular tax foreign tax credit). AMTI is equal to taxable income computed with specified adjustments and increased by tax preferences.

(2) Exemption. AMTI is offset by a $40,000 exemption. However, the exemption is reduced by 25% of AMTI over $150,000, and completely phased out once AMTI reaches $310,000.

(3)

AMT formula

| + |

Regular taxable income before Net Operation Loss (NOL) deduction

Tax preference items |

| +(–) |

Adjustments other than Adjusted Current Earnings (ACE) and NOL deduction |

| |

Pre-ACE AMTI |

| +(–) |

ACE adjustment (75% of difference between pre-ACE AMTI and ACE) |

| – |

AMT NOL deduction (limited to 90% of pre-NOL AMTI) |

| – |

AMTI

Exemption ($40,000 less 25% of AMTI over $150,000) |

| × |

Alternative minimum tax base

20% rate |

| – |

Tentative AMT before foreign tax credit

AMT foreign tax credit |

| – |

Tentative minimum tax (TMT)

Regular income tax (less regular tax foreign tax credit) |

|

Alternative minimum tax (if positive) |

(4) Preference items. The following are examples of items added to regular taxable income in computing pre-ACE AMTI:

(a) Tax-exempt interest on private activity bonds (net of related expenses). However, tax-exempt interest on private activity bonds issued in 2009 and 2010 is not an item of tax preference.

(b) Excess of accelerated over straight-line depreciation on real property and leased personal property placed in service before 1987

(c) The excess of percentage depletion deduction over the property’s adjusted basis

(d) The excess of intangible drilling costs using a ten-year amortization over 65% of net oil and gas income

(5)

Adjustments. The following are examples of adjustments to regular taxable income in computing pre-ACE AMTI:

(a) For real property placed in service after 1986 and before 1999, the difference between regular tax depreciation and straight-line depreciation over forty years

(b) For personal property placed in service after 1986, the difference between regular tax depreciation using the 200% declining balance method and depreciation using the 150% declining balance method

(c) The installment method cannot be used for sales of inventory-type items

(d) Income from long-term contracts must be determined using the percentage of completion method

(6)

Adjusted Current Earnings (ACE). ACE is a concept based on a corporation’s earnings and profits, and is calculated by making adjustments to pre-ACE AMTI.

AMTI before ACE adjustment and NOL deduction

| Add: |

Tax-exempt interest on municipal bonds (less expenses); except not interest on tax-exempt bonds issued in 2009 or 2010.

Tax-exempt life insurance death benefits (less expenses)

70% dividends-received deduction |

| Deduct: |

Depletion using cost depletion method

Depreciation using ADS straight-line for all property (this adjustment eliminated for property placed in service after 1993) |

| Other: |

Capitalize organizational expenditures and circulation expenses

Add increase (subtract decrease) in LIFO recapture amount (i.e., excess of FIFO value over LIFO basis)

Installment method cannot be used for non dealer sales of property

Amortize intangible drilling costs over five years |

| ACE (Adjusted Current Earnings) |

– Pre-ACE AMTI |

| Balance (positive or negative) |

× 75% |

|

ACE adjustment (positive or negative) |

EXAMPLE

Acme, Inc. has adjusted current earnings (ACE) of $100,000 and alternative minimum taxable income (before this adjustment) of $60,000. Since adjusted current earnings exceeds pre-ACE AMTI by $40,000, 75% of this amount must be added to Acme’s AMTI. Thus, Acme’s AMTI before exemption for the year is [$60,000 + ($40,000 × 75%)] = $90,000.

(a) The ACE adjustment can be positive or negative, but a negative ACE adjustment is limited in amount to prior years’ net positive ACE adjustments.

(b) The computation of ACE is not the same as the computation of a corporation’s E&P. For example, federal income taxes, penalties and fines, and the disallowed portion of business meals and entertainment would be deductible in computing E&P, but are not deductible in computing ACE.

(7)

Minimum tax credit. The amount of AMT paid is allowed as a credit against regular tax liability in future years.

(a) The credit can be carried forward indefinitely, but not carried back.

(b) The AMT credit can only be used to reduce regular tax liability, not future AMT liability.

(8) Small corporation exemption. A corporation is exempt from the corporate AMT for its first tax year (regardless of income levels). After the first year, it is exempt from AMT if it passes a gross receipts test. It is exempt for its second year if its first year’s gross receipts do not exceed $5 million. To be exempt for its third year, the corporation’s average gross receipts for the first two years must not exceed $7.5 million. To be exempt for the fourth year (and subsequent years), the corporation’s average gross receipts for all prior three-year periods must not exceed $7.5 million.

EXAMPLE

Zero Corp., a calendar-year corporation, was formed on January 2, 2010, and had gross receipts for its first four taxable years as follows:

| Year |

Gross receipts |

| 2010 |

$ 4,500,000 |

| 2011 |

9,000,000 |

| 2012 |

8,000,000 |

| 2013 |

6,500,000 |

Zero is automatically exempt from AMT for 2010. It is exempt for 2011 because its gross receipts for 2010 do not exceed $5 million. Zero also is exempt for 2012 because its average gross receipts for 2010-2011 do not exceed $7.5 million. Similarly, it is exempt for 2013 because its average gross receipts for 2010–2012 do not exceed $7.5 million. However, Zero will lose its exemption from AMT for 2014 and all subsequent years because its average gross receipts for 2011–2013 exceed $7.5 million.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 21 THROUGH 28

3. Gross income for a corporation is computed much the same as for individual taxpayers. However, there are a few differences.

a. A corporation does not recognize gain or loss on the

issuance of its own stock (including treasury stock), or on the lapse or acquisition of an option to buy or sell its stock (including treasury stock).

(1) It generally recognizes gain (but not loss) if it distributes appreciated property to its shareholders.

(2)

Contributions to capital are excluded from a corporation’s gross income, whether received from shareholders or non shareholders.

(a) If property is received from a shareholder, the shareholder recognizes no gain or loss, the shareholder’s basis for the contributed property transfers to the corporation, and the shareholder’s stock basis is increased by the basis of the contributed property.

(b) If property is received as a capital contribution from a non shareholder, the corporation’s basis for the contributed property is zero.

1] If money is received, the basis of property purchased within one year afterwards is reduced by the money contributed.

2] Any money not used reduces the basis of the corporation’s existing property beginning with depreciable property.

b. No gain or loss is recognized on the

issuance of debt.

(1) Premium or discount on bonds payable is amortized as income or expense over the life of bonds.

(2) Ordinary income/loss is recognized by a corporation on the repurchase of its bonds, determined by the relationship of the repurchase price to the net carrying value of the bonds (issue price plus or minus the discount or premium amortized).

(3) Interest earned and gains recognized in a bond sinking fund are income to the corporation.

c. Gains are treated as ordinary income on sales of property to or from a more than 50% shareholder, or between corporations which are more than 50% owned by the same individual, if the property is subject to depreciation in the hands of the buyer.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 29 THROUGH 33

4. Deductions for a corporation are much the same as for individuals. However, there are some major differences.

a. Adjusted gross income is not applicable to corporations.

b. A corporation may elect to deduct up to $5,000 of

organizational expenditures for the tax year in which the corporation begins business. The $5,000 amount must be reduced (but not below zero) by the amount by which organizational expenditures exceed $50,000. Remaining expenditures can be deducted ratably over the 180-month period beginning with the month in which the corporation begins business.

EXAMPLE

A calendar-year corporation was organized and began business during 2013 incurring $4,800 or organizational expenditures. The corporation may deduct the $4,800 of organizational expenditures for 2013.

EXAMPLE

A calendar-year corporation was organized during February 2013 incurring organizational expenditures of $6,000. Assuming the corporation begins business during April 2013, its maximum deduction for organizational expenditures for 2013 would be $5,000 + [($6,000 − $5,000) × 9/180] = $5,050.

EXAMPLE

A calendar-year corporation was organized during February 2013 incurring organizational expenditures of $60,000. Assuming the corporation begins business during April 2013, its maximum deduction for organizational expenditures for 2013 would be $60,000 × 9/180 = $3,000.

(1) For amounts paid or incurred after September 8, 2008, the corporation is deemed to have made the election, but instead may choose to forgo the deemed election by clearly electing to capitalize its costs on a timely filed return (including extensions) for the taxable year in which the corporation begins business.

(2) Organizational expenditures include expenses of temporary directors and organizational meetings, state fees for incorporation, accounting and legal service costs incident to incorporation (e.g., drafting bylaws, minutes of organizational meetings, and terms of original stock certificates).

(3) Expenditures connected with issuing or selling shares of stock, or listing stock on an exchange are neither deductible nor amortizable. Expenditures connected with the transfer of an asset to the corporation must be capitalized as part of the cost of the asset.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 34 THROUGH 37

c. The deduction for

charitable contributions is

limited to 10% of taxable income before the contributions deduction, the dividends received deduction, a NOL carryback (but after carryover), a capital loss carryback (but after carryover), and before the domestic production activities deductions (DPAD).

(1) Generally the same rules apply for valuation of contributed property as for individuals except

(a) Deduction for donations of inventory and other appreciated ordinary income-producing property is the donor’s basis plus one-half of the unrealized appreciation but limited to twice the basis, provided

1] Donor is a corporation (but not an S corporation)

2] Donee must use property for care of ill, needy, or infants

3] Donor must obtain a written statement from the donee that the use requirement has been met

4] No deduction allowed for unrealized appreciation that would be ordinary income under recapture rules

(b) Deduction for donation of appreciated scientific personal property to a college or university is the donor’s basis plus one-half the unrealized appreciation but limited to twice the basis, provided

1] Donor is a corporation (but not an S corporation, personal holding company, or service organization)

2] Property was constructed by donor and contributed within two years of substantial completion, and donee is original user of property

3] Donee must use property for research or experimentation

4] Donor must obtain a written statement from the donee that the use requirement has been met

5] No deduction allowed for unrealized appreciation that would be ordinary income under recapture rules

(2) Contributions are deductible in period paid (subject to 10% limitation) unless corporation is an accrual method taxpayer and then deductible (subject to 10% limitation) when authorized by board of directors if payment is made within 2 1/2 months after tax year end, and corporation elects to deduct contributions when authorized.

(3) Excess contributions over the 10% limitation may be carried forward for up to five years.

EXAMPLE

The books of a calendar-year, accrual method corporation for 2013 disclose net income of $350,000 after deducting a charitable contribution of $50,000. The contribution was authorized by the Board of Directors on December 24, 2013, and was actually paid on January 31, 2014. The allowable charitable contribution deduction for 2013 (if the corporation elects to deduct it when accrued) is $40,000, calculated as follows: ($350,000 + $50,000) × .10 = $40,000. The remaining $10,000 is carried forward for up to five years.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 38 THROUGH 44

d. A

100% Dividends Received Deduction (DRD) for dividends received from affiliated (i.e., at least 80% owned) corporations if a consolidated tax return is not filed.

(1) If a consolidated tax return is filed, intercompany dividends are eliminated in the consolidation process and not included in consolidated gross income.

(2) See Section D. for discussion of affiliated corporations

e. An

80% DRD is allowed for qualified dividends from taxable domestic unaffiliated corporations that are

at least 20% owned (but less than 80% owned).

(1) DRD may be limited to 80% of taxable income before the 80% dividends received deduction, the net operating loss deduction, a capital loss carryback, and the domestic production activities deduction (DPAD).

EXAMPLE

A corporation has income from sales of $20,000, dividend income of $10,000, and business expenses of $22,000, resulting in taxable income before the DRD of $8,000. Since taxable income before the DRD ($8,000) is less than dividend income ($10,000), the DRD is limited to $8,000 x 80% = $6,400. As a result, taxable income would be $8,000 − $6,400 = $1,600.

(2) Exception: The 80% of taxable income limitation does not apply if the full 80% DRD creates or increases a net operating loss.

EXAMPLE

In the example above, assume the same facts except that business expenses are $22,001, resulting in taxable income before the DRD of $7,999. Since the full DRD ($8,000) would create a $1 net operating loss ($7,999 − $8,000), the taxable income limitation does not apply and the full DRD ($8,000) would be allowed.

f. Only a

70% dividends received deduction (instead of 80%) is allowed for qualified dividends from taxable domestic unaffiliated corporations that are

less than 20% owned.

(1) A 70% of taxable income limitation (instead of 80%) and a limitation exception for a net operating loss apply as in e.(1) and (2) above.

(2) If dividends are received from both 20% owned corporations and corporations that are less than 20% owned, the 80% DRD and 80% DRD limitation for dividends received from 20% owned corporations is computed first. Then the 70% DRD and 70% DRD limitation is computed for dividends received from less than 20% owned corporations. For purposes of computing the 70% DRD limitation, taxable income is reduced by the total amount of dividends received from 20% owned corporations.

EXAMPLE

A corporation has taxable income before the dividends received deduction of $100,000. Included in taxable income are $65,000 of dividends from a 20% owned corporation and $40,000 of dividends from a less than 20% owned corporation. First, the 80% DRD for dividends received from the 20% owned corporation is computed. That deduction equals $52,000 [i.e., the lesser of 80% of the dividends received (80% × $65,000), or 80% of taxable income (80% × $100,000)].

Second, the 70% DRD for the dividends received from the less than 20% owned corporation is computed. That deduction is $24,500 [i.e., the lesser of 70% of the dividends received (70% × $40,000), or 70% of taxable income after deducting the amount of dividends from the 20% owned corporation (70% × [$100,000 − $65,000])].

Thus, the total dividends received deduction is $52,000 + $24,500 = $76,500.

g. A portion of a corporation’s 80% (or 70%) DRD will be disallowed if the dividends are directly attributable to

debt-financed portfolio stock.

(1) “Portfolio stock” is any stock (except stock of a corporation if the taxpayer owns at least 50% of the voting power and at least 50% of the total value of such corporation).

(2) The DRD percentage for debt-financed portfolio stock = [80% (or 70%) × (100% − average % of indebtedness on the stock)].

EXAMPLE

P, Inc. purchased 25% of T, Inc. for $100,000, paying with $50,000 of its own funds and $50,000 borrowed from its bank. During the year P received $9,000 in dividends from T, and paid $5,000 in interest expense on the bank loan. No principal payments were made on the loan during the year. If the stock were not debt financed, P’s DRD would be $9,000 × 80% = $7,200. However, because half of the stock investment was debt financed, P’s DRD is $9,000 × [80% × (100% − 50%)] = $3,600.

(3) The reduction in the DRD cannot exceed the interest deduction allocable to the portfolio stock indebtedness.

EXAMPLE

Assume the same facts as above except that the interest expense on the bank loan was only $3,000. The reduction in the DRD would be limited to the $3,000 interest deduction on the loan. The DRD would be ($9,000 × 80%) − $3,000 = $4,200.

h. No DRD is allowed if the dividend paying stock is held less than 46 days during the 91-day period that begins 45 days before the stock becomes ex-dividend. In the case of preferred stock, no DRD is allowed if the dividends received are for a period or periods in excess of 366 days and the stock has been held for less than 91 days during the 181-day period that begins 90 days before the stock becomes ex-dividend.

i. The

basis of stock held by a corporation must be reduced by the nontaxed portion of a non liquidating

extraordinary dividend received with respect to the stock, unless the corporation has held the stock for more than two years before the dividend is announced. To the extent the nontaxed portion of an extraordinary dividend exceeds the adjusted basis of the stock, the excess is recognized as gain for the taxable year in which the extraordinary dividend is received.

(1) The nontaxed portion of a dividend is generally the amount that is offset by the DRD.

(2) A dividend is considered “extraordinary” when it equals or exceeds 10% (5% for preferred stock) of the stock’s adjusted basis (or FMV if greater on the day preceding the ex-dividend date).

(3) Aggregation of dividends

(a) All dividends received that have ex-dividend dates that occur within a period of 85 consecutive days are treated as one dividend.

(b) All dividends received within 365 consecutive days are treated as extraordinary dividends if they in total exceed 20% of the stock’s adjusted basis.

(4) This provision is not applicable to dividends received from an affiliated corporation, and does not apply if the stock was held during the entire period the paying corporation (and any predecessor) was in existence.

EXAMPLE

Corporation X purchased 30% of the stock of Corporation Y for $10,000 during June 2013. During December 2013 X received a $20,000 dividend from Y. X sold its Y stock for $5,000 in February 2014.

Because the dividend from Y is an extraordinary dividend, the nontaxed portion (equal to the DRD allowed to X) $20,000 × 80% = $16,000 has the effect of reducing the Y stock basis from $10,000 to $0, with the remaining $6,000 recognized as gain for 2013. When the stock is sold in 2014, the excess of sale proceeds over the reduced stock basis $5,000 − $0 = $5,000 is also recognized as gain.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 45 THROUGH 50

j.

Losses in the ordinary course of business are deductible.

(1) Loss is

disallowed if the sale or exchange of property is between--

(a) A corporation and a more than 50% shareholder.

(b) A C corporation and an S corporation if the same persons own more than 50% of each.

(c) A corporation and a partnership if the same persons own more than 50% of the corporation, and more than 50% of the capital and profits interest in the partnership.

(d) Constructive ownership rules apply for purposes of determining stock ownership. Family constructive ownership includes an individual’s brothers and sisters, spouse, ancestors, and lineal descendants.

(e) In the event of a disallowed loss, the transferee on a subsequent disposition only recognizes gain to the extent it exceeds the disallowed loss.

(2) Any loss from the sale or exchange of property between corporations that are members of the same controlled group is deferred (instead of disallowed) until the property is sold outside the group. See controlled group definition in Section D.2., except substitute “more than 50%” for “at least 80%.”

(3) An accrual method C corporation is effectively placed on the cash method of accounting for purposes of deducting accrued interest and other expenses owed to a related cash method payee. No deduction is allowable until the year the amount is actually paid.

EXAMPLE

A calendar-year corporation accrues $10,000 of salary to an employee (a 60% shareholder) during 2013 but does not make payment until February 2014. The $10,000 will be deductible by the corporation and reported as income by the employee-shareholder in 2014.

(4)

Capital losses are deductible only to the extent of capital gains (i.e., may not offset ordinary income).

(a) Unused capital losses are carried back three years and then carried forward five years to offset capital gains.

(b) All corporate capital loss carrybacks and carry forwards are treated as short-term.

(5) Bad debt losses are treated as ordinary deductions.

(6) Casualty losses are treated the same as for an individual except

(a) There is no $100 floor

(b) If property is completely destroyed, the amount of loss is the property’s adjusted basis

(c) A partial loss is measured the same as for an individual’s nonbusiness loss (i.e., the lesser of the decrease in FMV, or the property’s adjusted basis)

(7) A corporation’s

NOL is computed the same way as its taxable income.

(a) The dividends received deduction is allowed without limitation.

(b) No deduction is allowed for a NOL carryback or carryover from other years, and no deduction is allowed for the domestic production activities deduction (DPAD).

(c) A NOL is generally carried back two years and forward twenty years to offset taxable income in those years. However, a three-year carryback is permitted for the portion of a NOL that is attributable to a presidentially declared disaster and is incurred by a small business corporation (i.e., a corporation whose average annual gross receipts are $5 million or less for the three-tax-year period preceding the loss year). A corporation may elect to forego carryback and only carry forward twenty years.

k. Depreciation and depletion computations are same as for individuals.

l. Research and development expenditures of a corporation (or individual) may be treated under one of three alternatives

(1) Currently expensed in year paid or incurred

(2) Amortized over a period of sixty months or more if life not determinable

(3) Capitalized and depreciated over determinable life

m. Contributions to a pension or profit-sharing plan

(1) Defined benefit plans

(a) Maximum deductible contribution is actuarially determined.

(b) There also are minimum funding standards.

(2) Defined contribution plans

(a) Maximum deduction for contributions to qualified profit-sharing or stock bonus plans is generally limited to 25% of the compensation paid or accrued during the year to covered employees.

(b) If more than 25% is paid, the excess can be carried forward as part of the contributions of succeeding years to the extent needed to bring the deduction up to 25%.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 51 THROUGH 58

5. In working a corporate problem, certain calculations must be made in a specific order [e.g., charitable contributions (CC) must be computed before the DRD]. The following memory device is quite helpful:

Gross income

| – |

Deductions (except CC, DRD, and DPAD) |

| – |

Taxable income before CC, DRD, and DPAD

CC (limited to 10% of TI before CC, DRD, capital loss and NOL carrybacks, and DPAD) |

| – |

Taxable income before DRD and DPAD

DRD (may be limited* to 80% or 70%) of TI before DRD, capital loss carryback, NOL carryover or carryback, and the DPAD) |

| – |

Taxable income before DPAD

DPAD (limited to 9% of TI before DPAD) |

| × |

Taxable income

Applicable rates |

=

– |

Tax liability before tax credits

Tax credits |

|

Tax liability |

6. A person sitting for the CPA examination should be able to

reconcile book and taxable income.

a. If you begin with book income to calculate taxable income, make the following adjustments:

(1)

Increase book income by

(a) Federal income tax expense

(b) Excess of capital losses over capital gains because a net capital loss is not deductible

(c) Income items in the tax return not included in book income (e.g., prepaid rents, royalties, interest)

(d) Charitable contributions in excess of the 10% limitation

(e) Expenses deducted on the books but not on the tax return (e.g., amount of business gifts in excess of $25, nondeductible life insurance premiums paid, 50% of business meals and entertainment)

(2)

Deduct from book income

(a) Income reported on the books but not on the tax return (e.g., tax-exempt interest, life insurance proceeds)

(b) Expenses deducted on the tax return but not on the books (e.g., MACRS depreciation above straight-line, charitable contribution carryover)

(c) The dividends received deduction

(d) The domestic production activities deduction

b. When going from taxable income to book income, the above adjustments would be reversed.

c.

Schedule M-1 of Form 1120 provides a reconciliation of income per books with taxable income before the NOL deduction and DRD, and must be completed by corporations with less than

$10 million of total assets. Schedule M-1 items are either

permanent book-to-tax differences (e.g., tax-exempt interest) or

temporary differences (e.g., accelerated depreciation used on tax return while straight-line used per books). The starting point on Schedule M-1 is net income (or loss) per books. Additions and subtractions are then made to reflect the differences between financial and tax accounting. The end result is the amount of taxable income before the NOL deduction and DRD that is reported on the current year return.

(1) Items added to book income include

(a) Federal income tax expense that was deducted per books

(b) Excess of capital losses over capital gains deducted per books but not deductible for tax purposes

(c) Income subject to tax in the current year but not included in current year book income (e.g., receipt of prepaid rent)

(d) Expenses deducted per books but not allowed in computing taxable income (e.g., 50% of business meals and entertainment, expenses incurred in the production of tax-exempt income, charitable contributions in excess of the 10% of taxable income limitation).

(2) Items subtracted from book income include

(a) Income reported on books this year not included in the tax return (e.g., tax-exempt interest, nontaxable life insurance proceeds)

(b) Deductions on the return not charged against book income this year (e.g., tax depreciation in excess of book depreciation, domestic production activities deduction)

EXAMPLE

A corporation discloses that it had net income after taxes of $36,000 per books. Included in the computation were deductions for charitable contributions of $10,000, a net capital loss of $5,000, and federal income taxes paid of $9,000. What is the corporation’s TI?

| Net income per books after tax |

$36,000 |

| Nondeductible net capital loss |

+ 5,000 |

| Federal income tax expense |

+ 9,000 |

| Charitable contributions |

+ 10,000 |

| Taxable income before CC |

$60,000 |

| CC (limited to 10% × 60,000) |

– 6,000 |

| Taxable income |

$54,000 |

d.

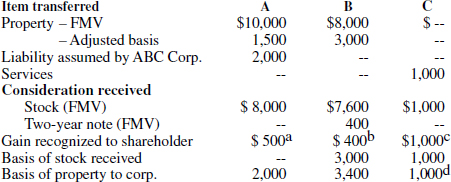

Schedule M-2 of Form 1120 analyzes changes in a corporation’s Unappropriated Retained Earnings per books between the beginning and end of the year.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 59 THROUGH 72

e.

Schedule M-3 Net Income (Loss) Reconciliation must be completed and attached to a corporation’s Form 1120 if the corporation’s total assets at the end of the tax year equal or exceed

$10 million. A corporation filing Schedule M-3 must not complete Schedule M-1. A corporation with total assets less than $10 million can elect to complete Schedule M-3 instead of completing Schedule M-1.

(1) Total assets at the end of the year must be determined using the same method as used for financial statement purposes. If a corporation uses the accrual method for financial statement purposes and the cash method for tax purposes, the corporation’s total assets must be determined using the accrual method.

(a) In the case of a US consolidated tax group, total assets at the end of the tax year must be determined based on the total year-end assets of all includible corporations, net of eliminations for intercompany transactions and balances between the includible corporations.

(b) A corporation is not required to file Schedule M-3 if total assets at the end of the current year are less than $10 million, even though the corporation was required to file Schedule M-3 for the preceding tax year.

(c) No schedule M-3 is required for taxpayers filing Form 1120-REIT (Real Estate Investment Trusts); Form 1120-RIC (Regulated Investment Companies); Form 1120-H (Homeowners Associations); and Form 1120-SF (Settlement Funds).

(2) Schedule M-3 consists of three parts: Part I adjusts worldwide income per books to worldwide book income for only those corporations includible on the tax return; Part II reconciles income and loss items for includible corporations; and Part III reconciles expense and deduction items. The total of items for Part III carry over to Part II for the overall reconciliation.

(a) Schedule M-3 requires much greater detail (Parts II and III contain a total of 66 line items) than Schedule M-1 (10 line items) because it requires taxpayers to separately list each type of transaction that gives rise to a book-tax difference and to identify whether each difference is permanent or temporary.

(b) Parts II and III each contain four columns: (a) income statement items; (b) temporary differences; (c) permanent differences; and, (d) tax return items. Part III requires a corporation to separate its book federal income tax expense between its current income tax expense and its deferred income tax expense. If its financial statements do not separately report current and deferred income tax expense, all income tax expense should be reported as current income tax expense in Part III.

(c) A US consolidated tax group required to file Schedule M-3 must file multiple Schedules M-3. It must file one Schedule M-3, Parts I, II, and III to reflect the activity of the entire US consolidated tax group. Additionally, a separate Schedule M-3 Parts II and III must be completed for the parent corporation and each subsidiary to reflect each corporation’s separate activity. Lastly, it generally is necessary to complete Parts II and III of a separate Schedule M-3 to eliminate differences related to intercompany transactions, and to include limitations on deductions (e.g., charitable contributions and capital loss limitations) and carryover amounts. As a result, a US consolidated group consisting of a parent corporation and three subsidiary corporations would have to complete a total of six Schedules M-3.

(d) A corporation or group of corporations that files a Form 1120 and is required to file Schedule M-3, must also file Schedule B (Form 1120), Additional Information for Schedule M-3 Filers. In the case of a consolidated group, a parent corporation files only one Schedule B (Form 1120) for the entire consolidated group.

(e)

Schedule UTP (Uncertain Tax Positions) must be completed and attached to Form 1120 if the corporation (1) has total assets of at least $100 million, and (2) the corporation has taken a tax position on its return and the corporation or a related party has either recorded a reserve with respect to that position in audited financial statements, or did not record a reserve because the corporation expects to litigate the position.

1] A tax position taken on a tax return is a tax position that would result in an adjustment to a line item on that return if the position is not sustained.

2] Schedule UTP requires a concise description of each uncertain tax position. Additionally, the corporation must rank each listed tax position by size, must indicate whether each position is temporary or permanent, and must disclose whether a tax position is greater than 10% of the aggregate amount of reserves for all tax positions.

3] If the corporation or a related party determined that, under applicable accounting standards, either no reserve was required for a tax position taken on a return because the amount was immaterial for audited financial statement purposes, or that a tax position was sufficiently certain so that no reserve was required, then the tax position is not required to be reported on Schedule UTP.

D. Affiliated and Controlled Corporations

1. An

affiliated group is a parent-subsidiary chain of corporations in which

at least 80% of the combined voting power and total value of all stock (except nonvoting preferred) are owned by includible corporations.

a. They may elect to file a consolidated return. Election is binding on all future returns.

b. If affiliated corporations file a consolidated return, intercompany dividends are eliminated in the consolidation process. If separate tax returns are filed, dividends from affiliated corporations are eligible for a 100% dividends received deduction.

c. Possible advantages of a consolidated return include the deferral of gain on intercompany transactions and offsetting operating/capital losses of one corporation against the profits/capital gains of another.

EXAMPLE

P Corp. owns 80% of the stock of A Corp., 40% of the stock of B Corp., and 45% of the stock of C Corp. A Corp. owns 40% of the stock of B Corp. A consolidated tax return could be filed by P, A, and B.

EXAMPLE

Parent and Subsidiary file consolidated tax returns using a calendar year. During 2012, Subsidiary paid a $10,000 dividend to Parent. Also during 2012, Subsidiary sold land with a basis of $20,000 to Parent for its FMV of $50,000. During 2013, Parent sold the land to an unrelated taxpayer for $55,000.

The intercompany dividend is eliminated in the consolidation process and is excluded from consolidated taxable income. Additionally, Subsidiary’s $30,000 of gain from the sale of land to Parent is deferred for 2012. The $30,000 will be included in consolidated taxable income for 2013 when Parent reports $5,000 of income from the sale of that land to the unrelated taxpayer.

2. A

controlled group of corporations is limited to an aggregate of $75,000 of taxable income taxed at less than 35%, one $250,000 accumulated earnings credit, one Sec. 179 expense election, and one $40,000 AMT exemption. There are three basic types of controlled groups.

a. Parent-subsidiary–Basically same as P-S group eligible to file consolidated return, except ownership requirement is 80% of combined voting power or total value of stock. Affiliated corporations are subject to the controlled group limitations if the corporations file separate tax returns.

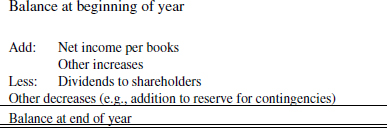

b. Brother-sister–Two or more corporations if 5 or fewer persons who are individuals, estates, or trusts own stock possessing more than 50% of the total combined voting power, or more than 50% of the total combined voting power, or more than 50% of the total value of all shares of stock of each corporation, taking into account the stock ownership of each person only to the extent such stock ownership is identical with respect to each corporation.

EXAMPLE

Corporations W and X are a controlled group since five or fewer individuals own more than 50% of each corporation when counting only identical ownership.

EXAMPLE

Corporations Y and Z are not a controlled group since shareholders F, G, and H do not own more than 50% of Y and Z when counting only identical stock ownership.

c. Combined–The parent in a P-S group is also a member of a brother-sister group of corporations.

EXAMPLE

Individual H owns 100% of the stock of Corporations P and Q. Corporation P owns 100% of the stock of Corporation S. P, S, and Q are members of one controlled group.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 73 THROUGH 79

E. Dividends and Distributions

1.

Ordinary corporate distributions

a. Corporate distributions of property to shareholders on their stock are subject to a

three-step treatment.

(1) Dividend–to be included in gross income

(2) Return of stock basis–nontaxable and reduces shareholder’s basis for stock

(3) Gain–to extent distribution exceeds shareholder’s stock basis

b. The amount of distribution to a shareholder is the cash plus the FMV of other property received, reduced by liabilities assumed.

c. A shareholder’s tax basis for distributed property is the property’s FMV at date of distribution (not reduced by liabilities).

d. A

dividend is a distribution of property by a corporation to its shareholders out of

(1) Earnings and profits of the current taxable year (CEP), computed at the end of the year, without regard to the amount of earnings and profits at the date of distribution; or,

(2) Earnings and profits accumulated after February 28, 1913 (AEP).

EXAMPLE

Corporation X has earnings and profits of $6,000 and makes a $10,000 distribution to its sole shareholder, A, who has a stock basis of $3,000. The $10,000 distribution to A will be treated as a dividend of $6,000, a nontaxable return of stock basis of $3,000, and a capital gain of $1,000.

(a) CEP are first allocated to distributions on preferred stock, then to common stock.

(b) CEP are allocated pro rata to multiple distributions on the same class of stock if distributions exceed CEP.

(c) AEP are allocated to distributions in the order in which the distributions are made.

EXAMPLE

A corporation has both preferred and common stock outstanding and no accumulated earnings and profits. For the current year, it has current earnings and profits of $15,000, and during the year distributes cash of $10,000 to its preferred shareholders, and $10,000 to its common shareholders. The $15,000 of CEP are first allocated to the distribution to the preferred shareholders, making all $10,000 taxable as a dividend. The remaining $5,000 of CEP is then allocated to the $10,000 distribution to common shareholders, making only $5,000 taxable as a dividend.

EXAMPLE

A corporation has accumulated earnings and profits of $4,000 and current earnings and profits of $20,000. During the current year its distributes $15,000 to its common shareholders in March, and another $15,000 to its common shareholders in October. The $20,000 of CEP are allocated pro rata to the two distributions, making $10,000 of the March distribution and $10,000 of the October distribution taxable as a dividend. The AEP of $4,000 are then allocated to the March distribution. As a result, $14,000 of the March distribution and $10,000 of the October distribution are taxable as a dividend.

e. The

distributing corporation recognizes gain on the distribution of appreciated property as if such property were sold for its FMV. However, no loss can be recognized on the non liquidating distribution of property to shareholders.

EXAMPLE

A corporation distributes property with an FMV of $10,000 and a basis of $3,000 to a shareholder. The corporation recognizes a gain of $10,000 − $3,000 = $7,000.

(1) If the distributed property is subject to a liability (or if the distributee assumes a liability) and the FMV of the distributed property is less than the amount of liability, then the gain is the difference between the amount of liability and the property’s basis.

EXAMPLE

A corporation distributes property with an FMV of $10,000 and a basis of $3,000 to a shareholder, who assumes a liability of $12,000 on the property. The corporation recognizes a gain of $12,000 − $3,000 = $9,000.

(2) The type of gain recognized (e.g., ordinary, Sec. 1231, capital) depends on the nature of the property distributed (e.g., recapture rules may apply).

2.

Earnings and profits

a.

Current earnings and profits (CEP) are

similar to book income, but are computed by making adjustments to taxable income.

(1) Add–tax-exempt income, dividends received deduction, excess of MACRS depreciation over depreciation computed under ADS, etc.

(2) Deduct–federal income taxes, net capital loss, excess charitable contributions, expenses relating to tax-exempt income, penalties, etc.

b. Accumulated earnings and profits (AEP) represent the sum of prior years’ CEP, reduced by distributions and net operating loss of prior years.

c. CEP are increased by the gain recognized on a distribution of appreciated property (excess of FMV over basis).

d. Distributions reduce earnings and profits (but not below zero) by

(1) The amount of money

(2) The face amount (or issue price if less) of obligations of the distributing corporation, and

(3) The adjusted basis (or FMV if greater) of other property distributed

(4) Above reductions must be adjusted for any liability assumed by the shareholder, or the amount of liability to which the property distributed is subject.

EXAMPLE

Z Corp. has two 50% shareholders, Alan and Baker. Z Corp. distributes a parcel of land (held for investment) to each shareholder. Gainacre with an FMV of $12,000 and an adjusted basis of $8,000 is distributed to Alan, while Lossacre with an FMV of $12,000 and an adjusted basis of $15,000 is distributed to Baker. Each shareholder assumes a liability of $3,000 on the property received. Z Corp. must recognize a gain of $4,000 on the distribution of property to Alan, but cannot recognize the loss on the distribution to Baker.

| |

Alan |

Baker |

| Dividend ($12,000 − $3,000) |

$ 9,000 |

$ 9,000 |

| Tax basis for property received |

12,000 |

12,000 |

| Effect (before tax) on Z’s earnings & profi ts: |

|

|

| |

Alan |

Baker |

| Increased by gain (FMV-basis) |

4,000 |

0 |

| Increased by liabilities distributed |

3,000 |

3,000 |

| Decreased by greater of FMV or adjusted basis of property distributed |

(12,000) |

(15,000) |

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 80 THROUGH 91

3.

Stock redemptions

a. A stock redemption is

treated as an exchange, generally resulting in capital gain or loss treatment to the shareholder if at least one of the following five tests is met. Constructive stock ownership rules of Sec. 318 generally apply in determining whether the exchange tests are met. For this purpose, an individual’s family consists of only spouse, children, grandchildren, and parents. A stock redemption will receive exchange treatment if:

(1) The redemption is not essentially equivalent to a dividend (this has been interpreted by Revenue Rulings to mean that a redemption must reduce a shareholder’s right to vote, share in earnings, and share in assets upon liquidation; and after the redemption the shareholder’s stock ownership [both direct and constructive] must not exceed 50%), or

(2) The redemption is substantially disproportionate (i.e., after redemption, shareholder’s percentage ownership is less than 80% of shareholder’s percentage ownership prior to redemption, and less than 50% of shares outstanding), or

(3) All of the shareholder’s stock is redeemed, or

(4) The redemption is from a non corporate shareholder in a partial liquidation, or

(5) The distribution is a redemption of stock to pay death taxes under Sec. 303.

b. If none of the above tests are met, the redemption proceeds are treated as an ordinary Sec. 301 distribution, taxable as a dividend to the extent of the distributing corporation’s earnings and profits.

c. A corporation cannot deduct amounts paid or incurred in connection with a redemption of its stock (except for interest expense on loans used to purchase stock).

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 92 THROUGH 94

4.

Complete liquidations

a. Amounts received by shareholders in liquidation of a corporation are treated as received in exchange for stock, generally resulting in capital gain or loss. Property received will have a basis equal to FMV.

b. A

liquidating corporation generally recognizes gain or loss on the sale or distribution of its assets in complete liquidation.

(1) If a distribution, gain or loss is computed as if the distributed property were sold to the distributee for FMV.

(2) If distributed property is subject to a liability (or a shareholder assumes a liability) in excess of the basis of the distributed property, FMV is deemed to be not less than the amount of liability.

c.

Distributions to related persons

(1) No loss is generally recognized to a liquidating corporation on the distribution of property to a related person if

(a) The distribution is not pro rata, or

(b) The property was acquired by the liquidating corporation during the five-year period ending on the date of distribution in a Sec. 351 transaction or as a contribution to capital. This includes any property whose basis is determined by reference to the adjusted basis of property described in the preceding sentence.

(2) Related person is a shareholder who owns (directly or constructively) more than 50% of the corporation’s stock. The constructive ownership rules of Sec. 267 apply to determine whether a person owns more than 50%. For this purpose, an individual’s family includes spouse, brothers and sisters, ancestors, and lineal descendants.

d.

Carryover basis property

(1) If a corporation acquires property in a Sec. 351 transaction or as a contribution to capital at any time after the date that is two years before the date of the adoption of the plan of complete liquidation, any loss resulting from the property’s sale, exchange, or distribution can be recognized only to the extent of the decline in value that occurred subsequent to the date that the corporation acquired the property.

(2) The above rule applies only where the loss is not already completely disallowed by c.(1) above, and is intended to apply where there is no clear and substantial relationship between the contributed property and the conduct of the corporation’s business. If the contributed property is actually used in the corporation’s business, the above rule should not apply if there is a business purpose for placing the property in the corporation.

EXAMPLE

During September 2012, a shareholder makes a capital contribution which includes property unrelated to the corporation’s business with a basis of $15,000 and an FMV of $10,000 on the contribution date. Within two years the corporation adopts a plan of liquidation and sells the property for $8,000. The liquidating corporation’s recognized loss will be limited to $10,000 − $8,000 = $2,000.

e.

Liquidation of subsidiary

(1) No gain or loss is recognized to a parent corporation under Sec. 332 on the receipt of property in complete liquidation of an 80% or more owned subsidiary. The subsidiary’s basis for its assets along with all tax accounting attributes (e.g., earnings and profits, NOL, and charitable contribution carry forwards) will transfer to the parent corporation.

(2)

No gain or loss is recognized to a

subsidiary corporation on the distribution of property to its parent if Sec. 332 applies to the parent corporation.

(a) If the subsidiary has debt outstanding to the parent, non recognition also applies to property distributed in satisfaction of the debt.

(b) Gain (but not loss) is recognized on the distribution of property to minority (20% or less) shareholders.

(3) Non recognition does not extend to minority shareholders. A minority shareholder’s gain or loss will be recognized under the general rule at 4.a. above.

EXAMPLE

Parent Corp. owns 80% of Subsidiary Corp., with the remaining 20% of Subsidiary stock owned by Alex. Parent’s basis in its Subsidiary stock is $100,000, while Alex has an basis for her Subsidiary stock of $15,000. Subsidiary Corp. is to be liquidated and will distribute to Parent Corp. assets with an FMV of $200,000 and a basis of $150,000, and will distribute to Alex assets with an FMV of $50,000 and a basis of $30,000. Subsidiary has an unused capital loss carryover of $10,000. The tax effects of the liquidation will be as follows:

Parent Corp. will not recognize gain on the receipt of Subsidiary’s assets in complete liquidation, since Subsidiary is an at least 80%-owned corporation. The basis of Subsidiary’s assets to Parent will be their transferred basis of $150,000, and Parent will inherit Subsidiary’s unused capital loss carryover of $10,000.

Alex will recognize a gain of $35,000 ($50,000 FMV − $15,000 stock basis) from the liquidation. Alex’s tax basis for Subsidiary’s assets received in the liquidation will be their FMV of $50,000.

Subsidiary Corp. will not recognize gain on the distribution of its assets to Parent Corp., but will recognize a gain of $20,000 ($50,000 FMV − $30,000 basis) on the distribution of its assets to Alex.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 95 THROUGH 103

5.

Stock purchases treated as asset acquisitions

a. An acquiring corporation that has purchased at least 80% of a target corporation’s stock within a 12-month period may elect under Sec. 338 to have the purchase of stock treated as an acquisition of assets.

b. Old target corporation is deemed to have sold all its assets on the acquisition date, and is treated as a new corporation that has purchased those assets on the day after the acquisition date.

(1) Acquisition date is the date on which at least 80% of the target’s stock has been acquired by purchase within a 12-month period.

(2) Gain or loss is generally recognized to old target corporation on deemed sale of assets.

(3) The deemed sales price for the target corporation’s assets is generally the FMV of the target’s assets as of the close of the acquisition date.

F. Personal Holding Company and Accumulated Earnings Taxes

1. Personal holding companies (PHC) are subject to a penalty tax on undistributed PHC income to discourage taxpayers from accumulating their investment income in a corporation taxed at lower than individual rates.

a. A

PHC is any corporation (except certain banks, financial institutions, and similar corporations) that meets two requirements.

(1) During anytime in the last half of the tax year, five or fewer individuals own more than 50% of the value of the outstanding stock directly or indirectly, and

(2) The corporation receives at least 60% of its adjusted ordinary gross income as “PHC income” (e.g., dividends, interest, rents, royalties, and other passive income)

b. Taxed at ordinary corporate rates on taxable income, plus 20% tax rate (15% for years before 2013) on undistributed PHC income

c. The PHC tax

(1) Is self-assessing (i.e., computed on Sch. PH and attached to Form 1120); a six-year statute of limitations applies if no Sch. PH is filed

(2) May be avoided by dividend payments sufficient in amount to reduce undistributed PHC income to zero

d. The PHC tax is computed as follows:

|

Taxable Income |

| + |

Dividends-received deduction |

| + |

Net operating loss deduction (except NOL of immediately preceding year allowed without a dividends-received deduction) |

| – |

Federal and foreign income taxes |

| – |

Charitable contributions in excess of 10% limit |

| – |

Net capital loss |

| – |

Net LTCG over NSTCL (net of tax) |

|

Adjusted Taxable Income |

| – |

Dividends paid during taxable year |

| – |

Dividends paid within 2 1/2 months after close of year (limited to 20% of dividends actually paid during year) |

| – |

Dividend carryover |

| – |

Consent dividends |

|

Undistributed PHC Income |

| × |

20% |

|

Personal Holding Company Tax |

e. Consent dividends are hypothetical dividends that are treated as if they were paid on the last day of the corporation’s taxable year. Since they are not actually distributed, shareholders increase their stock basis by the amount of consent dividends included in their gross income.

f. PHC tax liability for a previous year (but not interest and penalties) may be avoided by payment of a deficiency dividend within ninety days of a “determination” by the IRS that the corporation was a PHC for a previous year.

2. Corporations may be subject to an

accumulated earnings tax (AET), in addition to regular income tax, if they accumulate earnings beyond reasonable business needs in order to avoid a shareholder tax on dividend distributions.

a. The tax is not self-assessing, but is based on the IRS’ determination of the existence of tax avoidance intent.

b. AET may be imposed without regard to the number of shareholders of the corporation, but does not apply to personal holding companies.

c.

Accumulated earnings credit is allowed for greater of

(1) $250,000 ($150,000 for personal service corporations) minus the accumulated earnings and profits at end of prior year, or

(2) Reasonable needs of the business (e.g., expansion, working capital, to retire debt, etc.).

d. Balance of accumulated taxable income is taxed at 20% tax rate (15% for years before 2013).

e. The AET may be avoided by dividend payments sufficient in amount to reduce accumulated taxable income to zero.

f. The accumulated earnings tax is computed as follows:

|

Taxable Income |

| + |

Dividends-received deduction |

| + |

NOL deduction |

| – |

Federal and foreign income taxes |

| – |

Excess charitable contributions (over 10% limit) |

| – |

Net capital loss |

| – |

Net LTCG over net STCL (net of tax) |

|

Adjusted Taxable Income |

| – |

Dividends paid last 9 1/2 months of tax year and 2 1/2 months after close |

| – |

Consent dividends |

| – |

Accumulated earnings credit |

|

Accumulated Taxable Income |

| × |

20% |

|

Accumulated Earnings Tax |

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 104 THROUGH 122

G. S Corporations

An S corporation generally pays no corporate income taxes. Instead, it functions as a pass-through entity (much like a partnership) with its items of income, gain, loss, deduction, and credit passed through and directly included in the tax computations of its shareholders. Electing small business corporations are designated as S corporations; all other corporations are referred to as C corporations.

1.

Eligibility requirements for S corporation status

a. Domestic corporation

b. An S corporation may own any percent of the stock of a C corporation, and 100% of the stock of a qualified subchapter S subsidiary.

(1) An S corporation cannot file a consolidated return with an affiliated C corporation.

(2) A qualified subchapter S subsidiary (QSSS) is any domestic corporation that qualifies as an S corporation and is 100% owned by an S corporation parent, which elects to treat it as a QSSS. A QSSS is not treated as a separate corporation and all of its assets, liabilities, and items of income, deduction, and credit are treated as belonging to the parent S corporation.

c. Only one class of stock issued and outstanding. A corporation will not be treated as having more than one class of stock solely because of differences in voting rights among the shares of common stock (i.e., both voting and nonvoting common stock may be outstanding).

d.

Shareholders must be individuals, estates, or trusts created by will (only for a two-year period), voting trusts, an Electing Small Business Trust (ESBT), a Qualified Subchapter S Trust (QSST), or a trust all of which is treated as owned by an individual who is a citizen or resident of the US (i.e., Subpart E trust).

(1) A QSST and a Subpart E trust may continue to be a shareholder for two years beginning with the date of death of the deemed owner.

(2) Code Sec. 401(a) qualified retirement plan trusts and Code Sec. 501(c) charitable organizations that are exempt from tax under Code Sec. 501(a) are eligible to be shareholders of an S corporation. The S corporation’s items of income and deduction will flow through to the tax-exempt shareholder as unrelated business taxable income (UBIT).

e. No nonresident alien shareholders

f. The number of shareholders is limited to 100.

(1) Husband and wife (and their estates) are counted as one shareholder.

(2) Each beneficiary of a voting trust is considered a shareholder.

(3) If a trust is treated as owned by an individual, that individual (not the trust) is treated as the shareholder.

(4) All members of a family can elect to be treated as one shareholder. The election may be made by any family member and will remain in effect until terminated. Members of a family include the common ancestor, the lineal descendants of the common ancestor, and the spouses (or former spouses) of the common ancestor and lineal descendants. The common ancestor cannot be more than six generations removed from the youngest generation of shareholders at the time the S election is made.

2. An

election must be filed anytime in the preceding taxable year or on or before the fifteenth day of the third month of the year for which effective.

a. All shareholders on date of election, plus any shareholders who held stock during the taxable year but before the date of election, must consent to the election.

(1) If an election is made on or before the fifteenth day of the third month of taxable year, but either (1) a shareholder who held stock during the taxable year and before the date of election does not consent to the election, or (2) the corporation did not meet the eligibility requirements during the part of the year before the date of election, then the election is treated as made for the following taxable year.

(2) An election made after the fifteenth day of the third month of the taxable year is treated as made for the following year.

b. A newly formed corporation’s election will be timely if made within two and one-half months of the first day of its taxable year (e.g., a calendar-year corporation formed on April 6, 2013, could make an S corporation election that would be effective for its 2013 calendar year if the election is filed on or before June 20, 2013).

c. A valid election is effective for all succeeding years until terminated.

d. The IRS has the authority to waive the effect of an invalid election caused by a corporation’s inadvertent failure to qualify as a small business corporation or to obtain required shareholder consents (including elections regarding qualified subchapter S trusts), or both. Additionally, the IRS may treat late-filed subchapter S elections as timely filed if there is reasonable cause justifying the late filing.

3.

LIFO recapture. A C corporation using LIFO that converts to S status must recapture the excess of the inventory’s value using a FIFO cost flow assumption over its LIFO tax basis as of the close of its last tax year as a C corporation.

a. The LIFO recapture is included in the C corporation’s gross income and the tax attributable to its inclusion is payable in four equal installments.

b. The first installment must be paid by the due date of the tax return for the last C corporation year, with the three remaining installments due by the due dates of the tax returns for the three succeeding taxable years.

4. A corporation making an S election is generally required to

adopt or change to (1) a year ending December 31, or (2) a fiscal year that is the same as the fiscal year used by shareholders owning more than 50% of the corporation’s stock.

a. An S corporation may use a different fiscal year if a valid business purpose can be established (i.e., natural business year) and IRS permission is received. The business purpose test will be met if an S corporation receives at least 25% of its gross receipts in the last two months of the selected fiscal year, and this 25% test has been satisfied for three consecutive years.

EXAMPLE

An S corporation, on a calendar year, has received at least 25% of its gross receipts during the months of May and June for each of the last three years. The S corporation may be allowed to change to a fiscal year ending June 30.

b. An S corporation that otherwise would be required to adopt or change its tax year (normally to the calendar year) may elect to use a fiscal year if the election does not result in a deferral period longer than three months, or, if less, the deferral period of the year currently in use.

(1) The “deferral period” is the number of months between the close of the fiscal year elected and the close of the required year (e.g., if an S corporation elects a tax year ending September 30 and a tax year ending December 31 is required, the deferral period of the year ending September 30 is three months).

(2) An S corporation that elects a tax year other than a required year must make a “required payment” which is in the nature of a refundable, noninterest-bearing deposit that is intended to compensate the government for the revenue lost as a result of tax deferral. The required payment is due on May 15 each year and is recomputed for each subsequent year.

5. An S corporation must

file Form 1120S by the fifteenth day of the third month following the close of its taxable year (e.g., March 15 for a calendar-year S corporation).

a. An automatic six-month extension may be obtained by filing Form 7004.

b. Estimated tax payments must be made if estimated tax liability (e.g., built-in gains tax, excess net passive income tax) is expected to be $500 or more.

6.

Termination of S corporation status may be caused by

a. Shareholders owning

more than 50% of the shares of stock of the corporation consent to

revocation of the election.

(1) A revocation made on or before the fifteenth day of the third month of the taxable year is generally effective on the first day of such taxable year.

(2) A revocation made after the fifteenth day of the third month of the taxable year is generally effective as of the first day of the following taxable year.

(3) Instead of the dates mentioned above, a revocation may specify an effective date on or after the date on which the revocation is filed.

EXAMPLE

For a calendar-year S corporation, a revocation not specifying a revocation date that is made on or before 3/15/13 is effective as of 1/1/13. A revocation not specifying a revocation date that is made after 3/15/13 is effective as of 1/1/14. If a revocation is filed 3/11/13 and specifies a revocation date of 7/1/13, the corporation ceases to be an S corporation on 7/1/13.

b. The corporation’s failing to satisfy any of the eligibility requirements listed in 1. Termination is effective on the date an eligibility requirement is failed.

EXAMPLE

A calendar-year S corporation with common stock outstanding issues preferred stock on April 1, 2013. Since its S corporation status terminates on April 1, it must file an S corporation tax return (Form 1120S) for the period January 1 through March 31, and a C corporation tax return (Form 1120) for the period April 1 through December 31, 2013. Both tax returns would be due by March 15, 2014.

c. Passive investment income exceeding 25% of gross receipts for three consecutive taxable years if the corporation has subchapter C earnings and profits at the end of each of those years.

(1) Subchapter C earnings and profits are earnings and profits accumulated during a taxable year for which the corporation was a C corporation.

(2) Termination is effective as of the first day of the taxable year beginning after the third consecutive year of passive investment income in excess of 25% of gross receipts.

EXAMPLE

An S corporation with subchapter C earnings and profits had passive investment income in excess of 25% of its gross receipts for its calendar years 2011, 2012, and 2013. Its S corporation status would terminate 1/1/14.

d. Generally once terminated, S corporation status can be reelected only after five non–S corporation years.

(1) The corporation can request IRS for an earlier reelection.

(2) IRS may treat an inadvertent termination as if it never occurred.

7. An

S corporation generally pays no federal income taxes, but may have to pay a tax on its built-in gain, or on its excess passive investment income if certain conditions are met.

a. The S corporation is treated as a pass-through entity; the character of any item of income, expense, gain, loss, or credit is determined at the corporate level, and passes through to shareholders, retaining its identity.

b. An S corporation must recognize gain on the distribution of appreciated property (other than its own obligations) to its shareholders. Gain is recognized in the same manner as if the property had been sold to the distributee at its FMV.

EXAMPLE

An S corporation distributes property with an FMV of $900 and an adjusted basis of $100 to its sole shareholder. Gain of $800 will be recognized by the corporation. The character of the gain will be determined at the corporate level, and passed through and reported by its shareholder. The shareholder is treated as receiving a $900 distribution, subject to the distribution rules discussed in Section G.11.

c. Expenses and interest owed to any cash-method shareholder are deductible by an accrual-method S corporation only when paid.

EXAMPLE

An accrual-method calendar-year S corporation accrues $2,000 of salary to a cash-method employee (a 1% shareholder) during 2013, but does not make payment until February 2014. The $2,000 will be deductible by the corporation in 2014, and reported by the shareholder-employee as income in 2014.