6

Labour

CHAPTER OUTLINE

3. Important Factors for Controlling Labour Cost

4. Distinction between Direct and Indirect Labour Costs

10. Differential Piece-Rate System (or Taylor's Plan)

11. Merrick's Multiple Piece-Rate Plan

12. Gantt's Task and Bonus Wage Plan

LEARNING OBJECTIVES

After reading this chapter, you should be able to understand the following topics:

- Important factors for controlling labour cost

- Distinction between direct and indirect labour costs

- Labour turnover

- Causes of labour turnover

- Effects of labour turnover

- Measurement of labour turnover

- Time study

- Motion study

- Piece-rate system

- Incentive system of wage payment

6.1 INTRODUCTION

The second most important element of cost (material being the first one) of production is labour. Labour refers to human contribution to production. The efficiency of production to a large extent depends on the proper utilization of labour force. Therefore, control of labour cost is a major problem before a firm's management.

6.2 LABOUR COST

Labour cost is one of the most important factors considered by an entrepreneur before venturing into the industrial field. It helps in studying the extent of expenditure incurred by entrepreneurs on labour welfare and social security aspects, in addition to wages/salaries paid to labour.

Study of labour costs also helps in fixing wages on a realistic basis, logical collective bargaining, evaluation of welfare measures, studying trends over a period of time, deciding on the location of an industry, etc. Labour cost data are also important for policy formulation at the national and regional levels.

Various aspects of labour cost, such as wages/salaries, bonuses, contributions to provident and other funds, and staff welfare expenses for all employees employed directly or through contractors, are collected every year. The total of these components gives the labour cost. When used in line with the number of man-days worked, this gives the average labour cost per man-day worked.

6.3 IMPORTANT FACTORS FOR CONTROLLING LABOUR COST

To exercise an effective control over labour costs, the essential requisite is efficient utilization of labour and allied factors. The main points that need to be considered for controlling labour costs are the following:

- Assessment of manpower requirements.

- Control over timekeeping and time booking.

- Time and motion study.

- Control over idle time and overtime.

- Control over labour turnover.

- Wage systems.

- Incentive systems.

- Systems of wage payment and incentives.

- Control over casual, contract and other workers.

- Job evaluation and merit rating.

- Labour productivity.

6.4 DISTINCTION BETWEEN DIRECT AND INDIRECT LABOUR COSTS

Any labour cost that is specifically incurred for or can be readily charged to or identified with a specific job, contract, work order or any other unit of cost is termed direct labour cost; it includes all labour that is engaged in converting raw materials into manufactured articles in the case of manufacturing industries and other forms of labour that, although not immediately engaged in converting raw materials into manufactured articles, nonetheless are incurred wholly or specifically for any particular unit of production and, hence, can be readily identified with the unit of production.

Individual incentive plan

Straight piecework plan

Standard hour plan

Bedeaux plan

Taylor's differential piece-rate system

Merrick's multiple piece-rate system

Halsey's 50–50 method

Rowan's plan

Gantt's plan

6.5 LABOUR TURNOVER

Labour turnover is the rate at which employees join and leave an organization. In other words, it refers to ‘how long employees tend to stay’ or ‘the rate of traffic through the revolving door’. Turnover is measured for individual companies and for their industry as a whole. If an organization experiences higher rate of labour turnover as compared to their competitor, it is going to affect them adversely. High turnover can be harmful to a company's productivity if skilled workers are often leaving and the worker population contains a high percentage of novice workers.

It is a normal feature in every organization that some workers leave their jobs and some new workers take their place. This change in the labour force is known as labour turnover. In other words, labour turnover denotes the percentage of change in the labour force in an organization. Labour turnover refers to the number of workers left during the period in relation to the average number of workers employed during the period. It refers to the rate of displacement of labour employed in an organization. A high rate of labour turnover denotes that labour is not stable and that there is frequent change in the labour force in an organization. A high labour turnover rate (LTR) is an important indication of high labour cost. It is therefore not desirable.

6.5.1 Internal versus external turnover

Turnover can be classified as ‘'internal'’ or ‘'external'’. Internal turnover involves employees leaving their current positions and taking up new positions within the same organization. Both positive and negative effects of internal turnover exist and, therefore, it may be equally important to monitor this form of turnover as it is to monitor its external counterpart. Internal turnover might be moderated and controlled by typical human resources (HR) mechanisms, such as an internal recruitment policy or formal succession planning.

6.5.2 Voluntary versus involuntary turnover

Experts differentiate between instances of voluntary turnover, which are initiated at the choice of an employee, and instances of involuntary turnover, where the employee has no choice in his or her termination (such as long-term sickness, death, moving overseas, or employer-initiated termination).

Models of turnover

Over the years, there have been thousands of research articles exploring the various aspects of turnover, and in due course several models of employee turnover have been promulgated. The first model, and by far the one inviting the most attention from researchers, was put forward in 1958 by March and Simon. After this model was proposed, there were several efforts to extend the concept. Since 1958 the following models of employee turnover have been published:

- March and Simon (1958)—Process Model of Turnover

- Porter and Steers (1973)—Met Expectations Model

- Price (1977)—Causal Model of Turnover

- Mobley (1977)—Intermediate Linkages Model

- Hom and Griffeth (1991)—Alternative Linkages Model of Turnover

- Whitmore (1979)—Inverse Gaussian Model for Labour Turnover

- Steers and Mowday (1981)—Turnover Model

- Sheridan & Abelson (1983)—Cusp Catastrophe Model of Employee Turnover

- Jackofsky (1984)—Integrated Process Model

- Lee et al. (1991)—Unfolding Model of Voluntary Employee Turnover

- Aquino et al. (1997)—Referent Cognitions Model

- Mitchell and Lee (2001)—Job Embeddedness Model

6.5.3 Causes of labour turnover

A minimum value of labour turnover is common and is good for all industries. But excessive or high labour turnover is dangerous. Excessive labour turnover may occur due to the following reasons:

- Avoidable causes: low wages and allowances, dissatisfaction with the job, poor working conditions, odd working hours, poor interpersonal relationships, poor welfare facilities, unfair methods of product promotion.

- Unavoidable causes: retirement, death while in service, accident, illness, dismissals and marriages in case of women.

6.5.4 Effects of labour turnover

The major effects of labour turnover are as follows:

- Increased cost of new recruitment and training

- Interruption in production

- Decrease in production

- Lack of coordination

- New workers are more prone to accidents.

6.5.5 Costs of labour turnover

The major costs of labour turnover are as follows:

- Additional recruitment costs

- Lost production costs

- Increased costs of training replacement employees

- Loss of know-how and customer goodwill

- Potential loss of sales (for example, if there is high turnover among the sales force)

- Damage that may occur to morale and productivity (an intangible cost)

6.5.6 Benefits of labour turnover

Labour turnover does not just create costs. Some level of labour turnover is important to bring in new ideas, skills and enthusiasm to the labour force. A ‘natural’ level of labour turnover can be a way in which a business can slowly reduce its workforce without having to resort to redundancies.

6.5.7 Measurement of labour turnover

There are three methods for measuring labour turnover:

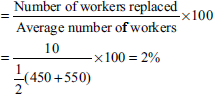

- Separation method (number of employees leaving):

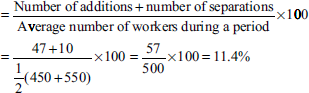

- Replacement method (number of employees joining):

- Flux rate method (number of separations + number of replacements):

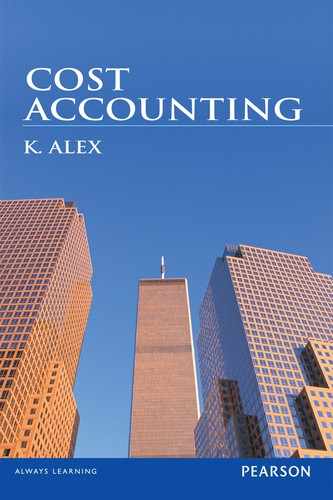

Illustration 1

From the following data provided, find the LTR by applying the (a) flux, (b) replacement and (c) separation methods:

| Number of workers on the payroll: | |

| At the beginning of the month | 450 |

| At the end of the month | 550 |

During the month, eight workers left, 25 workers were discharged and 80 workers were recruited. Of these, 10 workers were recruited in the vacancies of those leaving, whereas the rest of the workers were engaged for an expansion scheme.

Solution:

- LTR by applying the flux method:

- LTR by applying the replacement method:

- LTR by applying the separation method:

Problem 1.

From the following particulars supplied by the personnel department of a firm, calculate labour turnover:

| Total number of employees at the beginning of the month | 2,010 |

| Number of employees recruited during the month | 50 |

| Number of employees who left during the month | 100 |

| Total number of employees at the end of the month | 1,990 |

Illustration 1a

From the following information, calculate LTR:

| Number of workers at the beginning of the year | 3,900 |

| Number of workers at the end of the year | 4,300 |

During the year, 80 workers left while 160 workers were discharged. A total of 800 workers were recruited during the year; of these, 200 workers were recruited because of leavers and the rest were engaged in accordance with an expansion scheme.

Solution:

LTR:

Labour flux rate:

Labour flux rate denotes total change in the composition of labour force due to additions and separations of workers.

Problem 1a. Raghavendra Metal Company gives the following information

| Number of employees on 1 April 1989: 200 |

| Number of employees on 31 March 1990: 240 |

| Number of employees resigned: 40 |

| Number of employees discharged: 26 |

| Number of employees replaced: 11 |

Calculate labour turnover by applying the three methods.

[Madras, B.Sc., (ICE) May 2000; Bharathidasan, B.Com., April 1991]

[Ans: labour turnover under (a) separation method—18.18%, (b) replacement method—5% and (c) flux method—23.18%]

Illustration 1b

From the following data, find the LTR by applying the (a) flux, (b) replacement and (c) separation methods.

The number of workers on the payroll at the beginning of the month is 500 and that at the end of the month is 600. During the month, 15 workers left, 25 workers were discharged and 150 workers were recruited. Of these, 45 workers were recruited in the vacancies of those leaving, whereas the remaining workers were engaged for an expansion scheme.

Solution: Determination of LTR:

- Flux method

- Replacement method

- Separation method

Problem 1b. The personnel department of a concern provides the following information regarding its labour

| Number of employees on 1 January: 1,800 |

| Number of employees on 31 January: 2,200 |

During the month, 20 workers quit and services of 80 workers were terminated. Three-hundred workers are needed; of these, 50 workers are recruited. Calculate LTR.

[Madras, B.Com., (ICE) May 1999]

[Ans: LTR under (a) separation method—10%, (b) replacement method—2.5% and (c) flux method—12.5%]

Hint: The number of workers needed is irrelevant. Those who are actually recruited alone should be taken into account.

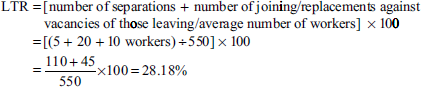

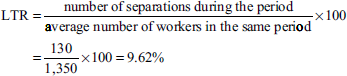

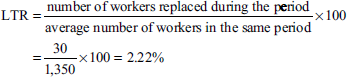

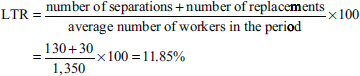

Illustration 2

Different methods of labour turnover

- What is meant by the term labour turnover? What is the effect of labour turnover on cost of production?

- From the following data given by the personnel department, calculate LTR by applying the (a) separation, (b) replacement and (c) flux methods:

Number of workers on the payroll: At the beginning of the month 1,200 At the end of the month 1,500

During the month, 20 workers left, 50 workers were discharged and 200 workers were recruited. Of these, 30 workers were recruited in the vacancies of those leaving, whereas the rest were engaged for an expansion scheme.

Solution:

Average number of workers = (1,200 + 1,500) ÷ 2 = 1,350

- Separation method

- Replacement method

- Flux method

Problem 2. From the following data provided, find the LTR by applying the (a) flux, (b) replacement and (c) separation methods

| Number of workers on the payroll: | |

| At the beginning of the month | 500 |

| At the end of the month | 600 |

During the month, five workers left, 20 workers were discharged and 125 workers were recruited. Of these, 10 workers were recruited in the vacancies of those leaving, whereas the rest were engaged for an expansion scheme.

[I.C.W.A. Inter, June 1993]

[Ans: (a) 18.18%, (b) 1.82%, (c) 20%]

Hint: Replacement method ignores recruitment for expansion. Flux method includes all recruitments including those for expansion.

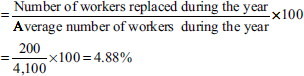

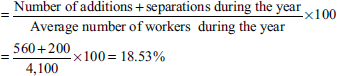

Illustration 2a

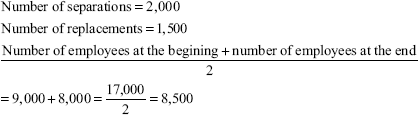

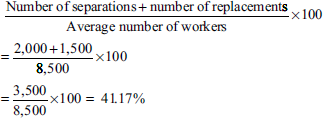

The number of workers on the roll at the commencement of the year were 9,000 and at the end of the year 8,000. The number of separations and replacements during the year were 2,000 and 1,500, respectively. Calculate LTR with the help of the flux method.

Solution: Labour turnover under the flux method:

∴ Under the flux method, LTR is calculated as follows:

Problem 2a. The following information is extracted from the records of a company for the month of October 1998:

| Number of employees at the beginning of the month | 950 |

| Number of employees at the end of the month | 1,050 |

| Number of employees who resigned | 10 |

| Number of employees who were discharged | 30 |

| Number of employees replaced in the vacancies | 20 |

| Number of employees appointed due to an expansion scheme | 120 |

Calculate LTR.

[Madras, B.Com., C & M, Oct. 1990]

[Ans: LTR under (a) separation method—4%, b) replacement method—2%; and (c) flux method—18%]

Hint: Replacement method ignores recruitment for expansion, and flux method includes all recruitments including those for expansions.

6.6 TIME AND MOTION STUDY

It is the analysis of time spent in going through the different motions of a job. Such studies were first instituted in offices and factories in the United States in the early twentieth century. They were widely adopted as a means of improving work methods by subdividing the different operations of a job into measurable elements.

The first effort at time study was made by F. W. Taylor in the 1880s. Early in the twentieth century, Frank and Lillian Gilbreth developed a more systematic and sophisticated method of time and motion study for industry, taking into account the limits of human physical and mental capacity and the importance of a good physical environment.

The idea of a time and motion study is even today often associated with production lines and the manufacturing industry. It is understood as a source of disagreement between management and workers. However, if used properly a time and motion study can be of benefit to modern companies and their workforce. Unfortunately, too many companies still see a time and motion study as simply a way to increase profits with no benefits returning to the workforce who are ultimately responsible for those profits.

6.6.1 Time study

Time study is an art of observing and recording the time required to complete a job. This analysis involves consideration of the following points:

- The worker should have average efficiency.

- The standard fixed cost may change from industry to industry.

- The person who observes the time (timekeeper) must be very careful.

- The standard cost should include necessary rest and accidental and unavoidable delays.

The time study finds the differences between efficient and inefficient workers.

6.6.2 Motion study

Motion study is an art of observing and recording the movements required to complete a job. There are 17 fundamental motions, which are always present in every human activity. Such studies help in eliminating the unnecessary movements of workers and avoid the wastage of energy.

The standard time can be determined accurately with the help of time and motion studies, which is important for determining labour remuneration.

6.6.3 Merits of time and motion studies

The following are some important advantages of time and motion studies:

- These studies help in determining the proper speed of work by eliminating unnecessary movements.

- They help in the fixation of suitable wage rates and introduction of wage incentive plans.

- Efficiency of workers is increased because they are asked to follow correct procedures and methods of work by avoiding useless movements and to save time and energy.

- They help in increasing output, result in greater efficiency in plant organization and lessen human fatigue.

- They help in assessing the correct labour requirements of an organization.

- These studies help to reduce cost of production per unit and increase total earnings of workers.

- They facilitate labour cost budgeting and labour cost control.

6.7 TIME WAGE SYSTEM

This is the traditional method of wage payment. The time spent on work is made the basis for wage calculations. Wages are paid according to the time spent by workers irrespective of their output.

6.7.1 Merits of time wage system

The merits of the time wage system are as follows:

- Simplicity: The method of wage payment is very simple. Workers do not find any difficulty in calculating their wages in this system.

- Guaranteed wage: Workers are guaranteed minimum wages for the time spent by them on the job. There is no link between wages and output; wages are paid irrespective of output.

- Better quality: When workers are assured of wages on time basis, they tend to improve the quality of goods. If wages are related to output, then workers may think of increasing production without bothering about the quality of goods produced.

- Accepted by unions: This method is acceptable to trade unions because it does not distinguish between workers on the basis of their performance.

- Suitable for beginners: Wage rate system is good for beginners because they may not be able to reach a particular level of production in the beginning.

- Less wastage: Under this system, workers are not in a hurry to push through production. Thus, material and equipment are properly handled without wastage.

6.7.2 Demerits of time wage payment

The demerits of time wage payment are as follows:

- Absence of incentive for efficiency: This method does not distinguish between efficient and inefficient workers.

- Wastage of time: Workers may while away their time because they will not be following a target of production.

- Low production: Since wages are not related to output, workers may produce goods at a slower rate.

- Difficulty in determining labour cost: Because wages are not related to output, employees find it difficult to determine labour cost per unit.

- Need for more supervision: Under this system, workers are not offered incentives for production.

- Employer–employee trouble: Treating all employees equally might lead to trouble between the management and workers.

6.8 PIECE WAGE SYSTEM

Piecework or piece work describes the types of employment in which a worker is paid a fixed ‘piece rate’ for each unit produced or action performed. Piecework is also a form of performance-related pay (PRP) and is the oldest form of performance pay.

In a manufacturing setting, the output of piecework can be measured by the number of physical items (pieces) produced, such as when a garment worker is paid per operational step completed regardless of the time required for the step. In a service setting, the output of piecework can be measured by the number of operations completed, as when a telemarketer is paid by the number of calls made or completed regardless of the outcome of the calls (pay for only certain positive outcomes is more likely to be called a sales commission or incentive pay).

6.8.1 Advantages of the piece wage system

- Piece rate can be used for jobs in which the quantity of work done by a person can be measured.

- Piece rate can be modified to provide a guaranteed hourly or weekly minimum wage.

- Piece rate can be used for jobs in which the quantity of work done by a person or a group is readily counted or calculated.

- The steadiness of production and the quality of the product are also fully ensured.

- This system encourages employees to produce more as their wages are related to their productivity.

- It is fair to both employers and employees.

- It provides workers with the opportunity to secure increased compensation.

- The computation of labour cost becomes a very easy task.

- It helps in preparing estimates or tenders.

- It is advantageous to consumers also as now they get products at affordable rates.

- Meritorious workers are rewarded and poor workers penalized under this system.

- Under this system, strict supervision of workers is not required.

6.8.2 Disadvantages of the piece wage system

The disadvantages of the piece wage system are as follows:

- It makes the workers feel insecure because they get wages on the basis of output.

- It lays too much stress on quantity of production at the cost of quality of a product.

- Labour unions oppose the system because it promotes rivalries among workers.

- This system weakens the labour unions because workers get no time for union activities.

- With the intension to produce more workers handle materials and machinery carelessly and damage them.

- In their eagerness for increased earnings, workers may exert themselves to the point of undermining their health and efficiency.

- As this system believes in strict supervision, workers turn hostile in their attitude.

6.9 STRAIGHT PIECE-RATE SYSTEM

Wages are paid in this system in accordance with the output of production. Wage is calculated irrespective of the time spent on a job. Table 6.1 shows the advantages and disadvantages of the straight piece-rate system.

Table 6.1 Advantages and Disadvantages of Straight Piece-Rate Syste

| Advantages | Disadvantages |

|---|---|

| Simple | Discourages quality focus |

| Easy-to-understand focus on productivity | No job security |

| No compensation for breakdown | |

| Suitable for efficient workers | No compensation for sickness |

| No guarantee of minimum wages | |

| Easy to pacify workers | Discourages group effort |

Suitability

|

6.10 DIFFERENTIAL PIECE-RATE SYSTEM (OR TAYLOR'S PLAN)

There are two types of wages fixes: lower and higher. Those who fail to reach the fixed standard are paid lower wages, and those who reach the standard or above the standard are given higher wages. Here the penalty for not reaching the standard is high; hence, workers tend to produce at the minimum fixed rate.

The idea behind this scheme is to induce all workers to at least attain the standard, at the same time if a worker is found efficient he or she stands to gain.

6.10.1 Advantages of the differential piece-rate system

Advantages of the differential piece-rate system are as follows:

- Provides incentives to efficient workers

- Penalizes inefficient workers

- Focuses on high production rate

- Simple and easy to implement

6.10.2 Disadvantages of the differential piece-rate system

Disadvantages of the differential piece-rate system are as follows:

- Minimum wage is not assured.

- There is no consideration for things that are beyond the control of workers, for example, machine failure and power failure.

- There is overemphasis on high production rate.

- There are chances that quality of work may suffer.

6.11 MERRICK'S MULTIPLE PIECE-RATE PLAN

This is a modification over Taylor's plan. In this plan, a minimum base wage is not guaranteed. Wage is calculated as follows:

- When output is less than 83% of standard output, the scheme for wage fixation is equal to piece-rate scheme.

- When output is 83% or more but less than 100% of the standard = 110% of piece rate.

- When output is 100% or more than 100% of the standard = 120% of piece rate.

6.11.1 Advantages of Merrick's multiple piece-rate plan

The advantage of Merrick's plan is that efficient workers are rewarded.

6.11.2 Disadvantages of Merrick's multiple piece-rate plan

The disadvantages of Merrick's plan are as follows:

- There is a wide gap between efficient and inefficient workers.

- Overemphasis is given on production.

6.12 GANTT'S TASK AND BONUS WAGE PLAN

In this plan, a minimum wage is guaranteed. Minimum wage is given to those workers who complete a job in standard time. If the job is completed in less time, then there is a hike in wage rate. This hike varies from 25% to 50% of the standard rate.

6.12.1 Advantages of Gantt's plan

The advantages of the Gantt's plan are as follows:

- Minimum wage is guaranteed.

- The plan is suited to efficient workers.

6.12.2 Disadvantages of Gantt's plan

The disadvantage of the Gantt's plan is that there is emphasis on high speed or high production rate.

6.13 HALSEY'S PREMIUM PLAN

In this plan, incentive is given to a worker who completes work before the standard time to complete a job. However, a minimum base wage is guaranteed to a worker who completes a job in the standard time fixed for the job.

6.13.1 Advantages of Halsey's premium plan

Advantages of Halsey's plan are as follows:

- It is simple.

- It benefits efficient workers.

- It causes no harm to non-performers.

- The management also benefits from the achievements of workers.

- Minimum base wage is guaranteed.

6.13.2 Disadvantages of Halsey's premium plan

Disadvantages of Halsey's plan are as follows:

- Workers get only a percentage of return on their overachievement.

- As a result of placing undue importance on quantity, quality suffers.

- Management gets the wrong picture of a worker's ability.

6.14 ROWAN'S PLAN

In this plan, an incentive for completing a job in lesser time than the standard time is paid to a worker. The incentive is paid on the basis of a ration, which is time saved over standard time per unit standard time.

6.14.1 Advantages of Rowan's plan

Advantages of the plan are as follows:

- Checks overspeeding and overstraining by workers.

- Assures minimum basic wage.

- Rewards efficiency.

6.14.2 Disadvantages of Rowan's plan

Disadvantages of the plan are as follows:

- Discourages workers from overachieving.

- Difficulty in ascertaining wages as it requires much processing of data.

- Sharing of profit for performance by workers may not be liked by them.

6.15 EMERSON'S EFFICIENCY PLAN

In this plan, a minimum time wage is guaranteed. Working conditions and standard output are fixed on the basis of time study. Bonus scheme is as follows (SO refers to standard output and GW refers to guaranteed wages):

- From 66.67% to 80% of (SO) = (GW) + 4% of output.

- From 66.67% to 90% of (SO) = (GW) + 10% of output.

- From 80% to 90% of (SO) = (GW) + 10% of output.

- From 90% to 100% of (SO) = (GW) + 20% of output.

- Above 100% of (SO) = (GW) + 20% of (SO) + 10% of the aforementioned output (SO).

6.15.1 Advantages of Emerson's efficiency plan

Advantages of Emerson's plan are as follows:

- Guarantees minimum wage till 66.67% of standard output.

- Efficient workers are rewarded handsomely.

6.15.2 Disadvantages of Emerson's efficiency plan

Disadvantages of the plan are as follows:

- Disproportionate rate of bonus below standard output

- Chances of overspeeding and compromise of quality

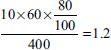

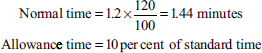

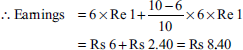

Illustration 3

A work measurement study was carried out in a firm for 10 hours and the following information was generated:

| Units produced | 400 | |

| Idle time | 20% | |

| Performance rating | 120% | |

| Allowance time | 10% of standard time | |

| What is the standard time for the task? |

Solution:

| Units produced | 400 | |

| Time spent | 10 hours | |

| Idle time | 20% |

Therefore, observed time per unit in minutes =

Time per unit is 1.2 minute when performance rating is 120%. Therefore, normal time per unit at 100% performance rating is

Therefore,

Alternatively, standard time may be calculated as follows:

Illustration 4

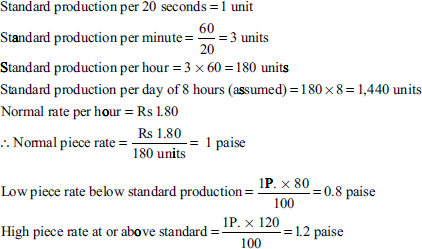

Calculate the earnings of workers A and B under straight piece-rate system and Taylor's differential piece-rate system from the following particulars

| Normal rate per hour = Rs 1.80 |

| Standard time per unit = 20 seconds |

| Differentials to be applied: |

| 80% of piece rate below standard |

| 120% of piece rate at or above standard |

| Worker A produces 1,700 units per day and worker B produces 2,000 units per day |

Solution:

Earnings of worker A:

Under straight piece-rate system,

Under Taylor's differential piece-rate system,

High piece rate has been applied because worker A's daily production of 1,700 units is more than the standard daily production of 1,440 units.

Earnings of worker B:

Under straight piece-rate system,

Under Taylor's differential piece-rate system,

High piece rate has been applied because worker B's daily production of 2,000 units is more than the standard daily production of 1,440 units.

Problem 4. On the basis of the following information, calculate the earnings of A and B under (a) straight piece-rate basis and (b) Taylor's differential rate system:

| Standard production: 8 units per hour |

| Normal time rate: Rs 4 per hour |

| Differential rates to be applied: |

| 80% of piece rate below standard |

| 120% of piece rate at or above standard |

| In a 9-hour day, A produced 54 units and B produced 75 units |

[B. Com., Andhra]

[Ans: (a) A = Rs 27.00 and B = Rs 37.50; (b) A = Rs 21.60 and B = Rs 45.00]

Illustration 5

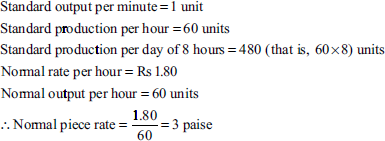

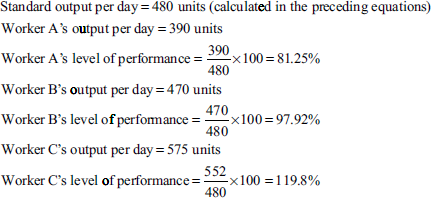

Calculate the earnings of workers A, B and C under straight piece-rate system and Merrick's multiple piece-rate system from the following particulars:

| Normal rate per hour | Rs 1.80 |

| Standard time per unit | 1 minute |

| Output per day is as follows: | |

| Worker A: 390 units | |

| Worker B: 470 units | |

| Worker C: 575 units | |

| Working hours per day are eight. |

Solution:

Calculation of level of performance:

Earnings of worker A:

Under the straight piece-rate system,

Under Merrick's multiple piece-rate system,

Normal piece rate has been applied because worker A's level of performance is 80%, which is below 83%.

Earnings of worker B:

Under the straight piece-rate system,

Under Merrick's multiple piece-rate system,

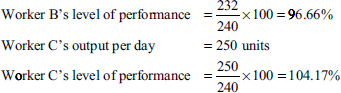

Worker B's level of performance is 93.75%, which is between 83% and 100%; so B is entitled to 110% of normal piece rate (that is, 110% of 3 paise or 3.3 paise per unit).

Earnings of worker C:

Under the straight piece-rate system,

Under Merrick's multiple piece-rate system,

Worker C's level of performance is 115%, which is more than 100% of standard output; so, C is entitled to 120% of normal piece rate (that is, 120% of 3 paise or 3.6 paise per unit).

Problem 5. On the basis of the following information, calculate the earnings of A, B, C and D under Merrick's differential piece-rate system

| Standard production per hour: 12 units | |

| Normal rate per unit: Rs 6 | |

| In an 8-hour day: | |

| A produced | 64 units |

| B produced | 96 units |

| C produced | 84 units |

| D produced | 100 units |

[B. Com. Tirupathi]

[Ans: A—Rs 384.00, B—Rs 633.60, C—Rs 554.40, D—Rs 720.00]

Illustration 6

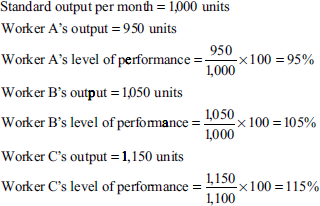

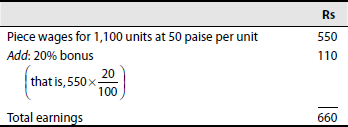

From the following data, calculate the total monthly remuneration of three workers A, B and C under the Gantt's task and bonus scheme:

- Standard production per month per worker is 1,000 units

- Actual production during the month: A—950 units, B—1,050 units and C—1,150 units

- Piecework rate: 50 paise per unit

Solution: Standard production per month is 1,000 units and piecework rate is 50 paise per unit, so guaranteed monthly payment is Rs 500 (that is, 1,000 units at 50 paise).

Level of performance:

Earnings of worker A:

Worker A's level of performance is 95%, which is below the standard performance; so A will get Rs 500, which is the guaranteed monthly payment.

Earnings of worker B:

Worker B's level of performance is 105%; so B will get wages for the standard time and a 20% bonus. Thus, B's earnings will be as follows:

| Rs | |

|---|---|

| Wages for 1,000 units at 50 paise per unit | 500 |

| Add: 20% bonus | 100 |

| 600 |

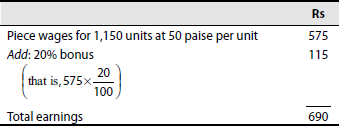

Earnings of worker C:

Worker C's level of performance is 110%, which is more than the standard performance; so C will get piece wages plus 20% bonus.

Thus, his earnings are as follows:

Problem 6. The following are particulars applicable to a work process:

| Time rate: Rs 5 per hour |

| High task: 40 units per week |

| Piece rate above high task: Rs 6.50 per unit |

| In a 40-hour week, each of the following workers produced |

| A—35 units |

| B—40 units |

| C—41 units |

Calculate the wages of the workers under Gantt's task and bonus plan.

[Madras, B.A. Corp. C& M, Sept. 1990]

[Ans: earnings: A: time wages 40 × 5 = Rs 200; B: time wages + 20%, bonus = 200 + 40 = Rs 240; C: high piece rate = 41 × 6.5 = Rs 266.5]

Illustration 7

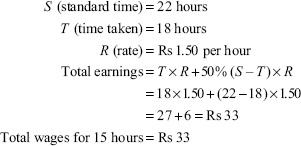

| Rate per hour = Rs 1.50 |

| Time allowed for the job = 22 hours |

| Time taken = 18 hours |

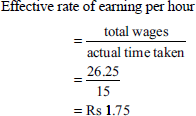

Calculate the total earnings of a worker under the Halsey plan. Also find the effective rate of earning.

Solution:

Therefore, effective rate of earning per hour

Note: The percentage of bonus is to be taken as 50% when it is not given.

Problem 7. Using the following data, calculate the wage payable to a worker under Rowan's premium bonus plan and Halsey's premium bonus plan:

| Time allowed: 40 hours |

| Time taken: 32 hours |

| Rate per hour: Rs 5.00 |

[B. Com., Nagarjuna]

[Ans: Rs 192.00 (Rowan); Rs 180.00 (Halsey)]

Illustration 8

A worker completes a job in a certain number of hours. The standard time allowed for the job is 10 hours, and the hourly rate of wages is Re 1. The worker earns at the 50% rate a bonus of Rs 3 under the Halsey plan. Ascertain the worker's total wages under the Rowan premium plan.

Solution: The worker earns Rs 3 as a bonus at 50%; so total bonus at 100% should be Rs 6. The hourly rate of wages being Re 1, the time saved should be 4 hours.

| Standard time allowed | 10 hours | |

| Add: | Time saved | 4 hours |

| Time taken | 6 hours |

Earnings under the Rowan's premium plan:

where,

T = time taken, that is, 6 hours

S = standard time, that is, 10 hours

R = rate per hour, that is, Re 1

Problem 8. In a manufacturing concern, employees are paid incentive bonus in addition to their normal wages at hourly rates. Incentive bonus is calculated in the proportion of time saved to time allowed. The following are the details of employee X

| Normal wages (rupees per hour) | 4 | |

| Completed units of production | 6,000 | |

| Time allowed (per 100 units) | 0.8 hour | |

| Actual time taken | 42 hours |

You are required to work out the amount of bonus earned and the total amount of wages received.

[Madras, B.A. Corp. C & M, March 1997]

[Ans: bonus earned = Rs 21; standard time = 48 hours; total wages = Rs 189]

Illustration 8a

From the following particulars, you are required to work out the earnings of a worker for a week under (a) straight piece-rate system, (b) differential piece-rate system, (c) Halsey's premium scheme (50% sharing) and (d) Rowan's premium scheme:

| Weekly working hours | 45 | |

| Hourly wage rate | Rs 8.00 | |

| Piece rate per unit | Rs 3.50 | |

| Normal time taken per piece | 20 minutes | |

| Normal output per week | 120 pieces | |

| Actual output per week | 150 pieces | |

| Differential piece rate | 80% of piece rate when output is below normal and 120% of piece rate when output is above normal. |

Solution: Statement showing the computation of earnings of a worker (in a week) under various wage schemes/incentives plans

| Particulars | Amount (Rs) |

|---|---|

| (a) Straight piece rate (actual output per week × piece rate per unit) = (150 units × Rs 3.5) | 525 |

| (b) Differential piece rate (actual output per week × differential piece rate per unit) = (150 units × Rs 3.5 × 120/100, as the output is above normal) | 630 |

| (c) Halsey premium scheme (hours worked per week × rate per hour) + (50% time saved in hours × hourly wage rate) = (45 hours × Rs 8) + 50% (time allowed 20/60 × 150 units = 50 hours − time taken 40 hours) × Rs 8 [= Rs 360 + Rs 40] | 400 |

| (d) Rowan premium scheme (hours worked × rate per hour) + (time saved/time allowed) × time taken × rate per hour = 45 × Rs 8 + [(10 hours/50 hours) × 40 hours × Rs 8] [= Rs 360 + Rs 64] | 424 |

Illustration 8b

Three workers (Govind, Ram and Shyam), having worked for 8 hours, produced 90, 120 and 140 pieces of a product X on a particular day in May in a factory. The time allowed for producing 10 units of X is 1 hour and their hourly rate is Rs 4. Calculate for each of the three workers earnings for the day under the (a) straight piece-rate, (b) Halsey’ premium bonus (50% sharing) and (c) Rowan's premium bonus methods of labour remuneration.

Solution:

- Straight piece-rate system:

Standard labour cost per unit (Rs.4/10) = Re 0.40

Earnings (total) = number of units produced rate per unit

Govind = (90 × Re 0.40) = Rs 36

Ram = (120 × Re 0.40 = Rs 48

Shyam = (140 × Re 0.40) = Rs 56

- Halsey's plan:

Hours worked × rate per hour) + time saved in hours × rate per hour)

Govind = (8 × Rs 4) + (0.50 × nil × Rs 4) Rs 32

Ram = (8 × Rs 4) + [0.50 × (10 – 8)] × Rs 4 = Rs 36

Shyam = (8 × Rs 4) + [0.50] × (12 – 8) × Rs 4 = Rs 40

- Rowan's plan:

(Hours worked × rate per hour) + (time saved / time allowed × time taken × rate per hour

Govind = (8 × Rs 4) + (1/8 hours) × 8 hours × Rs 4 = Rs 36

Ram = (8 × Rs 4) + (4/10) × 8 hours × Rs 4 = Rs 44.8

Shyam = (8 × Rs 4) + (6/12) × 8 hours × Rs 4 = Rs 48

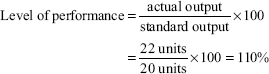

Illustration 9

Standard output per day of 8 hours is 20 units. Actual output of a worker for 8 hours is 22 units. Rate per hour is Rs 2.50. Calculate the wages payable to the worker according to Emerson's efficiency plan.

Solution:

Bonus payable is 45%, which is calculated as follows:

| At 100% efficiency | 20% of time wages |

| For next 10% efficiency at 1% for each | |

| 1% increase in efficiency beyond 100% | 10% of time wages |

| Total bonus payable | 30% of time wages |

Calculation of total wages:

Problem 9. In a manufacturing concern, the daily wages guaranteed for workers is Rs 40. The standard output for a month is 1,000 articles, representing 100% efficiency. The rate of wages is paid without bonus to those workers who show up to 66 2/3% efficiency. Beyond this, bonus is payable in a graded scale

| Efficiency (%) | Bonus (%) |

|---|---|

| 90 | 10 |

| 100 | 20 |

A further increase of 1% of bonus is provided for every 1% increase in efficiency. Calculate the total earnings of A, B, C and D who have worked 26 days in a month with the following productivity: A—500 units, B—900 units, C—1,000 units and D—1,200 units.

[Mysore, B.Com.]

[Ans: earnings of workers: A (only time wages)—26 × 40 = Rs 1,040; B—1,040 + 10% of 1,040 = Rs 1,144; C—1,040 + 20% of 1,040 = Rs 1,248; D—1,040 + 40% of 1,040 = Rs 1,456]

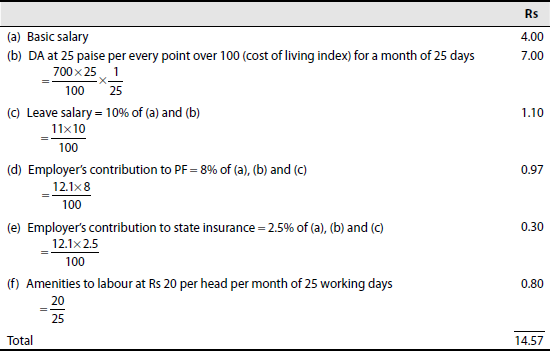

Illustration 10

Form the following particulars prepare labour cost per man-day of 8 hours

| (a) Basic salary | Rs 4 per day |

| (b) Dearness allowance (DA) | 25 paise per every point over 100 (cost of living index for working class); current cost of living index is 800 points |

| (c) Leave salary | 10% of (a) and (b) |

| (d) Employer's contribution to provident fund (PF) | 8% of (a), (b) and (c) |

| (e) Employer's contribution to state insurance | 2.5% of (a), (b) and (c) |

| (f) Expenditure on amenities to labour | Rs 20 per head per mensem |

| (g) Number of working days in a month | 25 days of 8 hours each |

Solution: Statement of labour cost (per man-day of 8 hours):

Problem 10. From the following data, prepare a statement showing the cost per day of 8 hours of engaging a particular type of labour

| (a) | Monthly basic salary plus DA: Rs 1,200 |

| (b) | Leave salary: 5% of (a) |

| (c) | Employer's contribution to PF: 8% of (a) and (b) |

| (d) | Employer's contribution to employees’ state insurance (ESI): 2.5% of (a) and (b) |

| (e) | Pro rata expenditure on amenities to labour: Rs 100 per month |

| (f) | Number of working hours in a month: 200. |

[BCom., Madurai, Calicut]

[Ans: Rs 59.70 per day]

Illustration 11

Calculate the normal and overtime wages payable to a worker from the following data:

| Days | Hours worked |

|---|---|

| Monday | 8 hours |

| Tuesday | 10 hours |

| Wednesday | 9 hours |

| Thursday | 11 hours |

| Friday | 10 hours |

| Saturday | 10 hours |

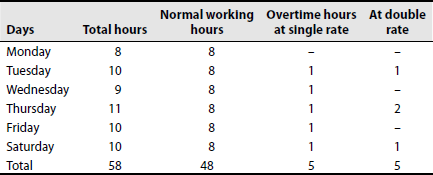

| Total | 58 hours |

| Normal working hours | 8 hours per day |

| Normal rate | Re 1 per hour |

| Overtime rate | Up to 9 hours in a day at single rate and over 9 hours in a day at double rate, or up to 48 hours in a week at single rate and over 48 hours at double rate, whichever is more beneficial to the workers |

Solution:

| Rs | |

|---|---|

| Normal wages for 48 hours at Re 1 | Rs 48 |

| Overtime wages: | |

| At single rate for 5 hours at Re 1 | Rs 5 |

| At double rate for 5 hours at Rs 2 = Rs 10 | Rs 15 |

| Total wages = | Rs 63 |

| Or | |

| Normal wages for 53 hours at Re 1 per hour = | Rs 53 |

| Overtime wages for 5 hours at Rs 2 per hour = | Rs 10 |

| Total wages = | Rs 63 |

Therefore, whichever method is followed, the amount of the wages payable to the worker is Rs 63.

Problem 11. From the following data, prepare a statement showing the cost per man-day of 8 hours:

| (a) | Basic salary and DAs: Rs 300 per month |

| (b) | Leave salary to a worker: 6% of the basic salary and DA |

| (c) | Employer's contribution to PF: 6% of (a) plus (b) |

| (d) | Employee's contribution |

| (e) | Pro rata expenditure on amenities to labour: Rs 25 per head per month |

| (f) | Number of working hours in a month: 200 |

[Madras, B.A. Corp., C & M, Sept. 1995]

[Ans: cost per man-day of 8 hours: Rs 14.48]

Hint: Ignore employee's contribution to PF.

Illustration 12

From the following particulars, prepare a statement of labour cost showing the cost per day (8 hours):

- Monthly salary: Rs 5,000

- Leave salary: 5% of basic salary

- Employer's contribution to PF: 8.5% of (a) and (b)

- Employer's contribution to ESI: 3% of (a) and (b)

- Pro rata experience on amenities to labour: Rs 600 per head per month

- Number of working hours in a month of 25 days: 8 hours per day

Solution: Statement showing the determination of labour cost per day

| Particulars | Amount (Rs) |

|---|---|

| (i) Monthly salary | 5,000 |

| (ii) Leave salary (0.05 × Rs 5,000) | 250 |

| (iii) Contribution to PF [0.85 × (Rs 5,000 + Rs 250)] | 446.25 |

| (iv) ESI (0.03 × Rs 5,250) | 157.3 |

| (v) Allocated share of expenditure on amenities | 600.0 |

| Total labour cost per month | 6,453.55 |

| Number of working days per month | 25 |

| Labour cost per day (Rs 5,828.38/25) | 258.14 |

Problem 12. From the following data, prepare a statement showing the cost per day of 8 hours of engaging in a particular type of labour:

| (a) | Monthly basic salary plus DA: Rs 400 |

| (b) | Leave salary: 5% of (a) |

| (c) | Employer's contribution to PF: 8% of (a) and (b) |

| (d) | Employer's contribution to ESI: 2 ½% of (a) and (b) |

| (e) | Pro rata expenditure on amenities to labour: Rs 35 per head per month |

| (f) | Number of working hours in a month: 200 |

[Madras, B.A. Corp., C & M, May 96]

[Ans: cost per day of 8 hours: Rs 19.96]

Illustration 13

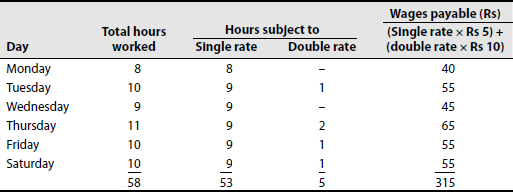

Calculate the normal and overtime wages payable to a worker form the following data:

| Days | Hours worked |

|---|---|

| Monday | 8 |

| Tuesday | 10 |

| Wednesday | 9 |

| Thursday | 11 |

| Friday | 10 |

| Saturday | 10 |

Normal working hours are 8 hours per day, and normal rate is Rs 5 per hour. Overtime rate is up to 9 hours in a day at single rate and over 9 hours at double rate, or up to 48 hours (in a 6-day week) at single rate and over 48 hours at double rate, whichever is beneficial to the workers.

Solution: Statement showing wages payable to a worker (first method):

Statement showing wages payable to a worker (second method):

| (53 hours × Rs 5 per hour) | Rs 265 |

| (5 hours × Rs 10 per hour) | Rs 50 |

| Rs 315 |

Note: Both the methods yield identical sum of wages payable to a worker.

Problem 13. Calculate the normal and overtime wages payable to a worker from the following data:

| Days | Hours worked |

|---|---|

| Monday | 8 |

| Tuesday | 10 |

| Wednesday | 9 |

| Thursday | 11 |

| Friday | 9 |

| Saturday | 4 |

| Total | 51 |

Normal working hours is eight per day, and normal rate is Re 0.50 per hour. Overtime rate is up to 9 hours in a day at single rate and over 9 hours in a day at double rate, or up to 48 hours in a week at single rate and over 48 hours at double rate, whichever is more beneficial to the workers.

[Madras, B. Com., April 2001; Oct. 2000; Madras, B.Com., (ICE) May 2000 (old); Madras, B.Com. C & M, April 1998; B.Com., Sept. 1992; March 1991]

[Ans: total wages paid for the week = Rs 27; on a day basis: normal wages = Rs 22 (44 × 0.5), overtime wages = Rs 5 (4 × .5 + 3 × 1); on a weekly basis: normal wages = Rs 24 (48 × 0.5), overtime wages: Rs 3 (3 × 1)]

Hint: Saturday should be taken as half day with four normal working hours.

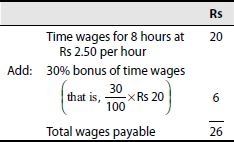

Illustration 14

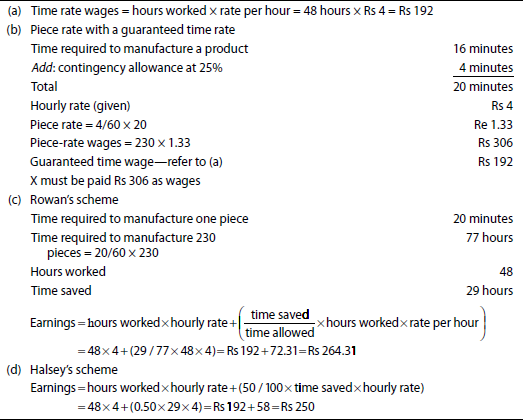

Computation of wages under various methods of wage payment: In an engineering factory, wages are paid on a weekly basis (48 hours per week) at a guaranteed hourly rate of Rs 4.00. A study revealed that the time required to manufacture a product is 16 minutes. However, a contingency allowance of 25% is to be added to this for normal idle time, setting up time, etc. During the first week of June 1986, X produced 230 pieces. Compute X's wages for the particular week using the following methods of wage payment: (a) time rate, (b) piece rate with a guaranteed time rate, (c) Rowan's premium bonus scheme and (d) Halsey's premium bonus scheme.

Solution:

Problem 14. Compute the earnings of a worker under the (a) time rate method, (b) piece-rate method, (c) Halsey's plan and (d) Rowan's plan for the information given as follows

| Wage rate: Rs 5 per hour |

| DA: Re 1 per hour |

| Standard hours: 80 |

| Actual hours: 50 |

[B. Com., Poona]

[Ans: (a) Rs 300, (b) Rs 450, (c) Rs 375 and (d) Rs 393.75]

Illustration 15

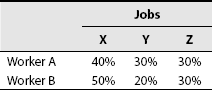

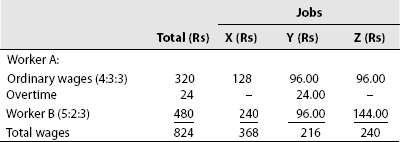

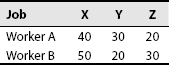

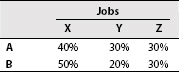

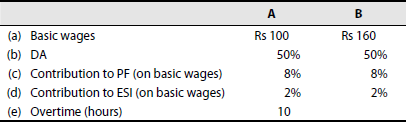

Calculation of workers’ earnings and their allocation to jobs: Calculate the earnings of A and B from the following particulars for a month and allocate the labour cost to each job X, Y and Z:

| A | B | |

|---|---|---|

| (i) Basic wages | Rs 200 | Rs 300 |

| (ii) DA | 50% | 50% |

| (iii) Contribution to PF (on basic wages) | 8% | 8% |

| (iv) Contribution to ESI (on basic wages) | 2% | 2% |

| (v) Overtime (hours) | 12 |

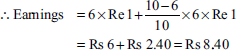

The normal working hours for the month are 200. Overtime is paid at double the total of normal wages and DA. Employer's contributions to ESI and PF are at equal rates with employees’ contributions. The two workers were employed on jobs X, Y and Z in the following proportions:

Overtime was done on job Y.

Solution: Statement showing the earnings of workers A and B

| A | B | |

|---|---|---|

| Workers | Rs 200.00 | Rs 300.00 |

| Basic Wages | 100.00 | 150.00 |

| DA (50% of basic wages) | ||

| Overtime wages [2 (basic wage + DA) 12 hours] ÷ 300 | 24.00 | – |

| = (2 × 150 × 10) ÷ 200 | ___________ | ___________ |

| Gross wages earned | 324.00 | 450.00 |

| Less: PF 8% of basic wages | 16.00 | 24.00 |

| ESI: 2% | 4.00 | 6.00 |

| Wages paid (net) | 344.00 | 480.00 |

Statement of labour cost:

| Gross wages (excluding overtime; Rs) | 300 | 450 |

| Employer's contribution to PF and ESI (Rs) | 20 | 30 |

| Ordinary wages (Rs) | 320 | 480 |

| Labour rate per hour of A (320 ÷ 200) | 1.6 | |

| Labour rate per hour of B (480 ÷ 200) | 2.4 |

Statement showing allocation of wages to jobs:

Problem 15. From the following particulars, prepare a statement of labour cost showing the cost per day (8 hours

| (a) | Monthly salary: Rs 900 |

| (b) | Leave salary: 5% of (a) |

| (c) | Employer's contribution to PF: 8 ½% of (a) and (b) |

| (d) | Employer's contribution to ESI: 3% of (a) and (b) |

| (e) | Pro rata expenditure on amenities to labour: Rs 112 per head per month |

| (f) | Number of working hours in a month of 25 days: 8 hours per day |

[Madras, B. Com. (ICE) C & M, May 1999]

[Ans: cost per day = Rs 46.63]

Illustration 16

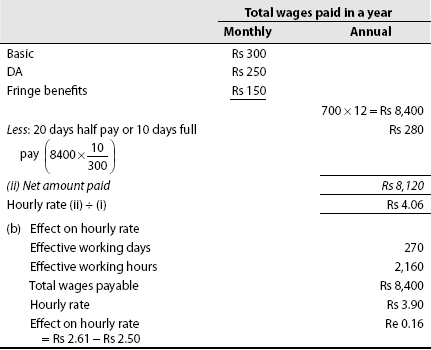

Labour hourly rate: Calculate the labour hour rate of a worker P from the following data:

| Basic pay | Rs 300 per month |

| DA | Rs 250 per month |

| Fringe benefits | Rs 150 per month |

Number of working days in a year is 300. Thirty days with full-pay leave and 20 days with half-pay leave in a year are availed and allowed. Assume 8-hour days. What would be the effect on hourly rate if only 30 days full pay leave is allowed?

Solution:

| (a) Effective working hours | |

| Working days in a year | 300 |

| Less: leave days (30 + 20) | 50 |

| Effective working days | 250 |

| Working hours in a day | 8 hours |

(i) Total effective working hours: 250 × 8 = 2,000 hours

Problem 16. Calculate the labour cost per hour for a worker from the following information

| Basic pay | Rs 200 per month |

| DA | Rs 150 |

| House rent allowance | Rs 100 |

| Number of working days per year—300 | |

| Leave rules | |

| 30 days paid leave (PL) with full pay | |

| 20 days sick leave (SL) with half pay |

Usually, sick leave is fully availed of.

[Madras, B.Com., March 1988]

[Ans: labour cost per hour = Rs 2.34; net labour cost per year = Rs 4,680; effective working days per annum = 250]

Hint: Assume a normal working day of 8 hours.

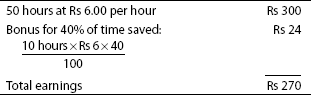

Illustration 17

Calculate the amount of wages and bonus for a worker from the following particulars:

| Job commenced: Monday, 24 December 1994 at 8 a.m. |

| Job finished: Saturday, 29 December 1994 at 1 p.m. |

| Quantity of work turned out: 638 |

| Quantity of pieces passed: 600 |

| Worker's rate: Rs 6.00 per hour |

| Time allowed: 10 pieces per hour |

| Bonus: 40% of time saved |

Assume that the employee worked for 9 hours a day and that there was no overtime.

Solution:

Time taken:

| Monday to Friday: 5 days, 9 hours per day | 45 hours |

| Saturday: 8 a.m. to 1 p.m. | 5 hours |

| 50 hours | |

| Standard time for 600 pieces at 10 pieces per hour | 60 hours |

| Time saved | 10 hours |

Wages for time taken:

Problem 17. The allowed time for a job was fixed as 1 hour by applying the principles of time and motion studies, but the job was completed in 40 minutes. Calculate the wages under the three methods of payment and find the cost per article, assuming the basic time rate of Rs 5 per hour.

[B. Com., Bangalore, Bombay]

[Ans: piece rate = Rs 5.00; Halsey = Rs 4.16; Rowan = Rs 4.44]

Illustration 18

What will be the earnings of a worker at Rs 6.50 per hour when the worker takes 140 hours to do a volume of work for which the standard time allowed is 200 hours. The plan of bonus is on sliding scale as unde

| Bonus within the first 10% of saving in standard time | 40% of time saved |

| Bonus within the second 10% of saving in standard time | 50% of time saved |

| Bonus within the third 40% of saving in standard time | 50% of time saved |

| Bonus within the fourth 10% of saving in standard time | 70% of time saved |

| Bonus for the rest | 75% of the time saved |

Solution:

Time saved = 200 hours − 140 hour = 60 hour

Basic wages = 140 hours × Rs 6.50 = Rs 910.00

Bonus:

| First 10% of 60 hours: 6 hours at 40% | 2.40 hours |

| Next 10% of 60 hours: 6 hours at 50% | 3.00 hours |

| Next 40% of 60 hours: 24 hours at 50% | 12.00 hours |

| Next 10% of 60 hours: 6 hours at 70% | 4.20 hours |

| Rest 30% of 60 hours: 18 hours at 75% | 13.50 hours |

| 100% 60 hours | 35.10 hours |

| 35.10 hours at Rs6.50 | 228.15 |

| Total earnings | Rs 1138.15 |

Problem 18. In a manufacturing concern, bonus to workers is paid on a slab rate based on cost saving towards labour and overheads. The following are the slab rates:

| Up to 10% saving | 5% of earnings |

| Up to 15% saving | 9% of earnings |

| Up to 20% saving | 13% of earnings |

| Up to 30% saving | 21% of earnings |

| Up to 40% saving | 28% of earnings |

| Above 40% saving | 32% of earnings |

The wage rates per hour of four workers P, Q, R and S are Re 1, Rs 1.10, Rs 1.20 and Rs 1.40, respectively. Overhead is recovered on direct wages at the rate of 200%. The standard cost under wages and overhead per unit of production is fixed at Rs 30. The workers completed one unit each in 8, 7, 5½ and 5 hours, respectively. Calculate the following for each worker

| (a) | Amount of hours earned |

| (b) | Total earnings |

| (c) | Total earnings per hour |

[Madras, B.A. Corp. C & M, March 1997]

[Ans: (a) P = Rs 8, Q = Rs 7.70, R = Rs 6.6, S = Rs 7; (b) P = Rs 9.04, Q = Rs 9.32, R = Rs 8.45, S = Rs 8.47; (c) P = Rs 1.13, Q = Rs 1.33, R = Rs 1.536, S = Rs 1.694]

6.16 ADVANCED-TYPE SOLVED PROBLEMS

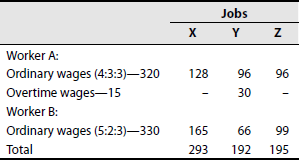

- Calculate the earnings of workers A and B from the following particulars for a month and allocate the earnings to each job X, Y and Z

A B (a) Basic wages Rs 200 Rs 200 (b) DA 50% 55% (c) PF (on basic wages) 8% 8% (d) ESI (on basic wages) 2% 2% (e) Overtime 10 hours – (f) Idle time and leave – 16 hours The normal working hours for the month are 200 hours. Overtime is paid at double the normal wage plus DA. Employer's contributions to ESI and PF are at equal in rate with employee's contributions. The month contains 25 working days and one paid holiday. The two workers were employed on jobs X, Y and Z in the following proportions:

Overtime was done on job Y.

Solution: Statement showing the earnings of workers

A (Rs) B (Rs) Basic wages 200 200 DA 100 110 Overtime wages 30 – Gross wages earned 330 310 Less: Employee's contribution to PF 16 16 Employee's contribution to ESI 4 4 Net wages due 310 290 Statement of labour cost Gross wages (excluding overtime) 300 310 Employer's contribution to PF and ESI 20 20 320 330 Labour cost per hour 1.60 1.65 Allocation of wages to jobs:

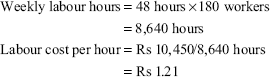

- A factory department has 180 workers who are paid an average wage of Rs 17.50 per week (48 hours) and DA per month (208 hours) of Rs 130. PF deduction is at 8% on gross, of which 1 1/6% is for family pension fund for half the number of workers, and ESI is at Rs 1.25 for each worker. The employer contributes an equivalent amount. The company gives only the minimum bonus of 8 1/3% and allows statutory leave of 2 weeks per year with pay. Show the weekly wage summary for the financial books from the departmental labour hour costs for job costing.

Solution:

Weekly wage summary:

Wages (180 workers at Rs 17.50 each) Rs 3,150.00 DA (48/208 × Rs 130 × 180) Rs 5,400.00 Rs 8,550.00 Bonus (8 1/3% of Rs 8,550) Rs 712.50 Rs 9,262.50 Less: PF contribution (8% -1 1/6% of Rs 8,550) Rs 584.00 Family pension (1/2 of 1 1/6 of Rs 8,550) Rs 50.00 ESI contribution at Rs 1.25 per worker Rs 225.00 Rs 859.00 Net wages Rs 8,403.50 Computation of departmental labour cost:

Wages 3,150.00 DA 5,400.00 Bonus 712.50 PF contribution (584 + 50) 634.00 ESI contribution 225.00 Leave pay (8,550 × 2/52) 328.50 Total labour cost 10,450.00

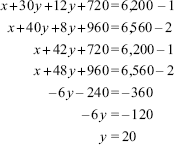

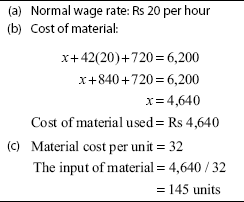

- In a factory, Raja and Ram produce the same product using the same input material at the same normal wage rate. Bonus is paid to both of them according to normal time wage rate adjusted by the proportion of time saved to standard time for the completion of the product. Time allotted to producing the product is 50 hours. Raja takes 30 hours and Ram takes 40 hours to produce the product. The factory costs of the product for Raja are Rs 6,200 and for Ram Rs 6,560. The factory overhead rate is Rs 24 per man-hour.

Calculate the (a) normal wage rate, (b) cost of material used for producing the product and (c) input of material if the unit material cost is Rs 32.

Solution:

Factory cost of Raja

Material x Wages 30y Bonus (40g × 10/50) 12y Overheads 720 x + 30y + 12y + 720 Factory cost of Ram

Material x Wages 40y Bonus (40g × 10/50) 8y Overheads 960 x + 40y + 8y + 960

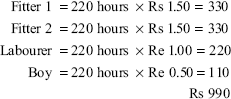

- Two fitters, a labourer and a boy, undertake a job on piece rate for Rs 1,290. The time spent by each of them is 220 ordinary working hours. The rates of pay on time rate basis are Rs 1.50 per hour for each of the two fitters, Re 1 per hour for the labourer and Re 0.50 per hour for the boy. Calculate the following:

- The amount of piecework premium and the share of each worker when the piecework premium is divided proportionately to the time wages paid.

- The selling price of the aforementioned job on the basis of the following additional data: Cost of direct material is Rs 2,010. Works overhead is 20% of prime cost. Selling overhead is 10% of works cost, and profit is 25% on the cost of sales.

Solution:

- Computation of wages:

- The amount of piecework premium:

Piecework wages = Rs 1,290

Time rate wages = Rs 990

Piecework premium = Rs 300

- Apportionment of piecework premium:

Ratio = 330:330:220:110

Fitter 1 = 100

Fitter 2 = 100

Labourer = 67

Boy = 33

- Selling price:

Direct material = Rs 2,010

Direct wages = Rs 1,290

Prime costs = Rs 3,300

Works overhead = Rs 660

Factory cost = Rs 3,960

Selling overhead = Rs 396

Cost of sales = Rs 4,356

Profit = Rs 1,089

Sales = Rs 5,445

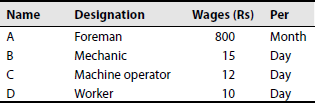

- Following are the particulars for March 2000 relating to four employees working in department A of a factory exclusively for job number 130:

The normal working hours per week of 6 days are 48, or 8 hours per day. All Sundays are paid holidays. (There are no other holidays during the month.)

PF contribution was 8% of monthly wages by employees.

PF contribution was 8% of monthly wages by the employer.

ESI contribution was 3% of monthly wages by employee and 5% of monthly wages by the employer.

From the foregoing data, calculate the following:

- Net monthly wages payable by the employer.

- The total amount of PF contribution to be deposited by the employer.

- ESI contribution to be deposited by the employer.

- Total labour cost to the employer for the month of April, chargeable to the job

- Total cost of the job including the cost of materials valued at Rs 6,000 overheads at 50% of prime cost.

Solution:

(a) Calculation of net wages payable for the month Gross wages for the month (a) Foreman at Rs 800 per month Rs 800.00 (b) Mechanic at Rs 15 per day × 30 days Rs 450.00 (c) Machine operator at Rs 12 per day × 30 days Rs 360.00 (d) Worker at Rs 10 per day × 30 days Rs 300.00 Rs 1,910.00 Less: deductions PF contribution at 8% at Rs 1,910 by employees Rs 152.80 ESI contribution at 3% of Rs 1,910 by employees Rs 57.30 Net wages payable Rs 1,699.90 (b) Employer's share of PF (8% of Rs 1,910) Rs 152.80 Employer's share of PF (8% of Rs 1,910) Rs 152.80 Total amount of PF contribution to be deposited by the employer Rs 305.60 (c) Employer's share of ESI (5% of Rs 1,910) Rs 95.50 Employer's share of ESI (3% of Rs 1,910) Rs 57.30 ESI contribution to be deposited by the employer Rs 152.80 (d) Total labour cost to the employer: Total gross wages Rs 1,910.00 Add: employer's contribution towards PF Rs 152.80 Employer's contribution towards ESI Rs 95.50 Rs 2,158.30 (e) Total cost of job Material Rs 6,000.00 Labour cost Rs 2,158.30 Prime cost Rs 8,158.30 Overheads at 50% of prime cost Rs 4,079.15 Total cost of job Rs 12,237.45 - A, B and C in a particular day produced 200, 250 and 300 pieces, respectively, of a product P. Time allowed for the production of 25 units of P is 1 hour and the hourly rate of wage payment is Rs 8. Calculate for each of these three workers the following under Halsey's premium bonus (50% sharing) and Rowan's premium bonus methods of labour remuneration:

- Earnings for the day (8 hours per day) and

- Effective rate of earnings per hour

Solution: Workers

(i) Computation of earnings per day

(a) Halsey's premium bonus method:

Earnings = hourly rate × time taken + time saved/2

A B C 8 × 8 8 × 8 + (8 × 2/10) 8 × 8 (8 × 8 × 4/12) Rs 64 Rs 76.80 Rs 85.33 - Computation of effective rate of earnings per hour:

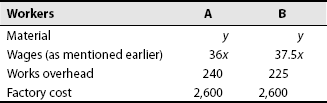

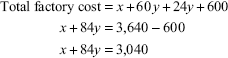

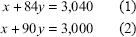

- A job can be calculated using either worker A or worker B. A takes 32 hours to complete the job, whereas B finishes it in 30 hours. The standard time to finish the job is 40 hours. The hourly wage rate is the same for both the workers. In addition, worker A is entitled to bonus according to Halsey's plan (50% sharing), whereas B is paid bonus as per Rowan's plan. Cost of the job comes to Rs 2,600 irrespective of the worker engaged. Find out the hourly wage rate and cost of raw materials input. Also, show the cost against each element of cost included in factory cost.

Solution:

- Computation of time saved and wages:

Workers A B Standard time (hours) 40 40 Actual time (hour) 32 30 Time saved (hour) 8 10 Wages paid for time taken at Rs x per hour (Rs) 32x 30x - Computation of bonus:

- Computation of total works:

Worker A: 32 + 4x = 36x

Worker B: 30x + 7.5x = 37.5x

- Computation of factory cost of the job:

From the aforementioned information, the following simultaneous equations can be written:

On submitting equation (i) from equation (ii), we get the following results:

15x – 15.x = 0or

1.5x = 15or

x = Rs 10 per hourOn substituting the value of x in equation (1), we get

36 × 10 + y + 240 = 2,600or

y = 2,600 – 360 – 240or

y = Rs 2,000The wage rate per hour is Rs 10 and the cost of raw material input is Rs 2,000 for the job.

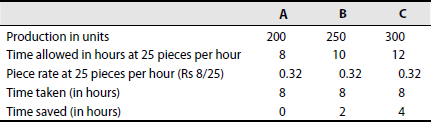

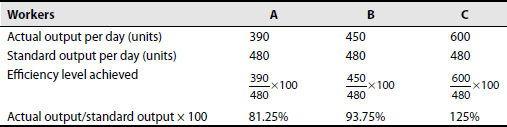

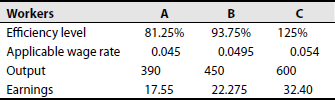

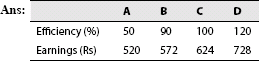

- Calculate the earnings of workers A, B and C under the straight piece-rate system and Merrick's piece-rate system from the following particulars:

Normal rate per hour: Rs 2.70

Standard time per unit: 1 minute

Output per day is as follows:

Worker A: 390 units

Worker B: 450 units

Worker C: 600 units

Working hours per day are eight.

Solution:

Basic calculations:

Normal rate per hour: Rs 2.70

Standard rate per hour: 60 units

Piece rate per unit (2.7/60): 0.045 paise

Efficiency level:

Up to 83% efficiency = Ordinary piece rate

83% to 100% efficiency = 110% of ordinary piece rate

Over 100% efficiency = 120% of ordinary piece rate

Statement of earnings of workers under Merrick's multiple piece-rate system:

- Two workers, Ram and Raju, produce the same product using the same material. Their normal wage rate is also the same. Ram is paid bonus according to the Rowan system, whereas Raju is paid bonus according to the Halsey system. The time allowed to finish the product is 100 hours. Ram takes 60 hours, whereas Raju takes 80 hours to complete the product. The factory overhead rate is Rs 10 per man-hour actually worked. The factory cost for the product for Ram is Rs 3,640 and for Raju is Rs 3,800.

You are required to do the following:

- Find the normal rate of wages

- Find the cost of materials

- Prepare a statement comparing the factory cost of the products as made by the two workers.

Solution:

Basic calculations:

Let x be the cost of material and y be the normal rate of wages per hour.

Factory cost of worker Ram:

Material x Wages 60y Bonus (60y × 40/100) 24y Overheads 600

Factory cost of worker Raju:

Material x Wages 80y Bonus (20y × 50/100) 10y Overheads 800

The two simultaneous equations can be solved as follows to ascertain the values of x and y:

On subtracting equation (1) from equation (2), we get

On putting the value of y in equation (1), we get

- y was presumed the normal wage rate. Hence, the normal wage rate per hour is 7.

- x was presumed the cost of material. Hence, its value is Rs 3,628.

Comparative statement of the factory costs of the products made by the two workers:

Ram Raju Material cost 3,628 3,628 Direct wages 420 560 Bonus 168 70 Factory overheads 600 800 Factory costs 3,640 3,800

CHAPTER SUMMARY

After reading this chapter one must understand that labour is the second most important cost component of a product. Labour cost has certain special features, and controlling it involves facing some peculiar difficulties. Thus, different incentive schemes are used. Labour cost is also important in the light of controlling labour turnover.

KEY FORMULAE

Calculation of labour turnover

-

- Separation method = number of separations during a period/average number of workers during a period × 100.

- Replacement method = number of replacements during a period/number of workers during a period × 100.

- Flux method = number of separations + number of replacements/average number of workers during a period × 100.

- Skill dilution index = number of persons over four years of service at present/total employees × 100.

- Skill wastage index = number of persons over four years of service at present/total employees four years ago × 100.

- Level of activity = actual production in standard hours/budgeted hours.

- Labour efficiency = actual production in standard hours/actual hours worked.

- Labour cost per unit = direct wages/total number of units.

- Labour utilization = actual hours/available hours.

- Absenteeism = number of absentees/average number of employees.

- Accident frequency per week = number of accidents to date/number of weeks to date.

- Illness = hours lost due to illness/total labour hours.

- Labour productivity = production in standard hours/actual hours.

- Earnings under time rate = hours worked × rate per hour.

- Earnings under the straight piece-rate system = number of units × rate per unit.

- Earnings under Taylor's differential piece-rate system = low piece rate if actual output is below the standard value and high piece rate if actual output is above standard.

- Merrick's differential piece-rate system.

Output payment

Up to 83% ordinary piece rate

83% to 100%: 110% of ordinary piece rate

Above 100%: 120% of ordinary piece rate

Labour

- Gantt's task and bonus plan

Output payment

Output below standard time rate

Output at standard 20% bonus on time rate

Output above standard high piece rate on the entire output

- Halsey's premium plan:

Earnings = hours worked × rate per hour + 50% of time saved × rate per hour

- Rowan system:

Earnings = hours worked × rate per hour + time saved / time allowed in hours worked × rate per hour

- Barth variable-sharing plan:

Earnings = rate per hour × square root of standard hours of actual hours

- Emerson's efficiency bonus:

Earnings = actual hours × rate per hour + bonus percentage × hours worked × rate per hour

Bonus calculation

Efficiency bonus

Up to 66 2/3%: no bonus

66 2/3–% to 100%: up to 20% bonus

Above 100%: 20% + 1% for every 1% increase in efficiency

EXERCISE FOR YOUR PRACTICE

Objective-Type Questions

I. State whether the following statements are true or false:

- Timekeeping and time booking are the same.

- The idle-time report should show normal idle time separately from abnormal idle time.

- For reducing labour cost per unit, a high input-to-output ratio is important.

- Productivity of workers can be improved only if they are supervised closely.

- Time and motion study refers to a study to establish a proper method and time.

- Labour once lost cannot be recouped.

- Time and motion study is conducted by the payroll department.

- Job evaluation and job analysis are the same.

- Labour cost is a second major element of cost.

- The human element in labour makes the control of labour cost difficult.

[Ans: 1—false, 2—true, 3—true, 4—false, 5—true, 6—false, 7—true, 8—true, 9—true, 10—true]

II. Choose the correct answer:

- Time and motion study is conducted by

- Payroll department

- Personnel department

- Timekeeping department

- Engineering department

Ans: (d)

- Wage sheet is prepared by

- Cost accounting department

- Payroll department

- Personnel department

- Timekeeping department

Ans: (b)

- Cost of normal idle time is charged to

- Factory overhead

- Office overhead

- Selling overhead

- Administrative overhead

Ans: (a)

- Under Emerson's efficiency plan, the worker gets wages at

- 100% efficiency

- 80% efficiency

- 33 1/3% efficiency

- 66 2/3% efficiency

Ans: (c)

- Under Gantt's task and bonus plan, no bonus is available to a worker if his or her efficiency is lower than

- 100%

- 50%

- 75%

- 66 2/3%

Ans: (a)

- The system that combines both time and piece rate is

- Emerson's system

- Merrick's differential system

- Halsey system

- Bedaux system

Ans: (a)

- The wage system that benefits the less-efficient workers is

- Time wage

- Piece rate

- Halsey's system

- Rowan's system

Ans: (a)

- The method of remuneration that gives stability of labour cost to the employer is

- Group bonus scheme

- Measured day work

- Premium bonus system

- Straight piece rate

Ans: (b)

- Incentive method of wage payment used for indirect workers is

- Gantt's task and bonus plan

- Rowan's plan

- Taylor's differential piece-rate system

- None of the above

Ans: (d)

- Under the high wage plan, a worker is paid

- Normal wage plus bonus

- At a double rate for overtime

- According to his or her efficiency

- At a time rate higher than the usual rate

Ans: (d)

DISCUSSION QUESTIONS

Short Answer-Type Questions

- What do you understand by the term labour turnover?

- What do you mean by labour?

- Discuss the possible effects of labour turnover.

- Enumerate the causes of labour turnover

- Write notes on (a) time study and (b) motion study.

- What is idle time?

Essay-Type Questions

- Discuss the advantages and disadvantages of the following methods of Remuneration: (a) time rate and (b) piece rate.

- How would you treat the following in cost: (a) overtime, (b) leave with pay, (c) idle time and (d) might shift allowance?

- Explain the causes of idle time.

- When is overtime premium charged as an indirect manufacturing cost?

- Distinguish between direct and indirect labour costs.

- Bring out the merits and demerits of the piece-rate system.

- What are the essential features of a sound wage incentive plan?

- Write about some important incentive wage plans.

PROBLEMS

- Rajan Ltd. follows Taylor's differential piece-rate system, 80 and 120 being the differentials for below-standard and above-standard work. From the following data, ascertain the earnings of workers X and Y:

Standard time: 15 minutes per unit Time worked: 8 hours Units produced: X—28 Y—35 Normal piece rate per unit: Rs 2 [Ans: earnings of X = Rs 44.80; earnings of Y = Rs 84.00]

- From the following particulars, calculate the earnings of workers A and B under the piece-rate system:

Standard time allowed: 10 units per hour Normal time rate per hour: Re 1 Differential to be applied: 80% of piece rate when below standard 120% of piece rate at or above standard In a day of 8 hours, A produced 75 units B produced 100 units [Madras, 1999]

[Ans: earnings of workers:]

A (Rs) B (Rs) Straight piece rate 7.5 10 Taylor's differential piece rate 6 12 - Calculate the earnings of workers A and B under the straight piece-rate system and Taylor's differential piece-rate system from the following particulars:

Normal rate per hours: Rs 1.80 Standard time per unit: 20 seconds Differentials to be applied: 80% of piece rate below standard 120% of piece rate at or above standard Worker A produces 1,300 units per day, and worker B produces 1,500 units per day [Madras, 1989]

[Ans: earnings of workers]

A B (Rs ps.) (Rs ps.) Straight piece-rate system 13.00 15.00 Taylor's differential piece-rate system 10.40 18.00 Hint: Assume normal working day of 8 hours.

- Set out a comparative statement showing the effect of paying wages on (a) Halsey and (b) Rowan premium plans assuming the following:

Standard time: 10 hours Hourly wage rate: Rs 5 Time taken: 8 hours Overhead rate per hour: Rs 6 [B. Com., Bangalore]

[Ans: wages are (a) Rs 45 and (b) Rs 48; employer's savings are (a) Rs 17 and (b) Rs 14]

- A worker takes 9 hours to complete a job on daily wages and 6 hours on a scheme of payment by results. His day rate is Rs 7.50 an hour, the material cost of the product is Rs 40 and the overheads are 150% of the total direct wages. Calculate the factory cost of the product under (a) piecework plan, (b) Rowan plan and (c) Halsey plan.

[B. Com., Bombay]

[Ans: (a) Rs 208.75, (b) Rs 190.00, (c) Rs 180.63]

- The standard time allowed for a job is 50 hours. The hourly rate of wages is Rs 4.00 plus a DA of 25 paise per hour worked. The actual time taken by the worker was 40 hours. Calculate the earnings per hour worked under Halsey's premium plan and Rowan's plan.

[B. Com., Madurai]

[Ans: total earnings and hourly rate under Halsey are Rs 190.00 and Rs4.75; total earnings and hourly rate under Rowan are Rs 202.00 and Rs5.05]

- What earnings will a worker receive under Halsey's plan and Rowan's plan if he executes a piece of work in 60 hours as against 75 hours allowed? His hourly rate is Rs 2.00 and he is paid 50% of the time saved under Halsey's plan. He gets a DA of Rs 8.00 per day of 8 hours worked, in addition to his wages.

[B.Com.]

[Ans: under Halsey's plan = Rs 195; under Rowan's plan = Rs 204]

Merrick's Multiple Piece-rate System

- Calculate the earnings of three workers A, B and C under Merrick's plan of piece-rate system, given the following:

Standard production: 120 units Production of A: 90 units Production of B: 100 units Production of C: 130 units Ordinary piece rate: Re 0.10 [Madras, 1999]

[Ans: earnings of workers—A = Rs 9.00, B = Rs 11.00 and C = Rs 15.60]

- On the basis of the following information, calculate the earnings of A, B, C and D under Merrick's differential piece-rate system:

Standard production per hour: 12 units Normal rate per hour: Re 0.60 In an 8-hour day: A produced 64 units, B produced 96 units, C produced 84 units and D produced 100 units [Madras, 1991]

[Ans: earnings of workers—A = Rs 3.20, B = Rs 5.28, C = Rs 4.62 and D = Rs 6.00]

Hint: At 100% efficiency also, 110% of the ordinary piece rate applies.

Halsey's Plan

- Calculate the earnings of a worker from the following information as per Halsey's plan: