![]()

Conducting the Perfect BPO

THE PERFECT BROKER PRICE OPINION (BPO)

I remember when I first learned about BPOs. I had no idea what it was. One person told me it stood for “best price obtainable.” Someone else told me a BPO is only used for short sales. After several months, I realized that BPO stands for “Broker Price Opinion” and it was one of the biggest assignments I ever had. It was tough. On my first BPO, I spent two nights back to back changing and revising, thinking out loud, “What does the bank want to see?” I had no idea. I was scared, but at the same time, I was excited.

The broker’s price opinion is used by the bank as a resource to determine the list price of the property. Banks want to maximize the sales price for a property, but at the same time, they don’t want to be priced out of the market. In a market where prices are going down, not having the optimal price the first time around can lead to a series of price cuts in order for the property to get sold.

This is what the banks don’t want. They don’t want the property to be priced too high, or they will have to slash and burn the list price in order to get an offer. They also don’t want to price their home too low. The broker’s price opinion is not just your opinion on the value of the home. It’s more than that.

The BPO is one of the most important assignments that you will complete. You must be accurate and detailed. Remember, you are not an appraiser, but you need to give your opinion on the value of the property. You are the expert in your area. The banks trust your expertise.

The BPO that you complete is a direct representation of your ability to successfully sell a home for the bank. How else would you be able to sell a home without knowing its true valuation? Always check your BPO twice before uploading it to your bank’s platform; there is zero room for error.

In your BPO, you will determine the as-is and repaired value of the property, recommend a marketing strategy for pricing to the bank based on the target buyer, outline and comment on repairs and suggested repair inspections, and present extensive photos that show completed repairs, potential liabilities, and a detailed representation of the interior home.

After completing about a thousand BPOs, I finally understood how to perfect them. In the beginning, when I first started doing BPOs, my only concern was choosing the best comparable property (comps) and pinpointing the correct values. Then, after a while, I started to focus more on the repairs and marketing strategy part of the BPO. Finally, I was able to put it all together to complete the perfect BPO. It’s actually an easy process; I’ll walk you through it step-by-step.

![]() INSIDER TIP

INSIDER TIP

Never try to lowball a BPO. Banks want to maximize the sales price from each asset without being priced out of the market. However, keep in mind that banks will order a state certified appraisal for the property to compare your valuation with. If your valuation differs substantially from the appraised valuation, that raises a big red flag.

YOUR BPO PICTURES

When I first started doing BPOs, I was not efficient. I was not taught how to do a perfect BPO, so I made mistakes, learned, made more mistakes, and finally got it right. I remember when I first started I would have to make five trips to the subject property (my REO) because I would always forget to do something. For example, I forgot to take a picture of the breaker panel open, so I went back. Or I forgot to take a picture of the street view, so I went back again. Finally, I learned it because I became more efficient. I found a way to do the perfect BPO without having to worry about making mistakes or forgetting something.

The first tool you need when conducting your BPO is a good camera. You need a digital camera, wide angle or lens, 35 mm, with a zoom and date-stamp feature. When you stand in the corner of a room, for example, only a wide lens camera will allow you to capture the depth of the room. The flash on the camera must be bright. However, don’t simply rely on your flash. You must have good lighting throughout the home—this is part of the reason it’s so important to have the utilities turned on. Expect to take about fifty pictures per property, if not more. If you think you’ve taken enough, take some more. Look at every detail.

Pretend the bank is in a foreign country and it wants to know every single detail about the property, from the color of the roses in the front lawn to the dust in the corners of the garage. It wants photos of everything. If your REO has three bedrooms and two and a half baths, you must take pictures of each room, including the extra half-bath. If you see a dead rat, rodents, a green pool with mold (pools must be blue), or a beehive, take a picture of it. Remember the “model” story from Chapter 4? Well, once that condo was vacant, guess what I found lying around everywhere? Used condoms. Yes, I took a picture of them.

When you first go to the property, take as many photos as you can. Then when you go home you can choose which ones you want to include in the BPO. It’s better to be safe than sorry. The three photos I most frequently see missing from new REO agents’ BPOs are:

- Breaker box (with electrical box open to view breaker switches)

- AC/internal air handlers for condos (sometimes they are located in the attic or ceiling compartment)

- Water heater (sometimes one water heater can be for the entire floor in a condo)

![]() INSIDER TIP

INSIDER TIP

Tankless water heaters are now becoming popular in homes, so look out for them and make sure to get a photograph.

Your pictures should also have a clear transition. For example, don’t take a picture of the balcony view after taking a picture of the living room, especially when you still have to include the family room. The goal with your BPO pictures is to story-tell. Start with the front lawn, then take a picture of the front door, then the living room, and work your way to the backyard.

If an asset manager is sitting in a different state or even a different country for that matter, they must be able to envision walking through the house and feeling the wood on the floor through your pictures. You must be a storyteller.

THE GOAL WITH YOUR BPO PICTURES IS TO STORYTELL

Pictures should be bright and clear. Do not include pictures that are blurry. If you need to go back to the property, go back—it’s OK. In the beginning, you may feel nervous and forget a couple of things. It’s normal; it happens all the time.

When taking pictures of rooms, you want to show the depth of the room, so open up all the closets, cabinetry, doors, etc. Stand in at least two corners of the room and take a picture of the entire room. Make sure the blinds are open; otherwise it will look like you are taking the pictures in a rush.

When you take pictures in the kitchen, include a separate picture of each appliance. This is important, because if the appliances get stolen in the future, you know exactly what replacements are necessary. Also, open the refrigerator, microwave, and oven doors, as well as the cabinets, to show the depth of the kitchen, cabinetry, and appliances.

Always include a picture of the breaker panel, thermostat, interior and exterior air conditioner units, water heater, and any other detailed aspects of the home. Personal property (e.g., left behind furniture) pictures should be taken and included at the end of the BPO pictures section with captions that illustrate the estimated value of the personal property. When determining the value of personal property, always take into consideration the garage sale value, not fair market price that you could sell the items for on eBay. Usually, the price is twenty-five cents on the dollar of what you can buy at a furniture store.

Don’t forget to take multiple pictures of the street views, so the asset manager can get an idea of the curb appeal and level of traffic that may or may not affect the value of the property. Stand in front of the driveway and face all directions (north, south, east, west). Think of yourself as a professional photographer, and your REO is the model. It’s better to take a hundred photos than to drive back to the property because you forgot one or two.

In your BPO, you will be recommending repairs. Therefore, it is crucial to include pictures for every repair that you recommend. Also, banks are huge on liability issues. Anything you see that screams “law suit” must be shot and labeled clearly. For example, a pool without a cage or cover poses a huge liability issue if a family views the home and brings their children—the children could fall in and drown. Think of it as if you were doing a final walk-through for a home buyer. What would you see that you would want to get replaced for your customer?

Finally, you must take pictures of your competing (comps) properties and active (actives) properties. You will have three comps and three actives in your BPO. Do not just download a picture from the MLS. Physically drive to all six properties and shoot the front door. Your comps and actives should all be within a half-mile radius. We have included a BPO Photo Checklist for you to print out and take with you in the field (see Appendix S).

BPO PHOTO CHECKLIST

![]() Exterior front

Exterior front

![]() Rear view

Rear view

![]() Steeet view (multiple views)

Steeet view (multiple views)

![]() Picture of the street intersection

Picture of the street intersection

![]() Picture of any highways or commercial buildings that are in direct view from subject

Picture of any highways or commercial buildings that are in direct view from subject

![]() Entrance view

Entrance view

![]() At least two pictures of every room (bathroom and bedrooms)

At least two pictures of every room (bathroom and bedrooms)

![]() Picture of balcony and/or door leading to balcony

Picture of balcony and/or door leading to balcony

![]() Picture of balcony view (left, middle, right)

Picture of balcony view (left, middle, right)

![]() Backyard

Backyard

![]() Interior AC handler

Interior AC handler

![]() External AC unit

External AC unit

![]() Water heater

Water heater

![]() Breaker panel

Breaker panel

![]() At least two pictures of every area (dining area, living area, etc.)

At least two pictures of every area (dining area, living area, etc.)

![]() At least two pictures of the kitchen

At least two pictures of the kitchen

![]() Picture of each appliance

Picture of each appliance

![]() Washer and dryer

Washer and dryer

![]() Breakfast nook

Breakfast nook

![]() Den

Den

![]() Stairs

Stairs

![]() Electrical meter

Electrical meter

![]() Any damage to the property

Any damage to the property

![]() Include a picture for each repair you recommend

Include a picture for each repair you recommend

![]() Pictures of the warning signs you have placed around the property

Pictures of the warning signs you have placed around the property

![]() Pictures of all three comparable closed sales

Pictures of all three comparable closed sales

![]() Picture of all three competitive listings

Picture of all three competitive listings

![]() Picture of personal property—added to the end with estimated garage sale value of each item

Picture of personal property—added to the end with estimated garage sale value of each item

After you have taken all the pictures, you will have to go home and choose the ones to present with your BPO. But first, reduce the file size of the pictures. The last thing you want is to upload all these pictures and then realize that the size of the BPO is too large to upload. You can find a free resizer software program online by searching Google.

When you finally do upload, make sure all your pictures are right side up. Your goal should be to turn around a BPO within forty-eight hours, regardless of whether the bank gives you more time. Some banks can give you up to seven days, and some will only give you forty-eight hours.

Also, always remember to include three pictures per page. Do not submit a BPO with a blank picture or blank white space. This looks like you put in only minimal effort. If you are stuck, re-use an exterior front picture to fill up the page.

The BPO is composed of different sections, all of which tie in together to give the bank as much information as possible on the property, its value, your recommended marketing price strategy, and ultimately what you plan to do to take the asset from its initial state to a successful sale.

When filling out the BPO, you will need forms that are consistent with your bank. Usually your bank will provide you with the forms or will direct you to use “forms software.” We have included some different software providers in Appendix A so you can shop around.

Also, we have included a sample BPO form (Appendix K) that you can follow along with in each section. For a free download, please visit reoboom.com. Note, each bank and BPO form is different. Therefore, we go over the most important sections in all BPO forms, not any particular ones. Now with that being said, let’s start with the first section: Client and General Information.

BPO SECTION 1: CLIENT AND GENERAL INFO

The first section contains pertinent information related to the property or asset you are valuing. Please remember the following when filling out section one:

- Make sure the REO ID number is 100 percent accurate. For example, do not confuse 0 with O. Always copy this ID from your original assignment letter, then paste it onto your BPO form.

- The asset manager’s name must be 100 percent spelled correctly. Do not insult your asset manager by not knowing how to spell his or her name.

- Completion Date: Aim to have this date no later than forty-eight hours from your initial assignment. DO NOT put a completion date prior to your assignment date; this is a big red flag.

- Remember to indicate which BPO you are completing; this is especially important when conducting an “updated BPO.” If you are doing an updated BPO or second BPO (remember the REO Lunch Method strategy from Chapter 2?), then switch the box from “initial” to “updated.”

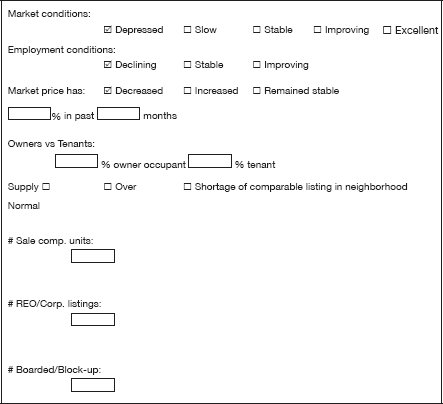

BPO SECTION 2: GENERAL MARKET CONDITIONS

The second section deals with the details on the general market conditions in which the subject property is located. These are the general conditions that may affect how you would currently market the property. The bank wants to know the general market trends in the neighborhood for which the subject is located.

- In today’s economy, most of the time the market condition will be “depressed.” This is good for you.

- Employment conditions will usually be “declining.” I believe we are at a national unemployment level of 9 percent as of the middle of 2011.

- Market price usually shows “decreased.” To determine what percentage the price has decreased, compare the difference of the tax assessed value for the subject in the past year (i.e., tax assessed value one year ago to the tax assessed value this year) divided by the tax assessed value one year ago.

Example:

2011 tax assessed value = $100,000

2012 tax assessed value = $85,000

Difference = $15,000

Divided by previous Year’s value ($15,000/$100,000) = 15% loss

- Calculate what percentage of tenants and owners reside in the neighborhood. Most MLS have functions that provide this information automatically. If your local MLS does not, consider looking at the sales versus rentals in the past twelve months for the neighborhood. Most likely, there will be a greater percentage of owners to tenants in the neighborhood.

- Calculate the supply of competitive listings (active and pending sales).

Normal Supply = 6 to 50 (Needs marketing updates every 25 days, if still on market. We discuss this in Chapter 7.) Over Supply = 51 + (Need to prevent overexposure to market, differentiate asset through repairs, marketing strategy, etc.) Shortage Supply = 0 to 5 (Can be priced with a longer time frame such as a 120-day marketing time period and can be sold “as-is.”) How many total competitive listings? Of which, how many are REOs? The more competitive the REO listings, the more attention you should pay to your marketing strategy/recommendation. How many are boarded up? Look at MLS pictures for listings to determine this.

Normal Supply = 6 to 50 (Needs marketing updates every 25 days, if still on market. We discuss this in Chapter 7.) Over Supply = 51 + (Need to prevent overexposure to market, differentiate asset through repairs, marketing strategy, etc.) Shortage Supply = 0 to 5 (Can be priced with a longer time frame such as a 120-day marketing time period and can be sold “as-is.”) How many total competitive listings? Of which, how many are REOs? The more competitive the REO listings, the more attention you should pay to your marketing strategy/recommendation. How many are boarded up? Look at MLS pictures for listings to determine this.

![]() INSIDER TIP

INSIDER TIP

Be sure that the supply of properties (normal, over, or shortage) does not conflict with the number of comparable listings.

BPO SECTION 3: YOUR SUBJECT PROPERTY

This section deals with your REO property (also called the “subject property”) and the general marketability of it. Components include how the subject property compares to other comparable properties, financing types available for the property, when the property was last listed for sale, and what, if any, reasons there are for its failure to sell, the type of property (e.g., condo, single family home, duplex, etc.), and the Homeowner’s Association information. Below are some important tips to consider while you are filling out this section:

- Range of values should be the range of closed comparable sales.

- Subject’s improvement: usually marked as “appropriate” unless subject is much superior or much inferior in quality relative to the comps.

- Average marketing time: Take the average of the days on market (DOM) for the closed comparable sales in the last six months. Use the three comps you will use for the BPO.

- Indicate if subject has been on market for the last twelve months and under what category (as a short sale, conventional sale, etc.). Also, was it listed by another broker? If subject was on property, indicate why didn’t it sell (i.e., it was over-priced, not repaired, not marketed appropriately).

- What types of financing are available? Please note here if subject does not qualify for FHA (Federal Housing Administration mortgage insurance backed mortgage loan) due to the community not being approved or if repairs are needed to make it conform to lending requirements. Typically, FHA loans apply to those properties that are in habitable condition. Also, if subject is a condo, is the current master insurance policy up to date?

- Unit type: Look at the tax records to determine if subject is single family detached versus attached (i.e., zero lot and block), multi-family, condo, co-op, mobile home (include mobile home serial number in comments and take a photo), condotel (condo that is operated as a hotel), townhome, modular, or other.

- Specify the accurate HOA/condo fee. Call the HOA and/or condo and ask:

What is the current monthly/quarterly fee for your unit? What does this fee cover? Are there any other associations that govern the subject? What are their fees? Include the phone number for the condo you just called. This will be used by many parties to communicate with the HOA/Condo. Verify that the phone number works before entering it into your BPO.

![]() INSIDER TIP

INSIDER TIP

Do not go on the MLS to find out the fee based on what other agents have put in the MLS. Always call and verify the current fee(s) for your subject property. Include the name of the contact person in addition to the name of the HOA/condo.

BPO SECTION 4: YOUR COMPETITION

Competitive Sold Properties (Comps)

This section deals with inputting data from three comparable closed sales. You will find your comps on the MLS. The key is to compare apples to apples. The best comparables are those that are most similar, most recent, and have a reasonable amount of days on market. Usually, when the DOM is very low, it is likely that the property was priced too low. However, to determine if this is true, you would have to look at the spread in list price versus sales price of these low DOM properties.

![]() INSIDER TIP

INSIDER TIP

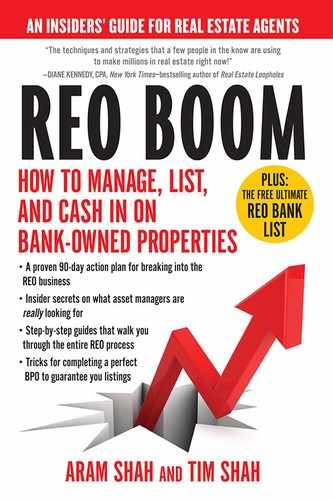

Choose the most recent and most comparable sales (must have been sold in last six months and within a half-mile radius of subject). If the comps you select are not within these guidelines, you must make a comment stating so.

Here are some guidelines to follow when choosing comps:

- Your local MLS will have various ways for you to find the best comps. In many cities, your local MLS will have a feature for you to draw a radius around your subject property. It’s best to use a half-mile circle radius.

- Choose comps with similar conditions.

- Address: Enter each address with correct state abbreviation. The three comparable sales should be located in the same building as subject (if a condo) or at least located in same subdivision if a house.

- Proximity: Choose to write in distance per miles or blocks. If the comps are in the same building, write “same bldg;” if they are in the same subdivision, write “same sdev.”

- Place a check mark in each of the comps that were REOs.

- Write the sales price for each of the three comps.

- Price/Gross Living Area (GLA): This is automatically calculated after you enter the GLA and sales price for each of the comps. If not, simply divide each sales price by the respective gross living area.

- Data Source: Include the MLS number.

- Sale Date and DOM: Sales date should be the closing date (some MLS refer to this as “CD”). Days on market should be calculated as the total days on market from the initial listing date to the sales date. Some agents may have expired listings that they have to relist, and thus DOM can be misinterpreted if you don’t manually verify the days on market. Always double check DOM to ensure accurate figures.

![]() INSIDER TIP

INSIDER TIP

When verifying the sales price, look in the tax records, not the MLS, as the MLS may not always be accurate. Garbage in is garbage out. Always double check to validate your figures.

Making Adjustments

Before moving on to your marketing pricing strategy (Section 5), I want to discuss making “adjustments” to your comps to match your subject. Adjustments are needed to compensate for differences of features between your comps and your REO home. Remember, your subject property is the base or standard. Therefore, you will be adjusting the value of the comparable sales to reflect the standard. Never, under any circumstances, make adjustments to your subject property. Think of it as a finished statue. Here are the two basic adjustment rules:

Rule #1: If your comparable sale includes a superior quality, then a negative adjustment is required.

Rule #2: If your comparable sale includes an inferior quality, then a positive adjustment is required.

I included some typical adjustments items you will see when conducting your BPO:

- Sales or Financing Concessions: If the comparable sale included any seller contributions, make a negative adjustment for that amount.

- Location: All comparable sales should be in the same location; thus this field should be the same for all properties. Select: Suburban, Rural, Resort, Rural Sub, Downtown, Urban, etc.

- Site: Indicate size of the lot in terms of acres. You can also use square feet. Remember to be consistent across all comparable sales and competitive listings when choosing how to specify site. For condos, include the percentage of ownership to common elements.

- View: Very important for high rise, lake homes, and units where view is a major component of the homebuyer’s decision to purchase one unit versus another unit in the same subdivision/condo. Always check the comparable sales listing and photos. Do not just rely on the listing remarks. Verify with the photos that the comparable sale has the view it claimed in the listing. When in doubt, err on the side of conservativeness. Carefully determine how much of an adjustment you are providing to “view.” Guideline: Keep the view adjustment within 10 percent of the competitive sale’s price.

- Design/Appeal: Indicate whether it is one story, two story, split level, etc. Try to use comparable sales of the same design/appeal. If you know your home is two stories, look for two-story comparable sales from the beginning. Don’t get to this point only to realize, “Oh, this is a one-story home.”

- Quality of Construction: Indicate type and quality of construction. For example, concrete block structures (CBS)/typical, stucco/wood-frame, etc. Try to compare CBS construction homes to CBS construction homes.

- Age versus Year Built: Be sure you input what the required field is asking. Note that age is the number of years since the subject was originally constructed, while year built is the exact year the property was built. Do not confuse the two.

- Condition:

Poor: Boarded up, uninhabitable, hazardous conditions, severe structural damage. Fair: Habitable but not well maintained. Average: Generally well maintained, no updates visible in interior or exterior. Good: Improvements to property including roof, interior, exterior. Very well maintained. Excellent: Excellent workmanship and all major facets of home updated. Visually above par from exterior and interior.

- Room Count:

Total: include living room, dining room, kitchen, bedrooms, bathrooms, etc. Bedrooms: Include total number of bedrooms. Bathrooms: Include total number of bathrooms (use .5 to add half bathrooms).

- Gross Living Area:

Include the total gross living area. Be consistent. Always compare GLA to GLA.

- Functional Utility:

Described as “good,” “typical,” “average,” “excellent.” Most comparables should have the same functional utility as subject.

- Heating/Cooling:

Describe the heating and cooling. For example, central heating and cooling (CHAC) that runs on electricity versus CHAC running on gas, window air conditioner, base board electric, etc.

- Energy Efficient Items: Is there a tankless water heater? Include it.

- Garage/Carport: Include if property has a carport or a single/double/triple car garage; if the property is a condo, how many parking spaces, detached or attached garage?

- Pool/Fence: Indicate which comparable sales have a pool or fence and adjust accordingly.

It is very important to never double adjust. For example, if you are adjusting for square footage and adjusting for bed and bath, make sure that the additional adjustment is valid and necessary. Most often, an adjustment for interior square footage encompasses adjustments for bed and bath.

Below are some common maximum adjustments you can make to your comps. I have included a full chart in Appendix M, or feel free to download a free chart from reoboom.com.

COMMON ADJUSTMENTS

Competitive Listings (Actives)

The competing active listings are similar to your sold comps but require you to input data on the properties that are listed for sale. This gives you a better understanding of the competition you will face when you do, in fact, list the property for sale. Knowing what other properties are listed for is extremely important. Words of caution: Some properties are listed at very high prices and have been on the market for a while. It is important to find properties that have a reasonable amount of days on the market.

Follow the same guidelines for closed sales (comps) as you would for actives. Note: If you are having a difficult time finding comparable active listings, you may also use “pending sales,” but this must be disclosed in the comments section of your BPO.

BPO SECTION 5: YOUR REPAIR STRATEGY

In the repair section, you will list the necessary repairs for the property. Even if you do not recommend doing certain repairs, you should still list them so your asset manager knows what could be done.

In addition to listing the repairs, you will estimate the cost of repairs. Finally, if you are recommending repairing the items, be sure to place a checkmark on each repair you are recommending for the bank to complete. Typically, you should not include regular maintenance as part of the repairs, since these items will automatically be addressed by the cleaning company.

It is critical to include a picture for every repair that you are recommending. The asset manager needs to see to what extent the repairs you mention are necessary. You also want to include any type of inspection that you recommend, including termite, roof, structural HVAC, etc.

I have included some general benchmarks for you to use. See Appendix M for a full list of repairs.

- Carpet replacement can be estimated at .75 × Adj. Sq. Ft.

- Interior paint can be estimated at 1.5 × Adj. Sq. Ft.

- Water heater can be estimated at $450

- Appliances can be estimated at $600

- Interior and Exterior AC units can be estimated at $3,500

Many agents prefer to recommend interior paint and new carpets (if applicable) at the very minimum. The rationale is that the cost of interior paint and carpet replacement is so nominal that it is worth the extra marketability it brings. Remember to target your recommended repairs to your target buyer (home owner or investor).

If targeting homeowners, think neutrality. You don’t want to reduce the marketability of your subject by having bold colors in the home. If the colors aren’t neutral, recommend re-painting the interior. Also, consider the time involved. If you are recommending any repairs such as interior paint, you may as well recommend carpet replacement.

If your target buyer is an investor, you may recommend an as-is strategy, because investors usually have their own contractors and their own way of doing repairs.

BPO SECTION 6: YOUR MARKET

PRICING STRATEGY

In the market pricing strategy section, you are recommending the best way to sell your REO. Should you complete repairs? Or should you sell it as-is? Who is the target buyer (home owner or investor)? Who is the most likely buyer? Will the cost of repairs be outweighed by the return from the additional spread in sales price? If so, to what extent?

Think about all these factors when you choose which marketing strategy to recommend. If you are recommending doing repairs, verify that the cost of repairing your subject property is outweighed by the increased value, less the cost of keeping the property off the market for the time it takes to complete the repairs.

For example, let’s assume you have:

As-Is Value: $100,000

Cost of Repairs: $5,000

Time to Do Repair (est. at $1,000/day): 5 days

As-Repaired Value: $115,000

In this case, it is a good idea to recommend repairs, because by doing $5,000 of repairs, you are increasing the value of the home by $15,000, a difference of $10,000 that required only five days of time.

On the contrary, let’s assume you have:

As-Is Value: $100,000

Cost of Repairs: $5,000

Time to Do Repair (est. at $1,000/day): 5 days

As-Repaired Value: $102,500

In this case, it will not be a good idea to recommend repairs, because by doing $5,000 of repairs, you are increasing the value of the home by $2,500, plus losing an additional five days that could have been used to market the property.

There are eight factors indicating that the most likely customer of your REO will be an investor:

- Excessive repairs are needed.

- Subject property has several liens.

- There is no financing available.

- Condo or townhome does not have a master insurance policy.

- Subject property is in an area that is predominantly tenant occupied.

- Subject has two or more illegal units.

- Subject is currently occupied and the purchaser is responsible for removing occupants.

- Cost of repairs does not outweigh the difference in what a homeowner versus an investor would pay.

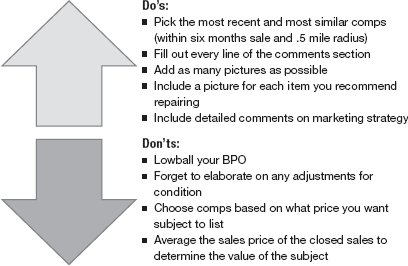

Most BPOs will require that you insert the “as-is” and “repaired” market value, and, in addition, the “suggested listing price.” Remember that competitive active listings do not have a strong indication of value because those properties have not sold. Closed comps, on the other hand, give you a better indication of what the market is willing to pay for similar properties. In the market value comments section, you must include why you recommend to market the property “as-is” or “repaired.” You have to state your case.

![]() INSIDER TIP

INSIDER TIP

Make sure your BPO value is in line with the adjusted market value of comparable closed sales.

Some common reasons for marketing “as-is” are: very little repairs are required, the increase from value of repairs is not outweighed by costs, and the subject property is in a high demand area. Similarly, some common reasons for marketing the REO as “repaired” are that financing will require repairs, and the marginal difference between the additional sales price and cost of repairs is worth the time investment to complete the repairs.

BPO SECTION 7: FINAL COMMENTS

When I first started, I used to take four hours to complete a BPO. After doing hundreds of BPOs, it now takes me less than an hour for a condo or a townhome and less than an hour and a half for a single family home. This does not include the time spent inspecting and taking pictures of the REO. What takes me under an hour and a half to complete takes an asset manager less than a minute and a half to review. The first thing they glance at is the opinion of value, followed by the comments section.

In the comments section, you should include which of the properties were “short sales” versus “conventional sales” versus “REOs.” It is important to realize that comparing an REO to an REO is better than comparing an REO to a short sale. To put it another way, if you are doing a BPO on a condo, and there is a similar unit in the same building that is an REO, when selling agents show your unit, they will compare it to the other REO.

So, your property must have a differential advantage, either in price or marketability. Use the comments section to include comments that aren’t otherwise explicit in the BPO. Try not to be redundant, and use the section to make comments on items that can’t be found by reading the data of your BPO. Some key components of your comments section are:

- Speak about which comparable you gave the most weight to in order to come up with your final valuation.

- Mention why your marketing strategy (as-is or repaired) is best to reach your target buyer (homeowner or investor).

- Speak about the competition. Is there a surplus of competitive listings? What does the asset manager need to know that can’t be seen from the data?

- Speak about the return on repairs, if you recommend repairs. What type of return (in the form of increased sales price) will repairs bring?

- Note the days on market of your competitive sales, and how those days and marketing strategies affect your bank’s marketing strategy. For example, some banks want to market an REO for sixty to ninety days. Refer back to the closed sales and their marketing strategies to infer which marketing strategy will work best for the subject.

- Mention any other market specific comments, such as location, economic justification on marketing strategy, and demand factors.

PUTTING IT ALL TOGETHER

As you can see, the BPO is just more than an opinion of value. It includes many points: details on the subject property (your REO), nature of the competition as a whole and specific comparable listings and sales, the best marketing strategy to target the most likely buyer, repairs that are needed versus repairs that are recommended, and factors that support your price and marketing strategy given the specific guidelines of the bank.

Some say that the BPO is the most important part of the REO cycle. An asset manager can tell a good BPO from a poor BPO right away. A good BPO will not look like it was done in a rush; rather, it will be detailed and have valid points and fundamental elements as described earlier. As the bank’s REO listing agent, you should strive to impress your asset manager by mastering the BPO elements in this chapter. You should be visualizing the best way to market the property to maximize the sales price for the bank. It’s important to understand that REOs do not compete only on price.

In my history of selling REOs, I’d say about 75 percent of them went through repairs. Because of the way I marketed the repairs, and how I used our marketing strengths to advertise how my REOs were superior to the competitive REOs, it was very easy and worthwhile to justify doing repairs.

In fact, I realized that many of the deals that went through were because of my ability to speak to a cooperating agent or homebuyer and tell them about how we repaired the property and how it was in “move-in condition.” To attract the most buyers and the best offers, you need to know how to leverage the repairs that you’ve done to magnify your marketing. But before I delve into the marketing madness, let’s learn how to manager repairs and inspections, which is Step 3 of the REO cycle.

![]() SHARE YOUR STORY

SHARE YOUR STORY

Do you have a success story you’d like to share about conducting your first BPO? Any wild pictures you took or adjustments you made? Please log on and submit it for your chance to be featured in the next revised edition of REO Boom:

POINTS TO REMEMBER

- Make sure your final BPO value is in line with your closed comps.

- When making adjustments if your comps are superior, adjust downwards, and if your comps are inferior adjust upwards. Never make adjustments to your subject property.

- Use comparables in the same building/subdivision as frequently as possible.

- Look at the condition of the comparable by going through the MLS pictures, calling up the listing agent, searching tax records, and noting these remarks in the comments section of your BPO.

- Every recommended repair must have a photo showing the repair needed.

- Your turnaround time on BPOs should be no more than forty-eight hours.

- Make sure the electricity is on when you do your BPO so you can include pictures of the interior with lighted background.

- The meat of the BPO is the comps, and the potatoes are the photos. Choose the best comps and make sure your photos are detailed, clean, and organized.