Module 31: Debtor-Creditor Relationships

Overview

The first part of this module discusses the rights and duties of debtors and creditors. One of the important areas is the idea of a lien. Note the different types of liens and their effect on debtors and creditors. Also covered are the concepts of composition agreements with creditors and assignments for the benefit of creditors. These can be used as alternatives to bankruptcy.

A. Rights and Duties of Debtors and Creditors

B. Nature of Suretyship and Guaranty

C. Creditor’s Rights and Reme

D. Surety’s/Guarantor’s Rights and Remedies

E. Surety’s/Guarantor’s Defenses

F. Cosureties

G. Surety Bonds

Key Terms

Multiple-Choice Questions

Multiple-Choice Answers and Explanations

Simulations

Simulation Solutions

This module also discusses the concepts of guaranty and suretyship. These two are nearly the same concept. The main difference is that the guarantor is typically secondarily liable to the creditor, whereas the surety is normally primarily liable to the creditor. The rights and duties are otherwise almost the same for both the guarantors and the sureties. Before beginning the reading you should review the key terms at the end of the module.

A. Rights and Duties of Debtors and Creditors

1. Liens are creditors’ claims on real or personal property to secure payment of debt or performance of obligations

2. Mechanic’s lien or materialman’s lien

a. Statutory lien on real property (real estate) to secure payment of debts for services or materials to improve real property

EXAMPLE

Worker puts a new roof on an owner’s building. Since the owner has not paid, the worker puts a lien on the building to secure payment. The worker may, after giving notice to the owner, foreclose on the property.

3. Artisan’s lien

a. Occurs when one repairs or improves personal property for another and retains possession of that personal property

EXAMPLE

A has a mechanic repair his car. Upon completion of the repairs, the mechanic retains possession of the car until A pays for the repairs.

b. Artisan’s lien terminates when creditor receives or is offered payment or when s/he gives up possession of property

c. Artisan’s lien generally has priority over other liens or interests as long as creditor retains possession of the personal property

d. If debtor does not pay, most statutes allow lienholder to give notice to owner and then to sell property

4. Innkeeper’s lien allows hotel to keep possession of guest’s baggage until hotel charges are paid

5. Tax lien is imposed by federal, state, or local governments to secure the payment of taxes

6. Attachment is a court-ordered seizure of property due to lack of payment

prior to court judgment for past-due debt

a. If creditor wins at trial, property is sold to pay off debt

b. There are certain constitutional requirements to protect debtors because property is seized based on word of creditors

c. Writ of attachment allows creditor to take possession of personal property to satisfy debt pursuant to successful legal action

7. Writ of execution is remedy in which court order directs sheriff to seize debtor’s property which can then be sold at judicial sale to pay off creditor

a. Any excess over debt owed is paid to debtor

b. Some property is exempt from seizure

8. Garnishment allows creditor to seize property, usually money, owed to debtor by third party

a. Garnishment involves seizing debtor’s property possessed by third parties such as banks (debtor’s bank account) or employers (debtor’s wages)

EXAMPLE

Creditor obtains a writ of garnishment from the court to collect from a bank $5,000 in the debtor’s bank account.

b. State and federal laws limit amount of wages that can be garnished

9. Judgment lien

a. Occurs when a party is awarded damages by a court and the party files a lien against property to secure payment

b. Debtor sometimes fraudulently tries to prevent creditor from satisfying a judgment (fraudulent conveyance)

(1) Evidence of fraud includes one or more of the following:

(a) Transfer of all assets

(b) Debtor maintains use or possession of property after the alleged transfer

(c) Secret transfer

(d) Transfer made to a family member

(e) Transfer made for inadequate consideration

(f) Transfer done in anticipation of litigation

(2) Conveyance is usually set aside

EXAMPLE

Debtor appears to sell all interest in some property but in fact names herself as the beneficiary as she conveys the legal title to the trustee.

10. Composition agreement with creditors (also called composition of creditors’ agreement)

a. Occurs by two or more creditors’ agreement with debtor to accept less than full amount of debt as full satisfaction of debt

b. Based on contract law so needs new consideration to be enforceable

(1) New consideration is construed as two or more creditors each agreeing to accept less than full amount

(a) Note that all creditors need not be part of agreement

(b) Creditors need not be treated equally but treatment must be disclosed and agreed to by affected parties

(2) Once debtor pays creditors at agreed rates, those debts are discharged

(a) If debtor does not perform as agreed in composition agreement, creditors may choose to enforce either original debts or reduced debts under composition agreement.

(b) Creditors not part of agreement are not bound by agreement and thus may resort to bankruptcy law or settle debt by own method

11. Assignment for the benefit of creditors

a. Debtor voluntarily transfers all of his/her assets to an assignee (or trustee) to be sold for the benefit of creditors

b. Assignee takes legal title

(1) Debtor must give up control of assets

c. No agreement between creditors is necessary

(1) Creditors who accept assignment receive pro rata share of debt they are owed

(2) Dissatisfied creditors may file a petition in bankruptcy and assignments may be set aside

d. Debts are not discharged unless they are paid in full by assignee

12. Homestead exemption

a. In addition to providing exemptions against execution on debtor’s assets, also provides exception for debtor’s home so that unsecured creditors and trustees in bankruptcy may not satisfy debts from equity in debtor’s home

(1) However, mortgage liens and IRS tax liens take priority over homestead exemption

13. Fair Debt Collection Practices Act restricts how creditors may collect debts

a. Collection agencies are prevented from contacting debtor-consumer at inconvenient hours, inconvenient places, or at work if employer objects

(1) Also generally prevented from directly contacting debtor represented by an attorney

b. Collection agencies may not use methods that are abusive or misleading

c. Debt collector must provide debtor written notice of amount of debt and to whom the debt is owed within five days of first communication

d. When debtor contests validity of debt, collection attempts must cease until collector sends debtor verification

e. Debt collectors must bring suit in court near debtors residence or in jurisdiction where contract signed

f. If debt collector violates Act, that person is liable for actual damages plus other damages such as court costs and attorneys’ fees

g. Federal Trade Commission enforces this Act

(1) May use cease and desist orders against debt collector

(2) Civil lawsuits for damages are also allowed

h. Act applies to collection agent collecting debt for another—does not apply if creditor collects own debt

14. Truth-in-Lending Act requires lenders and sellers to disclose credit terms on loans to consumer-debtors

a. Disclosures include finance charges and annual percentage rate of interest charged

b. Consumer has right to rescind credit within three days

c. The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 not only has far-reaching effects on US Bankruptcy Code (see Module 30), but also affects the Truth-in-Lending Act

(1) The following are important provisions that are testable on the CPA exam:

(a) Consumer lenders required to make additional disclosures in credit card statements relating to minimum payments, late fees, and introductory rates

1] Also required to disclose toll-free number that consumer may call for estimate of time required to repay balance by making only minimum payments

(b) Consumer lenders required to make more disclosures on tax consequences of home equity loans, and Internet-based credit card solicitations

(c) Preserves defenses and claims of consumers against predatory loans sold by bankruptcy trustees that are covered by Truth-in-Lending Act

15. Equal Credit Opportunity Act prohibits discrimination in consumer credit transactions based on marital status, sex, race, color, religion, national origin, age, or receipt of welfare, or because applicant has exercised legal rights

a. If creditor denies or revokes credit or worsens credit terms, must provide notice to debtor of specific reasons for adverse action

b. Provides for civil and criminal penalties

16. Fair Credit Reporting Act prohibits consumer reporting agencies from including in consumer reports any inaccurate or obsolete information

a. Information includes creditworthiness, mode of living, character, reputation in general

b. Consumer is allowed access to credit reports

c. If consumer disagrees with information in report, agency must investigate and correct if appropriate

(1) If dispute remains, consumer may file statement of his/her version that becomes part of permanent consumer’s credit record

17. Fair Credit Billing Act allows consumer to complain of billing errors and requires creditor to either explain or correct them

a. If dispute remains, debtor may use lawsuit.

18. Fair Credit and Charge Card Disclosure Act requires disclosure of annual percentage rate, membership fee, etc. for credit or charge card solicitations or applications

a. Credit card holder’s liability is limited to $50 per credit card for unauthorized charges due to lost or stolen credit cards

(1) Additional limitation—not liable for any charges after holder notifies issuer

EXAMPLE

Abel carelessly lost his credit card. He quickly notified the issuer. The person who found the card charged $100 on the card. All of this was after the issuer was notified that the card was lost. Abel is not liable for any of the unauthorized charges.

19. Bank debit cards

a. Banks are liable for wrongful dishonor for failure to pay electronic fund transfer when customer has sufficient funds in account

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 1 THROUGH 6

B. Nature of Suretyship and Guaranty

1. In both suretyship and guaranty, third party promises to pay debt owed by debtor if debtor does not pay

a. Third party’s credit acts as security for debt to creditor

b. Purpose of a suretyship agreement is to protect creditor by providing creditor with added security for obligation and to reduce creditor’s risk of loss

EXAMPLE

In order for D to obtain a loan from C, S (who has a good credit standing) promises to C that S will pay debt if D does not.

2. Suretyship and guaranty agreements involve three parties

a. Creditor (C in above example)

(1) Obligee of principal debtor

b. Principal debtor (D in above example)

(1) Has liability for debt owed to creditor

c. Surety (S in above example) or guarantor

(1) Promises to perform or pay debt of principal debtor

(2) Also referred to as accommodation party or consignor

3. Suretyship and guaranty contracts are similar, but many courts distinguish them as such

a. In strict suretyship, the surety promises to be responsible for the debt and is

primarily liable for debt

(1) Creditor can demand payment from surety when debt is due

(2) Unconditional guaranty is the standard suretyship relationship in which there are no further conditions required for guarantor to be asked to pay if debtor does not

EXAMPLE

G agreed in writing to act as surety when D took out a loan with C, the lender. If D does not pay, C may proceed directly against G. C need not try to collect from D first.

(a) Creditor need not attempt collection from debtor first

(b) Creditor need not give notice of debtor’s default

b. In contrast to suretyship, in guaranty contract, guarantor is normally

secondarily liable

(1) Guarantor can be required to pay debt only after debtor defaults and creditor demands payment from debtor

(2) Sometimes guaranty contract requires creditor to both seek payment from debtor and bring suit if necessary, but do not assume that the creditor must sue the debtor first unless the Examiners specifically state that a lawsuit is required against the debtor before proceeding against the guarantor under the terms of the suretyship agreement

(a) Called guarantor of collection

NOTE: With those few exceptions noted in this outline, the rights and duties of both guarantors and sureties are essentially the same and the remainder of this outline will generally use surety and guarantor interchangeably.

4. Examples of typical suretyship and guaranty arrangements

a. Seller of goods on credit requires buyer to obtain a surety to guarantee payment for goods purchased

b. Bank requires owners or directors of closely held corporation to act as sureties for loan to corporation

c. Endorser of negotiable instrument agrees to pay if instrument not paid

d. In order to transfer a check or note, transferor may be required to obtain a surety (accommodation endorser) to guarantee payment

e. Purchaser of real property expressly assumes seller’s mortgage on property (i.e., promises to pay mortgage debt)

(1) Seller then has become surety

5. Suretyship and guaranty contracts should satisfy elements of contracts in general

a. If surety’s or guarantor’s agreement arises at same time as the contract between creditor and debtor, no separate consideration is needed

(1) If creditor gave loan or credit before surety’s promise, separate consideration is necessary to support surety’s new promise

EXAMPLE

C loaned $200,000 to D. Terms provided that the loan is callable by C with one month notice to D. C gave the agreed notice and exercised her right to call the loan. D requested a sixty-day extension. C agreed to the extension when S agreed to be a surety on this loan. There is consideration for the new surety agreement since C gave up the right to call the loan sooner.

(a) Consideration need not be received by surety—often it is principal debtor that benefits

b. Surety’s agreement to answer for debt or default of another must be in writing

(1) Recall that under the Statute of Frauds under contract law, this is one of the types of contracts that must be in writing

(2) However, if guarantor’s promise is primarily for his/her own benefit, (“Main Purpose Doctrine”) it need not be in writing

EXAMPLE

S agrees to pay D’s debt to D’s creditor if he defaults. The main motive of S is to keep D in business to assure a steady supply of an essential component. S’s agreement need not be in writing.

EXAMPLE

A del credere agent is one who sells goods on credit to purchasers for the principal and agrees to pay the principal if the customers do not. Since his promise is primarily for his own benefit, it need not be in writing.

6. Third-party beneficiary contract is not a suretyship contract

a. Third-party beneficiary contract is one in which third party receives benefits from agreement made between promisor and promisee, although third person is not party to contract

EXAMPLE

Father says: “Ship goods to my son and I will pay for them.” This describes a third-party beneficiary contract, not a suretyship arrangement. Father is not promising to pay the debt of another, but rather engaging in an original promise to pay for goods that creditor delivers to son.

7. Indemnity contract is not a suretyship contract

a. An indemnity contract is between two parties (rather than three) whereby indemnitor makes a promise to a potential debtor, indemnitee, (not to creditor as in suretyship arrangement), to indemnify and reimburse debtor for payment of debt or for loss that may arise in future. Indemnitor pays because it has assumed risk of loss, not because of any default by principal debtor as in suretyship arrangement.

EXAMPLE

Under terms of standard automobile collision insurance policy, insurance company agrees to indemnify automobile owner against damage to his/her car caused by collision.

8. Warranty (sometimes called guaranty) is not same as the type of guaranty under suretyship law

a. Warranties arise under, for example, real property law or sales law

(1) Involve making representations as to facts, title, quality, etc. of property

9. Capacity to act as surety or guarantor

a. In general, individuals that have capacity to contract

b. Partnerships may act as sureties unless partnership agreement expressly prohibits it from entering into suretyship contracts

c. Individual partner normally has no authority to bind partnership as surety

d. Modern trend is that corporations may act as sureties

NOW REVIEW MULTIPLE-CHOICE QUESTION 7

C. Creditor’s Rights and Remedies

1. Against principal debtor

a. Creditor has right to receive payment or performance specified in contract

b. Creditor may proceed immediately against debtor upon default, unless contract states otherwise

c. When a debtor has more than one debt outstanding with same creditor and makes a part payment, debtor may give instructions as to which debt the payment is to apply

(1) If debtor gives no instructions, creditor is free to apply part payment to whichever debt s/he chooses; fact that one debt is guaranteed by surety and other is not makes no difference in absence of instructions by debtor

2. Against surety

a. Creditor may proceed immediately against surety upon principal debtor’s default

(1) Unless contract requires it, it is not necessary to give surety notice of debtor’s default

(2) Since surety is immediately liable, s/he can be sued without creditor first attempting to collect from debtor

3. Against guarantor of collection

a. A guarantor of collection’s liability is conditioned on creditor notifying guarantor of debtor’s default and creditor first attempting to collect from debtor

b. Creditor must exhaust remedies by going against debtor before guarantor of collection’s liability arises, even by lawsuit if necessary

c. The specific language “guarantor of collection” must be used on the CPA Exam for these rules to apply; normally the Examiners are testing the ordinary surety.

d. Note that a guarantor of collection is different than a mere guarantor. A creditor only needs to request payment from the debtor before proceeding against a guarantor, whereas the creditor must exhaust all legal remedies against the debtor before proceeding against a guarantor of collection.

4. Against security (collateral) held by surety or creditor

a. Upon principal debtor’s default, creditor may resort to collateral to satisfy debt

(1) If creditor does resort to collateral, any excess collateral or amount realized by its disposal over debt amount must be returned to principal debtor

(2) If collateral is insufficient to pay debt, creditor may proceed against surety or debtor for balance due (deficiency)

b. Creditor is not required to use collateral; creditor may instead proceed immediately against surety or principal debtor

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 8 THROUGH 12

D. Surety’s/Guarantor’s Rights and Remedies

1. When the debt or obligation for which surety has given promise is due

a. Exoneration

(1) Surety may require (by lawsuit if necessary) debtor to pay obligation if debtor is able before surety has paid

(2) Exoneration is not available if creditor demands prompt performance from surety

b. Surety may request creditor to resort first to collateral if surety can show collateral is seriously depreciating in value, or if surety can show undue hardship will otherwise result

2. When surety pays debt or obligation

a. S/he is entitled to right of reimbursement from debtor

(1) May recover only actual payments to creditor

(2) Surety is entitled to resort to collateral as satisfaction of right of reimbursement

(3) Surety’s payment after having received notice of principal debtor’s valid defense against creditor causes surety to lose right of reimbursement

b. S/he has right of subrogation

(1) Upon payment, surety obtains same rights against principal debtor that creditor had

(a) That is, surety steps into creditor’s shoes

(b) If debtor is bankrupt, surety is subrogated to rights of creditor’s priority in bankruptcy proceeding

EXAMPLE

C, the creditor, required D, the debtor, to put up personal property as collateral on a loan and to also use S as a surety on the same loan. Upon D’s default, C chooses to resort to S for payment. Upon payment, S may now sell the collateral under the right of subrogation because the creditor could have used the same right of sale of the collateral.

3. Creditor owes duty to surety to disclose, before surety agrees to contract, any information about material risks that are greater than surety aware of

a. Creditor must also disclose facts inquired by surety

E. Surety’s/Guarantor’s Defenses

1. Surety may generally exercise defenses on contract that would be available

to debtor

a. Breach or failure of performance by creditor

b. Impossibility or illegality of performance

c. Creditor obtains debtor’s promise by fraud, duress, or misrepresentation

d. Statute of limitations

e. Except that surety may not use debtor’s personal defenses as discussed later

2. Surety may take advantage of

own contractual defenses

a. Fraud or duress

(1) If creditor obtains surety’s promise by fraud or duress, contract is voidable at surety’s option

EXAMPLE

Creditor forces X to sign suretyship agreement at threat of great bodily harm.

(2) If creditor gets principal debtor’s promise using fraud or duress, then surety not liable

(a) Exception: surety is liable if was aware of fraud or duress before s/he became surety

(3) Fraud by principal debtor on surety to induce a suretyship agreement will

not release surety if creditor has extended credit in good faith

(a) But if creditor had knowledge of debtor’s fraudulent representations, then surety may avoid liability

EXAMPLE

Y asked Ace to act as surety on a loan from Bank. In order to induce Ace to act as surety, Y made fraudulent representations concerning its financial position to Ace. This fraud by Y will not release surety, Ace, if the creditor, Bank, had no knowledge of the fraud and extended credit in good faith. But if Bank had knowledge of Y’s fraudulent representations, then Ace has a good defense and can avoid liability. Note that if Bank finds out about Y’s fraudulent representations after Bank has extended credit, Ace has no defense.

b. Suretyship contract itself is void due to illegality

c. Incapacity of surety (e.g., surety is a minor)

d. Failure of consideration for suretyship contract

(1) However, when surety’s and principal debtor’s obligations are incurred at same time, there is no need for any separate consideration beyond that supporting principal debtor’s contract; if surety’s undertaking is entered into subsequent to debtor’s contract, it must be supported by separate consideration (see section B.5.a. of this outline)

e. Suretyship agreement is not in writing as required under Statute of Frauds

f. Creditor fails to notify surety of any material facts within creditor’s knowledge concerning debtor’s ability to perform

EXAMPLE

Creditor’s failure to report to surety that debtor has defaulted on several previous occasions.

EXAMPLE

Creditor’s failure to report to surety that debtor submitted fraudulent financial statements to surety to induce suretyship agreement.

g. Surety, in general, may use any obligations owed by creditor to surety as a setoff against any payments owed to creditor

(1) True even if setoff arises from separate transaction

3. Acts of creditor or debtor materially affecting surety’s obligations

a. Tender of performance by debtor or surety and refusal by creditor will discharge surety

(1) However, tender of performance for obligation to pay money does not normally release principal debtor but stops accrual of interest on debt

b. Release of principal debtor from liability by creditor without consent of surety will also discharge surety’s liability

(1) But surety is not released if creditor specifically reserves his/her rights against surety

(a) However, surety upon paying may then seek recovery from debtor

NOTE: If the Examiners test this issue of the creditor releasing the debtor, they usually have the creditor reserve its rights against the surety; thus the surety is still liable to the creditor. The reason the release of the debtor does not materially affect the surety’s obligation is that the surety is primarily liable to the creditor. Thus, the creditor already had the right to pursue the debt directly from the surety.

c. Release of surety by creditor

(1) Does not release principal debtor because debtor is liable whether or not surety is liable

d. Proper performance by debtor or satisfaction of creditor through collateral will discharge surety

e. Variance in terms and conditions of contract subsequent to surety’s undertaking

(1) Accommodation (noncompensated) surety is completely discharged for any change in contract made by creditor on terms required of principal debtor

(2) Commercial (compensated) surety is completely released if modification in principal debtor’s contract materially increases risk to surety

(a) If risk not increased materially, then surety not released but his/her obligation is reduced by amount of loss due to modification

(3) Surety may consent to modifications so that they are not defenses

(4) Surety is not released if creditor modifies principal debtor’s duties to be beneficial to surety (i.e., decreases surety’s risk)

EXAMPLE

Creditor reduces interest rate on loan to principal debtor from 12% to 10%.

(5) Modifications that affect rights of sureties based on above principles

(a) Extension of time on principal debtor’s obligation, but only to the extent that the extension causes a loss to the surety and only that additional loss will be discharged.

(b) Change in amount, place, or manner of principal debtor’s obligations

(c) Modification of duties of principal debtor

(d) Substitution of debtor’s or delegation of debtor’s obligation to another

1] Note how this may result in change in risk to the surety

(e) Release, surrender, destruction, or impairment of collateral by creditor before or after debtor’s default releases surety by amount decreased

EXAMPLE

S is a surety on a $10,000 loan between Creditor and Debtor. Creditor is also holding $1,000 of Debtor’s personal property as collateral on the $10,000 loan. Before the loan is paid, Creditor returns the collateral to Debtor. This action releases S from $1,000 of the $10,000 loan.

EXAMPLE

S is a compensated surety for a loan between Debtor and Creditor. The loan had also been secured by collateral. Upon default, Creditor took possession of the collateral but let it get damaged by rain. The collateral was impaired by $500. Creditor also sought payment from S, the compensated surety. S may reduce his payment to Creditor by $500.

(6) In order to release surety, there must be an actual alteration or variance in terms of contract and not an option or election that principal debtor can exercise under express terms of original agreement which surety has guaranteed

EXAMPLE

Tenant and landlord entered into a two-year leasing agreement which expressly contained an option for an additional year which could be exercised by tenant, with X acting as surety on lease contract. If tenant exercises this option, X still remains bound as surety.

4. Following are not defenses of surety/guarantor

a. Personal defenses of principal debtor

(1) Death of debtor or debtor’s lack of capacity (e.g., debtor is a minor or was legally insane when contract was made)

(2) Insolvency (or discharge in bankruptcy) of debtor

(a) Possibility of debtor’s insolvency is a primary reason for engaging in a surety arrangement

(3) Personal debtor’s setoffs

(a) Unless debtor assigns them to surety

b. Creditor did not give notice to surety of debtor’s default or creditor did not first proceed against principal debtor

(1) Unless a conditional guarantor and creditor violated condition

c. Creditor does not resort to collateral

d. Creditor delays in proceeding against debtor unless delay exceeds statute of limitations

e. When creditor is owed multiple debts by same debtor, creditor may choose to apply payment to any of the debts unless debtor directs otherwise—surety cannot direct which debt payment applies to

EXAMPLE

Debtor owes two debts to Creditor. S is acting as a surety on one of these debts. When Debtor makes a payment, Creditor applies it to the debt on which S is not a surety since Debtor did not indicate which one. The surety has no defense from these facts and is not released.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 13 THROUGH 20

F. Cosureties

1. Cosureties exist when there is more than one surety for same obligation of principal debtor to same creditor

a. Not relevant whether cosureties are aware of each other or became cosureties at different times

(1) Must be sureties for same debtor for same obligation

b. Cosureties need not be bound for same amount; they can guarantee equal or unequal amounts of debt

(1) Collateral, if any, need not be held equally

c. Cosureties need not sign same document

2. Cosureties are jointly and severally liable to creditor

a. That is, creditor can proceed against any of the sureties jointly or against each one individually to extent surety has assumed liability

b. If creditor sues multiple sureties, s/he may recover in any proportion from each, but may not recover more than debtor’s total obligation

c. Proceeding against one or more sureties does not release remaining surety or sureties

3. Right of contribution exists among cosureties

a. Right of contribution arises when cosurety, in performance of debtor’s obligation, pays more than his/her proportionate share of total liability, and thereby entitles cosurety to compel other cosureties to compensate him/her for excess amount paid (i.e., contribution from other cosureties for their pro rata share of liability)

4. Cosureties are only liable in contribution for their proportionate share

a. Cosurety’s pro rata share is proportion that each surety’s risk (i.e., amount each has personally guaranteed) bears to total amount of risk assumed by all sureties by using the following formula:

EXAMPLE

X and Y are cosureties for $5,000 and $10,000, respectively, of a $10,000 debt. Each is liable in proportion to amount each has personally guaranteed. Since X guaranteed $5,000 of debt and Y guaranteed $10,000 of debt, then X is individually liable for 1/3 ($5,000/$15,000) of debt and Y is individually liable for 2/3 ($10,000/$15,000) of debt. If debtor defaults on only $3,000 of debt, X is liable for $1,000 (1/3 × $3,000) and Y is liable for $2,000 (2/3 × $3,000). Although creditor may recover $3,000 from either, each cosurety has right of contribution from other cosurety.

EXAMPLE

Refer to the preceding example. If the creditor recovers all of the $3,000 debt from Y, then Y, under the right of contribution, can recover $1,000 from X so that each will end up paying his/her proportionate amount.

5. Each cosurety is entitled to share in any collateral pledged (either held by creditor or other cosurety) in proportion to cosurety’s liability for debtor’s default

EXAMPLE

If in above illustration, cosurety Y held collateral pledged by debtor worth $900, both cosureties X and Y would be entitled to share in collateral in proportion to their respective liabilities. X would be entitled to 1/3 ($5,000/$15,000) of $900 collateral, or $300; and Y would be entitled to 2/3 ($10,000/$15,000) of $900 collateral, or $600.

6. Discharge or release of one cosurety by creditor results in a reduction of liability of remaining cosurety

a. Remaining cosurety is released only to extent of released cosurety’s pro rata share of debt liability (unless there is a reservation of rights by creditor against remaining cosurety)

EXAMPLE

A and B are cosureties for $4,000 and $12,000, respectively, on a $12,000 debt. If creditor releases cosurety A, cosurety B is released to extent of cosurety A’s liability. Each is liable in proportion to amount each has personally guaranteed. Since A guaranteed $4,000 of debt and B guaranteed $12,000 of debt, then A is individually liable for 1/4 ($4,000/$16,000) of debt and B is individually liable for 3/4 ($12,000/$16,000) of debt, that is, $9,000. Therefore, cosurety B is released of A’s pro rata liability of $3,000 (1/4 × $12,000), and only remains a surety for $9,000 ($12,000 − $3,000) of debt.

7. A cosurety is not released from obligation to perform merely because another cosurety refuses to perform

a. However, upon payment of full obligation, cosurety can demand a pro rata contribution from his/her nonperforming cosurety

b. Cosurety is not released if other cosureties are

unable to pay (i.e., dead, bankrupt)

(1) In which case, modify the formula found at Section F.4.a. by taking those cosureties that cannot pay completely out of formula and use it with all remaining cosureties

8. Cosureties have rights of exoneration, reimbursement, and subrogation like any surety

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 21 THROUGH 27

G. Surety Bonds

1. An acknowledgment of an obligation to make good the performance by another of some act or responsibility

a. Usually issued by companies which for a stated fee assume risk of performance by bonded party

b. Performance of act or responsibility by bonded party discharges surety’s obligation

2. Performance bonds are used to have surety guarantee completion of terms of contracts

a. Construction bond guarantees builder’s obligation to complete construction

(1) If builder breaches contract, surety can be held liable for damages but not for specific performance (i.e., cannot be required to complete construction)

(a) Surety may complete construction if chooses to

3. Fidelity bonds are forms of insurance that protects an employer against losses sustained due to acts of dishonest employees.

4. Official bond is guaranteeing that public officials will faithfully execute their duties.

5. Surety bonding company retains right of subrogation against bonded party

KEY TERMS

Assignment for the benefit of creditors. A possible alternative to bankruptcy. This occurs where a debtor assigns assets to a third party who uses those assets to pay the debtor’s creditors. It is important to remember that an assignment for the benefit of creditors does not release the debtor from the debt, unless the debts are paid in full.

Bond. A contract involving a compensated surety.

Composition. A possible alternative to bankruptcy; compare and contrast to the assignment for the benefit of creditors (above). This is an agreement between a debtor and its creditors where the debtor will repay a portion of the debt owed. This agreement releases the debtor from its obligations only to the creditors who are part of the composition.

Contribution. When a cosurety pays more than its proportionate share of the debt it can demand payment from other cosureties so that each surety is paying its proportionate share of the debt.

Cosurety. Two or more sureties are guaranteeing the same debt.

Guarantor. Similar to a surety, but a guarantor is secondarily liable to the creditor. Thus, in the event that the debtor defaults the creditor must at least ask the debtor to pay, but it the event the debtor says no, then the creditor may seek payment from the guarantor.

Reimbursement. If the surety pays the debt, the surety is entitled to receive whatever it paid to the creditor from the debtor.

Subrogation. After the surety has paid the debt it acquires the rights of the creditor and may now exercise those rights against the debtor. Thus, if the debtor had given the creditor collateral, the surety would have rights against the collateral.

Surety. A party who promises to pay the debts of another party. Sureties are primarily liable to the creditor.

Multiple-Choice Questions (1–27)

A. Rights and Duties of Debtors and Creditors

1. A debtor may attempt to conceal or transfer property to prevent a creditor from satisfying a judgment. Which of the following actions will be considered an indication of fraudulent conveyance?

2. A homestead exemption ordinarily could exempt a debtor’s equity in certain property from postjudgment collection by a creditor. To which of the following creditors will this exemption apply?

| |

Valid home mortgage lien |

Valid IRS tax lien |

| a. |

Yes |

Yes |

| b. |

Yes |

No |

| c. |

No |

Yes |

| d. |

No |

No |

3. Which of the following statements is (are) correct regarding debtors’ rights?

I. State exemption statutes prevent all of a debtor’s personal property from being sold to pay a federal tax lien.

II. Federal social security benefits received by a debtor are exempt from garnishment by creditors.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

4. Under the Federal Fair Debt Collection Practices Act, which of the following would a collection service using improper debt collection practices be subject to?

a. Abolishment of the debt.

b. Reduction of the debt.

c. Civil lawsuit for damages for violating the Act.

d. Criminal prosecution for violating the Act.

5. Which of the following liens generally require(s) the lienholder to give notice of legal action before selling the debtor’s property to satisfy the debt?

| |

Mechanic’s lien |

Artisan’s lien |

| a. |

Yes |

Yes |

| b. |

Yes |

No |

| c. |

No |

Yes |

| d. |

No |

No |

6. Which of the following prejudgment remedies would be available to a creditor when a debtor owns no real property?

| |

Writ of attachment |

Garnishment |

| a. |

Yes |

Yes |

| b. |

Yes |

No |

| c. |

No |

Yes |

| d. |

No |

No |

B. Nature of Suretyship and Guaranty

7. Which of the following involve(s) a suretyship relationship?

I. Transferee of a note requires transferor to obtain an accommodation endorser to guarantee payment.

II. The purchaser of goods agrees to pay for the goods but to have them shipped to another party.

III. The shareholders of a small, new corporation agree in writing to be personally liable on a corporate loan if the corporation defaults.

a. I only.

b. II only.

c. I and II only.

d. I and III only.

C. Creditor’s Rights and Remedies

8. Which of the following events will reduce a surety’s liability to the creditor?

a. The principal debtor was involuntarily petitioned into bankruptcy.

b. The creditor failed to notify the surety of a partial surrender of the principal debtor’s collateral.

c. The creditor was adjudicated incompetent after the debt arose.

d. The principal debtor exerted duress to obtain the surety agreement.

9. Reuter Bank loaned Sabean Corporation $500,000 in writing. As part of the agreement, Reuter required that the three owners of Sabean act as sureties on the loan. The corporation also required that some real estate owned by Sabean Corporation be used as collateral for 40% of the loan. The collateral and suretyship agreements were put in writing and signed by all relevant parties. When the $500,000 loan became due, which of the following rights does Reuter Bank have?

I. May demand payment of the full amount immediately from the sureties when the corporation defaults on the loan.

II. May demand payment of the full amount immediately from the sureties even if Reuter does not attempt to recover any amount from the collateral.

III. May attempt to recover up to $200,000 from the collateral and the remainder from the sureties, even if the remainder is more than $300,000.

IV. Must first attempt to collect the debt from Sabean Corporation before it can resort to the sureties or the collateral.

a. I and III only.

b. II only.

c. I, II, and III only.

d. IV only.

10. Belmont acts as a surety for a loan to Diablo from Chaffin. In which of the following cases would Belmont be released from liability?

I. Diablo dies.

II. Diablo files bankruptcy.

III. Chaffin modifies Diablo’s contract, increasing Diablo’s risk of nonpayment.

a. I only.

b. III only.

c. I and III only.

d. I, II, and III.

11. A party contracts to guaranty the collection of the debts of another. As a result of the guaranty, which of the following statements is correct?

a. The creditor may proceed against the guarantor without attempting to collect from the debtor.

b. The guaranty must be in writing.

c. The guarantor may use any defenses available to the debtor.

d. The creditor must be notified of the debtor’s default by the guarantor.

12. Sorus and Ace have agreed, in writing, to act as guarantors of collection on a debt owed by Pepper to Towns, Inc. The debt is evidenced by a promissory note. If Pepper defaults, Towns will be entitled to recover from Sorus and Ace unless

a. Sorus and Ace are in the process of exercising their rights against Pepper.

b. Sorus and Ace prove that Pepper was insolvent at the time the note was signed.

c. Pepper dies before the note is due.

d. Towns has not attempted to enforce the promissory note against Pepper.

D. Surety’s and Guarantor’s Rights and Remedies

13. Which of the following rights does a surety have?

| |

Right to compel the creditor to collect from the principal debtor |

Right to compel the creditor to proceed against the principal debtor’s collateral |

| a. |

Yes |

Yes |

| b. |

Yes |

No |

| c. |

No |

Yes |

| d. |

No |

No |

14. Under the law of suretyship, which are generally among the rights that the surety may use?

I. Subrogation.

II. Exoneration.

III. Reimbursement from debtor.

a. I only.

b. III only.

c. I and II only.

d. I, II, and III.

E. Surety’s and Guarantor’s Defenses

15. Which of the following defenses would a surety be able to assert successfully to limit the surety’s liability to a creditor?

a. A discharge in bankruptcy of the principal debtor.

b. A personal defense the principal debtor has against the creditor.

c. The incapacity of the surety.

d. The incapacity of the principal debtor.

16. Which of the following events will release a noncompensated surety from liability?

a. Release of the principal debtor’s obligation by the creditor but with the reservation of the creditor’s rights against the surety.

b. Modification by the principal debtor and creditor of their contract that materially increases the surety’s risk of loss.

c. Filing of an involuntary petition in bankruptcy against the principal debtor.

d. Insanity of the principal debtor at the time the contract was entered into with the creditor.

17. Which of the following is not a defense that a surety may use to avoid payment of a debtor’s obligation to a creditor?

a. The creditor had committed fraud against the debtor to induce the debtor to take on the debt with this creditor.

b. The creditor had committed fraud against the surety to induce the surety to guarantee the debtor’s payment of a loan.

c. The statute of limitations has run on the debtor’s obligation.

d. The debtor took out bankruptcy.

18. Which of the following acts always will result in the total release of a compensated surety?

a. The creditor changes the manner of the principal debtor’s payment.

b. The creditor extends the principal debtor’s time to pay.

c. The principal debtor’s obligation is partially released.

d. The principal debtor’s performance is tendered.

19. Green was unable to repay a loan from State Bank when due. State refused to renew the loan unless Green provided an acceptable surety. Green asked Royal, a friend, to act as surety on the loan. To induce Royal to agree to become a surety, Green fraudulently represented Green’s financial condition and promised Royal discounts on merchandise sold at Green’s store. Royal agreed to act as surety and the loan was renewed. Later, Green’s obligation to State was discharged in Green’s bankruptcy. State wants to hold Royal liable. Royal may avoid liability

a. If Royal can show that State was aware of the fraudulent representations.

b. If Royal was an uncompensated surety.

c. Because the discharge in bankruptcy will prevent Royal from having a right of reimbursement.

d. Because the arrangement was void at the inception.

20. Wright agreed to assure King’s loan from Ace Bank. Which of the following events would release Wright from the obligation to pay the loan?

a. Ace seeking payment of the loan only from Wright.

b. King is granted a discharge in bankruptcy.

c. Ace is paid in full by King’s spouse.

d. King is adjudicated mentally incompetent.

F. Cosureties

21. A distinction between a surety and a cosurety is that only a cosurety is entitled to

a. Reimbursement (Indemnification).

b. Subrogation.

c. Contribution.

d. Exoneration.

22. Ivor borrowed $420,000 from Lear Bank. At Lear’s request, Ivor entered into an agreement with Ash, Kane, and Queen for them to act as cosureties on the loan. The agreement between Ivor and the cosureties provided that the maximum liability of each cosurety was: Ash, $84,000; Kane, $126,000; and Queen, $210,000. After making several payments, Ivor defaulted on the loan. The balance was $280,000. If Queen pays $210,000 and Ivor subsequently pays $70,000, what amounts may Queen recover from Ash and Kane?

a. $0 from Ash and $0 from Kane.

b. $42,000 from Ash and $63,000 from Kane.

c. $70,000 from Ash and $70,000 from Kane.

d. $56,000 from Ash and $84,000 from Kane.

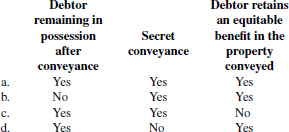

23. Nash, Owen, and Polk are cosureties with maximum liabilities of $40,000, $60,000, and $80,000, respectively. The amount of the loan on which they have agreed to act as cosureties is $180,000. The debtor defaulted at a time when the loan balance was $180,000. Nash paid the lender $36,000 in full settlement of all claims against Nash, Owen, and Polk. The total amount that Nash may recover from Owen and Polk is

a. $0

b. $ 24,000

c. $ 28,000

d. $140,000

24. Ingot Corp. lent Flange $50,000. At Ingot’s request, Flange entered into an agreement with Quill and West for them to act as compensated cosureties on the loan in the amount of $100,000 each. Ingot released West without Quill’s or Flange’s consent, and Flange later defaulted on the loan. Which of the following statements is correct?

a. Quill will be liable for 50% of the loan balance.

b. Quill will be liable for the entire loan balance.

c. Ingot’s release of West will have no effect on Flange’s and Quill’s liability to Ingot.

d. Flange will be released for 50% of the loan balance.

25. Mane Bank lent Eller $120,000 and received securities valued at $30,000 as collateral. At Mane’s request, Salem and Rey agreed to act as uncompensated cosureties on the loan. The agreement provided that Salem’s and Rey’s maximum liability would be $120,000 each.

Mane released Rey without Salem’s consent. Eller later defaulted when the collateral held by Mane was worthless and the loan balance was $90,000. Salem’s maximum liability is

a. $30,000

b. $45,000

c. $60,000

d. $90,000

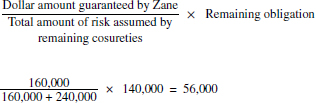

26. Lane promised to lend Turner $240,000 if Turner obtained sureties to secure the loan. Turner agreed with Rivers, Clark, and Zane for them to act as cosureties on the loan from Lane. The agreement between Turner and the cosureties provided that compensation be paid to each of the cosureties. It further indicated that the maximum liability of each cosurety would be as follows: Rivers $240,000, Clark $80,000, and Zane $160,000. Lane accepted the commitments of the sureties and made the loan to Turner. After paying ten installments totaling $100,000, Turner defaulted. Clark’s debts, including the surety obligation to Lane on the Turner loan, were discharged in bankruptcy. Later, Rivers properly paid the entire outstanding debt of $140,000. What amount may Rivers recover from Zane?

a. $0

b. $56,000

c. $70,000

d. $84,000

27. Which of the following rights does one cosurety generally have against another cosurety?

a. Exoneration.

b. Subrogation.

c. Reimbursement.

d. Contribution.

Multiple-Choice Answers and Explanations

Answers

Explanations

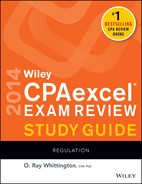

1. (a) Fraudulent conveyance of property is done with the intent to defraud a creditor, hinder or delay him/her, or put the property out of his/her reach. If the debtor maintains possession of the property, secretly transfers or hides the property, or retains an equitable interest in the property, then a fraudulent conveyance has occurred as all of the three actions prevent the creditor from receiving the full property.

2. (d) Although a homestead exemption can exempt a debtor’s equity in certain property from postjudgment collection by a creditor, the exemption applies to general creditors and the bankruptcy trustee, not secured creditors or lien holders.

3. (b) Under garnishment procedures, creditors may attach a portion of the debtor’s wages to pay off a debt. There are legal limits as to how much of the wages can be garnished. Likewise, federal social security benefits are protected from garnishment by creditors. Therefore, statement II is correct. Statement I, however, is incorrect because federal tax liens can be used to sell a debtor’s personal property to pay taxes.

4. (c) The Federal Fair Debt Collection Practices Act was passed to prevent debt collectors from using unfair or abusive collection methods. The Federal Trade Commission is charged with enforcement of this Act but aggrieved parties may also use a civil lawsuit against the debt collector who violates this Act. Answers (a) and (b) are incorrect because the remedy is a suit for damages or a suit for up to $1,000 for violation of the Act if damages are not proven. The remedy is not a reduction or abolishment of the debt. Answer (d) is incorrect because this Act does not provide for criminal prosecution.

5. (a) Liens are used by creditors to secure payment for services or materials, in the case of a mechanic’s lien, or for repairs, in the case of an artisan’s lien. They require that notice be given to the debtor before the creditor can sell the property to satisfy the debt. Generally, a debtor is entitled to notice prior to the disposition of his/her property for any type of lien.

6. (a) When a creditor wishes to collect a past-due debt from the debtor, s/he may use a writ of attachment. This is a prejudgment remedy in which the creditor is allowed to take into possession some personal property of the debtor prior to getting a judgment in a lawsuit for the past-due debt. The debtor may also wish to collect the debt by use of garnishment. This allows the creditor to obtain property of the debtor that is held by a third party. Typical examples include garnishing wages owed by the employer to the employee-debtor or garnishing the debtor’s bank account. To avoid abuses, there are limitations on both of these remedies.

7. (d) Statement I illustrates a suretyship relationship in which the endorser of the note is the surety. Statement II illustrates a third-party beneficiary contract, not a suretyship relationship. The purchaser has agreed to pay for the goods as his/her own debt. The party to receive the goods is the third-party beneficiary. Statement III illustrates a suretyship relationship in which the shareholders are sureties.

8. (b) The release or impairment of collateral injures a surety’s interest since a surety would acquire rights against the collateral upon paying the off the debt. Accordingly if collateral is released or impaired, then the surety’s obligation is reduced by the value of the collateral or by the amount of the impairment. Answer (a) is incorrect—bankruptcy is a personal defense of the debtor and is not a defense for the surety. Answer (c) is incorrect because this is a debt that is voidable at the option of the creditor. Answer (d) is incorrect because there is a possible wrong against the debtor but this does not release the surety.

9. (c) The creditor, Reuter Bank, has a lot of flexibility in remedies. Although Reuter may attempt to collect from Sabean when the loan is due, it is not required to but instead may resort to the sureties or to the collateral up to the 40% agreed upon, or both.

10. (b) When the creditor modifies the debtor’s contract, increasing the surety’s risk, the surety is released. Note that death of the principal debtor or the debtor’s filing bankruptcy are personal defenses of the debtor that the surety cannot use. Such risks are some of the reasons creditors prefer sureties.

11. (b) Under the Statute of Frauds under contract law, a surety’s (guarantor’s) agreement to answer for the debt or default of another must be in writing. Answer (a) is incorrect, as a guarantor of collection’s liability is conditioned on the creditor notifying the guarantor of the debtor’s default and the creditor first attempting to collect from the debtor. Answer (c) is incorrect as the guarantor may not use the debtor’s personal defenses, such as death or insolvency. Answer (d) is incorrect because it is the creditor that must notify the guarantor of the debtor’s default, not vice versa.

12. (d) A guarantor’s liability is conditioned on the creditor notifying the guarantor of the debtor’s default and the creditor first attempting to collect from the debtor. In this case, if Towns has not attempted to collect against Pepper, then Towns would not yet be able to collect against Sorus and Ace. Answer (a) is incorrect because Sorus’ and Ace’s performance of the right of reimbursement from Pepper does not preclude Towns’ recovery from Sorus and Ace. Answers (b) and (c) are incorrect because insolvency of the debtor and death of the debtor are not valid defenses of the guarantor against the creditor.

13. (d) The surety is primarily liable on the debt of the principal debtor. Therefore, the creditor can seek payment directly from the surety as soon as the debt is due. For this reason, the surety cannot require the creditor to collect from the debtor nor can s/he compel the creditor to proceed against any collateral the principal debtor may have.

14. (d) Upon payment, the surety obtains the right of subrogation which is the ability to use the same rights the creditor had. Also, the surety may resort to the right of exoneration by requiring the debtor to pay when s/he is able if the creditor has not demanded immediate payment directly from the surety. If the surety has paid the debtor’s obligation, the surety may attempt reimbursement from the debtor.

15. (c) The surety may use his/her own defenses of incapacity of the surety or bankruptcy of the surety to limit his/her own liability. Although the surety may use most defenses that the debtor has to limit his/her (surety’s) liability, the surety may not use the personal defenses of the debtor. These include the debtor’s bankruptcy and the debtor’s incapacity; therefore answers (a), (b), and (d) are incorrect.

16. (b) A modification by the principal debtor and creditor in the terms and conditions of their original contract without the surety’s consent will automatically release the surety if the surety’s risk of loss is thereby materially increased. Note that a noncompensated surety is discharged even if the creditor does not change the surety’s risk. However, a compensated surety is discharged only if the modification causes a material increase in risk. Answers (c) and (d) are incorrect because a surety may not exercise the principal debtor’s personal defenses (i.e., insolvency and insanity). Answer (a) is incorrect because although a release of the principal debtor without the surety’s consent will usually discharge the surety, there is no discharge if the creditor expressly reserves rights against the surety.

17. (d) Personal defenses that the debtor has such as bankruptcy or death of the debtor cannot be used by the surety to avoid payment of the debtor’s obligation to the creditor. Answer (a) is incorrect because the surety may generally exercise the defenses on the contract that the debtor has against the creditor. Answer (b) is incorrect because the surety may take advantage of his/her own personal defenses such as fraud by the creditor against the surety. Answer (c) is incorrect because the surety generally may exercise the defenses on the contract that would be available to the debtor such as the running of the statute of limitations.

18. (d) A compensated surety will be released from an obligation to the creditor upon tender of performance by either the principal debtor or the surety. A compensated surety will also be completely released if modifications are made to the principal debtor’s contract which materially increase risk to the surety. However, if the risk is not materially increased, the surety is not completely released but rather his/her obligation is reduced by the amount of loss due to modification. The surety also is not released if the modifications are beneficial to the surety. Answers (a) and (b) are incorrect because these modifications will not necessarily result in a material increase in the surety’s risk or could even be beneficial to the surety. Answer (c) is incorrect because partial release of the principal debtor’s obligation will result in partial release of the surety.

19. (a) Normally, fraud by the debtor on the surety to induce him/her to act as a surety will not release the surety. However, when the creditor is aware of the debtor’s fraudulent misrepresentation, then the surety can avoid liability. Answer (b) is incorrect because the above principle is true whether the surety is compensated or not. Answer (c) is incorrect because the risk of bankruptcy is one of the reasons that the creditor desires a surety. Answer (d) is incorrect because fraudulent misrepresentations do not make a contract void but can make it voidable.

20. (c) Once the debt is paid by someone, both the principal debtor and the cosigner are released from obligations to pay the loan. Answer (a) is incorrect because the creditor may proceed against the cosigner without needing to proceed against the principal debtor. Answer (b) is incorrect because the possibility that the principal debtor may qualify for bankruptcy is one of the reasons that the creditor may desire a cosigner. Answer (d) is incorrect because even if the main debtor is adjudicated mentally incompetent, this can allow the main debtor to escape liability but not the cosigner.

21. (c) A suretyship relationship exists when one party agrees to answer for the obligations of another. Cosureties exist when there is more than one surety guaranteeing the same obligation of the principal debtor. Answer (a) is incorrect because both sureties and cosureties are entitled to reimbursement from the debtor if the surety pays the obligation. Answer (b) is incorrect because sureties and cosureties both have the right of subrogation in that upon making payment, the surety has the same rights against the principal debtor that the creditor had. Answer (d) is incorrect because both are also entitled to exoneration. Sureties and cosureties both may require the debtor to pay the obligation for which they have given promise if the debtor is able to do so. The right of contribution, however, exists only among cosureties. If a cosurety pays more than his/her proportionate share of the total liability, he/she is entitled to be compensated by the other cosureties for the excess amount paid.

22. (b) The right of contribution arises when one cosurety, in performance of the principal debtor’s obligation, pays more than his/her proportionate share of the total liability. The right of contribution allows the performing cosurety to receive reimbursement from the other cosureties for their pro rata shares of the liability. The pro rata shares of the cosureties are determined as follows:

Thus, Queen is entitled to receive $42,000 from Ash and $63,000 from Kane.

23. (c) A surety relationship is present when one party agrees to answer for the obligation of another. When there is more than one surety guaranteeing the same obligation of the principal debtor, the sureties become cosureties jointly and severally liable to the claims of the creditor. A right of contribution arises when one cosurety, in performance of the debtor’s obligation, pays more than his proportionate share of the total liability. The right of contribution entitles the performing cosurety to reimbursement from the other cosureties for their pro rata shares of the liability. The pro rata shares of the cosureties are determined as follows:

Thus, Nash is entitled to recover $12,000 from Owen and $16,000 from Polk for a total of $28,000.

24. (a) A discharge or release of one cosurety by a creditor results in a reduction of liability of the remaining cosurety. The remaining cosurety is released to the extent of the released cosurety’s pro rata share of debt liability, unless there is a reservation of rights by the creditor against the remaining cosurety. Quill and West each had maximum liability of $100,000. Thus, Ingot’s release of West will result in Quill’s liability being reduced by West’s pro rata share of the total debt liability, which was one-half. Therefore, Quill’s liability has been reduced to $25,000 (i.e., 50% of the loan balance) due to the release of West as a cosurety. Answer (c) is therefore incorrect. Answer (d) is incorrect because the release of the cosurety does not release the principal debtor since the debtor’s obligation is not affected in any way by Ingot’s release of West. Answer (b) is incorrect because as discussed above, Quill’s liability has been reduced due to Ingot’s release of West.

25. (b) The discharge or release of one cosurety by the creditor results in a reduction of liability of the remaining cosurety. This reduction of liability is limited to the released cosurety’s pro rata share of debt liability (unless there is a reservation of rights by the creditor against the remaining cosurety). Since Mane released Rey without reserving rights against Salem, Salem is released to the extent of Rey’s pro rata share of the $90,000 liability. Salem’s maximum liability can be calculated as follows:

26. (b) The right of contribution arises when one cosurety, in performance of debtor’s obligation, pays more than his proportionate share of the total liability. The right of contribution entitles the performing cosurety to reimbursement from the other cosureties for their pro rata shares of the liability. Since Clark’s debts have been discharged in bankruptcy, River may only exercise his right of contribution against Zane, and may recover nothing from Clark. Zane’s pro rata share of the remaining $140,000 would be determined as follows:

27. (d) Cosureties are jointly and severally liable to the creditor up to the amount of liability each agreed to. If a cosurety pays more than his/her proportionate share of the debt, s/he may seek contribution from the other cosureties for the excess. Answer (a) is incorrect because the right of exoneration refers to the surety requiring the debtor to pay the debt when able. Answer (b) is incorrect because subrogation refers to the right of the surety to obtain the same rights against the debtor that the creditor had, once the surety pays the creditor. Answer (c) is incorrect because the right of reimbursement allows the surety to recover payments from the debtor that the surety has made to the creditor.

Simulation

Task-Based Simulation 1

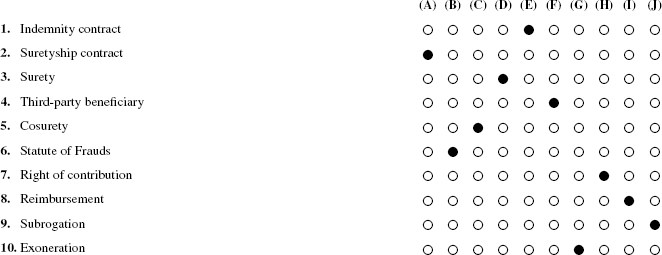

For each of the numbered words or phrases, select the one best phrase or sentence from the list A through J. Each response may be used only once.

A. Relationship whereby one person agrees to answer for the debt or default of another.

B. Requires certain contracts to be in writing to be enforceable.

C. Jointly and severally liable to creditor.

D. Promises to pay debt on default of principal debtor.

E. One party promises to reimburse debtor for payment of debt or loss if it arises.

F. Receives intended benefits of a contract.

G. Right of surety to require the debtor to pay before surety pays.

H. Upon payment of more than his/her proportionate share, each cosurety may compel other cosureties to pay their shares.

I. Upon payment of debt, surety may recover payment from debtor.

J. Upon payment, surety obtains same rights against debtor that creditor had.

Simulation Solution

Task-Based Simulation 1

Explanations

1. (E) An indemnity contract is not a suretyship contract. Instead it is a contract involving two parties in which the first party agrees to indemnify and reimburse the second party for covered debts or losses should they take place.

2. (A) The suretyship contract involves three parties. The surety agrees with the creditor to pay for the debt or default if the debtor does not.

3. (D) The surety is the party that agrees to pay the creditor if the debtor defaults.

4. (F) When two parties make a contract that intends to benefit a third party, that party is a third-party beneficiary.

5. (C) When two or more sureties agree to be sureties for the same obligation to the same creditor, they are known as cosureties. They have joint and several liability.

6. (B) The Statute of Frauds sets out rules that require certain contracts to be in writing, such as those in which a surety agrees to answer for the debt or default of another.

7. (H) Cosureties are liable in contribution for their proportionate shares of the debt. If a cosurety pays more than this amount, s/he may seek contribution for the excess from the other cosureties.

8. (I) The right of reimbursement is against the debtor to collect any amounts paid by the surety.

9. (J) When the surety pays the creditor, it “steps into the shoes of the creditor” and obtains the same rights against the debtor that the creditor had.

10. (G) If the debtor is able to pay, the surety may require the debtor to pay before the surety pays. This is called exoneration.