Module 28: Commercial Paper

Overview

Coverage of commercial paper includes the types of negotiable instruments, the requirements of negotiability, negotiation, the holder in due course concept, defenses to a claim of liability, and the rights of parties to a negotiable instrument. The functions of commercial paper are to provide a medium of exchange that is readily transferable like money and to provide an extension of credit. It is easier to transfer commercial paper than contract rights and not subject to as many defenses as contracts are. To be negotiable, an instrument must

A. General Concepts of Commercial Paper

B. Types of Commercial Paper

C. Requirements of Negotiability

D. Interpretation of Ambiguities in Negotiable Instruments

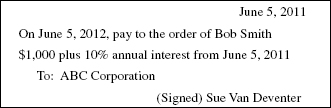

E. Negotiation

F. Holder in Due Course

G. Rights of a Holder in Due Course

H. Liability of Parties

I. Additional Issues

J. Banks

K. Electronic Fund Transfer Act and Regulation E

L. Fund Transfers under UCC Article 4A

M. Transfer of Negotiable Documents of Title

N. Agencies Involved in Banking

Key Terms

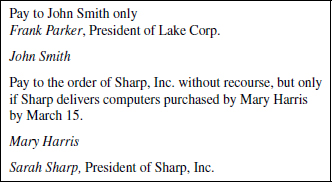

Multiple-Choice Questions

Multiple-Choice Answers and Explanations

Simulations

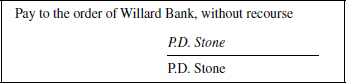

Simulation Solutions

These requirements must be present on the face of the instrument. Instruments that do not comply with these provisions are nonnegotiable and are transferable only by assignment. The assignee of a nonnegotiable instrument takes it subject to all defenses, whereas a holder of a negotiable instrument may avoid certain defenses.

A central theme of exam questions on negotiable instruments is the liability of the primary parties and of the secondarily liable parties under various fact situations. Similar questions in different form emphasize the rights that a holder of a negotiable instrument has against primary and secondary parties. Your review of this area should emphasize the legal liability arising upon execution of negotiable commercial paper, the legal liability arising upon various types of endorsements, and the warranty liabilities of various parties upon transfer or presentment for payment. A solid understanding of the distinction between real and personal defenses is required. Also tested is the relationship between a bank and its customers. Before beginning the reading you should review the key terms at the end of the module.

A. General Concepts of Commercial Paper

B. Types of Commercial Paper

C. Requirements of Negotiability

D. Interpretation of Ambiguities in Negotiable Instruments

E. Negotiation

F. Holder in Due Course

G. Rights of a Holder in Due Course

I. Additional Issues

J. Banks

K. Electronic Fund Transfer Act and Regulation E

L. Fund Transfers under UCC Article 4A

M. Transfer of Negotiable Documents of Title

N. Agencies Involved in Banking

KEY TERMS

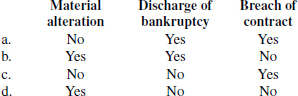

Bearer paper. A negotiable instrument that is payable to whomever possesses it.

Contract liability. When a party is responsible to pay the holder/HDC the face value of the instrument.

Draft. A type of negotiable instrument that contains an order to pay money. A draft has three parties: A drawer, a drawee, and the payee.

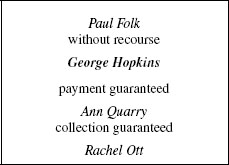

Drawer. The person who creates the draft and signs the draft on its face.

Drawee. The party that the drawer has instructed to pay the payee; typically this is the drawer’s bank.

Endorsement. A signature, usually on the back of a negotiable instrument, by the payee or some other holder. The endorsement is necessary to further negotiate the instrument when the instrument is order paper.

Face value. The amount for which the instrument is payable.

Holder. A person who has possession of a negotiable instrument, and the instrument has all necessary endorsements.

Holder in due course (HDC). A holder with enhanced rights in the negotiable instrument. Those rights include the best claim of ownership, and HDC’s claims for payment cannot be denied because of a personal defense.

Maker. The person who creates a note and has primary liability for its payment.

Negotiable. A characteristic of an instrument that means the instrument is freely transferable from one party to another.

Negotiation. The actual transfer of ownership of a negotiable instrument from one party to another. Negotiation can be accomplished by delivery alone if the instrument is bearer paper; if the instrument is order paper, then it must be transferred by delivery and the necessary endorsements.

Note. A two-party (the maker and payee) negotiable instrument that contains a promise to pay money.

Order paper. An instrument that is payable to a particular party.

Payee. The party to whom the negotiable instrument was originally payable.

Primary liability. The party from whom the holder/HDC of a negotiable instrument must first seek payment: the maker of a note or the acceptor of a draft.

Secondary liability. Parties who are liable to the holder/HDC if the primary party dishonors the instrument: endorsers and drawers.

Warranty liability. Responsibility to a holder/HDC to return the money actually paid for the negotiable instrument.

Multiple-Choice Questions (1–50)

B. Types of Commercial Paper

1.

The above instrument is a

a. Draft.

b. Postdated check.

c. Trade acceptance.

d. Promissory note.

2. Which of the following statements regarding negotiable instruments is not correct?

a. A certificate of deposit is a type of note.

b. A check is a type of draft.

c. A promissory note is a type of draft.

d. A certificate of deposit is issued by a bank.

3. Based on the following instrument:

The instrument is a

a. Promissory demand note.

b. Sight draft.

c. Check.

d. Trade acceptance.

4. Under the Commercial Paper Article of the UCC, which of the following documents would be considered an order to pay?

I. Draft

II. Certificate of deposit

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

C. Requirements of Negotiability

5. An instrument that is otherwise negotiable on its face states “Pay to Jenny Larson.” Which of the following statements is (are) correct?

I. It is negotiable if it is a check.

II. It is negotiable if it is a draft drawn on a corporation.

III. It is negotiable if it is a promissory note.

a. I only.

b. I and II only.

c. II and III only.

d. I, II, and III.

6. Under the Commercial Paper Article of the UCC, for a note to be negotiable it must

a. Be payable to order or to bearer.

b. Be signed by the payee.

c. Contain references to all agreements between the parties.

d. Contain necessary conditions of payment.

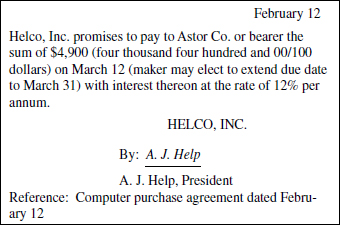

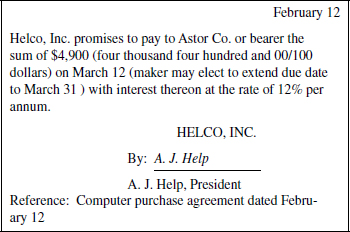

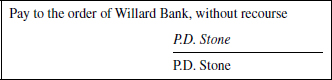

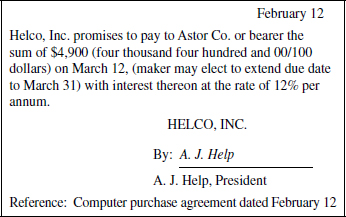

7. On February 15, P.D. Stone obtained the following instrument from Astor Co. for $1,000. Stone was aware that Helco, Inc. disputed liability under the instrument because of an alleged breach by Astor of the referenced computer purchase agreement. On March 1, Willard Bank obtained the instrument from Stone for $3,900. Willard had no knowledge that Helco disputed liability under the instrument.

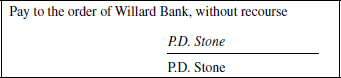

The reverse side of the instrument is endorsed as follows:

The instrument is

a. Nonnegotiable, because of the reference to the computer purchase agreement.

b. Nonnegotiable, because the numerical amount differs from the written amount.

c. Negotiable, even though the maker has the right to extend the time for payment.

d. Negotiable, when held by Astor, but nonnegotiable when held by Willard Bank.

8. A draft made in the United States calls for payment in Canadian dollars.

a. The draft is nonnegotiable because it calls for payment in money of another country.

b. The draft is nonnegotiable because the rate of exchange may fluctuate thus violating the sum certain rule.

c. The instrument is negotiable if it satisfies all of the other elements of negotiability.

d. The instrument is negotiable only if it has the exchange rate written on the draft.

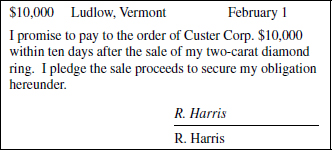

9. An instrument reads as follows:

Which of the following statements correctly describes the above instrument?

a. The instrument is nonnegotiable because it is not payable at a definite time.

b. The instrument is nonnegotiable because it is secured by the proceeds of the sale of the ring.

c. The instrument is a negotiable promissory note.

d. The instrument is a negotiable sight draft payable on demand.

10. Kline is holding a promissory note in which he is the payer and Breck is the promissor. One of the terms of the note states that payment is subject to the terms of the contract dated March 1 of the current year between Breck and Kline. Does this term destroy negotiability?

a. No, if the contract is readily available.

b. No, since the note can be enforced without regard to the mentioned contract.

c. No, as long as the terms in the mentioned contract are commercially reasonable.

d. Yes, since this term causes the note to have a conditional promise.

11. Based on the following instrument:

The instrument is

a. Nonnegotiable even though it is payable on demand.

b. Nonnegotiable because the numeric amount differs from the written amount.

c. Negotiable even though a payment date is not specified.

d. Negotiable because of Abner’s guaranty.

12. A note has an interest rate that varies based on the stated rate of 2% above the prime rate as determined by XYZ Bank in New York City. Under the Revised Article 3 of the Uniform Commercial Code, which of the following is true?

a. This interest rate provision destroys negotiability since it does not constitute a sum certain.

b. This note is not negotiable because the holder has to look outside the instrument to determine what the prime rate is.

c. The interest rate provision destroys negotiability because the prime rate can vary before the time the note comes due.

d. The interest rate provision is allowed in negotiable notes and does not destroy negotiability.

13. While auditing your client, Corbin Company, you see a check that is postdated and states “Pay to Corbin Company.” You also see a note that is due in forty days and also says “Pay to Corbin Company.” You note that both instruments contain all of the elements of negotiability except for possibly the ones raised by this fact pattern. Which of the following is(are) negotiable instruments?

a. The check.

b. The note.

c. Both the check and the note.

d. Neither the check nor the note.

14. Under the Revised Article 3 of the Uniform Code, which of the following is true if the maker of a note provides that payment must come out of a designated fund?

a. This is allowed even though the maker is not personally obligated to pay.

b. Since the instrument is not based on the general credit of the maker, the instrument is not negotiable.

c. The promise to pay is conditional; therefore, the note is not negotiable.

d. The instrument is not negotiable if the designated fund has insufficient funds.

D. Interpretation of Ambiguities in Negotiable Instruments

15. Wyden holds a check that is written out to him. The check has the amount in words as five hundred dollars. The amount in figures on this check states $200. Which of the following is correct?

a. The check is cashable for $500.

b. The check is cashable for $200.

c. The check is not cashable because the amounts differ.

d. The check is not cashable because the amounts differ by more than 10%.

e. Negotiation

16. Under the Negotiable Instruments Article of the UCC, an endorsement of an instrument “for deposit only” is an example of what type of endorsement?

a. Blank.

b. Qualified.

c. Restrictive.

d. Special.

17. Under the Commercial Paper Article of the UCC, which of the following requirements must be met for a transferee of order paper to become a holder?

I. Possession

II. Endorsement of transferor

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

18. The following endorsements appear on the back of a negotiable promissory note payable to Lake Corp.

Which of the following statements is correct?

a. The note became nonnegotiable as a result of Parker’s endorsement.

b. Harris’ endorsement was a conditional promise to pay and caused the note to be nonnegotiable.

c. Smith’s endorsement effectively prevented further negotiation of the note.

d. Harris’ signature was not required to effectively negotiate the note to Sharp.

19. A note is made payable to the order of Ann Jackson on the front. On the back, Ann Jackson signs it in blank and delivers it to Jerry Lin. Lin puts “Pay to Jerry Lin” above Jackson’s endorsement. Which of the following statements is false concerning this note?

a. After Lin wrote “Pay to Jerry Lin,” the note became order paper.

b. After Jackson endorsed the note but before Lin wrote on it, the note was bearer paper.

c. Lin needs to endorse this note to negotiate it further, even though he personally wrote “Pay to Jerry Lin” on the back.

d. The note is not negotiable because Lin wrote “Pay to Jerry Lin” instead of “Pay to the order of Jerry Lin.”

20. You are examining some negotiable instruments for a client. Which of the following endorsements can be classified as a special restrictive endorsement?

a. Pay to Alex Ericson if he completes the contracted work within ten days, (signed) Stephanie Sene.

b. Pay to Alex Ericson without recourse (signed) Stephanie Sene.

c. For deposit only, (signed) Stephanie Sene.

d. Pay to Alex Ericson, (signed) Stephanie Sene.

21. On February 15, P.D. Stone obtained the following instrument from Astor Co. for $1,000. Stone was aware that Helco, Inc. disputed liability under the instrument because of an alleged breach by Astor of the referenced computer purchase agreement. On March 1, Willard Bank obtained the instrument from Stone for $3,900. Willard had no knowledge that Helco disputed liability under the instrument.

The reverse side of the instrument is endorsed as follows:

Which of the following statements is correct?

a. Willard Bank cannot be a holder in due course because Stone’s endorsement was without recourse.

b. Willard Bank must endorse the instrument to negotiate it.

c. Neither Willard Bank nor Stone are holders in due course.

d. Stone’s endorsement was required for Willard Bank to be a holder in due course.

F. Holder in Due Course

22. Under the Commercial Paper Article of the UCC, which of the following circumstances would prevent a person from becoming a holder in due course of an instrument?

a. The person was notified that payment was refused.

b. The person was notified that one of the prior endorsers was discharged.

c. The note was collateral for a loan.

d. The note was purchased at a discount.

23. One of the requirements needed for a holder of a negotiable instrument to be a holder in due course is the value requirement. Ruper is a holder of a $1,000 check written out to her. Which of the following would not satisfy the value requirement?

a. Ruper received the check from a tax client to pay off a four-month-old debt.

b. Ruper took the check in exchange for a negotiable note for $1,200 which was due on that day.

c. Ruper received the check in exchange for a promise to do certain specified services three months later.

d. Ruper received the check for a tax service debt for a close relative.

24. Larson is claiming to be a holder in due course of two instruments. One is a draft that is drawn on Picket Company and says “Pay to Brunt.” The other is a check that says “Pay to Brunt.” Both are endorsed by Brunt on the back and made payable to Larson. Larson gave value for and acted in good faith concerning both the draft and the check. Larson also claims to be ignorant of any adverse claims on either instrument which are not overdue or have not been dishonored. Which of the following is (are) true?

I. Larson is a holder in due course of the draft.

II. Larson is a holder in due course of the check.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

25. In order to be a holder in due course, the holder, among other requirements, must give value. Which of the following will satisfy this value requirement?

I. An antecedent debt.

II. A promise to perform services at a future date.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

G. Rights of a Holder in Due Course

26. Bond fraudulently induced Teal to make a note payable to Wilk, to whom Bond was indebted. Bond delivered the note to Wilk. Wilk negotiated the instrument to Monk, who purchased it with knowledge of the fraud and after it was overdue. If Wilk qualifies as a holder in due course, which of the following statements is correct?

a. Monk has the standing of a holder in due course through Wilk.

b. Teal can successfully assert the defense of fraud in the inducement against Monk.

c. Monk personally qualifies as a holder in due course.

d. Teal can successfully assert the defense of fraud in the inducement against Wilk.

27. To the extent that a holder of a negotiable promissory note is a holder in due course, the holder takes the note free of which of the following defenses?

a. Minority of the maker where it is a defense to enforcement of a contract.

b. Forgery of the maker’s signature.

c. Discharge of the maker in bankruptcy.

d. Nonperformance of a condition precedent.

28. Under the Commercial Paper Article of the UCC, in a nonconsumer transaction, which of the following are real defenses available against a holder in due course?

29. On February 15, P.D. Stone obtained the following instrument from Astor Co. for $1,000. Stone was aware that Helco, Inc. disputed liability under the instrument because of an alleged breach by Astor of the referenced computer purchase agreement. On March 1, Willard Bank obtained the instrument from Stone for $3,900. Willard had no knowledge that Helco disputed liability under the instrument.

The reverse side of the instrument is endorsed as follows:

If Willard Bank demands payment from Helco and Helco refuses to pay the instrument because of Astor’s breach of the computer purchase agreement, which of the following statements would be correct?

a. Willard Bank is not a holder in due course because Stone was not a holder in due course.

b. Helco will not be liable to Willard Bank because of Astor’s breach.

c. Stone will be the only party liable to Willard Bank because he was aware of the dispute between Helco and Astor.

d. Helco will be liable to Willard Bank because Willard Bank is a holder in due course.

30. Northup made out a negotiable promissory note that was payable to the order of Port. This promissory note was meant to purchase some furniture that Port used to own, but he lied to Northup when he claimed he still owned it. Port immediately negotiated the note to Johnson who knew about Port’s lie. Johnson negotiated the note to Kenner who was a holder in due course. Kenner then negotiated the note back to Johnson. When Johnson sought to enforce the promissory note against Northup, she refused claiming fraud. Which of the following is correct?

a. Johnson, as a holder through a holder in due course, can enforce the promissory note.

b. Northup wins because Johnson does not have the rights of a holder in due course.

c. Northup wins because she has a real defense on this note.

d. Johnson’s knowledge of the lie does not affect his rights on this note.

31. Goran wrote out a check to Ruz to pay for a television set he purchased at a flea market from Ruz. When Goran got home, he found out the box did not have the television set but some weights. Goran immediately gave his bank a stop payment order over the phone. He followed this up with a written stop payment order. In the meantime, Ruz negotiated the check to Schmidt who qualified as a holder in due course. Schmidt gave the check as a gift to Buck. When Buck tried to cash the check, the bank and Goran both refused to pay. Which of the following is correct?

a. Buck cannot collect on the check from the bank because Goran has a real defense.

b. Buck cannot collect on the check from Goran because Goran has a personal defense.

c. Buck can require the bank to pay because Buck is a holder through a holder in due course.

d. Buck can require Goran to pay on the check even though the check was a gift.

32. Under the Negotiable Instruments Article of the UCC, which of the following parties will be a holder but not be entitled to the rights of a holder in due course?

a. A party who, knowing of a real defense to payment, received an instrument from a holder in due course.

b. A party who found an instrument payable to bearer.

c. A party who received, as a gift, an instrument from a holder in due course.

d. A party who, in good faith and without notice of any defect, gave value for an instrument.

33. A holder in due course will take free of which of the following defenses?

a. Infancy, to the extent that it is a defense to a simple contract.

b. Discharge of the maker in bankruptcy.

c. A wrongful filling-in of the amount payable that was omitted from the instrument.

d. Duress of a nature that renders the obligation of the party a nullity.

34. Cobb gave Garson a signed check with the amount payable left blank. Garson was to fill in, as the amount, the price of fuel oil Garson was to deliver to Cobb at a later date. Garson estimated the amount at $700, but told Cobb it would be no more than $900. Garson did not deliver the fuel oil, but filled in the amount of $1,000 on the check. Garson then negotiated the check to Josephs in satisfaction of a $500 debt with the $500 balance paid to Garson in cash. Cobb stopped payment and Josephs is seeking to collect $1,000 from Cobb. Cobb’s maximum liability to Josephs will be

a. $0

b. $ 500

c. $ 900

d. $1,000

35. A maker of a note will have a real defense against a holder in due course as a result of any of the following conditions except

a. Discharge in bankruptcy.

b. Forgery.

c. Fraud in the execution.

d. Lack of consideration.

H. Liability of Parties

36. Which of the following parties has (have) primary liability on a negotiable instrument?

I. Drawer of a check.

II. Drawee of a time draft before acceptance.

III. Maker of a promissory note.

a. I and II only.

b. II and III only.

c. I and III only.

d. III only.

37. Which of the following actions does not discharge a prior party to a commercial instrument?

a. Good faith payment or satisfaction of the instrument.

b. Cancellation of that prior party’s endorsement.

c. The holder’s oral renunciation of that prior party’s liability.

d. The holder’s intentional destruction of the instrument.

38. Under the Negotiable Instruments Article of the UCC, when an instrument is endorsed “Pay to John Doe” and signed “Faye Smith,” which of the following statements is (are) correct?

| Payment of the instrument is guaranteed | The instrument can be further negotiated | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

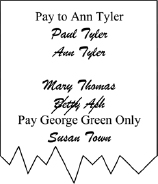

39.

Susan Town, on receiving the above instrument, struck Betty Ash’s endorsement. Under the Commercial Paper Article of the UCC, which of the endorsers of the above instrument will be completely discharged from secondary liability to later endorsers of the instrument?

a. Ann Tyler.

b. Mary Thomas.

c. Betty Ash.

d. Susan Town.

40. A subsequent holder of a negotiable instrument may cause the discharge of a prior holder of the instrument by any of the following actions except

a. Unexcused delay in presentment of a time draft.

b. Procuring certification of a check.

c. Giving notice of dishonor the day after dishonor.

d. Material alteration of a note.

41. A check has the following endorsements on the back:

Which of the following conditions occurring subsequent to the endorsements would discharge all of the endorsers?

a. Lack of notice of dishonor.

b. Late presentment.

c. Insolvency of the maker.

d. Certification of the check.

42. Robb, a minor, executed a promissory note payable to bearer and delivered it to Dodsen in payment for a stereo system. Dodsen negotiated the note for value to Mellon by delivery alone and without endorsement. Mellon endorsed the note in blank and negotiated it to Bloom for value. Bloom’s demand for payment was refused by Robb because the note was executed when Robb was a minor. Bloom gave prompt notice of Robb’s default to Dodsen and Mellon. None of the holders of the note were aware of Robb’s minority. Which of the following parties will be liable to Bloom?

| Dodsen | Mellon | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | No |

| d. | No | Yes |

43. Vex Corp. executed a negotiable promissory note payable to Tamp, Inc. The note was collateralized by some of Vex’s business assets. Tamp negotiated the note to Miller for value. Miller endorsed the note in blank and negotiated it to Bilco for value. Before the note became due, Bilco agreed to release Vex’s collateral. Vex refused to pay Bilco when the note became due. Bilco promptly notified Miller and Tamp of Vex’s default. Which of the following statements is correct?

a. Bilco will be unable to collect from Miller because Miller’s endorsement was in blank.

b. Bilco will be able to collect from either Tamp or Miller because Bilco was a holder in due course.

c. Bilco will be unable to collect from either Tamp or Miller because of Bilco’s release of the collateral.

d. Bilco will be able to collect from Tamp because Tamp was the original payee.

44. Under the Commercial Paper Article of the UCC, which of the following statements best describes the effect of a person endorsing a check “without recourse”?

a. The person has no liability to prior endorsers.

b. The person makes no promise or guarantee of payment on dishonor.

c. The person gives no warranty protection to later transferees.

d. The person converts the check into order paper.

J. Banks

45. A check is postdated to November 20 even though the check was written out on November 3 of the same year. The drawer provided notice to the bank of the postdated check. Which of the following is correct under the Revised Article 3 of the Uniform Commercial Code?

a. The check is payable on demand on or after November 3 because part of the definition of a check is that it be payable on demand.

b. The check ceases to be demand paper and is payable on November 20.

c. The postdating destroys negotiability.

d. A bank that pays the check is automatically liable for early payment.

46. Stanley purchased a computer from Comp Electronics with a personal check. Later that day, Stanley saw a better deal on the computer so he orally stopped payment on the check with his bank. The bank, however, still paid Comp Electronics when the check was presented three days later. Which of the following is correct?

a. The bank is liable to Stanley for failure to follow the oral stop payment order.

b. The bank is not liable to Stanley because the stop payment order was not in writing.

c. The bank is not liable to Stanley if Comp Electronics qualifies as a holder in due course.

d. Comp Electronics is liable to Stanley to return the amount of the check.

M. Transfer of Negotiable Documents of Title

47. A trade acceptance is an instrument drawn by a

a. Seller obligating the seller or designee to make payment.

b. Buyer obligating the buyer or designee to make payment.

c. Seller ordering the buyer or designee to make payment.

d. Buyer ordering the seller or designee to make payment.

48. Under the Documents of Title Article of the UCC, which of the following statements is (are) correct regarding a common carrier’s duty to deliver goods subject to a negotiable bearer bill of lading?

I. The carrier may deliver the goods to any party designated by the holder of the bill of lading.

II. A carrier who, without court order, delivers goods to a party claiming the goods under a missing negotiable bill of lading is liable to any person injured by the misdelivery.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

49. Which of the following is not a warranty made by the seller of a negotiable warehouse receipt to the purchaser of the document?

a. The document transfer is fully effective with respect to the goods it represents.

b. The warehouseman will honor the document.

c. The seller has no knowledge of any facts that would impair the document’s validity.

d. The document is genuine.

50. Under the UCC, a warehouse receipt

a. Will not be negotiable if it contains a contractual limitation on the warehouseman’s liability.

b. May qualify as both a negotiable warehouse receipt and negotiable commercial paper if the instrument is payable either in cash or by the delivery of goods.

c. May be issued only by a bonded and licensed warehouseman.

d. Is negotiable if by its terms the goods are to be delivered to bearer or the order of a named person.

Multiple-Choice Answers and Explanations

Answers

Explanations

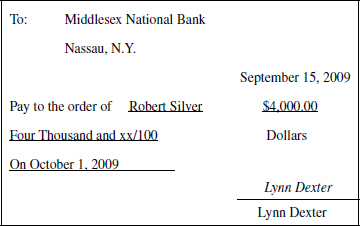

1. (a) This instrument is a draft because it is a three-party instrument where a drawer (Dexter) orders a drawee (Middlesex National Bank) to pay a fixed amount in money to the payee (Silver). Answer (b) is incorrect because in order for the instrument to qualify as a check, the instrument must be payable on demand. In this situation, the instrument held by Silver is a time draft which specifies the payment date as October 1, 2009. Answer (d) is incorrect because a promissory note is a two-party instrument in which one party promises to pay a fixed amount in money to the payee. Answer (c) is incorrect because a trade acceptance is a special type of draft in which a seller of goods extends credit to the buyer by drawing a draft on that buyer directing the buyer to pay a fixed amount in money to the seller on a specified date. The seller is therefore both the drawer and payee in a trade acceptance.

2. (c) Under the Revised Article 3 of the UCC, there are two basic categories of negotiable instruments (i.e., promissory notes and drafts). Answers (a) and (d) are incorrect because a certificate of deposit is a promissory note issued by a bank. Answer (b) is incorrect because a check is a draft drawn on a bank and payable on demand unless it is postdated.

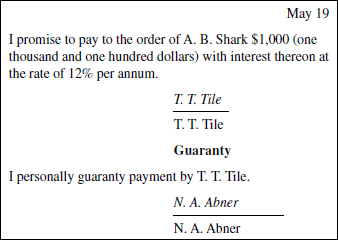

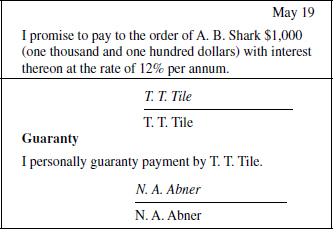

3. (a) A promissory demand note is a two-party instrument in which the maker (T. T. Tile) promises to pay to the order of the payee (A. B. Shark) and the payment is made upon demand with no time period stated. N. A. Abner made a guaranty but it is still a two-party note. Answers (b), (c), and (d) are all incorrect because sight drafts, checks, and trade acceptances are all three-party instruments requiring a drawee.

4. (a) Drafts and checks are three-party instruments in which the drawer orders the drawee to pay the payee. Notes and certificates of deposit are two-party instruments in which the maker promises to pay the payee.

5. (a) All negotiable instruments are required to be payable to order or bearer with the exception of checks. This instrument says “Pay to Jenny Larson,” therefore, it can only be negotiable if it is a check. All of these instruments in the question would be negotiable if they said “Pay to the order of Jenny Larson,” including a check.

6. (a) One of the elements of negotiability is that the note be payable to order or to bearer. Under the revised UCC, this is true for all negotiable instruments except checks that do not need the words “to the order of” or “bearer.” Answer (b) is incorrect because signing by the payee is a method of negotiation but is not a requirement to make the instrument negotiable. Answer (c) is incorrect because such references are not required. Answer (d) is incorrect because the elements of negotiability do not require the stating of any conditions of payment. In fact, such conditions can destroy negotiability.

7. (c) This promissory note is negotiable because it meets all of the requirements of negotiability. It is written and signed. It contains an unconditional promise to pay a fixed amount in money. It is payable at a definite time under the UCC even though the maker may extend the due date to March 31, because this option of the maker to extend the time is limited to a definite date. And finally, the instrument is payable to bearer because it states “Pay to Astor Co. or bearer.” Answer (a) is incorrect because the reference to the computer purchase agreement does not condition payment on this agreement, it simply refers to it. Answer (b) is incorrect because when the words and numbers are contradictory, the written words control and thus, the instrument still contains a fixed amount. Answer (d) is incorrect because once an instrument is negotiable and remains unaltered, it is negotiable for all parties.

8. (c) The Revised Article 3 of the UCC allows a negotiable instrument to be payable in any medium of exchange of the US or a foreign government. Therefore, answer (a) is incorrect. Answer (b) is incorrect because negotiability is maintained despite the fact that rate of exchange can fluctuate. This is a fact of doing business internationally. Answer (d) is incorrect because the exchange rate can be determined readily.

9. (a) This instrument satisfies all of the requirements for negotiability except for the requirement that it be payable on demand or at a definite time. Since it is payable ten days after the sale of the maker’s diamond ring, the time of payment is not certain as to the time of occurrence. It is unknown when, or if, the ring will be sold. Answer (b) is incorrect because a negotiable instrument may contain a promise to provide collateral. Answer (c) is incorrect because although it is a two-party note, it is not negotiable because it is not payable at a definite time. Answer (d) is incorrect because it is not negotiable and is not a draft. A draft requires a drawer ordering a drawee to pay the payee.

10. (d) Since this note is subject to the terms of another document, the promise in the note is conditional, causing negotiability to be destroyed. Answer (a) is incorrect because since one must look to a document outside of the note, this destroys negotiability. Answer (b) is incorrect because the note itself makes its promise conditioned on the contract. Thus, the contract cannot be ignored. Answer (c) is incorrect because the contract, which is outside of the note, must be examined. This destroys the note’s negotiability.

11. (c) For a note to be negotiable, it must be written and signed by the maker, contain an unconditional promise to pay a fixed amount in money, be payable at a definite time or on demand, and be payable to order or to bearer. This note fulfills all of these requirements. It is therefore negotiable and does not require that the payment date be specified because it is payable on demand. Answer (a) is incorrect because the note fulfills all the requirements of negotiability. Answer (b) is incorrect because in cases of inconsistencies between words and figures, the words control. Answer (d) is incorrect because although the guaranty may make the note more desirable, it was already negotiable.

12. (d) Under the Revised Article 3 of the UCC, interest rates are allowed to be variable or fluctuate. Negotiability is not destroyed. Answer (a) is incorrect because the sum certain rule allows the interest rate to vary based on such things as the prime rate of interest of a given bank. Answer (b) is incorrect because negotiability is not destroyed by needing to resort to information outside of the negotiable instrument. Answer (c) is incorrect because it is allowed for the interest to vary while the negotiable instrument is still outstanding.

13. (a) Under the Revised Article 3 of the UCC, a check may be postdated and need not be payable to order. The words “Pay to Corbin Company” are allowed for checks. However, all negotiable instruments other than checks need to be payable to order or to bearer.

14. (a) Under the Revised Article 3 of the UCC, unlike under earlier versions, payment on a negotiable instrument may be designated to come from a particular source or fund. The maker or drawer does not have to be personally obligated. Therefore, answer (b) is incorrect. Answer (c) is incorrect because this provision is not deemed to make the instrument not negotiable for reason of a conditional promise. Answer (d) is incorrect because lack of payment due to insufficient funds does not destroy negotiability.

15. (a) When the amount in words differs from the amount in figures on a negotiable instrument, the words control over the figures. Answer (b) is incorrect because the law has settled this ambiguity in favor of the words on negotiable instruments. Answer (c) is incorrect because the instrument is still negotiable and can be cashed. Answer (d) is incorrect because there is no such rule involving 10%.

16. (c) This is a very common type of restrictive endorsement. Answer (a) is incorrect because a blank endorsement is one that does not specify any endorsee. Answer (b) is incorrect because a qualified endorsement is one in which the endorser disclaims liability to pay the holder or any subsequent endorser for the instrument if it is later dishonored. An example of this is the endorser putting in the words “without recourse” on the back of the instrument. Answer (d) is incorrect because a special endorsement refers to when the endorser indicates a specific person who needs to subsequently endorse it.

17. (c) Although negotiating bearer paper only requires delivery, negotiating order paper requires both delivery and endorsement by the transferor. Delivery requires that the holder get possession of the instrument.

18. (d) Since John Smith endorsed the instrument in blank (i.e., did not specify any endorsee) it became bearer paper. Since it was bearer paper in Harris’s hands, she did not need to endorse it to negotiate it to the next party, Sharp. Answer (a) is incorrect because when Parker endorsed “Pay to John Smith only” he made the instrument require John Smith’s signature to negotiate it further. Parker’s endorsement will not restrict negotiations beyond John Smith’s and it does not destroy negotiability. Answer (b) is incorrect as although conditions on the front generally destroy the negotiability of an instrument, conditions put into an endorsement do not. Answer (c) is incorrect because the wording “Pay to John Smith only” will not restrict further negotiation after John Smith. When John Smith endorsed it in blank, it became bearer paper.

19. (d) The words “Pay to the order of Jerry Lin” are not necessary because the note is already negotiable on its face where it was payable to the order of Ann Jackson. Answer (a) is not chosen because although when Jackson endorsed the note in blank, it became bearer paper, it was converted back to order paper when Lin put “Pay to Jerry Lin” above Jackson’s endorsement. Answer (b) should not be chosen because when Jackson endorsed it without specifying any payee, the note became bearer paper. Answer (c) should not be chosen because it became order paper once “Pay to Jerry Lin” was written, whether he personally did it or not.

20. (a) This endorsement is special because it indicates “Pay to Alex Ericson” and it is restrictive because of the phrase “if he completes . . .” Answer (b) is incorrect because this endorsement is special and qualified. Answer (c) is incorrect because although it is restrictive, it is also a blank endorsement. Answer (d) is incorrect because although it is a special endorsement stating “Pay to Alex Ericson,” it is not restrictive.

21. (b) Although the note was originally a bearer instrument, Stone endorsed it with a special endorsement when s/he indicated “Pay to the order of Willard Bank, without recourse” above the endorsement. This means that Willard Bank must endorse the note to negotiate it further. Answer (a) is incorrect because qualified endorsements such as “without recourse” disclaim some liability but do not prevent subsequent parties from becoming a holder in due course. Answer (c) is incorrect because although Stone is not a holder in due course because s/he had notice that the maker disputed liability under the note, Willard Bank is a holder in due course because Willard was unaware that Helco disputed liability on the note. Additionally, Willard meets the other requirements to be a holder in due course, because he was a holder of a negotiable note, gave value ($3,900) for it, took in good faith, and had no notice, not only of the alleged breach by Astor, but of any other relevant problems such as being overdue or having been dishonored. Answer (d) is incorrect because the note was bearer paper when Stone received it and thus did not require an endorsement.

22. (a) To be a holder in due course, the holder must, among other things, take without notice that the instrument is overdue, has been dishonored, or that any person has a defense or claim to it. In this case, the person was notified that payment was refused. Answer (b) is incorrect because a prior endorser being discharged does not mean that person necessarily had a defense to the instrument. Answer (c) is incorrect because the use of a note as collateral does not prevent a holder from becoming a holder in due course. Answer (d) is incorrect because reasonable discounts are allowed and do not indicate bad faith or that a person has a defense or claim to the instrument.

23. (c) An executory promise does not satisfy the value requirement to be a holder in due course until the promise is actually performed. Answer (a) is incorrect because Ruper received the check to pay off a previous debt owed to her. Taking in satisfaction of a previous debt constitutes value to be a holder in due course. Answer (b) is incorrect because she took the check in exchange for another negotiable instrument. The fact that the check was for less than the face value of the negotiable note does not violate the value requirements. Answer (d) is incorrect because taking the check to pay off an antecedent debt constitutes value whether the debtor was a relative or not.

24. (b) In order to be a holder in due course, the individual must be a holder of a negotiable instrument as well as fulfilling the additional requirements referred to in the question. In this case, the draft is not negotiable because it is not payable to order or to bearer. However, the check is negotiable because checks do not have to be payable to order or to bearer to be negotiable.

25. (a) Even though an antecedent debt would not be valid for the consideration requirement under contract law, it is valid for the value requirement under negotiable instruments law. A promise to perform services at a future date is an executory promise and is not value until actually performed.

26. (a) Monk is not personally a HDC because although he was a holder of the negotiable note for which he gave value, he did not take in good faith because he had knowledge of the fraud before he purchased the note. Furthermore, he had notice that the note was overdue. Therefore, answer (c) can be ruled out. Answer (a) however, is correct because even though Monk was not a HDC, he obtained the instrument from Wilk who was a HDC. Therefore, Monk qualifies as a holder through a HDC and thus obtains all of the rights of a HDC. Answers (b) and (d) are incorrect because fraud in the inducement is a personal defense. Wilk, as a HDC, and Monk, as a holder through a HDC, both take the note free of personal defenses.

27. (d) A holder in due course takes an instrument free of personal defenses but is subject to real defenses. Answer (d) is correct because it involves a breach of contract or nonperformance of a condition precedent which describes a personal defense. Answer (c) is incorrect because bankruptcy is a real defense. Answer (a) is incorrect because when a minor may disaffirm a contract, it is treated as a real defense. Answer (b) is incorrect because a forgery of a maker’s or drawer’s signature is a real defense.

28. (b) Real defenses include bankruptcy and material alterations of the instrument. Material alterations include a change of any monetary amount. They also include changes in the interest rate, if any, on the instrument or changes in the date if the date affects when it is paid or the amount of interest to be paid. Personal defenses include the more typical defenses such as breach of contract, breach of warranty, and fraud in the inducement.

29. (d) Helco is claiming breach of contract which is a personal defense. The general rule is that transfer of a negotiable instrument to a holder in due course cuts off all personal defenses against the holder in due course. Since Willard Bank is a holder in due course, Helco is liable to Willard Bank. Answer (a) is incorrect because Willard Bank meets all of the requirements to be a holder in due course. That is, Willard is a holder of a negotiable instrument, gave value, took in good faith, and took without notice of certain problems such as Helco’s disputed liability. The fact that Stone was not a holder in due course does not change this. Answer (b) is incorrect because Willard Bank as a holder in due course wins against Helco’s claim of Astor’s breach. The breach of contract would only constitute a personal defense. Answer (c) is incorrect because Helco is liable to Willard Bank.

30. (b) When a negotiable instrument is negotiated from a holder in due course to another holder, this other holder normally obtains the rights of a holder in due course. However, an important exception applies to this case. Since Johnson knew of the lie when he first acquired the note, he was not a HDC and cannot improve his status by reacquiring from a HDC. Answer (a) is incorrect because he did not qualify as a HDC due to his knowledge of the defense. Answer (c) is incorrect because fraud in the inducement is a personal, not real, defense. Answer (d) is incorrect because his knowledge of the lie prevents his becoming a HDC at first and prevents his later becoming a holder through a holder in due course.

31. (d) Even though Buck did not personally qualify as a HDC, he was a holder through a holder in due course and can collect from the drawer despite the drawer’s personal defense. Answer (a) is incorrect because Goran’s defense is a personal defense. Also, the bank is permitted to follow the customer’s stop payment order. Answer (b) is incorrect because Buck as a holder through a holder in due course can collect despite the personal defense. Answer (c) is incorrect because the bank is permitted to refuse payment and then Buck collects from the drawer.

32. (b) A party who found an instrument payable to bearer is a holder but not a holder through a holder in due course. To be the latter, s/he must obtain a negotiable instrument from a holder in due course. If this had been the case, s/he would have obtained the rights of a holder in due course. However, since s/he found the instrument, it cannot be established that the previous holder was a holder in due course. Answer (a) is incorrect because s/he did receive the instrument from a holder in due course. S/he, therefore, does obtain the rights of a holder in due course even though s/he cannot be a holder in due course him/herself because of having notice of the defense on the instrument. Answer (c) is incorrect because the party received the instrument from a holder in due course and thus becomes a holder through a holder in due course. Answer (d) is incorrect because this party personally qualifies as a holder in due course, thereby obtaining those rights.

33. (c) An unauthorized completion of an incomplete instrument is a personal defense, and, as such, will not be valid against a HDC. Infancy (unless the instrument is exchanged for necessaries), bankruptcy of the maker, and extreme duress are all real defenses which are good against a HDC, thus answers (a), (b), and (d) are incorrect.

34. (d) Since Cobb left the amount blank on the signed check and Garson filled it in contrary to Cobb’s instructions, this is a case of unauthorized completion which is a personal defense. Garson then negotiated the check to Josephs who is a holder in due course because he gave value for the negotiable instrument and took in good faith without notice of any problems. He gave value for the full $1,000 since cash and taking the check for a previous debt are both value under negotiable instrument law. Therefore, Josephs may collect the full $1,000 and win over the personal defense that Cobb has.

35. (d) A maker of a note may use real defenses against a holder in due course but not personal defenses. Lack of consideration is a personal defense. Discharge in bankruptcy, forgery, and fraud in the execution are all real defenses, which create a valid defense against a holder in due course.

36. (d) The maker of a note has primary liability on that note. No one has primary liability on a draft or check unless the drawee accepts it. This is true because although the drawee has been ordered by the drawer to pay, the drawee has not agreed to pay unless it accepts the draft or check.

37. (c) When there are multiple endorsers on a negotiable instrument, each is liable to subsequent endorsers or holders. Oral renunciation of a prior party’s liability does not discharge that party’s liability. Renunciation must be in writing to discharge liability. Answer (a) is incorrect because once the primary party pays on the instrument, all endorsers are discharged from liability. Answer (b) is incorrect because cancellation of a prior party’s endorsement does discharge that party’s liability. Answer (d) is incorrect because when a holder intentionally destroys a negotiable instrument, the prior endorsers are discharged.

38. (a) When a negotiable instrument is endorsed and a specific person is indicated, the instrument is order paper and can be further negotiated by that person. Note also that payment of the instrument is guaranteed. If the primary party to the negotiable instrument does not pay, the endorser(s) are obligated to pay on the instrument when the holder demands payment or acceptance in a timely manner.

39. (c) Striking out the endorsement of a person discharges that person’s secondary liability and discharges subsequent endorsers who have already endorsed. This does not, however, discharge any of the prior parties. Therefore, in this case, Betty Ash is discharged from secondary liability to the later endorsers.

40. (c) Various acts or failures of a holder can cause a discharge of prior holders of an instrument. Among these are an unexcused delay in presenting an instrument, cancellation or renunciation of the instrument, fraudulent or material alteration, and certification of a check. Notice of dishonor generally should be given by midnight of the third business day after the dishonor or notice of the dishonor. Banks must give notice by midnight of the next banking day. In either case, answer (c) is correct. Answers (a), (b), and (d) are all incorrect because they are all acts that cause the discharge of prior holders.

41. (d) When a holder procures certification of a check, all prior endorsers are discharged. This is true because when a bank certifies a check, it has accepted the check and agreed to honor it as presented. Answers (a) and (b) are incorrect because although lack of notice of dishonor to other endorsers and late presentment of the instrument will normally discharge all endorsers, this is not true if the lack of notice of dishonor or the late presentment is excused. They can be excused in such cases as the delay is beyond the party’s control or the presentment is waived. Furthermore in this fact pattern, Hopkins endorsed the check “payment guaranteed” and Quarry endorsed it “collection guaranteed.” When words of guaranty are used, presentment or notice of dishonor are not required to hold the users liable. Answer (c) is incorrect because when the maker is insolvent the endorsers will likely be sought after for payment.

42. (d) Since Dodsen did not endorse the note, s/he gave transfer warranties and presentment warranties only to the immediate transferee (i.e., Mellon). Mellon gave these warranties to Bloom. Therefore although Mellon will be liable to Bloom, Dodsen will not be.

43. (c) Normally, Bilco could seek collection on the defaulted note from the previous endorsers, Tamp and Miller. However, in this case, Bilco agreed to release the collateral underlying this note. Since this materially affects the rights of Tamp and Miller to use this collateral, this act releases them. Answer (a) is incorrect because except for the release of the collateral, Bilco could have collected from his/her immediate transferor even without the endorsement. Answers (b) and (d) are incorrect because the release of the collateral releases Tamp and Miller.

44. (b) When a person endorses a negotiable instrument, s/he is normally secondarily liable to later endorsers. This liability means that the endorser can be required to make good on the instrument. If s/he endorses without recourse, the endorser can avoid this liability. Answer (a) is incorrect because the endorser is not liable to prior endorsers anyway whether or not s/he endorses without recourse. Answer (c) is incorrect because the endorser still gives the transferor’s warranties with some modification. Answer (d) is incorrect because a check is converted into order paper only if the endorser also specifies a payee.

45. (b) Under the Revised Article 3, postdating a check does not destroy negotiability but makes the check properly payable on or after the date written on the check. Although the postdated check is not properly payable before the date on the instrument, if a bank pays it earlier, it is not liable unless the drawer had notified the bank that the check was postdated.

46. (c) If the bank fails to follow a stop payment order, it is liable to the customer only if the customer had a valid defense on the check and therefore suffers a loss. Comp Electronics, the payee, can qualify as a HDC and Stanley would have to pay anyway despite the stop payment order. Answer (a) is incorrect because the bank did not cause Stanley a loss. Answer (b) is incorrect because oral stop payment orders are valid for fourteen days. Answer (d) is incorrect because from the facts given, there is no evidence that Comp Electronics breached the contract.

47. (c) A trade acceptance is a special type of draft in which a seller of goods extends credit to the buyer by drawing the draft on the buyer ordering the buyer to make payment to the seller on a specified date.

48. (c) A negotiable bearer bill of lading is a document of title that under the UCC allows the bearer the rights to the goods mentioned including the right to designate who will receive delivery of the goods. The carrier is required to deliver the goods to the holder of negotiable bearer bill of lading or to that holder’s designee. The carrier is liable for any misdelivery for any damages caused.

49. (b) A person who negotiates a negotiable document of title for value extends the following warranties to the immediate purchaser: (1) negotiation by the transferor is rightful and fully effective with respect to the goods it represents, (2) the transferor has no knowledge of any facts that would impair the document’s validity or worth, and (3) the document is genuine. However, the transferor of a negotiable warehouse receipt does not necessarily warrant that the warehouseman will honor the document.

50. (d) A negotiable warehouse receipt is a document issued as evidence of receipt of goods by a person engaged in the business of storing goods for hire. The warehouse receipt is negotiable if the face of the document contains the words of negotiability (order or bearer). Answer (a) is incorrect because the negotiability of the warehouse receipt is not destroyed by the inclusion of a contractual limitation on the warehouseman’s liability. Answer (b) is incorrect because to qualify as commercial paper, the instrument must be payable only in money. If an instrument is payable in money or by the delivery of goods, it is a nonnegotiable instrument. Answer (c) is incorrect because the UCC does not state that only a bonded and licensed warehouseman can issue a warehouse receipt.

Simulations

Task-Based Simulation 1

This simulation has four separate fact patterns, each followed by five legal conclusions relating to the fact pattern preceding those five numbered legal conclusions. Determine whether each conclusion is Correct or Incorrect.

An instrument purports to be a negotiable instrument. It otherwise fulfills all the elements of negotiability and it states “Pay to Rich Crane.”

| Correct | Incorrect | |

| 1. It is negotiable if it is a check and Rich Crane has possession of the check. | ||

| 2. It is negotiable if it is a draft drawn on a corporation. | ||

| 3. It is negotiable if it is a promissory note due one year later with 5% interest stated on its face. | ||

| 4. It is negotiable if it is a certificate of deposit. | ||

| 5. It is negotiable even if it is a cashier’s check. |

Another instrument fulfills all of the elements of negotiability except possibly one, that is, the instrument does not identify any payee.

| Correct | Incorrect | |

| 6. The instrument is not negotiable if it is a draft. | ||

| 7. The instrument is bearer paper if it is a check. | ||

| 8. The instrument is negotiable if it is a promissory note. | ||

| 9. The instrument is bearer paper if it is a promissory note. | ||

| 10. The instrument is negotiable only if it also states the word “negotiable” on its face. |

A promissory note states that the maker promises to pay to the order of ABC Company $10,000 plus interest at 2% above the prime rate of XYZ Bank in New York City one year from the date on the promissory note.

| Correct | Incorrect | |

| 11. The interest rate provision destroys negotiability because the prime rate can fluctuate during the year. | ||

| 12. The interest rate provision destroys negotiability because one has to look outside the note to see what the prime rate of XYZ Bank is. | ||

| 13. The maker is obligated to pay only the $10,000 because the amount of interest is not a sum certain. | ||

| 14. The maker must pay $10,000 plus the judgment rate of interest because the amount of interest cannot be determined without referring to facts outside the instrument. | ||

| 15. Any holder of this note could not qualify as a holder in due course because of the interest provision. |

An individual fills out his personal check. He postdates the check for ten days later, notifies his bank of the postdated check, and notes on the face of the check that it is for “Payment for textbooks.”

| Correct | Incorrect | |

| 16. The instrument is demand paper because it is a check and is thus payable immediately. | ||

| 17. The check is not payable before the date on its face. | ||

| 18. If a bank pays on this check before its stated date, the bank is liable to the drawer. | ||

| 19. The notation “Payment for textbooks” destroys negotiability because it makes payment conditional. | ||

| 20. The notation “Payment for textbooks” does not destroy negotiability but only if the check was actually used to pay for textbooks. |

Task-Based Simulation 2

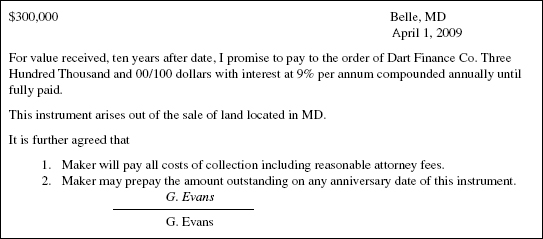

During an audit of Trent Realty Corp.’s financial statements, Clark, CPA, reviewed two instruments.

Instrument 1

The following transactions relate to Instrument 1.

- On March 15, 2010, Dart endorsed the instrument in blank and sold it to Morton for $275,000.

- On July 10, 2010, Evans informed Morton that Dart had fraudulently induced Evans into signing the instrument.

- On August 15, 2010, Trent, which knew of Evans’ claim against Dart, purchased the instrument from Morton for $50,000.

Items 1 through 5 relate to Instrument 1. For each item, select from List I the correct answer. An answer may be selected once, more than once, or not at all.

List I |

||

| A. Draft | E. Holder in due course | H. Nonnegotiable |

| B. Promissory Note | F. Holder with rights of a holder in due course under the shelter provision | I. Evans, Morton, and Dart |

| C. Security Agreement | J. Morton and Dart | |

| D. Holder | G. Negotiable | K. Only Dart |

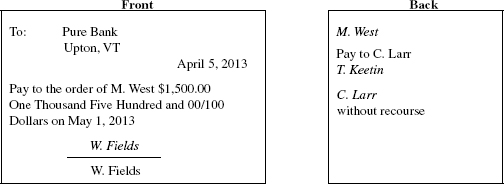

Instrument 2

Items 6 through 13 relate to Instrument 2. For each item, select from List II the correct answer. An answer may be selected once, more than once, or not at all.

List II |

|

| A. Bearer paper | F. Nonnegotiable |

| B. Blank | G. Note |

| C. Check | H. Order paper |

| D. Draft | I. Qualified |

| E. Negotiable | J. Special |

Simulation Solutions

Task-Based Simulation 1

| Correct | Incorrect | |

| 1. It is negotiable if it is a check and Rich Crane has possession of the check. | ||

| 2. It is negotiable if it is a draft drawn on a corporation. | ||

| 3. It is negotiable if it is a promissory note due one year later with 5% interest stated on its face. | ||

| 4. It is negotiable if it is a certificate of deposit. | ||

| 5. It is negotiable even if it is a cashier’s check. |

Explanations

1. (C) Even though the instrument states “Pay to Rich Crane,” it is negotiable because a check does not have to be payable to order or bearer.

2. (I) A draft to be negotiable must be payable to order or to bearer, regardless of the drawer of the draft. “Pay to the order of Rich Crane” would have made it negotiable.

3. (I) Promissory notes to be negotiable must be payable to order or to bearer.

4. (I) Certificates of deposit, unlike checks, must be payable to order or to bearer.

5. (C) A cashier’s check is an actual check and thus does not have to be payable to order or to bearer.

| Correct | Incorrect | |

| 6. The instrument is not negotiable if it is a draft. | ||

| 7. The instrument is bearer paper if it is a check. | ||

| 8. The instrument is negotiable if it is a promissory note. | ||

| 9. The instrument is bearer paper if it is a promissory note. | ||

| 10. The instrument is negotiable only if it also states the word “negotiable” on its face. |

Explanations

6. (I) If an instrument does not name any payee, it is considered to be payable to bearer. Thus, negotiability is not destroyed.

7. (C) If no payee is named, it is bearer paper.

8. (C) Since no payee was named, it is bearer paper and thus negotiability is maintained.

9. (C) Like the cases of drafts, checks, and certificates of deposit, it is bearer paper.

10. (I) There is no such requirement to state “negotiable” on its face.

| Correct | Incorrect | |

| 11. The interest rate provision destroys negotiability because the prime rate can fluctuate during the year. | ||

| 12. The interest rate provision destroys negotiability because one has to look outside the note to see what the prime rate of XYZ Bank is. | ||

| 13. The maker is obligated to pay only the $10,000 because the amount of interest is not a sum certain. | ||

| 14. The maker must pay $10,000 plus the judgment rate of interest because the amount of interest cannot be determined without referring to facts outside the instrument. | ||

| 15. Any holder of this note could not qualify as a holder in due course because of the interest provision. |

Explanations

11. (I) The negotiability of an instrument is not destroyed simply because the interest rate used may fluctuate.

12. (I) Negotiability is not destroyed even if one has to look outside of the document to determine what the actual rate is.

13. (I) Even though the interest rate may fluctuate, the maker is still obligated to pay the $10,000 plus the interest.

14. (I) The maker must pay the $10,000 plus the interest described on the promissory note.

15. (I) Since this note is negotiable despite the possible fluctuation of the interest rate, a holder could qualify to be a holder in due course under those applicable rules.

| Correct | Incorrect | |

| 16. The instrument is demand paper because it is a check and is thus payable immediately. | ||

| 17. The check is not payable before the date on its face. | ||

| 18. If a bank pays on this check before its stated date, the bank is liable to the drawer. | ||

| 19. The notation “Payment for textbooks” destroys negotiability because it makes payment conditional. | ||

| 20. The notation “Payment for textbooks” does not destroy negotiability but only if the check was actually used to pay for textbooks. |

Explanations

16. (I) Normally a check is demand paper. However, when it is postdated, it is not payable until that date.

17. (C) The postdating overrides the normal characteristic that it is payable on demand.

18. (C) The bank is liable because the drawer has given the bank prior notice of the postdating.

19. (I) Notations on negotiable instruments that note what it is for do not put conditions on the payment and thus do not destroy negotiability.

20. (I) These notations can be ignored because they are not conditions of payment.

Task-Based Simulation 2

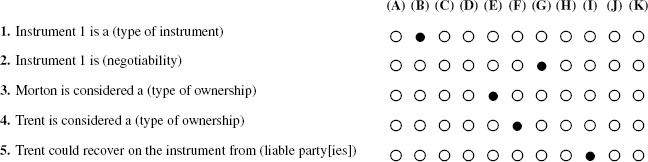

Explanations

1. (B) Instrument 1 is a two-party instrument in which Evans promises to pay a fixed amount in money to Dart; therefore it qualifies as a promissory note. A promissory note may be payable on demand or at a specific point in time.

2. (G) Instrument 1 meets the requirements of negotiability. It is written and signed by the maker. It contains an unconditional promise or order to pay a fixed amount in money, at a definite time or on demand. The document is also payable to order. The fact that it is payable on a certain date subject to acceleration does not destroy its negotiability.

3. (E) To qualify as a holder in due course, an individual must be a holder of a properly negotiated negotiable instrument, give value for the instrument, and take the instrument in good faith and without notice that it is overdue, has been dishonored, or that any person has a defense or claim to it.

4. (F) When a negotiable instrument is negotiated from a holder in due course to a second holder, the second holder usually acquires the rights of a holder in due course through the shelter provision. The shelter provision applies to holders who have not previously held the instrument with knowledge of any defenses.

5. (I) A holder with rights of a holder in due course under the shelter provision obtains all the rights of a holder in due course. A holder in due course takes an instrument free of personal defenses, including fraud in the inducement. Therefore, Evans’ claim that Dart had fraudulently induced Evans into signing the instrument would not prevent Trent from recovering from Evans. Trent would also be able to recover from Morton and Dart based on his holder in due course status.

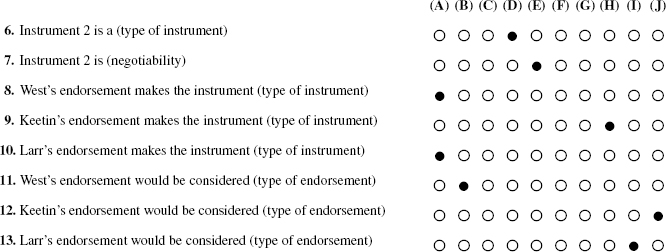

Explanations

6. (D) Instrument 2 is a draft because it is a three-party instrument where a drawer (Fields) orders a drawee (Pure Bank) to pay a fixed amount in money to the payee (West). It is not a check because it is not payable on demand.

7. (E) The draft qualifies as a negotiable instrument as it meets all of the required elements of negotiability. The draft is written and signed by the drawer. It contains an unconditional order to pay a fixed amount in money. It is made payable to order and is payable at a definite time.

8. (A) A blank endorsement which does not specify any endorsee converts order paper to bearer paper.

9. (H) An endorsement which indicates the specific person to whom the endorsee wishes to negotiate the instrument is a special endorsement. The use of a special endorsement converts bearer paper into order paper.

10. (A) Because Larr’s endorsement does not specify any endorsee, the endorsement converts the order paper into bearer paper.

11. (B) West’s endorsement is a blank endorsement because it does not specify any endorsee.

12. (J) Because Keetin’s endorsement indicates a specific person to whom the instrument is being negotiated, the endorsement is a special endorsement.

13. (I) Larr’s endorsement is a qualified endorsement because Larr disclaimed liability by signing without recourse.