Appendix B: Regulation Sample Testlet Released by AICPA

1. Which of the following statements concerning the similarities between a general partnership and a corporation are correct?

a. Corporate stockholders and general partners have limited personal liability.

b. Corporations and general partnerships have perpetual existence.

c. Corporations and general partnerships can declare bankruptcy.

d. Corporations and general partnerships are recognized as taxpayers for federal income tax purposes.

1. (c) The requirement is to identify the similarity between a general partnership and a corporation. Answer (c) is correct because under the federal securities laws both a corporation and a general partnership may file for bankruptcy. Answer (a) is incorrect because general partners do not have limited liability for partnership debts. Answer (b) is incorrect because while corporations have perpetual existence, general partnerships do not. Answer (d) is incorrect because while a corporation is a taxpaying entity, a partnership is a flow-through entity. The partners of the partnership pay the taxes.

2. Furl Corp., a corporation organized under the laws of State X, sued Row, a customer residing in State Y, for nonpayment for goods sold. Row attempted to dismiss the suit brought by Furl in State Y on the grounds that Furl was conducting business in State Y but had not obtained a certificate of authority from State Y to transact business therein. Which of the following actions by Furl would generally result in the court ruling that Furl was conducting business in State Y?

a. Maintaining bank accounts in State Y.

b. Shipping goods across state lines into State Y.

c. Owning and operating a small manufacturing plant in State Y.

d. Holding board of directors meetings in State Y.

2. (c) The requirement is to identify the actions that would result in Furl Corp. legally conducting business in a state. Furl Corp. is a domestic corporation in State X because Furl incorporated there. Furl is a foreign corporation in State Y because it was not incorporated in that state. When Furl is conducting business in State Y, Furl may be denied access to the courts to sue persons residing in State Y unless it qualified to do business in State Y by obtaining a certificate of authority from that state. Therefore, an important issue that the court examines is whether Furl was conducting business in State Y since Furl sued Row, a customer residing in this state. Generally a foreign corporation is ruled as conducting business in a state if the corporation’s transactions are continuous rather than isolated. Owning and operating even a small manufacturing plant in the state would generally result in a ruling that Furl is conducting business in that state. Answer (a) is incorrect because merely maintaining a bank account in the state does not meet the definition of conducting business in that state. Answer (b) is incorrect because solely shipping goods across state lines into State Y does not meet the definition of conducting business in that state. Answer (d) is incorrect because Furl Corp. may hold its meetings for the board of directors in a state without meeting the definition of conducting business in that state.

3. Which of the following rights is a holder of a public corporation’s cumulative preferred stock always entitled to?

a. Conversion of the preferred stock into common stock.

b. Voting rights.

c. Dividend carryovers from years in which dividends were not paid, to future years.

d. Guaranteed dividends.

3. (c) Preferred shares of stock are shares that have a contractual preference over other classes of stock as to liquidations and dividends. If a preferred stock is cumulative, the shareholder would be entitled to dividend carryovers from years in which dividends were not paid, to future years and would receive all dividends in arrears before any dividend is paid to owners of common stock. Answers (a) and (b) are incorrect because in order for a shareholder to be entitled to convert preferred stock into common stock or to have voting rights, it must be stated in the articles of incorporation. These are not rights that a holder of preferred stock would always be entitled to. Answer (d) is incorrect because although a preferred stockholder has preference over other classes of stock as to declared dividends, the board of directors’ power to declare dividends is discretionary and thus dividends are not guaranteed.

4. Leker exchanged a van that was used exclusively for business and had an adjusted tax basis of $20,000 for a new van. The new van had a fair market value of $10,000, and Leker also received $3,000 in cash. What was Leker’s tax basis in the acquired van?

a. $20,000

b. $17,000

c. $13,000

d. $ 7,000

4. (b) The requirement is to determine the basis for Leker’s new van. The exchange of Leker’s old van with a basis of $20,000 that was used exclusively for business, for a new van worth $10,000 plus $3,000 cash qualified as a like-kind exchange. Since it is a like-kind exchange, Leker’s realized loss of $20,000 − ($10,000 + $3,000) = $7,000 cannot be recognized, but instead is reflected in the basis of the new van. The new van’s basis is the adjusted basis of Leker’s old van of $20,000 reduced by the $3,000 of cash boot received, resulting in a basis of $17,000.

5. If a corporation’s charitable contributions exceed the limitation for deductibility in a particular year, the excess

a. Is not deductible in any future or prior year.

b. May be carried back or forward for one year at the corporation’s election.

c. May be carried forward to a maximum of five succeeding years.

d. May be carried back to the third preceding year.

5. (c) The requirement is to select the correct statement regarding a corporation’s charitable contributions in excess of the limitation for deductibility in a particular year. Corporate charitable contributions in excess of the 10% of taxable income limitation may be carried forward to a maximum of 5 succeeding years, subject to a 10% limitation in those years.

6. Strom acquired a 25% interest in Ace Partnership by contributing land having an adjusted basis of $16,000 and a fair market value of $50,000. The land was subject to a $24,000 mortgage, which was assumed by Ace. No other liabilities existed at the time of the contribution. What was Strom’s basis in Ace?

a. $0

b. $16,000

c. $26,000

d. $32,000

6. (a) The requirement is to determine Strom’s initial basis for the 25% interest in Ace Partnership that was received in exchange for land, subject to a mortgage that was assumed by Ace. Strom’s initial basis for the 25% partnership interest received consists of the $16,000 basis of the land contributed, less the net reduction in Strom’s liabilities resulting from the partnership’s assumption of the $24,000 mortgage. Since Strom received a 25% partnership interest, the net reduction in Strom’s liability is $24,000 × 75% = $18,000. Since Strom cannot have a negative basis, his basis for his 25% interest in Ace is $16,000 − $18,000 = $0. Additionally, note that Strom must recognize a $2,000 gain because the liability reduction exceeded the basis of the transferred land.

7. Which of the following statements concerning the similarities between a general partnership and a corporation are correct?

a. Corporate stockholders and general partners have limited personal liability.

b. Corporations and general partnerships have perpetual existence.

c. Corporations and general partnerships can declare bankruptcy.

d. Corporations and general partnerships are recognized as taxpayers for federal income tax purposes.

7. (c) The requirement is to identify the similarity between a general partnership and a corporation. Answer (c) is correct because under the federal securities laws both a corporation and a general partnership may file for bankruptcy. Answer (a) is incorrect because general partners do not have limited liability for partnership debts. Answer (b) is incorrect because while corporations have perpetual existence general partnerships do not. Answer (d) is incorrect because while a corporation is a taxpaying entity, a partnership is a flow-through entity. The partners of the partnership pay the taxes.

Task-Based Simulation 1

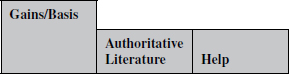

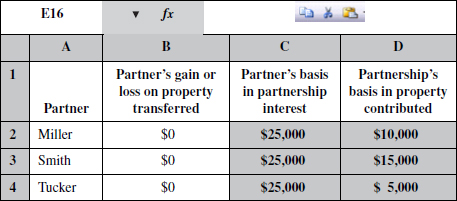

Miller, Smith, and Tucker decided to form a partnership to perform engineering services. All of the partners have extensive experience in the engineering field and now wish to pool their resources and client contacts to begin their own firm. The new entity, Sabre Consulting, will begin operations on April 1, 2013, and will use the calendar year for reporting purposes.

All of the partners expect to work full time for Sabre and each will contribute cash and other property to the company sufficient to commence operations. The partners have agreed to share all income and losses of the partnership equally. A written partnership agreement, duly executed by the partners, memorializes this agreement among the partners.

The table below shows the estimated values for assets contributed to Sabre by each partner. None of the contributed assets’ costs have been previously recovered for tax purposes.

Complete the shaded cells in the following table by entering the gain or loss recognized by each partner on the property contributed to Sabre Consulting, the partner’s basis in the partnership interest, and Sabre’s basis in the contributed property. Loss amounts should be recorded as a negative number.

Solution to Task-Based Simulation 1

Generally, no gain or loss is recognized on the contribution of property in exchange for a partnership interest. As a result, a partner’s initial basis for a partnership interest consists of the amount of cash plus the adjusted basis of noncash property contributed. Similarly, a partnership receives a transferred basis for contributed noncash property equal to the partner’s basis for the property prior to contribution. Miller’s initial partnership basis consists of the $15,000 cash plus the $10,000 adjusted basis of noncash property contributed, or $25,000. Smith’s partnership basis consists of the $10,000 cash plus the $15,000 basis of noncash property contributed, or $25,000. Tucker’s partnership basis consists of the $20,000 cash plus the $5,000 basis of noncash property contributed, or $25,000.

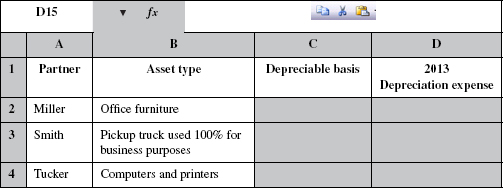

Task-Based Simulation 2

Miller, Smith, and Tucker decided to form a partnership to perform engineering services. All of the partners have extensive experience in the engineering field and now wish to pool their resources and client contacts to begin their own firm. The new entity, Sabre Consulting, will begin operations on April 1, 2013, and will use the calendar year for reporting purposes.

All of the partners expect to work full time for Sabre and each will contribute cash and other property to the company sufficient to commence operations. The partners have agreed to share all income and losses of the partnership equally. A written partnership agreement, duly executed by the partners, memorializes this agreement among the partners.

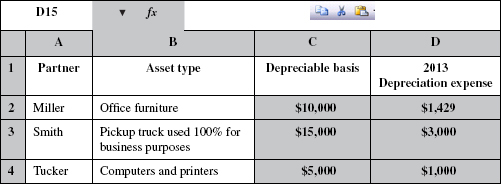

The table below shows the estimated values for assets contributed to Sabre by each partner. None of the contributed assets’ costs have been previously recovered for tax purposes.

Using the MACRS table (which can be found by clicking the Resources tab) and the partnership basis in the contributed assets calculated on the prior tab, complete the following table to determine Sabre’s tax depreciation expense for 2013. Assume that none of the original cost of any asset was expensed by the partnership under the provisions of Section 179, and that the partnership elected not to take bonus depreciation.

Solution to Task-Based Simulation 2

The Sabre partnership’s depreciable basis for the contributed property is a transferred basis equal to the contributing partner’s basis for the property prior to contribution. The office furniture has a 7-year recovery period, while the pickup truck and computers and printers have a 5-year recovery period. The MACRS depreciation table that was provided is based on the 200% declining-balance method and already incorporates the half-year convention which permits just a half-year of depreciation for the year that depreciable personalty is placed in service. Thus, the 2013 depreciation expense for the office furniture is $10,000 × 14.29% = $1,429 (i.e., $10,000 × 2/7 × 1/2). The 2013 depreciation for the pickup truck is $15,000 × 20% = $3,000 (i.e., $15,000 × 2/5 × 1/2). The 2013 depreciation expense for the computers and printers is $5,000 × 20% = $1,000 (i.e., $5,000 × 2/5 × 1/2).

Task-Based Simulation 3

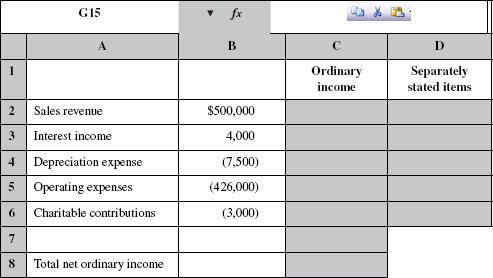

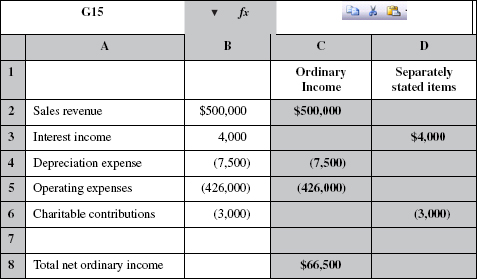

Assume that Sabre (a partnership) had only the items of income and expense shown in the following table for the 2013 tax year. Complete the remainder of the table by properly classifying each item of income and expense as ordinary business income that is reportable on page 1, Form 1065, or as a separately stated item that is reportable on Schedule K, Form 1065. Some entries may appear in both columns.

Solution to Task-Based Simulation 3

Partnership items having special tax characteristics (e.g., passive activity losses, deductions subject to dollar or percentage limitations, etc.) must be separately stated and shown on Schedules K and K-1 so that their special characteristics are preserved when reported on partners’ returns. In contrast, partnership ordinary income and deduction items having no special tax characteristics can be netted together in the computation of a partnership’s ordinary income and deductions from trade or business activities on page 1 of Form 1065. Here, assuming the $4,000 of interest income is from investments, it represents portfolio income and must be separately stated on Schedule K. Similarly, the charitable contributions of $3,000 must be separately stated so that the appropriate percentage limitations can be applied when passed through to partners. Sales, depreciation, and operating expenses are ordinary items and result in net ordinary income of $66,500.

Task-Based Simulation 4

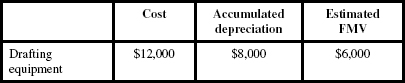

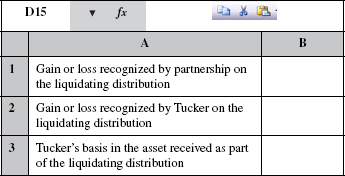

The partners have decided to liquidate Sabre Consulting at December 31, 2013. On that date, Tucker received the following asset as a liquidating distribution in exchange for his entire partnership interest. There were no partnership liabilities at the date of liquidation. Tucker’s basis in the partnership interest at the date of liquidation was $3,000.

Based on the foregoing information, complete the following table. Loss amounts should be recorded as a negative number.

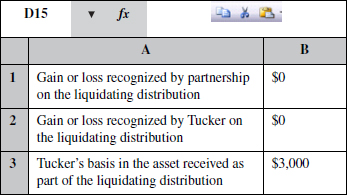

Solution to Task-Based Simulation 4

Generally, no gain or loss is recognized by a partnership on the distribution of noncash property in complete liquidation of the partnership. Similarly, no gain or loss is generally recognized by a distributee partner when noncash property is received in complete liquidation of the partner’s partnership interest. Here, Sabre recognizes no gain when it distributes drafting equipment with an FMV of $6,000 and an adjusted basis of $4,000, and Tucker recognizes no gain when he receives the drafting equipment in liquidation of his partnership interest. Although distributed property generally has a transferred basis, the basis of the drafting equipment to Tucker is limited to his $3,000 basis for his partnership interest before the distribution.

Task-Based Simulation 5

Use the research materials available to you by clicking the Authoritative Literature button to research the answer to the following questions. Find the code section that addresses the question, and enter the section citation in the shaded boxes below. Give the most precise a citation possible (i.e., both code section and subsection, if applicable). Do not copy the actual text of the citation.

During its initial tax year, Sabre Consulting incurred $2,000 of legal fees and $750 of accounting fees to organize the partnership. What code section and subsection permits the partnership to deduct these expenses for federal tax purposes?

Solution to Task-Based Simulation 5

Code Sec. 709(b) allows a partnership to deduct up to $5,000 of organizational expenditures for the tax year in which the partnership begins business. The $5,000 amount must be reduced by the amount by which organizational expenditures exceed $50,000. Remaining expenditures are deducted ratably over the 180-month period beginning with the month in which the partnership begins business.