![]()

The Art of Offers

OFFER EXPECTATIONS

The secret to making a million dollars in this business is mastering offers. The buck stops here. You can have the perfect BPO, have the best listing price, have a pristine condition home, but if you cannot quickly screen buyers or give good recommendations to asset managers, then all the work you have done will be in vain. There is one thing that the public doesn’t know about the offer process—the listing agent has power.

You have come a long way in the REO cycle. You have learned to master the BPO, as well as how to get a property repaired and ready for the market, and now you are at the most critical part standing in the way of closing the deal. The offer process is nothing like the offer process in conventional real estate. It is quick and dirty. Banks will not cross out and initial on your standard contract and send it back. They will email you one line or enter one comment in their online platform, and you will have to dictate that to the buyer or other cooperating agent.

Most banks have their own addendum that supersedes any state-regulated real estate contract. They also have a waiver in which the buyer waives all rights to sue the bank after the sale of the property for whatever reason.

Below is the order of the offer process:

REO Offer Process

- Initial Offer

- Counter Offer

- Multiple Offer

REO Offer Actions

- Accepted

- Rejected

- Countered

As an REO listing agent, you will be responsible for managing the entire offer process. If you are using the REO Bootstrap Model, you will be the one entering in the offers in your bank’s platform. If you surpassed thirty active listings and are using the REO Plus Model, you will have your transaction coordinator handle the offer process.

The offer process begins only after you have a listing price and the property is placed on the MLS. Until then, banks will not entertain any offers. Remember, banks promote home ownership and neighborhood stabilization, so they want an even playing field for all parties.

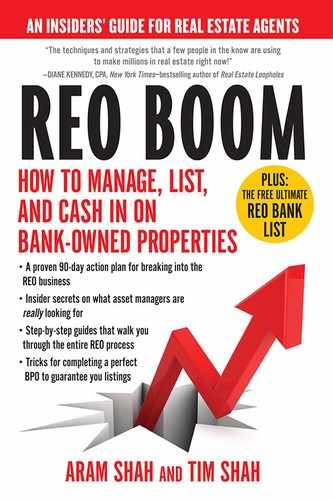

From the bank’s perspective, it does them no good to take a low-ball offer; therefore, they usually have a requirement to let a property stay on the market for a certain time period before entertaining any offers. Some banks require that the property stay on the market for three full days before any offers will be considered.

BANK THREE-DAY RULE: PROPERTY MUST STAY ACTIVE ON MLS FOR THREE FULL CALENDAR DAYS. NO OFFERS WILL BE CONSIDERED DURING THIS TIME.

Each bank is different, but they all generally have a first-time home buyer (FHB) privilege period, where they give bona-fide first-time home buyers (i.e., owner occupants who intend to purchase a home as their primary residence) a chance to bid on the REO before they open up the doors to investors. Typically this period is the first fifteen days from the time the property is listed.

FHBs are usually required to sign an occupancy certificate or affi-davit stating their intent to use the home as their primary residence. Sometimes, consumers who have purchased a home before but are looking to upgrade their home may be eligible to qualify as an FHB. However, because you do not make decisions for the bank (remember, you are not the seller) your job is to present the facts to the banks and let them decide. Never act as a seller by speaking for them or making decisions for them; it is a sure way of losing your bank contract.

In addition, public entities (PE) such as cities, counties, etc., that are using special types of government-sponsored or subsidized public funds (e.g., HUD neighborhood stabilization program, grants, housing trust funds, etc.) also have preferential treatment in purchasing homes within the first fifteen days. This also includes homeowners who intend to occupy the home using public funds.

After day fifteen, all offers are considered. Investor offers come from private individuals, syndicate corporations, and even second-time home buyers looking to park their money in real estate are fair game. Investors are defined as buyers not looking to occupy the property themselves.

BANK FIFTEEN-DAY RULE: ONLY OFFERS FROM BONA-FIDE HOMEOWNERS AND PUBLIC ENTITIES WILL BE CONSIDERED WITHIN THE FIRST FIFTEEN DAYS OF THE PROPERTY BEING ACTIVE ON MLS

OFFER ACCEPTED TIMELINE

If there is one take-away message you must learn in this chapter, it is to present every single offer. First-time home buyer, second-time home buyer, corporations, public entities or individuals using public funds, the mayor, a senator, or even the president—it doesn’t matter. Even though you know an offer will be rejected within the first three days, you must present it.

Remember, you are not the seller. You do not own the property, therefore, you cannot decide its fate. Email your asset manager the facts, update your online platform, and let the bank decide. Always cover your assets (CYA).

Hiding offers or going back to cooperating agents and prolonging their offer because of a technical error (missing a document, spelling error, missing initial, etc.) is the fastest way of losing your bank contract.

Banks usually have one perspective when dealing with offers: give everyone a fair chance with impartial consideration to maximize the sales price of a given home. Therefore, every offer must always be presented, no matter when it was received (even if it’s before the listing price is given to you), for what amount it is, or from whom it was sent by.

PRESENT EVERY OFFER TO MAXIMIZE SALES PRICE

A very important element in handling offers is keeping clean records of all emails, faxes, and conversations. Updating your asset manager and your online platform is critical. At the end of the day, it’s whatever is in writing that counts.

Make sure when dealing with offers that you have written proof. Verbal offers are generally not accepted along with offers without consideration (earnest money deposits, or EMDs). Expect a minimum of forty-eight hours for the banks to respond to your offers.

There are seven general expectations (E’s) the banks look for in offers submitted to them. The best thing you can do is set the upfront expectations for your buyers and other selling agents in the marketplace; otherwise, you will be setting yourself up for failure.

- E1: Banks want to maximize their sales price.

- E2: Banks have no preference whether offer is cash or financing.

- E3: Banks want all offers submitted to them within twenty-four hours.

- E4: Banks want to minimize their liability and therefore require every offer submitted, regardless of the circumstance or time.

- E5: Banks generally prefer first-time home buyers to support local housing initiatives and therefore may require a ninety-day or greater deed restriction prohibiting the resale of a home for investor offers.

- E6: Banks will only execute their attorney-drafted documents in a “take it or leave it” stance.

- E7: Banks will sell their properties as-is and will make a buyer sign a waiver at closing.

THE OFFER PACKAGE

Every bank is different, but generally the majority of them want to promote homeownership and want to give a fair shot to the public, especially first-time home buyers and public entities that use public funds subsidized by the government to purchase homes. Your offer package should consist of the following elements:

- State or local promulgated contract

- Bank addendum and disclosures

- Any owner occupied certifications or affidavits

- Earnest money deposit (EMD) copy

- Pre-qualification letter (optional)

- Proof of funds (POF) for cash offers (optional)

![]() INSIDER TIP

INSIDER TIP

Create a very transparent offer package for selling agents to use. Less is more. The easier the package is for a selling agent and buyer to fill out, the faster you will get the REO under contract.

The pre-qualification letter for financing offers and proof of funds for cash offers are required for some banks but not for all. They may allow an offer to be submitted, but they won’t accept the offer until it is produced. Usually if a selling agent or buyer presents an offer without a pre-qualification letter or proof of funds and it is the highest offer, the bank will counter, asking for the missing document. Even though the banks want the highest and best price for the home, they do not want to waste time with an unqualified buyer. A thorough pre-qualification letter or proof of funds should include:

- Maximum loan qualification based on monthly income-to-debt ratios (e.g., can qualify up to $150,000)

- Credit bureau report or credit score

- Verification of paycheck stubs

- Recent bank statement showing sufficient monies for down payment and closing costs

- Recent bank statement showing sufficient funds for purchase of entire home plus closing costs (cash offers)

With earnest money deposits, most banks simply require a copy of the check. It would be nice if the majority of banks required an earnest money escrow statement or certified funds, but because the demand is so high for REOs, they usually require only a copy of a check even if there is no money in the bank account. That is an inherent risk that has to be dealt with. Expect one out of ten winning bidders to fall out. Many buyers place offers on multiple properties without physically seeing them to ensure they get something.

![]() INSIDER TIP

INSIDER TIP

FHBs usually give 1 to 3 percent of the offer amount or greater as consideration for their EMD. Investors usually give 10 percent as consideration. EMDs are usually payable to the bank’s designated settlement agent or the listing brokerage company (you).

If you have a public entity or individual using public funds, their EMD requirement may be waived or reduced to as low as $500. This is the case if they have an approval letter indicating the source of funds (from whom, amount, etc.).

REVIEWING OFFERS

Your offer packet can be streamlined and perfect. You can have perfect instructions on the MLS and still have selling agents who will butcher the offer packet (putting numbers in wrong lines, missing initials on pages, missing spouses’ names on contract and addendums, leaving sections blank, overlooking expired pre-approval letters or post-dated earnest money checks, etc.).

Below is an internal offer checklist you can use to ensure the offer you receive is as complete as possible before sending it to the bank. Remember, even if the offer is not perfect, you still must present it to the bank. Simply notify your asset manager of the specific items that may be missing.

Internal Offer Checklist

- Price

- Seller concessions amount

- Offer type: FHB, PE, INVESTOR

- Owner occupied certificate or affidavit (y/n)

- Copy of EMD (y/n)

- Copy of POF if cash (y/n)

- Closing date

- Loan type (FHA/VA/conventional, cash)

- Public funds used (y/n)

- Selling agent involved (y/n)

- Pre-qualification letter (y/n)

- All pages initialed and signed in contract and bank addendum

![]() INSIDER TIP

INSIDER TIP

Submit all offers to the bank within one day of receipt; the sooner the better. Even if it’s missing a document from your offer packet, submit it and email your asset manager what is missing (e.g., proof of funds, owner occupied certificate, etc.). When in doubt, submit it.

Who pays closing costs and who chooses the settlement agent? There is only one answer: whatever is negotiated between the buyer and seller. Sometimes counties require the seller to pay title fees or vice versa. If you receive an offer that doesn’t mention the bank is to pay the buyer’s closing costs and it gets accepted, the bank will not pay the closing costs.

If a selling agent asks you about closing costs, you need them to put them in writing with the offer. Generally, banks pay up to 6 percent toward the buyer’s closing costs and other concessions such as repairs. Please be as detailed as possible. You can include a clause in your contract like:

Seller will contribute up to $______ toward buyer’s closing costs, title insurance, settlement fees, attorney fees, hazard insurance, points, prepaids, home warranty, home repairs, etc.

Buyers generally can choose whomever they like to act as their settlement agent. Sometimes banks require the buyer to close with the bank’s designated settlement agent but will give a special credit toward buyer title fees, etc. It again depends on the offer. If an offer comes in highest and best among all and the buyer is requesting that the bank designate the buyer’s specific title company to close the transaction, the bank usually complies because it wants to maximize the sale price.

SUBMITTING THE CLEAN COPY

The offer packet that you place on the MLS for selling agents to fill out and the actual offer you submit into the bank once it is the winning offer are two different phases. The latter is what I call the “clean copy.” It is the winning offer in its pristine form combined into one PDF for the bank’s asset manager to sign off on.

- Step 1: Streamline the offer packet placed on MLS.

- Step 2: Enter all offers manually into the bank’s online platform offer screen using the internal offer checklist.

- Step 3: Have the selling agent resubmit the winning or accepted offer to you in perfect form.

- Step 4: Review each element to ensure completeness to produce a clean copy for the bank to sign off on.

- Step 5: Combine pristine copy into one PDF and email to asset manager for signature.

After you attach your streamlined offer packet with the basic elements into the MLS, you will enter all offers into your bank’s platform offer screen. You will use your internal offer checklist to ensure the meat of the offer packet is included. Don’t be too concerned with spelling errors or missing initials. Your goal is to get the price, terms, and major elements of the offer, such as seller contribution request, into the bank’s hands. Your job is to present all offers, and the bank’s job is to maximize its sales price.

Once the bank picks the winning offer, you then email the selling agent to fix any errors or provide any missing documents such as proof of funds of EMD, occupancy certifications, etc. The selling agent should return the clean copy to you within twenty-four hours. Upon receipt of the clean copy, you will combine all pages into one PDF so the asset manager can quickly review the document and sign off. Remember, your job as the listing agent is to ensure everything is perfect before emailing the clean copy to the asset manager. The last thing you want is an email or phone call saying an initial is missing from a page or that an entire document is missing.

![]() INSIDER TIP

INSIDER TIP

After the bank picks the winning offer, prepare the clean copy yourself and email to selling agent or buyer to simply sign off on it. It’s more efficient and it will ensure you get back the clean copy within twenty-four hours; otherwise, it can take days for the selling agent or buyer to get it right.

Before you submit the clean copy, pay particular attention to details. If you are using the REO Plus Model (see Chapter 3) make sure you provide your transaction coordinator with step-by-step instructions to producing a clean copy (see Appendix G). Have them email it to you when they think it is perfect so you can be the final eyes glancing over it before submitting it to your asset manager.

THE MULTIPLE OFFER MONSTER (MOM)

I remember when I received my first offer on my first REO. It was exciting. I couldn’t believe I had received an offer within five days from the time I listed the home on the market. It was thrilling but nerve-wracking dealing with countering the offer, reviewing the addendum, negotiating the price and terms, picking title companies, etc. After about ten offers, I finally had a good handle on the process—until I ran into the MOM (Multiple Offer Monster).

The MOM will destroy you. She will put you under the magnifying glass by scrutinizing your procedures, scream at you by filing complaints, reprimand you by calling you into her corporate office, and will always sleep with one eye open to make sure you are kept on your toes.

Multiple offers are when you have more than one offer on a property. This can be from the time you listed it, from the time the bank accepted an offer, or from the time you put your yard sign on the front lawn.

Unlike multiple offers, single offers are easy. You present it to the bank and it gets accepted, rejected, or countered. You go back to the selling agent or buyer and relay the information until you have a meeting of the minds. When you are dealing with a multiple offer situation things get sticky, especially when a seasoned MOM is constantly looking over your shoulder.

MULTIPLE OFFER MONSTER (MOM) = MORE THAN ONE OFFER ON A PROPERTY

Your job as an REO listing agent is to present all offers. The bank’s job is to maximize the value of the asset. Therefore, the bank wants every single offer in for review. The following are the steps you take when dealing with the MOM.

- Email all selling agents or buyers (if you represent both sides) that there is a multiple offer situation.

- Email or fax all selling agents/buyers a multiple offer notification provided to you by your bank.

- Set and email a deadline (usually forty-eight hours) for all selling agents or buyers to re-submit their highest and best (H&B) offer on the bank’s form. The deadline will be determined by your bank’s guidelines. Example:

- Highest and best offer must be received in writing to the listing agent no later than ________ (Date/Time).

- Update your online bank platform and notify the asset manager there is a multiple offer situation. Provide them with the MLS ID along with the date the property was listed to make it easier for them to make a decision. Example:

- Multiple offer situations exist for REO XYZ. The MLS ID is x123456. List date was xx/xx/xxxx. Deadline for all H&B offers is _________(Date/Time).

- Update the MLS and clearly state in the comments section there is a multiple offer situation and when the deadline is to submit all H&B offers.

- Email your asset manager immediately and await their response if the following occurs:

- Offer comes in after the deadline passed.

- Offer comes in after the bank already picked or is negotiating with the H&B offer.

- Selling agent or buyer is threatening you with “filing a complaint.”

![]() INSIDER TIP

INSIDER TIP

Set up a special email to handle all your offers, along with an auto-responder ([email protected], see Appendix F for sample). This will enable you to search any offer by property address or name instantly in case MOM gives you the third degree.

So, the winner is …? Whatever you do, do not inform the selling agent or buyer their offer is accepted until you get in writing from your asset manager who has presented the winning offer. Many times, asset managers will go into their system and reject all offers because of upper management discretion.

Imagine informing a potential winner their offer was accepted and then calling them the next day informing them they now have to rebid. Those are shoes you do not want to fill.

THE FIVE OFFER STATUSES

To make matters more confusing, sometimes banks will have “verbally accepted” and “accepted” as different categories internally on their bank platform. Usually there are five offer statuses:

- Pending Offer

- Verbally Accepted Offer

- Accepted Offer

- Awaiting Approval

- Rejected

If you submit the offer into the bank and the asset manager has not looked at it yet, the offer status is pending. They have not taken any action. If there was a tug-of-war situation (offer-counter-offer) and the bank decided to accept an offer, the status usually goes first to “verbally accepted.” This is, the bank verbally accepted it but still needs management approval to sign off. It is not formalized yet.

On the other hand, “accepted” means the bank chose the winning bidder. Once you see the words “accepted” in your online platform or receive an email from your asset manager, you are safe to inform all parties who has the winning offer. You can also change the status in the MLS to “pending sale.”

Sometimes before the offer can be fully accepted, it may fall into an “awaiting approval” state. This is when the bank has chosen to approve it, but may need a special signature from someone else in management to sign off, possibly because there is something missing or the offer is substantially lower than the listing price. Finally, “rejected” status is when all negotiations between buyers and sellers are ceased.

Sometimes buyers tend to play hardball and submit low offers, which get rejected immediately. These investor-type offerers usually come back if they really want the property and submit a new offer. Also, some banks will automatically reject properties if the offer falls within the first three days of the no-offer-accepted period or if an investor submits an offer during the first fifteen-day FHB protection period.

Usually the MOM comes into play when a property was priced too low or is in an incredibly hot area. This is the time when the pressure is on. Not following the multiple offer process is crossing the invisible line into the three shady offer tactics that selling agents use. This is playing with fire, as we shall discuss below.

The Busted Offer

Even when MOM situations exist, there are many times that the offer that is ultimately accepted ends up busting out or falling through (i.e., the buyer backs out and terminates the contract agreement). In these cases, it is necessary that you reach out to all the other agents/buyers who were interested in the property. Tell them it’s their lucky day and have them resubmit their offer. In most cases, they will be delighted to do so. Many banks also allow backup offers, in which case the next highest and best offer will be accepted without the listing agent having to relist the property.

Don’t fret if a buyer or selling agent backs out. This happens. Don’t take it personally. Just be thankful that you have multiple offers so that you can reach out to the others and get a solid contract executed. In cases where banks do not have a backup offer policy, be sure to follow these seven steps as soon as the buyer or selling agent tells you they want to cancel.

- Call up the selling agent and buyer to find out the reason for their cancellation.

- Send them the termination agreement (an addendum to cancel the contract) and give them a deadline by which to return it.

- Inform your asset manager that the deal has fallen through, but you are still waiting for the signed termination agreement from the buyer/selling agent. Inform the asset manager that you will change the status in MLS from “pending sale” to “active” and that you will reach out to any other offers that are in the system.

- Change status from “pending sale” to “active.”

- Email each party who made an offer for the property to see if they are still interested. Call and confirm that they received the email and that they will reach out to the respective buyer to determine if an offer should be re-presented.

- If a new MOM situation exists, inform each party when their highest and best offer is due by.

- Input all highest and best offers.

THREE SHADY OFFER TACTICS

I have seen a lot of offers. I have seen the same listing agents continue to sell hot properties to the same buyers without even a chance of those properties hitting the market to give a fair shot to the general public.

We strongly advise against using the following methods. They are unfair, immoral, and unethical. We can almost guarantee that if you do get away with such tactics once or twice, your behavior will come back to haunt you and will cost you your bank contract (and possibly a lot more).

Shady Offer Tactic #1: High-Low Method

When a property is in demand, you will know. You will get multiple calls a day on the property. The key will get stolen from the lockbox. You will get threatened by a consumer. It’s a multiple offer monster situation, and the bank will soon inform all parties to resubmit their H&B within a certain time period.

MOM SITUATION = H&B OFFERS NEEDED

Many co-operating agents who have been seasoned selling REOs have learned how to master the MOM process by implementing the high-low method. Basically, when the bank requests the H&B offer from all parties, a co-operating agent will exaggerate the offer to ensure the bank picks it.

If the property is listed at $200,000 and the property is in an MOM situation, a typical H&B offer will come in around 30 to 50 percent higher—$260,000 to $300,000. They will also put on the offer “first-time home buyer and FHA financing.” Remember, most banks want to promote homeownership since they are receiving government subsidies (bail-out funds), so they usually give preferential treatment to first-time home buyers.

Then, after the co-operating agent’s customer is the winning bidder, they will obtain an FHA appraisal during the thirty-day closing period as a tool to drop the price back down to the current market value. For example:

Listing Price: $200,000 on 1/1/2012

Offer 1: $205,000; cash; investor

Offer 2: $225,000; conventional financing; homeowner

Offer 3: $245,000; FHA financing; second home; homeowner

Offer 4: $285,000; FHA financing; first-time homebuyer (High-low method winner)

- High-low method buyer wins contract and orders required FHA appraisal

- FHA appraisal comes in at $201,000; ordered on 1/15/2012

- Bank reduces home from $285,000 to $201,000 on 1/20/2012

Most banks usually pick the highest dollar amount of the offer presented regardless of the type of financing the buyer chooses. To the seller (bank), there is not much difference between a cash offer and a financing offer because either way they will receive cash at closing. Therefore, most banks would rather entertain a higher financing offer than any other offer because it is most likely to yield the highest sales dollar to the bank.

Even though Offer 4 (high-low method winner) was clearly over listing price and possibly market value, the bank will pick it because it maximizes their value or pocketbook. Plus, the offer is from a homeowner and the bank thus meets its initiative of stabilizing neighborhoods throughout the country.

High-Low Method with Seller Contribution

Sometimes offers will come in requesting the seller to contribute a certain percentage (e.g., 6 percent) from the sales price to cover the buyer’s closing costs. However, this request is used as a tool for negotiation to sway the asset manager’s decision in agreeing to the high-low method request. For example, the selling agent will explain to the listing agent (you) that the buyer really wants the house and is even willing to forego the seller contribution it initially requested due to the buyer’s strong desire to buy the home.

High-Low Method with Inspection Report

In addition, even when most banks sell their property as-is, the selling agent will order an inspection report (separate from appraisal) to further support their high-low method request. The goal of the inspection report is to itemize as many flaws in the home as possible that can be used to obtain repair credit. The selling agent will not necessarily count on the repair credit being issued, but they will use the inspection as another tool to boost their negotiation efforts.

They will make the case that the buyer is willing to make all of the repairs out of pocket and even waive a seller contribution, only if the seller complies with the state-certified appraisal to reduce the purchase price. Nine times out of ten, if the selling agent is good and makes a good case using the seller contribution and repair credit tactic, the bank will grant the purchase price reduction.

![]() INSIDER TIP

INSIDER TIP

Many banks require homeowners to sign an occupancy certificate verifying they are a bona-fide homeowner and do not intend to resell the home for up to twelve months. Search local county records to make sure the winning buyer does not own a home currently, and inform your asset manager if they do to prevent the high-low method.

High-Low Method Summary

- Buyer submits exaggerated H&B offer with seller contribution to secure contract.

- Buyer orders inspection and point out damages to home.

- Buyer offers to pay for inspection damages out of pocket and even waives any seller contribution to show sincerity in purchasing home.

- Seller complies and reduces home to state certified appraisal amount.

Shady Offer Tactic #2: The Proxy Offer

This next tactic is dirty; a low blow. A co-operating agent creates a proxy offer with a fraudulent pre-approval letter and submits the H&B offer to the bank during the MOM deadline. After they win the bid (as in the high-low method above) and all other competing offers are rejected, the following steps occur:

- Co-operating agent informs bank during the inspection period (usually ten days) that their customer is no longer interested during their inspection period.

- Bank informs listing agent (you) to re-list the property bank on the MLS (usually within twenty-four hours).

- Same co-operating agent submits another offer (this time a real customer) at full list price.

- Same co-operating agent removes key from lockbox so previous buyers and their co-operating agents (or new ones) cannot gain access to show the home while it is re-listed.

- Same co-operating agent wins property at the retail list price.

- Same co-operating agent uses appraisal and repair credits to negotiate purchase price down even further.

Because there is a lead time between when the property is pending sale and active on the MLS (due to the speed of the listing agent), the original co-operating agent has a narrow window of time to slip in his second offer while all other co-operating agents and buyers are left in the dark thinking the property is off the market.

Shady Offer Tactic #3: Straw Offer

The final tactic is for selling agents to go around the first-time home buyer protection period—the period of time that a property is on the market whereby investors are not allowed to win a contract on a property. This allows the investor to purchase a property when only a homeowner is allowed to do so. Most banks do not allow for second home purchasers to win a contract during the homeowner period.

The following steps have been used to make straw offers:

- Selling agent puts in an offer for a fictitious buyer (in a relative’s name) who does not appear in tax records as owning a residence.

- When this offer gets accepted, and after the contract is executed (i.e., signed by both seller and buyer), the selling agent then requests to add a name to the contract (name of investor).

- Ten days prior to closing, selling agent will inform the listing agent that the fictitious buyer’s name needs to be removed from the contract (due to financing and/or other reasons).

Thus, the investor will be the only party on the contract and the selling agent will keep the investor’s name under the radar during the first-time homeowner protection period. Even better, the investor will not need to sign a homeowner occupancy certification since his or her name was added after the contract was executed and onto a separate addendum.

THE FIVE BIGGEST ROOKIE OFFER MISTAKES

When starting in the business, you may feel that sense of euphoria when you get one, two, or a few offers within seven days of listing your property. Unfortunately, the offer process in the REO cycle is the most analyzed and critical process. There is zero room for error and zero tolerance for excuses. Below are the five biggest rookie mistakes new agents make when presenting offers:

- Disclosing what the highest offer is to other agents.

- Not presenting every offer regardless of if the offer is missing pages or addendums, or if the MOM expiration period has expired.

- Not sending back an MOM notification to each buyer or cooperating agent.

- Not placing listings into the MLS properly and within twenty-four hours.

- Making it cumbersome for others to present an offer.

Your name and your word is all you have in this business. It can take years to build a reputation. but one complaint to put you out of business. Your goal is to protect your name, your company, and your reputation at all times. Avoid shady tactics and basic mistakes, and you are well on your way to becoming a respected REO expert in your area.

Rookie Mistake #1: Disclosing the Highest Offer

Banks are very smart and loaded with cash. With cash comes leverage to recruit top talent. They will send mystery shoppers or proxy buyers to call your office, your cell, your assistants, whatever it takes to see if you can walk the talk. Are you ethical? Will you follow their guidelines? Can they count on you to handle volume during busy REO boom times? This is what they want to find out—if your word is your bond.

I was once coaching a fairly new REO broker, Michelle in Georgia. She was quite ambitious and had the business down to a science. Around August one year she had an incredible month. Her in-house sales ratio (where she represented both sides of the commission) was over 60 percent. She was double-dipping and leaving no cream in the Oreo cookie.

She called me one Saturday morning at maybe 8 or 9 A.M. When I said hello, she was frantic; talking fast, nervous, and scared, as if she was about to have a breakdown. She told me there was a $400,000 home she had listed and for which she had lined up a couple of in-house buyers. Three out of five offers came in a little over list price, another came in at list price, and one customer told her he would do whatever it took to get the home.

He went on stating he was an all cash buyer, he would use her as his agent exclusively, and he even would sign a buyer-broker agreement. He would come into her office within one hour to sign a contract, and he really wanted the house for his new family. To top it off, he said he was a cash buyer who had just sold his house in Arizona and needed to buy something within thirty days because of his new job relocation.

As soon as she started off with the buyer’s rhetoric I immediately knew what was going to happen. Either he really wanted to purchase the home or it was a set up by a mystery shopper. Judging by the call coming in on early Saturday morning, I had a feeling it was the latter. He had the bait hooked and he was fishing for answers.

As he had her thinking about the nice vacation she was going to take with the $24,000 commission ($400,000 × 6 percent), he said, “Look I’m about twenty minutes away from your office. I will leave shortly, but before I go just want to make sure I have a chance to win this home. I want to offer $435,000 cash. That shouldn’t be a problem, right?” Such a convincing and innocent remark, or so it seemed. She said with all trust, “Yes, you’ll be fine; the highest offer we have is $412,000, and that’s financing anyways.”

You know what happened next? The gentleman said, “Thank you very much. I’ll see you shortly” and hung up. After about thirty minutes when he didn’t show, Michelle quickly looked into her iPhone to check recent calls and noticed the number was blocked. She attempted to redial the number, but nothing.

Immediately her stomach fell to the floor with guilt and embarrassment. A month later she was called into the bank’s corporate office for a meeting with the REO management disposition team, where they gave her a performance review. She was given one last opportunity before a final termination. Unfortunately, she never received the same level of inventory from her supplier again because she had tarnished her name, her ethics, and her reputation.

Therefore, no matter how clever the question sounds (“Is it above XYZ amount? Is it south of XYZ price? I don’t want to waste your time or mine with this offer—will I have a chance?”) do not answer. Simply state, “Please present your offer and I will submit it into the bank.” In addition, make sure you email that buyer or selling agent in writing that their offer has been submitted.

Rookie Mistake #2: Failing to Present Every Offer

We cannot belabor enough the point of presenting every offer. It is the single most important item in this chapter. Some banks may automatically give you authority to tell the selling agent or buyer their offer is rejected if it falls within the three-day rule (or the fifteen-day rule for investor offers). This does not mean you do not enter the offer. You still enter the offer letting the asset manager know the exact circumstance.

Each bank is different and has its own policy; however they all usually shadow around the three-day and fifteen-day rules. Below are the scenarios and recommended templates you should use when presenting offers in the bank’s platform. Always provide the type of offer, the date it was placed in the MLS, the MLS ID number, days left in protection period, items you have received or are missing from the offer packet, and finally whether you recommend or reject the offer.

1. Offer is received from an investor during first fifteen days of listing on MLS:

Investor offer received. Property was listed on __/__/___. The MLS ID is: X123456. The days left in FHB protection period are XYZ DAYS. We received proof of funds via bank statements. We are missing copy of EMD. We recommend rejecting this offer as per page ___ of our sales policy manual guidelines as offer falls within the first fifteen days of the home buyer protection period.

Normally, if you receive a bona-fide first-time home buyer offer and an investor offer during the first fifteen-day protection period (between days four and fifteen), a MOM situation does not exist, because an investor offer is usually automatically rejected. However, each bank is different; therefore, submit all offers and wait for instructions from your asset manager.

2. Offer is received from a first-time home buyer or investor during first three days of listing on MLS:

First-time home buyer/investor offer received. Property was listed on __/__/___. The MLS ID is: A123456. The days left in FHB protection period are XYZ DAYS. We received pre-approval letter from buyer’s financial institution. We are missing copy of EMD. We recommend rejecting this offer as per page ___ of our sales policy manual guidelines as offer falls within the first three days of the no-offers acceptance period.

Giving your recommendation is a good thing. It shows you can follow the bank’s guidelines and shows you are looking out to save the asset manager’s time. Of course, back up your recommendations with facts (your bank’s guidelines). Once the bank follows your recommendation and does in fact reject the offer (in this example), then send an email to the selling agent (or buyer if you are representing your in-house buyer) and inform them why the offer was rejected (because of the three-day rule) and encourage them to resubmit it during the appropriate time.

![]() INSIDER TIP

INSIDER TIP

Time is money for asset managers. The more things you can provide them without them having to dig around, the more efficient you will be and the more inventory you will receive.

Rookie Mistake #3: Not Sending a MOM Notification to Every Party

Next, do not forget to send a MOM notification to all parties. Your supplier will provide you with their form to use. Even if the offers that come in during the first round state they are already “highest and best,” you still must send to each selling agent and/or buyer a MOM notification.

What constitutes a MOM situation? By definition a Multiple Offer Monster situation is when more than one offer is placed on a property. However, some banks consider only multiple first-time home buyer offers as a MOM situation.

So if a homeowner offer comes in on day five and an investor offer comes in on day fourteen, the property would not fall under a MOM situation because the investor offer would automatically be rejected for falling within the fifteen-day bank rule. Other banks have a catchall phrase where a MOM is more than one offer regardless of the intent of the buyer (to occupy the home or to invest). When in doubt, email your asset manager immediately and wait for direction.

Never evade a multiple offer situation. For example, if you have a first-time home buyer offer come in on day four and the bank counters it, and meanwhile another first-time home buyer offer comes in on day five, do not tell the other selling agent it’s too late and the bank is negotiating with an offer already. You must notify your asset manager so they can reject all offers and you can present an MOM notice to all parties. Remember, the goal is to provide the most bang for the buck to the bank; maximize its sales price; and provide it the most value.

Another scenario is if a first-time home buyer offer comes in on day four—let’s say for $100,000—and the bank decides to accept the offer. However, it falls under “awaiting approval” status (meaning it’s not officially accepted) and you receive another offer on day fourteen for a substantially greater price, such as $150,000. Expect the asset manager to reject all offers and request a MOM situation.

Even though the original offer might have been your own customer and the second offer is from a cooperating agent, you must always maximize the bank’s value. This means not talking the second offer’s selling agent or buyer out of buying the property, answering your phones, and of course presenting the second offer.

Do not wait an extra day to see if the original offer becomes fully accepted. You may rationalize it to yourself by thinking the second offer came in after office hours or they called on a non-working day (Saturday/Sunday). However, the banks will not follow your questionable logic, especially if they find out you did not present a $50,000 higher offer. In that case, the selling agent or the buyer for the higher offer will file a complaint to the bank (banks usually have toll-free hot-lines) and the heat will be on you. Do not walk over dollars to pick up pennies. It’s not worth it. Present every offer and present every MOM notice promptly.

Rookie Mistake #4: Not Placing the Property in MLS Properly

The next biggest rookie mistake is not placing the property in the MLS entirely, because you may have an in-house buyer you are working with already. During a conference I attended in 2009, I met an REO agent from Tampa, Florida, who was quite pretentious; we’ll call him Hubris.

I believe he was working in real estate part-time and at a packaging facility similar to UPS part-time, and he was bragging about the big $20,000 commission checks that he would make. He was gloating about how he was “strategically missing in action” when it came time to putting the property on the MLS. He would get his leads from his yard signs or his online marketing, get his buyers pre-approved, and keep them waiting until he received his list price from the bank.

As soon as he received his list price, he would write up an offer with his customer and present it to the bank after the first three days. As soon as the single offer was accepted, he would then enter the listing into the MLS and backdate the listing date field by three days.

- Bank gives List Price 12/1/12

- Hubris waits until 12/4/12 to enter his customer’s sole offer (usually at list price)

- Customer offer fully accepted by 12/5/12

- Hubris enters the listing as “active” into MLS on 12/5/12 at 6:00 A.M. Eastern with a back date of 12/2/12 in the listing date field

- Hubris changes status of property on 12/5/12 at 6:05 A.M. Eastern to pending sale.

Therefore, before a soul is awake, he has entered the listing and immediately placed it under contract or “pending sale” five minutes later. Because he backdates the listing by three days, he still falls within his bank guidelines of entering listings into the MLS within twenty-four hours. He gets rich from both sides of the commission and he puts his competition out of business.

As everyone piled up around the water cooler listening to his shady tactics, I knew it would be a matter of time before he would get caught and fired. Sure enough, a couple of months later I heard his license had been revoked and he was back at the packaging facility, this time working full-time.

Moral of the story: place your listings in the MLS ethically and on time. You may cheat the system for a while, but it will catch up to you in the end and perhaps even put you out of business permanently.

Rookie Mistake #5: Making It Difficult for Buyers to Place an Offer

Finally, I have seen agents make it extremely difficult for selling agents and/or consumers to place offers by having thirty- to forty-page offer packets filled with disclosures and requirements so stringent it is as if someone was applying to work for the IRS. The offer packet needs to be as simple as possible. Remember, banks want to promote homeowner-ship and give everyone a fair shot at owning a home. Never put any rules in your offer packet such as “no offers will be submitted without XYZ.”

Also, do not require offers to have a pre-approval by a certain bank unless it’s in your bank’s policies. I have seen many MLS listings that state “pre-approval required by XYZ lender” or “must be approved by XYZ bank for offer to be submitted.” In addition, I have seen many offer packets that have an instruction sheet on how to properly fill out offers. Although this may be helpful for you, it deters buyers from placing offers and selling agents from showing your REO listing. Keep your offer packets pristine and user friendly.

The REO business is about volume. In order to receive it, you must perform ethically. If you hinder offer submissions or violate any of the five biggest rookie mistakes, it will be only a matter of time before you, too, will be looking for employment elsewhere. Only by playing by the rules and working hard will you achieve long-term success. Remember, REOs are not a race—they’re a marathon.

THE DREADED PERFORMANCE REVIEW

There may come a point where you have done everything right, worked 24/7 nonstop to keep your asset manager happy, and gone the extra mile when you had the opportunity to. Even after all this, you can get the dreaded call from the asset manager regarding your performance. This is how it will sound: “Good afternoon, I’m calling about REO AXXXXXX, there were several issues brought up regarding your performance and I think it’s best for you to come into our office to discuss.”

Don’t worry. It happens to the best of us. First, do not panic. Next, never admit guilt! Ever! Don’t give anyone a reason to terminate you; if an asset manager wants you terminated, let them work and prove it. Don’t make it easy for them by admitting guilt (assuming of course you were not guilty).

If they request that you come in, make sure you have at least five days before going in to their office. The first two days will be for you to internalize what just happened, and then the next three days will be for preparing. You will need to prepare for two outcomes:

- Prepare an explanation or apology for your performance issue and say that it will never happen again.

- Gather hard facts and statistics that show how good of an REO listing agent you are and then fight to show that this performance was out of the ordinary.

The latter option will always be better. You want to prove your dedication and drive to be successful, and you will let actions speak louder than words by writing up a detailed report to prevent the occurrence from happening again. In the report, highlight your success with handling their inventory, discuss your eight successful measurement tools (Chapter 11), and discuss how your team or company’s goals are aligned with the bank’s. Try to get two weeks to create this.

Believe it or not, when asset managers call you in for a performance review, they don’t care about how good you once were or how well other asset managers like you; they simply want you to know that your performance was an issue and that they will either suspend you or terminate you. If you have proven your case and have hard facts that show the actual performance issue was out of your control, you can further validate your case by asking for voluntary suspension.

This is when you ask them for time to restructure and minimize errors (whether you had them or not) so you will avoid having them put you on involuntary suspension. You are putting yourself on the offensive. It makes you look good, highlights your work ethic, and shows that you are sincere.

Once you master offers, you will be ready to receive the next biggest document that will leave you one step closer in cashing in on your ATM: the executed contract.

![]() SHARE YOUR STORY

SHARE YOUR STORY

Do you have a success story you would like to share about offers? How about how you spotted one of the three shady offer tactics and how you handled it? How about dealing with mystery shoppers or the dreaded performance review? Please log on and submit it for your chance to be featured in the next revised edition of REO Boom:

POINTS TO REMEMBER

- Never admit guilt in a performance review committee. State your case with hard facts and further validate it by requesting a voluntary suspension.

- Encourage all offers to be submitted, enter listing into the MLS within twenty-four hours, email MOM notices to all parties, present every offer to the bank regardless of time, and keep every offer you receive entirely confidential.

- Avoid the three shady offer tactics (the straw offer, the proxy offer, and the high-low method) at all times and double check county records to make sure first-time home buyers are not investors.

- Call all selling agents and buyers and inform them of their lucky day if the original offer busts.

- Multiple Offer Monster (MOM) is when there is more than one offer on a property and highest and best (H&Bs) offers are needed.

- Use the internal offer checklist to review and submit all offers.

- Prepare the clean copy yourself and email to the selling agent or buyer to sign off on to ensure a twenty-four-hour turnaround time.

- Keep a very short and concise offer package with only the state contract, bank addendum, and any occupancy certifications to sign. Avoid rules and cover pages. If an offer is missing any element, submit it and state what is missing.

- Banks want to maximize their sales price within the shortest period of time.

- The bank’s three-day rule rejects all offers submitted, and the bank’s fifteen-day rule rejects all investor offers submitted.