Appendix A: Regulation Sample Examination

Testlet 1

1. Able, Bray, and Carry form a general partnership to produce and sell widgets. Able is a CPA, Bray has an MBA, and Carry has few skills. In their partnership agreement, they decide to split any profits they have in the following respective proportions: 45%, 45%, and 10%. They fail to agree on how they will share any losses. At the end of the first year of operations they have a large loss. Assuming each of the partners has sufficient assets to cover the loss of their partnership, how will they split the losses between Able, Bray, and Carry, respectively?

a. 45%, 45%, and 10%.

b. Equally.

c. It cannot be determined yet until they agree upon a loss-sharing plan.

d. A court of law will have to decide upon the way they will each share the loss.

2. CPAs must be concerned with their responsibilities in the performance of professional services. In performing an audit, a CPA

a. Is strictly liable for failure to exercise due professional care.

b. Is strictly liable for failure to detect management fraud.

c. Is not liable unless the CPA is found to be grossly negligent.

d. Is strictly liable for failure to detect illegal acts.

3. The Apex Surety Company wrote a general fidelity bond covering defalcations by the employees of Watson, Inc. Thereafter, Grand, an employee of Watson, embezzled $18,900 of company funds. When his activities were discovered, Apex paid Watson the full amount in accordance with the terms of the fidelity bond, and then sought recovery against Watson’s auditors, Kane & Dobbs, CPAs. Which of the following would be Kane & Dobbs’ best defense?

a. Apex is not in privity of contract.

b. The shortages were the result of clever forgeries and collusive fraud that would not be detected by an examination made in accordance with generally accepted auditing standards.

c. Kane & Dobbs were not guilty either of gross negligence or fraud.

d. Kane & Dobbs were not aware of the Apex-Watson surety relationship.

4. If a stockholder sues a CPA for common law fraud based on false statements contained in the financial statements audited by the CPA, which of the following, if present, would be the CPA’s best defense?

a. The stockholder lacks privity to sue.

b. The false statements were immaterial.

c. The CPA did not financially benefit from the alleged fraud.

d. The contributory negligence of the client.

5. Mathews is an agent for Sears with the express authority to solicit orders from customers in a geographic area assigned by Sears. Mathews has no authority to grant discounts or to collect payment on orders solicited. Mathews secured an order from Davidson for $1,000 less a 10% discount if Davidson makes immediate payment. Davidson had previously done business with Sears through Mathews but this was the first time that a discount-payment offer had been made. Davidson gave Mathews a check for $900 and, thereafter, Mathews turned in both the check and the order to Sears. The order clearly indicated that a 10% discount had been given by Mathews. Sears shipped the order and cashed the check. Later, Sears attempted to collect $100 as the balance owed on the order from Davidson. Which of the following is correct?

a. Sears can collect the $100 from Davidson because Mathews contracted outside the scope of his express or implied authority.

b. Sears cannot collect the $100 from Davidson because Mathews, as an agent with express authority to solicit orders, had implied authority to give discounts and collect.

c. Sears cannot collect the $100 from Davidson as Sears has ratified the discount granted and made to Mathews.

d. Sears cannot collect the $100 from Davidson because, although Mathews had no express or implied authority to grant a discount and collect, Mathews had apparent authority to do so.

6. Regulation D of the Securities Act of 1933 is available to issuers without regard to the dollar amount of an offering only when the

a. Purchasers are all accredited investors.

b. Number of purchasers who are nonaccredited is thirty-five or less.

c. Issuer is not a reporting company under the Securities Exchange Act of 1934.

d. Issuer is not an investment company.

7. Nat purchased a typewriter from Rob. Rob is not in the business of selling typewriters. Rob tendered delivery of the typewriter after receiving payment in full from Nat. Nat informed Rob that he was unable to take possession of the typewriter at that time, but would return later that day. Before Nat returned, the typewriter was destroyed by a fire. The risk of loss

a. Passed to Nat upon Rob’s tender of delivery.

b. Remained with Rob, since Nat had not yet received the typewriter.

c. Passed to Nat at the time the contract was formed and payment was made.

d. Remained with Rob, since title had not yet passed to Nat.

8. On April 14, 2010, Seeley Corp. entered into a written agreement to sell to Boone Corp. 1,200 cartons of certain goods at $.40 per carton, delivery within 30 days. The agreement contained no other terms. On April 15, 2010, Boone and Seeley orally agreed to modify their April 14 agreement so that the new quantity specified was 1,500 cartons, same price and delivery terms. What is the status of this modification?

a. Enforceable.

b. Unenforceable under the statute of frauds.

c. Unenforceable for lack of consideration.

d. Unenforceable because the change is substantial.

9. Purdy purchased real property from Hart and received a warranty deed with full covenants. Recordation of this deed is

a. Not necessary if the deed provides that recordation is not required.

b. Necessary to vest the purchaser’s legal title to the property conveyed.

c. Required primarily for the purpose of providing the local taxing authorities with the information necessary to assess taxes.

d. Irrelevant if the subsequent party claiming superior title had actual notice of the unrecorded deed.

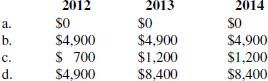

10. Richard Brown, who retired on May 31, 2012, receives a monthly pension benefit of $700 payable for life. His life expectancy at the date of retirement is ten years. The first pension check was received on June 15, 2012. During his years of employment, Brown contributed $12,000 to the cost of his company’s pension plan. How much of the pension amounts received may Brown exclude from taxable income for the years 2012, 2013, and 2014?

11. Lee, an attorney, uses the cash receipts and disbursements method of reporting. In 2013, a client gave Lee 500 shares of a listed corporation’s stock in full satisfaction of a $10,000 legal fee the client owed to Lee. This stock had a fair market value of $8,000 on the date it was given to Lee. The client’s basis for this stock was $6,000. Lee sold the stock for cash in January 2014. In Lee’s 2013 income tax return, what amount of income should be reported in connection with the receipt of the stock?

a. $10,000

b. $ 8,000

c. $ 6,000

d. $0

12. Don Wolf became a general partner in Gata Associates on January 1, 2013, with a 5% interest in Gata’s profits, losses, and capital. Gata is a distributor of auto parts. Wolf does not materially participate in the partnership business. For the year ended December 31, 2013, Gata had an operating loss of $100,000. In addition, Gata earned interest of $20,000 on a temporary investment. Gata has kept the principal temporarily invested while awaiting delivery of equipment that is presently on order. The principal will be used to pay for this equipment. Wolf’s passive loss for 2013 is

a. $0

b. $4,000

c. $5,000

d. $6,000

13. In 2013, Don Mills, a single taxpayer, had $70,000 in taxable income before personal exemptions. Mills had no tax preferences. His itemized deductions were as follows:

| State and local income taxes | $5,000 |

| Home mortgage interest on loan to acquire residence | 6,000 |

| Miscellaneous deductions that exceed 2% of adjusted gross income | 2,000 |

What amount did Mills report as alternative minimum taxable income before the AMT exemption?

a. $72,000

b. $75,000

c. $77,000

d. $83,000

14. An accuracy-related penalty applies to the portion of tax underpayment attributable to

I. Negligence or a disregard of the tax rules or regulations.

II. Any substantial understatement of income tax.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

15. Smith, an individual calendar-year taxpayer, purchased 100 shares of Core Co. common stock for $15,000 on November 15, 2013, and an additional 100 shares for $13,000 on December 30, 2013. On January 3, 2014, Smith sold the shares purchased on November 15, 2013, for $13,000. What amount of loss from the sale of Core’s stock is deductible on Smith’s 2013 and 2014 income tax returns?

| 2013 | 2014 | |

| a. | $0 | $0 |

| b. | $0 | $2,000 |

| c. | $1,000 | $1,000 |

| d. | $2,000 | $0 |

16. Strom acquired a 25% interest in Ace Partnership by contributing land having an adjusted basis of $16,000 and a fair market value of $50,000. The land was subject to a $24,000 mortgage, which was assumed by Ace. No other liabilities existed at the time of the contribution. What was Strom’s basis in Ace?

a. $0

b. $16,000

c. $26,000

d. $32,000

Items 17 and 18 are based on the following data:

Mike Reed, a partner in Post Co., received the following distribution from Post:

| Post’s basis | Fair market value | |

| Cash | $11,000 | $11,000 |

| Land | 5,000 | 12,500 |

Before this distribution, Reed’s basis in Post was $25,000.

17. If this distribution were nonliquidating, Reed’s recognized gain or loss on the distribution would be

a. $11,000 gain.

b. $ 9,000 loss.

c. $ 1,500 loss.

d. $0.

18. If this distribution were in complete liquidation of Reed’s interest in Post, Reed’s basis for the land would be

a. $14,000

b. $12,500

c. $ 5,000

d. $ 1,500

19. Finbury Corporation’s taxable income for the year ended December 31, 2013, was $2,000,000 on which its tax liability was $680,000. In order for Finbury to escape the estimated tax underpayment penalty for the year ending December 31, 2014, Finbury’s 2014 estimated tax payments must equal at least

a. 90% of the 2014 tax liability.

b. 93% of the 2014 tax liability.

c. 100% of the 2014 tax liability.

d. The 2014 tax liability of $680,000.

20. Barbaro Corporation’s retained earnings at January 1, 2013, was $600,000. During 2013 Barbaro paid cash dividends of $150,000 and received a federal income tax refund of $26,000 as a result of an IRS audit of Barbaro’s 2010 tax return. Barbaro’s net income per books for the year ended December 31, 2013, was $274,900 after deducting federal income tax of $183,300. How much should be shown in the reconciliation Schedule M-2, of Form 1120, as Barbaro’s retained earnings at December 31, 2013?

a. $443,600

b. $600,900

c. $626,900

d. $750,900

21. Brooke, Inc., an S corporation, was organized on January 2, 2013, with two equal stockholders who materially participate in the S corporation’s business. Each stockholder invested $5,000 in Brooke’s capital stock, and each loaned $15,000 to the corporation. Brooke then borrowed $60,000 from a bank for working capital. Brooke sustained an operating loss of $90,000 for the year ended December 31, 2013. How much of this loss can each stockholder claim on his 2013 income tax return?

a. $ 5,000

b. $20,000

c. $45,000

d. $50,000

22. When Jim and Nina became engaged in April 2013, Jim gave Nina a ring that had a fair market value of $50,000. After their wedding in July 2013, Jim gave Nina $75,000 in cash so that Nina could have her own bank account. Both Jim and Nina are US citizens. What was the amount of Jim’s 2013 marital deduction?

a. $0

b. $ 75,000

c. $115,000

d. $125,000

23. Ross, a calendar-year, cash-basis taxpayer who died in June 2013, was entitled to receive a $10,000 accounting fee that had not been collected before the date of death. The executor of Ross’ estate collected the full $10,000 in July 2013. This $10,000 should appear in

a. Only the decedent’s final individual income tax return.

b. Only the estate’s fiduciary income tax return.

c. Only the estate tax return.

d. Both the fiduciary income tax return and the estate tax return.

24. Kopel was engaged to prepare Raff’s 2012 federal income tax return. During the tax preparation interview, Raff told Kopel that he paid $3,000 in property taxes in 2012. Actually, Raff’s property taxes amounted to only $600. Based on Raff’s word, Kopel deducted the $3,000 on Raff’s return, resulting in an understatement of Raff’s tax liability. Kopel had no reason to believe that the information was incorrect. Kopel did not request underlying documentation and was reasonably satisfied by Raff’s representation that Raff had adequate records to support the deduction. Which of the following statements is correct?

a. To avoid the preparer penalty for willful understatement of tax liability, Kopel was obligated to examine the underlying documentation for the deduction.

b. To avoid the preparer penalty for willful understatement of tax liability, Kopel would be required to obtain Raff’s representation in writing.

c. Kopel is not subject to the preparer penalty for willful understatement of tax liability because the deduction that was claimed was more than 25% of the actual amount that should have been deducted.

d. Kopel is not subject to the preparer penalty for willful understatement of tax liability because Kopel was justified in relying on Raff’s representation.

Hints for Testlet 1

1. Losses are essentially negative profits.

2. Professionals must exercise due professional care.

3. Compliance with GAAS indicates due care.

4. Recall proof requirements.

5. The principal accepted the benefits of the unauthorized act.

6. Recall the requirements for a private placement.

7. Rob is not a merchant.

8. After modification, contract is for >$500.

9. Notice can be constructive or actual.

10. Each payment is part income and part a return of Brown’s investment.

11. The amount of compensation is determined from the value of the property received.

12. Interest is generally considered portfolio income.

13. Qualified residence interest in the form of acquisition indebtedness is deductible for AMT purposes.

14. The items listed are two components of the accuracy-related penalty.

15. The acquisition of substantially identical stock within a thirty-day period before or after the date of the loss results in a wash sale.

16. The 75% net reduction in liability is treated as a deemed cash distribution.

17. No loss can be recognized in a non liquidating distribution.

18. No loss can be recognized in a liquidating distribution if property other than cash, receivables, or inventory is received.

19. Because of taxable income in excess of $1 million, Finbury cannot use its tax for the preceding year as a safe estimate.

20. Schedule M-2 provides a reconciliation of unappropriated retained earnings per books.

21. Shareholders do not receive basis for the corporation’s debts to third parties.

22. The taxpayer must be married on the date of gift to qualify for the marital deduction.

23. The fee qualifies as income in respect of a decedent.

24. A preparer is not required to audit or examine a client’s books and records.

Answers to Testlet 1

Explanations

1. (a) If partners agree on unequal profit sharing but are silent on loss sharing, losses are shared based on the profit-sharing proportions.

2. (a) CPAs are required ethically and legally to exercise due professional care in the performance of all services.

3. (b) The surety with respect to this loss is given the same rights as the client under common law and may sue for ordinary negligence. The CPAs’ best defense is that an audit performed in accordance with professional standards would not have detected the fraud.

4. (b) Under common law, the shareholder has the right to sue for fraud on the part of the auditor. The auditor’s best defense is to show that the false statements are not material.

5. (c) Sears cannot collect from Davidson because Sears ratified the discount granted by shipping the goods and cashing the check.

6. (b) Rule 506 allows private placement of unlimited amounts of securities if the number of unaccredited investors is no more than 35.

7. (a) Risk of loss passes to the buyer on tender of delivery unless the seller is a merchant.

8. (b) Modification of contract must be in writing if contract, as modified, is covered by the Statue of Frauds (i.e., sale of goods for $500 or more).

9. (d) Under a notice-type statute, a subsequent purchaser, whether he or she records or not, prevails over a previous purchaser who did not record before that subsequent purchase.

10. (c) The amount that is not taxable is based on the ratio of contribution to total expected benefits. This ratio is $12,000/(120 months × $700), which is equal to $12,000/$84,000 or 1/7. In 2012, the nontaxable amount would equal $700 [1/7 × ($700 × 7 months)]. In 2013 and 2014, the nontaxable amount would equal $1,200 [1/7 × ($700 × 12)].

11. (b) The stock should be recognized as revenue at its fair market value when it is received.

12. (c) The interest income is portfolio income. Therefore, Wolf would have a passive loss of $5,000.

13. (c) The alternative minimum taxable income is $77,000 ($70,000 + $5,000 + $2,000). Since the mortgage interest was from a loan used to acquire a personal residence, it does not have to be added back.

14. (c) An accuracy-related penalty applies to both situations.

15. (a) The sale is a wash sale and the loss is not deductible.

16. (a) The basis of a partner’s partnership interest is increased by the adjusted basis of the property contributed. Since the basis of the property ($16,000) is less than the amount of the mortgage assumed by the partnership ($24,000), the partner’s basis is $0.

17. (d) A partner recognizes gain only to the extent that the money received exceeds the partner’s partnership basis.

18. (a) The land absorbs Reed’s basis in the partnership after adjusting for the receipt of the cash, or $14,000 ($25,000 basis − $11,000 cash received).

19. (c) No penalty will be assessed if the estimated tax payments are equal to at least 100% of the current year’s tax.

20. (d) Retained earnings at year end should be shown as $750,900 ($600,000 + $274,900 net income + $26,000 tax refund − $150,000 dividends).

21. (b) The shareholders are limited to their basis in the corporation ($5,000 cash contributed + $15,000 loan to the corporation).

22. (b) The marital deduction is generally unlimited. Therefore, the entire $75,000 is a deduction. The value of the ring is not considered because the individuals were not married when the gift was made.

23. (d) The amount would be included in both returns.

24. (d) The preparer is not required to audit the information and may accept the taxpayer’s representation unless it is unreasonable.

Testlet 2

1. Three partners have formed a general partnership that they desire to last for several years. They have not agreed to any specified time period. Which of the following is true under the Revised Uniform Partnership Act?

a. The partnership agreement is required to be in writing.

b. All three partners are required to share profits or losses equally.

c. Each of the three partners has an equal right to participate in the management of the partnership.

d. A partner may assign his or her interest in the partnership only if the other two agree.

2. Which of the following is true concerning the rights of shareholders?

a. Shareholders have the right to receive dividends when the corporation makes a profit.

b. Shareholders have the right to manage the corporation.

c. Shareholders have no right to inspect the books and records of the corporation.

d. Shareholders can vote by proxy when they have voting rights.

3. Rhodes Corp. desired to acquire the common stock of Harris Corp. and engaged Johnson & Co., CPAs, to audit the financial statements of Harris Corp. Johnson failed to discover a significant liability in performing the audit. In a common law action against Johnson, Rhodes at a minimum must prove

a. Gross negligence on the part of Johnson.

b. Negligence on the part of Johnson.

c. Fraud on the part of Johnson.

d. Johnson knew that the liability existed.

4. A debtor will be denied a discharge in bankruptcy if the debtor

a. Failed to timely list a portion of his debts.

b. Unjustifiably failed to preserve his books and records which could have been used to ascertain the debtor’s financial condition.

c. Has negligently made preferential transfers to favored creditors within ninety days of the filing of the bankruptcy petition.

d. Has committed several willful and malicious acts that resulted in bodily injury to others.

5. Which of the following is a part of the social security law?

a. A self-employed person must contribute an annual amount that is equal to the combined contributions of an employee and his or her employer.

b. Upon the death of an employee prior to his retirement, his estate is entitled to receive the amount attributable to his contributions as a death benefit.

c. Social security benefits must be fully funded and payments, current and future, must constitutionally come only from social security taxes.

d. Social security benefits are taxable as income when they exceed the individual’s total contributions.

6. Duval Manufacturing Industries, Inc. orally engaged Harris as one of its district sales managers for an eighteen-month period commencing April 1, 2009. Harris commenced work on that date and performed his duties in a highly competent manner for several months. On October 1, 2009, the company gave Harris a notice of termination as of November 1, 2009, citing a downturn in the market for its products. Harris sues seeking either specific performance or damages for breach of contract. Duval pleads the Statute of Frauds and/or a justified dismissal due to the economic situation. What is the probable outcome of the lawsuit?

a. Harris will prevail because he has partially performed under the terms of the contract.

b. Harris will lose because his termination was caused by economic factors beyond Duval’s control.

c. Harris will lose because such a contract must be in writing and signed by a proper agent of Duval.

d. Harris will prevail because the Statute of Frauds does not apply to contracts such as his.

7. Kent, a wholesale distributor of cameras, entered into a contract with Williams. Williams agreed to purchase 100 cameras with certain optional attachments. The contract was made on March 1, 2009, for delivery by March 15, 2009; terms: 2/10, net 30. Kent shipped the cameras on March 6, and they were delivered on March 10. The shipment did not conform to the contract, in that one of the attachments was not included. Williams immediately notified Kent that he was rejecting the goods. For maximum legal advantage Kent’s most appropriate action is to

a. Bring an action for the price less an allowance for the missing attachment.

b. Notify Williams promptly of his intention to cure the defect and make a conforming delivery by March 15.

c. Terminate his contract with Williams and recover for breach of contract.

d. Sue Williams for specific performance.

8. Wilmont owned a tract of waterfront property on Big Lake. During Wilmont’s ownership of the land, several frame bungalows were placed on the land by tenants who rented the land from Wilmont. In addition to paying rent, the tenants paid for the maintenance and insurance of the bungalows, repaired, altered and sold them, without permission or hindrance from Wilmont. The bungalows rested on surface cinderblock and were not bolted to the ground. The buildings could be removed without injury to either the buildings or the land. Wilmont sold the land to Marsh. The deed to Marsh recited that Wilmont sold the land, with buildings thereon, “subject to the rights of tenants, if any, . . .” When the tenants attempted to remove the bungalows, Marsh claimed ownership of them. In deciding who owns the bungalows, which of the following is least significant?

a. The leasehold agreement itself, to the extent it manifested the intent of the parties.

b. The mode and degree of annexation of the buildings to the land.

c. The degree to which removal would cause injury to the buildings or the land.

d. The fact that the deed included a general clause relating to the buildings.

9. Tremont Enterprises, Inc. needed some additional working capital to develop a new product line. It decided to obtain intermediate term financing by giving a second mortgage on its plant and warehouse. Which of the following is true with respect to the mortgages?

a. If Tremont defaults on both mortgages and a bankruptcy proceeding is initiated, the second mortgagee has the status of general creditor.

b. If the second mortgagee proceeds to foreclose on its mortgage, the first mortgagee must be satisfied completely before the second mortgagee is entitled to repayment.

c. Default on payment to the second mortgagee will constitute default on the first mortgage.

d. Tremont cannot prepay the second mortgage prior to its maturity without the consent of the first mortgagee.

10. Frank Lanier is a resident of a state that imposes a tax on income. The following information pertaining to Lanier’s state income taxes is available:

| Taxes withheld in 2013 | $3,500 |

| Refund received in 2013 of 2012 tax | 400 |

| Deficiency assessed and paid in 2013 for 2011: | |

| Tax | 600 |

| Interest | 100 |

What amount should Lanier utilize as state and local income taxes in calculating itemized deductions for his 2013 federal tax return?

a. $3,500

b. $3,700

c. $4,100

d. $4,200

11. Ace Rentals, Inc., an accrual-basis taxpayer, reported rent receivable of $35,000 and $25,000 in its 2013 and 2012 balance sheets, respectively. During 2013, Ace received $50,000 in rent payments and $5,000 in nonrefundable rent deposits. In Ace’s 2013 corporate income tax return, what amount should Ace include as rent revenue?

a. $50,000

b. $55,000

c. $60,000

d. $65,000

12. Sol and Julia Crane (both age 41) are married, and filed a joint return for 2013. Sol earned a salary of $125,000 in 2013 from his job at Troy Corp., where Sol is covered by his employer’s pension plan. In addition, Sol and Julia earned interest of $3,000 in 2013 on their joint savings account. Julia is not employed, and the couple had no other income. On January 15, 2013, Sol contributed $4,000 to an IRA for himself, and $4,000 to an IRA for his spouse. The allowable IRA deduction in the Cranes’ 2013 joint return is

a. $0

b. $5,000

c. $6,000

d. $10,000

13. Spencer, who itemizes deductions, had adjusted gross income of $60,000 in 2013. The following additional information is available for 2013:

| Cash contribution to church | $4,000 |

| Purchase of art object at church bazaar (with a fair market value of $800 on the date of purchase) | 1,200 |

| Donation of used clothing to Salvation Army (fair value evidenced by receipt received) | 600 |

What is the maximum amount Spencer can claim as a deduction for charitable contributions in 2013?

a. $5,400

b. $5,200

c. $5,000

d. $4,400

14. The following information pertains to Wald Corp.’s operations for the year ended December 31, 2013:

| Worldwide taxable income | $300,000 |

| US source taxable income | 180,000 |

| US income tax before foreign tax credit | 96,000 |

| Foreign nonbusiness-related interest earned | 30,000 |

| Foreign income taxes paid on nonbusiness-related interest earned | 12,000 |

| Other foreign source taxable income | 90,000 |

| Foreign income taxes paid on other foreign source taxable income | 27,000 |

What amount of foreign tax credit may Wald claim for 2013?

a. $28,800

b. $36,600

c. $38,400

d. $39,000

15. Platt owns land that is operated as a parking lot. A shed was erected on the lot for the related transactions with customers. With regard to capital assets and Section 1231 assets, how should these assets be classified?

| Land | Shed | |

| a. | Capital | Capital |

| b. | Section 1231 | Capital |

| c. | Capital | Section 1231 |

| d. | Section 1231 | Section 1231 |

16. At partnership inception, Black acquires a 50% interest in Decorators Partnership by contributing property with an adjusted basis of $80,000. Black recognizes a gain if

I. The fair market value of the contributed property exceeds its adjusted basis.

II. The property is encumbered by a mortgage with a balance of $100,000.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

Items 17 and 18 are based on the following data:

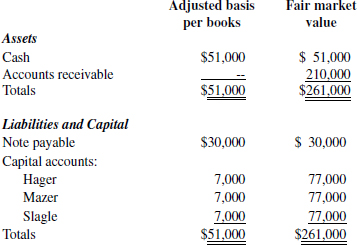

The partnership of Hager, Mazer & Slagle had the following cash-basis balance sheet at December 31, 2013:

Slagle, an equal partner, sold his partnership interest to Burns, an outsider, for $77,000 cash on January 1, 2014. In addition, Burns assumed Slagle’s share of partnership liabilities.

17. What was the total amount realized by Slagle on the sale of his partnership interest?

a. $67,000

b. $70,000

c. $77,000

d. $87,000

18. How much ordinary income should Slagle report in his 2014 income tax return on the sale of his partnership interest?

a. $0

b. $10,000

c. $70,000

d. $77,000

19. Eastern Corp., a calendar-year corporation, was formed in 2012. On January 2, 2013, it placed five-year property in service. The property was depreciated under the general MACRS system. Eastern did not elect to use the straight-line method. The following information pertains to Eastern:

| Eastern’s 2013 taxable income | $300,000 |

| Adjustment for the accelerated depreciation taken on 2013 five-year property | 1,000 |

| 2013 tax-exempt interest from specified private activity bonds issued in 2007 | 5,000 |

What was Eastern’s 2013 alternative minimum taxable income before the adjusted current earnings (ACE) adjustment?

a. $306,000

b. $305,000

c. $304,000

d. $301,000

20. Bank Corp. owns 80% of Shore Corp.’s outstanding capital stock. Shore’s capital stock consists of 50,000 shares of common stock issued and outstanding. Shore’s 2013 net income was $140,000. During 2013, Shore declared and paid dividends of $60,000. In conformity with generally accepted accounting principles, Bank recorded the following entries in 2013:

| Debit | Credit | |

| Investment in Shore Corp. common stock | $112,000 | |

| Equity in earnings of subsidiary | $112,000 | |

| Cash | 48,000 | |

| Investment in Shore Corp. common stock | 48,000 |

In its 2013 consolidated tax return, Bank should report dividend revenue of

a. $48,000

b. $14,400

c. $ 9,600

d. $0

21. Kari Corp., a manufacturing company, was organized on January 2, 2013. Its 2013 federal taxable income was $400,000 and its federal income tax was $100,000. What is the maximum amount of accumulated taxable income that may be subject to the accumulated earnings tax for 2013 if Kari takes only the minimum accumulated earnings credit?

a. $300,000

b. $150,000

c. $ 50,000

d. $0

22. On February 10, 2013, Ace Corp., a calendar-year corporation, elected S corporation status and all shareholders consented to the election. There was no change in shareholders in 2013. Ace met all eligibility requirements for S status during the pre-election portion of the year. What is the earliest date on which Ace can be recognized as an S corporation?

a. February 10, 2013.

b. February 10, 2014.

c. January 1, 2013.

d. January 1, 2014.

23. Lyon, a cash-basis taxpayer, died on January 15, 2013. In 2013, the estate executor made the required periodic distribution of $9,000 from estate income to Lyon’s sole heir. The following pertains to the estate’s income and disbursements in 2013:

2013 Estate Income |

|

$20,000 |

Taxable interest |

10,000 |

Net long-term capital gains allocable to corpus |

2013 Estate Disbursements |

|

$5,000 |

Administrative expenses attributable to taxable income |

For the 2013 calendar year, what was the estate’s distributable net income (DNI)?

a. $15,000

b. $20,000

c. $25,000

d. $30,000

24. A tax return preparer may disclose or use tax return information without the taxpayer’s consent to

a. Facilitate a supplier’s or lender’s credit evaluation of the taxpayer.

b. Accommodate the request of a financial institution that needs to determine the amount of taxpayer’s debt to it, to be forgiven.

c. Be evaluated by a quality or peer review.

d. Solicit additional nontax business.

Hints for Testlet 2

1. Partners have many rights in a partnership unless they give up those rights.

2. Shareholders may assign their voting rights.

3. Rhodes Corp. is the client, not Harris Corp.

4. Preferential transfers will simply be set aside.

5. There is no other party to split the payments with.

6. The agreement cannot be performed within one year.

7. Kent is subject to the perfect tender rule.

8. Recall factors determining whether item is a fixture.

9. First mortgage has priority.

10. Include amounts withheld or actually paid during the year.

11. Try setting up a “T” account and analyzing the journal entries that would have been made.

12. The deduction is subject to a special phase-out since Sol (but not Julia) is a participant in a qualified employer retirement plan.

13. The amount of contribution includes the excess of the amount paid over the value of the object received.

14. A separate FTC limitation applies to non-business-related interest.

15. The definition of capital assets excludes property used in a trade or business.

16. Generally no gain is recognized when property is transferred in exchange for a partnership interest.

17. The amount realized includes the buyer’s assumption of the seller’s share of partnership liabilities.

18. Ordinary income must be reported to the extent of the seller’s share of unrealized receivables and appreciated inventory.

19. The 150% declining balance method of depreciation must be used for AMT purposes.

20. Intercompany dividends from affiliated group members are eliminated in the consolidation process.

21. The minimum accumulated earnings credit is $250,000 for non service corporations.

22. An election is generally effective at the beginning of a corporation’s tax year.

23. The computation of DNI excludes capital gains allocable to corpus.

24. Only one answer choice merits disclosure.

Answers to Testlet 2

Explanations

1. (c) In a general partnership all general partners have a right to participate in management.

2. (d) Shareholders have the right to vote by proxy at shareholder meetings. The other items are not rights and would require action by the board of directors.

3. (b) Since Rhodes engaged Johnson, Rhodes is the client and in privity of contract. Therefore, Johnson could be held liable for ordinary negligence.

4. (b) Failing to keep books of account or records will bar the discharge of all debts.

5. (a) A self-employed individual must pay both halves of the required contribution.

6. (c) Agreements that cannot be performed within one year from the date of the agreement must be in writing to be enforceable under the Statute of Fraud.

7. (b) To get maximum legal advantage, the buyer must notify the seller of rejection of the goods on a timely basis.

8. (d) A general clause in the deed would have the least significance.

9. (b) The first mortgage has priority before repayment of any portion of the second mortgage.

10. (c) The taxes paid in 2013 are equal to $4,100 ($3,500 withheld and $600 for deficiency). The refund is included in income and the interest is not deductible.

11. (d) The amount of rent revenue is equal to $65,000 ($50,000 received − $25,000 beginning receivable + $35,000 ending receivable + $5,000 nonrefundable deposits).

12. (b) Julia’s $5,000 contribution is allowable but Sol’s is not because he is a participant in a pension plan and their combined compensation is greater than $115,000.

13. (c) The maximum is $5,000 ($4,000 cash contribution + $400 excess of purchase price over fair value of art object + $600 clothing contribution).

14. (b) The amount of credit that can be currently used cannot exceed the amount of US tax that is attributable to the foreign income. This foreign tax credit limitation can be expressed as follows:

One limitation must be computed for foreign source passive income (e.g., interest, dividends, royalties, rents, annuities), with a separate limitation computed for all other foreign source taxable income.

In this case, the foreign income taxes paid on other foreign source taxable income of $27,000 is fully usable as a credit in 2013 because it is less than the applicable limitation amount (i.e., the amount of US tax attributable to the income).

On the other hand, the credit for the $12,000 of foreign income taxes paid on non-business-related interest is limited to the amount of US tax attributable to the foreign interest income, $9,600.

Thus, Wald Corp.’s foreign tax credit for 2013 totals $27,000 + $9,600 = $36,600. The $12,000 − $9,600 = $2,400 of unused foreign tax credit resulting from the application of the limitation of foreign taxes attributable to foreign source interest income can be carried back one year and forward ten years to offset US income tax in those years.

15. (d) Both of the assets are Section 1231 property.

16. (d) No gain is recognized on the transfer. A gain would only be recognized if the decrease in the partner’s liability exceeds his or her partnership basis.

17. (d) The amount realized is $87,000 ($77,000 cash received + $10,000 liability assumed).

18. (c) The ordinary income would be equal to his share of the unrealized receivables or $70,000 ($210,000 × 1/3). The remainder would be capital gain.

19. (a) The amount of alternative minimum taxable income before ACE adjustment is equal to $306,000 ($300,000 taxable income + $5,000 tax-exempt private activity bond interest + $1,000 excess depreciation).

20. (d) On the consolidated tax return intercompany dividends are eliminated.

21. (c) The accumulated taxable income that may be subject to the accumulated earnings tax is $50,000 ($400,000 taxable income − $100,000 income tax − $250,000 accumulated earnings credit). The credit is equal to $250,000 ($250,000 − the accumulated earnings and profits at the end of the prior year which is $0).

22. (c) Since the election was filed on or before the fifteenth day of the third month of the year, it is effective as of the beginning of that year.

23. (a) DNI would be net income $25,000 ($20,000 + $10,000 − $5,000) minus $10,000 net capital gains allocable to corpus, which equals $15,000.

24. (c) The only allowed use of the information is if the preparer is being evaluated under a quality or peer review.

Testlet 3

1. Which of the following is (are) included in the Articles of Incorporation when a corporation is formed?

a. The number of authorized shares of stock.

b. The name of the registered agent of the corporation.

c. The names and addresses of the incorporators.

d. All of the above.

2. Which of the following is (are) true under the Americans with Disabilities Act?

I. The Act requires companies to make reasonable accommodations for disabled persons unless this results in undue hardship on the operations of the company.

II. The Act requires that companies with 100 or more employees set up a plan to hire Americans with disabilities.

a. Both I and II.

b. Neither I nor II.

c. I only.

d. II only.

3. The partnership of Maxim & Rose, CPAs, has been engaged by their largest client, a limited partnership, to examine the financial statements in connection with the offering of 2,000 limited-partnership interests to the public at $5,000 per subscription. Under these circumstances, which of the following is true?

a. Maxim & Rose may disclaim any liability under the Federal Securities Acts by an unambiguous, boldfaced disclaimer of liability on its audit report.

b. Under the Securities Act of 1933, Maxim & Rose has responsibility only for the financial statements as of the close of the fiscal year in question.

c. The dollar amount in question is sufficiently small so as to provide an exemption from the Securities Act of 1933.

d. The Securities Act of 1933 requires a registration despite the fact that the client is not selling stock or another traditional “security.”

4. One of the major purposes of federal security regulation is to

a. Establish the qualifications for accountants who are members of the profession.

b. Eliminate incompetent attorneys and accountants who participate in the registration of securities to be offered to the public.

c. Provide a set of uniform standards and tests for accountants, attorneys, and others who practice before the Securities and Exchange Commission.

d. Provide sufficient information to the investing public who purchases securities in the marketplace.

5. Which of the following statements is (are) true of the National Environment Policy Act?

I. The Act provides tax breaks for those companies that help accomplish national environmental policy.

II. Enforcement of the Act is primarily accomplished by litigation of persons who decide to challenge federal government decisions.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

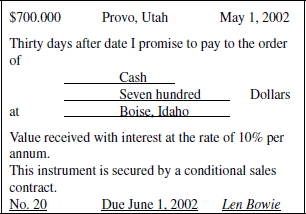

6. Your client has in its possession the following instrument:

This instrument is

a. A negotiable time draft.

b. A nonnegotiable note since it states that it is secured by a conditional sales contract.

c. Not negotiable until June 1, 2002.

d. A negotiable bearer note.

7. In which of the following situations would an oral agreement without any consideration be binding under the Uniform Commercial Code?

a. A renunciation of a claim or right arising out of an alleged breach.

b. A firm offer by a merchant to sell or buy goods which gives assurance that it will be held open.

c. An agreement that is a requirements contract.

d. An agreement that modifies an existing sales contract.

8. A dispute has arisen between two merchants over the question of who has the risk of loss in a given sales transaction. The contract does not specifically cover the point. The goods were shipped to the buyer who rightfully rejected them. Which of the following factors will be the most important factor in resolving their dispute?

a. Who has title to the goods.

b. The shipping terms.

c. The credit terms.

d. The fact that a breach has occurred.

9. Moch sold her farm to Watkins and took back a purchase money mortgage on the farm. Moch failed to record the mortgage. Moch’s mortgage will be valid against all of the following parties except

a. The heirs or estate of Watkins.

b. A subsequent mortgagee who took a second mortgage since he had heard there was a prior mortgage.

c. A subsequent bona fide purchaser from Watkins.

d. A friend of Watkins to whom the farm was given as a gift and who took without knowledge of the mortgage.

10. For the year ended December 31, 2013, Don Raff earned $1,000 interest at Ridge Savings Bank on a certificate of deposit scheduled to mature in 2014. In January 2014, before filing his 2013 income tax return, Raff incurred a forfeiture penalty of $500 for premature withdrawal of the funds. Raff should treat this $500 forfeiture penalty as a

a. Reduction of interest earned in 2013, so that only $500 of such interest is taxable on Raff’s 2013 return.

b. Deduction from 2014 adjusted gross income, deductible only if Raff itemizes his deductions for 2014.

c. Penalty not deductible for tax purposes.

d. Deduction from gross income in arriving at 2014 adjusted gross income.

11. Axis Corp. is an accrual-basis calendar-year corporation. On December 13, 2013, the Board of Directors declared a 2% of profits bonus to all employees for services rendered during 2013 and notified them in writing. None of the employees own stock in Axis. The amount represents reasonable compensation for services rendered and was paid on March 13, 2014. Axis’ bonus expense may

a. Not be deducted on Axis’ 2013 tax return because the per share employee amount cannot be determined with reasonable accuracy at the time of the declaration of the bonus.

b. Be deducted on Axis’ 2013 tax return.

c. Be deducted on Axis’ 2014 tax return.

d. Not be deducted on Axis’ tax return because payment is a disguised dividend.

12. On August 1, 2013, Graham purchased and placed into service an office building costing $264,000 including $30,000 for the land. What was Graham’s MACRS deduction for the office building in 2013?

a. $9,600

b. $6,000

c. $3,600

d. $2,250

13. This item is based on the following selected 2013 information pertaining to Sam and Ann Hoyt, who filed a joint federal income tax return for the calendar year 2013. The Hoyts had adjusted gross income of $34,000 and itemized their deductions for 2013. Among the Hoyts’ cash expenditures during 2013 were the following:

- $2,500 repairs in connection with 2013 fire damage to the Hoyt residence. This property has a basis of $50,000. Fair market value was $60,000 before the fire and $55,000 after the fire. Insurance on the property had lapsed in 2012 for nonpayment of premium.

- $800 appraisal fee to determine amount of fire loss.

What amount of fire loss were the Hoyts entitled to deduct as an itemized deduction on their 2013 return?

a. $5,000

b. $2,500

c. $1,500

d. $1,100

14. A calendar-year taxpayer filed an individual tax return for 2012 on March 20, 2013. The taxpayer neither committed fraud nor omitted amounts in excess of 25% of gross income on the tax return. What is the latest date that the Internal Revenue Service can assess tax and assert a notice of deficiency?

a. March 20, 2016.

b. March 20, 2015.

c. April 15, 2016.

d. April 15, 2015.

15. On July 1, 2013, Riley exchanged investment real property, with an adjusted basis of $160,000 and subject to a mortgage of $70,000, and received from Wilson $30,000 cash and other investment real property having a fair market value of $250,000. Wilson assumed the mortgage. What is Riley’s recognized gain in 2013 on the exchange?

a. $ 30,000

b. $ 70,000

c. $ 90,000

d. $100,000

16. In 2011, Martha received as a gift several shares of Good Corporation stock. The donor’s basis of this stock was $2,800, and he paid gift tax of $50. On the date of the gift, the fair market value of the stock was $2,600. If Martha sells this stock in 2013 for $2,700, what amount and type of gain or loss should Martha report in her 2013 income tax return?

a. $50 long-term capital gain.

b. $100 long-term capital gain.

c. $100 long-term capital loss.

d. No gain or loss.

17. Hall and Haig are equal partners in the firm of Arosa Associates. On January 1, 2013, each partner’s adjusted basis in Arosa was $40,000. During 2013 Arosa borrowed $60,000, for which Hall and Haig are personally liable. Arosa sustained an operating loss of $10,000 for the year ended December 31, 2013. The basis of each partner’s interest in Arosa at December 31, 2013, was

a. $35,000

b. $40,000

c. $65,000

d. $70,000

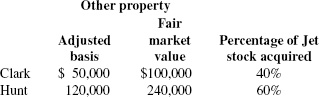

18. Clark and Hunt organized Jet Corp. with authorized voting common stock of $400,000. Clark contributed $60,000 cash. Both Clark and Hunt transferred other property in exchange for Jet stock as follows:

What was Clark’s basis in Jet stock?

a. $0

b. $100,000

c. $110,000

d. $160,000

19. Roberta Warner and Sally Rogers formed the Acme Corporation on October 1, 2013. On the same date Warner paid $75,000 cash to Acme for 750 shares of its common stock. Simultaneously, Rogers received 100 shares of Acme’s common stock for services rendered. How much should Rogers include as taxable income for 2013 and what will be the basis of her stock?

| Taxable income | Basis of stock | |

| a. | $0 | $0 |

| b. | $0 | $10,000 |

| c. | $10,000 | $0 |

| d. | $10,000 | $10,000 |

20. The following information pertains to Hull, Inc., a personal holding company, for the year ended December 31, 2013:

| Undistributed personal holding company income | $100,000 |

| Dividends paid during 2013 | 20,000 |

| Consent dividends reported in the 2013 individual income tax returns of the holders of Hull’s common stock, but not paid by Hull to its stockholders | 10,000 |

In computing its 2013 personal holding company tax, what amount should Hull deduct for dividends paid?

a. $0

b. $10,000

c. $20,000

d. $30,000

21. Bern Corp., an S corporation, had an ordinary loss of $36,500 for the year ended December 31, 2013. At January 1, 2013, Meyer owned 50% of Bern’s stock. Meyer held the stock for forty days in 2013 before selling the entire 50% interest to an unrelated third party. Meyer’s basis for the stock was $10,000. Meyer was a full-time employee of Bern until the stock was sold. Meyer’s share of Bern’s 2013 loss was

a. $0

b. $ 2,000

c. $10,000

d. $18,300

22. On July 1, 2013, in connection with a recapitalization of Yorktown Corporation, Robert Moore exchanged 1,000 shares of stock that cost him $95,000 for 1,000 shares of new stock worth $108,000 and bonds in the principal amount of $10,000 with a fair market value of $10,500. What is the amount of Moore’s recognized gain during 2013?

a. $0

b. $10,500

c. $23,000

d. $23,500

23. Steve and Kay Briar, US citizens, were married for the entire 2013 calendar year. In 2013, Steve gave a $32,000 cash gift to his sister. The Briars made no other gifts in 2013. They each signed a timely election to treat the $30,000 gift as made one-half by each spouse. Disregarding the unified credit and estate tax consequences, what amount of the 2013 gift is taxable to the Briars?

a. $18,000

b. $ 6,000

c. $ 4,000

d. $0

24. Following are the fair market values of Wald’s assets at the date of death:

| Personal effects and jewelry | $1,400,000 |

| Land bought by Wald with Wald’s funds five years prior to death and held with Wald’s sister as joint tenants with right of survivorship | 4,900,000 |

The executor of Wald’s estate did not elect the alternate valuation date. The amount includible as Wald’s gross estate in the federal estate tax return is

a. $1,400,000

b. $3,850,000

c. $4,900,000

d. $6,300,000

Hints for Testlet 3

1. The Articles of Incorporation contain much important information.

2. ADA applies to employers with at least fifteen employees; forbidding discrimination.

3. Must comply with all requirements of the 1933 Act.

4. The goal is to help investors avoid fraudulent offerings.

5. The EPA ensures compliance with environmental protection laws.

6. A note is a two-party instrument.

7. Review Module 24, Section A.2.d.

8. Risk of loss is independent of title under UCC.

9. To prevail, subsequent party must give value and must not have notice.

10. The interest forfeiture results in a deduction.

11. The amount must be fixed by a predetermined formula.

12. Remember to use the midmonth averaging convention.

13. Remember to subtract a $100 floor and 10% of AGI.

14. A return filed early is treated as filed on its due date for statute of limitations purposes.

15. The assumption of Riley’s mortgage is treated as boot received.

16. The basis for gain is $2,800, and the basis for loss is $2,600.

17. An increase in partnership liabilities is treated as a deemed cash contribution.

18. Clark’s basis must reflect his non recognition of gain.

19. The shares received as compensation are worth $100 per share.

20. Consent dividends are included as part of the corporation’s dividends paid deduction.

21. S corporation items are allocated per share, per day to shareholders.

22. The definition of boot (other property) includes the FMV of an excess principal amount of security received.

23. The gift is treated as made one-half by each spouse.

24. In the case of jointly held property by other than spouses, the property is included in the gross estate except to the extent that the surviving tenant contributed toward the purchase.

Answers to Testlet 3

Explanations

1. (d) The Articles of Incorporation include the number of authorized shares of stock, the name of the registered agent, and the names and addresses of the incorporators, among other information.

2. (c) The Americans with Disabilities Act requires companies to make reasonable accommodations for disabled persons. It also prohibits discrimination but does not require setting up plans to hire disabled persons.

3. (d) The Securities Act of 1933 covers sales of limited-partnership interests to the public.

4. (d) One of the major purposes of federal security regulation is to assure full and fair disclosure of information to the investing public.

5. (b) The National Environment Policy Act enforcement is primarily accomplished by litigation of persons who decide to challenge federal government decisions.

6. (d) The instrument is a negotiable bearer note because it is payable to the bearer (cash), unconditional, payable on a fixed date, and specifies a certain amount of cash.

7. (d) The only oral agreement that would be binding without consideration would be an agreement that modifies an existing sales contract.

8. (d) Risk of loss transfers when title passes unless there is a breach of contract.

9. (c) A subsequent bona fide purchaser would take the property over a previous mortgage holder who fails to record.

10. (d) The penalty may be deducted from gross income in arriving at 2014 adjusted gross income.

11. (b) The bonuses are deductible provided that they are paid within 21/2 months of the close of the tax year.

12. (d) The depreciation allowed is $2,250 ($234,000 × 4.5 × 468 months). Notice that the midmonth convention is used.

13. (c) The casualty loss is equal to $5,000 ($60,000 FMV before the casualty − $55,000 FMV after the casualty). The deductible loss is equal to $1,500 ($5,000 loss − $100 floor − $3,400 [10% of adjusted gross income]).

14. (c) The normal period for assessment of a tax deficiency is three years after the date of the return or three years after the return is filed, whichever is later.

15. (d) The gain is equal to $100,000, which is the amount of boot received in the like-kind exchange. The boot is equal to the $30,000 cash received plus the $70,000 liability assumed.

16. (d) Martha’s basis for a gain is the basis of the donor increased by any gift tax paid, or $2,850. The basis for a loss is the lesser of gain basis ($2,850) or the FMV on the date of gift ($2,600). Therefore, no gain or loss is recognized.

17. (c) The basis of each partner’s interest was $65,000 ($40,000 January 1 basis + $30,000 share of liability − $5,000 share of loss).

18. (c) Clark’s basis is equal to $110,000 ($60,000 cash + $50,000 adjusted basis of property contributed).

19. (d) Rogers must include the FMV of the stock at the date of receipt in his taxable income. The basis of the investment in the stock also is the FMV of the stock at date of receipt.

20. (d) The corporation may deduct both regular and consent dividends.

21. (b) The amount of ordinary loss is $2,000 [$36,500 × 50% × (40 days/365 days)].

22. (b) The FMV of the bonds represents boot in the reorganization. Therefore, the recognized gain is $10,500.

23. (c) The amount taxable is $4,000 ($32,000 − $28,000 [two annual exclusions of $14,000 each]).

24. (d) The gross estate is equal to $6,300,000. The entire FMV of the land is included because it is held in joint tenancy and acquired by purchase by other than spouses.

Testlet 4

Task-Based Simulation 1

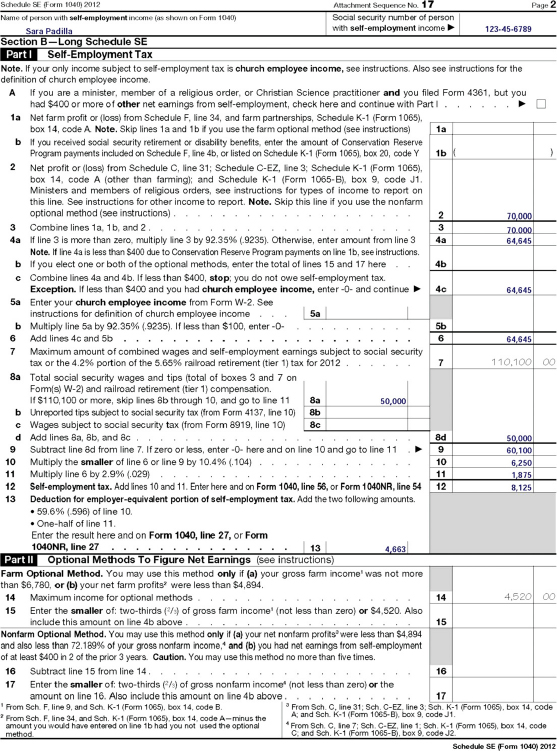

Sara Padilla (social security #123-45-6789) works as a financial consultant and had a net profit from her sole proprietorship reported on Schedule C, line 31, of $70,000 for 2012. Sara also worked a second job as an employee and had social security wages of $50,000 for 2012.

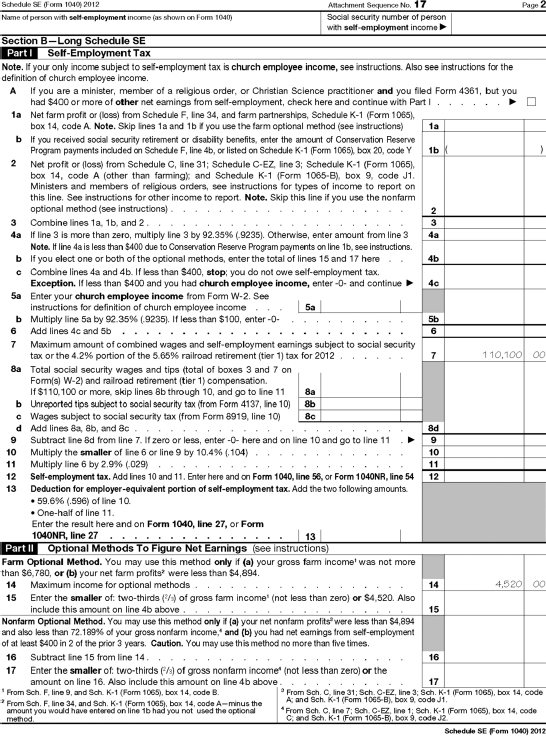

Complete the following 2012 Form 1040 Schedule SE to compute Sara’s self-employment tax and her self-employment tax deduction.

Task-Based Simulation 2

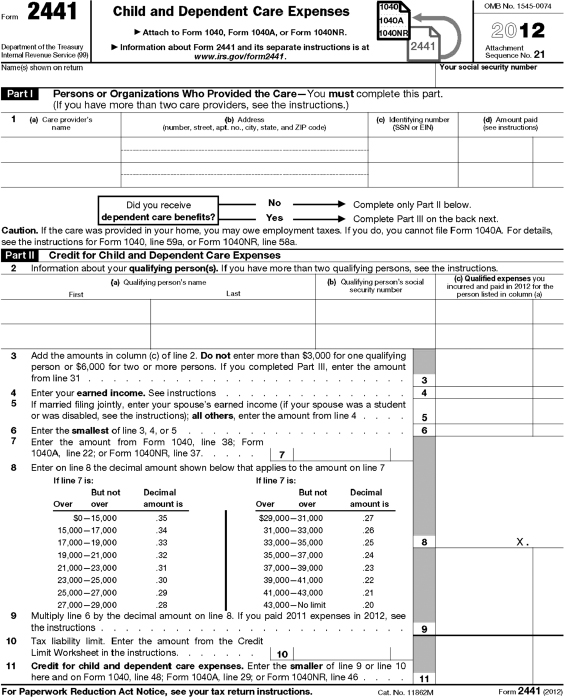

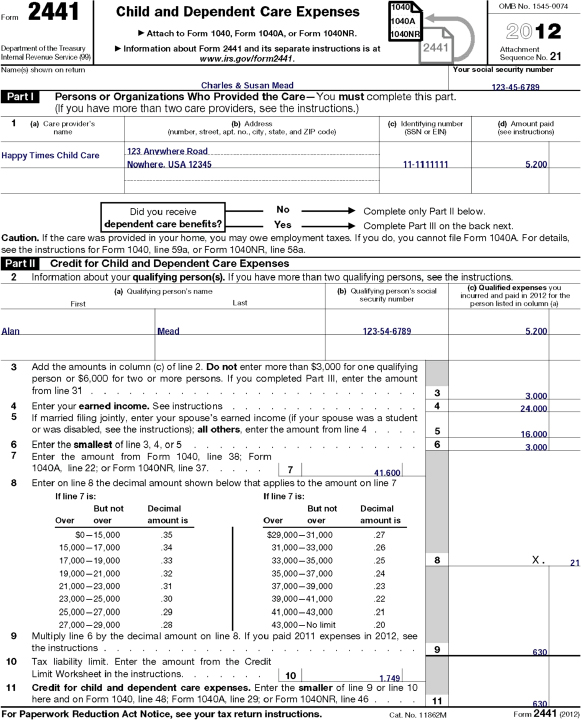

Charles (social security #123-45-6789) and Susan Mead were married and gainfully employed throughout 2012. Charles earned $24,000 and Susan earned $16,000 in wages during the year. The couple have a son, Alan (social security #123-54-6789), who is sent to an after-school child care center (Happy Times Child Care, 123 Anywhere Road, Nowhere, USA 12345, EIN #11-1111111) to enable the Meads to work. The Meads paid Happy Times $5,200 during the year for the care of Alan, but did not receive any employer-provided dependent care benefits. The Meads’ adjusted gross income reported on Form 1040, line 38, was $41,600 for 2012, while their tax before credits shown on the Meads’ Form 1040, line 46, was $1,749. The Meads had no foreign tax credit on Form 1040, line 47.

Complete the following Form 2441 to determine the Meads’ available credit for child and dependent care expenses for 2012.

Task-Based Simulation 3

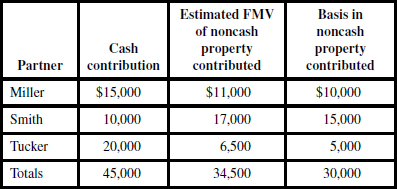

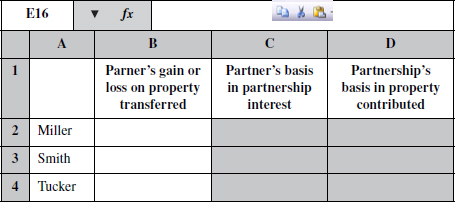

Miller, Smith, and Tucker decided to form a partnership to perform engineering services. All of the partners have extensive experience in the engineering field and now wish to pool their resources and client contacts to begin their own firm. The new entity, Sabre Consulting, will begin operations on April 1, 2013, and will use the calendar year for reporting purposes.

All of the partners expect to work full time for Sabre and each will contribute cash and other property to the company sufficient to commence operations. The partners have agreed to share all income and losses of the partnership equally. A written partnership agreement, duly executed by the partners, memorializes this agreement among the partners.

The table below shows the estimated values for assets contributed to Sabre by each partner. None of the contributed assets’ costs have been previously recovered for tax purposes.

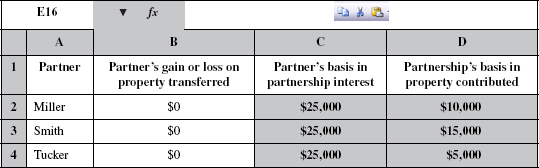

Complete the shaded cells in the following table by entering the gain or loss recognized by each partner on the property contributed to Sabre Consulting, the partner’s basis in the partnership interest, and Sabre’s basis in the contributed property. Loss amounts should be recorded as a negative number.

Task-Based Simulation 4

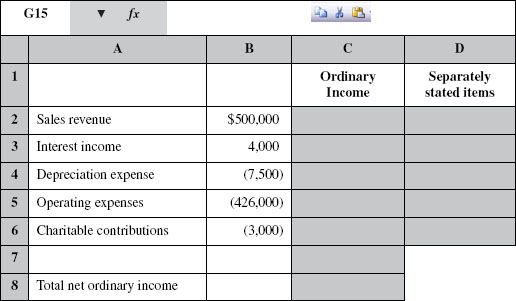

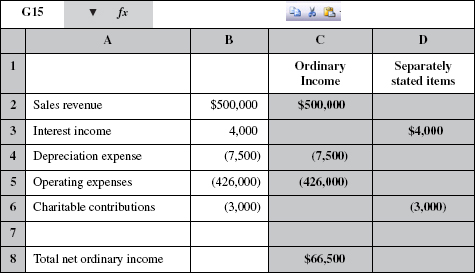

Assume that Wilson Partners (a general partnership) had only the items of income and expense show in the following table for the 2013 tax year. Complete the remainder of the table by properly classifying each item of income and expense as ordinary business income that is reportable on page 1, Form 1065, or as a separately stated item that is reportable on Schedule K, Form 1065. Some entries may appear in both columns.

Task-Based Simulation 5

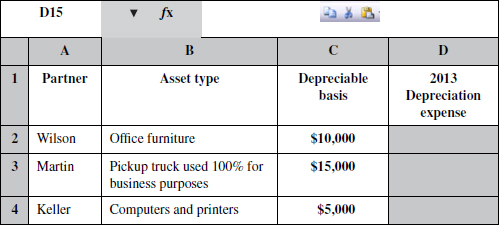

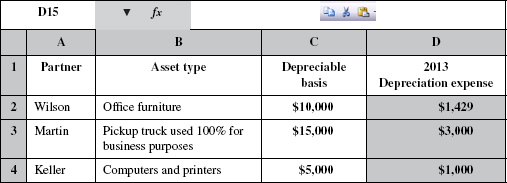

Wilson, Martin, and Keller form a general partnership, Express Supply Company, and each partner contributed property as described below. Using the MACRS table (which can be found by clicking the Resources tab), complete the following table to determine Express Supply’s tax depreciation expense for 2013. Assume that none of the original cost of any asset was expensed by the partnership under the provisions of Section 179, and that the partnership elected not to take bonus depreciation.

Task-Based Simulation 6

The credit for expenses for household and dependent care services necessary for gainful employment is allowed for expenses incurred for qualifying individuals. What Internal Revenue Code section and subsection defines a “qualified individual” for purposes of the child and dependent care credit?

Indicate the reference to that citation in the shaded boxes below.

Solutions to Testlet 4

Solution to Task-Based Simulation 1

Solution to Task-Based Simulation 2

Solution to Task-Based Simulation 3

Generally, no gain or loss is recognized on the contribution of property in exchange for a partnership interest. As a result, a partner’s initial basis for a partnership interest consists of the amount of cash plus the adjusted basis of noncash property contributed. Similarly, a partnership receives a transferred basis for contributed noncash property equal to the partner’s basis for the property prior to contribution. Miller’s initial partnership basis consists of the $15,000 cash plus the $10,000 adjusted basis of noncash property contributed, or $25,000. Smith’s partnership basis consists of the $10,000 cash plus the $15,000 basis of noncash property contributed, or $25,000. Tucker’s partnership basis consists of the $20,000 cash plus the $5,000 basis of noncash property contributed, or $25,000.

Solution to Task-Based Simulation 4

Partnership items having special tax characteristics (e.g., passive activity losses, deductions subject to dollar or percentage limitations, etc.) must be separately stated and shown on Schedules K and K-1 so that their special characteristics are preserved when reported on partners’ returns. In contrast, partnership ordinary income and deduction items having no special tax characteristics can be netted together in the computation of a partnership’s ordinary income and deductions from trade or business activities on page 1 of Form 1065. Here, assuming the $4,000 of interest income is from investments, it represents portfolio income and must be separately stated on Schedule K. Similarly, the charitable contributions of $3,000 must be separately stated so that the appropriate percentage limitations can be applied when passed through to partners. Sales, depreciation, and operating expenses are ordinary items and result in net ordinary income of $66,500.

Solution to Task-Based Simulation 5

The office furniture has a 7-year recovery period, while the pickup truck and computers and printers have a 5–year recovery period. The MACRS depreciation table that was provided is based on the 200% declining-balance method and already incorporates the half-year convention which permits just a half-year of depreciation for the year that depreciable personalty is placed in service. Thus, the 2013 depreciation expense for the office furniture is $10,000 × 14.29% = $1,429 (i.e., $10,000 × 2/7 × 1/2). The 2013 depreciation for the pickup truck is $15,000 × 20% = $3,000 (i.e., $15,000 × 2/5 × 1/2). The 2013 depreciation expense for the computers and printers is $5,000 × 20% = $1,000 (i.e., $5,000 × 2/5 × 1/2).

Solution to Task-Based Simulation 6

Internal Revenue Code Section 21, subsection (b), defines a qualifying individual for purposes of the child and dependent care credit.