Core-periphery decomposition

by Ágnes Vidovics-Dancs, Kata Váradi, Tamás Vadász, Ágnes Tuza, Balázs Árpád Szucs,

R: Data Analysis and Visualization

Core-periphery decomposition

by Ágnes Vidovics-Dancs, Kata Váradi, Tamás Vadász, Ágnes Tuza, Balázs Árpád Szucs,

R: Data Analysis and Visualization

- R: Data Analysis and Visualization

- Table of Contents

- R: Data Analysis and Visualization

- I. Module 1: Data Analysis with R

- 1. RefresheR

- 2. The Shape of Data

- 3. Describing Relationships

- 4. Probability

- 5. Using Data to Reason About the World

- 6. Testing Hypotheses

- 7. Bayesian Methods

- 8. Predicting Continuous Variables

- 9. Predicting Categorical Variables

- 10. Sources of Data

- 11. Dealing with Messy Data

- 12. Dealing with Large Data

- 13. Reproducibility and Best Practices

- II. Module 2: R Graphs

- 1. R Graphics

- 2. Basic Graph Functions

- Introduction

- Creating basic scatter plots

- Creating line graphs

- Creating bar charts

- Creating histograms and density plots

- Creating box plots

- Adjusting x and y axes' limits

- Creating heat maps

- Creating pairs plots

- Creating multiple plot matrix layouts

- Adding and formatting legends

- Creating graphs with maps

- Saving and exporting graphs

- 3. Beyond the Basics – Adjusting Key Parameters

- Introduction

- Setting colors of points, lines, and bars

- Setting plot background colors

- Setting colors for text elements – axis annotations, labels, plot titles, and legends

- Choosing color combinations and palettes

- Setting fonts for annotations and titles

- Choosing plotting point symbol styles and sizes

- Choosing line styles and width

- Choosing box styles

- Adjusting axis annotations and tick marks

- Formatting log axes

- Setting graph margins and dimensions

- 4. Creating Scatter Plots

- Introduction

- Grouping data points within a scatter plot

- Highlighting grouped data points by size and symbol type

- Labeling data points

- Correlation matrix using pairs plots

- Adding error bars

- Using jitter to distinguish closely packed data points

- Adding linear model lines

- Adding nonlinear model curves

- Adding nonparametric model curves with lowess

- Creating three-dimensional scatter plots

- Creating Quantile-Quantile plots

- Displaying the data density on axes

- Creating scatter plots with a smoothed density representation

- 5. Creating Line Graphs and Time Series Charts

- Introduction

- Adding customized legends for multiple-line graphs

- Using margin labels instead of legends for multiple-line graphs

- Adding horizontal and vertical grid lines

- Adding marker lines at specific x and y values using abline

- Creating sparklines

- Plotting functions of a variable in a dataset

- Formatting time series data for plotting

- Plotting the date or time variable on the x axis

- Annotating axis labels in different human-readable time formats

- Adding vertical markers to indicate specific time events

- Plotting data with varying time-averaging periods

- Creating stock charts

- 6. Creating Bar, Dot, and Pie Charts

- Introduction

- Creating bar charts with more than one factor variable

- Creating stacked bar charts

- Adjusting the orientation of bars – horizontal and vertical

- Adjusting bar widths, spacing, colors, and borders

- Displaying values on top of or next to the bars

- Placing labels inside bars

- Creating bar charts with vertical error bars

- Modifying dot charts by grouping variables

- Making better, readable pie charts with clockwise-ordered slices

- Labeling a pie chart with percentage values for each slice

- Adding a legend to a pie chart

- 7. Creating Histograms

- Introduction

- Visualizing distributions as count frequencies or probability densities

- Setting the bin size and the number of breaks

- Adjusting histogram styles – bar colors, borders, and axes

- Overlaying a density line over a histogram

- Multiple histograms along the diagonal of a pairs plot

- Histograms in the margins of line and scatter plots

- 8. Box and Whisker Plots

- Introduction

- Creating box plots with narrow boxes for a small number of variables

- Grouping over a variable

- Varying box widths by the number of observations

- Creating box plots with notches

- Including or excluding outliers

- Creating horizontal box plots

- Changing the box styling

- Adjusting the extent of plot whiskers outside the box

- Showing the number of observations

- Splitting a variable at arbitrary values into subsets

- 9. Creating Heat Maps and Contour Plots

- 10. Creating Maps

- 11. Data Visualization Using Lattice

- Introduction

- Creating bar charts

- Creating stacked bar charts

- Creating bar charts to visualize cross-tabulation

- Creating a conditional histogram

- Visualizing distributions through a kernel-density plot

- Creating a normal Q-Q plot

- Visualizing an empirical Cumulative Distribution Function

- Creating a boxplot

- Creating a conditional scatter plot

- 12. Data Visualization Using ggplot2

- 13. Inspecting Large Datasets

- 14. Three-dimensional Visualizations

- 15. Finalizing Graphs for Publications and Presentations

- Introduction

- Exporting graphs in high-resolution image formats – PNG, JPEG, BMP, and TIFF

- Exporting graphs in vector formats – SVG, PDF, and PS

- Adding mathematical and scientific notations (typesetting)

- Adding text descriptions to graphs

- Using graph templates

- Choosing font families and styles under Windows, Mac OS X, and Linux

- Choosing fonts for PostScripts and PDFs

- III. Module 3: Learning Data Mining with R

- 1. Warming Up

- 2. Mining Frequent Patterns, Associations, and Correlations

- An overview of associations and patterns

- Market basket analysis

- Hybrid association rules mining

- Mining sequence dataset

- The R implementation

- High-performance algorithms

- 3. Classification

- Classification

- Generic decision tree induction

- High-value credit card customers classification using ID3

- Web spam detection using C4.5

- Web key resource page judgment using CART

- Trojan traffic identification method and Bayes classification

- Identify spam e-mail and Naïve Bayes classification

- Rule-based classification of player types in computer games and rule-based classification

- 4. Advanced Classification

- 5. Cluster Analysis

- 6. Advanced Cluster Analysis

- Customer categorization analysis of e-commerce and DBSCAN

- Clustering web pages and OPTICS

- Visitor analysis in the browser cache and DENCLUE

- Recommendation system and STING

- Web sentiment analysis and CLIQUE

- Opinion mining and WAVE clustering

- User search intent and the EM algorithm

- Customer purchase data analysis and clustering high-dimensional data

- SNS and clustering graph and network data

- 7. Outlier Detection

- Credit card fraud detection and statistical methods

- Activity monitoring – the detection of fraud involving mobile phones and proximity-based methods

- Intrusion detection and density-based methods

- Intrusion detection and clustering-based methods

- Monitoring the performance of the web server and classification-based methods

- Detecting novelty in text, topic detection, and mining contextual outliers

- Collective outliers on spatial data

- Outlier detection in high-dimensional data

- 8. Mining Stream, Time-series, and Sequence Data

- 9. Graph Mining and Network Analysis

- 10. Mining Text and Web Data

- IV. Module 4: Mastering R for Quantitative Finance

- 1. Time Series Analysis

- 2. Factor Models

- 3. Forecasting Volume

- 4. Big Data – Advanced Analytics

- 5. FX Derivatives

- 6. Interest Rate Derivatives and Models

- 7. Exotic Options

- A general pricing approach

- The role of dynamic hedging

- How R can help a lot

- A glance beyond vanillas

- Greeks – the link back to the vanilla world

- Pricing the Double-no-touch option

- Another way to price the Double-no-touch option

- The life of a Double-no-touch option – a simulation

- Exotic options embedded in structured products

- References

- 8. Optimal Hedging

- 9. Fundamental Analysis

- 10. Technical Analysis, Neural Networks, and Logoptimal Portfolios

- 11. Asset and Liability Management

- 12. Capital Adequacy

- 13. Systemic Risks

- V. Module 5: Machine Learning with R module

- 1. Introducing Machine Learning

- 2. Managing and Understanding Data

- R data structures

- Managing data with R

- Exploring and understanding data

- Exploring the structure of data

- Exploring numeric variables

- Measuring the central tendency – mean and median

- Measuring spread – quartiles and the five-number summary

- Visualizing numeric variables – boxplots

- Visualizing numeric variables – histograms

- Understanding numeric data – uniform and normal distributions

- Measuring spread – variance and standard deviation

- Exploring categorical variables

- Exploring relationships between variables

- 3. Lazy Learning – Classification Using Nearest Neighbors

- 4. Probabilistic Learning – Classification Using Naive Bayes

- 5. Divide and Conquer – Classification Using Decision Trees and Rules

- Understanding decision trees

- Example – identifying risky bank loans using C5.0 decision trees

- Understanding classification rules

- Example – identifying poisonous mushrooms with rule learners

- 6. Forecasting Numeric Data – Regression Methods

- Understanding regression

- Example – predicting medical expenses using linear regression

- Understanding regression trees and model trees

- Example – estimating the quality of wines with regression trees and model trees

- 7. Black Box Methods – Neural Networks and Support Vector Machines

- 8. Finding Patterns – Market Basket Analysis Using Association Rules

- 9. Finding Groups of Data – Clustering with k-means

- 10. Evaluating Model Performance

- 11. Improving Model Performance

- 12. Specialized Machine Learning Topics

- Working with proprietary files and databases

- Working with online data and services

- Working with domain-specific data

- Improving the performance of R

- Managing very large datasets

- Learning faster with parallel computing

- GPU computing

- Deploying optimized learning algorithms

- Building bigger regression models with biglm

- Growing bigger and faster random forests with bigrf

- Training and evaluating models in parallel with caret

- A. Reflect and Test Yourself Answers

- Module 1: Data Analysis with R

- Chapter 1: RefresheR

- Chapter 2: The Shape of Data

- Chapter 3: Describing Relationships

- Chapter 4: Probability

- Chapter 5: Using Data to Reason About the World

- Chapter 6: Testing Hypotheses

- Chapter 7: Bayesian Methods

- Chapter 8: Predicting Continuous Variables

- Chapter 9: Predicting Categorical Variables

- Chapter 10: Sources of Data

- Chapter 11: Dealing with Messy Data

- Chapter 12: Dealing with Large Data

- Module 2: R Graphs

- Chapter 1: R Graphics

- Chapter 2: Basic Graph Functions

- Chapter 3: Beyond the Basics – Adjusting Key Parameters

- Chapter 4: Creating Scatter Plots

- Chapter 5: Creating Line Graphs and Time Series Charts

- Chapter 6: Creating Bar, Dot, and Pie Charts

- Chapter 7: Creating Histograms

- Chapter 8: Box and Whisker Plots

- Chapter 9: Creating Heat Maps and Contour Plots

- Module 4: Mastering R for Quantitative Finance

- Module 5: Machine Learning with R

- Chapter 1: Introducing Machine Learning

- Chapter 2: Managing and Understanding Data

- Chapter 3: Lazy Learning – Classification Using Nearest Neighbors

- Chapter 4: Probabilistic Learning – Classification Using Naive Bayes

- Chapter 5: Divide and Conquer – Classification Using Decision Trees and Rules

- Chapter 6: Forecasting Numeric Data – Regression Methods

- Chapter 7: Black Box Methods – Neural Networks and Support Vector Machines

- Chapter 8: Finding Patterns – Market Basket Analysis Using Association Rules

- Module 1: Data Analysis with R

- B. Bibliography

- Index

Interbank markets are tiered and operate in a hierarchical fashion. It is a well-known characteristic of these markets that many banks are dealing with only a small number of big institutions, while these big institutions are acting like intermediaries or money-center banks. These big institutions are considered to be the core of the network, and the others are the periphery.

Many papers focused on this characteristic of real-world networks. For example, Borgatti and Everett (1999) examined this phenomenon on a network made of citation data, and found three journals to be the members of the core. Craig and von Peter (2010) used this core/periphery structure for the German interbank market. Their findings suggest that bank-specific features help to explain how banks position themselves in the interbank market. There is a strong correlation between the size and position in the network. As tiering is not random but behavioral, there are economic reasons (for example, fixed costs) why the banking system organizes itself around a core of money-center banks. This finding also implies that coreness can be a good measure of systemic importance.

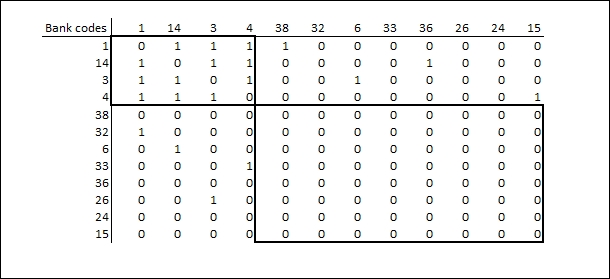

A perfect core-periphery structure of a network can be presented easily by the matrix in Figure 13.3. Core banks are in the upper-left corner of the matrix. All of these banks are connected to each other. They can be considered as intermediaries. They are responsible for the stability of the market, and other banks are connected to each other through these core institutions. In the lower-right corner, there are periphery banks. They have no connection with other periphery institutions. They are only connected to the core as shown in the following screenshot:

Figure 13.4: The adjacency matrix in a core periphery structure

Craig and von Peter (2010) also suggest that not only the core-core or the periphery-periphery part of the matrix is important but the core-periphery part is important as well (the upper-right and the lower-left part). They emphasize that all of the core banks should have at least one connection with a periphery institution. This characteristic means that this periphery bank has no other possibility to be on this market but through a core bank. Although it is an important issue, we think that due to possible contagious effects, being a core bank in itself can result in systemic importance.

In many cases, it is impossible to get pure core/periphery decomposition in the case of real-world networks. This is true especially when we also have requirements for the core-periphery part of the matrix. For this reason, in the first step, we will try to solve the maximum clique problem (for example, by using the Bron-Kerbosch algorithm, Bron and Kerbosch 1973), and then, in the second step, we will choose the result with the lowest average degree in the periphery-periphery part. There are many other different methods to make a core-periphery decomposition. Due to its simplicity, we have chosen this one.

In this subsection, we show how to program the core-periphery decomposition. We will cover all the relevant information, from downloading essential R packages to loading the data set, and from the decomposition itself to the visualization of the results. We will show the code in small parts, and will give a detailed explanation on each of them.

We set the library that we will use during the simulation. The code will look for the input data files in this library. We download an R package igraph, which is an important tool in the visualization of financial networks. Of course, after the first run of this code, this row might be deleted since the installation process should not be repeated again. Finally, after the installation, the package should also be loaded first to the current R session.

install.packages("igraph") library(igraph)

As the second step, we load the dataset, which is only the matrix in this case. The imported data is a data frame that has to be converted in a matrix form. As we have shown before (Figure 13.1), the matrix doesn't contain data when there are no transactions between two banks. The third row fills those cells with a 0. Then, since we only need the adjacency matrix, we change all the non-zero cells to 1. Finally, we create a graph as an object from the adjacency matrix.

adj_mtx <- read.table("mtx.csv", header = T, sep = ";") adj_mtx <- as.matrix(adj_mtx) adj_mtx[is.na(adj_mtx)] <- 0 adj_mtx[adj_mtx != 0] <- 1 G <- graph.adjacency(adj_mtx, mode = "undirected")

The igraph package has a function called largest.clique, which results in a list of the solutions of the largest clique problem. CORE will contain all the sets of the largest cliques. The command is as follows:

CORE <- largest.cliques(G)

The largest clique will be the core of the graph and its complement will be the periphery. We create this periphery for every resulted largest clique. Then, we set different colors for the core nodes and for the periphery. This helps to distinguish them on the chart.

for (i in 1:length(CORE)){ core <- CORE[[i]] periphery <- setdiff(1:33, core) V(G)$color[periphery] <- rgb(0,1,0) V(G)$color[core] <- rgb(1,0,0) print(i) print(core) print(periphery)

Then, we count the average degree of the periphery-periphery matrix. For the identification of systemically important financial institutions, the best solution is when this average degree is the lowest.

H <- induced.subgraph(G, periphery) d <- mean(degree(H))

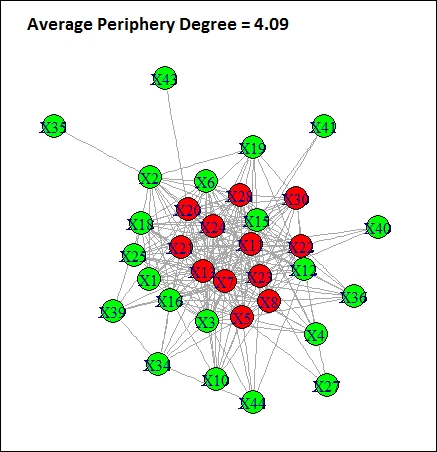

Finally, we plot the graph in a new window. The chart will also contain the average degree of the periphery matrix.

windows() plot(G, vertex.color = V(G)$color, main = paste("Avg periphery degree:", round(d,2) ) )}

By running the code, we get the charts of all the solutions for core-periphery decomposition. In every case, the average periphery degree will be presented on these charts. We have chosen the solution with the smallest average periphery degree. This means that in this solution, the periphery banks have very limited connection with each other. A problem in the core might make them unable to access the market. On the other side, as the core is completely connected, the contagion process might be fast and can reach every bank. All in all, the default of any core banks jeopardizes the access of periphery banks to the market and may be the source of a contagious process. Figure 13.5 presents the best solution of core-periphery decomposition with this simple method.

According to the results, 12 banks can be considered as systemically important institutions, namely 5, 7, 8, 11, 13, 20, 21, 22, 23, 24, 28, and 30.

Figure 13.5: Core-periphery decomposition with the smallest periphery degree

-

No Comment