7

Overheads Analysis

CHAPTER OUTLINE

3. Classification of Overheads

6. Allocation Vs Apportionment

8. Primary Distribution of Overheads

9. Secondary Distribution of Overheads

LEARNING OBJECTIVES

After reading this chapter, you will be able to understand:

- Overhead costs

- Classification of overheads

- Allocation of overheads

- Apportionment of overheads

- Allocation versus apportionment

- Bases for apportionment

- Distribution of overheads: primary and secondary

7.1 INTRODUCTION

The aggregate of indirect material, indirect labour and indirect expenses is called overhead. These are the costs that cannot be directly allocated to a product or a service. Therefore, these costs have to be shared among various products or services. These overheads are shared among different cost centres and units that use the resources of the organisation.

7.2 OVERHEAD COSTS

Besides materials, direct labour and chargeable expenses, an organization incurs overhead costs. These are the expenses expended for the business as a whole and cannot be attributed to any single department. Therefore, it has become mandatory that these expenses are treated in some sensible manner.

7.2.1 Definition of overhead costs

Overhead costs include all indirect manufacturing and general costs that cannot be associated with specific units of production. Whatever expenses are incurred outside the direct materials and direct labour groups are called overhead costs. Either these expenses cannot be related to particular production departments or they are so small in amount that it is undesirable to assign them to production departments. At the same time, they are essential in some way to the operation of a firm and have to be accounted for. The nature of these expenses is such that they do not increase or decrease proportionately with output.

It must be understood that there is a distinction between indirect expenses and overheads. Overheads represent the estimated or budgeted costs with respect to the indirect material or indirect labour and other indirect expenses. On the other hand, indirect expenses are experienced costs—the actual amounts that have been spent on various items, which cannot be attached to individual units of production.

Overhead is defined as the aggregate of indirect material cost, indirect wages and indirect expenses. The term indirect denotes “that which cannot be allocated but which can be apportioned to or absorbed by cost centres or cost units”. Overhead, therefore, refers to those items of cost that cannot be identified with particular products, jobs or processes. Therefore, they have to be allocated or apportioned on an equitable basis.

7.3 CLASSIFICATION OF OVERHEADS

Overhead charges can be classified in many ways. But the following are the important bases of segregation or classification:

- Functional classification

- Element-wise classification

- Behaviour-wise classification

7.3.1 Functional classification

Functional classification of overheads is based on the three important functions of a business, production, administration and sales, grouped together as overheads. In a large organization, their separation is necessary.

7.3.1.1 Works/factory/production/manufacturing overheads

Manufacturing or production over-heads are also called works on cost and manufacturing or factory cost. These are the expenses incurred in maintaining and operating a manufacturing division of an organization. This category includes all indirect materials used, indirect labour used and other indirect costs incurred in the factory premises. The items that are included under works on cost are the following:

- Operating supplies

- Repairs and maintenance supplies

- Labour cost of set-up, inspection, and moving and rearranging of machinery and equipment

- Factory rent (or a charge where the building is occupied by the owner)

- Factory rates and insurance

- Power and fuel

- Salaries of foremen, supervisors and other operating officers, remuneration of technical directors

- Wages of gatemen, patrolmen, night watchmen, factory clerks, timekeeper, inspectors, storekeepers, tool-room staff, etc.

- Idle time payments, fringe benefits

- Lighting and heating of the works

- Depreciation and maintenance of tools, plant, machinery, land and factory buildings

- Waste disposal

- Training costs

- Hire of machinery

- Laundering

- Cleaning

7.3.1.2 Administrative overheads

These are the indirect expenses that pertain to the performance of management functions. This overhead includes all expenditures incurred in formulating the plans, directing the organization and controlling the operations. These costs are policy costs, which are of fixed

nature and are, therefore, uncontrollable. The common items falling under administrative costs are the following:

- Rent rates and insurance of general offices; lighting, heating and cleaning costs of offices

- Office salaries, including salaries of administrative directors

- Depreciation of office buildings, furniture, machinery, etc.

- Bank charges

- Hire of office machinery

- Audit fees

- Legal expenses

- Office telephone and postages

- Printing and stationery

- Superannuation

7.3.1.3 Selling and distribution overheads

Selling costs are incurred to create demand and to procure orders. Their aim is to promote sales in markets. Distribution costs are expenditures, which begin with making the package produced available for dispatch. The common items falling under selling and distribution costs are the following:

- Salaries, commissions and travelling expenses of salespeople, technical representatives and sales managers

- Advertising

- Catalogues, price lists, etc.

- Rent, rates, maintenance and insurance of showrooms and sales offices

- Selling department's salaries and stationery

- Bad debts and collection charges, etc.

- Legal costs in connection with salespeople's agreements, etc.

- Telephones and postages connected with selling

- Cash discounts allowed

- Market research

- Carriage outward and transport

- Wastage of finished goods

- Warehouse expenses

- Packing materials (secondary)

- Carriage and freight outwards

- Rent, rates, depreciation and insurance of warehouses

- Depreciation and running costs of delivery vans

- Wages of packers, van drivers, etc.

7.3.2 Element-wise classification

Classification of overheads is also done according to the nature and source of expenditure. This classification results from the definition of the overhead concerned. The classification of the total overhead is done element-wise into the following groups:

- Indirect material

- Indirect labour

- Indirect expenses

There are various types of expenses that fall under the categories of indirect material, indirect labour costs and indirect expenses. Some examples of indirect material are consumable stores, fuel and gas. Wages to indirect workers and salaries of foremen and works managers come under indirect labour costs, whereas expenses like insurance, rent and depreciation come under indirect expenses. Expenses that fall under the three categories are shown in Table 7.1.

Table 7.1 Expenses That Fall Under the Categories of Indirect Material, Indirect Labour and Indirect Expenses

| Indirect material | Indirect labour | Indirect expenses |

|---|---|---|

| Fuel | Wages for maintenance workers | Salaries of factory staff |

| Lubricating oil | General indirect labour, salary of storekeeper and foremen | Training expenses |

| Stores consumed for repair and maintenance work | Idle time | Depreciation, plant, machinery and buildings |

| Sundry stores of small value expended for factory use | Workmen's compensation | Insurance |

| Small tools for general use | Overtime and nightshift bonus | Taxes |

| Cotton waste, etc. | Employer's contribution to funds | Rates and rents, lighting and heating of factory |

| Deficiencies, loss and deterioration of stores | Holiday pay/leave pay, miscellaneous allowances to funds | Hospital and dispensary canteen |

7.3.3 Behaviour-wise classification

This classification is made on the basis of the behaviour or nature of overhead costs. The nature of expenses is such that some of them change with the level of activity in the enterprise, while others remain constant. This leads to the fixed, variable and semi-variable categories of overheads such that

Total cost = fixed cost + variable cost + semi-varriable cost

7.3.3.1 Fixed overhead costs

Fixed overhead costs represent costs that are unaffected by variations in the volume of output. These are expenses that must be met regardless of the quantity of production. Managing director's salary is an example, as also is the interest paid on loans, rent, rates, audit fees, etc. These do not vary with variation in the volume of production. But this is not true at all times. After a certain level of activity, fixed costs start to rise, although definitely not in direct proportion with the volume of output.

7.3.3.2 Variable overhead costs

Variable overhead costs tend to increase or decrease in their total amount with changes in productive activity. In many cases, the change is in direct proportion with the output. But this may not always be the case. The examples of variable costs, in addition to direct materials and direct labour, are as follows:

Repair

Power

Fuel

Indirect labour

Indirect material

Lubricants

Store's handling and losses

Worker's compensation

Tools and spares

Salespeople's commission

7.3.3.3 Semi-variable overhead costs

Semi-variable overhead costs are costs that neither remain fixed nor vary directly with the output. These are mixed costs; they are partly fixed and partly variable. A part of the cost remains fixed up to a particular level, and the other part fluctuates with fluctuations in activity. For example, power, repair, maintenance, clerical cost and depreciation may remain fixed up to a certain level of output. But after this level, they vary with the production.

Another good example of semi-fixed overhead is telephone expenses. The rent is a fixed portion of overhead, whereas charges for calls are variable overheads. However, the range and extent of variability may be different for different items of overhead costs.

7.4 ALLOCATION OF OVERHEADS

It is a process of charging the full amount of cost to a cost centre or cost unit. The allocation can be done only when the cost definitely relates to a particular cost centre. Cost allocation is possible when we can identify a cost as specifically attributable to a particular cost centre; for example, the salary of the manager of the packing department can be allocated to the packing department cost centre. It is not necessary to share a salary cost over several different cost centres.

7.5 APPORTIONMENT OF OVERHEADS

It is a process of charging expenses in an equitable proportion to the various cost centres or cost units. Apportionment is done for those items that cannot be allocated to any specific cost centre. Cost apportionment is necessary when it is not possible to allocate a cost to a specific cost centre. In this case, the cost is shared by two or more cost centres according to the estimated benefit received by each cost centre. As far as possible the basis for apportionment is selected to reflect the benefit received.

7.6 ALLOCATION VERSUS APPORTIONMENT

Allocation is distinct from apportionment in the following aspects:

- Allocation deals with whole items of cost. Apportionment deals with a portion of items of cost.

- Allocation does not need any bases. Apportionment is mainly done according to some bases.

- Allocation is a direct distribution of costs. Apportionment is an indirect distribution of costs.

7.7 BASES FOR APPORTIONMENT

Some of the bases that are generally adopted for the apportionment of expenses are stated in Table 7.2.

Table 7.2 Some of Bases Adopted for the Apportionment of Expense

| Expenses | Bases |

|---|---|

| Factory rent | Square feet |

| Power | Kilowatt hour (KWH) |

| Indirect material | Direct material |

| Indirect wages | Direct wages |

| Repairs to plan | Plant value |

| Depreciation | Plant value |

| Lightings | Light points |

| Supervision | Number of employees |

| Fire insurance of stock | Stock value |

| Fire insurance of capital assets | Value of capital assets |

| Employees’ state insurance (ESI)/provident fund (PF) contribution of employer | Wages of each department |

| Labour welfare expenses | Number of employees |

| General factory overheads | Labour hours/direct wages |

| Audit fees | Sales/total cost |

| Delivery expenses | Weight/volume |

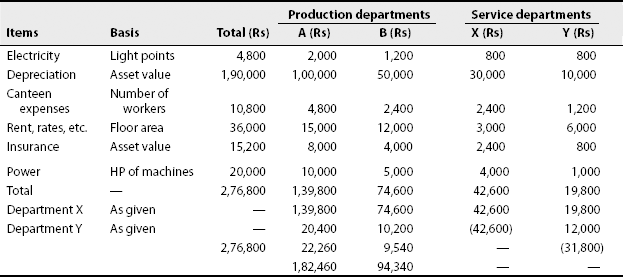

7.8 PRIMARY DISTRIBUTION OF OVERHEADS

It is the process of allocating and apportioning costs on a suitable basis to all departments or cost centres. Primary distribution is done without any distinction between production and service departments. It is an overhead apportionment process by which common expenses are distributed among the user departments. The apportionment is done on a suitable basis. Appropriate bases for the distribution of common expenses are given in Table 7.3.

Table 7.3 Appropriate Bases for the Distribution of Common Expense

| Cost items | Apportionment bases |

|---|---|

| 1.Repairs and maintenance of buildings | Floor space |

| 2. Lighting | Watts allotted or sub-meter reading |

| 3. Water | Volume consumed |

| 4. Telephone | Number of calls |

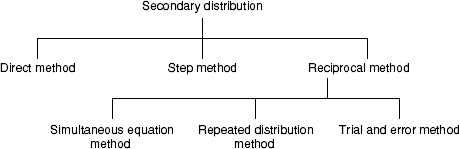

7.9 SECONDARY DISTRIBUTION OF OVERHEADS

It is a process of redistribution of service departments’ costs to production departments. Secondary distribution is also known as reapportionment or redistribution.

Figure 7.1 Reveals the various methods of secondary distribution of overheads.

Figure 7.1 Various Methods of Secondary Distribution of Overheads

ILLUSTRATIONS—BASES FOR APPORTIONMENT

Illustration 1

Indicate the basis you would adopt for apportioning the following items of overhead expenses to different departments:

- Factory rent

- Factory lighting

- Power

- Depreciation of plant and machinery

- Insurance of plant and machinery, and fire insurance of stock

- Welfare expenses

- Material-handling charges

- Indirect material

- Indirect wages

- Supervision

- Repairs to plant

- Insurance of building

- Staff recreation

- Canteen expenses

- Creche expenses

- Employer's contribution to ESI

- Employer's contribution to PF

- Stores’ expenses

- Sundry expenses

Solution: Bases for apportionment of overhead expenses

| Expenses | Basis for apportionment |

|---|---|

| (a) Factory rent | Floor area |

| (b) Factory lighting | Light points, floor area |

| (c) Power | KWH; horsepower (HP) of plant |

| (d) Depreciation of plant and machinery | Machine hours, value of plant |

| (e) Insurance of plant and machinery | Insurable value of plant and machinery |

| (f) Insurance of stock | Value of stock |

| (g) Welfare expenses | Number of employees |

| (h) Material-handling charges | Value of material |

| (i) Indirect material | Direct material |

| (j) Indirect wages | Direct wages |

| (k) Supervision | Number of employees |

| (l) Repairs to plant | Value of plant |

| (m) Insurance of building | Value of building, floor area |

| (n) Staff recreation | Number of employees |

| (o) Canteen expenses | Number of employees |

| (p) Creche expenses | Number of female employees |

| (q) Employer's contribution to ESI | Wages of each department, number of employees |

| (r) Employer's contribution to PF | Wages of each department, number of employees |

| (s) Stores expenses | Materials consumed by each department |

| (t) Sundry expenses | Labour hours, direct wages |

Problem 1. Indicate the bases of apportionment for the following overhead expenses: (1) rent, rates and taxes; (2) employees’ contribution to state insurance; (3) power; (4) repairs and maintenance; (5) employer's contribution to PF; (6) supervision; (7) factory cleaning; (8) insurance of building; (9) general expenses; and (10) creche expenses.

[Ans: (1) floor area, (2) wages, (3) KWH or HP of machines, (4) asset value, (5) wages, (6) number of employees, (7) floor area, (8) building value, (9) labour hours or direct wages, (10) number of female employees]

Illustration 2

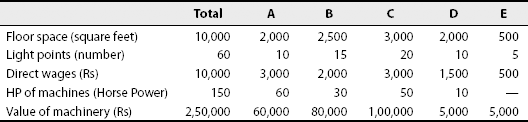

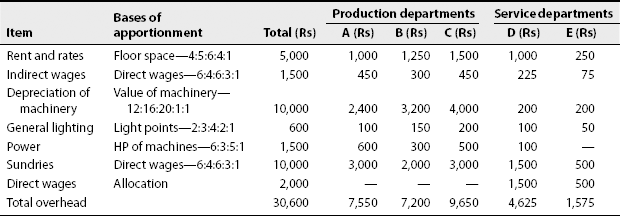

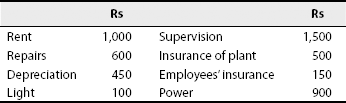

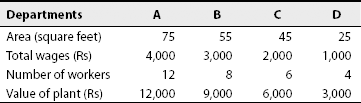

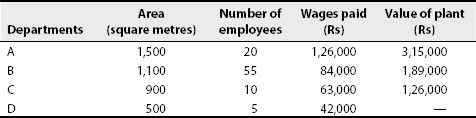

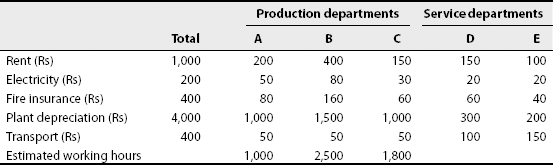

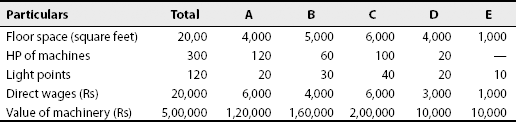

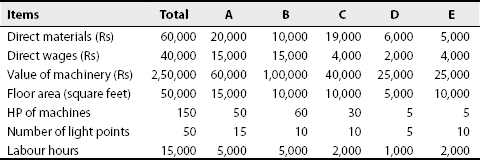

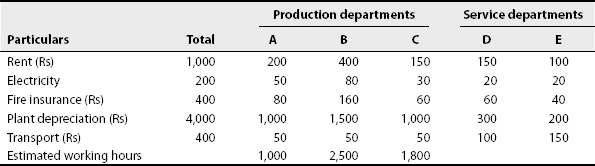

Kumaresh Ltd. has three production departments, A, B and C, and two service departments, D and E. The following figures are extracted from the records of the company:

| Rs | |

|---|---|

| Rent and rates | 5,000 |

| Indirect wages | 1,500 |

| Depreciation of machinery | 10,000 |

| General lighting | 600 |

| Power | 1,500 |

| Sundries | 10,000 |

The following further details are available:

Apportion the cost to various departments on the most equitable basis by preparing a primary departmental distribution summary.

Solution: Primary overhead distribution summary:

Note: Direct wages of service departments are also included in the distribution summary since they should also be reapportioned to the production departments and should finally be absorbed by the output. Ignoring the direct wages of service departments will result in ‘unabsorbed expenses’.

Problem 2. A company has four departments. The following are the expenses recorded for a period of three months:

The following data are also available:

Prepare a statement showing the apportionment of cost to the various departments. Compute departmental rates of recovery.

[B. Com., Bangalore]

[Ans: A—Rs 2,053; B—Rs 1,483; C—Rs 1,067; D—Rs 597]

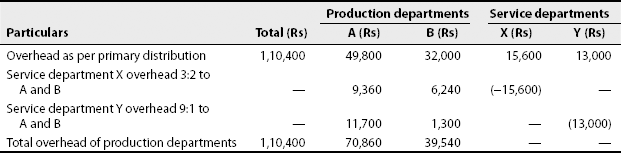

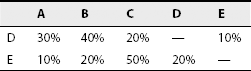

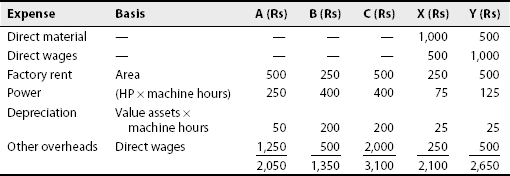

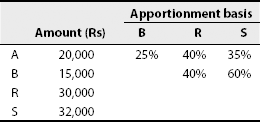

Illustration 2a

Calculate the overheads allocated to production departments A and B from the following information: There are two service departments X and Y. X renders service to A and B in the ratio 3:2 and Y renders service to A and B in the ratio 9:1. The overheads as per primary overhead distribution are as follows: A—Rs 49,800; B—Rs 32,000; X—Rs 15,600; and Y—Rs 13,000

Solution: Secondary overhead distribution summary:

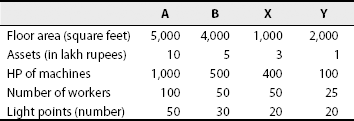

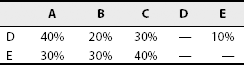

Illustration 3

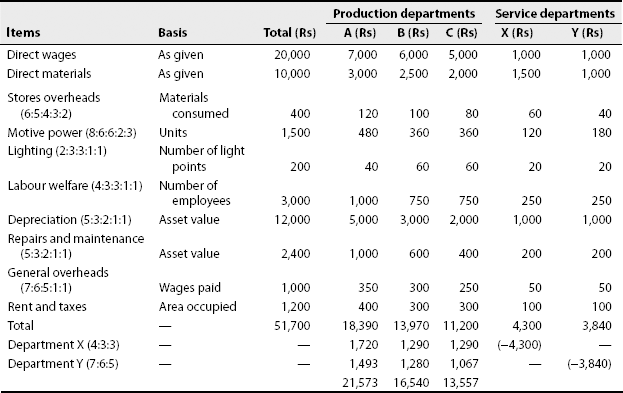

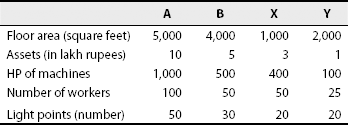

Calicut Soaps Ltd. supplies you the following information for the month ending on January 1988. You are required to apportion the overheads to production departments:

The expenses (in rupees) for the month were as follows:

| Stores overheads | Rs 400.00 |

| Motive power | Rs 1,500 |

| Lighting | Rs 200 |

| Labour welfare | Rs 3,000 |

| Depreciation | Rs 12,000 |

| Repairs and maintenance | Rs 2,400 |

| General overheads | Rs 1,000 |

| Rent and rates | Rs 1,200 |

Apportion the expenses of department Y in the proportion of direct wages and those of X in the ratio 4:3:3 to departments A, B and C, respectively.

Solution: Apportionment of overhead to production departments:

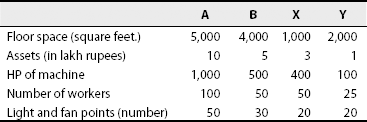

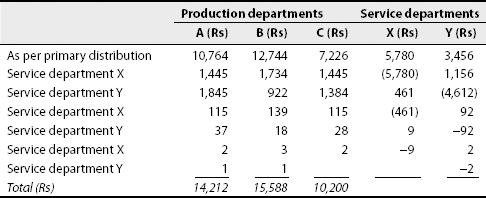

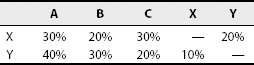

Problem 3. Calculate the overheads applicable to production departments A and B. There are also two service departments X and Y. X renders services worth Rs 12,000 to Y and the balance to A and B in the ratio 3:2. Y renders services to A and B in the ratio 9:1.

Expenses and charges are

[B. Com., Madras]

[Ans: A—Rs 1,86,780; B—Rs 90,020]

Illustration 4

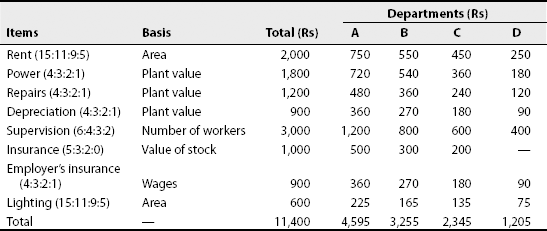

A company has four departments. The actual costs for a period are given here. Apportion the costs to various departments using the most equitable method.

| Rs | |

|---|---|

| Rent | 2,000 |

| Repairs | 1,200 |

| Depreciation | 900 |

| Light | 200 |

| Supervision | 3,000 |

| Employer's liability insurance | 300 |

| Insurance | 1,000 |

| Power | 1,800 |

The following data are also available for four departments:

Solution: Apportionment of cost to departments:

Note: Insurance has been apportioned on the basis of the value of stock, under the assumption that it is only with regard to stock. Lighting has been distributed on the basis of area as no other relevant data are available as to the number of light points.

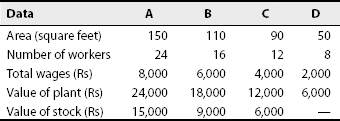

Problem 4. A company has four departments, of which A, B and C are production departments and D is a service department. Costs of department D are apportioned on the basis of wages paid. The actual costs for the year are

| Rent | Rs 21,000 |

| Repairs to plant | Rs 1,26,000 |

| Depreciation of plant | Rs 9,450 |

| Light and power | Rs 2,100 |

| Supervision | Rs 31,500 |

| Repairs to building | Rs 8,400 |

The following information about departments is available and is used as a basis for the distribution of costs:

Apportion these costs to production departments.

[Ans: A—Rs 1,08,547.50; B—Rs 83,220.50; C—Rs 48,682.00]

Illustration 5

Calculate the overheads that can be allocated to the production departments A and B. There are also two service departments X and Y. X renders services worth Rs 12,000 to Y and the balance to A and B in the ratio 2:1. Y renders services to A and B in the ratio 7:3.

The expenses include

| Rs | |

|---|---|

| Depreciation | 1,90,000 |

| Rent, rates, etc. | 36,000 |

| Insurance | 15,200 |

| Power | 20,000 |

| Canteen expenses | 10,800 |

| Electricity | 4,800 |

Solution: Overhead distribution summary:

Problem 5. The following figures have been extracted from the accounts of a manufacturing concern for the month of January

| Rs | |

|---|---|

| Indirect materials: | |

| Production department X | 950 |

| Production department Y | 1,200 |

| Production department Z | 200 |

| Maintenance department P | 1,500 |

| Stores department Q | 400 |

| Indirect wages: | |

| Production department X | 900 |

| Production department Y | 1,100 |

| Production department Z | 300 |

| Maintenance department P | 1,000 |

| Stores department Q | 650 |

| Power and light | 6,000 |

| Rent and rates | 2,800 |

| Insurance on assets | 1,000 |

| Meal charges | 3,000 |

Depreciation is at 5% on capital value of assets. From the following additional information, calculate the share of overheads for each production department:

[B. Com., Madras]

[Ans: X—Rs 9,000; Y—Rs 9,600; Z—Rs 4,400]

Illustration 6

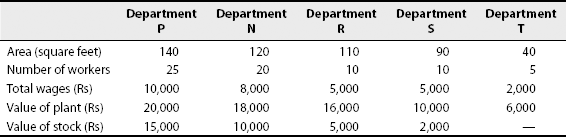

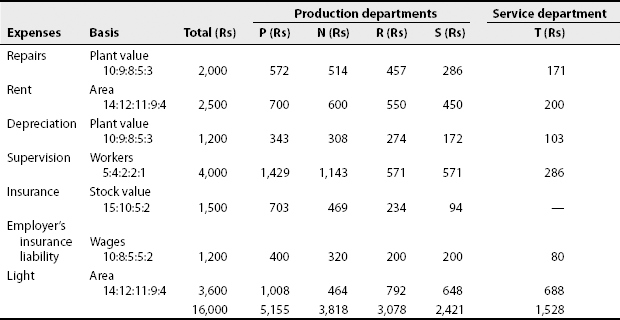

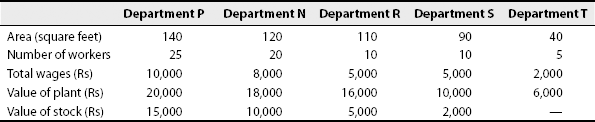

Amit Company has five departments; P, N, R and S are producing departments, and T is a service department. The actual costs for a period are as follows:

| Rs | |

|---|---|

| Repairs | 2,000 |

| Rent | 2,500 |

| Depreciation | 1,200 |

| Supervision | 4,000 |

| Insurance | 1,500 |

| Employer's liability of employees’ insurance | 1,200 |

| Light | 3,600 |

The following data are also available regarding the five departments:

Apportion the costs to various departments on an equitable basis.

Solution: Apportionment of costs to departments:

Problem 6. Superfines Ltd. furnished the following particulars for the half year ending on 31 March 1994. Compute the departmental overhead rates for each of the production departments, assuming that overheads are recovered as a percentage of direct wages.

Overhead expenses for the aforementioned period were

| Rs | |

|---|---|

| Motive power | 3,300 |

| Lighting | 400 |

| Stores expenses | 800 |

| Staff welfare expenses | 4,800 |

| Depreciation | 30,000 |

| Repairs | 15,000 |

| Rent, rates and taxes | 1,200 |

| General expenses | 12,000 |

Apportion the expenses of service department X in proportion to direct wages and those of service department Y in the ratio 5:3:2 to production departments A, B and C, respectively.

[Ans: A—Rs 26,871; B—Rs 22,144; C—Rs 18,485; overhead rates as a percentage of direct wages: A—671.78%, B—369.07%, C—231.06%]

7.10 STEP METHOD

Under this method, all service departments are arranged in the order of their utility in terms of service provided to other departments. Then, the cost of the most serviceable section is first apportioned to another service department as well as to production departments. The service department that serves the next largest number of departments is then taken up, and in this way the process continues till the costs of all service departments are apportioned. Obviously, the cost of the last service department will be apportioned only to production departments.

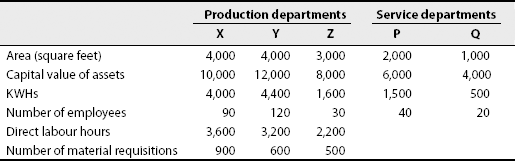

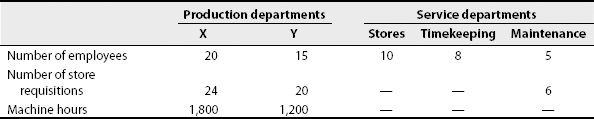

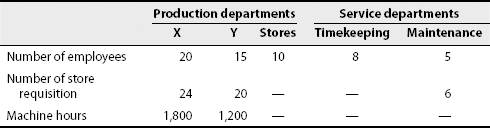

Illustration 7

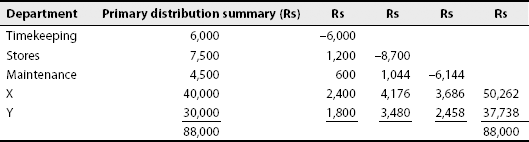

A manufacturing company has two production departments, X and Y, and three service departments, timekeeping, stores and maintenance. The departmental distribution summary showed the following expenses for January 1986:

| Production departments | |

| X | Rs 40,000 |

| Y | Rs 30,000 |

| Service departments | |

| Stores | Rs 7,500 |

| Timekeeping | Rs 6,000 |

| Maintenance | Rs 4,500 |

Other information relating to these departments is as follows:

Apportion the costs of service departments to production departments X and Y.

Solution:

Basis of apportionment:

| Timekeeping—10:5:20:15 (number of employees) |

| Stores—6:24:20 (number of requisitions) |

| Maintenance—18:12 (machine hours) |

Problem 7. A manufacturing company has two production departments, X and Y, and three service departments, timekeeping, stores and maintenance. The departmental summary shows the following expenses for October:

| Rs | Rs | |

|---|---|---|

| Production departments: | ||

| X | 16,000 | |

| Y | 10,000 | 26,000 |

| Service departments: | ||

| Timekeeping | 4,000 | |

| Stores | 5,000 | |

| Maintenance | 3,000 | |

| 12,000 | ||

| 38,000 |

Other information regarding the departments is as follows:

You are required to make departmental allocation of expenses.

[B.Com., Madurai]

[Ans: X—Rs 22,845; Y—Rs 15,155]

7.11 RECIPROCAL METHOD

Reciprocal method recognizes that if one service department receives service from another department the department receiving the service should be charged. It two service departments provide service to one another, each department should be charged for the cost of service rendered by the other.

There are three methods that may be used for reciprocal distribution:

- Simultaneous equations method

- Repeated distribution method

- Trial-and-error method

7.11.1 Simultaneous equations method

In this method, the total overhead cost for each service department is expressed in the form of algebraic equations with the help of percentage distribution of service cost. These simultaneous equations are solved to arrive at the results.

7.11.2 Repeated distribution method

This method consists of closing and reopening the departmental service accounts by successive distributions. The steps involved in this method are as follows:

- Apply the given percentages to distribute the primary total of the first service department. This closes the account of the first service department and charges the amounts to other departments.

- Apply the given percentage to the second service department whose total is made up of primary charges plus the amount apportioned from service department number 1. This closes the second department's account.

- Apply the same percentage to all other service departments.

- Repeat this process of distribution again with service department number 1 whose total at present consists of only amounts apportioned from other service departments. In this way, the service department totals become lower and lower with each process of distribution, because for each distribution a substantial amount is charged to the producing departments.

- Stop this process at the point where it is felt that the remaining figures are too small to be of any consequence.

7.11.3 Trial-and-error method

This method can be easily used when there are two or three service centres involved. Here, the cost of one service centre is apportioned to another centre. The cost of another centre plus the share received from the first centre is apportioned back to the first centre, and this process is repeated till the balancing figure becomes negligible.

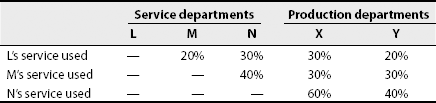

Illustration 8

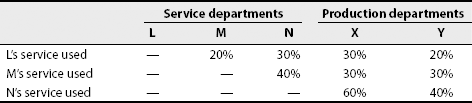

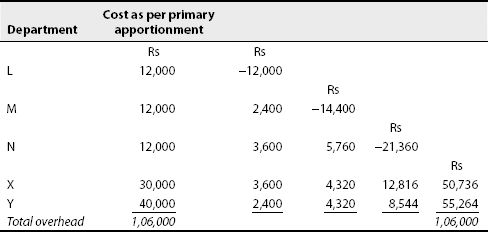

A factory has three service departments, L, M and N, and two production departments, X and Y. The following are the expenses allocated and apportioned to the departments as per primary distribution summary:

The following additional information extracted on the basis of a detailed analysis is also available:

Prepare a statement showing apportionment of service department overheads under the step method.

Solution: Statement showing secondary distribution of overhead:

Note: While writing the different departments in the statement under the step method, the service departments that service the largest number of other departments should be written first. For example, in the aforementioned case, L department serves four other departments. Similarly, in the order of number of other departments served the remaining service departments are written. Finally, the production departments are written one by one.

Problem 8. A manufacturing company has two production departments, P1 and P2, and three service departments, time booking, stores and maintenance. The following are the particulars for July 1978:

| Production departments: | ||

| P1 | Rs 16,000 | |

| P2 | Rs 10,000 | Rs 26,000 |

| Service departments: | ||

| Stores | Rs 5,000 | |

| Time booking | Rs 4,000 | |

| Maintenance | Rs 3,000 | Rs 12,000 |

| Rs 38,000 |

Other information relating to the departments is as follows:

Apportion the cost of service departments to production departments as per the step method.

[Madras, B.Com., March 1988; Madurai, B.Com., April 1998]

[Ans: total overheads of production departments: P1—Rs 22,842; P2—Rs 15,158]

Hint: Apportion time-booking expenses to other departments in the number of employees ratio.

Illustration 9

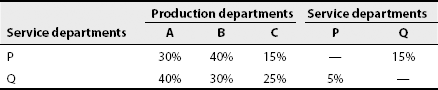

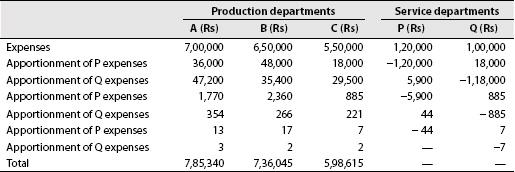

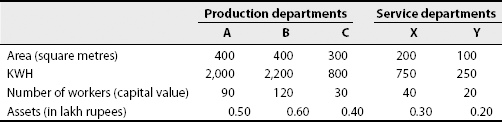

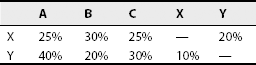

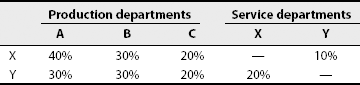

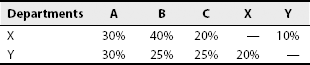

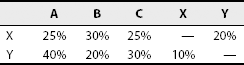

In a factory, there are two service departments P and Q and three production departments A, B and C. In April, the departmental expenses were as follows:

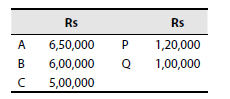

| A—Rs 7,00,000 | P—Rs 1,20,000 |

| B—Rs 6,50000 | Q—Rs 1,00,000 |

| C—Rs 5,50,000 |

The service department expenses are allotted on a percentage basis as follows:

Prepare a statement showing the distribution of expenses of the two service departments to three departments under the repeated distribution and simultaneous equations methods.

Solution: Repeated distribution method:

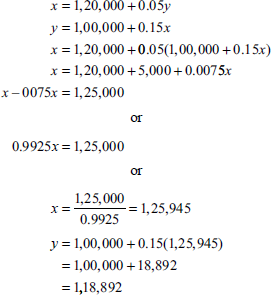

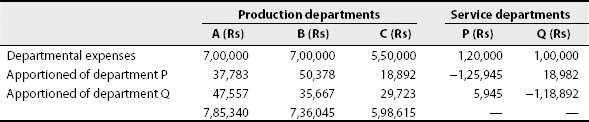

Simultaneous equations method:

Let x be the total overhead of department P

Let y be the total overhead of department Q

Apportionment of overheads:

Problem 9. A company has three production and two service departments. Departments and their respective expenditures are given as follows

| Production departments | Service departments |

| A—Rs 800 | X—Rs 234 |

| B—Rs 700 | Y—Rs 300 |

| C—Rs 500 |

Service departments provide services in the following manner to various departments:

You are required to show the distribution.

[B.Com., Bangalore]

[Ans: A—Rs 992; B—Rs 887; C—Rs 655]

Illustration 10

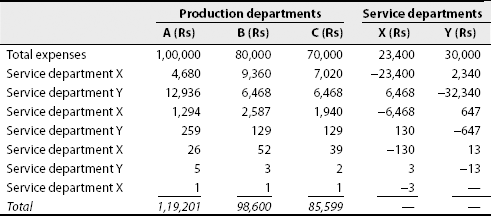

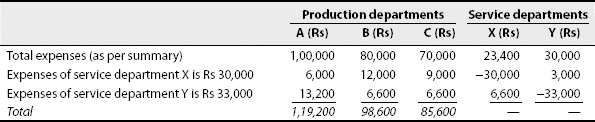

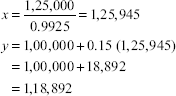

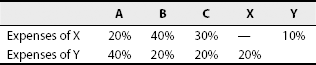

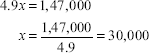

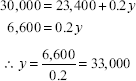

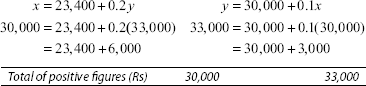

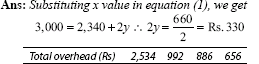

A company has three production departments A, B and C and two service departments X and Y. The expenses incurred by them during a month are as follows

| A—Rs 1,00,000 | X—Rs 23,400 |

| B—Rs 80,000 | Y—Rs 30,000 |

| C—Rs 70,000 |

The expenses of service departments are apportioned to production departments on the following basis:

Show clearly as to how the expenses of departments X and Y would be apportioned to departments A, B and C.

Solution:

Secondary distribution summary:

Alternatively:

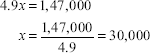

Let x = total overheads of department X and y = total overheads of department Y

Adding equations (3) and (2), we get

By substituting equation (1),

Verification:

Alternatively (trial-and-error method).

| Service departments | ||

|---|---|---|

| X | Y | |

| As per summary (Rs) | 23,400 | 30,000 |

| Transfer to Y (10% of 23,400) | — | 2,340 |

| Transfer to X (20% of 32,430) | 6,468 | — |

| Transfer to Y (10% of 6,468) | — | 647 |

| Transfer to X (20% of 647) | 129 | — |

| Transfer to Y (10% of 129) | — | 13 |

| Transfer to X (20% of 13) | 3 | — |

| Transfer to Y (10% of 3) | — | — |

| Total of positive figures (Rs) | 30,000 | 33,000 |

Problem 10. In a factory, there are two service departments P and Q and three production departments A, B and C. In April 1991, the departmental expenses were as follows:

Expenses of the service department are allocated on a percentage basis as follows:

Prepare secondary distribution summary under the simultaneous equations method.

[Andhra, B.Com., April 1992]

[Ans: total overhead of production departments: A—Rs 7,35,340; B—Rs 6,86,045; C—Rs 5,48,615]

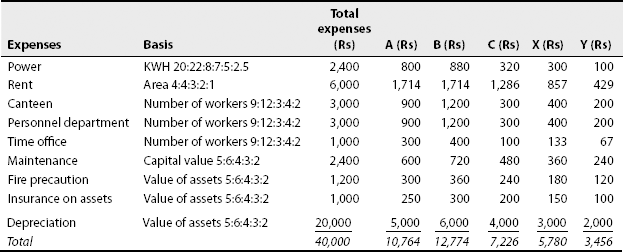

Illustration 11

A company has three production departments A, B and C and two service departments X and Y. The following information is available regarding various expenses:

| Rs | |

|---|---|

| Power | 2,400 |

| Rent | 6,000 |

| Canteen | 3,000 |

| Personnel department | 3,000 |

| Time office | 1,000 |

| Maintenance of buildings | 2,400 |

| Fire precaution service | 1,200 |

| Insurance on assets | 1,000 |

| Depreciation (10% of capital value) |

We also have the following data:

The services of departments X and Y are used by other departments in the following proportion:

Calculate the total overheads of production departments after reapportioning the service department overheads.

Solution: Departmental overhead distribution summary:

Repeated distribution method:

Problem 11. In a factory, there are two service departments P and Q and three production departments A, B and C. During April 1985, the departmental expenses were as follows

| Rs | |

|---|---|

| Department A | 65,000 |

| Department B | 60,000 |

| Department C | 50,000 |

| Department P | 12,000 |

| Department Q | 10,000 |

The expenses of service departments are allocated as follows:

Distribute the expenses of service departments over the production departments under the repeated distribution method.

[Madras, B.Com., March 1988]

[Ans: Expenses of service departments are distributed to A—Rs 8,534; B—Rs 8,604; C—Rs 4,862. Total overhead: A—Rs 73,534; B—Rs 68,604; C—Rs 54,862]

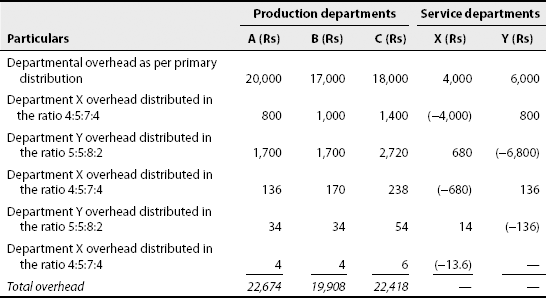

Illustration 12

A manufacturing concern has three production departments and two service departments. In July 1990, the departmental expenses were as follows

| Rs | |

|---|---|

| Production departments | |

| A | 20,000 |

| B | 17,000 |

| C | 18,000 |

| Service departments | |

| X | 4,000 |

| Y | 6,000 |

Expenses of service departments are charged on a percentage basis, viz,

Prepare a statement of secondary distribution under the repeated distribution method.

Solution: Secondary overhead distribution summary:

Problem 12. A factory has two production departments and two service departments. The overhead departmental distribution summary is as follows:

The expenses of service departments are to be charged on a percentage basis as follows:

Show how the expenses of the service departments are to be charged to the two production departments?

[B. Com., Madurai]

[Ans: A—Rs 7,425; B—Rs 5,245]

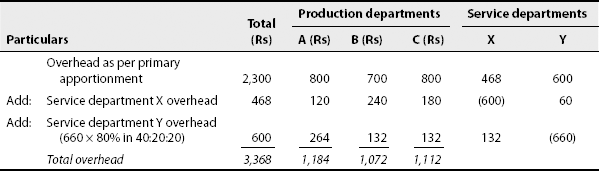

Illustration 12a

A company has three production departments and two service departments; their respective expenditures are as follows:

| Production departments | Service departments |

| A—Rs 800 | X—Rs 468 |

| B—Rs 700 | |

| C—Rs 800 | Y—Rs 600 |

Service departments provide service in the following manner to various departments:

You are required to show the distribution of service department overheads under the simultaneous equation method.

Solution:

Let x be the total overhead of department X and y be the total overhead of department Y.

Then,

Substituting y value in (1)

x = 600 substituting in (2)

Secondary overhead distribution summary:

Illustration 13

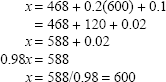

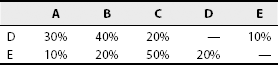

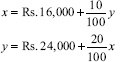

A company is having three production departments, X, Y and Z, and two service departments, boiler house and pump room. The boiler house depends on the pump room for supply of water, and pump room in its turn depends on the boiler house for supply of steam power for driving the pump. The expenses incurred by the production departments are the following: X—Rs 6,00,000; Y—Rs 5,25,000; Z—Rs 3,75,000. The expenses for boiler house are Rs 87,750 and pump room are Rs 1,12,500.

The expenses for the boiler house and the pump room are apportioned to the production departments on the following basis:

Show clearly how the expenses of boiler house and pump room would be apportioned to X, Y and Z departments by following the simultaneous equations method.

Solution:

(i) Let

x = Total overhead of boiler house

y = Total overhead of pump room

Therefore,

x = Rs 87,750 + 20% of y

y = Rs 1,12,500 + 10% of x

Rearranging and multiplying to eliminate percentage, we get

Multiply equation (1) by −1 and equation (2) by 10:

Deducting equation (4) from equation (3), we get

Substituting this value in equation

Problem 13. From the following information, work out the production hour rate of recovery of overheads in departments A, B and C:

The expenses of service departments D and E are to be apportioned as follows:

[Ans: A—Rs 1,663; B—Rs 2,606; C—Rs 1,731. Overhead rates: A—Rs 1.66; B—Rs 1.04; C—Rs 0.96]

Illustration 14

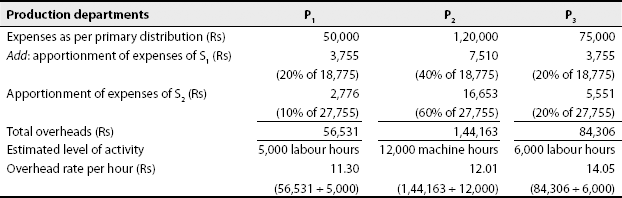

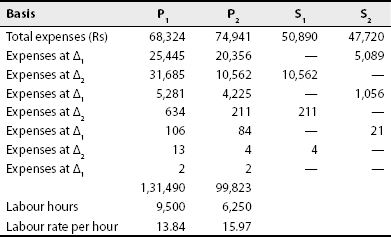

A factory has three production departments (P1, P2 and P3) and two service departments (S1 and S2). Budgeted overheads for the following year have been allocated/apportioned by the cost department to the five departments. The secondary distribution of service department overheads is pending and the following details are given

| Department | Overheads apportioned/allocated | Estimated level of activity |

|---|---|---|

| P1 | Rs 50,000 | 5,000 labour hours |

| P2 | Rs 1,20,000 | 12,000 machine hours |

| P3 | Rs 75,000 | 6,000 labour hours |

| Apportionment of service department costs | ||

| S1 | Rs 16,000 | P1 (20%), P2 (40%), P3 (20%), S2 (20%) |

| S2 | Rs 24,000 | P1 (10%), P2 (60%), P3 (20%), S1 (10%) |

Solution:

Let x be the total overheads of S1 and y be the total overheads of S2. Then we get two simultaneous equations as follows:

On solving these equations, we get x = Rs 18,775 and y = Rs 27,755. The apportioning of expenses of service departments to production departments will be as follows: Statement showing apportionment of expenses of service departments to production departments and calculation of the overhead rate of each production department:

7.12 ADVANCED-TYPE SOLVED PROBLEMS

- A department store has several departments. What bases would you recommend for apportioning the following items of expense to its departments?

- Fire insurance buildings

- Rent

- Delivery expenses

- Purchase department's expenses

- Credit department's expenses

- General administration expenses

- Advertisement

- Sales assistants’ salaries

- Personnel department's expenses

- Sales commission

Solution:

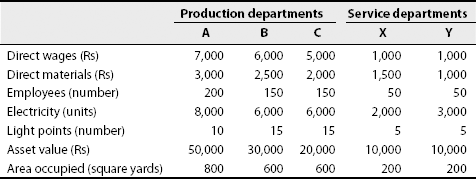

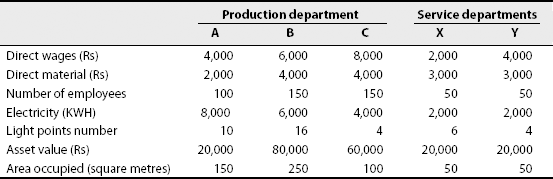

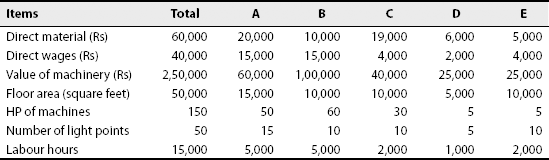

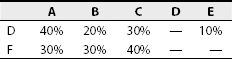

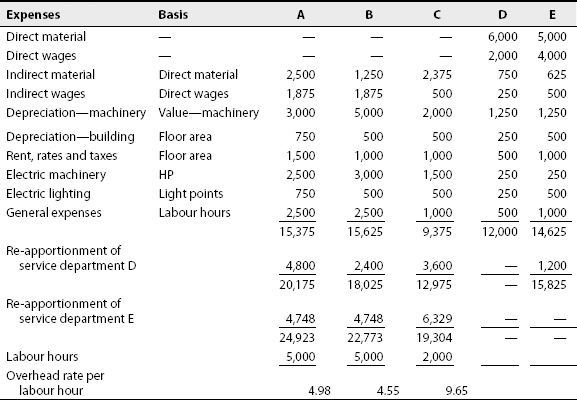

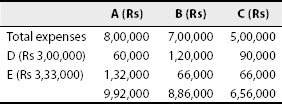

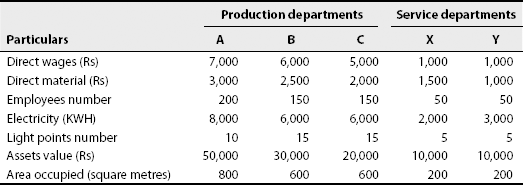

Items of expenses Bases 1. Fire insurance of building Value, floor area 2. Rent Floor area 3. Delivery expenses Volume or weight or both 4. Purchase department's expenses Number of purchase orders, value of the purchases 5. Credit department's expenses Credit sales value 6. General administration expenses Works cost 7. Advertisement Sales value 8. Sales assistants’ salaries Sales value, actual time devoted 9. Personnel department's expenses Number of employees 10. Sales commission Actual sales value - Win Ltd. has three production departments (A, B and C) and two service departments (D and E). From the following figures extracted from the records of the company, calculate the overhead rate per labour hour:

Indirect material 7,500 Indirect wages 5,000 Depreciation on machinery 12,500 Depreciation on building 2,500 Rent, rates and taxes 5,000 Electric power for machinery 7,500 Electric power for lighting 2,500 General expenses 7,500

The expenses of service departments D and E are to be apportioned as follows:

Solution:

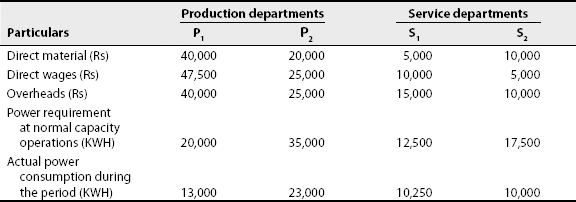

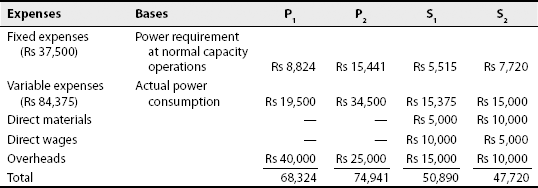

- A company has two production departments and two service departments. The following data relates to a particular period:

The power requirements of these departments are met by a power generation plant. The said plant incurred an expenditure, which is not included in the aforementioned information, of Rs 1,21,875 out of which a sum of Rs 84,375 was variable and the rest fixed. After apportionment of power generation plant costs to the four departments, the service department overheads must be redistributed on the following bases:

You are required to perform the following:

- Apportion the power generation plant costs to the four departments.

- Re-apportion the costs of service departments to production departments.

- Calculate the overhead rate per rate of direct labour hour of production departments, given that the direct wages rates of P1 and P2 are Rs 5 and Rs 4 per hour, respectively.

Solution:

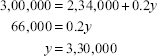

- A factory is having three production departments A, B and C and two service departments D and E. Department D has to depend upon E for the supply of water and E in its turn is dependent on D for the supply of power. The expenses incurred by the production departments during a period are A—Rs 8,00,000; B—Rs 7,00,000; and C—Rs 5,00,000. The expenses for D are Rs 2,34,000 and E are Rs 3,00,000. The expenses of departments D and E are apportioned to the production departments on the following basis:

Show clearly how the expenses of D and E would be apportioned to departments A, B and C using algebraic equations.

Solution:

Let x be the total expenses of department D. Let y be the total expenses of department E. Then,

If x = 3,00,000, then

Distribution of overheads:

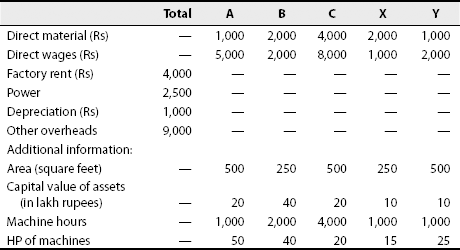

- Blue Ltd. is a manufacturing company having three production departments A, B and C and two service departments X and Y. The following was the budget for December 2001:

Factory rent Rs 2,000 Power Rs 1,250 Depreciation Rs 500 Other overheads Rs 4,500 Additional information:

A technical assessment of the apportionment of expenses of service departments is as follows:

You are required to provide:

- A statement showing the distribution of overheads to various departments.

- A statement showing the re-distribution of expenses of service departments to production departments.

- Machine hour rates of the production departments A, B and C.

Solution: Apportionment of expenses:

Redistribution of expenses:

Machine hour rates:

CHAPTER SUMMARY

After reading this chapter, you should be able to understand the various types of overheads, and the allocation, apportionment, absorption and methods of distribution of overheads. It should also be clear that overheads comprise all the expenses connected with the general organization of an enterprise.

KEY FORMULAE

Bases of distribution of overheads are given in Table 7.4.

Table 7.4 Bases of Distribution of Overhead

| Item | Bases |

|---|---|

| Canteen expenses, timekeeping staff welfare, etc. | Number of employees or wages |

| Depreciation | Value of assets or value of investments |

| Electric power | Number of light points or floor space, HP or HP × machine hours |

| Delivery expenses | Weight, volume or tonne mile |

| Audit fees | Sales or total cost |

| Cost of storekeeping | Number of requisitions |

| Rent | Area |

| Supervision | Number of employees |

| Insurance | Value of assets |

- Overhead absorption rate or overhead recovery rate = overhead incurred/basis of absorption.

- Overhead rate (predetermined) = budgeted overhead for the period/budgeted base for the period.

- Overhead rate (blanket rate) = overhead cost for the factory/total quantum of the base selected.

EXERCISE FOR YOUR PRACTICE

Objective-type Questions

I. State whether the following statements are true or false:

- ‘Factory overhead’ and ‘other expenses’ are synonymous terms.

- Departments that assist producing departments indirectly are called service departments.

- Variable overheads vary with time.

- Cost of indirect material is apportioned to various departments.

- Director's remuneration and expenses form a part of administrative overheads.

- Variable overhead cost is a periodic cost.

- Fixed overhead cost is an output cost.

- Fixed overhead cost is a committed cost.

- Depreciation is a semi-variable expense.

- Variable overhead cost is a discretionary cost.

[Ans: 1—false, 2—true, 3—false, 4—false, 5—true, 6—true, 7—true, 8—false, 9—false, 10—true]

II. Choose the correct answer:

- Which of the following is a service department?

- Finishing department

- Refining department

- Receiving department

- Machine department

Ans: (c)

- Packing cost is a

- Manufacturing overhead

- Selling overhead

- Distribution overhead

- Any of the above

Ans: (d)

- Factory overheads should be absorbed on the basis of

- Machine hours

- Direct labour hours

- Direct labour cost

- Relationship to cost incurred

Ans: (d)

- Administration overheads are recorded as a percentage of

- Works cost

- Prime cost

- Direct materials

- Direct wages

Ans: (a)

- A cost seeking to create and stimulate demand and secure orders is

- Distribution cost

- Selling cost

- Administrative cost

- Research cost

Ans: (b)

- Warehouse expenses is an example of

- Factory overhead

- Administrative overhead

- Selling overhead

- Distribution overhead

Ans: (d)

- Which of the following is not a selling overhead?

- Royalty on sales

- Distribution of samples

- Legal cost for debt realization

- Insurance to cover sold goods while in transit

Ans: (d)

- Salary to a foreman should be classified as a

- Variable overhead

- Fixed overhead

- Semi-variable or semi-fixed overhead

- None of the above

Ans: (c)

- Information regarding depreciation is obtained from

- Plant register

- Invoice

- Cash book

- Store requisition

Ans: (a)

- Over which of the following costs is the management likely to have least control?

- Advertising cost

- Building insurance cost

- Machine breakdown cost

- Wage cost

Ans: (b)

DISCUSSION QUESTIONS

Short Answer-Type Questions

- What is the meaning of the term overhead?

- Explain fixed, variable and semi-variable overheads.

- Explain various classifications of overheads.

- What do you understand by allocation and apportionment in relation to overhead?

- What are the methods of secondary distribution of overheads?

Essay-Type Questions

- Explain the differences between primary and secondary distribution of overheads.

- Explain the terms appropriation and apportionment of overheads.

PROBLEMS

- The factory of a large manufacturing company has several departments. Indicate the bases you would adopt for apportionment of the following overhead expenses to various departments:

(1) Indirect material (2) Indirect wages (3) Depreciation (4) Electricity for power purpose (5) Lighting and heating (6) Creche expenses (7) Material-handling charges (8) Recreation expenses (9) Welfare department's expenses (10) Stores service (11) Fire insurance of stock (12) Timekeeping expenses [Ans: (1) direct material, (2) direct wages, (3) asset value, (4) KWH or HP of machines, (5) light points, units consumed or floor area, (6) number of female workers, (7) material consumed, (8) number of employees, (9) number of employees, (10) material consumed, (11) stock value, (12) number of workers]

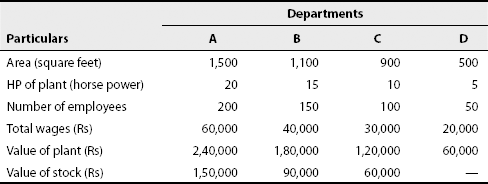

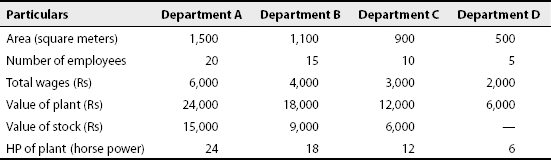

- A producing concern Krishna is divided into four departments. A, B and C are production departments and D is a service department. The actual expenses for a period are as follows:

Rs Rs Rent 10,000 Repairs to plant 6,000 Depreciation to plant 4,500 Lighting expenses 1,200 Supervisory expenses 15,000 Fire insurance (on stock) 5,000 Power 9,000 The following information is available for the four departments:

Apportion the costs to various departments on the most equitable method.

[Madras, 1999]

[Ans: departmental overhead: A—Rs 20,500; B—Rs 14,930; C—Rs 10,420; D—Rs 24,850]

Hint: For service department D, wages are also included in overheads because service departments do not produce anything, and their wages and materials are also treated as overheads.

- Modern Co. is divided into four departments. A, B and C are producing departments, and D is a service department. The actual costs for a period are as follows:

Rs Rent 1,000 Repairs to plant 600 Depreciation on plant 450 Employer's liability for insurance 150 Supervision 1,000 Fire insurance in respect of stock 500 Power 900 Light 120 The following information is available for the four departments:

Apportion the costs to various departments on the most equitable basis.

[Madra.s, 1995]

[Ans: departmental overheads: A—Rs 1,910; B—Rs 1,388; C—Rs 972; D—2,450 (including wages)]

Hint: For a service department, wages and materials are also part of overhead.

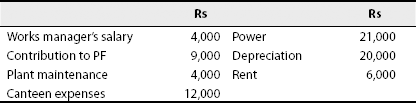

- Apportion the overheads among the departments A, B, C and D.

Rs Rs Works manager's salary 4,000 Contribution to PF 9,000 Plant maintenance 4,000 Canteen expenses 12,000 Power 21,000 Depreciation 20,000 Rent 6,000 Additional information:

[Ans: departmental overheads: A—Rs 32,800; B—Rs 30,400; C—Rs 9,700; D—Rs 3,100]

Hint: Works manager's salary is based on the number of employees.

- The following data were obtained from the books of a company for the half year ending on 30 June 1995:

The expenses for six months were: stores overhead—Rs 400; motive power—Rs 1,500; electric light—Rs 200; labour welfare—Rs 3,000; depreciation—Rs 6,000; repairs and maintenance—Rs 1,200; general overhead—Rs 10,000; rent and taxes—Rs 600. Prepare a primary distribution table for the departments.

[Madras, 1998]

[Ans: total overhead of departments: A—Rs 18,340; B—Rs 14,720; C—Rs 12,100; X—Rs 4,100; Y—Rs 3,640]

Hint: Include direct wages and direct materials also in the case of service departments.

5a. Calculate the overheads allocated to production departments A and B. There are also two service departments X and Y. X renders service worth Rs 12,000 to Y and the balance to A and B in the ratio 3:2. Y renders service to A and B in the ratio 9:1:

Expenses and charges are as follows:

Rs Rs Depreciation 1,90,000 Rent, rates and taxes 36,000 Insurance 15,200 Power 20,000 Canteen expenses 10,800 Electricity 4,800 [Madras, 1988]

[Ans: overhead after primary distribution: A—Rs 1,35,800; B—Rs 76,200; X—Rs 44,200; Y—Rs 20,600. Total overhead after secondary distribution: department A—Rs 1,84,460; B—Rs 92,340]

- Modern company has three production departments A, B and C and two service departments D and E. The following is an abstract from the records of the company for the month of March 1993:

Rs Rs Rent and rates 20,000 Indirect wages 6,000 Depreciation on machinery 40,000 Power 6,000 General lighting 2,400 Sundries 40,000 The following further details are available:

Apportion the expenses to the departments on a suitable basis.

[Madras, 1998]

[Ans: overheads of departments: A—Rs 30,200; B—Rs 28,800; C—Rs 38,600; D—Rs 15,500; E—Rs 5,300]

Hint: Include direct wages also in the case of service departments.

6a. Tamil Nadu Co. Ltd. is a manufacturing company having three production departments, A, B and C, and two service departments X and Y. The following is the budget for December 1985:

A technical assessment for the apportionment of expenses of service departments is as follows:

You are required to prepare the following:

(a) Statement showing distribution of overheads to various departments. (b) Statement showing distribution of service departments’ expenses to production departments. [Madras, 1987]

[Ans: (a) A—Rs 2,700; B—Rs 3,700; C—Rs 6,000; X—Rs 4,750; Y—Rs 5,350; (b) A—Rs 8,481; B—Rs 6,506; C—Rs 7,513]

Hint: Divide power cost in the combined ratio of machine hours and HP.

10:16:16:3:5.

- Janak Ltd. has two production departments M and N and two service departments R and S. After primary distribution, the following were the departmental overheads for the month of March 1998:

Rs Production departments: M 50,000 N 40,000 Service departments: R 12,000 S 16,000 A detailed survey revealed that the services of department R are utilized by the production departments in the ratio 7:3. The services of S were used by M and N equally. Ascertain the total overhead of departments M and N by preparing a secondary distribution summary.

[Ans: total overhead: M—Rs 66,400; N—Rs 51,600]

- Using the repeated distribution method, solve the following problem:

(a) Service department A—expenses are to be allocated in the ratio 30:30:20:20 to production departments X, Y and Z and the service department B. (b) Service department B—expenses are to be allocated in the ratio 50:20:20:10 to production departments X, Y and Z and the service department A. (c) Expenses incurred: Production departments X Rs 50,000 Y Rs 20,000 Z Rs 25,000 Service departments A Rs 5,000 B Rs 8,000 [B. Com., Calicut]

[Ans: X—Rs 56,367; Y—Rs 23,612; Z—Rs 28,021]

- PH Ltd. is a manufacturing company having three production departments A, B and C and two service departments E and Y. The following is the budget for December 1994:

Additional information:

A technical assessment of the apportionment of expenses of service departments is as follows:

You are required to prepare

- (i) A statement showing the distribution of overheads to various departments.

- (ii) A statement showing the redistribution of expenses of service departments to production departments.

[B. Com. Madurai]

[Ans: A—Rs 9,726; B—Rs 5,412; C—Rs 7,364. Machine hour rate: A—Rs 9.73, B—Rs 2.71, C—Rs 1.84]

- Modern Machines Ltd. has three production departments (A, B and C) and two service departments (D and E). From the following figures extracted from the records of the company, calculate the overhead rate per labour hour:

Rs Indirect materials 15,000 Indirect wages 10,000 Depreciation on machinery 25,000 Depreciation on buildings 5,000 Rent, rates and taxes 10,000 Electric power for machinery 15,000 Electric power for lighting 500 General expenses 15,000 95,500

The expenses of service departments D and E are to be apportioned as follows:

(I.C.W.A.)

[Ans: A—Rs 41,892; B—Rs 39,731; C—Rs 30,877. Overhead rate per labour hour: A—Rs 8.38; B—Rs 7.95; C—Rs 15.44]

- PH Ltd. is a manufacturing company having the production departments A, B and C and two service departments X and Y. The following is the budget for December:

A technical assessment for the apportionment of expenses of service departments is as follows:

You are required to prepare the following:

(a) A statement showing distribution of overheads to various departments. (b) A statement showing redistribution of service departments’ expenses to production departments. (c) Machine hour rates of the production departments A, B and C. [Ans: (a) A—Rs 4,100; B—Rs 2,700; C—Rs 6,200; X—Rs 4,200; Y—Rs 5,300; (b) A—Rs 9,569; B—Rs 5,385; C—Rs 7,546; (c) A—Rs 9.57; B—Rs 2.69; c—Rs 1.89]

- Bulls & Bears Ltd. has three production departments A, B and C in its factory. They are served by two service departments D and E. D is the purchasing department and E is the timekeeping department.

The following are the departmental overheads after primary distribution is completed: A—Rs 22,650; B—Rs 21,600; C—Rs 28,950; D—Rs 13,875 and E—Rs 4,725. The following additional details are available:

Prepare a secondary overhead distribution summary, showing the total overhead of the production departments.

[Ans: total overhead for A—Rs 30,562.5; total overhead for B—Rs 26,985; total overhead for C—Rs 34,252.5]

- The following details are available for the month of May 1998 relating to two service departments A and B and two production departments R and S:

Prepare a summary of overhead distribution under the stepladder method.

[Ans: total overhead of production departments: R—Rs 46,000 and S—Rs 51,000]

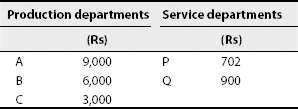

- A company has three production departments and two service departments, and for a period the departmental distribution summary has the following totals:

Rs Production departments: A—Rs 1,600; B—Rs 1,400; C—Rs 1,000 4,000 Service departments: P—Rs 702; Q—Rs 900 1,602 5,602 The expenses of service departments are charged on a percentage basis as follows:

Prepare a statement showing the apportionment of the expenses of the two service departments to production departments by the simultaneous equations method.

[Madras, 1987]

[Ans: service department overheads apportioned to production departments: A—Rs 576, B—Rs 558, C—Rs 468. Total overheads: A—Rs 2,176; B—Rs 1,958; C—Rs 1,468]

- The following particulars relate to a manufacturing company, which has three production departments A, B and C and two service departments X and Y:

The company decided to charge the costs of its service departments on the basis of the following percentages:

Find the total overheads of the production departments using the repeated distribution method.

[Madras, 1984]

[Ans: total overheads of production departments: A—Rs 9,050; B—Rs 9,650; C—Rs 4,300]

- A company has three production departments and two service departments. The distribution summary of overheads is as follows:

The expenses of service departments are charged on a percentage basis as follows:

Apportion the expenses of service departments on the basis of the repeated distribution method.

[Rajasthan 1994]

[Ans: expenses of services departments apportioned to production departments: A—Rs 576, B—Rs 558, C—Rs 468; total overhead: A—Rs 9,576; B—Rs 6,558; C—Rs 3,468]

- A company reapportions the costs incurred by its two service centres D and E to its three production centres A, B and C. The following are the overhead costs, which have been allocated and apportioned to the five cost centres:

Rs Machining 4,00,000 Finishing 2,00,000 Assembling 1,00,000 Material handling 1,00,000 Inspection 50,000 Estimates of the benefits received by each cost centre are as follows:

You are required to calculate the charge for overhead to each of the three production cost centres, including the amounts reapportioned from the two service centres using the continuous allotment or repeated distribution method.

[Madras, 1997]

[Ans: charge for overheads to production departments: A—Rs 4,42,965; B—Rs 2,43,845; C—Rs 1,63,190]

- You are supplied the following information and required to prepare secondary distribution summary under the trial-and-error method. Overhead as per primary distribution:

Rs Production departments A 9,500 B 15,000 C 7,000 Service departments X 12,000 Y 10,000 The service department expenses are allocated as follows:

[Ans: service department overheads after distribution under the trial-and-error method: X—Rs 13,265 and Y—Rs 12,653; net amount to be distributed to A, B and C: X—Rs 13,265 × 80% = Rs 10,612; Y—12,653 × 90% = Rs 11,388; overhead finally charged: A—Rs 18,540.5; B—Rs 21,449; C—Rs 13,510.5]

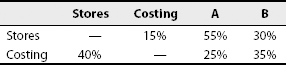

- An analysis of overhead costs is as follows:

Service departments: Stores—Rs 26,400 Costing—Rs 28,200 Production departments: A—Rs 27,000 B—Rs 24,000 Service rendered by the service department is

Prepare the overhead distribution summary under the simultaneous equations method.

[B. Com., Bangalore]

[Ans: A—Rs 57,600; B—Rs 48,000]

- Vasanth Engineering & Co. has three production departments and two service centres. The overhead analysis gives the following overhead costs:

Rs Production centres A 1,380 B 2,190 C 1,290 Service departments D 630 E 510 The overheads of service departments are apportioned as follows:

You are required to prepare secondary distribution summary under the trial-and-error method.

[Ans: service department overheads after distribution under the trial-and-error method: D—Rs 747 and E—Rs 584; net amount to be distributed to A, B and C: D—Rs 672 and E —Rs 468; overhead finally charged: A—Rs 1,662.5; B—Rs 2,606; C—Rs 1,731.5]

- A company has three production departments and two service departments, and for a period the departmental distribution summary has the following totals:

Rs Production departments A 8,000 B 7,000 C 5,000 Service departments X 2,340 Y 3,000 The expenses of service departments are charged on a percentage basis as follows:

Prepare a statement showing the apportionment of expenses of the two service departments to the production departments.

[Kuwempu 1992]

[Ans: total overhead of production departments: A—Rs 9,890; B—Rs 9,025; C—Rs 6,425]

Hint: The simultaneous equations method is used in the absence of specific instruction. Any one of the other methods also can be used.

- A manufacturing company has three production departments and two service departments. The departmental expenses are as follows:

The service department expenses are charged on the following percentage basis:

Prepare a statement showing the apportionment of overheads of the two service departments to the production departments.

[Madras, 1985]

[Ans: total overheads of the production departments: A—Rs 11,352; B—Rs 9,763; C—Rs 13,885]

Hint: The repeated distribution method is used in the absence of specific instruction.

- From the following information, work out the production hour rate of recovery of overheads in departments A, B and C:

The expenses of service departments D and E are apportioned as follows:

(Madras, 1984)

[Ans: departmental overheads after secondary apportionment: A—Rs 1,663; B—Rs 2,606; C—Rs 1,731; production hour rate: A—Rs 1.663; B—Rs 1.042; C—Rs 0.962]

EXAMINATION PROBLEMS

- Indicate the basis you would adopt for apportionment of the following items of overhead expenses to different departments:

- Factory rent

- Factory lighting

- Power

- Depreciation of plant and machinery

- Insurance of plant and machinery, and fire insurance of stock

- Welfare expenses

- Material-handling charges

- Indirect material

- Indirect wages

- Supervision

- Repairs to plant

- Insurance of building

- Staff recreation

- Canteen expenses

- Creche expenses

- Employer's contribution to ESI

- Employer's contribution to PF

- Stores expenses

- Sundry expenses

Ans: Bases for the apportionment of overhead expenses:

Floor area Light points, floor area KWH; HP of plant Machine hours; value of plant Insurable value of plant and machinery Value of stock Number of employees Value of material Direct material Direct wages Number of employees Value of plant Value of building, floor area Number of employees Number of employees Number of female employees Wages of each department, number of employees Wages of each department, number of employees Materials consumed by each department Labour hours; direct wages - Kumaresh Ltd. has three production departments A, B and C and two service departments D and E. The following figures are extracted from the records of the company:

Rs Rent and rates 5,000 Indirect wages 1,500 Depreciation of machinery 10,000 General lighting 600 Power 1,500 Sundries 10,000 The following further details are available:

Apportion the cost to various departments on the most equitable basis by preparing a primary departmental distribution summary.

Note: Direct wages of service departments are also included in the distribution summary since they should also be reapportioned to the production departments and then finally be absorbed by the output. Ignoring the direct wages of service departments will result in unabsorbed expenses.

- Calculate the overheads allocated to production departments A and B from the following: There are two service departments X and Y. X renders service to A and B in the ratio 3:2 and Y renders service to A and B in the ratio 9:1. Overhead as per primary overhead distribution is A—Rs 49,800; B—Rs 29,600; X—Rs 15,600; Y—Rs 10,800.

- Calicut Soaps Ltd. supplies you the following information for the month ending on January 1988. You are required to apportion the overheads to the production departments:

The expenses (in rupees) for the month were as follows:

Stores overheads (Rs) 400 Motive power (Rs) 1,500 Lighting (Rs) 200 Labour welfare (Rs) 3,000 Depreciation (Rs) 6,000 Repairs and maintenance (Rs) 1,200 General overheads (Rs) 1,000 Rent and rates (Rs) 600 Apportion the expenses of X in the ratio 4:3:3 and those of department Y in the proportion of direct wages to departments A, B and C, respectively.

- A company has four departments. The actual costs for the period are given as follows. Apportion the costs to the various departments by the most equitable method.

Rs Rent 2,000 Repairs 1,200 Depreciation 900 Light 200 Supervision 3,000 Employer's liability insurance 300 Insurance 1,000 Power 1,800 The following data are also available for the four departments:

Note: Insurance has been apportioned on the basis of the value of stock, under the assumption that it is only with regard to stock. Lighting has been distributed on the basis of area as no other relevant data are available as to the number of light points.

- Calculate the overheads that can be allocated to the production departments A and B. There are also two service departments X and Y. X renders service worth Rs 12,000 to Y and the balance to A and B in the ratio 3:2. Y renders service to A and B in the ratio 9:1.

The expenses include the following:

Rs Depreciation 1,90,000 Rent, rates, etc. 36,000 Insurance 15,200 Power 20,000 Canteen expenses 10,800 Electricity 4,800

- Amit Company has five departments of which P, N, R and S are producing departments and T is a service department. The actual costs for a period are as follows:

Rs Repairs 2,000 Rent 2,500 Depreciation 1,200 Supervision 4,000 Insurance 1,500 Employer's liability of employees’ insurance 600 Light 1,800 The following data are also available for the five departments:

Apportion the costs to the various departments on an equitable basis.

- A manufacturing company has two production departments, X and Y, and three service departments, timekeeping, stores and maintenance. The departmental distribution summary showed the following expenses for January 1986:

Production departments X Rs 36,000 Y Rs 24,000 Service departments Stores Rs 7,500 Timekeeping Rs 6,000 Maintenance Rs 4,500 Other information relating to these departments are as follows:

Apportion the cost of the service departments to Production departments X and Y.

Ans: x 46262 y 31738 78,000 Bases of apportionment:

Timekeeping 10:5:20:15 (number of employees) Stores 6:24:20 (number of requisition) Maintenance 18:12 (machine hours) - A factory has three service departments L, M and N and two production departments X and Y. The following are the expenses allocated and apportioned to the departments as per the primary distribution summary:

The following additional information is also available on the basis of a detailed analysis:

Prepare a statement showing the apportionment of service department overheads under the step method.

Note: While doing a sum under the step method, the service departments that service the largest number of other departments should be written first. For example, in the aforementioned case, department L serves four other departments. Similarly, the remaining service departments should be written in the order of number of other departments served. Finally, the production departments are written one by one.

Hint: Apportion time-booking expenses to other departments in the ratio of number of employees.

- In a factory, there are two service departments P and Q and three production departments A, B and C. In April, the departmental expenses were as follows:

A—Rs 6,50,000 P—Rs 1,20,000 B—Rs 6,00,000 Q—Rs 1,00,000 C—Rs 5,00,000 The service department expenses are allotted on a percentage basis as follows:

Prepare a statement showing the distribution of expenses of the two service departments to the three production departments under the repeated distribution method and the simultaneous equations method.

Simultaneous equations method:

or

- A company has three production departments A, B and C and two service departments X and Y. The expenses incurred by the departments during a month are as follows:

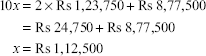

A—Rs 80,000 X—Rs 23,400 B—Rs 70,000 Y—Rs 30,000 C—Rs 50,000 The expenses of service departments are apportioned to the production departments on the following basis:

Show clearly how the expenses of departments X and Y would apportioned to departments A, B and C.

Alternatively,

Let x = total overheads of department X

Let y = total overheads of department Y

Multiplying equation (1) by 5, we get

Adding equations (3) and (2), we get

By substituting equation (1), we get

Verification:

- A company has three production departments A, B and C and two service departments X and Y. The following information is available regarding various expenses:

Rs Rs Power 2,400 Rent 4,200 Canteen 3,000 Personnel department 3,000 Time office 1,000 Maintenance of buildings 2,400 Fire precaution service 1,200 Insurance on assets 1,000 Depreciation (10% of capital value) We also have the following data:

The services of departments X and Y are used by the other departments in the following proportion:

Calculate the total overheads of production departments after reapportioning the service department overheads.

- A manufacturing concern has three production departments and two service departments. In July 1990, the departmental expenses were as follows:

Rs Production departments A 16,000 B 13,000 C 14,000 Service departments X 4,000 Y 6,000 The expenses of service departments are charged on a percentage basis, viz,

Prepare a statement of secondary distribution under repeated distribution method.

- A company has three production departments and two service departments; their respective expenditures are as follows:

Production departments Service departments A—Rs 800 X—Rs 234 B—Rs 700 C—Rs 500 Y—Rs 300 Service departments provide service in the following manner to various departments:

Show the distribution of service department overheads under the simultaneous equation method.

- A company is having three production departments, X, Y and Z, and two service departments, boiler house and pump room. The boiler house depends upon the pump room for supply of water and pump room in its turn is dependent on the boiler house for supply of steam power for driving the pump. The expenses incurred by the production departments are X—Rs 6,00,000; Y—Rs 5,25,000; and Z—Rs 3,75,000. The expenses for the boiler house are Rs 1,75,500 and the pump room are Rs 2,25,000. Expenses of the boiler house and the pump room are apportioned to the production departments on the following basis:

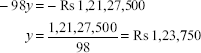

Show clearly how the expenses of boiler house and pump room would be apportioned to X, Y and Z departments by following the simultaneous equations method.

Ans:

10x = 2 × Rs 2,47,500 + Rs 17,55,000

= Rs 4,95,000 + Rs 17,55,000 = Rs 22,50,000

x = Rs 2,25,000

- A factory has three departments (P1, P2 and P3) and two service departments (S1 and S2). Budgeted overheads for the following year have been allocated/apportioned by the cost department among the five departments. The secondary distribution of service department overheads is pending and the following details are given:

Department Overheads apportioned/allocated Estimated levels of activity P1 Rs 48,000 5,000 labour hours P2 Rs 1,12,000 12,000 machine hours P3 Rs 52,000 6,000 labour hours Apportionment of service department costs S1 Rs 16,000 P1 (20%), P2 (40%), P3 (20%), S2 (20%) S2 Rs 24,000 P1 (10%), P2 (60%), P3 (20%), S1 (10%) Ans: Let x be the total overhead of S1 and y be the total overhead of S2.

Then we get two simultaneous equations as follows:

Solving these equations, we get x = Rs 18,775 and y = Rs 27,755

P1 P2 P3 (54,531 ÷ 5,000) (1,36,163 ÷ 12,000) (61,306 ÷ 6,000)