Module 37: Partnership Taxation

Overview

This module presents the federal tax treatment of partnerships and partners. The tax consequences of partnership formation are covered first, followed by a review of the pass-through of partnership income and loss to partners. A partner’s basis for a partnership interest is covered next, with emphasis on the effect of partnership liabilities on a partner’s basis. Next reviewed are the special rules that apply to transactions with controlled partnerships, as well as the limitations that apply to a partnership’s adoption of a tax year. The module continues with a review of the tax effects of a partner’s sale of a partnership interest, and concludes with a review of the rules that apply to a partnership’s distribution of property to partners in both current and liquidating distributions. It is important to be able to determine a partner’s basis for distributed property, as well as the effect of the distribution on the partner’s basis for the partnership interest.

A. Entity Classification

B. Partnership Formation

C. Partnership Income and Loss

D. Partnership Agreements

E. Partner’s Basis in Partnership

F. Transactions with Controlled Partnerships

G. Taxable Year of Partnership

H. Partnership’s Use of Cash Method

I. Termination or Continuation of Partnership

J. Sale of a Partnership Interest

K. Pro Rata Distributions from Partnership

L. Non-Pro-Rata Distributions from Partnership

M. Optional Sec. 754 Adjustment to Basis of Partnership Property

N. Mandatory Adjustments to Basis of Partnership Property

Key Terms

Multiple-Choice Questions

Multiple-Choice Answers and Explanations

Simulations

Simulation Solution

Partnerships are organizations of two or more persons to carry on business activities for profit. For tax purposes, partnerships also include a syndicate, joint venture, or other unincorporated business through which any business or financial operation is conducted. Partnerships do not pay any income tax, but instead act as a conduit to pass through tax items to the partners. Partnerships file an informational return (Form 1065), and partners report their share of partnership ordinary income or loss and other items on their individual returns. The nature or character (e.g., capital, ordinary, Sec. 1231) of income or deductions is not changed by the pass-through nature of the partnership.

A. Entity Classification

B. Partnership Formation

| Adjusted basis of contributed property | $ 4,000 |

| Less: portion of mortgage allocated to other partners (80% × $6,000) | (4,800) |

| Partner’s basis (not reduced below 0) | $ 0 |

C. Partnership Income and Loss

| DR. | CR. | |

| Net sales | $160,000 | |

| Cost of goods sold | $ 88,000 | |

| Tax-exempt income | 1,500 | |

| Sec. 1231 casualty gain | 9,000 | |

| Section 1231 gain (other than casualty) | 6,000 | |

| Section 1250 gain | 20,000 | |

| Long-term capital gain | 7,500 | |

| Short-term capital loss | 6,000 | |

| Guaranteed payments ($8,000 per partner) | 24,000 | |

| Charitable contributions | 9,000 | |

| Advertising expense | 2,000 | |

| $129,000 | $204,000 | |

| Partnership ordinary income is $66,000, computed as follows: | ||

| Book income | $ 75,000 | |

| Add: | ||

| Charitable contributions | $ 9,000 | |

| Short-term capital loss | 6,000 | 15,000 |

| $ 90,000 | ||

| Deduct: | ||

| Tax-exempt income | $ 1,500 | |

| Sec. 1231 casualty gain | 9,000 | |

| Section 1231 gain (other than casualty) | 6,000 | |

| Long-term capital gain | 7,500 | 24,000 |

| Partnership ordinary income | $66,000 | |

| Each partner’s share of partnership ordinary income is $22,000. |

D. Partnership Agreements

E. Partner’s Basis in Partnership

| Beginning partnership basis | $15,000 | |

| Add: | ||

| Distributive share of partnership ordinary income | 22,000 | |

| Tax-exempt income | 500 | |

| Sec. 1231 casualty gain | 3,000 | |

| Section 1231 gain (other than casualty) | 2,000 | |

| Long-term capital gain | 2,500 | 30,000 |

| $45,000 | ||

| Less: | ||

| Short-term capital loss | $ 2,000 | |

| Charitable contributions | 3,000 | 5,000 |

| Ending partnership basis | $40,000 |

| Beginning basis | $ 75,000 |

| Individual assumption of mortgage | + 90,000 |

| $165,000 | |

| Distribution of warehouse | −120,000 |

| Partner’s share of decrease in partnership’s liabilities | − 30,000 |

| Basis after distribution | $15,000 |

F. Transactions with Controlled Partnerships

G. Taxable Year of Partnership

H. Partnership’s Use of Cash Method

I. Termination or Continuation of Partnership

J. Sale of a Partnership Interest

| Adjusted basis | Fair market value | |

| Accounts receivable | 0 | $10,000 |

| Inventory | 4,000 | 10,000 |

| Potential Sec. 1250 recapture | 0 | 10,000 |

| $4,000 | $30,000 |

K. Pro Rata Distributions from Partnership

| Partnership basis | FMV | |

| Property A | $15 | $15 |

| Property B | 15 | 5 |

| Total | $30 | $20 |

| Partnership basis | FMV | |

| Property C | $ 5 | $40 |

| Property D | 10 | 10 |

| Total | $15 | $50 |

L. Non-Pro Rata Distributions from Partnership

| Adjusted basis | FMV | |

| Cash | $ 6,000 | $ 6,000 |

| Inventory | 6,000 | 12,000 |

| Land | 9,000 | 18,000 |

| $21,000 | $36,000 |

M. Optional Sec. 754 Adjustment to Basis of Partnership Property

N. Mandatory Adjustments to Basis of Partnership Property

KEY TERMS

Current distribution. A nonliquidating partnership distribution made to a partner (i.e., the distribution does not terminate the partner’s partnership interest.

Limited liability partnership. Differs from general partnerships in that with an LLP, a partner is not liable for damages resulting from the negligence, malpractice, or fraud committed by other partners. However, each partner is personally liable for his or her own negligence, malpractice, or fraud.

Limited partnership. A partnership with two classes of partners, with at least one general partner and at least one limited partner. A limited partner generally cannot participate in the active management of the partnership, and in the event of losses, generally can lose no more than his or her capital contribution.

Liquidating distribution. A single distribution, or one of a planned series of distributions, that completely terminates a partner’s interest in the partnership.

Partnership ordinary income or loss. All partnership items that do not have to be separately stated (because they have no special tax characteristics) and can be combined and just the net amount is passed through to partners.

Sec. 751 property. A partnership’s unrealized receivables (including the recapture potential in depreciable assets) and appreciated inventory. The gain on sale of a partnership interest generally must be recognized as ordinary income to the extent of the selling partner’s share of unrealized receivables and appreciated inventory. These assets are sometimes referred to as

Sec. 754 election. An optional election that can be made by a partnership to adjust the basis of its assets to prevent any inequities that might occur as a result of the partnership’s distribution of property or the sale by a partner of a partnership interest.

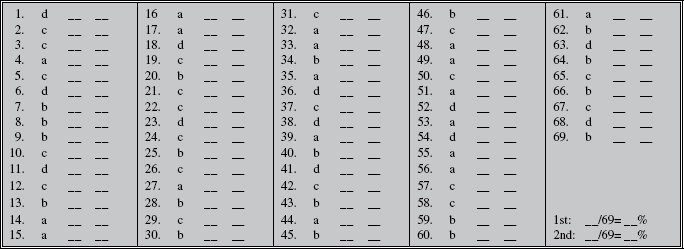

Multiple-Choice Questions (1–69)

B. Partnership Formation

1. At partnership inception, Black acquires a 50% interest in Decorators Partnership by contributing property with an adjusted basis of $250,000. Black recognizes a gain if

I. The fair market value of the contributed property exceeds its adjusted basis.

II. The property is encumbered by a mortgage with a balance of $100,000.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

2. On June 1, 2013, Kelly received a 10% interest in Rock Co., a partnership, for services contributed to the partnership. Rock’s net assets at that date had a basis of $70,000 and a fair market value of $100,000. In Kelly’s 2013 income tax return, what amount must Kelly include as income from transfer of the partnership interest?

a. $ 7,000 ordinary income.

b. $ 7,000 capital gain.

c. $10,000 ordinary income.

d. $10,000 capital gain.

3. Ola Associates is a limited partnership engaged in real estate development. Hoff, a civil engineer, billed Ola $40,000 in 2013 for consulting services rendered. In full settlement of this invoice, Hoff accepted a $15,000 cash payment plus the following:

| Fair market value | Carrying amount on Ola’s books | |

| 3% limited partnership interest in Ola | $10,000 | N/A |

| Surveying equipment | 7,000 | $3,000 |

What amount should Hoff, a cash-basis taxpayer, report in his 2013 return as income for the services rendered to Ola?

a. $15,000

b. $28,000

c. $32,000

d. $40,000

4. The following information pertains to property contributed by Gray on July 1, 2013, for a 40% interest in the capital and profits of Kag & Gray, a partnership:

| As of June 30, 2012 | |

| Adjusted basis | Fair market value |

| $24,000 | $30,000 |

After Gray’s contribution, Kag & Gray’s capital totaled $150,000. What amount of gain was reportable in Gray’s 2013 return on the contribution of property to the partnership?

a. $0

b. $ 6,000

c. $30,000

d. $36,000

5. The holding period of a partnership interest acquired in exchange for a contributed capital asset begins on the date

a. The partner is admitted to the partnership.

b. The partner transfers the asset to the partnership.

c. The partner’s holding period of the capital asset began.

d. The partner is first credited with the proportionate share of partnership capital.

6. The following information pertains to Carr’s admission to the Smith & Jones partnership on July 1, 2013:

- Carr’s contribution of capital: 800 shares of Ed Corp. stock bought in 1999 for $30,000; fair market value $150,000 on July 1, 2013.

- Carr’s interest in capital and profits of Smith & Jones: 25%.

- Fair market value of net assets of Smith & Jones on July 1, 2013, after Carr’s admission: $600,000.

Carr’s gain in 2013 on the exchange of the Ed Corp. stock for Carr’s partnership interest was

a. $120,000 ordinary income.

b. $120,000 long-term capital gain.

c. $120,000 Section 1231 gain.

d. $0.

7. The holding period of property acquired by a partnership as a contribution to the contributing partner’s capital account

a. Begins with the date of contribution to the partnership.

b. Includes the period during which the property was held by the contributing partner.

c. Is equal to the contributing partner’s holding period prior to contribution to the partnership.

d. Depends on the character of the property transferred.

8. On September 1, 2013, James Elton received a 25% capital interest in Bredbo Associates, a partnership, in return for services rendered plus a contribution of assets with a basis to Elton of $25,000 and a fair market value of $40,000. The fair market value of Elton’s 25% interest was $50,000. How much is Elton’s basis for his interest in Bredbo?

a. $25,000

b. $35,000

c. $40,000

d. $50,000

9. Basic Partnership, a cash-basis calendar-year entity, began business on February 1, 2013. Basic incurred and paid the following during 2013:

| Filing fees incident to the creation of the partnership | $ 3,600 |

| Accounting fees to prepare the representations in offering materials | 12,000 |

If Basic wishes to deduct organizational costs, what is the maximum amount that Basic can deduct on the 2013 partnership return?

a. $15,600

b. $ 3,600

c. $ 660

d. $ 220

C. Partnership Income and Loss

10. Thompson’s basis in Starlight Partnership was $60,000 at the beginning of the year. Thompson materially participates in the partnership’s business. Thompson received $20,000 in cash distributions during the year. Thompson’s share of Starlight’s current operations was a $65,000 ordinary loss and a $15,000 net long-term capital gain. What is the amount of Thompson’s deductible loss for the period?

a. $15,000

b. $40,000

c. $55,000

d. $65,000

11. In computing the ordinary income of a partnership, a deduction is allowed for

a. Contributions to recognized charities.

b. The first $100 of dividends received from qualifying domestic corporations.

c. Short-term capital losses.

d. Guaranteed payments to partners.

12. Which of the following limitations will apply in determining a partner’s deduction for that partner’s share of partnership losses?

| At-risk | Passive loss | |

| a. | Yes | No |

| b. | No | Yes |

| c. | Yes | Yes |

| d. | No | No |

13. Dunn and Shaw are partners who share profits and losses equally. In the computation of the partnership’s 2013 book income of $100,000, guaranteed payments to partners totaling $60,000 and charitable contributions totaling $1,000 were treated as expenses. What amount should be reported as ordinary income on the partnership’s 2013 return?

a. $100,000

b. $101,000

c. $160,000

d. $161,000

14. The partnership of Martin & Clark sustained an ordinary loss of $84,000 in 2013. The partnership, as well as the two partners, are on a calendar-year basis. The partners share profits and losses equally. At December 31, 2013, Clark, who materially participates in the partnership’s business, had an adjusted basis of $36,000 for his partnership interest, before consideration of the 2013 loss. On his individual income tax return for 2013, Clark should deduct a(n)

a. Ordinary loss of $36,000.

b. Ordinary loss of $42,000.

c. Ordinary loss of $36,000 and a capital loss of $6,000.

d. Capital loss of $42,000.

15. The partnership of Felix and Oscar had the following items of income during the taxable year ended December 31, 2013.

| Income from operations | $156,000 |

| Tax-exempt interest income | 8,000 |

| Dividends from foreign corporations | 6,000 |

| Net rental income | 12,000 |

What is the total ordinary income of the partnership for 2013?

a. $156,000

b. $174,000

c. $176,000

d. $182,000

D. Partnership Agreements

16. A guaranteed payment by a partnership to a partner for services rendered, may include an agreement to pay

I. A salary of $5,000 monthly without regard to partnership income.

II. A 25% interest in partnership profits.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

17. Chris, a 25% partner in Vista partnership, received a $20,000 guaranteed payment in 2013 for deductible services rendered to the partnership. Guaranteed payments were not made to any other partner. Vista’s 2013 partnership income consisted of

| Net business income before guaranteed payments | $80,000 |

| Net long-term capital gains | 10,000 |

What amount of income should Chris report from Vista Partnership on her 2013 tax return?

a. $37,500

b. $27,500

c. $22,500

d. $20,000

18. On January 2, 2013, Arch and Bean contribute cash equally to form the JK Partnership. Arch and Bean share profits and losses in a ratio of 75% to 25%, respectively. For 2013, the partnership’s ordinary income was $40,000. A distribution of $5,000 was made to Arch during 2013. What amount of ordinary income should Arch report from the JK Partnership for 2013?

a. $ 5,000

b. $10,000

c. $20,000

d. $30,000

19. Guaranteed payments made by a partnership to partners for services rendered to the partnership, that are deductible business expenses under the Internal Revenue Code, are

I. Deductible expenses on the US Partnership Return of Income, Form 1065, in order to arrive at partnership income (loss).

II. Included on Schedule K-1 to be taxed as ordinary income to the partners.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

20. The method used to depreciate partnership property is an election made by

a. The partnership and must be the same method used by the “principal partner.”

b. The partnership and may be any method approved by the IRS.

c. The “principal partner.”

d. Each individual partner.

21. Under the Internal Revenue Code sections pertaining to partnerships, guaranteed payments are payments to partners for

a. Payments of principal on secured notes honored at maturity.

b. Timely payments of periodic interest on bona fide loans that are not treated as partners’ capital.

c. Services or the use of capital without regard to partnership income.

d. Sales of partners’ assets to the partnership at guaranteed amounts regardless of market values.

22. Dale’s distributive share of income from the calendar-year partnership of Dale & Eck was $50,000 in 2013. On December 15, 2013, Dale, who is a cash-basis taxpayer, received a $27,000 distribution of the partnership’s 2013 income, with the $23,000 balance paid to Dale in February 2014. In addition, Dale received a $10,000 interest-free loan from the partnership in 2013. This $10,000 is to be offset against Dale’s share of 2014 partnership income. What total amount of partnership income is taxable to Dale in 2013?

a. $27,000

b. $37,000

c. $50,000

d. $60,000

23. At December 31, 2012, Alan and Baker were equal partners in a partnership with net assets having a tax basis and fair market value of $100,000. On January 2, 2013, Carr contributed securities with a fair market value of $50,000 (purchased in 2011 at a cost of $35,000) to become an equal partner in the new firm of Alan, Baker, and Carr. The securities were sold on December 15, 2013, for $47,000. How much of the partnership’s capital gain from the sale of these securities should be allocated to Carr?

a. $0

b. $ 3,000

c. $ 6,000

d. $12,000

24. Gilroy, a calendar-year taxpayer, is a partner in the firm of Adams and Company which has a fiscal year ending June 30. The partnership agreement provides for Gilroy to receive 25% of the ordinary income of the partnership. Gilroy also receives a guaranteed payment of $1,000 monthly which is deductible by the partnership. The partnership reported ordinary income of $88,000 for the year ended June 30, 2013, and $132,000 for the year ended June 30, 2014. How much should Gilroy report on his 2013 return as total income from the partnership?

a. $25,000

b. $30,500

c. $34,000

d. $39,000

25. On December 31, 2012, Edward Baker gave his son, Allan, a gift of a 50% interest in a partnership in which capital is a material income-producing factor. For the year ended December 31, 2013, the partnership’s ordinary income was $100,000. Edward and Allan were the only partners in 2013. There were no guaranteed payments to partners. Edward’s services performed for the partnership were worth a reasonable compensation of $40,000 for 2013. Allan has never performed any services for the partnership. What is Allan’s distributive share of partnership income for 2013?

a. $20,000

b. $30,000

c. $40,000

d. $50,000

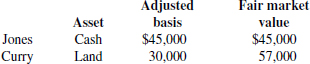

Items 26 and 27 are based on the following:

Jones and Curry formed Major Partnership as equal partners by contributing the assets below.

The land was held by Curry as a capital asset, subject to a $12,000 mortgage, that was assumed by Major.

26. What was Curry’s initial basis in the partnership interest?

a. $45,000

b. $30,000

c. $24,000

d. $18,000

27. What was Jones’ initial basis in the partnership interest?

a. $51,000

b. $45,000

c. $39,000

d. $33,000

Items 28 and 29 are based on the following:

Flagg and Miles are each 50% partners in Decor Partnership. Each partner had a $200,000 tax basis in the partnership on January 1, 2013. Decor’s 2013 net business income before guaranteed payments was $45,000. During 2013, Decor made a $7,500 guaranteed payment to Miles for deductible services rendered.

28. What total amount from Decor is includible in Flagg’s 2013 tax return?

a. $15,000

b. $18,750

c. $22,500

d. $37,500

29. What is Miles’s tax basis in Decor on December 31, 2013?

a. $211,250

b. $215,000

c. $218,750

d. $222,500

30. Peters has a one-third interest in the Spano Partnership. During 2013, Peters received a $16,000 guaranteed payment, which was deductible by the partnership, for services rendered to Spano. Spano reported a 2013 operating loss of $70,000 before the guaranteed payment. What is (are) the net effect(s) of the guaranteed payment?

I. The guaranteed payment decreases Peters’ tax basis in Spano by $16,000.

II. The guaranteed payment increases Peters’ ordinary income by $16,000.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

E. Partner’s Basis in Partnership

31. Dean is a 25% partner in Target Partnership. Dean’s tax basis in Target on January 1, 2013, was $20,000. At the end of 2013, Dean received a nonliquidating cash distribution of $8,000 from Target. Target’s 2013 accounts recorded the following items:

| Municipal bond interest income | $12,000 |

| Ordinary income | 40,000 |

What was Dean’s tax basis in Target on December 31, 2013?

a. $15,000

b. $23,000

c. $25,000

d. $30,000

32. On January 4, 2013, Smith and White contributed $4,000 and $6,000 in cash, respectively, and formed the Macro General Partnership. The partnership agreement allocated profits and losses 40% to Smith and 60% to White. In 2013, Macro purchased property from an unrelated seller for $10,000 cash and a $40,000 mortgage note that was the general liability of the partnership. Macro’s liability

a. Increases Smith’s partnership basis by $16,000.

b. Increases Smith’s partnership basis by $20,000.

c. Increases Smith’s partnership basis by $24,000.

d. Has no effect on Smith’s partnership basis.

33. Gray is a 50% partner in Fabco Partnership. Gray’s tax basis in Fabco on January 1, 2013, was $5,000. Fabco made no distributions to the partners during 2013, and recorded the following:

| Ordinary income | $20,000 |

| Tax exempt income | 8,000 |

| Portfolio income | 4,000 |

What is Gray’s tax basis in Fabco on December 31, 2013?

a. $21,000

b. $16,000

c. $12,000

d. $10,000

34. On January 1, 2013, Kane was a 25% equal partner in Maze General Partnership, which had partnership liabilities of $300,000. On January 2, 2013, a new partner was admitted and Kane’s interest was reduced to 20%. On April 1, 2013, Maze repaid a $100,000 general partnership loan. Ignoring any income, loss, or distributions for 2013, what was the net effect of the two transactions for Kane’s tax basis in Maze partnership interest?

a. Has no effect.

b. Decrease of $35,000.

c. Increase of $15,000.

d. Decrease of $75,000.

35. Lee inherited a partnership interest from Dale during 2013. The adjusted basis of Dale’s partnership interest was $50,000, and its fair market value on the date of Dale’s death (the estate valuation date) was $70,000. What was Lee’s original basis for the partnership interest?

a. $70,000

b. $50,000

c. $20,000

d. $0

36. Which of the following should be used in computing the basis of a partner’s interest acquired from another partner?

| Cash paid by transferee to transferor | Transferee’s share of partnership liabilities | |

| a. | No | Yes |

| b. | Yes | No |

| c. | No | No |

| d. | Yes | Yes |

37. Hall and Haig are equal partners in the firm of Arosa Associates. On January 1, 2013, each partner’s adjusted basis in Arosa was $40,000. During 2013 Arosa borrowed $60,000, for which Hall and Haig are personally liable. Arosa sustained an operating loss of $10,000 for the year ended December 31, 2013. The basis of each partner’s interest in Arosa at December 31, 2013, was

a. $35,000

b. $40,000

c. $65,000

d. $70,000

F. Transactions with Controlled Partnerships

38. Doris and Lydia are sisters and also are equal partners in the capital and profits of Agee & Nolan. The following information pertains to 300 shares of Mast Corp. stock sold by Lydia to Agee & Nolan.

| Year of purchase | 2006 |

| Year of sale | 2013 |

| Basis (cost) | $9,000 |

| Sales price (equal to fair market value) | $4,000 |

The amount of long-term capital loss that Lydia recognized in 2013 on the sale of this stock was

a. $5,000

b. $3,000

c. $2,500

d. $0

39. In March 2013, Lou Cole bought 100 shares of a listed stock for $10,000. In May 2013, Cole sold this stock for its fair market value of $16,000 to the partnership of Rook, Cole & Clive. Cole owned a one-third interest in this partnership. In Cole’s 2013 tax return, what amount should be reported as short-term capital gain as a result of this transaction?

a. $6,000

b. $4,000

c. $2,000

d. $0

40. Kay Shea owns a 55% interest in the capital and profits of Dexter Communications, a partnership. In 2013, Kay sold an oriental lamp to Dexter for $5,000. Kay bought this lamp in 2007 for her personal use at a cost of $1,000 and had used the lamp continuously in her home until the lamp was sold to Dexter. Dexter purchased the lamp as an investment. What is Kay’s reportable gain in 2013 on the sale of the lamp to Dexter?

a. $4,000 ordinary income.

b. $4,000 long-term capital gain.

c. $2,200 ordinary income.

d. $1,800 long-term capital gain.

41. Gladys Peel owns a 50% interest in the capital and profits of the partnership of Peel and Poe. On July 1, 2013, Peel bought land the partnership had used in its business for its fair market value of $10,000. The partnership had acquired the land five years ago for $16,000. For the year ended December 31, 2013, the partnership’s net income was $94,000 after recording the $6,000 loss on the sale of land. Peel’s distributive share of ordinary income from the partnership for 2013 was

a. $47,000

b. $48,500

c. $49,000

d. $50,000

G. Taxable Year of Partnership

42. Under Section 444 of the Internal Revenue Code, certain partnerships can elect to use a tax year different from their required tax year. One of the conditions for eligibility to make a Section 444 election is that the partnership must

a. Be a limited partnership.

b. Be a member of a tiered structure.

c. Choose a tax year where the deferral period is not longer than three months.

d. Have less than seventy-five partners.

43. Which one of the following statements regarding a partnership’s tax year is correct?

a. A partnership formed on July 1 is required to adopt a tax year ending on June 30.

b. A partnership may elect to have a tax year other than the generally required tax year if the deferral period for the tax year elected does not exceed three months.

c. A “valid business purpose” can no longer be claimed as a reason for adoption of a tax year other than the generally required tax year.

d. Within thirty days after a partnership has established a tax year, a form must be filed with the IRS as notification of the tax year adopted.

44. Without obtaining prior approval from the IRS, a newly formed partnership may adopt

a. A taxable year which is the same as that used by one or more of its partners owning an aggregate interest of more than 50% in profits and capital.

b. A calendar year, only if it comprises a twelve-month period.

c. A January 31 year-end if it is a retail enterprise, and all of its principal partners are on a calendar year.

d. Any taxable year that it deems advisable to select.

45. Irving Aster, Dennis Brill, and Robert Clark were partners who shared profits and losses equally. On February 28, 2013, Aster sold his interest to Phil Dexter. On March 31, 2013, Brill died, and his estate held his interest for the remainder of the year. The partnership continued to operate and for the fiscal year ending June 30, 2013, it had a profit of $45,000. Assuming that partnership income was earned on a pro rata monthly basis and that all partners were calendar-year taxpayers, the distributive shares to be included in 2013 gross income should be

a. Aster $10,000, Brill $0, Estate of Brill $15,000, Clark $15,000, and Dexter $5,000.

b. Aster $10,000, Brill $11,250, Estate of Brill $3,750, Clark $15,000, and Dexter $5,000.

c. Aster $0, Brill $11,250, Estate of Brill $3,750, Clark $15,000, and Dexter $15,000.

d. Aster $0, Brill $0, Estate of Brill $15,000, Clark $15,000, and Dexter $15,000.

I. Termination or Continuation of Partnership

46. On January 3, 2013, the partners’ interests in the capital, profits, and losses of Able Partnership were

| % of capital profits and losses | |

| Dean | 25% |

| Poe | 30% |

| Ritt | 45% |

On February 4, 2013, Poe sold her entire interest to an unrelated person. Dean sold his 25% interest in Able to another unrelated person on December 20, 2013. No other transactions took place in 2013. For tax purposes, which of the following statements is correct with respect to Able?

a. Able terminated as of February 4, 2013.

b. Able terminated as of December 20, 2013.

c. Able terminated as of December 31, 2013.

d. Able did not terminate.

47. Curry’s sale of her partnership interest causes a partnership termination. The partnership’s business and financial operations are continued by the other members. What is (are) the effect(s) of the termination?

I. There is a deemed distribution of assets to the remaining partners and the purchaser.

II. There is a hypothetical recontribution of assets to a new partnership.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

48. Cobb, Danver, and Evans each owned a one-third interest in the capital and profits of their calendar-year partnership. On September 18, 2013, Cobb and Danver sold their partnership interests to Frank, and immediately withdrew from all participation in the partnership. On March 15, 2014, Cobb and Danver received full payment from Frank for the sale of their partnership interests. For tax purposes, the partnership

a. Terminated on September 18, 2013.

b. Terminated on December 31, 2013.

c. Terminated on March 15, 2014.

d. Did not terminate.

49. Partnership Abel, Benz, Clark & Day is in the real estate and insurance business. Abel owns a 40% interest in the capital and profits of the partnership, while Benz, Clark, and Day each owns a 20% interest. All use a calendar year. At November 1, 2013, the real estate and insurance business is separated, and two partnerships are formed: Partnership Abel & Benz takes over the real estate business, and Partnership Clark & Day takes over the insurance business. Which one of the following statements is correct for tax purposes?

a. Partnership Abel & Benz is considered to be a continuation of Partnership Abel, Benz, Clark & Day.

b. In forming Partnership Clark & Day, partners Clark and Day are subject to a penalty surtax if they contribute their entire distributions from Partnership Abel, Benz, Clark & Day.

c. Before separating the two businesses into two distinct entities, the partners must obtain approval from the IRS.

d. Before separating the two businesses into two distinct entities, Partnership Abel, Benz, Clark & Day must file a formal dissolution with the IRS on the prescribed form.

50. Under which of the following circumstances is a partnership that is not an electing large partnership considered terminated for income tax purposes?

I. Fifty-five percent of the total interest in partnership capital and profits is sold within a twelve-month period.

II. The partnership’s business and financial operations are discontinued.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

51. David Beck and Walter Crocker were equal partners in the calendar-year partnership of Beck & Crocker. On July 1, 2013, Beck died. Beck’s estate became the successor in interest and continued to share in Beck & Crocker’s profits until Beck’s entire partnership interest was liquidated on April 30, 2013. At what date was the partnership considered terminated for tax purposes?

a. April 30, 2013.

b. December 31, 2013.

c. July 31, 2012.

d. July 1, 2012.

J. Sale of a Partnership Interest

52. On December 31, 2013, after receipt of his share of partnership income, Clark sold his interest in a limited partnership for $30,000 cash and relief of all liabilities. On that date, the adjusted basis of Clark’s partnership interest was $40,000, consisting of his capital account of $15,000 and his share of the partnership liabilities of $25,000. The partnership has no unrealized receivables or appreciated inventory. What is Clark’s gain or loss on the sale of his partnership interest?

a. Ordinary loss of $10,000.

b. Ordinary gain of $15,000.

c. Capital loss of $10,000.

d. Capital gain of $15,000.

Items 53 and 54 are based on the following:

The personal service partnership of Allen, Baker & Carr had the following cash basis balance sheet at December 31, 2013:

| Assets | Adjusted basis per books | Market value |

| Cash | $102,000 | $102,000 |

| Unrealized accounts receivable | __ | 420,000 |

| Totals | $102,000 | $522,000 |

| Liability and Capital | ||

| Note payable | $ 60,000 | $ 60,000 |

| Capital accounts: | ||

| Allen | 14,000 | 154,000 |

| Baker | 14,000 | 154,000 |

| Carr | 14,000 | 154,000 |

| Totals | $102,000 | $522,000 |

Carr, an equal partner, sold his partnership interest to Dole, an outsider, for $154,000 cash on January 1, 2014. In addition, Dole assumed Carr’s share of the partnership’s liability.

53. What was the total amount realized by Carr on the sale of his partnership interest?

a. $174,000

b. $154,000

c. $140,000

d. $134,000

54. What amount of ordinary income should Carr report in his 2014 income tax return on the sale of his partnership interest?

a. $0

b. $ 20,000

c. $ 34,000

d. $140,000

55. On April 1, 2013, George Hart, Jr. acquired a 25% interest in the Wilson, Hart, and Company partnership by gift from his father. The partnership interest had been acquired by a $50,000 cash investment by Hart, Sr. on July 1, 2007. The tax basis of Hart, Sr.’s partnership interest was $60,000 at the time of the gift. Hart, Jr. sold the 25% partnership interest for $85,000 on December 17, 2013. What type and amount of capital gain should Hart, Jr. report on his 2013 tax return?

a. A long-term capital gain of $25,000.

b. A short-term capital gain of $25,000.

c. A long-term capital gain of $35,000.

d. A short-term capital gain of $35,000.

56. On June 30, 2013, James Roe sold his interest in the calendar-year partnership of Roe & Doe for $30,000. Roe’s adjusted basis in Roe & Doe at June 30, 2013, was $7,500 before apportionment of any 2013 partnership income. Roe’s distributive share of partnership income up to June 30, 2013, was $22,500. Roe acquired his interest in the partnership in 2008. How much long-term capital gain should Roe report in 2013 on the sale of his partnership interest?

a. $0

b. $15,000

c. $22,500

d. $30,000

K. Pro Rata Distributions from Partnership

57. Stone and Frazier decided to terminate the Woodwest Partnership as of December 31. On that date, Woodwest’s balance sheet was as follows:

| Cash | $2,000 |

| Land (adjusted basis) | 2,000 |

| Capital—Stone | 3,000 |

| Capital—Frazier | 1,000 |

The fair market value of the land was $3,000. Frazier’s outside basis in the partnership was $1,200. Upon liquidation, Frazier received $1,500 in cash. What gain should Frazier recognize?

a. $0

b. $250

c. $300

d. $500

58. Curry’s adjusted basis in Vantage Partnership was $5,000 at the time he received a nonliquidating distribution of land. The land had an adjusted basis of $6,000 and a fair market value of $9,000 to Vantage. What was the amount of Curry’s basis in the land?

a. $9,000

b. $6,000

c. $5,000

d. $1,000

59. Hart’s adjusted basis in Best Partnership was $9,000 at the time he received the following nonliquidating distribution of partnership property:

| Cash | $ 5,000 |

| Land | |

| Adjusted basis | 7,000 |

| Fair market value | 10,000 |

What was the amount of Hart’s basis in the land?

a. $0

b. $ 4,000

c. $ 7,000

d. $10,000

60. Day’s adjusted basis in LMN Partnership interest is $50,000. During the year Day received a nonliquidating distribution of $25,000 cash plus land with an adjusted basis of $15,000 to LMN, and a fair market value of $20,000. How much is Day’s basis in the land?

a. $10,000

b. $15,000

c. $20,000

d. $25,000

Items 61 and 62 are based on the following:

The adjusted basis of Jody’s partnership interest was $50,000 immediately before Jody received a current distribution of $20,000 cash and property with an adjusted basis to the partnership of $40,000 and a fair market value of $35,000.

61. What amount of taxable gain must Jody report as a result of this distribution?

a. $0

b. $ 5,000

c. $10,000

d. $20,000

62. What is Jody’s basis in the distributed property?

a. $0

b. $30,000

c. $35,000

d. $40,000

63. On June 30, 2013, Berk, a calendar-year taxpayer, retired from his partnership. At that time, his capital account was $50,000 and his share of the partnership’s liabilities was $30,000. Berk’s retirement payments consisted of being relieved of his share of the partnership liabilities and receipt of cash payments of $5,000 per month for eighteen months, commencing July 1, 2013. Assuming Berk makes no election with regard to the recognition of gain from the retirement payments, he should report income of

| 2013 | 2014 | |

| a. | $13,333 | $26,667 |

| b. | 20,000 | 20,000 |

| c. | 40,000 | __ |

| d. | __ | 40,000 |

64. The basis to a partner of property distributed in complete liquidation of the partner’s interest is the

a. Adjusted basis of the partner’s interest increased by any cash distributed to the partner in the same transaction.

b. Adjusted basis of the partner’s interest reduced by any cash distributed to the partner in the same transaction.

c. Adjusted basis of the property to the partnership.

d. Fair market value of the property.

Items 65 and 66 are based on the following data:

Mike Reed, a partner in Post Co., received the following distribution from Post:

| Post’s basis | Fair market value | |

| Cash | $11,000 | $11,000 |

| Inventory | 5,000 | 12,500 |

Before this distribution, Reed’s basis in Post was $25,000.

65. If this distribution were nonliquidating, Reed’s basis for the inventory would be

a. $14,000

b. $12,500

c. $ 5,000

d. $ 1,500

66. If this distribution were in complete liquidation of Reed’s interest in Post, Reed’s recognized gain or loss resulting from the distribution would be

a. $7,500 gain.

b. $9,000 loss

c. $1,500 loss.

d. $0.

67. In 2008, Lisa Bara acquired a one-third interest in Dee Associates, a partnership. In 2013, when Lisa’s entire interest in the partnership was liquidated, Dee’s assets consisted of the following: cash, $20,000 and tangible property with a basis of $46,000 and a fair market value of $40,000. Dee has no liabilities. Lisa’s adjusted basis for her one-third interest was $22,000. Lisa received cash of $20,000 in liquidation of her entire interest. What was Lisa’s recognized loss in 2013 on the liquidation of her interest in Dee?

a. $0.

b. $2,000 short-term capital loss.

c. $2,000 long-term capital loss.

d. $2,000 ordinary loss.

68. For tax purposes, a retiring partner who receives retirement payments ceases to be regarded as a partner

a. On the last day of the taxable year in which the partner retires.

b. On the last day of the particular month in which the partner retires.

c. The day on which the partner retires.

d. Only after the partner’s entire interest in the partnership is liquidated.

69. John Albin is a retired partner of Brill & Crum, a personal service partnership. Albin has not rendered any services to Brill & Crum since his retirement in 2011. Under the provisions of Albin’s retirement agreement, Brill & Crum is obligated to pay Albin 10% of the partnership’s net income each year. In compliance with this agreement, Brill & Crum paid Albin $25,000 in 2013. How should Albin treat this $25,000?

a. Not taxable.

b. Ordinary income.

c. Short-term capital gain.

d. Long-term capital gain.

Multiple-Choice Answers and Explanations

Answers

Explanations

1. (d) The requirement is to determine which statements are correct regarding Black’s recognition of gain on transferring property with an adjusted basis of $250,000 in exchange for a 50% partnership interest. Generally, no gain is recognized when appreciated property is transferred to a partnership in exchange for a partnership interest. However, gain will be recognized if the transferred property is encumbered by a mortgage, and the partnership’s assumption of the mortgage results in a decrease in the transferor’s individual liabilities that exceeds the basis of the property transferred. Here, the basis of the property transferred is $250,000, and the net decrease in Black’s individual liabilities is $50,000 (i.e., $100,000 × 50%), so no gain is recognized.

2. (c) The requirement is to determine the amount that must be included on Kelly’s 2013 income tax return as the result of the receipt of a 10% partnership interest in exchange for services. A taxpayer must recognize ordinary income when a capital interest in a partnership is received as compensation for services rendered. The amount of ordinary income to be included on Kelly’s 2013 return is the fair market value of the partnership interest received ($100,000 × 10% = $10,000).

3. (c) The requirement is to determine the amount that Hoff, a cash-basis taxpayer, should report as income for the services rendered to Ola Associates. A cash-basis taxpayer generally reports income when received, unless constructively received at an earlier date. The amount of income to be reported is the amount of money, plus the fair market value of other property received. In this case, Hoff must report a total of $32,000, which includes the $15,000 cash, the $10,000 FMV of the limited partnership interest, and the $7,000 FMV of the surveying equipment received. Note that since Hoff is a cash-basis taxpayer, he would not report income at the time that he billed Ola $40,000, nor would he be entitled to a bad debt deduction when he accepts $32,000 of consideration in full settlement of his $40,000 invoice.

4. (a) The requirement is to determine the amount of gain reportable in Gray’s return as a result of Gray’s contribution of property in exchange for a 40% partnership interest. Generally, no gain or loss is recognized on the contribution of property in exchange for a partnership interest. Note that this nonrecognition rule applies even though the value of the partnership capital interest received (40% × $150,000 = $60,000) exceeds the fair market value of the property contributed ($30,000).

5. (c) The requirement is to determine the correct statement regarding the holding period for a partnership interest acquired in exchange for a contributed capital asset. The holding period for a partnership interest that is acquired through a contribution of property depends upon the nature of the contributed property. If the contributed property was a capital asset or Sec. 1231 asset to the contributing partner, the holding period of the acquired partnership interest includes the period of time that the capital asset or Sec. 1231 asset was held by the partner. For all other contributed property, a partner’s holding period for a partnership interest begins when the partnership interest is acquired.

6. (d) The requirement is to determine the amount of gain recognized on the exchange of stock for a partnership interest. Generally no gain or loss is recognized on the transfer of property to a partnership in exchange for a partnership interest. Since Carr’s gain is not recognized, there will be a carryover basis of $30,000 for the stock to the partnership, and Carr will have a $30,000 basis for the 25% partnership interest received.

7. (b) The requirement is to determine the holding period for property acquired by a partnership as a contribution to the contributing partner’s capital account. Generally no gain or loss is recognized on the contribution of property to a partnership in exchange for a capital interest. Since the partnership’s basis for the contributed property is determined by reference to the contributing partner’s former basis for the property (i.e., a transferred basis), the partnership’s holding period includes the period during which the property was held by the contributing partner.

8. (b) The requirement is to determine Elton’s basis for his 25% interest in the Bredbo partnership. Since Elton received a capital interest with an FMV of $50,000 in exchange for property worth $40,000 and services, Elton must recognize compensation income of $10,000 ($50,000 − $40,000) on the transfer of services for a capital interest. Thus, Elton’s basis for his partnership interest consists of the $25,000 basis of assets transferred plus the $10,000 of income recognized on the transfer of services, a total of $35,000.

9. (b) The requirement is to determine the maximum amount of filing fees and accounting fees that Basic could deduct on the 2013 partnership return. The filing fees incident to the creation of the partnership are organizational expenditures. A partnership may deduct up to $5,000 of organizational expenditures for the tax year in which the partnership begins business, with any remaining expenditures deducted ratably over the 180-month period beginning with the month in which the partnership begins business. Here, since the organizational expenditures total only $3,600, they can be fully deducted for 2013.

The accounting fees to prepare the representations in offering materials are considered syndication fees. Syndication fees include the costs connected with the issuing and marketing of partnership interests such as commissions, professional fees, and printing costs. These costs must be capitalized and can neither be amortized nor depreciated.

10. (c) The requirement is to determine the amount of loss that Thompson can deduct as a result of his interest in the Starlight Partnership. A partner’s distributive share of partnership losses is generally deductible to the extent of the tax basis for the partner’s partnership interest at the end of the year. All positive basis adjustments and all reductions for distributions must be taken into account before determining the amount of deductible loss. Here, Thompson’s basis of $60,000 at the beginning of the year would be increased by the $15,000 of net long-term capital gain, reduced by the $20,000 cash distribution, to $55,000. As a result, Thompson’s deduction of the ordinary loss for the current year is limited to $55,000 which reduces the basis for his partnership interest to zero. He cannot deduct the remaining $10,000 of ordinary loss currently, but will carry it forward and deduct it when he has sufficient basis for his partnership interest.

11. (d) The requirement is to determine the item that is deductible in the computation of the ordinary income of a partnership. Guaranteed payments to partners are always deductible in computing a partnership’s ordinary income. Contributions to recognized charities and short-term capital losses cannot be deducted in computing a partnership’s ordinary income because they are subject to special limitations and must be separately passed through so that any applicable limitations can be applied at the partner level. Similarly, dividends are an item of portfolio income and must be separately passed through to partners in order to retain its character as portfolio income when reported on partners’ returns.

12. (c) The requirement is to determine whether the at-risk and passive activity loss limitations apply in determining a partner’s deduction for that partner’s share of partnership losses. A partner’s distributive share of partnership losses is generally deductible by the partner to the extent of the partner’s basis in the partnership at the end of the taxable year. Additionally, the deductibility of partnership losses is limited to the amount of the partner’s at-risk basis, and will also be subject to the passive activity loss limitations if they are applicable. Note that the at-risk and passive activity loss limitations apply at the partner level, rather than at the partnership level.

13. (b) The requirement is to determine the amount to be reported as ordinary income on the partnership’s return given partnership book income of $100,000. The $60,000 of guaranteed payments to partners were deducted in computing partnership book income and are also deductible in computing partnership ordinary income. However, the $1,000 charitable contribution deducted in arriving at partnership book income must be separately passed through to partners on Schedule K-1 and cannot be deducted in computing partnership ordinary income. Thus, the partnership’s ordinary income is $100,000 + $1,000 = $101,000.

14. (a) The requirement is to determine the amount and type of partnership loss to be deducted on Clark’s individual return. Since a partnership functions as a pass-through entity, the nature of a loss as an ordinary loss is maintained when passed through to partners. However, the amount of partnership loss that can be deducted by a partner is limited to a partner’s tax basis in the partnership at the end of the partnership taxable year. Thus, Clark’s distributive share of the ordinary loss ($42,000) is only deductible to the extent of $36,000. The remaining $6,000 of loss would be carried forward by Clark and could be deducted after his partnership basis has been increased.

15. (a) The requirement is to determine the ordinary income of the partnership. Income from operations is considered ordinary income. The net rental income and the dividends from foreign corporations are separately allocated to partners and must be excluded from the computation of the partnership’s ordinary income. Tax-exempt income remains tax-exempt and must also be excluded from the computation of ordinary income. Thus, ordinary income only consists of the income from operations of $156,000.

16. (a) The requirement is to determine the correct statement(s) concerning agreements for guaranteed payments. Guaranteed payments are payments made to a partner for services or for the use of capital if the payments are determined without regard to the amount of partnership income. Guaranteed payments are deductible by a partnership in computing its ordinary income or loss from trade or business activities, and must be reported as self-employment income by the partner receiving payment. A payment that represents a 25% interest in partnership profits could not be classified as a guaranteed payment because the payment is conditioned on the partnership having profits.

17. (a) The requirement is to determine the amount of income that Chris should report as a result of her 25% partnership interest. A partnership is a pass-through entity and its items of income and deduction pass through to be reported on partners’ returns even though not distributed. The amount to be reported by Chris consists of her guaranteed payment, plus her 25% share of the partnership’s business income and capital gains. Since Chris’s $20,000 guaranteed payment is for deductible services rendered to the partnership, it must be subtracted from the partnership’s net business income before guaranteed payments of $80,000 to determine the amount of net business income to be allocated among partners. Chris’s reportable income from the partnership includes

| Guaranteed payment | $20,000 |

| Business income [($80,000 − $20,000) × 25%] | 15,000 |

| Net long-term capital gain ($10,000 × 25%) | 2,500 |

| $37,500 |

18. (d) The requirement is to determine Arch’s share of the JK Partnership’s ordinary income for 2013. A partnership functions as a pass-through entity and its items of income and deduction are passed through to partners according to their profit and loss sharing ratios, which may differ from the ratios used to divide capital. Here, Arch’s distributive share of the partnership’s ordinary income is $40,000 × 75% = $30,000. Note that Arch will be taxed on his $30,000 distributive share of ordinary income even though only $5,000 was distributed to him.

19. (c) The requirement is to determine whether the statements regarding partners’ guaranteed payments are correct. Guaranteed payments made by a partnership to partners for services rendered are an ordinary deduction in computing a partnership’s ordinary income or loss from trade or business activities on page 1 of Form 1065. Partners must report the receipt of guaranteed payments as ordinary income (self-employment income) and that is why the payments also must be separately listed on Schedule K and Schedule K-1.

20. (b) The requirement is to determine the correct statement regarding a partnership’s election of a depreciation method. The method used to depreciate partnership property is an election made by the partnership and may be any method approved by the IRS. The partnership is not restricted to using the same method as used by its “principal partner.” Since the election is made at the partnership level, and not by each individual partner, partners are bound by whatever depreciation method that the partnership elects to use.

21. (c) The requirement is to determine the correct statement regarding guaranteed payments to partners. Guaranteed payments are payments made to partners for their services or for the use of capital without regard to the amount of the partnership’s income. Guaranteed payments are deductible by the partnership in computing its ordinary income or loss from trade of business activities, and must be reported as self-employment income by the partners receiving payment.

22. (c) The requirement is to determine the total amount of partnership income that is taxable to Dale in 2013. A partnership functions as a pass-through entity and its items of income and deduction are passed through to partners on the last day of the partnership’s taxable year. Income and deduction items pass through to be reported by partners even though not actually distributed during the year. Here, Dale is taxed on his $50,000 distributive share of partnership income for 2013, even though $23,000 was not received until 2014. The $10,000 interest-free loan does not effect the pass-through of income for 2013, and the $10,000 offset against Dale’s distributive share of partnership income for 2014 will not effect the pass-through of that income in 2014.

23. (d) The requirement is to determine the amount of the partnership’s capital gain from the sale of securities to be allocated to Carr. Normally, the entire amount of precontribution gain would be allocated to Carr. However, in this case the allocation to Carr is limited to the partnership’s recognized gain resulting from the sale, $47,000 selling price − $35,000 basis = $12,000.

24. (c) The requirement is to determine the amount that Gilroy should report for 2013 as total income from the partnership. Gilroy’s income will consist of his share of the partnership’s ordinary income for the fiscal year ending June 30, 2013 (the partnership year that ends within his year), plus the twelve monthly guaranteed payments that he received for that period of time.

| 25% × $88,000 | = | $22,000 |

| 12 × $ 1,000 | = | 12,000 |

| Total income | = | $34,000 |

25. (b) The requirement is to determine Allan’s distributive share of the partnership income. In a family partnership, services performed by family members must first be reasonably compensated before income is allocated according to the capital interests of the partners. Since Edward’s services were worth $40,000, Allan’s distributive share of partnership income is ($100,000 − $40,000) × 50% = $30,000.

26. (c) The requirement is to determine Curry’s initial basis for the 50% partnership interest received in exchange for a contribution of property subject to a $12,000 mortgage that was assumed by the partnership. Generally, no gain or loss is recognized on the contribution of property in exchange for a partnership interest. As a result, Curry’s initial basis for the partnership interest received consists of the $30,000 adjusted basis of the land contributed to the partnership, less the net reduction in Curry’s individual liability resulting from the partnership’s assumption of the $12,000 mortgage. Since Curry received a 50% partnership interest, the net reduction in Curry’s individual liability is $12,000 × 50% = $6,000. As a result, Curry’s basis for the partnership interest is $30,000 − $6,000 = $24,000.

27. (a) The requirement is to determine Jones’ initial basis for the 50% partnership interest received in exchange for a contribution of cash of $45,000. Since partners are individually liable for their share of partnership liabilities, an increase in partnership liabilities increases a partner’s basis in the partnership by the partner’s share of the increase. Jones’ initial basis consists of the $45,000 of cash contributed, increased by the increase in Jones’ individual liability resulting from the partnership’s assumption of Curry’s mortgage ($12,000 × 50% = $6,000). Thus, Jones’ initial basis for the partnership interest is $45,000 + $6,000 = $51,000.

28. (b) The requirement is to determine the total amount includible in Flagg’s 2013 tax return as a result of Flagg’s 50% interest in the Decor Partnership. Decor’s net business income of $45,000 would be reduced by the guaranteed payment of $7,500, resulting in $37,500 of ordinary income that would pass through to be reported on partners’ returns. Here, Flagg’s share of the includible income would be $37,500 × 50% = $18,750.

29. (c) The requirement is to determine Miles’s tax basis for his 50% interest in the Decor Partnership on December 31, 2013. The basis for a partner’s partnership interest is increased by the partner’s distributive share of partnership income that is taxed to the partner. Here, Decor’s net business income of $45,000 would be reduced by the guaranteed payment of $7,500, resulting in $37,500 of ordinary income that would pass through to be reported on partners’ returns and increase the basis of their partnership interests. Here, Miles’s beginning tax basis for the partnership interest of $200,000 would be increased by Miles’s distributive share of ordinary income ($37,500 × 50% = $18,750), to $218,750.

30. (b) The requirement is to determine the net effect(s) of the $16,000 guaranteed payment made to Peters by the Spano Partnership who reported an operating loss of $70,000 before deducting the guaranteed payment. A guaranteed payment is a partnership payment made to a partner for services or for the use of capital if the payment is determined without regard to the amount of partnership income. A guaranteed payment is deductible by a partnership in computing its ordinary income or loss from trade or business activities and must be reported as self-employment income by the partner receiving the payment, thereby increasing Peters’ ordinary income by $16,000. However, since Peters has only a one-third interest in the Spano Partnership, the $16,000 of guaranteed payment deducted by Spano would have the effect of reducing Peters’ tax basis in Spano by only one-third of $16,000.

31. (c) The requirement is to determine the basis for Dean’s 25% partnership interest at December 31, 2013. A partner’s basis for a partnership interest is increased or decreased by the partner’s distributive share of all partnership items. Basis is increased by the partner’s distributive share of all income items (including tax-exempt income) and is decreased by all loss and deduction items (including nondeductible items) and distributions received from the partnership. In this case, Dean’s beginning basis of $20,000 would be increased by the pass-through of his distributive share of the partnership’s ordinary income ($40,000 × 25% = $10,000) and municipal bond interest income ($12,000 × 25% = $3,000), and would be decreased by the $8,000 cash nonliquidating distribution that he received.

32. (a) The requirement is to determine the effect of a $40,000 increase in partnership liabilities on the basis for Smith’s 40% partnership interest. Since partners are individually liable for their share of partnership liabilities, a change in the amount of partnership liabilities affects a partner’s basis for a partnership interest. When partnership liabilities increase, it is effectively treated as if each partner individually borrowed money and then made a capital contribution of the borrowed amount. As a result, an increase in partnership liabilities increases each partner’s basis in the partnership by each partner’s share of the increase. Here, Smith’s basis is increased by his 40% share of the mortgage (40% × $40,000 = $16,000).

33. (a) The requirement is to determine Gray’s tax basis for a 50% interest in the Fabco Partnership. The basis for a partner’s partnership interest is increased by the partner’s distributive share of all partnership items of income and is decreased by the partner’s distributive share of all loss and deduction items. Here, Gray’s beginning basis of $5,000 would be increased by Gray’s 50% distributive share of ordinary income ($10,000), tax-exempt income ($4,000), and portfolio income ($2,000), resulting in an ending basis of $21,000 for Gray’s Fabco partnership interest.

34. (b) The requirement is to determine the net effect of the two transactions on Kane’s tax basis for his Maze partnership interest. A partner’s basis for a partnership interest consists of the partner’s capital account plus the partner’s share of partnership liabilities. A decrease in a partner’s share of partnership liabilities is considered to be a deemed distribution of money and reduces a partner’s basis for the partnership interest. Here, Kane’s partnership interest was reduced from 25% to 20% on January 2, resulting in a reduction in Kane’s share of liabilities of 5% × $300,000 = $15,000. Subsequently, on April 1, when there was a $100,000 repayment of partnership loans, there was a further reduction in Kane’s share of partnership liabilities of 20% × $100,000 = $20,000. Thus, the net effect of the reduction of Kane’s partnership interest to 20% from 25%, and the repayment of $100,000 of partnership liabilities would be to reduce Kane’s basis for the partnership interest by $15,000 + $20,000 = $35,000.

35. (a) The requirement is to determine the original basis of Lee’s partnership interest that was received as an inheritance from Dale. The basis of property received from a decedent dying during 2013 is generally its fair market value as of date of death. Since fair market value on the date of Dale’s death was used for estate tax purposes, Lee’s original basis is $70,000.

36. (d) The requirement is to determine whether cash paid by a transferee, and the transferee’s share of partnership liabilities are to be included in computing the basis of a partner’s interest acquired from another partner. When an existing partner sells a partnership interest, the consideration received by the transferor partner, and the basis of the transferee’s partnership interest includes both the cash actually paid by the transferee to the transferor, as well as the transferee’s assumption of the transferor’s share of partnership liabilities.

37. (c) The requirement is to determine the basis of each partner’s interest in Arosa at December 31, 2013. Since there are two equal partners, each partner’s adjusted basis in Arosa of $40,000 on January 1, 2013, would be increased by 50% of the $60,000 loan and would be decreased by 50% of the $10,000 operating loss. Thus, each partner’s basis in Arosa at December 31, 2013, would be $40,000 + $30,000 liability − $5,000 loss = $65,000.

38. (d) The requirement is to determine the amount of long-term capital loss recognized by Lydia from the sale of stock to Agee & Nolan. A loss is disallowed if incurred in a transaction between a partnership and a person owning (directly or constructively) more than a 50% capital or profits interest. Although Lydia directly owns only a 50% partnership interest, she constructively owns her sister’s 50% partnership interest. Since Lydia directly and constructively has a 100% partnership interest, her $5,000 loss is disallowed.

39. (a) The requirement is to determine the amount to be reported as short-term capital gain on Cole’s sale of stock to the partnership. If a person engages in a transaction with a partnership other than as a partner of such partnership, any resulting gain is generally recognized just as if the transaction had occurred with a nonpartner. Here, Cole’s gain of $16,000 − $10,000 = $6,000 is fully recognized. Since the stock was not held for more than twelve months, Cole’s $6,000 gain is treated as a short-term capital gain.

40. (b) The requirement is to determine the amount and nature of Kay’s gain from the sale of the lamp to Admor. A gain that is recognized on a sale of property between a partnership and a person owning a more than 50% partnership interest will be treated as ordinary income if the property is not a capital asset in the hands of the transferee. Although Kay has a 55% partnership interest, the partnership purchased the lamp as an investment (i.e., a capital asset), and Kay’s gain will solely depend on how she held the lamp. Since she used the lamp for personal use, Kay has a $5,000 − $1,000 = $4,000 long-term capital gain.

41. (d) The requirement is to determine Peel’s distributive share of ordinary income from the partnership. Although the $6,000 loss that was deducted in arriving at the partnership’s net income would also be deductible for tax purposes, it must be separately passed through to partners because it is a Sec. 1231 loss. Thus, the $6,000 loss must be added back to the $94,000 of partnership net income and results in partnership ordinary income of $100,000. Peel’s share is $100,000 × 50% = $50,000.

42. (c) The requirement is to determine the correct statement regarding a partnership’s eligibility to make a Sec. 444 election. A partnership must generally adopt the same taxable year as used by its one or more partners owning an aggregate interest of more than 50% in partnership profits and capital. However, under Sec. 444, a partnership can instead elect to adopt a fiscal year that does not result in a deferral period of longer than three months. The deferral period is the number of months between the end of its selected year and the year that it generally would be required to adopt. For example, a partnership that otherwise would be required to adopt a taxable year ending December 31, could elect to adopt a fiscal year ending September 30. The deferral period would be the months of October, November, and December. The partnership is not required to be a limited partnership, be a member of tiered structure, or have less than seventy-five partners.

43. (b) The requirement is to determine the correct statement regarding a partnership’s tax year. A partnership must generally determine its taxable year in the following order: (1) it must adopt the taxable year used by its one or more partners owning an aggregate interest of more than 50% in profits and capital; (2) if partners owning a more than 50% interest in profits and capital do not have the same year-end, the partnership must adopt the same taxable year as used by all of its principal partners; and (3) if principal partners have different taxable years, the partnership must adopt the taxable year that results in the least aggregate deferral of income to partners.

A different taxable year other than the year determined above can be used by a partnership if a valid business purpose can be established and IRS permission is received. Alternatively, a partnership can elect to use a tax year (other than one required under the general rules in the first paragraph), if the election does not result in a deferral of income of more than three months. The deferral period is the number of months between the close of the elected tax year and the close of the year that would otherwise be required under the general rules. Thus, a partnership that would otherwise be required to adopt a tax year ending December 31 could elect to adopt a fiscal year ending September 30 (three-month deferral), October 31 (two-month deferral), or November 30 (one-month deferral). Note that a partnership that makes this election must make “required payments” which are in the nature of refundable, noninterest-bearing deposits that are intended to compensate the Treasury for the revenue lost as a result of the deferral period.

44. (a) A newly formed partnership must adopt the same taxable year as is used by its partners owning a more than 50% interest in profits and capital. If partners owning more than 50% do not have the same taxable year, a partnership must adopt the same taxable year as used by all of its principal partners (i.e., partners with a 5% or more interest in capital and profits). If its principal partners have different taxable years, a partnership must adopt the tax year that results in the least aggregate deferral of income to partners.

45. (b) The requirement is to determine the distributive shares of partnership income for the partnership fiscal year ended June 30, 2013, to be included in gross income by Aster, Brill, Estate of Brill, Clark, and Dexter. Clark was a partner for the entire year and is taxed on his distributive 1/3 share ($45,000 × 1/3 = $15,000). Since Aster sold his entire partnership interest to Dexter, the partnership tax year closes with respect to Aster on February 28. As a result, Aster’s distributive share is $45,000 × 1/3 × 8/12 = $10,000. Dexter’s distributive share is $45,000 × 1/3 / 4/12 = $5,000.

Additionally, a partnership tax year closes with respect to a deceased partner as of date of death. Since Brill died on March 31, the distributive share to be included in Brill’s 2013 Form 1040 would be $45,000 × 1/3 × 9/12 = $11,250. Since Brill’s estate held his partnership interest for the remainder of the year, the estate’s distributive share of income is $45,000 × 1/3 × 3/12 = $3,750.

46. (b) The requirement is to determine the correct statement regarding the termination of the Able Partnership. A partnership is terminated for tax purposes when there is a sale or exchange of 50% or more of the total interests in partnership capital and profits within any twelve-month period. Since Poe sold her 30% interest on February 4, 2013, and Dean sold his 25% partnership interest on December 20, 2013, there has been a sale of 55% of the total interests within a twelve-month period and the Able Partnership is terminated on December 20, 2013.

47. (c) The requirement is to determine which statements are correct concerning the termination of a partnership. A partnership will terminate when there is a sale of 50% or more of the total interests in partnership capital and profits within any twelve-month period. When this occurs, there is a deemed distribution of assets to the remaining partners and the purchaser, and a hypothetical recontribution of these same assets to a new partnership.

48. (a) The requirement is to determine the date on which the partnership terminated for tax purposes. The partnership was terminated on September 18, 2013, the date on which Cobb and Danver sold their partnership interests to Frank, since on that date there was a sale of 50% or more of the total interests in partnership capital and profit.

49. (a) The requirement is to determine the correct statement concerning the division of Partnership Abel, Benz, Clark, & Day into two partnerships. Following the division of a partnership, a resulting partnership is deemed to be a continuation of the prior partnership if the resulting partnership’s partners had a more than 50% interest in the prior partnership. Here, as a result of the division, Partnership Abel & Benz is considered to be a continuation of the prior partnership because its partners (Abel and Benz) owned more than 50% of the interests in the prior partnership (i.e., Abel 40% and Benz 20%).

50. (c) The requirement is to determine under which circumstances a partnership, other than an electing large partnership, is considered terminated for income tax purposes. A partnership will be terminated when (1) there are no longer at least two partners, (2) no part of any business, financial operation, or venture of the partnership continues to be carried on by any of its partners in a partnership, or (3) within a twelve-month period there is a sale or exchange of 50% or more of the total interest in partnership capital and profits.

51. (a) The requirement is to determine the date on which the partnership was terminated. A partnership generally does not terminate for tax purposes upon the death of a partner, since the deceased partner’s estate or successor in interest continues to share in partnership profits and losses. However, the Beck and Crocker Partnership was terminated when Beck’s entire partnership interest was liquidated on April 30, 2013, since there no longer were at least two partners and the business ceased to exist as a partnership.

52. (d) The requirement is to determine the amount and character of gain or loss recognized on the sale of Clark’s partnership interest. A partnership interest is a capital asset and a sale generally results in capital gain or loss, except that ordinary income must be reported to the extent of the selling partner’s share of unrealized receivables and appreciated inventory. Here, Clark realized $55,000 from the sale of his partnership interest ($30,000 cash + relief from his $25,000 share of partnership liabilities). Since the partnership had no unrealized receivables or appreciated inventory and the basis of Clark’s interest was $40,000, Clark realized a capital gain of $55,000 − $40,000 = $15,000 from the sale.

53. (a) The requirement is to determine the total amount realized by Carr on the sale of his partnership interest. The total amount realized consists of the amount of cash received plus the buyer’s assumption of Carr’s share of partnership liabilities. Thus, the total amount realized is $154,000 + ($60,000 × 1/3) = $174,000.

54. (d) The requirement is to determine the amount of ordinary income that Carr should report on the sale of his partnership interest. Although the sale of a partnership interest generally results in capital gain or loss, ordinary income must be recognized to the extent of the selling partner’s share of unrealized receivables and appreciated inventory. Here, Carr must report ordinary income to the extent of his 1/3 share of the unrealized accounts receivable of $420,000, or $140,000.

55. (a) The requirement is to determine the amount and type of capital gain to be reported by Hart, Jr. from the sale of his partnership interest. Since the partnership interest was acquired by gift from Hart, Sr., Jr.’s basis would be the same as Sr.’s basis at date of gift, $60,000. Since Jr.’s basis is determined from Sr.’s basis, Jr.’s holding period includes the period the partnership interest was held by Sr. Thus, Hart, Jr. will report a LTCG of $85,000 − $60,000 = $25,000.

56. (a) The requirement is to determine the amount of LTCG to be reported by Roe on the sale of his partnership interest. Roe’s basis for his partnership interest of $7,500 must first be increased by his $22,500 distributive share of partnership income, to $30,000. Since the selling price also was $30,000, Roe will report no gain or loss on the sale of his partnership interest.

57. (c) The requirement is to determine Frazier’s recognized gain resulting from the cash received in liquidation of his partnership interest. A distributee partner will recognize any realized gain or loss resulting from the complete liquidation of the partner’s interest if only cash is received. Since Frazier’s basis for his partnership interest was $1,200 and he received $1,500 cash, Frazier must recognize a $300 capital gain.

58. (c) The requirement is to determine the basis for land acquired in a nonliquidating partnership distribution. Generally, no gain or loss is recognized on the distribution of partnership property to a partner. As a result, the partner’s basis for distributed property is generally the same as the partnership’s former basis for the property (a transferred basis). However, since the distribution cannot reduce the basis for the partner’s partnership interest below zero, the distributed property’s basis to the partner is limited to the partner’s basis for the partnership interest before the distribution. In this case, Curry’s basis for the land will be limited to the $5,000 basis for his partnership interest before the distribution.