Now that we have an idea of designing a video game for creating a backtesting trading system, we can begin our object-oriented approach by first defining the required classes for the various components in our trading system.

We are interested in implementing a simple backtesting system to test a mean-reverting strategy. Using the daily historical prices from Google Finance, we will take the closing price of each day to compute the volatility of price returns for a particular stock, using the ticker symbol AAPL as an example. We want to test a theory that if the standard deviation of returns for an elapsed number of days is far from the mean of zero by a particular threshold, a buy or sell signal is generated. When such a signal is indeed generated, a market order is sent to the exchange to be executed at the opening price of the next trading day.

As soon as we open a position, we would like to track our unrealized and realized profits till date. Our open position can be closed when an opposing signal is generated. On completion of the backtest, we will plot our profits and losses to see how well our strategy holds.

Does our theory sound like a viable trading strategy? Well, let's find out! The following sections explain the classes that will be used for implementing a backtesting system.

The TickData class represents a single unit of data received from a market data source. In this example, we are interested in just the stock symbol, the timestamp of the data, the opening price, and the last price:

""" Store a single unit of data """

class TickData:

def __init__(self, symbol, timestamp,

last_price=0, total_volume=0):

self.symbol = symbol

self.timestamp = timestamp

self.open_price = 0

self.last_price = last_price

self.total_volume = total_volumeDetailed descriptions of a single unit of tick data, such as the total volume, bid price, ask price, or last volume can be added as our system evolves.

An instance of this class is used throughout the system to store and retrieve prices by the various components. Essentially, a container is used to store the last tick data. Additional helper functions are included to provide easy reference to the required information:

class MarketData:

def __init__(self):

self.__recent_ticks__ = dict()

def add_last_price(self, time, symbol, price, volume):

tick_data = TickData(symbol, time, price, volume)

self.__recent_ticks__[symbol] = tick_data

def add_open_price(self, time, symbol, price):

tick_data = self.get_existing_tick_data(symbol, time)

tick_data.open_price = price

def get_existing_tick_data(self, symbol, time):

if not symbol in self.__recent_ticks__:

tick_data = TickData(symbol, time)

self.__recent_ticks__[symbol] = tick_data

return self.__recent_ticks__[symbol]

def get_last_price(self, symbol):

return self.__recent_ticks__[symbol].last_price

def get_open_price(self, symbol):

return self.__recent_ticks__[symbol].open_price

def get_timestamp(self, symbol):

return self.__recent_ticks__[symbol].timestampThe

MarketDataSource class helps us fetch historical data from an external source, such as Google Finance or Yahoo! Finance. The required parameter values, such as start, end, ticker, and source are provided from the host component of this class, which we will discuss later. After saving the opening and closing prices of each day, the event_tick variable that represents a function handled by the host component will be invoked on every tick event. Notice that we are using the DataReader function of pandas to retrieve historical prices. The acceptable parameters are yahoo for Yahoo! Finance data source and google for Google Finance data source:

import pandas.io.data as web

""" Download prices from an external data source """

class MarketDataSource:

def __init__(self):

self.event_tick = None

self.ticker, self.source = None, None

self.start, self.end = None, None

self.md = MarketData()

def start_market_simulation(self):

data = web.DataReader(self.ticker, self.source,

self.start, self.end)

for time, row in data.iterrows():

self.md.add_last_price(time, self.ticker,

row["Close"], row["Volume"])

self.md.add_open_price(time, self.ticker, row["Open"])

if not self.event_tick is None:

self.event_tick(self.md)The

Order class represents a single order sent by the strategy to the server. Each order contains a timestamp, the symbol, quantity, price, and the size of the order. In this example, we are using market orders only. Other order types, such as limit and stop orders, can be further implemented if desired. Once an order is filled, the order is further updated with the filled time, quantity, and price:

class Order:

def __init__(self, timestamp, symbol, qty, is_buy,

is_market_order, price=0):

self.timestamp = timestamp

self.symbol = symbol

self.qty = qty

self.price = price

self.is_buy = is_buy

self.is_market_order = is_market_order

self.is_filled = False

self.filled_price = 0

self.filled_time = None

self.filled_qty = 0The

Position class helps us keep track of our current market position and account balance. Note that the position_value variable starts with a value of zero. When stocks are bought, the value of the securities is debited from this account. When stocks are sold, the value of the securities is credited into this account:

class Position:

def __init__(self):

self.symbol = None

self.buys, self.sells, self.net = 0, 0, 0

self.realized_pnl = 0

self.unrealized_pnl = 0

self.position_value = 0

def event_fill(self, timestamp, is_buy, qty, price):

if is_buy:

self.buys += qty

else:

self.sells += qty

self.net = self.buys - self.sells

changed_value = qty * price * (-1 if is_buy else 1)

self.position_value += changed_value

if self.net == 0:

self.realized_pnl = self.position_value

def update_unrealized_pnl(self, price):

if self.net == 0:

self.unrealized_pnl = 0

else:

self.unrealized_pnl = price * self.net +

self.position_value

return self.unrealized_pnlThe

Strategy class is the base class for all other strategy implementations. The event_tick method is called when new market tick data arrives. The event_order method is called whenever there are order updates. The event_position method is called whenever there are updates to our positions. The send_market_order method is called when the implementing strategy sends a market order to the host component to be routed to the server for execution:

""" Base strategy for implementation """

class Strategy:

def __init__(self):

self.event_sendorder = None

def event_tick(self, market_data):

pass

def event_order(self, order):

pass

def event_position(self, positions):

pass

def send_market_order(self, symbol, qty, is_buy, timestamp):

if not self.event_sendorder is None:

order = Order(timestamp, symbol, qty, is_buy, True)

self.event_sendorder(order)In this example, we are implementing a mean-reverting strategy with the MeanRevertingStrategy class that inherits the Strategy class. We will use the stock symbol AAPL.

The event_position method is overridden and updates the state of the strategy to indicate a long or a short on every change in position. Knowing the current state of the strategy prevents us from adding on to our positions and entering more orders than intended.

The event_tick method is overridden to perform the trade logic decision on every incoming tick data, which is stored as a pandas DataFrame object, to calculate the strategy parameters. The lookback_intervals variable defines a maximum of 20 days of historical prices to store.

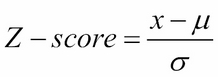

The calculate_z_score method implements our mean-reverting calculations. The daily percentage change of close prices over the previous day is computed. The dropna function removes any empty values from the result. The returns are then Z-scored, such as:

Here, ![]() is the most recent return,

is the most recent return, ![]() is the mean of returns, and

is the mean of returns, and ![]() is the standard deviation of returns. A

is the standard deviation of returns. A z_score value of 0 indicates that the score is the same as the mean. When the value of z_score reaches 1.5 or -1.5, as defined by the sell_threshold and buy_threshold variables respectively, this could indicate a strong sell or buy signal, since the Z-score for the following periods is expected to revert back to the mean of zero. When a signal is generated it can be used to either open a position or to close an existing position:

"""

Implementation of a mean-reverting strategy

based on the Strategy class

"""

import pandas as pd

class MeanRevertingStrategy(Strategy):

def __init__(self, symbol,

lookback_intervals=20,

buy_threshold=-1.5,

sell_threshold=1.5):

Strategy.__init__(self)

self.symbol = symbol

self.lookback_intervals = lookback_intervals

self.buy_threshold = buy_threshold

self.sell_threshold = sell_threshold

self.prices = pd.DataFrame()

self.is_long, self.is_short = False, False

def event_position(self, positions):

if self.symbol in positions:

position = positions[self.symbol]

self.is_long = True if position.net > 0 else False

self.is_short = True if position.net < 0 else False

def event_tick(self, market_data):

self.store_prices(market_data)

if len(self.prices) < self.lookback_intervals:

return

signal_value = self.calculate_z_score()

timestamp = market_data.get_timestamp(self.symbol)

if signal_value < self.buy_threshold:

self.on_buy_signal(timestamp)

elif signal_value > self.sell_threshold:

self.on_sell_signal(timestamp)

def store_prices(self, market_data):

timestamp = market_data.get_timestamp(self.symbol)

self.prices.loc[timestamp, "close"] =

market_data.get_last_price(self.symbol)

self.prices.loc[timestamp, "open"] =

market_data.get_open_price(self.symbol)

def calculate_z_score(self):

self.prices = self.prices[-self.lookback_intervals:]

returns = self.prices["close"].pct_change().dropna()

z_score = ((returns-returns.mean())/returns.std())[-1]

return z_score

def on_buy_signal(self, timestamp):

if not self.is_long:

self.send_market_order(self.symbol, 100,

True, timestamp)

def on_sell_signal(self, timestamp):

if not self.is_short:

self.send_market_order(self.symbol, 100,

False, timestamp)After defining all of our core components, we are now ready to implement the backtesting engine as the Backtester class.

The start_backtest method initializes our strategy, defines the order handler for this strategy with the evthandler_order method, sets up and runs the market data source function. When data is received from the market data source function, the function evthandler_tick method handles each incoming tick data and passes them to our strategy.

Thereafter, the match_order_book method, in conjunction with the is_order_unmatched method, is called to make an attempt to match any outstanding orders in our system, given the current market prices. The is_order_unmatched method returns True when no order is filled, or False otherwise. On filling an order, it calls the update_filled_position method for further processing. This includes updating the position values, notifying the Strategy object of a position update, and keeping track of our profits and losses. The is_order_unmatched method also notifies the Strategy object of an order update event when an order is filled.

Lastly, the position updates are printed to the console to help us keep track of our account status. This main loop of the backtesting engine continues until the last tick is available from the source of the market data. The full implementation of the Backtester class is given as follows:

import datetime as dt

import pandas as pd

class Backtester:

def __init__(self, symbol, start_date, end_date,

data_source="google"):

self.target_symbol = symbol

self.data_source = data_source

self.start_dt = start_date

self.end_dt = end_date

self.strategy = None

self.unfilled_orders = []

self.positions = dict()

self.current_prices = None

self.rpnl, self.upnl = pd.DataFrame(), pd.DataFrame()

def get_timestamp(self):

return self.current_prices.get_timestamp(

self.target_symbol)

def get_trade_date(self):

timestamp = self.get_timestamp()

return timestamp.strftime("%Y-%m-%d")

def update_filled_position(self, symbol, qty, is_buy,

price, timestamp):

position = self.get_position(symbol)

position.event_fill(timestamp, is_buy, qty, price)

self.strategy.event_position(self.positions)

self.rpnl.loc[timestamp, "rpnl"] = position.realized_pnl

print self.get_trade_date(),

"Filled:", "BUY" if is_buy else "SELL",

qty, symbol, "at", price

def get_position(self, symbol):

if symbol not in self.positions:

position = Position()

position.symbol = symbol

self.positions[symbol] = position

return self.positions[symbol]

def evthandler_order(self, order):

self.unfilled_orders.append(order)

print self.get_trade_date(),

"Received order:",

"BUY" if order.is_buy else "SELL", order.qty,

order.symbol

def match_order_book(self, prices):

if len(self.unfilled_orders) > 0:

self.unfilled_orders =

[order for order in self.unfilled_orders

if self.is_order_unmatched(order, prices)]

def is_order_unmatched(self, order, prices):

symbol = order.symbol

timestamp = prices.get_timestamp(symbol)

if order.is_market_order and timestamp > order.timestamp:

# Order is matched and filled.

order.is_filled = True

open_price = prices.get_open_price(symbol)

order.filled_timestamp = timestamp

order.filled_price = open_price

self.update_filled_position(symbol,

order.qty,

order.is_buy,

open_price,

timestamp)

self.strategy.event_order(order)

return False

return True

def print_position_status(self, symbol, prices):

if symbol in self.positions:

position = self.positions[symbol]

close_price = prices.get_last_price(symbol)

position.update_unrealized_pnl(close_price)

self.upnl.loc[self.get_timestamp(), "upnl"] =

position.unrealized_pnl

print self.get_trade_date(),

"Net:", position.net,

"Value:", position.position_value,

"UPnL:", position.unrealized_pnl,

"RPnL:", position.realized_pnl

def evthandler_tick(self, prices):

self.current_prices = prices

self.strategy.event_tick(prices)

self.match_order_book(prices)

self.print_position_status(self.target_symbol, prices)

def start_backtest(self):

self.strategy = MeanRevertingStrategy(self.target_symbol)

self.strategy.event_sendorder = self.evthandler_order

mds = MarketDataSource()

mds.event_tick = self.evthandler_tick

mds.ticker = self.target_symbol

mds.source = self.data_source

mds.start, mds.end = self.start_dt, self.end_dt

print "Backtesting started..."

mds.start_market_simulation()

print "Completed."To run our backtester, simply create an instance of the class with the required parameters. Here, we defined the ticker symbol AAPL for the period January 1, 2014 to December 31, 2014. By default, our target market data source is defined as google. Then, we will call the start_backtest method:

>>> backtester = Backtester("AAPL", ... dt.datetime(2014, 1, 1), ... dt.datetime(2014, 12, 31)) >>> backtester.start_backtest()

The output will begin to run like this:

Backtesting started... 2014-02-27 Received order: SELL 100 AAPL 2014-02-28 Filled: SELL 100 AAPL at 75.58 2014-02-28 Net: -100 Value: 7558.0 UPnL: 40.0 RPnL: 0 2014-03-03 Net: -100 Value: 7558.0 UPnL: 19.0 RPnL: 0 2014-03-04 Net: -100 Value: 7558.0 UPnL: -31.0 RPnL: 0 …

Almost a year's worth of daily information will be printed onto the console. The output will end with something like this:

… 014-12-29 Net: -100 Value: 12504.0 UPnL: 1113.0 RPnL: 1278.0 2014-12-30 Net: -100 Value: 12504.0 UPnL: 1252.0 RPnL: 1278.0 2014-12-31 Net: -100 Value: 12504.0 UPnL: 1466.0 RPnL: 1278.0 Completed.

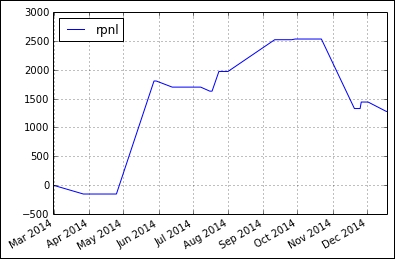

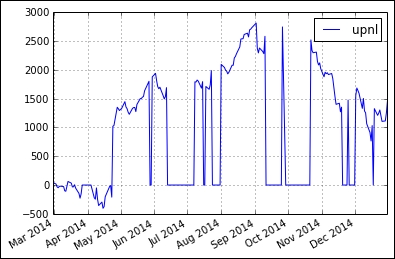

In the MeanRevertingStrategy class, we trade shares of AAPL in quantities of 100. Note that when the backtest is completed, we still have an outstanding short position of 100 shares. Our realized profit and loss is $1,278, while the unrealized profit from the short position is $1,466.

Since we store the daily realized and unrealized profits and losses into a pandas DataFrame object, named rpnl and upnl respectively, we can plot the results to visualize the returns from our strategy:

>>> import matplotlib.pyplot as plt >>> backtester.rpnl.plot() >>> plt.show()

>>> backtester.upnl.plot() >>> plt.show()

The following is the output for the preceding commands:

In this section, we looked at creating a simple backtesting system based on daily closing prices for a mean-reverting strategy. There are several areas of considerations to make such a backtesting model more realistic. Are historical daily prices sufficient to test our model? Should intra-day limit orders be used instead? Our account value started from zero; how can we reflect our capital requirements accurately? Are we able to borrow shares for shorting?

Since we took an object-oriented approach to create a backtesting system, how easy would it be to integrate other components in future? A trading system could accept more than one source of market data. We could also create components that allow us to deploy our system to the product environment.

The list of concerns mentioned are not exhaustive. To guide us in implementing a robust backtesting model, the next section spells out ten considerations in the design of such a system.