Short-term spot rates can be derived directly from various short-term securities, such as zero-coupon bonds, T-bills, notes, and Eurodollar deposits. However, longer-term spot rates are typically derived from the prices of long-term bonds through a bootstrapping process, taking into account the spot rates of maturities corresponding to the coupon payment date. After obtaining short-term and long-term spot rates, the yield curve can then be constructed.

Let's illustrate the bootstrapping of the yield curve with an example. The following table shows a list of bonds with different maturities and prices:

|

Bond face value in Dollars |

Time to maturity in years |

Annual coupon in Dollars |

Bond cash price in Dollars |

|---|---|---|---|

|

100 |

0.25 |

0 |

97.50 |

|

100 |

0.50 |

0 |

94.90 |

|

100 |

1.00 |

0 |

90.00 |

|

100 |

1.50 |

8 |

96.00 |

|

100 |

2.00 |

12 |

101.60 |

An investor of a 3-month zero-coupon bond today at $97.50 would earn an interest of $2.50. The 3-month spot rate can be calculated as follows:

Thus, the 3-month zero rate is 10.127 percent with continuous compounding. The spot rates of the zero-coupon bonds are computed in the following table:

|

Time to maturity in years |

Spot rate (in percent) |

|---|---|

|

0.25 |

10.127 |

|

0.50 |

10.469 |

|

1.00 |

10.536 |

Using these spot rates, we can now price the 1.5-year bond as:

To solve for y, the spot rate for the 1.5-year bond and 2-year bond is 10.681 percent and 10.808 percent respectively.

The following code is an implementation of bootstrapping a yield curve in Python. Save this code to BootstrapYieldCurve.py:

""" Bootstrapping the yield curve """

import math

class BootstrapYieldCurve():

def __init__(self):

self.zero_rates = dict() # Map each T to a zero rate

self.instruments = dict() # Map each T to an instrument

def add_instrument(self, par, T, coup, price,

compounding_freq=2):

""" Save instrument info by maturity """

self.instruments[T] = (par, coup, price, compounding_freq)

def get_zero_rates(self):

""" Calculate a list of available zero rates """

self.__bootstrap_zero_coupons__()

self.__get_bond_spot_rates__()

return [self.zero_rates[T] for T in self.get_maturities()]

def get_maturities(self):

""" Return sorted maturities from added instruments. """

return sorted(self.instruments.keys())

def __bootstrap_zero_coupons__(self):

""" Get zero rates from zero coupon bonds """

for T in self.instruments.iterkeys():

(par, coup, price, freq) = self.instruments[T]

if coup == 0:

self.zero_rates[T] =

self.zero_coupon_spot_rate(par, price, T)

def __get_bond_spot_rates__(self):

""" Get spot rates for every marurity available """

for T in self.get_maturities():

instrument = self.instruments[T]

(par, coup, price, freq) = instrument

if coup != 0:

self.zero_rates[T] =

self.__calculate_bond_spot_rate__(

T, instrument)

def __calculate_bond_spot_rate__(self, T, instrument):

""" Get spot rate of a bond by bootstrapping """

try:

(par, coup, price, freq) = instrument

periods = T * freq # Number of coupon payments

value = price

per_coupon = coup / freq # Coupon per period

for i in range(int(periods)-1):

t = (i+1)/float(freq)

spot_rate = self.zero_rates[t]

discounted_coupon = per_coupon *

math.exp(-spot_rate*t)

value -= discounted_coupon

# Derive spot rate for a particular maturity

last_period = int(periods)/float(freq)

spot_rate = -math.log(value /

(par+per_coupon))/last_period

return spot_rate

except:

print "Error: spot rate not found for T=%s" % t

def zero_coupon_spot_rate(self, par, price, T):

""" Get zero rate of a zero coupon bond """

spot_rate = math.log(par/price)/T

return spot_rateWe can instantiate the BootstrapYieldCurve class, and add each bond's information from the preceding table:

>>> from BootstrapYieldCurve import BootstrapYieldCurve >>> yield_curve = BootstrapYieldCurve() >>> yield_curve.add_instrument(100, 0.25, 0., 97.5) >>> yield_curve.add_instrument(100, 0.5, 0., 94.9) >>> yield_curve.add_instrument(100, 1.0, 0., 90.) >>> yield_curve.add_instrument(100, 1.5, 8, 96., 2) >>> yield_curve.add_instrument(100, 2., 12, 101.6, 2) >>> y = yield_curve.get_zero_rates() >>> x = yield_curve.get_maturities()

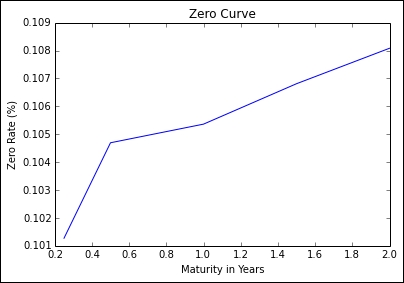

Calling the get_zero_rates method in the class returns a list of spot rates in the same order as the maturities, which are stored in the y and x variables respectively. When we plot x and y on a graph, we get the following output:

>>> import matplotlib.pyplot as plt >>> plt.plot(x, y) >>> plt.title("Zero Curve") >>> plt.ylabel("Zero Rate (%)") >>> plt.xlabel("Maturity in Years") >>> plt.show()

In a normal yield curve environment, where the interest rates increase as the maturities increase, we can obtain an upward-sloping yield curve.