Chapter 1: Beginning Your CPA Review Program

GENERAL COMMENTS ON THE EXAMINATION

The Uniform CPA Examination is delivered using computer-based testing (CBT). Computer-based testing has several advantages. You may take the exam one section at a time. As a result, your studies can be focused on that one section, improving your chances for success. In addition, you may take the exam on your schedule, eight months of the year, six days a week and in the morning or in the afternoon.

Successful completion of the Regulation section of the CPA Examination is an attainable goal. Keep this point foremost in your mind as you study the first four chapters in this volume and develop your study plan.

Purpose of the Examination1

The Uniform CPA Examination is designed to test the entry-level knowledge and skills necessary to protect the public interest. These knowledge and skills were identified through a Practice Analysis performed in 2008, which served as a basis for the development of the content specifications for the exam.

The CPA examination is one of many screening devices to assure the competence of those licensed to perform the attest function and to render professional accounting services. Other screening devices include educational requirements, ethics examinations, and work experience.

The examination appears to test the material covered in accounting programs of the better business schools. It also appears to be based upon the body of knowledge essential for the practice of public accounting and the audit of a medium-sized client. Since the examination is primarily a textbook or academic examination, you should plan on taking it as soon as possible after completing your accounting education.

Examination Content

Guidance concerning topical content of the computer-based exam in Regulation can be found in a document prepared by the Board of Examiners of the AICPA entitled Content and Skill Specifications for the Uniform CPA Exam. We have included the content outline for Regulation at the beginning of Chapter 5. The outline should be used as an indication of the topics’ relative emphasis on the exam.

The Board’s objective in preparing this detailed listing of topics tested on the exam is to help “in assuring the continuing validity and reliability of the Uniform CPA Examination.” These outlines are an excellent source of guidance concerning the areas and the emphasis to be given each area on future exams.

The new Content and Skill Specification Outlines for the CPA examination go into effect January 1, 2014. In addition, the AICPA adopted CBT-e, which is a new computer platform. The major change from your standpoint is that simulations are smaller in size and a larger number of these “task-based simulations” are included on the Auditing and Attestation, Financial Accounting and Reporting, and Regulation exams. In addition, all questions that test writing skills have been moved to the Business Environment and Concepts exam.

The exam covers the Internal Revenue Code and federal tax regulations in effect six months before the particular testing window. For the Regulation section, federal laws are tested six months following their effective date and for uniform acts one year after their adoption by a simple majority of jurisdictions. This section deals with federal and widely adopted uniform laws. If there is no federal or uniform law on a topic, the questions are intended to test knowledge of the law of the majority of jurisdictions. Professional ethics questions are based on the AICPA Code of Professional Conduct because it is national in its application, whereas codes of other organizations and jurisdictions may be limited in their application. The AICPA posts content changes regularly on its Internet site. The address is www.cpa-exam.org.

Nondisclosure and Computerization of Examination

Beginning May 1996, the Uniform CPA Examination became nondisclosed. For each exam section, candidates are required to agree to a Statement of Confidentiality, which states that they will not divulge the nature and content of any exam question. The CPA exam is computer-based, and candidates take the exam at Prometric sites in the 55 jurisdictions in which the exam is offered. The CPA exam is offered continually during the testing windows shown below.

One or more exam sections may be taken during any exam window, and the sections may be taken in any desired order. However, no candidate will be allowed to sit for the same section more than once during any given testing window. In addition, a candidate must pass all four sections of the CPA exam within a “rolling” eighteen-month period, which begins on the date he or she passes a section. In other words, you must pass the other three sections of the exam within eighteen months of when you pass the first section. If you do not pass all sections within the eighteen-month period, credit for any section(s) passed outside the eighteen-month period will expire and the section(s) must be retaken.

Types of Questions

The computer-based Uniform CPA Examination consists of two basic question formats.

The multiple-choice questions are much like the ones that have constituted a majority of the CPA examination for years. And the good news is that these types of questions constitute 60% of the Regulation section.

Process for Sitting for the Examination

While there are some variations in the process from state to state, the basic process for sitting for the CPA examination may be described as follows.

Applying to Take the Examination

The right to practice public accounting as a CPA is governed by individual state statutes. While some rules regarding the practice of public accounting vary from urisdiction to jurisdiction, all State Boards of Accountancy use the Uniform CPA Examination and AICPA advisory grading service as one of the requirements to practice public accounting. Every candidate should contact the applicable State Board of Accountancy to determine the requirements to sit for the exam (e.g., education requirements). For comparisons of requirements for various state boards and those policies that are uniform across jurisdictions you should refer to the website of the National Association of State Boards of Accountancy (NASBA) at www.nasba.org.

A frequent problem candidates encounter is failure to apply by the deadline. Apply to sit for the examination early. Also, you should use extreme care in filling out the application and mailing required materials to your State Board of Accountancy. If possible, have a friend review your completed application before mailing with check and other documentation. The name on your application must appear exactly the same as it appears on the identification you plan to use at the testing center. Candidates may miss a particular CPA examination window simply because of minor technical details that were overlooked (check not signed, items not enclosed, question not answered on application, etc.). Because of the very high volume of applications received in the more populous states, the administrative staff does not have time to call or write to correct minor details and will simply reject your application.

The NASBA website has links to the registration information for all 55 jurisdictions. It is possible for candidates to sit for the examination at a Prometric site in any state or territory. Candidates desiring to do so should refer to the registration information for the applicable State Board of Accountancy.

International Applicants

International administration of the CPA Exam is currently offered in Brazil, Japan, Bahrain, Kuwait, Lebanon, and the United Arab Emirates. If you live in one of these testing locations, or other select countries, you may be able to take the Exam without traveling to the U.S. The Exam is only offered in English, and is the same computerized test as the one administered in the U.S. You are required to meet the same eligibility requirements and complete the same licensure requirements as your U.S. counterparts.

Applicants from countries other than the U.S. must follow the same basic steps as U.S. applicants. This means they must select the jurisdiction in which they wish to qualify and file an application with the board of accountancy (or its designated agent) in that jurisdiction. Any special instructions for candidates who have completed their education outside the U.S. are included in the board of accountancy requirements. For more information on the international administration of the CPA Examination, visit the International section of the NASBA website.

Obtaining the Notice to Schedule

Once your application has been processed and you have paid all fees, you will receive a Notice to Schedule (NTS) from NASBA. The NTS will list the section(s) of the examination that you are approved to take. When you receive the NTS, verify that all information is correct. Be certain that the name appearing on the NTS matches EXACTLY the name on the identification documents that you will use during check-in at the testing center. If the information is incorrect or the name does not match, immediately contact your board of accountancy or its designated agent to request a correction. You must bring your NTS with you to the examination.

Exam Scheduling

Once you have been cleared to take the exam by the applicable state board, you will receive by mail a Notice to Schedule (NTS) and may then schedule to sit for one or more sections of the exam.

You have the following two options for scheduling your examination:

You should also be aware that if you have to cancel or reschedule your appointment, you may be subject to a cancellation/rescheduling fee. The AICPA’s Uniform CPA Examination Candidate Bulletin lists the rescheduling and cancellation fees.

To assure that you get your desired location and time period it is imperative that you schedule early. To get your first choice of dates, you are advised to schedule at least 45 days in advance. You will not be scheduled for an exam fewer than 5 days before testing.

ATTRIBUTES OF EXAMINATION SUCCESS

Your primary objective in preparing for the Regulation section is to pass. Other objectives such as learning new and reviewing old material should be considered secondary. The six attributes of examination success discussed below are essential. You should study the attributes and work toward achieving/developing each of them before taking the examination.

Common Candidate Mistakes

The CPA Exam is a formidable hurdle in your accounting career. With a pass rate of about 45% on each section, the level of difficulty is obvious. The good news, though, is that about 75% of all candidates (first-time and re-exam) sitting for each examination eventually pass. The authors believe that the first-time pass rate could be higher if candidates would be more careful. Seven common mistakes that many candidates make are

These mistakes are not mutually exclusive. Candidates may commit one or more of the above items. Remind yourself that when you decrease the number of common mistakes, you increase your chances of successfully becoming a CPA. Take the time to read carefully the exam question requirements. Do not jump into a quick start, only to later find out that you didn’t understand what information the examiners were asking for. Read slowly and carefully. Take time to recall your knowledge. Respond to the question asked. Apply an exam strategy such as allocating your time among all question formats. Do not spend too much time on the multiple-choice testlets, leaving no time to spend on preparing your simulation responses. Answer questions quickly but precisely, avoid common mistakes, and increase your score.

PURPOSE AND ORGANIZATION OF THIS REVIEW TEXTBOOK

This book is designed to help you prepare adequately for the Regulation Examination. There is no easy way to prepare for the successful completion of the CPA Examination; however, through the use of this manual, your approach will be systematic and logical.

The objective of this book is to provide study materials supportive to CPA candidates. While no guarantees are made concerning the success of those using this text, this book promotes efficient preparation by

As you read the next few paragraphs which describe the contents of this book, flip through the chapters to gain a general familiarity with the book’s organization and contents. Chapters 2, 3, and 4 are to help you “maximize your score.”

Chapter 2 Examination Grading

Chapter 3 The Solutions Approach

Chapter 4 Taking the Examination

Chapters 2, 3, and 4 contain material that should be kept in mind throughout your study program. Refer back to them frequently. Reread them for a final time just before you sit for the exam.

The Regulation Modules contain

Also included at the end of this text is a complete Sample Regulation Examination. The sample exam is included to enable candidates to gain experience in taking a “realistic” exam. While studying the modules, the candidate can become accustomed to concentrating on fairly narrow topics. By working through the sample examination near the end of their study programs, candidates will be better prepared for taking the actual examination. Because some task-based simulations require the use of research materials, it is useful to have the appropriate electronic research database (Internal Revenue Code and Income Tax Regulations) or printed versions of the Internal Revenue Code and Income Tax Regulations to complete the sample examination. Remember that this research material will not be available to answer the multiple-choice questions.

Other Textbooks

This text is a comprehensive compilation of study guides and outlines; it should not be necessary to supplement them with accounting textbooks and other materials for most topics. You probably already have business law and tax textbooks. In such a case, you must make the decision whether to replace them and trade familiarity (including notes therein, etc.), with the cost and inconvenience of obtaining the newer texts containing a more updated presentation.

Before spending time and money acquiring a new book, begin your study program with the Wiley CPAexcel Exam Review: Regulation to determine your need for a supplemental text.

Ordering Other Textual Materials

If you want to order AICPA materials, locate an AICPA educator member to order your materials, since educator members are entitled to a discount and may place website or telephone orders.

A variety of supplemental CPA products is available from John Wiley & Sons, Inc. By using a variety of learning techniques, such as software, computer-based learning, and audio CDs, the candidate is more likely to remain focused during the study process and to retain information for a longer period of time. Visit our website at www.wiley.com/cpa for other products, supplements, and updates.

Working CPA Questions

The AICPA content outlines, study outlines, etc., will be used to acquire and assimilate the knowledge tested on the examination. This, however, should be only one-half of your preparation program. The other half should be spent practicing how to work questions. Some candidates probably spend over 90% of their time reviewing material tested on the CPA exam. Much more time should be allocated to working previous examination questions under exam conditions. Working examination questions serves two functions. First, it helps you develop a solutions approach as well as solutions that will maximize your score. Second, it provides the best test of your knowledge of the material.

The multiple-choice questions and answer explanations can be used in many ways. First, they may be used as a diagnostic evaluation of your knowledge. For example, before beginning to review commercial paper you may wish to answer 10 to 15 multiple-choice questions to determine your ability to answer CPA examination questions on commercial paper. The apparent difficulty of the questions and the correctness of your answers will allow you to determine the necessary breadth and depth of your review. Additionally, exposure to examination questions prior to review and study of the material should provide motivation. You will develop a feel for your level of proficiency and an understanding of the scope and difficulty of past examination questions. Moreover, your review materials will explain concepts encountered in the diagnostic multiple-choice questions.

Second, the multiple-choice questions can be used as a poststudy or postreview evaluation. You should attempt to understand all concepts mentioned (even in incorrect answers) as you answer the questions. Refer to the explanation of the answer for discussion of the alternatives even though you selected the correct response. Thus, you should read the explanation of the unofficial answer unless you completely understand the question and all of the alternative answers.

Third, you may wish to use the multiple-choice questions as a primary study vehicle. This is probably the quickest but least thorough approach in preparing for the exam. Make a sincere effort to understand the question and to select the correct response before referring to the unofficial answer and explanation. In many cases, the explanations will appear inadequate because of your lack of familiarity with the topic. Always refer back to an appropriate study source, such as the outlines and text in this volume, your business law and tax textbooks, Code Sections, etc.

The multiple-choice questions outnumber the task-based simulations by greater than 10 to 1 in this book. This is similar to the proposed content of the new computer-based examination. One problem with so many multiple-choice questions is that you may overemphasize them. Candidates generally prefer to work multiple-choice questions because they are

Another problem with the large number of multiple-choice questions is that you may tend to become overly familiar with the questions. The result may be that you begin reading the facts and assumptions of previously studied questions into the questions on your examination. Guard against this potential problem by reading each multiple-choice question with extra care.

Beginning with the introduction of the computer-based examination, the AICPA began testing with simulations. Simulations released by the AICPA, prepared by the author, and revised from prior CPA exam problems are incorporated in the modules to which they pertain. (See the listing of question material at the beginning of Chapter 5.)

The questions and solutions in this volume provide you with an opportunity to diagnose and correct any exam-taking weaknesses prior to sitting for the examination. Continually analyze your incorrect solutions to determine the cause of the error(s) during your preparation for the exam. Treat each incorrect solution as a mistake that will not be repeated (especially on the examination). Also attempt to generalize your weaknesses so that you may change, reinforce, or develop new approaches to exam preparation and exam taking.

SELF-STUDY PROGRAM

CPA candidates generally find it difficult to organize and complete their own self-study programs. A major problem is determining what and how to study. Another major problem is developing the self-discipline to stick to a study program. Relatedly, it is often difficult for CPA candidates to determine how much to study (i.e., determining when they are sufficiently prepared.) The following suggestions will assist you in developing a systematic, comprehensive, and successful self-study program to help you complete the Regulation exam.

Remember that these are only suggestions. You should modify them to suit your personality, available study time, and other constraints. Some of the suggestions may appear trivial, but CPA candidates generally need all the assistance they can get to systemize their study programs.

Study Facilities and Available Time

Locate study facilities that will be conducive to concentrated study. Factors that you should consider include

You will probably find different study facilities optimal for different times (e.g., your kitchen table during early morning hours and local libraries during early evening hours).

Next review your personal and professional commitments from now until the exam to determine regularly available study time. Formalize a schedule to which you can reasonably commit yourself. At the end of this chapter, you will find a detailed approach to managing your time available for the exam preparation program.

Self-Evaluation

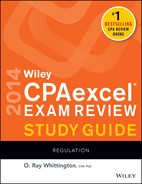

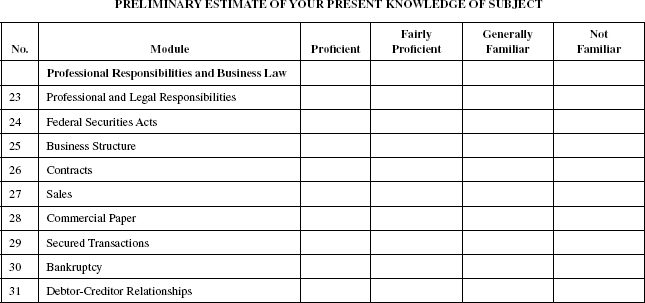

The Wiley CPAexcel Exam Review: Regulation self-study program is partitioned into 17 topics or modules. Since each module is clearly defined and should be studied separately, you have the task of preparing for the CPA Regulation exam by tackling 17 manageable tasks. Partitioning the overall project into 17 modules makes preparation psychologically easier, since you sense yourself completing one small step at a time rather than seemingly never completing one or a few large steps.

By completing the following “Preliminary Estimate of Your Present Knowledge of Subject” inventory below, organized by the 17 modules in this program, you will tabulate your strong and weak areas at the beginning of your study program. This will help you budget your limited study time. Note that you should begin studying the material in each module by answering up to 1/4 of the total multiple-choice questions covering that module’s topics (see instruction 4.A. in the next section). This “mini-exam” should constitute a diagnostic evaluation as to the amount of review and study you need.

Time Allocation

The study program below entails an average of 68 hours (Step 5. below) of study time. The breakdown of total hours is indicated in the left margin.

| [2 1/2 hrs.] | 1. Study Chapters 2–4 in this volume. These chapters are essential to your efficient preparation program. (Time estimate includes candidate’s review of the examples of the solutions approach in Chapters 2 and 3.) |

| [1/2 hr.] | 2. Begin by studying the introductory material at the beginning of Chapter 5. |

| 3. Study one module at a time. The modules are listed above in the self-evaluation section. | |

| 4. For each module | |

| [6 hrs.] | A. First, review the listing of key terms at the end of the module. Then, work 1/4 of the multiple-choice questions (e.g., if there are 40 multiple-choice questions in a module, you should work every 4th question). Score yourself.

This diagnostic routine will provide you with an index of your proficiency and familiarity with the type and difficulty of questions.

The outlines for each module are broken into smaller sections that refer you to multiple-choice questions to test your comprehension of the material. You may find this organization useful in breaking your study into smaller bites.

Time estimate: 3 minutes each, not to exceed 1 hour total.

|

| [22 hrs.] | B. Study the outlines and illustrations. Where necessary, refer to your business law and tax textbooks and original authoritative pronouncements (e.g., code sections). (This will occur more frequently for topics in which you have a weak background.)

Time estimate: 1 hour minimum per module with more time devoted to topics less familiar to you.

|

| [15 hrs.] | C. Work the remaining multiple-choice questions. Study the explanations of the multiple-choice questions you missed or had trouble answering.

Time estimate: 3 minutes to answer each question and 2 minutes to study the answer explanation of each question missed.

|

| [18 hrs.] | D. Under exam conditions, work at least 6 simulations per module and the questions and task-based simulations in Appendices B and C. Work additional questions and simulations as time permits.

Time estimate: 2 minutes for each multiple-choice question, 15 minutes for each simulation, and 10 minutes to review the solution for each simulation worked.

|

| [4 hrs.] | E. Work through the sample CPA examination presented as Appendix B. Each exam should be taken in one sitting.

Take the examination under simulated exam conditions (i.e., in a strange place with other people present [your local municipal library or a computer lab]). Apply your solutions approach to each question and your exam strategy to the overall exam.

You should limit yourself to the time you will have when taking the actual CPA exam section (3 hours for the Regulation section). Spend time afterwards grading your work and reviewing your effort.

Time estimate: To take the exam and review it later, approximately 4 hours.

|

| 5. The total suggested time of 68 hours is only an average. Allocation of time will vary candidate by candidate. Time requirements vary due to the diverse backgrounds and abilities of CPA candidates. Allocate your time so you gain the most proficiency in the least time. Remember that while 68 hours will be required, you should break the overall project down into 17 more manageable tasks. Do not study more than one module during each study session. |

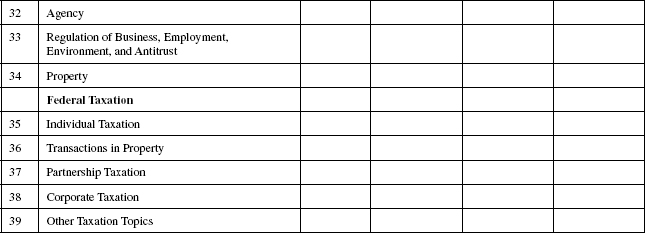

Using Notecards

Below are one candidate’s notecards on business law topics which illustrate how key definitions, lists, etc., can be summarized on index cards for quick review. Since candidates can take these anywhere they go, they are a very efficient review tool.

Level of Proficiency Required

What level of proficiency must you develop with respect to each of the topics to pass the exam? You should work toward a minimum correct rate on the multiple-choice questions of 80%. Working toward a correct rate of 80% or higher will give you a margin.

Warning: Disproportional study time devoted to multiple-choice (relative to task-based simulations) can be disastrous on the exam. You should work a substantial number of simulation problems under exam conditions, even though multiple-choice questions are easier to work and are used to gauge your proficiency. The authors believe that practicing simulation problems will also improve your proficiency on the multiple-choice questions.

Multiple-Choice Feedback

One of the benefits of working through previous exam questions is that it helps you to identify your weak areas. Once you have graded your answers, your strong areas and weak areas should be clearly evident. Yet, the important point here is that you should not stop at a simple percentage evaluation. The percentage only provides general feedback about your knowledge of the material contained within that particular module. The percentage does not give you any specific feedback regarding the concepts which were tested. In order to get this feedback, you should look at the questions missed on an individual basis because this will help you gain a better understanding of why you missed the question.

This feedback process has been facilitated by the fact that within each module where the multiple-choice answer key appears, two blank lines have been inserted next to the multiple-choice answers. As you grade the multiple-choice questions, mark those questions which you have missed. However, instead of just marking the questions right and wrong, you should now focus on marking the questions in a manner which identifies why you missed the question. As an example, a candidate could mark the questions in the following manner: ![]() for math mistakes, x for conceptual mistakes, and ? for areas which the candidate was unfamiliar with. The candidate should then correct these mistakes by reworking through the marked questions.

for math mistakes, x for conceptual mistakes, and ? for areas which the candidate was unfamiliar with. The candidate should then correct these mistakes by reworking through the marked questions.

The objective of this marking technique is to help you identify your weak areas and thus, the concepts which you should be focusing on. While it is still important for you to get between 75% and 80% correct when working multiple-choice questions, it is more important for you to understand the concepts. This understanding applies to both the questions answered correctly and those answered incorrectly. Remember, questions on the CPA exam will be different from the questions in the book; however, the concepts will be the same. Therefore, your preparation should focus on understanding concepts, not just getting the correct answer.

Conditional Candidates

If you have received conditional status on the examination, you must concentrate on the remaining section(s). Unfortunately, many candidates do not study after conditioning the exam, relying on luck to get them through the remaining section(s). Conditional candidates will find that material contained in Chapters 1–4 and the information contained in the appropriate modules will benefit them in preparing for the remaining section(s) of the examination.

PLANNING FOR THE EXAMINATION

Overall Strategy

An overriding concern should be an orderly, systematic approach toward both your preparation program and your examination strategy. A major objective should be to avoid any surprises or anything else that would rattle you during the examination. In other words, you want to be in complete control as much as possible. Control is of paramount importance from both positive and negative viewpoints. The presence of control on your part will add to your confidence and your ability to prepare for and take the exam. Moreover, the presence of control will make your preparation program more enjoyable (or at least less distasteful). However, a lack of organization will result in inefficiency in preparing for and taking the examination, with a highly predictable outcome. Likewise, distractions during the examination (e.g., inadequate lodging, long drive) are generally disastrous.

In summary, establishing a systematic, orderly approach to taking the examination is of paramount importance.

The following outline is designed to provide you with a general framework of the tasks before you. You should tailor the outline to your needs by adding specific items and comments.

Weekly Review of Preparation Program Progress

The following pages contain a hypothetical weekly review of program progress. You should prepare a similar progress chart. This procedure, taking only 5 minutes per week, will help you proceed through a more efficient, complete preparation program.

Make notes of materials and topics

| Weeks to go | Comments on progress, “to do” items, etc. |

| 8 |

1) Read RESP, FEDE →made notecards

2) Worked some MC Questions and Simulation Problems

|

| 7 |

1) Read CONT and SALES →made notecards

2) Worked some MC Questions and Simulation Problems in these areas

|

| 6 |

1) Read CPAP and SECU →made notecards

2) Worked some MC Questions and Simulation Problems in these areas

3) Reviewed remedies for breach

|

| 5 |

1) Read BANK, DBCR, AGEN →made notecards

2) Worked some MC Questions and Simulation Problems in these areas

3) Reviewed firm offer examples and battle of forms

|

| 4 |

1) Read RBUS, PROP →made notecards

2) Worked some MC Questions and Simulation Problems in these areas

|

| 3 |

1) Read ITAX, PTAX →made notecards

2) Worked some MC Questions and Simulation Problems in these areas

|

| 2 |

1) Read CTAX, GETX →made notecards

2) Worked some MC Questions and Simulation Problems in these areas

|

| 1 |

1) Worked Complete task-based simulations in Appendices B and C

2) Reviewed weak modules

|

| 0 |

1) Took sample exam in Regulation

2) Reviewed exam policies and procedures

3) Reviewed notecards

|

Time Management of Your Preparation

As you begin your CPA exam preparation, you obviously realize that there is a large amount of material to cover over the course of the next two to three months. Therefore, it is very important for you to organize your calendar, and maybe even your daily routine, so that you can allocate sufficient time to studying. An organized approach to your preparation is much more effective than a last week cram session. An organized approach also builds up the confidence necessary to succeed on the CPA exam.

An approach which we have already suggested is to develop weekly “to do” lists. This technique helps you to establish intermediate objectives and goals as you progress through your study plan. You can then focus your efforts on small tasks and not feel overwhelmed by the entire process. And as you accomplish these tasks you will see yourself moving one step closer to realizing the overall goal, succeeding on the CPA exam.

Note, however, that the underlying assumption of this approach is that you have found the time during the week to study and thus accomplish the different tasks. Although this is an obvious step, it is still a very important step. Your exam preparation should be of a continuous nature and not one that jumps around the calendar. Therefore, you should strive to find available study time within your daily schedule, which can be utilized on a consistent basis. For example, everyone has certain hours of the day which are already committed for activities such as jobs, classes, and, of course, sleep. There is also going to be the time you spend relaxing because CPA candidates should try to maintain some balance in their lives. Sometimes too much studying can be counterproductive. But there will be some time available to you for studying and working through the questions. Block off this available time and use it only for exam prep. Use the time to accomplish your weekly tasks and to keep yourself committed to the process. After awhile your preparation will develop into a habit and the preparation will not seem as overwhelming as it once did.

1More information may be obtained from the AICPA’s Uniform CPA Examination Candidate Bulletin, which you can find on the AICPA’s website at www.cpa-exam.org.