CHAPTER 15

Calculation 9: Net Operating Income

What It Means

Net operating income (NOI) is a property’s income after being reduced by vacancy and credit loss and all operating expenses. Mathematically, it is a property’s gross operating income less the sum of all operating expenses.

NOI represents a property’s profitability before consideration of taxes, financing, or recovery of capital. Perhaps easier is to think of it as the number of dollars a property returns in a given year if the property is purchased for all cash and if there is no consideration of income taxes or depreciation.

NOI is one of the most important calculations you’ll make in regard to any real estate investment. If you revisit Part I, Chapters 2 through 5 of this book, you’ll notice that NOI is at the center of almost every discussion. It represents an essential component of many of the chapters in Part II as well.

In order to calculate NOI correctly, you must be clear about what is and what is not an operating expense. An operating expense is one that is necessary for the maintenance of a piece of real property and ensures its continued ability to produce income. Loan payments, depreciation, and capital expenditures are not considered operating expenses.

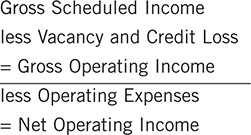

How to Calculate

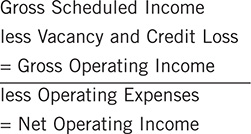

Net Operating Income = Gross Operating Income less Operating Expenses

You may prefer a “top-down” approach to this calculation, which is easier to visualize:

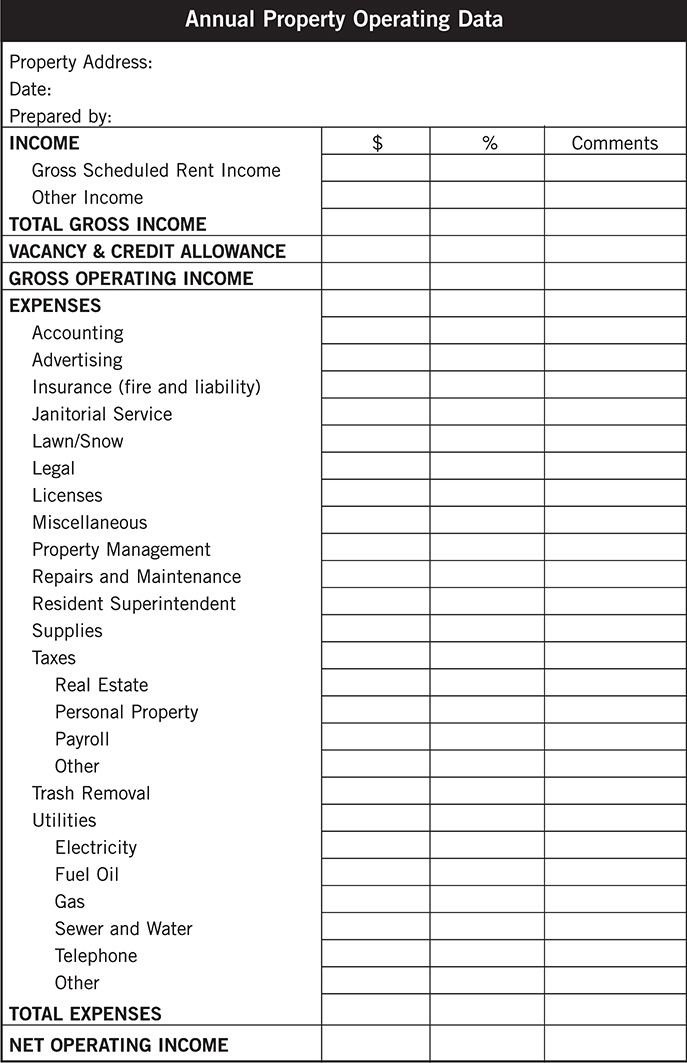

It is quite common to use an Annual Property Operating Data (APOD) form to simplify the computation of NOI. That form includes all of the most common line-item expenses. You saw it in Chapter 2, but because it is so useful to the calculation of NOI, we’ll repeat it on the following page for your convenience.

Example

You have a property with a scheduled gross income of $100,000, vacancy and credit loss of 3%, and total operating expenses of $35,000. What is this property’s net operating income?

Begin with the gross scheduled income and use that to calculate the dollar amount of the vacancy and credit loss:

Vacancy and Credit Loss = 100,000 × 0.03 = 3,000

Now you can calculate the GOI:

From this, subtract the operating expenses to determine the NOI:

Test Your Understanding

A seller presents you with the following information about a property:

Four units, all occupied; two rent for $1,000 per month, two rent for $1,200

per month

Property taxes, $4,800

Property insurance, $1,900

Water, $1,800

Sewer, $800

Repairs, $2,900

Advertising, $250

Supplies, $475

Lawn and Snow, $425

Depreciation, $2,900

Assume that you are able to confirm that these amounts are accurate.

Answer

Follow the top-down approach:

1. To calculate the annual gross scheduled income, first find the monthly income:

(2 × 1,000) + (2 × 1,200) = 2,000 + 2,400 = 4,400

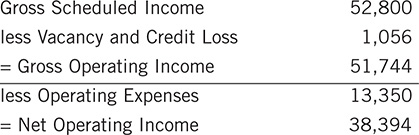

Multiply that by 12 to get the annual gross scheduled income of $52,800.

2. The seller has not volunteered any information about vacancy or credit loss other than to tell you that the property is now fully occupied. Use a nominal amount, 2%, as an allowance:

Vacancy and Credit Loss = 52,800 × 0.02 = 1,056

3. Sum the operating expenses. You’ve satisfied yourself that the figures the seller has given you are accurate. However, note that she included depreciation, which is not an operating expense. Add up all the others for a total of $13,350.