![]()

Blueprint to a Million in Twenty-Four Months

“Entrepreneurs are simply those who understand that there is little difference between obstacle and opportunity and are able to turn both to their advantage.”

—NICCOLO MACHIAVELLI

I’VE COACHED MANY real estate agents, and some of them do not want to grow their business. They are happy with what they have. They landed their first direct bank contract and they are content with the substantial income it is generating. I feel, however, that this is a temporary state of mind. The reason they do not want to take their business to the next level is fear. Fear of the unknown. They do not know how. They do not have a framework behind their motivation.

The REO business is new to many; agents have tried and failed by using old methods and tactics while others have succeeded by following a Plan-A blueprint. Anyone who is willing to follow a proven formula can overcome any challenge, capitalize off of every opportunity, and make a lot more than a million dollars. However, a right framework behind a strong desire is necessary in order to make it.

It will not happen overnight, but time is on your side. There are so many REOs on the streets but so few listing agents who are good at managing them. Have you ever dealt with an REO listing agent? Most of them do not know what they are doing, they don’t care to change, and they think their way is the only way.

The industry is changing. Banks are opening their doors to new REO agents. There are so many rumors and speculations floating around in the business that its hard to keep track of them all. My favorite is the “REO mafia” stigma, where only a selected few are privileged to participate. This is farthest from the truth.

When I started I knew no one. I didn’t have large amounts of capital, connections, or a big franchise name behind me for support. Most importantly, the demand wasn’t close to what it is today for REOs. It was a long and tedious up-hill battle. The only thing I had was a burning passion and faith. After painful trial and error sessions, I figured out the formula: first to land a contract then to manage it effectively so I could get more contracts and more REOs. It was a simple step-by-step process.

There is such a large supply of REO properties that banks are desperate for talent. Banks are looking for you. They need an agent who has the ability to grow. They need seasoned agents. If they feel the need to load you up with properties, you need to be able to deliver an exceptional performance, just as if it was not your first REO assignment.

You’ve already learned how to land your first account and how to manage it effectively to create a pipeline of cash flow. If you have not landed your first direct account yet, don’t worry; we have outlined a 90-day action plan for you in this chapter. Now, we want to share with you how to grow your business. This is the advanced REO section. Are you ready?

Some REO agents aren’t up for the tasks. They don’t have the time, framework, or desire to grow their business, so they only stick to the one or two accounts they have. If this is you, then you can stop reading here. On the other hand, other agents I coach have successfully grown their business to three, four, and five direct bank contracts and made millions. The best part about it was they did it just like everyone else.

They mastered the blueprint outlined here and hit the pavement running. They understood that there was very little difference between an obstacle and an opportunity, as they both require the same passion and diligence. So if this is you, let’s get started now.

THE MILLION-DOLLAR REO BLUEPRINT

It takes approximately twenty-four months to make a million dollars in the REO business. The blueprint is simple. In Chapter 2, I discussed how each bank contract can yield you approximately $1,000,000 in gross commission income (GCI), or over $372,000 net. Therefore, to achieve a million dollars net, you would need to land three direct bank contracts.

MILLION-DOLLAR REO BLUEPRINT (3 DIRECT BANK CONTRACTS)

$3 MM GCI / $1,116,000 NET

Input Needed

- 9 new BPO assignments a week

- 90 active listings on MLS

- 300 total properties in inventory

- 35% in-house buyer ratio

Remember from Chapter 2 that working with a direct account is very different from working with an outsourcer. While an outsourcer account will assign you properties sporadically, a direct account will continue to feed you properties. I would say having one direct account is the equivalent of having approximately five outsourcer accounts. Don’t get me wrong, both accounts are great. Just the consistency factor is different.

With a direct account, you will be fed properties until you demonstrate you cannot handle any more. Therefore, it’s a consistent pipeline of money coming in. Remember, there are five key benefits of working with a direct account that help you produce $372,000 net: you work with the decision maker, you earn full commission, you earn guaranteed commission, you get high volume of inventory, and you employ leverage.

It’s leverage that takes you from one direct account to three or more direct accounts. Once you master one, you have a proven track record to go after their competition. Usually what one major bank does, the rest follow. For example, if one bank offers you the ability to scan your checks into your phone without visiting a physical branch to make a deposit, the rest will eventually follow or they will lose customers.

Similarly, if you have what banks want (i.e., a system to maximize value and minimize disposition time for their REOs), then the other banks will want you and your team. In fact, once you perfect the REO Plus Model, you will have created an intangible asset. I say intangible because you’re not selling physical inventory or goods. You’re selling yourself, your team, your brand, your system, and your expertise. It’s all about you.

The rest of the banks will want your intangible asset to ease their pain. Just as you learned about building motivation before talking about business (MOB) when going after your first account, banks are motivated to work with you to help stop the bleeding if you are proven.

BANKS WANT YOUR INTANGBLE ASSET TO EASE THEIR PAIN

The great thing about working with a direct REO account is that it’s performance based. If you close on time, you get a new assignment; you either produce consistently or the bank finds someone who can—bottom line. That’s why it is so critical to master Chapters 4 through 9.

Because the REO business is performance based, meaning the better you perform the more inventory you will receive, all you need is three new BPO assignments a week from three different direct bank contracts (nine new assignments a week) to achieve a million dollars within twenty-four months.

9 NEW BPO ASSIGNMENTS A WEEK = $1MM NET IN 24 MONTHS

Of course all of this depends on how well you do at managing your REO business before branching off and going after more accounts. We say it takes twenty-four months because you need time to fine-tune your systems. If you get greedy and go after too many new accounts early while your team is not ready, you will fail.

You may get three direct bank accounts within ninety days, but when they all start firing away new BPO assignments at you and you’re sitting in front of your dual monitors thinking “there is no way I can do nine BPOs within twenty-four hours,” then you will fall flat on your face.

I have seen new REO agents receive up to 20 BPO assignments a week and have watched them go out of business within three months because they could not execute properly. They were late on all their tasks, they wouldn’t do weekly inspection checks, they wouldn’t submit offers from selling agents, etc., which all led to the bank asset manager re-assigning the properties to another team that was proven. You must be able to anticipate what asset managers want so you can save them and yourself time. This comes from experience, and experience takes time.

The first twelve months of your REO business should be focused on getting your first direct bank account and perfecting the REO Plus Model. The next twelve months should be spent investing your cash and leveraging it. In Chapter 2, we discussed how you will make $372,000 net from one direct REO account. This is a conservative number estimated at a 35 percent net profit margin.

Net profit is your gross commission income (GCI), minus your operating costs. Your operating costs are broken up into both variable costs and fixed costs.

GROSS COMMISSION INCOME (GCI)

-VARIABLE COSTS (VC)

-FIXED COSTS (FC)

NET PROFIT BEFORE TAXES (35% OR MORE)

After the first twelve months, you will have to invest in your business. You cannot be a jack of all trades. You must take a good portion of the $372,000 and leverage it. In the beginning, you might have been short on money but had a lot of time on your hands. Now that you have your systems in place and some cash, you need to leverage that so you can have a lot of time and tons of money.

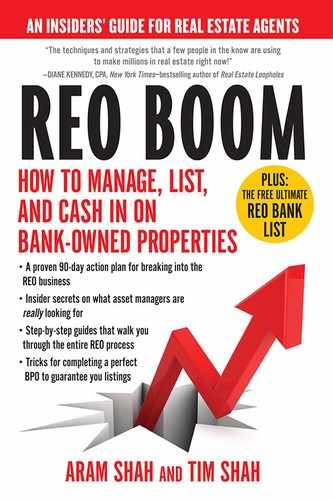

Thus, in order to leverage your business from one direct bank contract to three or more direct bank contracts, you must leverage your cash and bring on two key players to your dream team:

- Business Development Role (“closers”)

- Account Manager Role (“executioners”)

The business development role is finding a key person who can do what you did in the beginning to get your first account, just full-time and non-stop. Their only job is to land bank contracts, going after all the direct bank contracts and as many outsourcers as they can. The more the better; they are your closers.

They need to be able to see your vision, have the same values as you, and take the ball and run with it. They will promote your statistics, maintain your positive track record, and do everything you learned in Chapter 2, fifty to sixty hours a week. This includes fine-tuning your polished proposal and résumé, applying to more accounts, handling phone interviews, networking, and meeting and greeting. Once they land another contract, they will pass the ball off to your account managers.

The account manager role will take the new bank contract that the business development person procured and execute it; they are your executioners. They will supervise the entire REO Plus Model, including your dream team, and make sure every single task from the REO cycle is done accurately, timely, and to the highest quality. They will work hand-in-hand with the business development person and work as a team.

You will motivate both of them with residual income. For every single new account they bring in, you will give them a quarter of one percent (0.25 percent) from the listing commission (LC) on every deal that closes. For example, assuming a conservative 2.5 percent listing commission on a $100,000 home, both the closer and executioner will get a quarter of one point:

$100,000 × 0.0025 = $250.00 (to the closer)

$100,000 × 0.0025 = $250.00 (to the executioner)

It may not seem like a lot, but it adds up in volume. With one direct account you will be closing around twenty deals a month. Imagine three direct accounts (sixty deals a month). Now, multiply $250 × 60 deals a month × 12 months. What do you get? You get a win-win-win situation for both the business development person and the account manager to make great money, and for you to put your business on autopilot.

$250 × 60 deals a month × 12 months = $180,000 residual to both the closer & the executioner.

In addition, I would offer them both a base of no more than $2,000 a month to get them rolling until their residual income outweighs their base salary. Therefore, once they start making above $2,000 a month, their base is eliminated. This is usually removed after the first 90 to 120 days because the new contracts are kicking in and the REOs are cranking out cash. Remember, you have to invest in your business if you want it to grow.

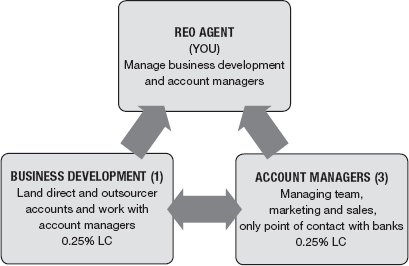

Also, you need only one business development person but multiple account managers. I find it works best when you have one person dedicated to landing bank contracts, as different banks have headquarters in different areas. They will be flying around to various conferences and visiting asset managers’ sites. Plus, it gives them exclusivity. Meanwhile, you will put each account manager in charge of each bank contract. They will be the bank’s main point of contact after the business development person lands the account.

![]() INSIDER TIP

INSIDER TIP

Always set goals with timelines with your business development role. If you are offering exclusivity to them along with residual income, they need to be able to produce results; otherwise you will find someone else who can. A ninety-day trial period is customary.

The best part of the two new roles is that it creates a system of checks and balances for you. Because the closer can only get paid if the executioner manages every task of the REO cycle, they will work hand-in-hand. If the executioner is late on assignments, the closer will be on top of them because it affects their pay. It’s one step closer to automation.

The account manager role will be put into place to supervise your REO Plus Model, so you can take a step back from working forty to fifty hours a week and put it all on autopilot. They will step in to your shoes and take over the day-to-day operations. They will be the main point of contact for the bank’s asset manager. All the members of your dream team will report to them, and they will report to you. The structure would look something like this:

THE ACCOUNT MANAGER ROLE

In addition, they will be responsible for selling and increasing your in-house buyer ratio. Remember, without much effort you will have a 35 percent in-house buyer ratio where you represent both sides of the transaction. I have many agents who share the selling side of their commission as well with their account managers as an incentive to them to get this ratio higher. It’s all up to you. How hands off do you really want to be?

![]() INSIDER TIP

INSIDER TIP

When bringing on both the business developer and account manager, keep the accounts payable role to yourself. Since they will be focusing on landing new accounts and executing, they may want to incur certain expenses that you may not agree with.

PUTTING IT ALL ON AUTOPILOT

The Million-Dollar REO Blueprint is more than just financial success. It’s about being well-balanced so you can have free time. For instance, no matter how much money I make, if it means being stuck in an office sixty hours a week, I am not interested. I would rather spend time at home with my family. Therefore, once you master the REO Plus Model, your job is to put it on cruise control.

In Chapter 3, you learned about standardization. Well, now I want to teach you about automation. That is the reason why bringing on account managers and business developers is so important. They help you work “on” your business instead of “in” your business. They free up your time so you can take a birds-eye view of what’s going on. Once you automate your business, you should be working twenty hours a week maximum.

BRING ON ACCOUNT MANAGERS SO YOU CAN FOCUS “ON” YOUR BUSINESS INSTEAD OF “IN” YOUR BUSINESS

Having this structure is critical to the longevity of your business. You want your business development person and account managers to be motivated to get more properties, which in turn will make them and you more money. They will help you achieve your targeted inputs so you can achieve your targeted outputs of $1,000,000 net a year.

While automating your sales-producing activities by bringing on a business development person and account managers, you also want to automate your operations functions with the use of technology so everyone in your dream team is on the same page.

Many large REO agents use software programs online to manage their REOs (see Appendix A), from offer submissions, expense tracking, BPO inputting, sending out automated emails to your team, and communicating with different bank platforms. Some are more expensive than others. Once you scale up to the REO Plus Model and start thinking about taking your business to the next level, you can look into the different software programs in the marketplace.

Technology will help your account managers by giving them resources to efficiently execute their day-to-day tasks and keep everyone organized. It will be the one tool that you can use to maximize the eight success measurement tools that are discussed later in this chapter.

LEVERAGING VIP LEADERS

Once you put your business on autopilot, you will be working less than twenty hours a week but giving away a lot of decision-making power to your team. Therefore, it is critical to find the right account managers, business development people, and members of your dream team. You do this by identifying leaders. Agents leave managers to join leaders. How many times have you encountered a manager in your career who competed with you or didn’t listen to your needs? They micromanaged you or played foolish power games to let you know who was “boss”. A critical success factor in achieving a million dollars net in the REO business is finding and leading people who are leaders; I call this leveraging leaders.

When you leverage leaders, you gain exponential growth. The REO business is people-driven. You are only good as your team. Would you rather have a team where you are the only leader and the rest are followers, or have a team where you are a leader managing five other leaders under you? Leaders attract other leaders. They usually have a large pool of influence with buyers, investors, and associates. Your goal when growing your team is to identify leaders and quickly offer them an opportunity.

You must also empower them to be successful with you. Provide them with the correct tools to build up a large network for your team. This includes giving them residual income and the proper technology so they can focus on what they do best. Some characteristics I use when identifying leaders is if they are a VIP leader:

- Vision

- Influence

- Passion

A VIP leader has three characteristics: vision, influence, and passion. Do they possess visionary thinking? Are they forward thinking, or past and present thinkers? Do they have a large sphere of influence? They should have good character, act ethically, and know how to build relationships.

Most importantly, they must be trustworthy. You will be outsourcing your entire REO cycle to them when starting (REO Bootstrap Model) in the beginning, and at the end when you bring on your two key roles, so your name will be on the line. After the vicious learning curve period is over (three to six months) you will feel a sense of euphoria as you will have built enough trust with them to know that your work will be turned in on time and it will be done to your standards.

Finally, each person must absolutely love what they do. They must be passionate. No part-timers allowed. You need someone who loves the real estate business and is willing to work 24/7 at it. Passion creates dedication. Passion gives people the extra push to stay up late, work extra hours, make sacrifices, and strive to achieve great results and hit your team goals.

LEVERAGING VIP LEADERS = EXPONENTIAL GROWTH

MEASURING YOUR PERFORMANCE

There’s an old management adage that says you cannot manage what you don’t measure. You can have the perfect dream team, have five direct bank contracts, and have the REO Plus Model down to a science, but if you don’t measure the results, you will not know if you are doing better or worse than before. Chances are if you stop getting your nine BPO assignments a week, you know you are doing something wrong. However, do you want to wait to get to that point?

I had many agents tell me that their asset manager just stopped giving them new assignments for no reason. This happens. Remember, asset managers are people with personalities. Some like to talk and some don’t. Some are so time crunched they don’t have time to take five minutes out of the day and tell you about your performance. It’s up to you to be proactive and highlight your performance to them.

So how do you measure your performance? How do you know if you are doing a good job? Just because you are receiving more properties doesn’t necessarily mean you are performing at your peak. Maybe there is just too much supply and you have the fortune of being at the right place and the right time. Maybe your supplier hasn’t brought on more agents in your market to spread the REOs.

To fool-proof or validate your growing number of properties, you need to measure and continue to measure your performance by eight key performance indicators or measuring tools. As you recall from Chapter 1, the timeline per property is approximately ninety days:

New BPO → Listed → Offer Accepted → Closed Deal = 90 DAYS (7–10 days) + (21 days) + (14 days) + (30–45 days)

Depending on your bank, properties are usually “coded” internally to reflect the current status during this timeline as follows:

- Value: Property is ready to be valued (new BPO needed)

- Repairs: Property is pending repairs to be completed

- Active or Listed: Property has a list price and is ready for MLS

- Accepted: Bank has accepted offer and is waiting or has executed contract

- Off the Market: Property has a lien/code/violation or is occupied by a homeowner or tenant and is off the market temporarily

- Closed: Property has sold

- Eliminated: Property has switched to another agent or gone to a large auction house

Your job is to go from “valuation” to “closed” as fast as possible. The following benchmarks will determine how well you are performing in a month. Always analyze your performance with the following eight success measuring tools.

THE EIGHT SUCCESS MEASUREMENT TOOLS

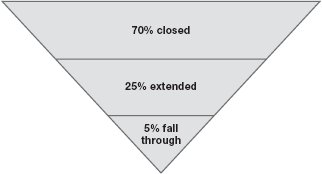

Success Tool #1: Closing Ratio Percentage (CRP)

The REO business is about results. Banks want closings. They need you to stop the bleeding as fast as possible. The number of closed transactions indicates how many properties you were able to close in any particular timeframe. The goal is to maximize the number of closed transactions, minimize the days it takes to close those transactions, and maximize the sales price for each transaction. In bank terms, they may refer to this as maximizing execution and minimizing disposition time. Therefore, a very critical tool to measure is your closing ratio.

- Closing Ratio % = Actual Closed/Scheduled to Close

- Example: 35 Closed/50 Scheduled = 70%

The higher your closing ratio, the better. The more closings you produce the more properties you will receive. Your CRP every month should be 70 percent or greater compared to what you have scheduled on the closing calendar. Don’t worry, the other 30 percent will still close, just not in that month. They will be extended to the following month usually due to a title or financing delay. Remember, the beauty of being an REO listing agent is that everything closes. It’s just a matter of when. On average, your monthly stats per account should look something like this:

So by the end of January 31, 2012, if you have thirty-five scheduled REO closings, on average expect 70 percent to close, 25 percent to be extended to February or March 2012, and 5 percent to fall through or bust out (not closing). The final 5 percent will have to be remarketed with an updated BPO and new pricing.

Success Tool #2: Days on Market (DOM)

Days on market (DOM) is defined as the difference in time between the date the property is “active” on the MLS to the date the bank accepted the offer and the property is considered “accepted” or “pending sale” from the MLS point of view.

- DOM = Date Accepted from Date Active

- Example: January 1, 2012, to January 15, 2012 = 15 Days

For example, you receive a list price and place the property on the MLS on January 1, 2012, and the bank accepts the offer January 15, 2012. Your DOM would be fifteen days. This is a direct measure of your ability to procure a contract; the faster the better.

The bank will usually price its property high enough to maximize its sales price but not so high as to be priced out of the market. The quicker your DOM, the more likely it is that you are marketing your properties effectively to get the property offer accepted. A DOM of thirty or less is ideal.

One variable that would affect this number would be repairs. If you get a property that is being repaired but the bank still wants you to list it on the market because the repairs are minimal, it may be a deterrent to potential buyers. In this scenario, your DOM may be slightly higher. This is when your management skills with your contracts are tested (see Chapter 8). Every day the repairs are delayed, your DOM will be affected. Be cautious.

From there, the average days to close (see below) measures your performance after the property is under contract.

Success Tool #3: Days to Close (DTC)

After the offer is accepted you need to keep your eye on the number of days it takes to close the REO. Days to close (DTC) has a direct correlation with how well you manage or, in many cases, babysit your buyers. Once the property is under contract, how will you prevent buyer’s remorse? Are you following up with all parties? Are you keeping the buyer motivated? Are the buyers’ financing cleared? Are the buyers mentally prepared for the new move?

DTC is the difference between the time the property is “accepted” to the time the property is “closed” or the transaction is closed. In the MLS, this would be labeled as “closed sale.”

DTC = Date Closed from Date Accepted

Example: January 15, 2012, to February 15, 2012 = 30 Days

This number should be as low as possible to ensure that you are not keeping a contract that has no potential for closing active on the market. If the buyer is not qualified, is uncertain, or is unlikely to close the deal, inform your asset manager so they can decide whether or not they want to grant an extension or move on to another buyer.

![]() INSIDER TIP

INSIDER TIP

Disclose, disclose, disclose. If you feel the buyer cannot close (e.g., buyer loses a job, buyer loses communication with you for days, etc.) for whatever reason, contact your asset manager immediately. Time is crucial in this business. It’s better to put the property back on the market and find an ironclad buyer than dance with lukewarm buyers who delay the closing for months. The faster you can get a qualified buyer to purchase the home, the better it is for all parties.

Success Tool #4: Resources Ratio (RR)

The resources ratio (RR) compares both the number of days the property is on the market (DOM) over the number of days it takes to close an REO (DTC). RR ratio measures how efficiently you are allocating your resources (your dream team’s attention). Are you pushing your staff to focus on selling and marketing, or are you pressuring title companies and mortgage lenders to execute?

RR Ratio = DOM / DTC

Example = 15 Days on Market / 30 Days to Close = 50%

There should be a clear balance between the two important functions (marketing and closing). This ratio should not be greater than two. If resources are all allocated to marketing but not closing, you will notice that your marketing efforts become futile; buyers back out because the contract expires and the title is not ready to close.

If resources are all allocated to closing, then you will notice that some properties will stay on the market for longer than average, and thus you will ultimately be biting off more than you can chew. Make sure your marketing efforts are perfected so that you can perfect your closing efforts. Both functions are critical, and there should be a balance between the two.

Success Tool #5: Gross Execution Percentage (GEP)

Gross Execution Percentage is the list price of an REO divided into the sales price.

Gross Execution % = SP/LP

Example: $126,000/$130,000 = 97%

It measures your ability to execute. Anything above a 95 percent GEP is good; above 100 percent GEP is excellent. Did you provide a good-quality BPO? Did you recommend the correct marketing strategy (repaired versus as-is)? These are factors that will affect your GEP percentage. Days on market and GEP percentage have an inverse relationship. The lower the days on market, the more likely the property sells at or above the list price and the higher the gross execution percentage.

This can occur when there is strong demand for a property and you have multiple offers above list price. Chapter 8 discusses the three shady tactics agents use to get offers accepted—avoid those! Remember, it’s not quantity but quality that you are looking for.

Success Tool #6: Price Accuracy Percentage (PAP)

If you think you can produce a low-ball BPO and submit it to an asset manager and get a low listing price, think again. Banks hate low-ball BPO. It speaks of carelessness and sloppiness from an REO agent. Mastering your BPO is important; if it pinpoints at the perfect market price, it will produce price accuracy. Each function of the REO business has checks and balances. Your BPO is checked by the bank’s appraiser to arrive at a final list price (see Chapter 5). The closer you are to the list price, the more you appear to be taking care of the bank’s interest—not your own pockets.

Price Accuracy % = BPO Value / List Price

Example: $120,000 / $130,000 = 92%

Because you will not know the list price until after the BPO and repairs (if any) are completed, price accuracy percentage is a post-measurement success tool. Your goal is to maintain a 90 percent or higher accuracy.

Success Tool #7: Aged Inventory Percentage (AIP)

Aging can feel depressing at times. No one likes it. Not even asset managers. If you see a little REO sitting on the market longer than ninety days, you will have your first aged property. It’s like your first white hair. You want to pluck it as soon as possible before anyone notices. The only reasons an REO hasn’t produced any offers is either it’s priced too high or you recommended the wrong marketing strategy (e.g., as-is versus all repairs).

Any active listing on the MLS for longer than ninety days that has not sold is considered aged. Comparing your aged listings to your total active listings tells you how good of a job you are doing procuring a buyer; the smaller the AIP the better. A good barometer to success would be keeping this number under 10 percent.

Aged Inventory % = Number of Listed > 90 days / Total Number Listed

Example: 3 Aged / 30 Total Active = 10%

AIP ≤ 10%

Success Tool #8: Run-Off Ratio (ROR)

A major part of your success will be based on closed sales. This is what counts. You can think that you did a great job by getting an offer accepted that is much higher than the listing price. But does it count? Did it close? Remember, always be closing!

RESULTS = CLOSINGS

Run-off ratio is based on the theory that you will get more inventories based on your performance in closings. The more you close, the more you get. The ratio should be as close as possible to 100 percent.

ROR = # of closed transactions in any time period / # of properties you have listed + # of properties you have accepted or under contract

Example: You closed 20 properties from January 1 to February 1. On February 1, you had 10 properties listed, and 10 properties under contract. Your run-off ratio would be: (20 / (10 + 10)) = 100%.

The premise is that your performance is based on what you close. You can be the best at listing and marketing, but if you can’t close, then your ROR will show it. Many asset managers use the ROR to determine who will get new assignments.

Think about it from their perspective, how can they justify giving new assignments if your ROR is low? If they do that, they will be contributing to make your ROR even lower (i.e., when they give you a new property to list, it will make the denominator bigger, and if your closings aren’t increasing, then they will be most likely think twice).

AGENT’S SCORECARD: MAKING THE BANK’S “A” LIST

It is critical to stay proactive in your REO business. Your first step is to continuously measure the eight key indicators. Just as you measure, some banks may also send you a report once a year, twice a year, or quarterly giving you a comparison among your competition. This is called an agent’s scorecard.

Why does it matter? Because if a bank has two agents in the same area, one with a very high scorecard and one with a very low scorecard, they will most likely give new assignments to the better agent. Although you can have all the internal measures based on the eight key metrics above, whereby you measure yourself and set goals to improve, you must also note how you are performing compared to others. Without a comparison to how other agents are performing, you have no benchmark other than what your past performance has been.

SAMPLE AGENT SCORECARD

| XYZ REALTY | VENDOR NUMBER: XXXXXXXXX |

|||

| 1ST QUARTER YEAR XXXX | ||||

| RUN OFF | 3 MO INVENTORY | CLOSINGS | ROR | PEER RATING |

| 33 | 25 | 75.76% | A | |

| AGING | 3 MO ENDING INV | AGED INV>90 DAYS | AIP | PEER RATING |

| 42 | 0 | 0.00% | A | |

| GROSS EXECUTION | 3 MO. AVG SP | 3 MO. AVG LP | GEP | PEER RATING |

| 120000 | 100000 | 120.00% | A | |

Why Do Ratios Matter?

You want to make the bank’s “A” list. The agent’s scorecard gives you exclusive information on how other agents are performing. You can use this information in a variety of ways, most importantly to focus your improvement initiatives in the right areas.

For example, if you have a run-off ratio of 75 percent and your peer rating is an “A,” then you should realize that even though you are not at the ideal 100 percent mark, you are still performing better than your competition (i.e., other agents).

Since your grade is an “A,” you may choose to focus on other key metrics instead of this one. However, had you not received an agent’s scorecard, you would never have known your true performance, as you would only have been able to see your performance at face value versus in comparison to others.

SHOWING OFF: TOTAL GROSS SALES VOLUME

I love to show off on semi-annual conference calls. Instead of gloating about my statistics, I will pose a question: I ask the group of competing listing agents or asset managers, “What is the average gross execution percentage or gross sales volume in the past quarter?” When you do this, half of the agents in the call will have no idea what you are talking about. The only ones who do will be you and the asset managers, their managers, or their director.

The best “show me off” number will be your gross sales volume. It is a broader measure of the number of closed transactions you did in a given month.

GROSS SALES VOLUME = # OF CLOSED TRANSACTIONS TIMES THE AVERAGE SALES PRICE OF ALL YOUR CLOSINGS

For example, closing thirty-five homes in January 2012 with an average sales price of $200,000 is closing $7,000,000 for one account ($200,000 × 35); not too bad. Two caveats. First, numbers are deceiving. For example, closing ten condominiums with an average sales price of $30,000 is equivalent in sales volume to closing one single-family home at a sales price of $300,000.

It costs the same for you (in time and money) as the REO listing agent to sell a $10,000 property versus a $300,000 property. Ideally, receiving all high-priced REOs is great, but unfortunately this is market specific. Expect 20 to 30 percent of your inventory to be low priced (under $75,000).

Second, you want to pay attention to your average monthly sales prices. Summing the gross sales volume for all thirty-five closings (e.g., $7,000,000) and then dividing it by the actual number of closings will give you your average sales price of $200,000. Watch this number compared to previous months or quarters.

If you notice your average selling price of a home in January 2012 ($200,000) is less than the average selling price a year ago in January 2011 ($300,000), you can infer that you are still in a down market. More supply is on the market than there are buyers, driving down prices; great for you as an REO agent but not so great for first-time home buyers or investors. This is valuable information you can share with your team and investor database.

MANAGING CASH FLOW

As your business picks up I want to caution you to carefully watch your cash flow; you need to monitor the amount of cash you have in the bank to make sure it’s not running out. Remember OVM from Chapter 3? The reason why the REO Bootstrap Model works so well is because it relies on OVM. If you don’t have the cash to pay for minor expenses under $1,000, your vendor is paying for it and you are reimbursing them within 120 days (or more). They are bank-rolling your operations. Nothing down!

Cash flow is more important to look at than your bottom line profits. Would you rather see a statement from your accountant that says you made $1,000,000 and have $100,000 in the bank or would you rather have $1,000,000 in the bank and have a statement that says you only made $100,000?

REOs are all about the bankroll. If you run out of cash to operate your business, you will be forced to shut down regardless of how much profit you make. Think about this. If you have a Ferrari Enzo that does zero to sixty miles per hour in 3.4 seconds racing against a Honda Accord EX, will you win? Sure, if you have gas.

In the REO business, cash flow is gas. If you can’t pay your utilities or hourly wages on the first and fifteenth of every month, then no matter what you say, your dream team will leave on the spot. No one works for free. That’s why when you have fewer than thirty active listings you must start with the REO Bootstrap Model, even if it means turning down additional accounts in the beginning.

I have seen a lot of companies in other industries hire the best sales force that goes and gets five to ten new accounts within a month’s time and then cannot service the customers because the company ran out of bankroll. This makes them look bad and non-credible. Don’t let this happen to your REO business.

TRIMMING THE FAT

Measuring your performance and monitoring your cash flow are necessary steps. If you can perform and have enough of a bankroll you will not have to worry about too much. However, if you notice your expenses rising while your sales are staying constant, or your sales decreasing while your expenses are staying constant, you have an expense problem; you’re spending too much money.

There are only 100 pennies in a dollar. Every penny you allow to leave your business that is unnecessary means the fewer dollars you will have. Pennies are your expenses, and the dollar is your profit.

I like to travel. I have visited many places outside the United States. One thing I noticed that was shocking while outside of the United States was no matter which country I visited, I did not find one penny (or equivalent currency) on the floor. In the United States, in almost any street you will find a penny, a nickel, and even dollars.

The secret to achieving a $1 million dollar net in this business is to watch your fixed expenses. Every penny you spend should be allocated with caution. If you are still printing documents in hard copy, signing in blue ink, or faxing via a traditional fax, you are throwing away pennies from your dollar. The more pennies that go out, the less you keep.

In your business there are two areas of fixed expenses or pennies you need to watch before they sneak away from you:

- Advertising

- Rent

Advertising, specifically print advertising, will kill your profits. Don’t even think about making a healthy bottom line if you are planning to do print ads. As an REO agent, you will rarely use print ads. With the advent of technology and the move to social media marketing, print ads are extinct. Plus, they are a rip-off.

The only exception is if you are in a small rural area with a local flyer that circulates for free around town and is what everyone reads—that might be the exception. Regardless, your annual advertising expense should not be greater than 1 percent of your gross commission income, and all of it should be spent online or for items outlined in Chapter 2.

$1,000,000 (GCI)

× 1%

$10,000 (Max Advertising Allowance)

Remember from Chapter 7 that you want to showcase as many of your REOs online as possible. The good news as an REO agent is that your banks will have all of your listings on their preferred marketing sites, which will provide approximately 60 percent of your leads. Since you are the REO listing agent, you will be the name and face on the listings on every preferred website. The 40 to 50 percent will have to come from you maximizing the magnet marketing plan and building relationships with consumers.

Sometimes it’s a hard thing to do, and the learning curve may be steep, but you must implement and use technology. It is your best friend. It makes you extremely efficient both with your time and your money. For example, some agents I have coached have eliminated printing entirely by using Adobe Professional to handle their printing needs.

Instead of printing out hard copies, they “print” and save the document to their computers. They even use Adobe to sign signatures digitally. It cuts about 50 percent of their time dealing with other cooperating selling agents, customers, and banks.

Rent is the next necessary evil. Although you will need it when transitioning to the REO Plus Model, you must keep a lid on it. Some of the REO agents I coach willingly choose not to transition from the REO Bootstrap Model. They know they will make less but they simply do not want to deal with a live office and the intricacies involved with it. The choice is yours.

However, remember that to achieve a million dollars within twenty-four months you must make the leap to the REO Plus Model as it ensures you achieving 35 to 50 percent net profit margins and high-quality work; sticking with the Bootstrap Model means you will be leaving big money on the table (see Chapter 3).

In the REO Bootstrap Model, your listing specialist works from home and either meets you at a title company, a local coffee shop, or at a virtual office to finalize a transaction. You then gather weekly conference calls and set up a physical meeting once a month with your team. If you do not feel comfortable transitioning, just remember you’re trading off your net income.

In the beginning, I had signed up for virtual offices. It ran less than $200 a month and allowed for six free hours a month to utilize a conference room on the fiftieth floor (out of sixty) of a high-rise overlooking the city and bay. It was in the best location possible. If I had physically leased a space there, I would have been bankrupt the next day, as the lease rates were $40 to $50 a square foot triple net.

Once you leverage your REO listing capacity above thirty active listings, you will want to transition into the REO Plus Model, and then you will physically need an office. Depending on which part of the country you are in, you will not need more than 1,500 square feet and should not pay more than $15 a square foot gross lease (meaning it includes utilities and taxes).

Finally, make sure your lease terms are flexible. Commercial landlords are hurting now as well. Get flexible terms such as “options to renew” at your below-market rent or get an escape clause allowing you to back out without penalty with a sixty-day notice.

![]() INSIDER TIP

INSIDER TIP

If the landlord is hesitant, offer to sign a confidentiality agreement where you will not disclose a below-market rent to other tenants in the office building.

Whatever you do, resist the urge of splurging on your office, especially after you land a big account or two. The times of incentiv-izing agents and staff with plush leather sofas and big offices are over. Everyone is on the road, working from home and out of coffee shops.

In my office, I have nothing but IKEA furniture. I assembled it myself. It looks good and is very inexpensive. Technology has changed the game. Lavish offices are an unnecessary expense and should be avoided.

SECRET TO MAKING A MILLION: STAY LEAN BY CUTTING ADVERTISING AND RENT EXPENSES

A couple of years ago, during the “easy” real estate days, I met this estate agent who we’ll call Brody. He probably had one of the best marketing campaigns money could buy. In addition, he was sharp as a tack and was pretty charming in person as well. Every time I would drive down the highway I would see his picture. It was him and his puppy. He was living on billboards.

If I had to guess, his marketing budget must have been at least $30,000 a month. Every other billboard within a three to five mile radius was him. I remember saying to myself, “Either this agent is really smart, or has a very high risk tolerance.” It was clear he was implementing the “old school method” of selling real estate; throw a whole bunch of mud on the wall via advertising and see what sticks.

During spring of 2007, I attempted to call him since I had some customers who were looking to list their home in his market, and his number was disconnected; I Googled him and nothing. No Facebook, no Twitter, no LinkedIn, it was as if he had disappeared. I called his old brokerage office, and they said he had left the real estate business. Turns out he did have a very high risk tolerance.

The biggest difference between today’s real estate markets, dealing with REOs, versus the old school conventional method of obtaining listings is how you control and manage your expenses. Before, in order to make a million dollars, you basically needed to mortgage your house, car, boat, and your kid’s college tuition plans.

This is exactly what Brody did. He was used to the good old days of average sales prices being $250,000 and earning a quick 3 percent listing side commission. Since financing was easy to obtain and the market was hot, he figured he could sell 453 homes a year; piece of cake.

453 HOMES A YEAR × $250,000 AVERAGE PRICE × 0.03 LISTING COMMISSION × 30% CONSERVATIVE PROFIT MARGIN = $1,019,250

Unfortunately the market shifted, homeowners became upside down on their mortgages, average home prices were brutally slashed in half, banks tightened their lending guidelines, and Brody went from living on billboards to possibly on park benches (I hope not).

The lesson is that the old days of aggressive prospecting and marketing are over. Old-school methods of spending big money do not work today. Remember, whoever controls the listings controls the cash. Therefore, the golden geese in today’s market are banks; the new-school method of real estate is going after the REO golden goose–bank contracts.

If you focus on spending your 1 percent advertising budget on revenue generating activities such as procuring new bank contracts (yielding you $1 million in GCI per contract) or online marketing of your REOs, while keeping your advertising and rent expenses low, you will increase your bottom line profits.

90-DAY ACTION PLAN

Becoming an REO listing agent is not something that will happen overnight. It takes time. The good news, however, is that everyone gets in. It’s just a matter of when. But it’s not going to happen by chance. It is your job to take action. The more passionate and disciplined you are, the shorter the time it will take you to land your first contract (in case you haven’t already).

In Chapter 2, I talked about all the strategies for you to get your foot in the door. Please re-read that chapter. It is very important. Whether it is your first contract or your tenth, the tools and strategies remain the same.

We have itemized a 90-day action plan for you to get started in the business immediately. Therefore, take action today. You have two options. The first one is that after you finish reading the next and final chapter, you close this book, store it in your collection, freeze, and say “you will get to it later,” or you take action today.

Commit to yourself today that you want change in your real estate career. You want to add an abundance of wealth to your life and your family’s. In the next chapter, we talk about the difference between wealth and money. They are two very different things. I also discuss my personal struggle and how the REO business literally changed my life. Review the 90-day action plan below, photocopy and print it out from Appendix L (or visit reoboom.com for a free download), and get started today.

90-DAY ACTION PLAN

DAYS 1 THROUGH 30 (PREPARE AND PLAN)

Week One:

■ Obtain all of your REO certifications. Research the REO listing agents in your area. Go to their websites. What certifications do they have? You must have at minimum these certifications.

■ Create your polished résumé (see Chapter 2) including the ten key tools. See Appendix O for a sample résumé.

■ Create the polished proposal (see Chapter 2). Print fifty portfolios, as these are necessary for you to obtain your first account.

■ Do mock BPOs on your own house and family and friends’ houses. Offer a free valuation. Watch how fast you will gain experience.

■ Use the Reach-Around Method from Chapter 2 and join a real estate office that is a “direct” listing agent. Offer to work for free. Ask to hang your real estate license with the company. Tell them that you have what it takes, that you will do it for free, and that you just need a couple of weeks to prove that you are the agent they have been looking for. Be the first one in the office and the last one to leave.

■ Gain experience. Handle calls, go to properties, and look at different REO listings. Use the information in this book and hands-on experience in the field to see what type of results that direct listing office is producing and how you can improve performance.

Week Two:

■ Start networking. Go to networking events, REO conventions, and local board meetings. Start spreading the word that you work with a direct REO listing office. Even though you may not have any listings, focus on the fact that you are the best REO listing agent on the market. It will come. It’s not a matter of “if” but “when.” Keep in the back of your mind, preparation + plug = first bank contract.

■ Print out business cards, show houses, follow listing agents at the office, and absorb as much information as you can. Learn. Learn. Learn.

■ Ask for one; just one listing. Even if you don’t make commission, you want to learn. Once you get it, use our systems to impress everyone. Make them believe in you.

■ Implement the REO Lunch Method. Find “aged” REO properties that have been on the market for greater than ninety days. Identify who the asset manager is. Contact the asset manager (remember MOB—motivation over business) and tell them that you work as a direct listing agent for XYZ and that you would like to do a FREE second opinion BPO. Continue doing this—you will see that the behavior is reciprocated by the asset manager giving you a listing.

■ Find a mentor who has done it. Ask them to give you some pointers. Take them out to lunch. Tell them once you get rolling and knee-deep in the business you will hire them on a consulting basis. However, if you have the money, invest it with your mentor. It’s worth every penny.

Week Three:

■ Start building your buyer network. Order one hundred yard signs and wire stands (one color, double-sided) and place them out in your farm area on Friday afternoon through Sunday evening. Use yard signs combined with landing pages and drip campaigns to build a large database; the larger your network, the more value you will add to the banks.

■ Start your REO Bus Tour (see Chapter 2). Gather investors and home buyers to go on a bus tour with you to visit REO properties for sale. Take them to the property that you are doing a second opinion BPO on. You shouldn’t be surprised if a passenger says, “Wow, I would buy that right now.” It works. Just make sure your co-op partner is pre-qualifying all the leads.

Week Four:

■ Network. Network. Network. Go to all REO conventions. Meet asset managers.

■ Use the REO FARM Play (see Chapter 2) when you get in front of asset managers.

■ Listen first. Draw out their motivation. What are they motivated to find from a listing agent? What are they lacking? What problems are they having in their local market? Build their motivation before getting into business. Remember, motivation before business (MOB).

■ Show them that you have what it takes to solve their problems, that you know how to stop the bleeding, and that you are different than the typical listing agent. It’s important to show them, not tell them. Give them an example, a story, a situation. Make them believe that what you have done before, you can do for them.

■ At the end of your fourth week, you should know all the items that are required of a listing agent. Now it’s time to apply.

DAYS 31 THROUGH 60 (PERSEVERE)

Week Five:

- Apply. Apply Apply. Apply everywhere (see Appendix B).

■ Spend time with the application questions. Don’t just respond the same for each application. Each bank is different. Each has different needs. Research their needs before completing the application.

■ Think through each response, re-read Chapter 2, and then complete the responses.

■ If you are applying online, be sure to include a print-out of your application along with your polished résumé and a polished proposal, and mail it to the bank that you are applying to.

Week Six:

■ Focus on the one. Just one asset manager, one bank, or one institution.

■ Go through your progress from weeks one through five. Which asset manager responded best to your REO FARM Play? Who was the most motivated? Who do you have the most likely chance of getting in with?

■ Once you choose the one you will most likely have success with, follow through. Go back to the REO Lunch Method. Bring out their motivation again and show them that you can solve their problems by using the REO Lunch Method and doing FREE BPOs. You can even find an aged property that they are managing that has been listed for more than ninety days. Either way, give them the free lunch and watch how they reciprocate with a listing!

■ Ask for the business. Tell them about your guarantee (from your résumé). Remember, they have nothing to lose.

Week Seven:

■ Re-read Chapter 5 and then perfect the second opinion BPO. You have to show your asset manager that you know what it takes to get the property sold.

Week Eight:

■ Submit your second opinion BPO and follow up with your asset manager using Double Ds (Chapter 9). Remind them about your large buyer network. Let them know that you took home buyers on a bus tour. Show them the pictures. Let them know the feedback from the buyers. Show them that you know what it takes to get the property sold.

DAYS 61 THROUGH 90 (CLOSE)

Week Nine:

■ Send a handwritten thank-you card to the asset manager you are targeting. Thank them for allowing you to do a second opinion BPO.

■ Follow through with your proposed magnet marketing plan (Chapter 7) for that property.

■ Strike when the iron is hot. Ask for the listing. Ask them to reassign the listing you did a second opinion BPO on. Show the asset manager that you can execute. Ask them for the opportunity and then prove your worth.

Week Ten:

■ Re-read Chapters 4 through 9 from this book.

■ Master the six steps of the REO cycle and execute. You need to know exactly what the banks are looking for. Remember, banks will test you out on one. You have one shot to shine.

Week Eleven:

■ Take the re-assigned property from “active” to “pending sale” on the MLS by the end of the week by sending the reassigned REO to your large buyers list. Implement the magnet marketing plan.

■ Follow up with Double Ds and manage the title company and lender (if any) until the transaction closes.

■ Show off your performance to the asset manager and let them know that you have what it takes and that you are dedicated to making sure that they meet their own goals.

■ Remind them again about your magnet marketing plan and go back to the REO Lunch Method. The asset manager has nothing to lose by you performing a second opinion BPO. In fact, if you are successful with the first one, you may end up with a new assignment without having to implement the REO Lunch Method again.

Week Twelve:

■ Follow up with your asset manager and show them that you are hungry and ready for more. Highlight your performance by showcasing your stats (the eight successful measurement tools).

■ Once you have successfully closed ten REOs (90/10 Rule), transition into the REO Bootstrap Model and begin forming your dream team.

■ Grow your business. Re-read this entire book to learn how to maximize your income using the REO Bootstrap Model and prepare to expand to the REO Plus Model.

Congratulations!

POINTS TO REMEMBER

Download your free 90-day action plan from reoboom.com, print it out, and take action today.

- Trim the fat by keeping an eye on your fixed expenses: advertising and rent. Never exceed 1 percent of your GCI on advertising and always make sure your lease is flexible with a sixty-day escape clause; sign a confidentiality agreement if you have to.

- Cash flow is more important to look at than your bottom line profits. If you run out of bankroll, then you will be out of business. Without gas in your car you will not win the race no matter how fast your car is.

- An agent’s scorecard is a chance for you to make the bank’s “A” list, as it compares you to your competition.

- You cannot manage what you do not measure. Use the eight critical success tools to show off with your asset manager, but also to stay proactive with your business rather than reactive.

- The eight critical success tool benchmarks are: CRP and DTC greater than 70 percent, DOM less than 30 percent, RR less than or equal to two, GEP 95 percent or higher, PAP greater than 90 percent, and AIP less than or equal to 10 percent.

- You are only as good as your team. Find VIP leaders—leaders who demonstrate vision, influence, and passion. After you find them, empower them.

- Put your business on autopilot by focusing “on” your business instead of “in” your business. Do this by bringing on your closer (business development role) and your executioner (account manager role). Remember, only one closer and multiple account managers. Motivate them by offering a quarter of one percent (0.25 percent) from the listing commission residually on each REO transaction that closes.

- Grow your REO Plus Model by following the Million-Dollar REO Blueprint. All it takes is three direct accounts to make a million dollars net; only nine new BPO assignments a week.

- Banks need you. They need your expertise, systems, and team (intangible assets) to help solve their pain. The demand is overwhelming. REO mafias are a myth. Banks are opening up the doors for those who truly want it. The time to seize the opportunity is now.

- Growing your business and making a million in twenty-four months is easy. All you need to do is follow a formula, a blueprint. As long as you have passion, dedication, and faith you will be unstoppable. Remember, it’s a science, but not rocket science.