Chapter 3: The Solutions Approach

The solutions approach is a systematic problem-solving methodology. The purpose is to assure efficient, complete solutions to CPA exam questions, some of which are complex and confusing relative to most undergraduate accounting problems. This is especially true with regard to the new simulation type problems. Unfortunately, there appears to be a widespread lack of emphasis on problem-solving techniques in accounting courses. Most accounting books and courses merely provide solutions to specific types of problems. Memorization of these solutions for examinations and preparation of homework problems from examples is “cookbooking.” “Cookbooking” is perhaps a necessary step in the learning process, but it is certainly not sufficient training for the complexities of the business world. Professional accountants need to be adaptive to a rapidly changing complex environment. For example, CPAs have been called on to interpret and issue reports on new concepts such as price controls, energy allocations, and new taxes. These CPAs rely on their problem-solving expertise to understand these problems and to formulate solutions to them.

The steps outlined below are only one of many possible series of solution steps. Admittedly, the procedures suggested are very structured; thus, you should adapt the suggestions to your needs. You may find that some steps are occasionally unnecessary, or that certain additional procedures increase your own problem-solving efficiency. Whatever the case, substantial time should be allocated to developing an efficient solutions approach before taking the examination. You should develop your solutions approach by working previous CPA questions and problems.

Note that the steps below relate to any specific question or problem; overall examination or section strategies are discussed in Chapter 4.

Multiple-Choice Screen Layout

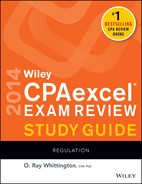

The following is a computer screenshot that illustrates the manner in which multiple-choice questions will be presented:

As indicated previously, multiple-choice questions will be presented in three individual testlets of 24 questions each. Characteristics of the computerized testlets of multiple-choice questions include the following:

The screenshot above was obtained from the AICPA’s sample examinations at www.cpa-exam.org. Candidates are urged to complete the tutorial and other example questions on the AICPA’s website to obtain additional experience with the computer-based testing.

Multiple-Choice Question Solutions Approach

Multiple-Choice Question Solutions Approach Example

A good example of the multiple-choice solutions approach follows.

13. On June 15, Peters orally offered to sell a used lawn mower to Mason for $125. Peters specified that Mason had until June 20 to accept the offer. On June 16, Peters received an offer to purchase the lawn mower for $150 from Bronson, Mason’s neighbor. Peters accepted Bronson’s offer. On June 17, Mason saw Bronson using the lawn mower and was told the mower had been sold to Bronson. Mason immediately wrote to Peters to accept the June 15 offer.

Which of the following statements is correct?

a. Mason’s acceptance would be effective when received by Peters.

b. Mason’s acceptance would be effective when mailed.

c. Peters’ offer had been revoked and Mason’s acceptance was ineffective.

d. Peters was obligated to keep the June 15 offer open until June 20.

Step 3:

Topical area? Contracts—Revocation and Attempted Acceptance

Step 4:

Principle? An offer may be revoked at any time prior to acceptance and is effective when received by offeree

Step 5:

a. Incorrect—Mason’s acceptance was ineffective because the offer had been revoked prior to Mason’s acceptance.

b. Incorrect—Same as a.

c. Correct—Peters’ offer was effectively revoked when Mason learned that the lawn mower had been sold to Bronson.

d. Incorrect Peters was not obligated to keep the offer open because no consideration had been paid by Mason. Note that if consideration had been given, an option contract would have been formed and the offer would have been irrevocable before June 20.

Currently, all multiple-choice questions are scored based on the number correct, weighted by a difficulty rating (i.e., there is no penalty for guessing). The rationale is that a “good guess” indicates knowledge. Thus, you should answer all multiple-choice questions.

Task-Based Simulations

Task-based simulations are short case-based problems designed to

- Test integrated knowledge

- More closely replicate real-world problems

- Assess research and other skills

Any of the following types of responses might be required on task-based simulations:

- Multiple selection

- Drop-down selection

- Numeric and monetary inputs

- Formula answers

- Check box response

- Enter spreadsheet formulas

- Research results

The screenshot below illustrates a simulation that requires the candidate to make a selection from a drop list.

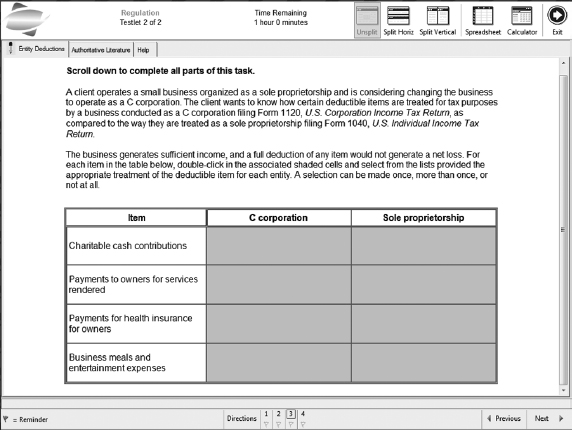

The screenshot below illustrates a requirement to complete a tax form.

To complete the simulations, candidates are provided with a number of tools, including

- A four-function computer calculator with an electronic tape

- Scratch spreadsheet

- The ability to split windows horizontally and vertically to show two tabs on the screen (e.g., you can examine the situation tab in one window and a particular requirement in a second window)

- Access to professional literature databases to answer research requirements

- Copy and paste functions

In addition, the resource tab provides other resources that may be needed to complete the problem. For example, a resource tab might contain a depreciation schedule for use in answering a tax problem.

A window on the screen shows the time remaining for the entire exam and the “Help” button provides instructions for navigating the simulation and completing the requirements.

The AICPA has introduced a new simulation interface which is described in this manual. You are urged to complete the tutorial and other sample tests that are on the AICPA’s website (www.cpa-exam.org) to obtain additional experience with the interface and computer-based testing.

Task-Based Simulations Solutions Approach

The following solutions approach is suggested for answering simulations:

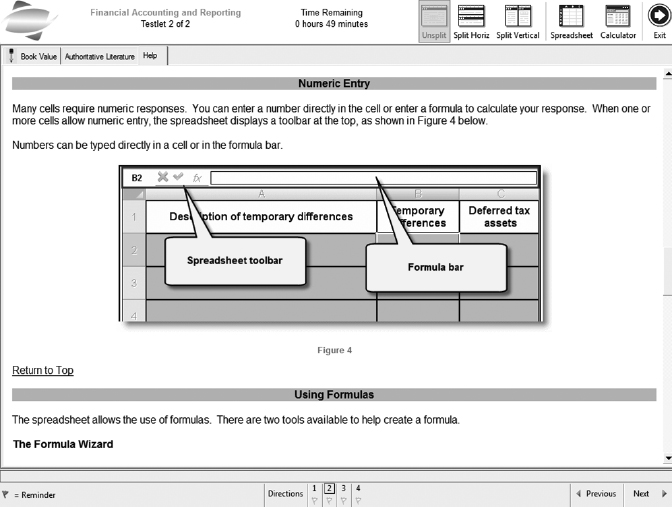

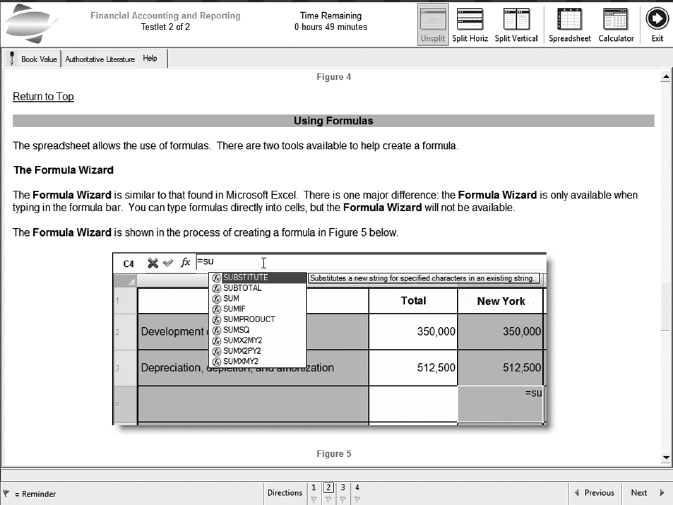

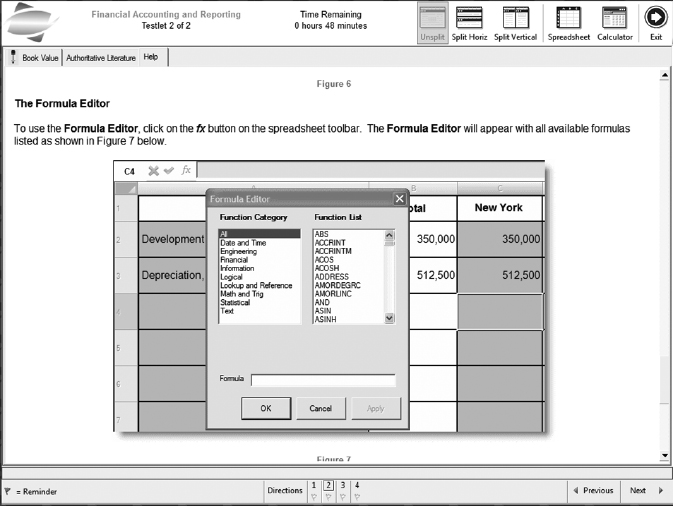

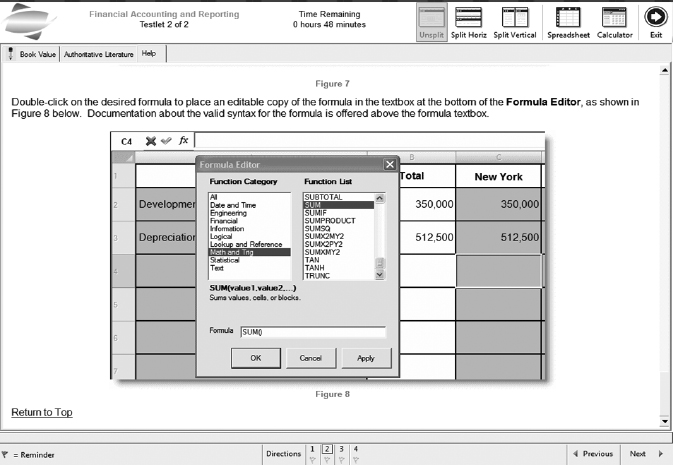

The screenshots below explain how the spreadsheet operates. Notice that mathematical operations can be input directly into a cell. A mathematical operation must be entered using a function in one of the two ways shown.

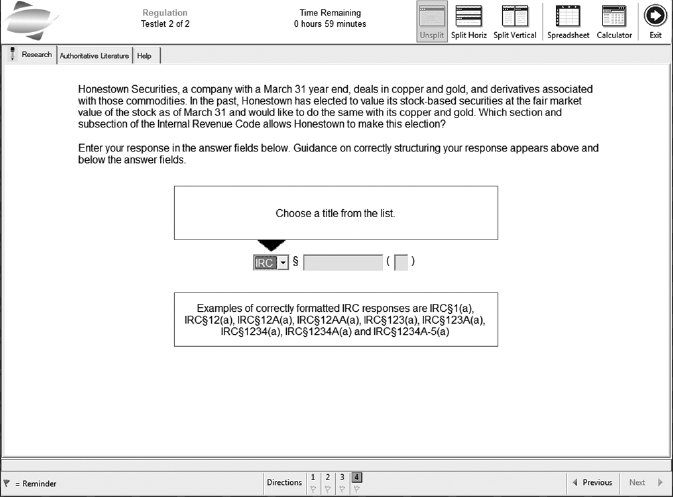

Research Simulations

One simulation on the Regulation section will be a research simulation. Research simulations require candidates to search the professional literature in electronic format and interpret the results. In the Regulation section the professional literature database includes

- Internal Revenue Code and Income Tax Regulations (IRC)

- Statements on Responsibilities in Tax Practice (TS)

Shown below is a screenshot of a task-based research simulation for the Regulation section of the CPA examination.

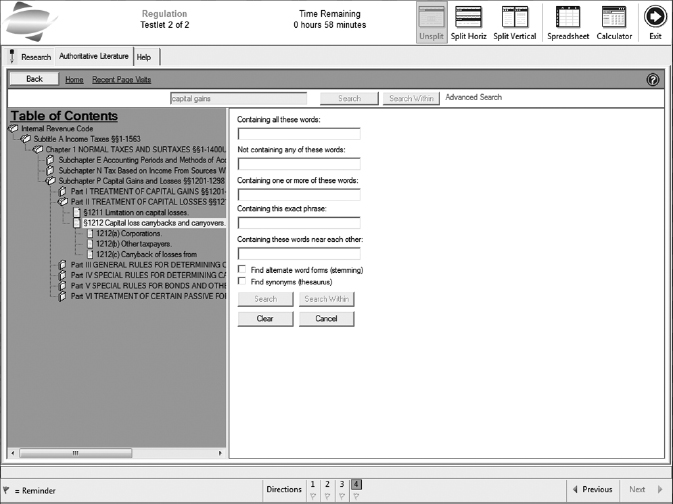

The literature may be searched using the table of contents or a keyword search. Therefore, knowing important code sections may speed up your search. If you use the search function, you must spell the term or terms correctly.

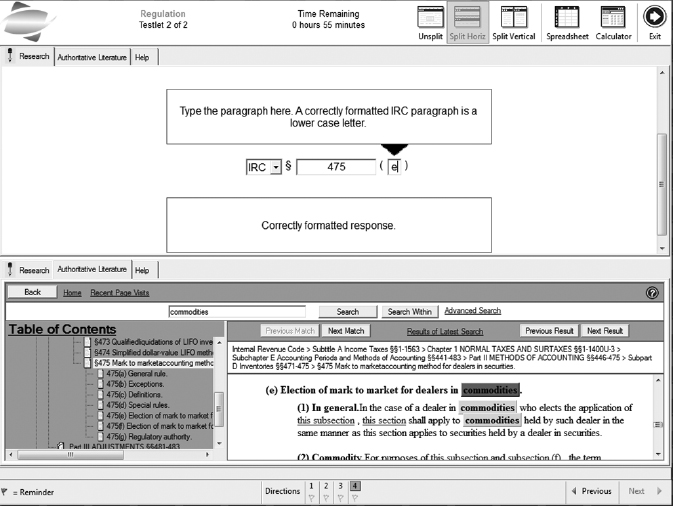

Once you have found the correct passage in the literature, you must input the citation in the answer box. To facilitate this process you should use the split screen function to view the literature in one screen and the answer box in the other as shown below.

If possible, it is important to get experience using the electronic version of the Internal Revenue Code to sharpen your skills. If that is not available, you should use the printed copy of the professional standards to answer the simulation problems in the manual.

Chapter 5 of this manual contains guidance on how to perform research on the Internal Revenue Code.

Time Requirements for the Solutions Approach

Many candidates bypass the solutions approach, because they feel it is too time-consuming. Actually, the solutions approach is a time-saver and, more importantly, it helps you prepare better solutions to all questions and simulations.

Without committing yourself to using the solutions approach, try it step-by-step on several questions and simulations. After you conscientiously go through the step-by-step routine a few times, you will begin to adopt and modify aspects of the technique which will benefit you. Subsequent usage will become subconscious and painless. The important point is that you must try the solutions approach several times to accrue any benefits.

In summary, the solutions approach may appear foreign and somewhat cumbersome. At the same time, if you have worked through the material in this chapter, you should have some appreciation for it. Develop the solutions approach by writing down the steps in the solutions approach at the beginning of this chapter, and keep them before you as you work CPA exam questions and problems. Remember that even though the suggested procedures appear very structured and time-consuming, integration of these procedures into your own style of problem solving will help improve your solutions approach. The next chapter discusses strategies for the overall examination.