![]()

DOUBLE/TRIPLE/QUADRUPLE DIPPING!

THE SIX HIDDEN INCOME STREAMS

So you learned how to land the million-dollar REO contract and mastered the six steps in the REO cycle. Now we want to tell you how the seasoned agents make it happen. This is the icing on the cake.

There are seven different streams of income in the REO business. You know the first one. We will now uncover the hidden six.

- Listing commission

- Selling commission

- Financing

- Buyer processing fees

- Home warranty

- Flipping

- Property preservation

When you first start in the business, you will primarily focus on satisfying the seller. You will only care about making sure everything goes perfectly as planned and you will be content with only making the listing side of the commission. It’s natural to feel overwhelmed at first. However, after a couple of months (six to twelve months) you will start seeing hidden opportunities to make additional cash. This chapter is going to shave at least six months off the learning curve for you!

Hidden Stream #1: Selling Commission

If the bread is the listing commissions, then the butter is the selling commissions. It’s the flavor, the 93 octane, the premium gas. In Chapter 2, we discussed how with little to no marketing effort you will, on average, achieve a 35 percent in-house buyer’s ratio. To refresh your memory, this is when you have your own buyer as opposed to a cooperating agent bringing a customer for your listing. To increase this 35 percent ratio to let’s say 50 percent, you need to direct your focus and energy on becoming the selling agent.

Remember, the selling agent is whoever sells the property and brings a buyer. Therefore, start showing properties. Show the potential buyer the property they called you about and other REOs that you have in inventory. If you are set up on the REO Plus Model, then you should be the one focusing on selling to maximize both sides of the commission.

Alternatively, instead of only showing your properties, you can cross-sell other REO listing agent’s properties. If you can’t beat them, join them. Here is how it works. Every buyer who calls in for one of your properties is a potential customer. If they call you for a home that you may have under contract, then your job is to invite them to your office and find them something else in the area on another listing agent’s REO. In essence, you now become the selling agent for another listed REO.

Remember, customers want to work directly with listing agents (you) for two reasons. First, they assume that by working with a listing agent, they are more likely to get their offer accepted, and second, they know that listing agents have experience from the inside so they will be better able to advise them. They are already sold on you.

Instead of saying, “Sorry, there is a contract already on the property you called about but if it falls through I’ll let you know,” jot down their contact information and sell them another listing agent’s REO. Stop throwing away leads; keep a log of customers who call in and cross-sell them.

There are many REOs on the market. Being that you know exactly what to do to get the customer’s offer completed in its entirety in a prompt manner, the chances of you getting your customer’s offer accepted are very large. In fact, many agents still don’t know how to fill out an offer properly, nor do they understand why their offers never get accepted. Remember, you are the listing agent. You are in control. You have the power. Turn those callers into customers. Always be closing.

The Three Lead Buckets: Hot, Warm, and Cold

Unfortunately, out of everyone who calls in, not all of the leads will be ready, willing, and able to actually buy. Therefore, you need to identify the ones who are and act upon them immediately. What I tell my REO agents that I coach is to put leads into three buckets. The first bucket or physical file folder should be labeled “HOT.” The next bucket should be labeled “WARM,” and the final should be labeled “COLD.”

Each lead who calls in should be placed in the respective folders. Some leads may be on the borderline and that is OK, as these folders are not mutually exclusive. The key to increasing your selling side commission (SC) is identifying who the “HOT” leads are and focusing in on them.

Hot Leads

Hot Leads (Ready/Willing/Able)

- Been on the market for more than four months.

- Seen over twenty listings.

- Made at least five offers, all of which have been rejected.

- Need (not want) to purchase by a certain date. E.g., they are relocating or they sold their current home and must find something.

- Has relatives or friends in a certain area who validate where they are looking to buy.

- Does not have an attorney who can destroy the deal. Remember, bank contracts are as-is, so when an attorney looks at it they will find at least five things “wrong” with the contract.

- Has proof of funds to purchase with all cash or to cover the down payment.

- Has a bona-fide pre-approval letter reflecting credit-worthiness.

I would say other than them being able to buy (i.e., #7 or #8), the hot lead having been on the market for more than four months is critical. When buyers first get on the market, their expectations are through the roof. They think because they are financeable or have cash it’s their way or the highway. However, after a couple of months, reality sinks in, especially after they see five or six dream homes slip away because they were too late in presenting an offer or did not want to offer full price for the REO. I have buyers call me and say, “I want this house and I will do whatever it takes. Please help me.” This is a HOT lead!

Warm Leads

Warm leads may not possess all eight criteria of hot leads but are pretty close. They already are pre-approved and have shown you proof of funds for the down payment or the entire purchase price amount if paying cash. However, they are just beginning their house hunting search. They are relatively new to bank-owned properties and are still in the learning phase. They are price sensitive and are reluctant to offer full price for an REO.

What I advise my agents to do is work with these leads but give them homework. For example, ask them to email back exactly what they are looking for and most importantly, why. Remember Chapter 2 when we discussed the REO FARM Play? You always build motivation before talking about the money. I actually say things to discourage them from purchasing to gauge their motivation. For example, “Why this house and not the one next door that’s cheaper?”

The more you say NO to them, the more they will say YES if they are motivated. It’s kind of like dealing with children. If you say no, they want it even more. Many times, I have buyers tell me “Oh, I don’t know we just started looking.” This is music to my ears. The best thing a home buyer can tell you is what bucket they are in—hot, warm, or cold.

Warm Leads

Cold Leads

Cold leads are the ones who just saw a sign while driving, and maybe the wife or the husband told the other, “Hey, call that home and let’s see how much it’s going for.” They had an idea pop into their minds about purchasing and started the curiosity stage. They may still be renting or living with family. They usually have not even begun online research (realtor.com, etc.). They most likely don’t have a pre-approval letter or proof of funds. Some buyers who call me have good reasons, such as “I’m getting married and need to start planning for a house.” Their time frames may be much longer into the future (one year or longer).

So do you turn them down? No. Everyone buys eventually, just like every REO sells. It’s a matter of massaging them into becoming a home buyer. You need to become their trusted advisor. Help them by referring them first to a good mortgage lender who can let you know if they qualify for a home loan or not. If they don’t, you want to make sure the lender can put them into a game plan to eventually purchase. Everyone should own their home. It’s a great feeling. It’s the American way.

Cold Leads

- Just started the curiosity phase.

- Has a time frame of about a year or greater to purchase.

- Has not been pre-approved for a loan yet.

- Looking for a guide/coach to hold their hands.

Whether the leads you get are hot, warm, or cold, you must follow up with them consistently. Put them on an email list and send them weekly newsletters, personal emails, and up-to-date property information. If a lead wants something in a specific neighborhood, make sure you tell them that as soon as a home becomes active and available, they will be the first to know.

One thing that I advise my REO agents to do is set up an exclusive weekly property list. Since they will have two hundred to three hundred properties in inventory but only 10 percent actually “active” with a list price (Chapter 3), the buyers can know what’s coming on the market ahead of time. They can start their due diligence by checking out a home is an area they could see themselves living in. One last thing—make sure you answer every phone call and handle every lead as if they were a hot lead. Everyone eventually buys. It’s just a matter of when. It’s better you close the lead and find them a home than someone else.

![]() INSIDER TIP

INSIDER TIP

By taking advantage of streams #2, #3, and #4, you can make an extra $100,000 a year.

Hidden Stream #2: Financing

Once you are comfortable in the business and you have your dream team ready to go, you need to think about automation and standardization. Remember, we discussed how the REO Plus Model is like an assembly line. The belt is constantly moving into a rainbow with a pot of gold at the end of it. However, if there is nothing on the belt, then your pot will be empty.

So, the first thing you need to do is get your mortgage loan originator license to receive referrals. It’s an incredible return for your investment of time. Take a course, pass the state test, and you will have a license to make money and the skills to sell to your customers.

How many times have you relied on a mortgage professional only to watch your deal fall apart? Well, imagine now quickly explaining to your customer the difference between an FHA, VA, or conventional loan with minimum down payments and what seller contributions can apply.

One of the fastest ways to boost your in-house buyer ratio to exceed 35 percent is to know your mortgage products. You can quickly qualify someone on the phone and know exactly which financing to place them in. Either you can originate the mortgage loan yourself (take the loan application, negotiate, etc.) or you can outsource the lead to a mortgage specialist and receive a referral fee.

Once you receive a buyer lead, assign it to a mortgage specialist, and sit back and let them go to work. Make sure your mortgage specialist is well versed in the business so you don’t get taken for a ride. Remember, you will not be doing the mortgage applications, gathering, documents, etc., for the borrower. You just need the knowledge and the license to legally get a referral fee (if your state allows it).

If you don’t have the time or energy for it, I understand. Handling REOs for banks is very demanding. Your second alternative is to bring someone on to your team who has a mortgage loan originator license. Ask your broker. Maybe someone in your office is recommended that is trustworthy. Once you’re legally allowed to make commission, you want that person to focus on pre-qualifying all of your leads.

Since you are holding all of the cards by being a direct REO agent, you control the work flow. Therefore, a common and customary split is fifty-fifty. Any mortgage professional who is ambitious and diligent will be more than glad to make this arrangement because they will know the value of leads. By offering 50 percent of their pay, they are treating that as an advertising expense for a “warm lead.” It’s a true win-win and easily done. Just make sure you choose someone who has years of experience and is not a fly-by-night affair. This commission split applies to a non-affiliated mortgage partner or someone you bring on your team with a license.

![]() INSIDER TIP

INSIDER TIP

When interviewing your mortgage partner, ask them what they would do if they got a lead that had a credit score of 600 or less. If they say they cannot work with them, move on to the next mortgage partner. You want someone who has the ability to place any lead into a home. Maybe not now, but if they can create a custom work-out plan to follow, eventually that lead will bear fruit.

Once you find your mortgage partner, your job is to have them qualify every single inquiry. Every lead is money. Instruct them to never reject a lead. Have them put the customer on a game plan and help them with their credit. Guide them, and within six months you might have turned a definite no into a yes.

In the REO game, the amount of cash closings and financing closings are pretty even. Sometimes one can outweigh another by 60 percent/40 percent, but usually you’re dead even. From the financed transactions, expect about 30 percent to successfully close per direct bank contract.

PER BANK CONTRACT

50% CASH CLOSINGS

50% FINANCING CLOSINGS

30% WITH YOUR MORTGAGE SPECIALIST

50% REFERRAL FEE

So if you are closing thirty transactions a month per direct bank contract, fifteen will be with financing and four or five of the fifteen (30 percent) should be generating you referral fees. How much is the fee? Usually you can expect about 1 percent of the loan amount. Using the national median home price of $158,800 and assuming a buyer puts 10 percent down, the potential referral fee commission is:

$158,800 × 90% = $142,920 × 1% = $ 1,429

$1,429.00 × 4 closings/mo. × 12mo.

$68,592.00 in Mortgage Referral Fees!

This is just for one direct bank contract. Multiply this by three to five and now you are talking about some serious cash. Even if you only do half of that, it’s still a nice chunk of change and a great return on your mortgage loan originator license. Remember, if you want to make even more money, you can always originate the loans yourself, and instead of receiving only 50 percent of the referral fee, you can keep all of it. Don’t forget to get licensed and check with your state’s laws on whether referral fees are legal or not.

Hidden Stream #3: Buyer Bonus Fees

Many times when you sign your master listing agreement, your contract will have a provision that will prevent you as an REO listing agent from charging your customer a buyer processing fee. It will say something like this: “Under no circumstances shall XYZ Company/Agent/Broker be entitled to any compensation which exceeds the net commission due … Seller shall not be obligated for any additional commissions arising out of co-broker or multiple listing agreements.”

In short, all they will pay you is the standard listing commission of 2.5 percent or 3 percent. If you put a standard “processing fee, storage fee, transaction fee, etc.” like many real estate companies do on the HUD-1 Settlement Statement, the seller will not approve the HUD and will request you to remove the clause.

Therefore, the trick is to have your buyer sign a special clause in your local state or promulgated as-is contract stating they will pay a standard processing fee or “additional commission fee” out of their own pocket to your brokerage company. With this clause, the title company will put the processing fee of $295, $395, $495, etc., on the buyer’s side of the HUD-1.

The clause should read something like: “A standard additional commission fee of $295.00 shall be applied at closing paid for by buyer.”

Every time you have a buyer, you need to make sure you have them agree to the additional commission fee. However, first make sure this is not in violation of the Real Estate Settlement Procedures Act Section (RESPA), or local or state laws.

![]() INSIDER TIP

INSIDER TIP

Make sure you label your processing fee as “commission” instead of “processing” because of a recent judge ruling in the U.S. District Court, Northern District of Alabama, Southern Division (Vicky Busby v. RealtySouth). Also disclose it on the buyer/broker agreement, GFE, and buyer proceeds costs on the HUD-1. Finally, have the title company disclose it on the same line item as the commission on the HUD-1. For example: real estate commission X % and $395.

Here are some fun and realistic numbers to expect within your first twelve to twenty-four months of hidden buyer’s processing fees per direct bank contract:

250 closings × 35% (where you represent your own buyer) × $395.00 = $34,562 in Buyer Bonus Fees!

Hidden Stream #4: Home Warranties

Next is the home warranty plan; every new closing should have a home warranty plan. A standard referral fee is around $75, depending on which company you are working with. Make sure you invest in obtaining your state home warranty license so you can receive referral fees.

Usually, this is run through your state’s department of financial services and allows you to legally receive commissions from companies that provide plans to new home buyers. After you obtain your license, you will want to sign the marketing service agreement with each new home warranty company so you can offer your customers some variety. Per direct bank contract, you can make an additional $6,562 in buyer home warranty fees:

250 closings × 35% (where you represent your own buyer) × $75 = $6,562 in Home Warranty Fees!

Hidden Stream 5: Flipping Your Own Listings

Real Estate Arbitrage

The best thing about being an REO agent is that you get to be involved in the transaction from the initial foreclosure of the original borrower, back to the bank, then to the end buyer. Once you get a good handle of the business (within six months) you will know immediately which deals are bad, which deals are good, and which deals are a steal.

One of the big ways you can make money as an REO agent is by purchasing your own listings. Of course, check your contracts and make sure it is not a conflict of interest with your suppliers. If all signs are a go, a good goal to have is to purchase and resell (i.e., flip) twelve homes in your first year as an REO agent.

If you recall from the REO cycle, after a listing comes into your inventory, your job is to market it and sell it for your bank within ninety days. After ninety days, the listing becomes old or “aged” and that’s when the bank usually sends it to a big auction house company to sell.

Banks have funny ways of accepting offers. Assume you had a listed property and your list price came in at $125,000. You can present an offer to the bank at $105,000 and the bank will most likely reject it. However, 120 days from now you find the same exact property sold for $85,000 at auction. Why? It’s an internal bank guideline. They cannot sell a property for a certain percentage within a certain timeframe, otherwise all the bank asset managers would use a slash and burn mentality just to meet their bonuses.

![]() INSIDER TIP

INSIDER TIP

Banks usually drop the list price 5 to 10 percent every thirty days if they see no movement.

This is excellent news for you. During your ninety-day listing period, you might even have received offers close to full asking price that were rejected by the bank. Usually the buyers who placed offers forget about the home when their offer is rejected and go shopping for another property.

As soon as the listing goes to auction, you have a golden opportunity to purchase the aged property, close on it, and turn around and sell it to any buyers who might have shown interest at a higher price from when you first listed it. For example:

- You listed a property on 6/1/12 at $100,000.

- You received five offers between $80,000 and $96,000, all of which were rejected by your asset manager.

- Property was assigned to an auction company on 9/15/12.

- You buy property at auction for $75,000 on 10/1/12.

- You contact all previous buyers who were interested but had their offers rejected.

- You relist on MLS for $90,000 on 10/15/12.

- You find a new buyer for $87,000 and close by 11/15/12.

- You make a $12,000 profit over 60 days (not including closing costs).

![]() INSIDER TIP

INSIDER TIP

Buy your own listings at auctions after they are aged for a deeper discount.

You tested the demand, you know all the ins and outs of the property, now you just have to go to the auction and purchase it yourself. The best thing about it is that you as an REO listing agent still make money from the listing commission. Usually, they discount all commissions paid to real estate agents to roughly 1 to 2 percent from both the listing side and selling side, but it’s still better than nothing. So you now have an opportunity to bid on a home, pick it up 20 to 30 percent cheaper than when you listed it, and still earn commission from both sides of the transaction.

Sometimes, auction companies will not pay you a selling commission if you represent yourself as a buyer. It’s always a good idea to put your broker at your office, as the broker representing you or another agent, and compensate them with a referral fee of 20 to 30 percent. It’s better than not receiving anything. Also, if you have any family members you will be partnering with and buying the home under, they usually will not pay you a commission. Be wary of this. Auction companies look at relatives and last names closely.

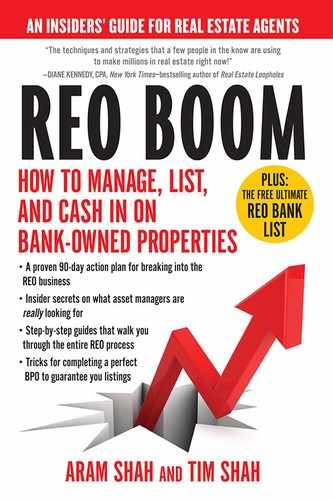

In auctions, some offer a minimum reserve, some allow you to see the highest bid current (like eBay), and some are anonymous. It all depends. The point is, you have an opportunity to participate in some real estate arbitrage by filling the void in the market. The six biggest auction houses where you will be purchasing your homes are:

Visit each one of them and check out the rules and regulations. Since you are already a listing agent for the bank, you will be facilitating the auction company to earn your discounted commission by doing some open houses or whatever else they require (e.g., upload documents, etc.) so you will already be familiar with the process.

STEALING PROPERTIES AT AUCTIONS

I went to a live auction once. It was hosted in a five-star hotel. If you have never attended one, I highly recommend doing so. Think of an auction in a movie or television show, and it is exactly like that. The room was packed with stadium-style seating. It was 7:30 A.M. open registration and the auction started around 8:15 A.M. Upon registering you need to bring your checkbook, proof of funds (i.e., a bank statement showing you have enough funds to purchase), and a cashier’s check for the minimum amount the auction company requires (around $2,500)

If you don’t have time to print out your statements or you didn’t bring them with you, they have work stations in the back with internet connection to facilitate you. Their main goal is nothing more than to sell, sell, and sell. Their business model works like this:

BANKS/DISTRESSED SELLERS

Auction companies solicit different large institutions and offer them a completely free service. Their sales pitch is that they will bring a room full of buyers and sell the bank’s homes. If the properties don’t sell, the banks have nothing to lose. Auction companies make their money from the buyers (you and I). They charge around 5 percent of the winning bid or a minimum amount (e.g., $2,500), whichever is greater.

Therefore, if you win a home for $200,000 your total purchase price will be $210,000. Alternatively, if you are buying a condo and win a bid for $30,000 they will charge you $2,500, making your total purchase price $32,500.

At the auction I attended, the minimum fee was $2,500. After registering, I received a property auction flyer list and an auction number; it looked like a bib number that you attach on your shirt when entering a marathon race. You raise this number up when you are bidding against other buyers in the room.

As I walked in past the registration booths, there were two rooms. The first room was where everyone sat down to bid; it had water stations and cheap chinaware in the back. The second room was a pit filled with dozens of desks and chairs with different employees waiting for winning bidders to come in and sign their life away.

I scanned the room to find a good area to sit and noticed a couple of things. First, the cash buyers and investors who had been to an auction before sat in the front third of the room. They were confident. They knew what they wanted, they were eager, and they were ready to purchase and get out as soon as possible. In contrast, the first-time home buyers and novice purchasers mingled around the back of the first room. Also, in the first room there was a small section with actual desks for buyers to sit down to place laptops on and work from. These were for buyers who purchased multiple properties and thus got the privilege of using a special area.

As I got my seat (in the front, of course), the auction started. There were three or four gentlemen in black tuxedos in the front. They all had beards and some were eccentrically groomed, with a third of their beards white, done intentionally. Behind them on top of the podium were the auctioneers and staff. Everyone was good looking. Everyone was upbeat, and they created a real buyer frenzy atmosphere with motivational money quotes flickering in the background.

By 8:30 A.M. the auctioneer was off. I had never heard someone talk so fast in such little time before. It was as if he had a motor in his mouth. Each property was numbered from 1 to 100. He went through each property, all of which were projected on the big screen behind the podium. What was interesting was they would list the “previously assessed value” from when the property sold two or three years ago while displaying a starting bid. So a property number one would look something like this:

Auction House Features

- Property #1-XYZ, CA

- 3 bedrooms, 2 baths, 2,400 square feet

- Previously valued at $550,000

- Starting bid $35,000

They would pitch every property that went up for auction as if it was the best buy you could ever make, even if it looked like a tornado had hit it. These people were professionals. Some properties that I did research on went for 10 to 20 percent above the actual market value just because people got emotional in the room.

The bidding process was interesting as well. Depending on the purchase price of the home, the auctioneer would start the bidding either at the minimum amount (e.g., $25,000) or start it at $500. They also increased the bid increments randomly while people were bidding depending on the mood of the audience. Some would increase by $2,500 rapidly until the crowd quieted down, and then bid increment would drop. For example:

- Starting bid: $25,000

- Increment 1: $27,500

- Increment 2: $30,000

- Increment 3: $32,500

- Increment 4: $35,000

- Increment 5: $33,750

The reason they had so much control was that the banks had a hidden reserve that wouldn’t be disclosed. Therefore, even if the highest bidder in the room won, they would mumble “subject to seller’s confirmation” underneath their breath right before congratulating the winning buyer.

The bank then would have fifteen days to decide whether or not they would accept the winning bidder’s offer or take the chance of putting it back on the market (with another REO agent or an outsourcing company) hoping for a buyer willing to pay what they wanted. Therefore, not only would you not win the home, you would spend two or three hours at the auction signing contracts and doing paperwork all for nothing.

![]() INSIDER TIP

INSIDER TIP

You will know when the property hasn’t met its reserve when the auctioneer stalls the bidding. He or she may repeat the highest bid (e.g., $33,750) five to ten times and mention how cheap the price per square foot is compared to the replacement costs, or throw out the word “new construction” even if the property was built five years ago. When they throw back-to-back adjectives during the bidding process, you know the property hasn’t met the reserve.

Some properties at the auction were clearly marked “cash only.” That doesn’t mean you need all cash on the spot to purchase, but there was no financing contingency allowed. Because closings are set thirty days out, you would put a deposit and bring the rest to the closing table with the seller’s designated title company. Other properties would be labeled “buyer assumes responsibility of occupancy,” meaning the bank is most likely selling the property with a tenant inside.

This means you will be responsible for starting or completing the eviction process before you can gain access. Remember, the banks will insure clear title, but they may not guarantee the property is vacant. Because auctions are advertised a minimum of thirty days in advance, you have ample time to do some homework. One thing to check for with properties that may have tenants in them is the court docket. Go to your local clerk of court and see if a writ of possession has been executed or not. If it has, then it will be easy for you to enforce the eviction. If not, then it may take you longer.

Hot Auction Properties

- Cash only

- Buyer assumes responsibility of occupancy

The best deals in auctions are when they limit the buying pool. Just by requiring only cash customers, a third of your competition is gone. Then, when they make you evict the tenant (whether you have to or not), another third is eliminated. Now you’re left with a third to compete with. This is how you pick up steals at auctions.

![]() INSIDER TIP

INSIDER TIP

If you do win a property that may be occupied, instead of evicting the tenant, do what the banks do. Knock on the door and offer them money to leave voluntarily. Ask them—would you rather work with me or with a sheriff with a badge and a gun? Ninety percent of the time, they will be grateful you are helping them with moving expenses.

When my number came up on the auction flyer list, I was ready for a bidding war. After the bidding process was over and I won my bid, I was approached by the auction staff and quickly shuffled to the side of the room. It was an assembly line. One person handed me a folder. The next person walked me to a place to verify documents. The third person walked me back to the back room (“the pit”), where I spent about another thirty to forty-five minutes waiting to sign all the relevant documents. As I was waiting, I took a tally of what properties sold for versus what they were previously assessed at.

AUCTION PROPERTIES SELL FOR APPROXIMATELY 50 PERCENT OF THEIR PREVIOUSLY ASSESSED VALUE

On average, I discovered, properties sold for approximately 50 percent of their previously assessed value. So if the auctioneer advertised a property assessed at $550,000 the highest bidder was almost around the $225,000, mark even if the starting bid was $500 or $25,000. Whatever you do, make sure you do all of your homework and due diligence in advance. Auctions are a buying frenzy atmosphere with a lot of emotions in the air. Write down the maximum you are willing to pay and stick to it. Don’t pay a penny more.

As I was wrapping up with the paperwork, one of the staff workers told me two interesting things. First, on average, they sell twenty-five homes per hour—sometimes less if a winning bidder doesn’t have proof of funds, or cashier’s check, or didn’t know it was a cash only purchase, because then the property goes back to the auction, slowing down the process.

Second, he said you could participate in the live auction from home on your computer. I sure wished I had known that before going. But even if I had, I still would have attended the live auction. It was quite a show. I highly recommend it.

AUCTIONS VERSUS LISTINGS

Whether you choose to purchase at auction or just purchase your own REO listings is up to you. Sometimes, you may have so much demand for a house (e.g., thirty phone calls within an hour’s period) that you buy the house for yourself. Of course, you have to disclose if it’s an agent purchase and follow your bank’s rules and regulations, but that is the benefit of being an REO listing agent. You are always one tick ahead.

Some other interesting things to point out: when purchasing through auction companies, their contracts are usually non-negotiable (take it or leave it) and force you to close with their own title companies. Also, forget about assigning properties (i.e., assigning your rights to your end buyer for a quick $5,000 flip), as their contracts always state the property is not assignable. Therefore, you will be forced to close on the first transaction, then put the property back on the market the following day and find an end buyer.

Also, because you will not be allowed to buy with your own title company, you most likely will not be able to do a “double close.” This is where you buy a property and close with the seller (bank) at 10 A.M., and sell the same property and close with your end buyer at 12 P.M., minimizing closing costs and lag time.

One caveat when thinking about buying at auction is to make sure the seller (bank) will issue a clear title and, if the property is a condo, will pay the entire estoppel amount. The last thing you want is to find yourself with a killer deal and be stuck with a $10,000 back-due homeowner association bill that wasn’t paid.

![]() INSIDER TIP

INSIDER TIP

Before closing with the seller’s title company, you will receive a title commitment. Give a copy of this to your own title company to make sure they have no issues clearing the title for you when you sell the property the next day.

THE THREE EXIT STRATEGIES

Depending on your purchasing goals, you will have various exit strategies. Basically, there are three:

- Hold and Rent

- Fix-to-Flip

- Lease to Own

Option #1: Hold & Rent: Twelve Homes in Twelve Months

Your main goal is to purchase homes extremely cheap. What does that mean? The home you buy must be cash flow positive. This means after all taxes, association fees, insurance, mortgage, etc., your bank account is positive every month. With REOs you will have a variety of options. You can purchase a condo, a high-end home, a duplex, a loft, a town-home, etc. Regardless of what it is, you first need to check the rentals comparable in the area. Look for how long the properties take to rent (average rental days on the market) and what prices the properties rented at.

Next, you need to take the structure into consideration. If the home is old, that is OK. Stay away from wood-frame homes and any roof damage structures. A little cosmetic work is good (paint/carpets/clean, etc.), but anything major such as plumbing or roof work can be detrimental.

![]() INSIDER TIP

INSIDER TIP

Other than structure, location is key. Try to buy rental properties close to schools and churches. Your vacancy rates are usually lower and the homes are usually in better conditions due to the high demand.

Assuming your goal is to get the friendly tax advantages of owning real estate, building a nest egg for your family, and investing your money in good old-fashioned tangible concrete, then you can turn your twelve homes into a nice retirement safe haven.

In order to purchase one property a month, you will have to either have credit, or some cash. However, by this time you should have saved over $250,000 through your REO listing business, which allows you to leverage your savings.

Remember from Chapter 2 that each bank account, if managed correctly, will produce you $372,120 net. With three to five bank contracts, you have the ability to produce a million dollars net. However, to be conservative, let’s stick with the figure of $250,000.

With the market how it is today, if you are buying investment homes, you will need at least a 20 percent down payment and you may be capped off at a certain amount of homes. For example:

$250,000 / 20% = $1,250,000 REO Purchasing Power

$1,250,000 / 12 Homes

$104,166 Max Price per Home

In this example, with your $1,250,000 purchasing power you can buy twelve REOs with a purchase price of no greater than $104,166. This doesn’t assume closing costs and other closing fees, but you get the picture.

“I work in Phoenix, Arizona. With the market shot, I took the advantage of buying as many cash-flow properties as I could. I used the one-a-month strategy and accumulated twelve homes. My goal is to keep each one rented until both of my kids go to college and hopefully double if not triple my money. I cannot believe how many deals are out there. Now is the opportunity to buy real estate. As long as the property cash flow is positive every month, you cannot go wrong.”

—George Garcia

Phoenix, AZ

REO listing agent

Sometimes your lender may cut you off after you reach four or five properties. When that happens, you have to be creative and purchase under your spouse’s name, your family’s name, a living revocable trust, a land trust, etc.

Alternatively, you can use “hard-money,” which usually has a higher interest rate than traditional financing and comes with more up-front fees (e.g., 14 percent interest rate and 4 to 5 percent of the purchase price in fees as “points” upfront at closing). Also, they will usually loan you no more than 60 percent of the home’s value.

So if you are looking at a $100,000 home, the max they will loan you is $60,000. This means, for you to continue to maintain your goal of twelve homes a year, instead of purchasing twelve homes at $104,166 you would have to find twelve homes at $52,000 or less.

If you do decide to build wealth through real estate while you continue to cash in on your ATM REOs, one very favorable option is to qualify your homes for Public Housing Choice Voucher programs (e.g., Section 8) designed by the U.S. Department of Housing and Urban Development (HUD). This is a subsidized housing program that assists low-income families, the elderly, and the disabled afford decent, safe, and sanitary homes.

Vouchers are administered locally by public housing agencies (PHAs) that receive federal monies from HUD. Many times, an eligible family may qualify for almost all of the rent or close to it, which is directly deposited into your bank account through the local PHA. This is a great way to minimize vacancy and get your rent automatically every month all while promoting the affordable housing initiative.

![]() INSIDER TIP

INSIDER TIP

When implementing the hold and rent strategy, as soon as any property increases in value by 50 percent, sell it and get your money out. You make money when you buy, not when you sell. Therefore, the faster you can sell your property the better of a deal you got when you purchased.

Is this the bottom?

I get asked this question all the time. The truth is, I will never know if this year or the next couple of years will be the bottom. All I know are the hard facts. If a property with all expenses included costs you $600 a month and you can easily rent the property for $1100 without breaking a sweat, then it doesn’t matter if it is the “bottom” or not.

A good rule of thumb to predict when a market is bottoming out is if hypothetically you were buying a home with 100 percent financing (remember those days?) and your principal, interest, taxes, insurance, and association fees (if any) are still less than the market rent.

Option #2: Fix-to-Flip

This is my favorite option. The easiest way to make extra income from REO listings is to follow the REO Fix-to-Flip Rule: Find an REO listing that has aged for more than ninety days, which requires it to be fixed up to meet basic FHA financeable standards, so you can flip it to a hungry first-time home buyer.

“One deal we worked on was a single family home in a good market area. It was a three bedroom, two bath, one car garage that was converted to an efficiency. We knew we couldn’t get a first-time home buyer approved for financing so we spent about $4,500 and converted the efficiency back into a garage. We had the FHA inspector go out and approve the work and immediately we sold the home. Our purchase price was $145,000. We purchased it with 50 percent down and got a hard-money lender to loan us $72,500 at 10 percent interest per year. We sold it for $175,000. After title closing costs (2 percent), co-operating agent commissions (2.5 percent), three months of hard-money interest fees ($1,812.50) and all rehab fees ($4,500), we made $15,812.50 net profit within four months.”

—Jason and Kristy Davis

Fort Lauderdale, FL

REO listing agent

If you are buying a condominium or loft, make sure the actual building is FHA approved. Usually FHA approval requires a maximum amount of percentage of foreclosures allowed in the building (e.g., no more than 15 percent), otherwise the building will not qualify for FHA financing. The last thing you want to happen is to get stuck with a property and have 60 percent of your potential buyers eliminated because they rely on financing to purchase your unit.

![]() INSIDER TIP

INSIDER TIP

Slow months of REO inventory are a great time to flip houses. There will be soft supply and strong demand from buyers. Because an REO takes up to ninety days to close, you have a three month gap to find a steal, fix it up, and flip it before you begin competing with new REOs that come on the market.

Option #3: The Lease-to-Own Program

Nationally, credit scores have never been worse. With unemployment rising, jobs being outsourced overseas, and an unstable economic environment, many consumers simply do not have the credit or the cash to buy their own home. However, what they do have is the desire. One great option that serves as a win-win solution for both you and your prospective tenant is a lease-to-own program.

Instead of collecting a first month’s rent and security deposit as you would do in a standard hold and rent strategy, here you will be collecting an non-refundable “option deposit” that will apply toward the purchase price (which is set by you) only if they decide to buy. For example, you find a hungry tenant who has a strong will and desire to purchase a home within the next two years by working on his credit. From one of the twelve homes you own, you offer it on a two-year lease-to-own option:

$150,000 purchase price (option to buy; expires in two years)

$7,500 (5% non-refundable option payment)

$142,500 (balance owed to you within two years)

If the tenants exercise their option to purchase, then the $7,500 will be credited against the purchase price. If the tenants fail to buy or cannot buy, the $7,500 is non-refundable and is yours to keep. Of course, your goal is to sell the home so you can cash out, but you can also choose to extend the contract for another twelve months for an additional 5 percent non-refundable option payment if the tenant is unable to purchase.

This benefits the tenant by locking in a purchase price today for two years out. This also benefits you by having a stable, steady renter for two years who would be foolish to walk away from his 5 percent option deposit payment by not paying the rent. You also have your locked-in rental price upfront.

![]() INSIDER TIP

INSIDER TIP

When doing a lease-to-own option, do not accept a potential renter unless they are willing to give you at least 5 percent of the purchase price; otherwise they will walk away from their deposit. Because you are doing them a favor by locking in the price of the home for two to three years from now, they have plenty of time to work on building their credit to buy.

Hidden Stream #6: Property Preservation Goldmine

Property preservation is by far one of the most important aspects of marketing for REO properties. No asset manager wants to be a subject of discussion on why an inspection revealed an REO to be marketed poorly. Yes, there are mystery shoppers who go and inspect homes. Yes, these mystery shoppers grade your assets on various criteria including, but not limited to, cleanliness, safety, marketability, etc. Asset managers want homes to be sold for as much as the market bears. So why not add value with property preservation?

Ten Frequently Used Preservation Needs

- Landscape package

- Pressure cleaning of driveway

- Carpet cleaning

- Heating, ventilation, and air conditioning (HVAC) inspections

- Securement of door frames and windows

- All locks (front/back/gates) changed

- Sliding doors secured

- Initial pool cleaning (if applicable)

- Periodic pool cleaning (if applicable)

- Removal of damaged material

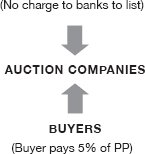

As you first start in the business, you will be approached by numerous vendors claiming to provide you with the best service and flexible payment terms. Many times companies will offer you an open line of credit. You pay them only after you get reimbursed from the bank.

Remember from Chapter 3 we discussed how to use other vendor’s money (OVM) to finance your REO Bootstrap Model. As you scale your business and change structures to the REO Plus Model, you may want to think about starting your own property preservation company. This is assuming it’s legal and doesn’t violate your bank master listing agreement, as some do not allow you to use affiliated members to handle property preservation.

If other companies are willing to give you 120-day terms and excellent service, there is profit to be made. Why give it away? Other than the money, as a real estate entrepreneur in the REO business, control is key. Because the work is so time sensitive as well as detail sensitive, your name is on the line. Therefore, it is important you control the property preservation and make some money while doing it.

There are six vital steps to starting your own property preservation company:

Step One: Create a property preservation company, similar to industry giants such as Safeguard Properties, Cyprexx Services, or Field Assets.

- For $200 (see Appendix A), you can find someone to create a website for the company you just created, with content that shows you as a reputable property preservation company. It’s well worth the upfront investment.

- Create a logo, virtual office, phone number, and email address.

- Open a business checking account.

Step Two: For each of the ten frequently used preservation needs (above), find a reliable low-budget sub-contractor who is in need of business and is results oriented (not effort oriented). Search Craigslist.com and negotiate rates with the promise of high-volume work. Set up a meeting, shake hands, and set your expectations: service within twenty-four hours, before and after pictures, and dependability.

Step Three: Set your margin requirements. Banks value the time you take to ensure the security and marketability of assets. As such, they usually set maximum reimbursement amounts for the services below.

![]() INSIDER TIP

INSIDER TIP

You should require at least a 50 percent return on your investment for each of the ten items below. If you can’t find a contractor to give you that margin, look further. They are out there, and they need business.

| Preservation Type | Typical Maximum Reimb. Amt. (from bank) | Max Out of Pocket Expense | Proft Margin |

| Landscape package | $250 | $100 | 40% |

| Pressure cleaning driveway | $250 | $150 | 60% |

| Carpet cleaning | $200 | $90 | 45% |

| HVAC inspections | $400 | $250 | 63% |

| Securement of door frames/windows | $500 | $300 | 60% |

| All locks changed (per unit) | $150 | $75 | 50% |

| Sliding doors secured | $150 | $60 | 40% |

| Initial pool cleaning (if applicable) | $500 | $300 | 60% |

| Periodic pool cleaning (if applicable) | $250 | $80 | 32% |

| Removal of damaged material | $500 | $220 | 44% |

| Average | $315 | $162.50 | 49% |

Step Four: Make bid proposals for all your properties. The bid should be on a professional document made from QuickBooks or similar accounting software. Be sure to include your logo, address, etc., as discussed in Step One. Email the bid to your brokerage company and submit the bid into the bank for approval.

Step Five: Obtain two bids to send to asset managers (one from an industry giant and second from your preservation company); the one you recommend should be the lowest cost. Your asset manager will want to improve the marketability of the home, so you should not have any hesitation making your request.

![]() INSIDER TIP

INSIDER TIP

Some banks do not require a bid and have automatic approvals for certain items.

Step Six: Once your preservation expense is approved, get your subcontractor to begin work and to send you before and after pictures. Once complete, update your records to indicate that the preservation/repair has been completed to satisfactory conditions. Finalize the payment by writing a check from your brokerage company to your property preservation company and another check from your property preservation company to your sub-contractor. Always keep clean records and books.

Never delay a payment to the local sub-contractor longer than thirty days, regardless of if you have received reimbursement from the bank or not. Remember, you are trading open credit terms for profit.

This should be repeated for every property and for every expense. Creating a system that performs these steps automatically will yield far more benefits than you probably would imagine.

There are two types of REO agents. The first is one who will lose out on an additional stream of income, lose out on making their asset manager look good by adding marketing improvements, and lose out on the opportunity to continue to get inventory by not maximizing the property preservation expenses above.

The second is one who will find a way to create value-added gains through each of the ten items mentioned! All it takes is some digging around to find cheap suppliers, and that’s it! Of course, always make sure you are not in violation of your MLA, as banks or outsourcers may prohibit the listing agent from using a contractor that is affiliated with him/her for repairs or any other type of property preservation.

HOW ABOUT TITLE REFERRALS?

Don’t even think about it. There are certain agents in the industry all across the country who are forcing their buyers to use their “preferred title company,” and in return, title companies are giving cash referral fees under the table.

If your brokerage company owns a title company and you give proper affiliated business arrangement disclosures and do not violate any laws, then by all means promote it. It’s good to have a seasoned title company that is experienced in the REO and foreclosure business. However, don’t even think about getting a referral fee or “kick back” from anyone else. You might get away with it once or twice, but the third one will catch up with you, and that is a serious RESPA offense.

![]() INSIDER TIP

INSIDER TIP

Did you know a title company makes approximately 70 percent commission off your customer’s title policy plus 100 percent off the settlement or closing fees? If your customer is paying anything above $395 for “settlement charges” as indicated on the HUD-1 (section 1100), they are paying too much.

![]() SHARE YOUR STORY

SHARE YOUR STORY

Do you have a success story you would like to share about how you milked your REO ATM? Any auction deals, any fix-to-flip opportunities, or any hidden income goldmines you took advantage of? Please log on and submit it for your chance to be featured in the next edition of REO Boom:

POINTS TO REMEMBER

- Title referrals are not hidden income; just say NO!

- Six steps to property preservation: form an LLC, source cheap contractors and set expectations upfront, set your margin requirements for the ten frequently used preservation needs (minimum 50 percent), create a bid, submit two bids to the bank, order work, verify, and pay out in thirty days.

- Auction properties sell for 50 percent of their previously assessed value.

- Real estate arbitrage is buying cash properties at live auction or purchasing your own listing and utilizing the three exit strategies to profit from: hold-to-rent via housing vouchers, fix-to-flip to FHA buyers, or lease-to-own.

- Banks drop their list price 5 to 10 percent every thirty days if they see no movement; after ninety days, property becomes aged and moves to a live auction.

- Obtain a home warranty license to earn an additional $6,500 on warranty plan referrals.

- Buyer bonus fees can earn you an extra $34,000 per direct bank contract. Have the buyer sign a buyer bonus agreement and disclose it on the HUD-1.

- 50 percent of closings are finance buyers; 30 percent of those who close will be with your mortgage specialist, who will pay you 50 percent referral fees (up to $68,000 per direct bank contract).

- Hot leads are those who are willing, able, and ready to buy, which will increase your in-house buyer selling commission ratio up to 50 percent.

- Focusing on the first streams of income is for beginning REO agents. The pros build up and focus on the hidden six: selling commission, financing, buyer processing fees, home warranties, flipping, and property preservation.