Module 36: Transactions in Property

Overview

This module presents the income tax consequences of property transactions including the sale, exchange, or other disposition of property. Basis is covered first with a review of the basis of property acquired by purchase, gift, and from a decedent. Tax-deferred transactions are covered next with a review of like-kind exchanges, involuntary conversions, and the sale of a principal residence. Next, sales and exchanges of securities are reviewed as well as the treatment of losses and expenses incurred in transactions with related taxpayers. Finally, capital gains and losses, as well as gains and losses from business property including Sec. 1231 and depreciation recapture are reviewed. Not only is it important to determine the extent of gain or loss recognition, but it is also important to be able to determine whether the character of the recognized gain or loss is capital, Sec. 1231, or ordinary.

A. Sales and Other Dispositions

B. Capital Gains and Losses

C. Personal Casualty and Theft Gains and Losses

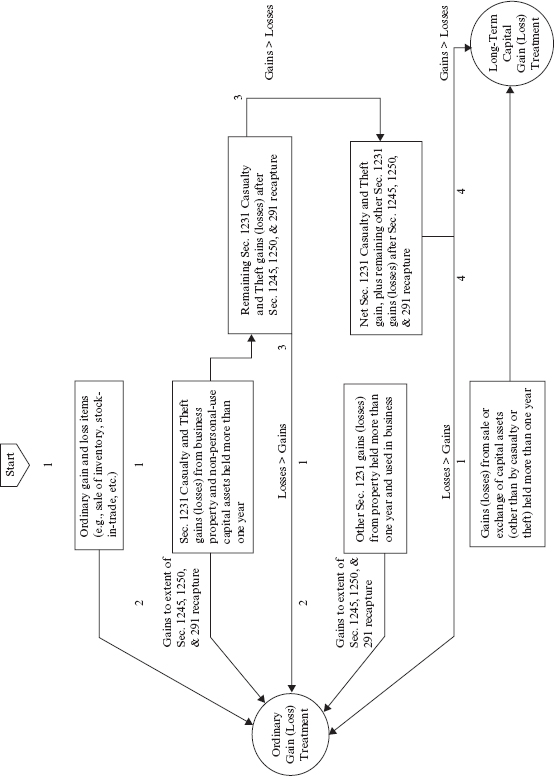

D. Gains and Losses on Business Property

Key Terms

Multiple-Choice Questions

Multiple-Choice Answers and Explanations

Simulations

Simulation Solutions

A. Sales and Other Dispositions

B. Capital Gains and Losses

| Net short-term capital loss | $(1,500) |

| 28% group—collectibles net gain | 900 |

| 25% group—unrecaptured Sec. 1250 net gain | 2,000 |

| 15% group—net gain | 5,000 |

| Net capital gain | $ 6,400 |

C. Personal Casualty and Theft Gains and Losses

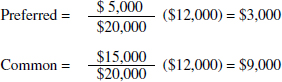

D. Gains and Losses on Business Property

| Total gain ($350,000 − $40,000) | $310,000 |

| Sec. 1250 ordinary income ($360,000 − $330,000) | (30,000) |

| Sec. 1231 gain | $280,000 |

| Total gain ($350,000 − $40,000) | $310,000 |

| Sec. 1250 ordinary income ($360,000 − $330,000) | (30,000)* |

| Additional ordinary income—20% of $280,000 (the additional amount that would have been ordinary income if the property were Sec. 1245 property) |

(56,000)* |

| Sec. 1231 gain | $224,000 |

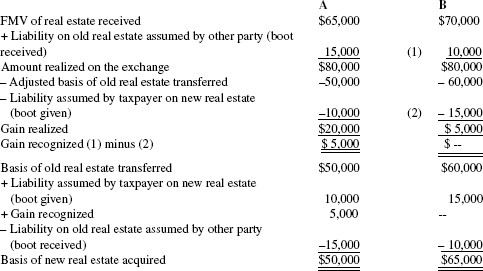

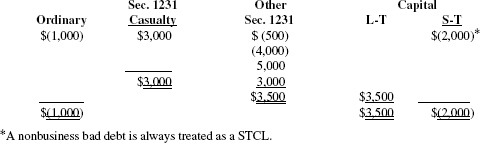

TAX TREATMENT OF GAINS AND LOSSES (OTHER THAN PERSONAL CASUALTY AND THEFT)

| Loss on condemnation of land used in business held fifteen months | $ (500) |

| Loss on sale of machinery used in business held two months | (1,000) |

| Bad debt loss on loan made three years ago to friend | (2,000) |

| Gain from insurance reimbursement for tornado damage to business property held ten years | 3,000 |

| Loss on sale of business equipment held three years | (4,000) |

| Gain on sale of land held four years and used in business | 5,000 |

KEY TERMS

Adjusted basis. The original cost or other basis of property increased by capital improvements and reduced by depreciation and losses.

Boot. Cash or other property not permitted to be received tax-free in certain nontaxable transactions. The receipt of boot will generally cause a realized gain to be recognized to the extent of the lesser of the fair market value of such boot received or the amount of realized gain.

Capital asset. Generally all assets except inventory, notes and accounts receivable, and depreciable and non depreciable property used in a trade or business. Capital assets generally consist of property held for investment and property held for personal use.

Involuntary conversion. Occurs when money or other property is received for property that has been destroyed, damaged, stolen, or condemned. Generally the recognition of any realized gain resulting from an involuntary conversion can, at the taxpayer’s election, be deferred if the taxpayer reinvests the proceeds of conversion within a specified period of time in property that is similar or related in service or use.

Like-kind exchange. An exchange of property held for productive use in a trade or business or for investment (excluding inventory, stocks and bonds, and partnership interests) for property of a like kind. Real property must be exchanged for real property, personal property must be exchanged for personal property within the same general asset class. Generally no gain is recognized unless unlike property (boot) is received.

Long-term capital gain or loss. Gain or loss realized from the sale or exchange of a capital asset held for more than one year.

Related-taxpayer transactions. Generally no loss can be recognized from the sale or exchange of property between related taxpayers. Related taxpayers included members of a family (spouse, brothers, sisters, ancestors, and lineal descendants), and an individual and a more than 50% owned entity. Additionally, gains resulting from transactions between related taxpayers that might otherwise be classified as capital or Sec. 1231 gains may instead be taxed as ordinary income.

Section 1231 property. Depreciable and nondepreciable property used in a trade or business and held for more than one year. Inventory, accounts and notes receivable, US government publications, copyrights, literary, musical, or artistic compositions in the hands of their creator are excluded from the definition.

Section 1245 property. Generally depreciable personal property used in a trade or business or held for the production of income (e.g., machinery, equipment, trucks, autos).

Section 1245 recapture. The gain from the sale or exchange of Sec. 1245 property must be reported as ordinary income to the extent of the lesser of (1) all depreciation (including straight-line), or the recognized gain.

Section 1250 property. Any real property (e.g., building) that (1) is not Sec. 1245 property and (2) is subject to the allowance of depreciation.

Section 1250 recapture. The gain from the sale or exchange of Sec. 1250 property must be reported as ordinary income to the extent that actual depreciation deductions exceeded what straight-line would have been. If Sec. 1250 property was held twelve months or less, gain on disposition is recaptured as ordinary income to the extent of all depreciation (including straight-line).

Wash sale. A loss from the sale of stock or securities is disallowed because the taxpayer, within 30 days before or after the sale, has acquired stock or securities that are substantially identical to those sold.

Multiple-Choice Questions (1–62)

A.1. Basis of Property

1. Ralph Birch purchased land and a building which will be used in connection with Birch’s business. The costs associated with this purchase are as follows:

| Cash down payment | $ 40,000 |

| Mortgage on property | 350,000 |

| Survey costs | 2,000 |

| Title and transfer taxes | 2,500 |

| Charges for hookup of gas, water, and sewer lines | 3,000 |

| Back property taxes owed by the seller that were paid by Birch | 5,000 |

What is Birch’s tax basis for the land and building?

a. $ 44,500

b. $394,500

c. $397,500

d. $402,500

2. Fred Berk bought a plot of land with a cash payment of $40,000 and a purchase money mortgage of $50,000. In addition, Berk paid $200 for a title insurance policy. Berk’s basis in this land is

a. $40,000

b. $40,200

c. $90,000

d. $90,200

A.1.c. Acquired by Gift

3. Smith made a gift of property to Thompson. Smith’s basis in the property was $1,200. The fair market value at the time of the gift was $1,400. Thompson sold the property for $2,500. What was the amount of Thompson’s gain on the disposition?

a. $0

b. $1,100

c. $1,300

d. $2,500

4. Julie received a parcel of land as a gift from her Aunt Agnes. At the time of the gift, the land had a fair market value of $84,000 and an adjusted basis of $24,000. This was the only gift that Julie received from Agnes during 2013. If Agnes paid a gift tax of $14,000 on the transfer of the gift to Julie, what tax basis will Julie have for the land?

a. $23,000

b. $35,000

c. $36,000

d. $84,000

Items 5 and 6 are based on the following data:

In 2010 Iris King bought shares of stock as an investment, at a cost of $10,000. During 2012, when the fair market value was $8,000, Iris gave the stock to her daughter, Ruth.

5. If Ruth sells the shares of stock in 2013 for $7,000, Ruth’s recognized loss would be

a. $3,000

b. $2,000

c. $1,000

d. $0

6. Ruth’s holding period of the stock for purposes of determining her loss

a. Started in 2010.

b. Started in 2012.

c. Started in 2013.

d. Is irrelevant because Ruth received the stock for no consideration of money or money’s worth.

Items 7 through 9 are based on the following data:

Laura’s father, Albert, gave Laura a gift of 500 shares of Liba Corporation common stock in 2012. Albert’s basis for the Liba stock was $4,000. At the date of this gift, the fair market value of the Liba stock was $3,000.

7. If Laura sells the 500 shares of Liba stock in 2013 for $5,000, her basis is

a. $5,000

b. $4,000

c. $3,000

d. $0

8. If Laura sells the 500 shares of Liba stock in 2013 for $2,000, her basis is

a. $4,000

b. $3,000

c. $2,000

d. $0

9. If Laura sells the 500 shares of Liba stock in 2013 for $3,500, what is the reportable gain or loss in 2013?

a. $3,500 gain.

b. $ 500 gain.

c. $ 500 loss.

d. $0.

A.1.d. Acquired from Decedent

10. On June 1, 2013, Ben Rork sold 500 shares of Kul Corp. stock. Rork had received this stock on May 1, 2013, as a bequest from the estate of his uncle, who died on February 1, 2013. Rork’s basis was determined by reference to the stock’s fair market value on February 1, 2013. Rork’s holding period for this stock was

a. Short-term.

b. Long-term.

c. Short-term if sold at a gain; long-term if sold at a loss.

d. Long-term if sold at a gain; short-term if sold at a loss.

11. Fred Zorn died on June 5, 2013, bequeathing his entire $6,000,000 estate to his sister, Ida. The alternate valuation date was validly elected by the executor of Fred’s estate. Fred’s estate included 2,000 shares of listed stock for which Fred’s basis was $380,000. This stock was distributed to Ida nine months after Fred’s death. Fair market values of this stock were

| At the date of Fred’s death | $400,000 |

| Six months after Fred’s death | 450,000 |

| Nine months after Fred’s death | 480,000 |

Ida’s basis for this stock is

a. $380,000

b. $400,000

c. $450,000

d. $480,000

Items 12 and 13 are based on the following data:

On October 1, 2013, Lois Rice learned that she was bequeathed 1,000 shares of Elin Corp. common stock under the will of her uncle, Pat Prevor. Pat had paid $5,000 for the Elin stock in 2009. Fair market value of the Elin stock on October 1, 2013, the date of Pat’s death, was $8,000 and had increased to $11,000 six months later. The executor of Pat’s estate elected the alternative valuation for estate tax purposes. Lois sold the Elin stock for $9,000 on December 1, 2013, the date that the executor distributed the stock to her.

12. Lois’ basis for gain or loss on sale of the 1,000 shares of Elin stock is

a. $ 5,000

b. $ 8,000

c. $ 9,000

d. $11,000

13. Lois should treat the 1,000 shares of Elin stock as a

a. Short-term Section 1231 asset.

b. Long-term Section 1231 asset.

c. Short-term capital asset.

d. Long-term capital asset.

A.1.e. Stock Received as a Dividend

Items 14 and 15 are based on the following data:

In January 2013, Joan Hill bought one share of Orban Corp. stock for $300. On March 1, 2013, Orban distributed one share of preferred stock for each share of common stock held. This distribution was nontaxable. On March 1, 2013, Joan’s one share of common stock had a fair market value of $450, while the preferred stock had a fair market value of $150.

14. After the distribution of the preferred stock, Joan’s bases for her Orban stocks are

| Common | Preferred | |

| a. | $300 | $0 |

| b. | $225 | $ 75 |

| c. | $200 | $100 |

| d. | $150 | $150 |

15. The holding period for the preferred stock starts in

a. January 2013.

b. March 2013.

c. September 2013.

d. December 2013.

16. On July 1, 2008, Lila Perl paid $90,000 for 450 shares of Janis Corp. common stock. Lila received a nontaxable stock dividend of 50 new common shares in August 2013. On December 20, 2013, Lila sold the 50 new shares for $11,000. How much should Lila report in her 2013 return as long-term capital gain?

a. $0

b. $ 1,000

c. $ 2,000

d. $11,000

A.4.a. Like-Kind Exchange

17. Tom Gow owned a parcel of investment real estate that had an adjusted basis of $25,000 and a fair market value of $40,000. During 2013, Gow exchanged his investment real estate for the items of property listed below.

| Land to be held for investment (fair market value) | $35,000 |

| A small sailboat to be held for personal use (fair market value) | 3,000 |

| Cash | 2,000 |

What is Tom Gow’s recognized gain and basis in his new investment real estate?

| Gain recognized | Basis for real estate | |

| a. | $2,000 | $22,000 |

| b. | $2,000 | $25,000 |

| c. | $5,000 | $25,000 |

| d. | $5,000 | $35,000 |

18. In a “like-kind” exchange of an investment asset for a similar asset that will also be held as an investment, no taxable gain or loss will be recognized on the transaction if both assets consist of

a. Convertible debentures.

b. Convertible preferred stock.

c. Partnership interests.

d. Rental real estate located in different states.

19. Pat Leif owned an apartment house that he bought in 2000. Depreciation was taken on a straight-line basis. In 2013, when Pat’s adjusted basis for this property was $200,000, he traded it for an office building having a fair market value of $600,000. The apartment house has 100 dwelling units, while the office building has 40 units rented to business enterprises. The properties are not located in the same city. What is Pat’s reportable gain on this exchange?

a. $400,000 Section 1250 gain.

b. $400,000 Section 1231 gain.

c. $400,000 long-term capital gain.

d. $0.

20. On July 1, 2013, Riley exchanged investment real property, with an adjusted basis of $160,000 and subject to a mortgage of $70,000, and received from Wilson $30,000 cash and other investment real property having a fair market value of $250,000. Wilson assumed the mortgage. What is Riley’s recognized gain in 2013 on the exchange?

a. $ 30,000

b. $ 70,000

c. $ 90,000

d. $100,000

21. On October 1, 2013, Donald Anderson exchanged an apartment building having an adjusted basis of $375,000 and subject to a mortgage of $100,000 for $25,000 cash and another apartment building with a fair market value of $550,000 and subject to a mortgage of $125,000. The property transfers were made subject to the outstanding mortgages. What amount of gain should Anderson recognize in his tax return for 2013?

a. $0

b. $ 25,000

c. $125,000

d. $175,000

22. The following information pertains to the acquisition of a six-wheel truck by Sol Barr, a self-employed contractor:

| Cost of original truck traded in | $20,000 |

| Book value of original truck at trade-in date | 4,000 |

| List price of new truck | 25,000 |

| Trade-in allowance for old truck | 6,000 |

| Business use of both trucks | 100% |

The basis of the new truck is

a. $27,000

b. $25,000

c. $23,000

d. $19,000

A.4.b. Involuntary Conversions

23. An office building owned by Elmer Bass was condemned by the state on January 2, 2012. Bass received the condemnation award on March 1, 2013. In order to qualify for nonrecognition of gain on this involuntary conversion, what is the last date for Bass to acquire qualified replacement property?

a. August 1, 2014.

b. January 2, 2015.

c. March 1, 2016.

d. December 31, 2016.

A.4.c. Sale or Exchange of Residence

24. In March 2013, Davis, who is single, purchased a new residence for $200,000. During that same month he sold his former residence for $380,000 and paid the realtor a $20,000 commission. The former residence, his first home, had cost $65,000 in 1994. Davis added a bathroom for $5,000 in 2009. What amount of gain is recognized from the sale of the former residence on Davis’ 2013 tax return?

a. $160,000

b. $ 90,000

c. $ 40,000

d. $0

25. The following information pertains to the sale of Al and Beth Oran’s principal residence:

| Date of sale | February 2013 |

| Date of purchase | October 1996 |

| Net sales price | $760,000 |

| Adjusted basis | $170,000 |

Al and Beth owned their home jointly and had occupied it as their principal residence since acquiring the home in 1996. In June 2013, the Orans bought a condo for $190,000 to be used as their principal residence. What amount of gain must the Orans recognize on their 2013 joint return from the sale of their residence?

a. $ 90,000

b. $150,000

c. $340,000

d. $400,000

26. Ryan, age fifty-seven, is single with no dependents. In January 2013, Ryan’s principal residence was sold for the net amount of $400,000 after all selling expenses. Ryan bought the house in 2000 and occupied it until sold. On the date of sale, the house had a basis of $180,000. Ryan does not intend to buy another residence. What is the maximum exclusion of gain on sale of the residence that may be claimed in Ryan’s 2013 income tax return?

a. $250,000

b. $220,000

c. $125,000

d. $0

A.5. Sales and Exchanges of Securities

27. Miller, an individual calendar-year taxpayer, purchased 100 shares of Maples Inc. common stock for $10,000 on July 10, 2012, and an additional fifty shares of Maples Inc. common stock for $4,000 on December 24, 2012. On January 8, 2013, Miller sold the 100 shares purchased on July 10, 2012, for $7,000. What is the amount of Miller’s recognized loss for 2013 and what is the basis for her remaining fifty shares of Maples Inc. stock?

a. $3,000 recognized loss; $4,000 basis for her remaining stock.

b. $1,500 recognized loss; $5,500 basis for her remaining stock.

c. $1,500 recognized loss; $4,000 basis for her remaining stock.

d. $0 recognized loss; $7,000 basis for her remaining stock.

28. Smith, an individual calendar-year taxpayer, purchased 100 shares of Core Co. common stock for $15,000 on December 15, 2012, and an additional 100 shares for $13,000 on December 30, 2012. On January 3, 2013, Smith sold the shares purchased on December 15, 2012, for $13,000. What amount of loss from the sale of Core stock is deductible on Smith’s 2012 and 2013 income tax returns?

| 2012 | 2013 | |

| a. | $0 | $0 |

| b. | $0 | $2,000 |

| c. | $1,000 | $1,000 |

| d. | $2,000 | $0 |

29. On March 10, 2013, James Rogers sold 300 shares of Red Company common stock for $4,200. Rogers acquired the stock in 2010 at a cost of $5,000.

On April 4, 2013, he repurchased 300 shares of Red Company common stock for $3,600 and held them until July 18, 2013, when he sold them for $6,000.

How should Rogers report the above transactions for 2013?

a. A long-term capital loss of $800.

b. A long-term capital gain of $1,000.

c. A long-term capital gain of $1,600.

d. A long-term capital loss of $800 and a short-term capital gain of $2,400.

30. Murd Corporation, a domestic corporation, acquired a 90% interest in the Drum Company in 2009 for $30,000. During 2013, the stock of Drum was declared worthless. What type and amount of deduction should Murd take for 2013?

a. Long-term capital loss of $1,000.

b. Long-term capital loss of $15,000.

c. Ordinary loss of $30,000.

d. Long-term capital loss of $30,000.

A.6. Losses on Deposits in Insolvent Financial Institutions

31. If an individual incurs a loss on a nonbusiness deposit as the result of the insolvency of a bank, credit union, or other financial institution, the individual’s loss on the nonbusiness deposit may be deducted in any one of the following ways except:

a. Miscellaneous itemized deduction.

b. Casualty loss.

c. Short-term capital loss.

d. Long-term capital loss.

A.7. Losses, Expenses, and Interest between Related Taxpayers

Items 32 and 33 are based on the following:

Conner purchased 300 shares of Zinco stock for $30,000 in 2009. On May 23, 2013, Conner sold all the stock to his daughter Alice for $20,000, its then fair market value. Conner realized no other gain or loss during 2013. On July 26, 2013, Alice sold the 300 shares of Zinco for $25,000.

32. What amount of the loss from the sale of Zinco stock can Conner deduct in 2013?

a. $0

b. $ 3,000

c. $ 5,000

d. $10,000

33. What was Alice’s recognized gain or loss on her sale?

a. $0.

b. $5,000 long-term gain.

c. $5,000 short-term loss.

d. $5,000 long-term loss.

34. In 2013, Fay sold 100 shares of Gym Co. stock to her son, Martin, for $11,000. Fay had paid $15,000 for the stock in 2009. Subsequently in 2013, Martin sold the stock to an unrelated third party for $16,000. What amount of gain from the sale of the stock to the third party should Martin report on his 2013 income tax return?

a. $0

b. $1,000

c. $4,000

d. $5,000

35. Among which of the following related parties are losses from sales and exchanges not recognized for tax purposes?

a. Mother-in-law and daughter-in-law.

b. Uncle and nephew.

c. Brother and sister.

d. Ancestors, lineal descendants, and all in-laws.

36. On May 1, 2013, Daniel Wright owned stock (held for investment) purchased two years earlier at a cost of $10,000 and having a fair market value of $7,000. On this date he sold the stock to his son, William, for $7,000. William sold the stock for $6,000 to an unrelated person on July 1, 2013. How should William report the stock sale on his 2013 tax return?

a. As a short-term capital loss of $1,000.

b. As a long-term capital loss of $1,000.

c. As a short-term capital loss of $4,000.

d. As a long-term capital loss of $4,000.

37. Al Eng owns 50% of the outstanding stock of Rego Corp. During 2013, Rego sold a trailer to Eng for $10,000, the trailer’s fair value. The trailer had an adjusted tax basis of $12,000, and had been owned by Rego and used in its business for three years. In its 2013 income tax return, what is the allowable loss that Rego can claim on the sale of this trailer?

a. $0

b. $2,000 capital loss.

c. $2,000 Section 1231 loss.

d. $2,000 Section 1245 loss.

B. Capital Gains and Losses

38. For a cash basis taxpayer, gain or loss on a year-end sale of listed stock arises on the

a. Trade date.

b. Settlement date.

c. Date of receipt of cash proceeds.

d. Date of delivery of stock certificate.

39. Lee qualified as head of a household for 2013 tax purposes. Lee’s 2013 taxable income was $100,000, exclusive of capital gains and losses. Lee had a net long-term capital loss of $8,000 in 2013. What amount of this capital loss can Lee offset against 2013 ordinary income?

a. $0

b. $3,000

c. $4,000

d. $8,000

40. For the year ended December 31, 2013, Sol Corp. had an operating income of $20,000. In addition, Sol had capital gains and losses resulting in a net short-term capital gain of $2,000 and a net long-term capital loss of $7,000. How much of the excess of net long-term capital loss over net short-term capital gain could Sol offset against ordinary income for 2013?

a. $5,000

b. $3,000

c. $1,500

d. $0

41. In 2013, Nam Corp., which is not a dealer in securities, realized taxable income of $160,000 from its business operations. Also, in 2013, Nam sustained a long-term capital loss of $24,000 from the sale of marketable securities. Nam did not realize any other capital gains or losses since it began operations. In Nam’s income tax returns, what is the proper treatment for the $24,000 long-term capital loss?

a. Use $3,000 of the loss to reduce 2013 taxable income, and carry $21,000 of the long-term capital loss forward for five years.

b. Use $6,000 of the loss to reduce 2013 taxable income by $3,000, and carry $18,000 of the long-term capital loss forward for five years.

c. Use $24,000 of the long-term capital loss to reduce 2013 taxable income by $12,000.

d. Carry the $24,000 long-term capital loss forward for five years, treating it as a short-term capital loss.

42. For assets acquired in 2013, the holding period for determining long-term capital gains and losses is more than

a. 18 months.

b. 12 months.

c. 9 months.

d. 6 months.

43. On July 1, 2013, Kim Wald sold an antique for $12,000 that she had bought for her personal use in 2011 at a cost of $15,000. In her 2013 return, Kim should treat the sale of the antique as a transaction resulting in

a. A nondeductible loss.

b. Ordinary loss.

c. Short-term capital loss.

d. Long-term capital loss.

44. Paul Beyer, who is unmarried, has taxable income of $30,000 exclusive of capital gains and losses and his personal exemption. In 2013, Paul incurred a $1,000 net short-term capital loss and a $5,000 net long-term capital loss. His capital loss carryover to 2014 is

a. $0

b. $1,000

c. $3,000

d. $5,000

B.1. Capital Assets

45. Capital assets include

a. A corporation’s accounts receivable from the sale of its inventory.

b. Seven-year MACRS property used in a corporation’s trade or business.

c. A manufacturing company’s investment in US Treasury bonds.

d. A corporate real estate developer’s unimproved land that is to be subdivided to build homes, which will be sold to customers.

46. Joe Hall owns a limousine for use in his personal service business of transporting passengers to airports. The limousine’s adjusted basis is $40,000. In addition, Hall owns his personal residence and furnishings, that together cost him $280,000. Hall’s capital assets amount to

a. $320,000

b. $280,000

c. $ 40,000

d. $0

47. In 2013, Ruth Lee sold a painting for $25,000 that she had bought for her personal use in 2007 at a cost of $10,000. In her 2013 return, Lee should treat the sale of the painting as a transaction resulting in

a. Ordinary income.

b. Long-term capital gain.

c. Section 1231 gain.

d. No taxable gain.

48. In 2013, a capital loss incurred by a married couple filing a joint return

a. Will be allowed only to the extent of capital gains.

b. Will be allowed to the extent of capital gains, plus up to $3,000 of ordinary income.

c. Will be allowed to the extent of capital gains, plus up to $6,000 of ordinary income.

d. Is not an allowable loss.

49. Platt owns land that is operated as a parking lot. A shed was erected on the lot for the related transactions with customers. With regard to capital assets and Section 1231 assets, how should these assets be classified?

| Land | Shed | |

| a. | Capital | Capital |

| b. | Section 1231 | Capital |

| c. | Capital | Section 1231 |

| d. | Section 1231 | Section 1231 |

50. In 2009, Iris King bought a diamond necklace for her own use, at a cost of $10,000. In 2013, when the fair market value was $12,000, Iris gave this necklace to her daughter, Ruth. No gift tax was due. This diamond necklace is a

a. Capital asset.

b. Section 1231 asset.

c. Section 1245 asset.

d. Section 1250 asset.

51. Which of the following is a capital asset?

a. Delivery truck.

b. Personal-use recreation equipment.

c. Land used as a parking lot for customers.

d. Treasury stock, at cost.

52. Don Mott was the sole proprietor of a high-volume drug store which he owned for fifteen years before he sold it to Dale Drug Stores, Inc. in 2013. Besides the $900,000 selling price for the store’s tangible assets and goodwill, Mott received a lump sum of $30,000 in 2013 for his agreement not to operate a competing enterprise within ten miles of the store’s location for a period of six years. The $30,000 will be taxed to Mott as

a. $30,000 ordinary income in 2013.

b. $30,000 short-term capital gain in 2013.

c. $30,000 long-term capital gain in 2013.

d. Ordinary income of $5,000 a year for six years.

53. In June 2013, Olive Bell bought a house for use partially as a residence and partially for operation of a retail gift shop. In addition, Olive bought the following furniture:

| Kitchen set and living room pieces for the residential portion |

$ 8,000 |

| Showcases and tables for the business portion | 12,000 |

How much of this furniture comprises capital assets?

a. $0

b. $ 8,000

c. $12,000

d. $20,000

C. Personal Casualty and Theft Gains and Losses

54. An individual’s losses on transactions entered into for personal purposes are deductible only if

a. The losses qualify as casualty or theft losses.

b. The losses can be characterized as hobby losses.

c. The losses do not exceed $3,000 ($6,000 on a joint return).

d. No part of the transactions was entered into for profit.

D. Gains and Losses on Business Property

55. Evon Corporation, which was formed in 2010, had $50,000 of net Sec. 1231 gain for its 2013 calendar year. Its net Sec. 1231 gains and losses for its three preceding tax years were as follows:

| Year | Sec. 1231 results |

| 2010 | Gain of $10,000 |

| 2011 | Loss of $15,000 |

| 2012 | Loss of $20,000 |

As a result, Evon Corporation’s 2013 net Sec. 1231 gain would be characterized as

a. A net long-term capital gain of $50,000.

b. A net long-term capital gain of $35,000 and ordinary income of $15,000.

c. A net long-term capital gain of $25,000 and ordinary income of $25,000.

d. A net long-term capital gain of $15,000 and ordinary income of $35,000.

56. Which one of the following would not be Sec. 1231 property even though held for more than twelve months?

a. Business inventory.

b. Unimproved land used for business.

c. Depreciable equipment used in a business.

d. Depreciable real property used in a business.

57. Vermont Corporation distributed packaging equipment that it no longer needed to Michael Jason who owns 20% of Vermont’s stock. The equipment, which was acquired in 2008, had an adjusted basis of $2,000 and a fair market value of $9,000 at the date of distribution. Vermont had properly deducted $6,000 of straight-line depreciation on the equipment while it was used in Vermont’s manufacturing activities. What amount of ordinary income must Vermont recognize as a result of the distribution of the equipment?

a. $0

b. $3,000

c. $6,000

d. $7,000

58. Tally Corporation sold machinery that had been used in its business for a loss of $22,000 during 2013. The machinery had been purchased and placed in service sixteen months earlier. For 2013, the $22,000 loss will be treated as a

a. Capital loss.

b. Sec. 1245 loss.

c. Sec. 1231 loss.

d. Casualty loss because the machinery was held less than two years.

59. On January 2, 2011, Bates Corp. purchased and placed into service seven-year MACRS tangible property costing $100,000. On July 31, 2013, Bates sold the property for $102,000, after having taken $47,525 in MACRS depreciation deductions. What amount of the gain should Bates recapture as ordinary income?

a. $0

b. $ 2,000

c. $47,525

d. $49,525

60. Thayer Corporation purchased an apartment building on January 1, 2010, for $200,000. The building was depreciated using the straight-line method. On December 31, 2013, the building was sold for $220,000, when the asset balance net of accumulated depreciation was $170,000. On its 2013 tax return, Thayer should report

a. Section 1231 gain of $42,500 and ordinary income of $7,500.

b. Section 1231 gain of $44,000 and ordinary income of $6,000.

c. Ordinary income of $50,000.

d. Section 1231 gain of $50,000.

61. For the year ended December 31, 2013, McEwing Corporation, a calendar-year corporation, reported book income before income taxes of $120,000. Included in the determination of this amount were the following gain and losses from property that had been held for more than one year:

| Loss on sale of building depreciated on the straight-line method |

$(7,000) |

| Gain on sale of land used in McEwing’s business |

16,000 |

| Loss on sale of investments in marketable securities |

(8,000) |

For the year ended December 31, 2013, McEwing’s taxable income was

a. $113,000

b. $120,000

c. $125,000

d. $128,000

62. David Price owned machinery which he had acquired in 2012 at a cost of $100,000. During 2013, the machinery was destroyed by fire. At that time it had an adjusted basis of $86,000. The insurance proceeds awarded to Price amounted to $125,000, and he immediately acquired a similar machine for $110,000.

What should Price report as ordinary income resulting from the involuntary conversion for 2013?

a. $14,000

b. $15,000

c. $25,000

d. $39,000

Multiple-Choice Answers and Explanations

Answers

Explanations

1. (d) The requirement is to determine Birch’s tax basis for the purchased land and building. The basis of property acquired by purchase is a cost basis and includes not only the cash paid and liabilities incurred, but also includes certain settlement fees and closing costs such as abstract of title fees, installation of utility services, legal fees (including title search, contract, and deed fees), recording fees, surveys, transfer taxes, owner’s title insurance, and any amounts the seller owes that the buyer agrees to pay, such as back taxes and interest, recording or mortgage fees, charges for improvements or repairs, and sales commissions.

2. (d) The requirement is to determine the basis for the purchased land. The basis of the land consists of the cash paid ($40,000), the purchase money mortgage ($50,000), and the cost of the title insurance policy ($200), a total of $90,200.

3. (c) The requirement is to determine the amount of gain recognized by Thompson resulting from the sale of appreciated property received as a gift. A donee’s basis for appreciated property received as a gift is generally the same as the donor’s basis. Since Smith had a basis for the property of $1,200 and Thompson sold the property for $2,500, Thompson must recognize a gain of $1,300.

4. (c) The requirement is to determine Julie’s basis for the land received as a gift. A donee’s basis for gift property is generally the same as the donor’s basis, increased by any gift tax paid that is attributable to the property’s net appreciation in value. That is, the amount of gift tax that can be added is limited to the amount that bears the same ratio as the property’s net appreciation bears to the amount of taxable gift. For this purpose, the amount of gift is reduced by any portion of the $14,000 annual exclusion that is allowable with respect to the gift. Thus, Julie’s basis is $24,000 + [$14,000 ($84,000 − 24,000) / ($84,000 − $14,000)] = $36,000.

5. (c) The requirement is to determine Ruth’s recognized loss if she sells the stock received as a gift for $7,000. Since the stock’s FMV ($8,000) was less than its basis ($10,000) at date of gift, Ruth’s basis for computing a loss is the stock’s FMV of $8,000 at date of gift. As a result, Ruth’s recognized loss is $8,000 − $7,000 = $1,000.

6. (b) The requirement is to determine Ruth’s holding period for stock received as a gift. If property is received as a gift, and the property’s FMV on date of gift is used to determine a loss, the donee’s holding period begins when the gift was received. Thus, Ruth’s holding period starts in 2012.

7. (b) The requirement is to determine the basis of the Liba stock if it is sold for $5,000. If property acquired by gift is sold at a gain, its basis is the donor’s basis ($4,000), increased by any gift tax paid attributable to the net appreciation in value of the gift ($0).

8. (b) The requirement is to determine the basis of the Liba stock if it is sold for $2,000. If property acquired by gift is sold at a loss, its basis is the lesser of (1) its gain basis ($4,000 above), or (2) its FMV at date of gift ($3,000).

9. (d) The requirement is to determine the amount of reportable gain or loss if the Liba stock is sold for $3,500. No gain or loss is recognized on the sale of property acquired by gift if the basis for loss ($3,000) results in a gain and the basis for gain ($4,000) results in a loss.

10. (b) The requirement is to determine the holding period for stock received as a bequest from the estate of a deceased uncle. Property received from a decedent is deemed to be held long-term regardless of the actual period of time that the decedent or beneficiary actually held the property and is treated as held for more than twelve months.

11. (c) The requirement is to determine Ida’s basis for stock inherited from a decedent. The basis of property received from a decedent is generally the property’s FMV at date of the decedent’s death, or FMV on the alternate valuation date (six months after death). Since the executor of Zorn’s estate elected to use the alternate valuation for estate tax purposes, the stock’s basis to Ida is its $450,000 FMV six months after Zorn’s death. Note, if the stock had been distributed to Ida within six months of Zorn’s death, the stock’s basis would be its FMV on date of distribution.

12. (c) The requirement is to determine Lois’ basis for gain or loss on the sale of Elin stock acquired from a decedent. Since the alternate valuation was elected for Prevor’s estate, but the stock was distributed to Lois within six months of date of death, Lois’ basis is the $9,000 FMV of the stock on date of distribution (12/1/13).

13. (d) The requirement is to determine how Lois should treat the shares of Elin stock that she inherited from her uncle who died during 2012. The stock should be treated as a capital asset held long-term since (1) property acquired from a decedent is considered to be held for more than twelve months regardless of its actual holding period, and (2) the stock is an investment asset in Lois’ hands. The stock is not a Sec. 1231 asset because it was not held for use in Lois’ trade or business.

14. (b) The requirement is to determine the basis for the common stock and the preferred stock after the receipt of a nontaxable preferred stock dividend. Joan’s original common stock basis must be allocated between the common stock and the preferred stock according to their relative fair market value.

| Common stock (FMV) | $450 |

| Preferred stock (FMV) | 150 |

| Total value | $600 |

The ratio of the common stock to total value is $450/$600 or 3/4. This ratio multiplied by the original common stock basis of $300 results in a basis for the common stock of $225. The basis of the preferred stock would be ($150/$600 × $300) = $75.

15. (a) The requirement is to determine the holding period for preferred stock that was received in a nontaxable distribution on common stock. Since the tax basis of the preferred stock is determined in part by the basis of the common stock, the holding period of the preferred stock includes the holding period of the common stock (i.e., the holding period of the common stock tacks on to the preferred stock). Thus, the holding period of the preferred stock starts when the common stock was acquired, January 2013.

16. (c) The requirement is to determine the amount of long-term capital gain to be reported on the sale of fifty shares of stock received as a nontaxable stock dividend. After the stock dividend, the basis of each share would be determined as follows:

Since the holding period of the new shares includes the holding period of the old shares, the sale of the fifty new shares for $11,000 results in a LTCG of $2,000 [$11,000 − (50 shares × $180)].

17. (c) The requirement is to determine Gow’s recognized gain and basis for the investment real estate acquired in a like-kind exchange. In a like-kind exchange of property held for investment, a realized gain ($15,000 in this case) will be recognized only to the extent of unlike property (i.e., boot) received. Here the unlike property consists of the $2,000 cash and $3,000 FMV of the sailboat received, resulting in the recognition of $5,000 of gain. The basis of the acquired like-kind property reflects the deferred gain resulting from the like-kind exchange, and is equal to the basis of the property transferred ($25,000), increased by the amount of gain recognized ($5,000), and decreased by the amount of boot received ($2,000 + $3,000), or $25,000.

18. (d) The requirement is to determine which exchange qualifies for nonrecognition of gain or loss as a like-kind exchange. The exchange of business or investment property solely for like-kind business or investment property is treated as a nontaxable exchange. Like-kind means “the same class of property.” Real property must be exchanged for real property, and personal property must be exchanged for personal property. Here, the exchange of rental real estate is an exchange of like-kind property, even though the real estate is located in different states. The like-kind exchange provisions do not apply to exchanges of stocks, bonds, notes, convertible securities, the exchange of partnership interests, and property held for personal use.

19. (d) The requirement is to determine the reportable gain resulting from the exchange of an apartment building for an office building. No gain or loss is recognized on the exchange of business or investment property for property of a like-kind. The term “like-kind” means the same class of property (i.e., real estate must be exchanged for real estate, personal property exchanged for personal property). Thus, the exchange of an apartment building for an office building qualifies as a like-kind exchange. Since no boot (money or unlike property) was received, the realized gain of $600,000 − $200,000 = $400,000 is not recognized.

20. (d) The requirement is to determine the amount of recognized gain resulting from a like-kind exchange of investment property. In a like-kind exchange, gain is recognized to the extent of the lesser of (1) “boot” received, or (2) gain realized.

| FMV of property received | $ 250,000 |

| Cash received | 30,000 |

| Mortgage assumed | 70,000 |

| Amount realized | $ 350,000 |

| Basis of property exchanged | (160,000) |

| Gain realized | $190,000 |

Since the “boot” received includes both the cash and the assumption of the mortgage, gain is recognized to the extent of the $100,000 of “boot” received.

21. (b) The requirement is to determine the amount of gain recognized to Anderson on the like-kind exchange of apartment buildings. Anderson’s realized gain is computed as follows:

| FMV of building received | $550,000 | |

| Mortgage on old building | 100,000 | |

| Cash received | 25,000 | |

| Amount realized | $675,000 | |

| Less: | ||

| Basis of old building | $375,000 | |

| Mortgage on new building | 125,000 | 500,000 |

| Realized gain | $175,000 |

Since the boot received in the form of cash cannot be offset against boot given in the form of an assumption of a mortgage, the realized gain is recognized to the extent of the $25,000 cash received.

22. (c) The requirement is to determine the basis of a new truck acquired in a like-kind exchange. The basis of the new truck is the book value (i.e., adjusted basis) of the old truck of $4,000 plus the additional cash paid of $19,000 (i.e., the list price of the new truck of $25,000 less the trade-in allowance of $6,000).

23. (d) The requirement is to determine the end of the replacement period for nonrecognition of gain following the condemnation of real property. For a condemnation of real property held for productive use in a trade or business or for investment, the replacement period ends three years after the close of the taxable year in which the gain is first realized. Since the gain was realized in 2013, the replacement period ends December 31, 2016.

24. (c) The requirement is to determine the amount of gain from the sale of the former residence that is recognized on Davis’ 2013 return. An individual may exclude from income up to $250,000 of gain that is realized on the sale or exchange of a residence, if the individual owned and occupied the residence as a principal residence for an aggregate of at least two of the five years preceding the sale or exchange. Davis’ former residence cost $65,000 and he had made improvements costing $5,000, resulting in a basis of $70,000. Since Davis sold his former residence for $380,000 and paid a realtor commission of $20,000, the net amount realized from the sale was $360,000. Thus, Davis realized a gain of $360,000 − $70,000 = $290,000. Since Davis qualifies to exclude $250,000 of the gain from income, the remaining $40,000 of gain is recognized and included in Davis’ income for 2013.

25. (a) The requirement is to determine the amount of gain to be recognized on the Orans’ 2013 joint return from the sale of their residence. An individual may exclude from income up to $250,000 of gain that is realized on the sale or exchange of a residence, if the individual owned and occupied the residence as a principal residence for an aggregate of at least two of the five years preceding the sale or exchange. The amount of excludable gain is increased to $500,000 for married individuals filing jointly if either spouse meets the ownership requirement, and both spouses meet the use requirement. Here, the Orans realized a gain of $760,000 − $170,000 = $590,000, and qualify to exclude $500,000 of the gain from income. The remaining $90,000 of gain is recognized and taxed to the Orans for 2013.

26. (b) The requirement is to determine the maximum exclusion of gain on the sale of Ryan’s principal residence. An individual may exclude from income up to $250,000 of gain that is realized on the sale or exchange of a residence, if the individual owned and occupied the residence as a principal residence for an aggregate of at least two of the five years preceding the sale or exchange. Since Ryan meets the ownership and use requirements, and realized a gain of $400,000 − $180,000 = $220,000, all of Ryan’s gain will be excluded from his gross income.

27. (b) The requirement is to determine Miller’s recognized loss and the basis for her remaining fifty shares of Maples Inc. stock. No loss can be deducted on the sale of stock if substantially identical stock is purchased within thirty days before or after the sale. Any loss that is not deductible because of this rule is added to the basis of the new stock. If the taxpayer acquires less than the number of shares sold, the amount of loss that cannot be recognized is determined by the ratio of the number of shares acquired to the number of shares sold. Miller purchased 100 shares of Maples stock for $10,000 and sold the stock on January 8, 2013, for $7,000, resulting in a loss of $3,000. However, only half of the loss can be deducted by Miller because on December 24, 2012 (within thirty days before the January 8, 2013 sale), Miller purchased an additional 50 shares of Maples stock. Since only $1,500 of the loss can be recognized, the $1,500 of loss not recognized is added to the basis of Miller’s remaining 50 shares resulting in a basis of $4,000 + $1,500 = $5,500.

28. (a) The requirement is to determine the amount of loss from the sale of Core stock that is deductible on Smith’s 2012 and 2013 income tax returns. No loss can be deducted on the sale of stock if substantially identical stock is purchased within thirty days before or after the sale. Any loss that is not deductible because of this rule is added to the basis of the new stock. In this case, Smith purchased 100 shares of Core stock for $15,000 and sold the stock on January 3, 2013, for $13,000, resulting in a loss of $2,000. However, the loss cannot be deducted by Smith because on December 30, 2012 (within thirty days prior to the January 3, 2013 sale), Smith purchased an additional 100 shares of Core stock. Smith’s disallowed loss of $2,000 is added to the $13,000 cost of the 100 Core shares acquired on December 30 resulting in a tax basis of $15,000 for those shares.

29. (c) The purchase of substantially identical stock within thirty days of the sale of stock at a loss is known as a wash sale. The $800 loss incurred in the wash sale ($5,000 basis less $4,200 amount realized) is disallowed. The basis of the replacement (substantially identical) stock is its cost ($3,600) plus the disallowed wash sale loss ($800). The holding period of the replacement stock includes the holding period of the wash sale stock. The amount realized ($6,000) less the basis ($4,400) results in a long-term gain of $1,600.

30. (c) Worthless securities generally receive capital loss treatment. However, if the loss is incurred by a corporation on its investment in an affiliated corporation (80% or more ownership), the loss is generally treated as an ordinary loss.

31. (d) A loss resulting from a nonbusiness deposit in an insolvent financial institution is generally treated as a nonbusiness bad debt deductible as a short-term capital loss. However, subject to certain limitations, an individual may elect to treat the loss as a casualty loss or as a miscellaneous itemized deduction.

32. (a) The requirement is to determine the amount of the $10,000 loss that Conner can deduct from the sale of stock to his daughter, Alice. Losses are disallowed on sales or exchanges of property between related taxpayers, including members of a family. For this purpose, the term family includes an individual’s spouse, brothers, sisters, ancestors, and lineal descendants (e.g., children, grandchildren, etc.). Since Conner sold the stock to his daughter, no loss can be deducted.

33. (a) The requirement is to determine the recognized gain or loss on Alice’s sale of the stock that she had purchased from her father. Losses are disallowed on sales or exchanges of property between related taxpayers, including family members. Any gain later realized by the related transferee on the subsequent disposition of the property is not recognized to the extent of the transferor’s disallowed loss. Here, her father’s realized loss of $30,000 − $20,000 = $10,000 was disallowed because he sold the stock to his daughter, Alice. Her basis for the stock is her cost of $20,000. On the subsequent sale of the stock, Alice realizes a gain of $25,000 − $20,000 = $5,000. However, this realized gain of $5,000 is not recognized because of her father’s disallowed loss of $10,000.

34. (b) The requirement is to determine the amount of gain from the sale of stock to a third party that Martin should report on his 2013 income tax return. Losses are disallowed on sales of property between related taxpayers, including family members. Any gain later realized by the transferee on the disposition of the property is not recognized to the extent of the transferor’s disallowed loss. Here, Fay’s realized loss of $15,000 − $11,000 = $4,000 is disallowed because she sold the stock to her son, Martin. Martin’s basis for the stock is his cost of $11,000. On the subsequent sale of the stock to an unrelated third party, Martin realizes a gain of $16,000 − $11,000 = $5,000. However, this realized gain of $5,000 is recognized only to the extent that it exceeds Fay’s $4,000 disallowed loss, or $1,000.

35. (c) The requirement is to determine among which of the related individuals are losses from sales and exchanges not recognized for tax purposes. No loss deduction is allowed on the sale or exchange of property between members of a family. For this purpose, an individual’s family includes only brothers, sisters, half-brothers and half-sisters, spouse, ancestors (parents, grandparents, etc.), and lineal descendants (children, grandchildren, etc.). Since in-laws and uncles are excluded from this definition of a family, a loss resulting from a sale or exchange with an uncle or between in-laws would be recognized.

36. (a) Losses are disallowed on sales between related taxpayers, including family members. Thus, Daniel’s loss of $3,000 is disallowed on the sale of stock to his son, William. William’s basis for the stock is his $7,000 cost. Since William’s stock basis is determined by his cost (not by reference to Daniel’s cost), there is no “tack-on” of Daniel’s holding period. Thus, a later sale of the stock for $6,000 on July 1 generates a $1,000 STCL for William.

37. (c) The requirement is to determine the amount of loss that Rego Corp. can deduct on a sale of its trailer to a 50% shareholder. Losses are disallowed on transactions between related taxpayers, including a corporation and a shareholder owning more than 50% of its stock. Since Al Eng owns only 50% (not more than 50%), the loss is recognized by Rego. Since the trailer was held for more than one year and used in Rego’s business, the $2,000 loss is a Sec. 1231 loss. Answer (d) is incorrect because Sec. 1245 only applies to gains.

38. (a) The requirement is to determine when gain or loss on a year-end sale of listed stock arises for a cash basis taxpayer. If stock or securities that are traded on an established securities market are sold, any resulting gain or loss is recognized on the trade date (i.e., the date on which the trade is executed) by both cash and accrual method taxpayers.

39. (b) The requirement is to determine the amount of an $8,000 net long-term capital loss that can be offset against Lee’s taxable income of $100,000. An individual’s net capital loss can be offset against ordinary income up to a maximum of $3,000 ($1,500 if married filing separately). Since a net capital loss offsets ordinary income dollar for dollar, Lee has a $3,000 net capital loss deduction for 2013 and a long-term capital loss carryover of $5,000 to 2014.

40. (d) The requirement is to determine the amount of excess of net long-term capital loss over net short-term capital gain that Sol Corp. can offset against ordinary income. A corporation’s net capital loss cannot be offset against ordinary income. Instead, a net capital loss is generally carried back three years and forward five years as a STCL to offset capital gains in those years.

41. (d) The requirement is to determine the proper treatment for a $24,000 NLTCL for Nam Corp. A corporation’s capital losses can only be used to offset capital gains. If a corporation has a net capital loss, the net capital loss cannot be currently deducted, but must be carried back three years and forward five years as a STCL to offset capital gains in those years. Since Nam had not realized any capital gains since it began operations, the $24,000 LTCL can only be carried forward for five years as a STCL.

42. (b) The requirement is to determine the holding period for determining long-term capital gains and losses. Long-term capital gains and losses result if capital assets are held more than twelve months.

43. (a) The requirement is to determine the treatment for the sale of the antique by Wald. Since the antique was held for personal use, the sale of the antique at a loss is not deductible.

44. (c) The requirement is to determine the capital loss carryover to 2014. The NSTCL and the NLTCL result in a net capital loss of $6,000. LTCLs are deductible dollar for dollar, the same as STCLs. Since an individual can deduct a net capital loss up to a maximum of $3,000, the net capital loss of $6,000 results in a capital loss deduction of $3,000 for 2013, and a long-term capital loss carryover to 2014 of $3,000.

45. (c) The requirement is to determine the item that is included in the definition of capital assets. The definition of capital assets includes property held as an investment and would include a manufacturing company’s investment in US Treasury bonds. In contrast, the definition specifically excludes accounts receivable arising from the sale of inventory, depreciable property used in a trade or business, and property held primarily for sale to customers in the ordinary course of a trade or business.

46. (b) The requirement is to determine the amount of Hall’s capital assets. The definition of capital assets includes investment property and property held for personal use (e.g., personal residence and furnishings), but excludes property used in a trade or business (e.g., limousine).

47. (b) The requirement is to determine the proper treatment for the gain recognized on the sale of a painting that was purchased in 2007 and held for personal use. The definition of “capital assets” includes investment property and property held for personal use (if sold at a gain). Because the painting was held for more than one year, the gain from the sale of the painting must be reported as a long-term capital gain. Note that if personal-use property is sold at a loss, the loss is not deductible.

48. (b) The requirement is to determine the correct treatment for a capital loss incurred by a married couple filing a joint return for 2013. Capital losses first offset capital gains, and then are allowed as a deduction of up to $3,000 against ordinary income, with any unused capital loss carried forward indefinitely. Note that a married taxpayer filing separately can only offset up to $1,500 of net capital loss against ordinary income.

49. (d) The requirement is to determine the proper classification of land used as a parking lot and a shed erected on the lot for customer transactions. The definition of capital assets includes investment property and property held for personal use, but excludes any property used in a trade or business. The definition of Sec. 1231 assets generally includes business assets held more than one year. Since the land and shed were used in conjunction with a parking lot business, they are properly classified as Sec. 1231 assets.

50. (a) The requirement is to determine the classification of Ruth’s diamond necklace. The diamond necklace is classified as a capital asset because the definition of “capital asset” includes investment property and property held for personal use. Answers (b), (c), and (d) are incorrect because Sec. 1231 generally includes only assets used in a trade or business, while Sections 1245 and 1250 only include depreciable assets.

51. (b) The requirement is to determine which asset is a capital asset. The definition of capital assets includes personal-use property, but excludes property used in a trade or business (e.g., delivery truck, land used as a parking lot). Treasury stock is not considered an asset, but instead is treated as a reduction of stockholders’ equity.

52. (a) The requirement is to determine how a lump sum of $30,000 received in 2013, for an agreement not to operate a competing enterprise, should be treated. A covenant not to compete is not a capital asset. Thus, the $30,000 received as consideration for such an agreement must be reported as ordinary income in the year received.

53. (b) The requirement is to determine the amount of furniture classified as capital assets. The definition of capital assets includes investment property and property held for personal use (e.g., kitchen and living room pieces), but excludes property used in a trade or business (e.g., showcases and tables).

54. (a) The requirement is to determine the correct statement regarding the deductibility of an individual’s losses on transactions entered into for personal purposes. An individual’s losses on transactions entered into for personal purposes are deductible only if the losses qualify as casualty or theft losses. Answer (b) is incorrect because hobby losses are not deductible. Answers (c) and (d) are incorrect because losses (other than by casualty or theft) on transactions entered into for personal purposes are not deductible.

55. (d) The requirement is to determine the characterization of Evon Corporation’s $50,000 of net Sec. 1231 gain for its 2013 tax year. Although a net Sec. 1231 gain is generally treated as a long-term capital gain, it instead must be treated as ordinary income to the extent of the taxpayer’s nonrecaptured net Sec. 1231 losses for its five preceding taxable years. Here, since the nonrecaptured net Sec. 1231 losses for 2011 and 2012 total $35,000, only $15,000 of the $50,000 net Sec. 1231 gain will be treated as a long-term capital gain.

56. (a) The requirement is to determine which item would not be characterized as Sec. 1231 property. Sec. 1231 property generally includes both depreciable and nondepreciable property used in a trade or business or held for the production of income if held for more than twelve months. Specifically excluded from Sec. 1231 is inventory and property held for sale to customers, as well as accounts and notes receivable arising in the ordinary course of a trade or business.

57. (c) The requirement is to determine the amount of ordinary income that must be recognized by Vermont Corporation from the distribution of the equipment to a shareholder. When a corporation distributes appreciated property, it must recognize gain just as if it had sold the property for its fair market value. As a result Vermont must recognize a gain of $9,000 − $2,000 = $7,000 on the distribution of the equipment. Since the distributed property is depreciable personal property, the gain is subject to Sec. 1245 recapture as ordinary income to the extent of the $6,000 of straight-line depreciation deducted by Vermont. The remaining $1,000 of gain would be treated as Sec. 1231 gain.

58. (c) The requirement is to determine the nature of a loss resulting from the sale of business machinery that had been held sixteen months. Property held for use in a trade or business is specifically excluded from the definition of capital assets, and if held for more than one year is considered Sec. 1231 property. Answer (b) is incorrect because Sec. 1245 only applies to gains.

59. (c) The requirement is to determine the amount of gain from the sale of property that must be recaptured as ordinary income. A gain from the disposition of seven-year tangible property is subject to recapture under Sec. 1245 which recaptures gain to the extent of all depreciation previously deducted. Here, Bates’ gain from the sale of the property is determined as follows:

| Selling price | $102,000 | |

| Cost | $100,000 | |

| Depreciation | –47,525 | |

| Adjusted basis | – 52,475 | |

| Gain | $49,525 |

Under Sec. 1245, Bates Corp’s gain is recaptured as ordinary income to the extent of the $47,525 deducted as depreciation. The remaining $2,000 of gain would be classified as Sec. 1231 gain.

60. (b) The requirement is to determine the proper treatment of the $50,000 gain on the sale of the building, which is Sec. 1250 property. Sec. 1250 recaptures gain as ordinary income to the extent of “excess” depreciation (i.e., depreciation deducted in excess of straight-line). The total gain less any depreciation recapture is Sec. 1231 gain. Since straight-line depreciation was used, there is no recapture under Sec. 1250. However, Sec. 291 requires that the amount of ordinary income on the disposition of Sec. 1250 property by corporations be increased by 20% of the additional amount that would have been ordinary income if the property had instead been Sec. 1245 property. If the building had been Sec. 1245 property the amount of recapture would have been $30,000 ($200,000 − $170,000). Thus, the Sec. 291 ordinary income is $30,000 × 20% = $6,000. The remaining $44,000 is Sec. 1231 gain.

61. (b) The requirement is to determine McEwing Corporation’s taxable income given book income plus additional information regarding items that were included in book income. The loss on sale of the building ($7,000) and gain on sale of the land ($16,000) are Sec. 1231 gains and losses. The resulting Sec. 1231 net gain of $9,000 is then treated as LTCG and will be offset against the LTCL of $8,000 resulting from the sale of investments. Since these items have already been included in book income, McEwing’s taxable income is the same as its book income, $120,000.

62. (a) The realized gain resulting from the involuntary conversion ($125,000 insurance proceeds − $86,000 adjusted basis = $39,000) is recognized only to the extent that the insurance proceeds are not reinvested in similar property ($125,000 − $110,000 = $15,000). Since the machinery was Sec. 1245 property, the recognized gain of $15,000 is recaptured as ordinary income to the extent of the $14,000 of depreciation previously deducted. The remaining $1,000 is Sec. 1231 gain.

Simulations

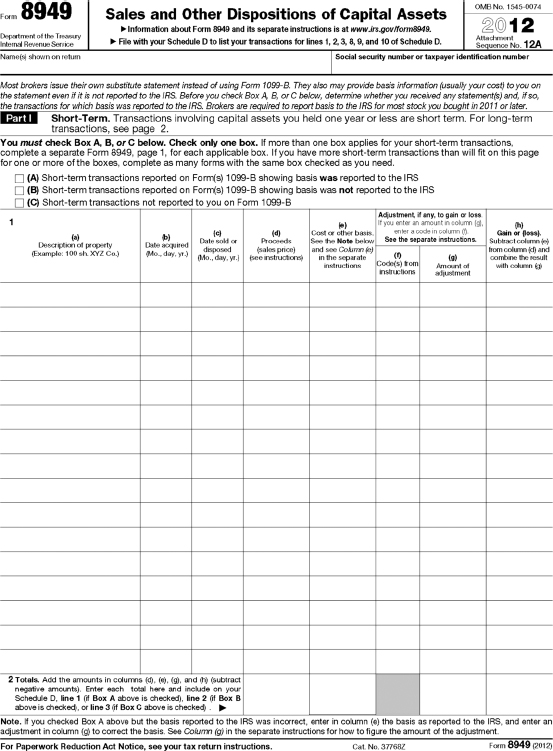

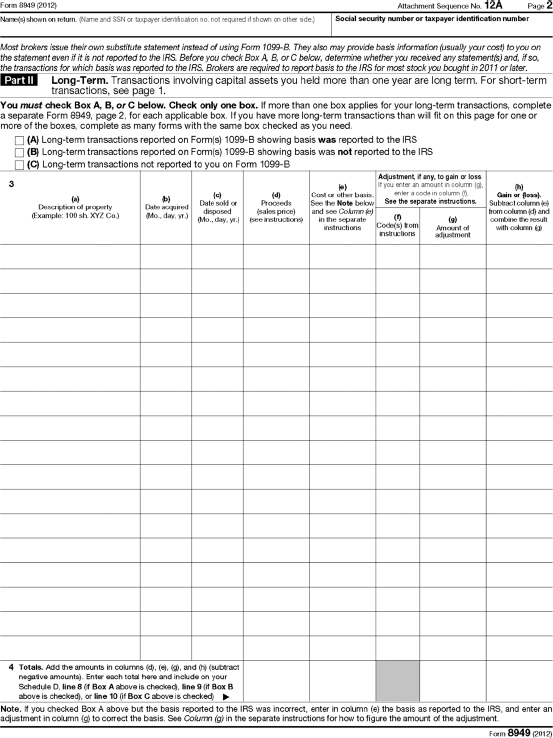

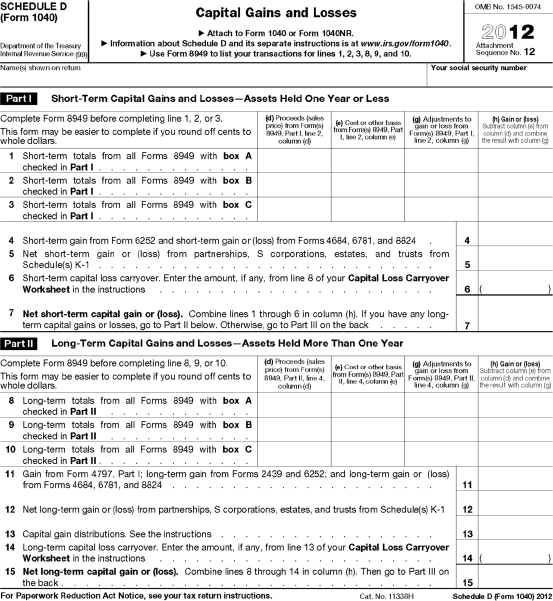

Task-Based Simulation 1

Situation

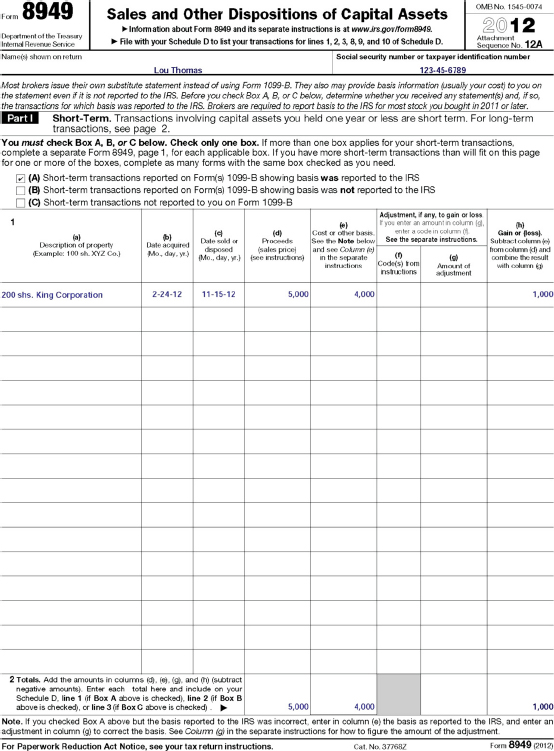

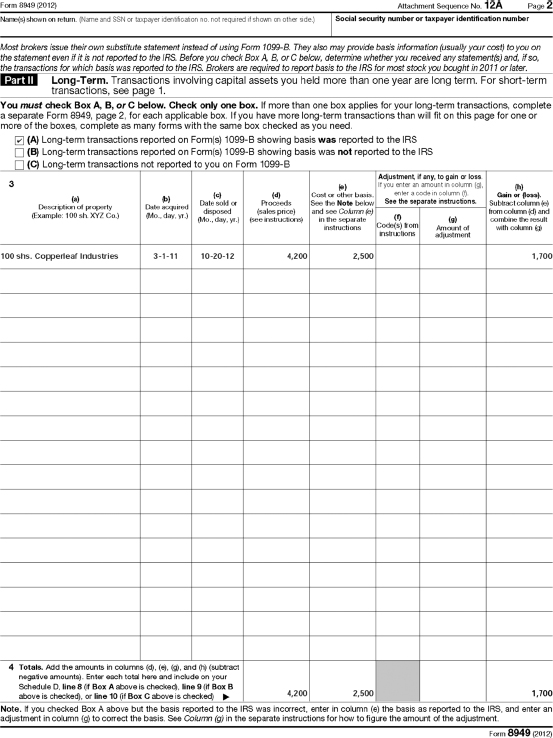

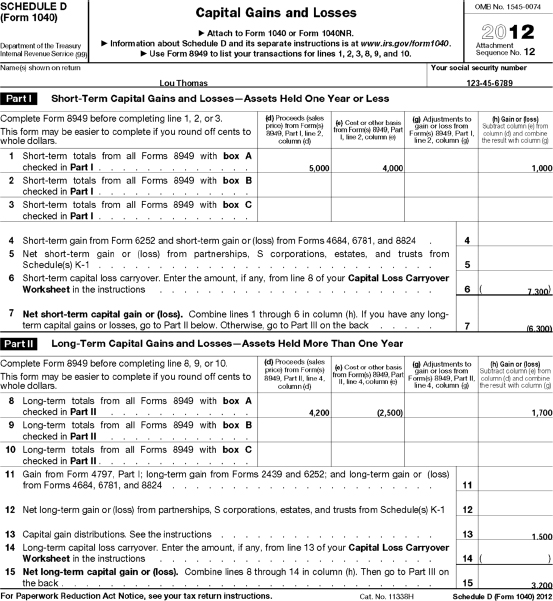

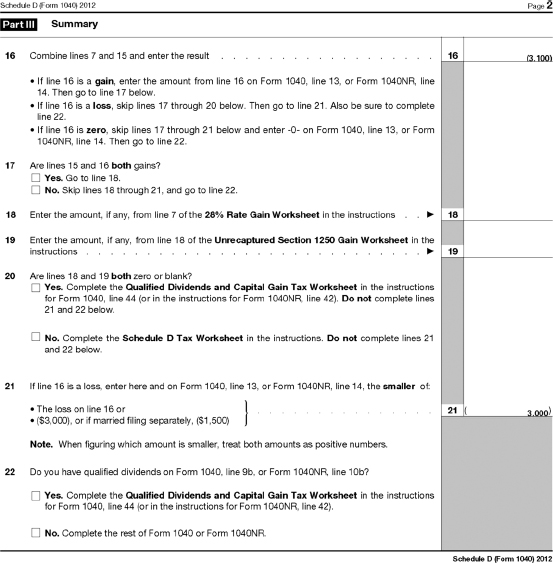

Lou Thomas (social security #123-45-6789) reported the following transactions for calendar-year 2012:

- Lou sold 100 shares of Copperleaf Industries on October 20, 2012, for $4,200. Lou had acquired the stock for $2,500 on March 1, 2011.

- Lou sold 200 shares of King Corporation stock for $5,000 on November 15, 2012. He had purchased the stock on February 24, 2012, for $4,000.

- Thomas had a net short-term capital loss carryforward from 2011 of $7,300, and during December 2012 received a $1,500 capital gain distribution from the Brooks Mutual fund.

- Thomas did not receive any qualified dividends during this year.

Use the above information to complete the following 2012 Form 8949 and Form 1040 Schedule D for Thomas.

Task-Based Simulation 2

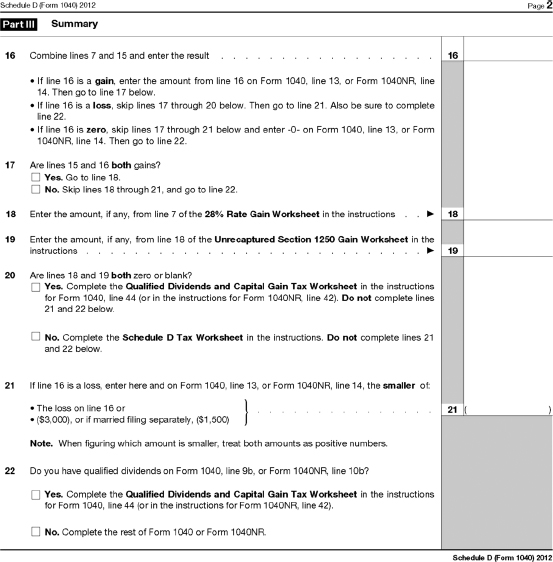

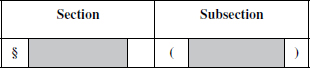

Thomas contacts you and indicates that he expects to incur a substantial net capital loss for calendar-year 2013 and wonders what the treatment of the carryforwards will be in future years. Which code section and subsection provides for the treatment of an individual’s capital loss carryforward? Indicate the reference to that citation in the shaded boxes below.

Simulation Solutions

Task-Based Simulation 1

Task-Based Simulation 2

Internal Revenue Code Section 1212, subsection (b) provides that for taxpayers other than corporations, an excess of net short-term capital loss over net long-term capital gain for a taxable year shall be treated as a short-term capital loss in the succeeding taxable year. Similarly, an excess of net long-term capital loss over net short-term capital gain for a taxable year shall be treated as a long-term capital loss in the succeeding taxable year.