9

Reconciliation of Cost and Financial Accounts

CHAPTER OUTLINE

LEARNING OBJECTIVES

After reading this chapter, you will be able to understand:

- The reasons for the difference in the profit or loss as per financial and cost accounts;

- The need for reliability of cost accounts;

- To coordinate the activities of financial and cost accounts;

- The method of reconciling the cost and financial profits;

- The circumstances that lead to the difference between cost and financial profits;

- Solving the sums when any of the profits (cost/profit) is given;

- Solving the sums when both the profits are given; and

- Solving the sums when both the profits are not given.

9.1 INTRODUCTION

The accounting procedure adopted in financial accounts differs from those adopted in cost accounts (for example, actual amounts are considered in financial accounts, where as in cost accounts, estimated amounts are considered, stock is valued at market value or book value whichever is less in financial but in cost accounts stock is always valued at book value, etc.). Due to the difference in the procedures the profit disclosed by these accounts will differ. Therefore, it becomes necessary to reconcile these two accounts and find out the reasons for the difference.

9.2 REASONS FOR DISAGREEMENT IN PROFIT

- Items shown only in financial accounts: There are a number of items included only in financial accounts but not in cost accounts. These may be items of income or items of expenditure. Items of expenditure decrease the profit and items of income increase the profit. For example,

- loss on sale of assets

- loss on investments

- taxes on income

- dividend paid.

- Items shown only in cost accounts: There are certain items, which are included only in cost accounts and not in financial accounts. These items are not shown in financial accounts because the amount is not actually spend or paid.

For example,

- interest on own premises

- interest on own capital

- salary to proprietor.

- Method of stock valuation: In financial accounts, stock is valued on the basis of its cost or market value whichever is less. In cost accounts, stock isvalued at its cost value.

- Method of charging depreciation: In financial accounts, straight-line method or diminishing balance method, whichever accepted by the Income tax authorities is used. In cost accounts, any method whichever suitable can be used.

- Absorption of overheads: In financial accounts, the question of absorption does not arise as the actual expenses are shown. In cost accounts, overheads are absorbed at predetermined rates which leads to either under absorption or over absorption.

Procedure for reconciliation:

There are two methods of reconciliation based on the base taken:

- Profit as per cost account/loss as per financial account is taken as the base.

- Profit as per financial account/loss as per cost account is taken as the base.

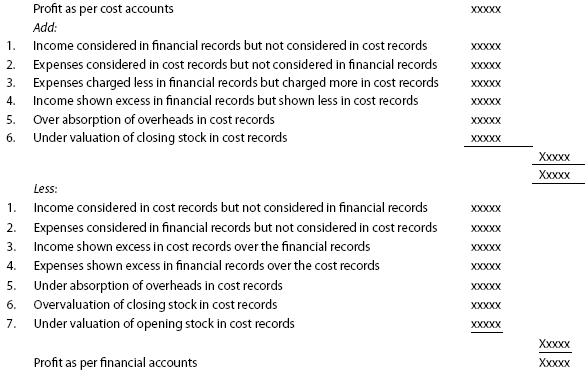

Rules when profit as per cost account is taken as the base

| Profit as per cost accounts | xxxxx | |

| Add: | ||

| Income considered in financial records but not considered in cost records | xxxxx | |

| Expenses considered in cost records but not considered in financial records | xxxxx | |

| Expenses charged less in financial records but charged more in cost records | xxxxx | |

| Income shown excess in financial records but shown less in cost records | xxxxx | |

| Over absorption of overheads in cost records | xxxxx | |

| Under valuation of closing stock in cost records | xxxxx | |

| xxxxx | ||

| xxxxx | ||

| Less: | ||

| Income considered in cost records but not considered in financial records | xxxxx | |

| Expenses considered in financial records but not considered in cost records | xxxxx | |

| Income shown excess in cost records over the financial records | xxxxx | |

| Expenses shown excess in financial records over the cost records | xxxxx | |

| Under absorption of overheads in cost records | xxxxx | |

| Overvaluation of closing stock in cost records | xxxxx | |

| Under valuation of opening stock in cost records | xxxxx | |

| xxxxx | ||

| Profit as per financial accounts | xxxxx |

When cost profit is taken as the base, we must observe the effect of an item on cost profit. If an item increases cost profit then such item should be deducted from the cost profit and if it decreases the cost profit, it should be added to the cost profit. The same principle is applied when financial profit is taken as the base.

Items to be added and deducted are reversed if the profit as per financial account is taken as the base.

Circumstances where reconciliation statement can be avoided:

When the cost and financial accounts are integrated, there is no need to have a separate reconciliation statement between the two sets of accounts. Integration means that the same set of accounts fulfil the requirement of both i.e., cost and financial accounts.

Types of problems

- When both the profits are given: In such cases, the sum can be done by starting with cost profit and ending with financial profit and vice versa.

- When only one of the two profits is given: In such cases, the sum should be solved based on the profit given. If cost profit is given, then the resultant profit will be financial profit and vice versa.

- When both the profits are not given: In such cases, cost sheet is prepared to arrive at cost profit, a combined trading, profit and loss account is prepared to arrive financial profit and then reconciliation statement is prepared as usual.

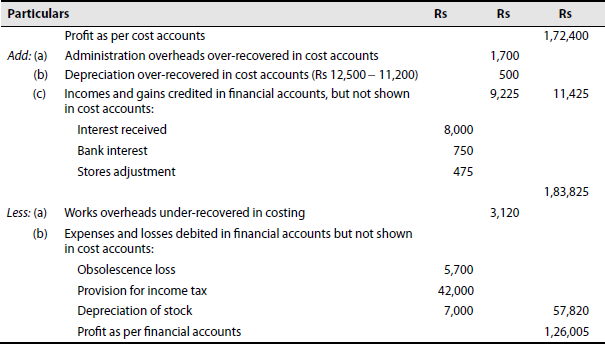

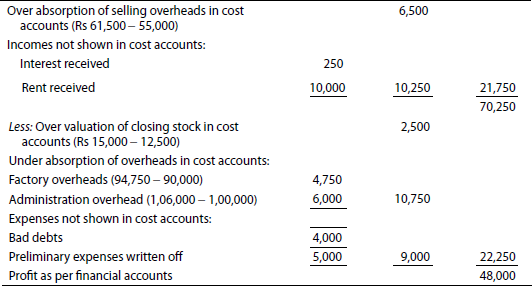

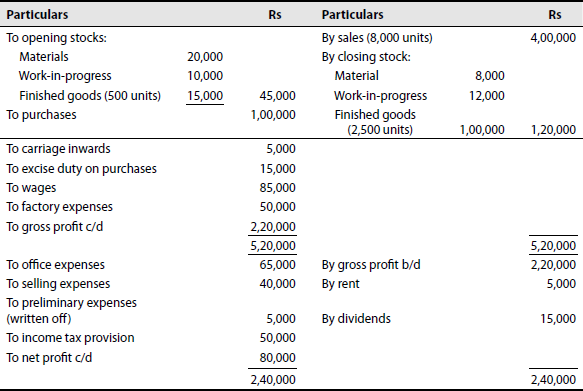

Illustration 1

From the following figures, prepare a reconciliation statement between cost and financial records:

| Rs | |

|---|---|

| Net profit as per financial records | 1,26,005 |

| Net profit as per costing records | 1,72,400 |

| Works overheads under-recovered in costing | 3,120 |

| Administrative overheads recovered in excess | 1,700 |

| Depreciation charged in financial records | 12,000 |

| Depreciation recovered in costing | 12,500 |

| Interest received but not included in costing | 8,000 |

| Obsolescence loss charged in financial records | 5,700 |

| Income tax provided in financial books | 42,000 |

| Bank interest credited in financial books | 750 |

| Stores adjustment (credit in financial books) | 475 |

| Depreciation of stock charged in financial books | 7,000 |

(Madras, 1995)

Solution:

Reconciliation statement

Note: The terms ‘absorption’ and ‘recovery’ are used interchangeably and they mean the same thing.

Problem 1. Ascertain the profit as per the financial books from the following information

| Rs | |

|---|---|

| Profit as per cost accounts | 25,000 |

| Closing stock overvalued in cost books | 12,500 |

| Preliminary expenses written off | 3,000 |

| Profit on sale of building | 30,000 |

| Administrative expenses over-recovered in cost books | 50,375 |

| Works overheads under-recovered in cost books | 30,375 |

| Bank interest and transfer fee in financial books | 5,000 |

| Interest on investment recorded in financial books | 10,000 |

| Depreciation shown in excess in cost books | 4,000 |

| Provision made for income tax | 40,000 |

(Madras, 1998)

[Ans: profit as per financial books = Rs 38,500]

Illustration 2

Reconciliation involving loss

Prepare a reconciliation statement from the following details:

| Rs | |

|---|---|

| Net loss as per cost accounts | 3,44,800 |

| Net loss as per financial accounts | 4,37,340 |

| Depreciation overcharged in costing | 2,600 |

| Interest on investments | 17,500 |

| Administrative overheads over-recovered in costing | 2,600 |

| Goodwill written off | 95,000 |

| Stores adjustment in financial books | 1,000 |

| Depreciation of stock charged in financial books | 15,000 |

(Madras, 1987)

Solution:

Reconciliation statement

Note: Incomes like interest on investments and intangible assets written off like goodwill are not shown in cost accounts in the normal course.

Problem 2. Prepare a reconciliation statement from the following information

| Rs | |

|---|---|

| Net profits as per cost accounts | 2,00,000 |

| Income tax | 60,000 |

| Share transfer fee credited | 4,000 |

| Provision for doubtful debts | 20,000 |

| Overheads as per cost accounts | 34,000 |

| Overheads as per finance books | 28,000 |

| Directors’ fees in financial books only | 10,000 |

| Depreciation charged only in finance books | 7,000 |

| Closing stock in cost accounts | 18,750 |

| Closing stock in finance books | 20,750 |

| Goodwill written off | 10,000 |

| Stores adjustment (credit in finance books) | 1,000 |

| Interest on investments | 4,000 |

(Madras, 1999)

[Ans: profit as per financial accounts = Rs 1,10,000]

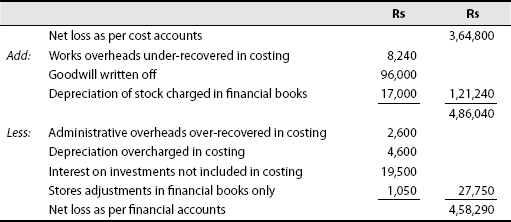

Illustration 3

Prepare a reconciliation statement:

| Net loss as per cost accounts | 3,64,800 |

| Net loss as per financial accounts | 4,58,290 |

| Works overheads under-recovered in costing | 8,240 |

| Depreciation overcharged in costing | 4,600 |

| Interest on investments | 19,500 |

| Administrative overheads over-recovered in costing | 2,600 |

| Goodwill written off | 96,000 |

| Stores adjustment in financial books (credit) | 1,050 |

| Depreciation of stock charged in financial books | 17,000 |

(Madras University, 1988)

Solution:

Reconciliation statement

Problem 3. From the following figures prepare a reconciliation statement:

| Rs | |

|---|---|

| Net loss as per costing records | 1,72,400 |

| Works overhead under-recovered in costing | 3,120 |

| Administrative overheads recovered in excess | 1,700 |

| Depreciation charged in financial records | 11,200 |

| Depreciation recovered in costing | 12,500 |

| Interest received not included in costing | 8,000 |

| Obsolescence loss charged in financial records | 5,700 |

| Income-tax provided in financial books | 45,000 |

| Bank interest credited in financial books | 750 |

| Stores adjustments (credit) in financial books | 475 |

| Value of opening stock in: | |

| Cost accounts | 52,600 |

| Financial accounts | 54,000 |

| Value of closing stock in: | |

| Cost accounts | 52,000 |

| Financial accounts | 49,600 |

| Interest charged in cost accounts but not in financial accounts | 6,000 |

| Preliminary expenses written off in financial accounts | 1,000 |

| Provision for doubtful debts in financial accounts | 300 |

[Ans: net loss as per financial records = Rs 2,13,095]

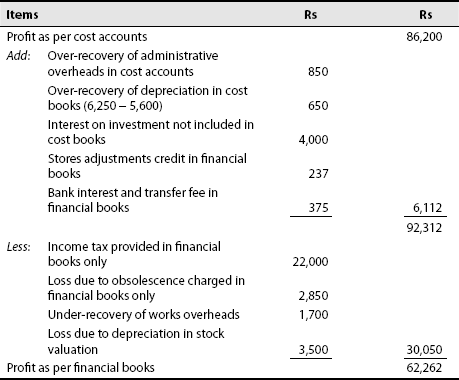

Illustration 4

The net profit of Kamat Manufacturing Company Ltd appeared at Rs 64,337 as per financial records for the year ended 31 December 1986. The cost books, however, showed a net profit of Rs 86,200 for the same period. A scrutiny of the figures from both the sets of accounts revealed the following facts.

| Rs | |

|---|---|

| Works overheads under-recovered in cost | 1,700 |

| Administrative overheads over-recovered in cost | 850 |

| Depreciation charged in financial accounts | 5,600 |

| Depreciation recovered in cost | 6,250 |

| Interest on investment not included in cost | 4,000 |

| Loss due to obsolescence charged in financial accounts | 2,850 |

| Income tax provided in financial accounts | 22,000 |

| Bank interest and transfer fee in financial books | 375 |

| Stores adjustments (credit in financial books) | 237 |

| Loss due to depreciation in values (charged in financial accounts) | 3,500 |

Prepare a statement showing reconciliation between the figures of net profit as per cost accounts and the figures of net profit shown in the financial books.

Solution:

Statement showing reconciliation

Problem 4. The net profit of ‘A’ Co. Ltd appeared at Rs 60,652 as per financial records for the year ended 31 March 1993. The cost books, however, showed a net profit of Rs 86,200 for the same period. A scrutiny of the figures from both the sets of accounts revealed the following facts:

| Rs | |

|---|---|

| Works overheads under-recovered in costing | 1,560 |

| Administrative overheads over-recovered in costing | 850 |

| Depreciation charged in financial accounts | 5,600 |

| Depreciation recovered in costing | 6,250 |

| Interest on investments not included in costing | 4,000 |

| Loss due to obsolescence charged in financial accounts | 2,850 |

| Income tax provided in financial accounts | 20,150 |

| Bank interest and transfer fee in financial books | 375 |

| Stores adjustment (credited in financial books) | 237 |

| Value of opening stock: | |

| Cost accounts | 24,800 |

| Financial accounts | 26,300 |

| Value of closing stock: | |

| Cost accounts | 25,000 |

| Financial accounts | 23,000 |

| Interest charged in cost accounts | 2,000 |

| Goodwill written off | 7,000 |

| Loss on the sale of furniture | 1,000 |

Prepare statements showing reconciliation between the figures of net profit as per cost accounts and the figures of net profit as shown in the financial books.

(Madras, 1991)

[Ans: reconciliation = Rs 60,652 + 1,560 + 2,850 + 20,150 + 2,000 + 7,000 + 1,000 − 850 − 650 + 1,500 − 4,000 − 375 − 237 − 2,000 = Rs 88,600]

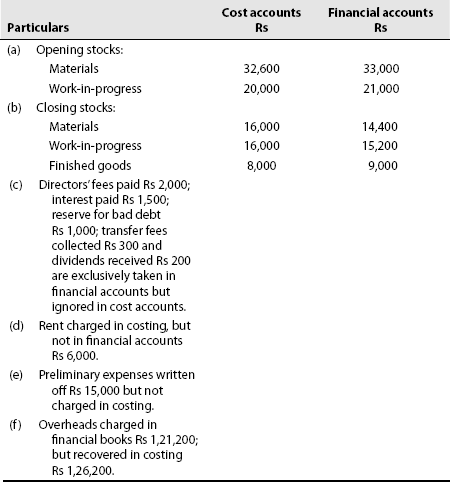

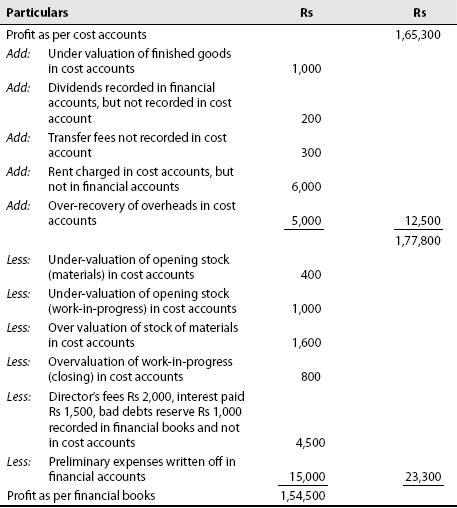

Illustration 5

Profit as per cost accounts is Rs 1,65,300. The following details are ascertained on comparison of the cost and financial accounts:

Find out the profits as per financial accounts and draw up a reconciliation statement.

Solution:

Reconciliation statement

Problem 5. A company maintains separate cost and financial accounts and the costing profit for the year 1991 differed from that revealed in the financial accounts which was shown as Rs 50,000. The following information is available:

You are required to determine the profit figure, which was shown in the cost accounts.

(Delhi, 1992)

[Ans: profit as per cost accounts = Rs 52,200]

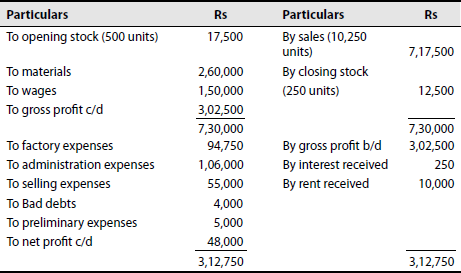

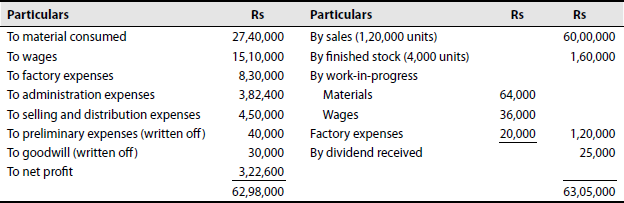

Illustration 6

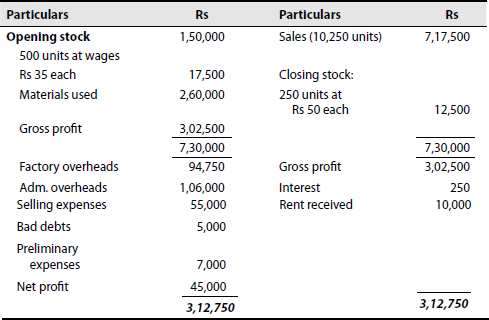

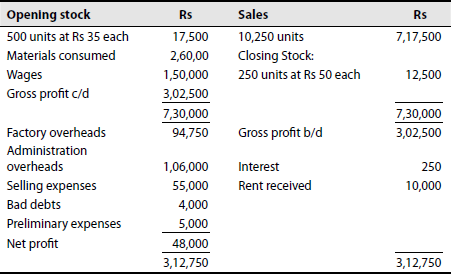

SV Ltd. has furnished you the following information from the financial books for the year ended 30 June:

Profit and loss account (ended 30 June)

The cost sheet shows the cost of materials at Rs 26 per unit and the labour cost as Rs 15 per unit. The factory overheads are absorbed at 60% of labour cost and administration overheads at 20% of factory cost. Selling expenses are charged at Rs 6 per unit. The opening stock of finished goods is valued at Rs 45 per unit.

You are required to prepare:

- A statement showing profit as per cost accounts for the year ended 30 June.

- Statement showing the reconciliation of profit disclosed in cost accounts with the profit shown in the financial accounts.

(Andhra University, March 2002)

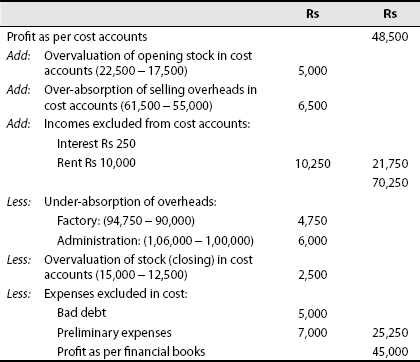

Solution:

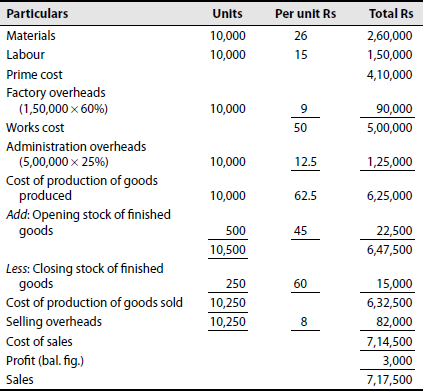

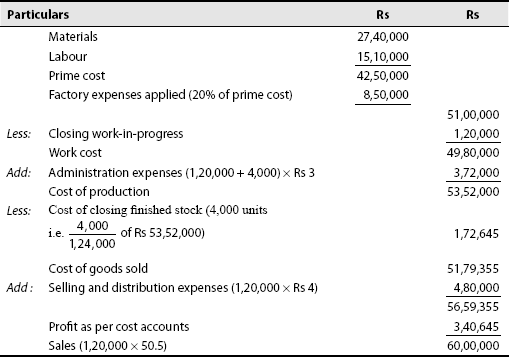

Profit as per cost accounts

| Per unit Rs | Total Rs | |

|---|---|---|

| (Production during the year = 10,250+250−500=10,000) | ||

| Cost of materials | 26 | 2,60,000 |

| Labour cost | 15 | 1,50,000 |

| Prime cost | 41 | 4,10,000 |

| Factory overheads 60% of labour | 9 | 90,000 |

| Factory cost | 50 | 5,00,000 |

| Administrative overheads 20% of factory cost | 10 | 1,00,000 |

| Cost of production of 10,000 units × 60 | 6,00,000 | |

| Add: Opening stock: 500 × 45 | 22,500 | |

| 6,22,500 | ||

| Less: Closing stock: 250 × 60 | 15,000 | |

| Cost of goods sold (10,250 units) | 6,07,500 | |

| Add: Selling expenses at Rs 6 per unit | 61,500 | |

| Total cost of units sold (10,250) | 6,69,000 | |

| Profit | 48,500 | |

| Sales | 7,17,500 | |

| Therefore, the profit = 48,500 |

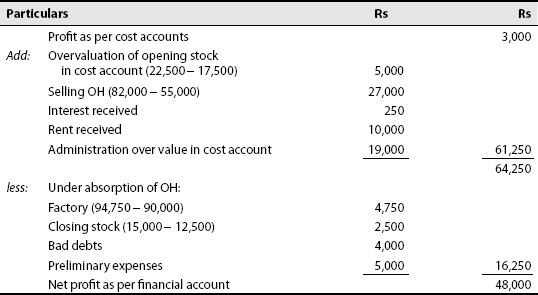

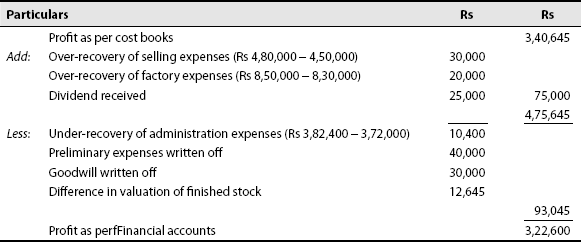

Reconciliation statement

Problem 6. ***M/s. Ashokan Ltd, made a profit of Rs 19,000 during the year 1995 as per their costing system, whereas their final accounts disclose a profit of Rs 15,000. From the following profit and loss account for the year ended 31 December 1995 as per the financial books, you are required to prepare a reconciliation statement showing the causes for this difference.

Profit and loss account

Costing records show the following:

- Stock ledger closing balance Rs 89,000.

- Direct labour Rs 23,000.

- Factory overheads Rs 13,000.

- Administrative overheads and selling expenses are calculated at 8% each of the selling price.

(Madras, 1992)

[Ans: reconciliation = Rs 19,000 + 3,000 + 7,500 + 2,500 − 15,000 − 2,000 = Rs 15,000]

Illustration 7

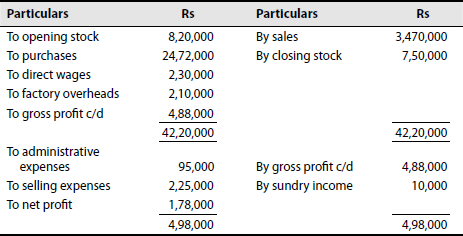

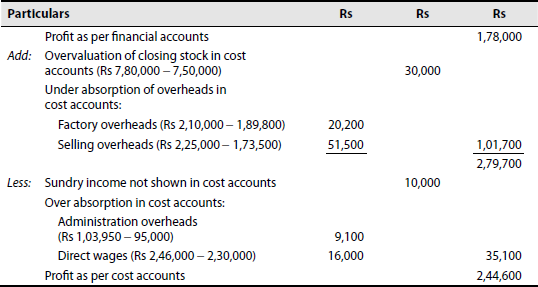

During a particular year the auditors certified the financial accounts showing a profit of Rs 1,78,000 whereas the profit as per costing books was accounted to be Rs 2,44,600. With the following information provided you are required to prepare a reconciliation statement showing clearly the reasons for the gap:

Trading and profit and loss account

The costing records show:

- Book value of closing stock Rs 7,80,000.

- Factory overheads have been absorbed to the extent of Rs 1,89,800.

- Sundry income is not considered.

- Administrative expenses are recovered at 3% of sales.

- Total absorption of direct wages Rs 2,46,000.

- Selling prices include 5% for selling expenses.

(Madras, 1991)

Solution:

Reconciliation statement

Working Note:

Administration overheads in cost acconts = 34,70,000 × 3%

= Rs 1,04,100

Selling expenses in cost accounts = 34,70,000 × 5%

= Rs 1,73,500

Problem 7. Rama & Co.'s profit and loss account for the year 1985 is given below:

In cost accounts, works overheads was 50% of wages, office overheads was Rs 18,000 and selling overheads 5% on sales.

Prepare a reconciliation statement.

[Ans: profit as per cost accounts = Rs 1,67,000]

Illustration 8

S.V. Ltd, has furnished you the following information from the financial books for the year ended 31 March 1996:

Profit and loss account for the year ended 31 March 1996

The cost sheet shows the cost for materials at Rs 26 per unit and the labour cost Rs 15 per unit. Factory overheads are absorbed at 60% of labour cost and administration overheads at 25% of works cost. Selling expenses are charged at Rs 8 per unit. The opening stock of finished goods is valued at Rs 45 per unit.

You are required to prepare:

- A statement showing cost and profit as per cost accounts.

- A statement showing the reconciliation of profit disclosed in cost accounts with the profit shown in financial accounts.

(CA INTER)

Solution:

Statement showing cost and profit

Note:

Production = Sales + closing stock −opening stock

= 10,250 + 250 −500 = 10,000 units

Reconciliation statement

Problem 8. The following is the profit and loss account of ‘X’ Ltd:

The profit as per cost accounts was Rs 57,000.

You are required to prepare a reconciliation statement of the cost and financial profits using the following additional data:

- Factory overheads in cost accounts is absorbed at 100% on wages.

- Closing stock is valued at Rs 10,000 in costing.

- Administration and selling overheads were recovered at 5 and 7% on sales, respectively.

- Depreciation was charged in costing at Rs 3,000.

[Madurai, B.Com.]

[Ans: reconciliation: Rs 65,000 + 3,000 + 2,000 − 4,000 − 1,000 − 1,000 − 2,000 − 5,000 = Rs 57,000]

Illustration 9

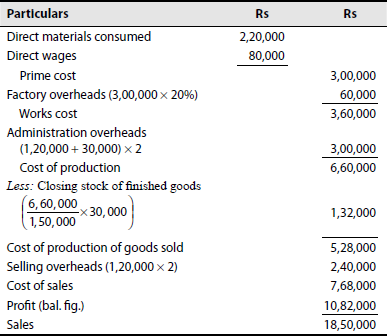

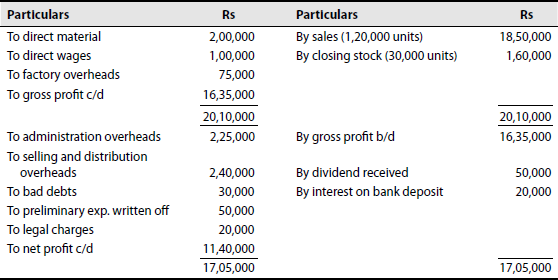

The following figures are available from financial accounts for the year ended 31 March 1997:

| Rs | |

|---|---|

| Direct material consumed | 2,00,000 |

| Direct wages | 1,00,000 |

| Factory overheads | 75,000 |

| Administrative overheads | 2,25,000 |

| Selling and distribution overheads | 2,40,000 |

| Bad debts | 30,000 |

| Preliminary expenses written off | 50,000 |

| Legal charges | 20,000 |

| Dividend received | 50,000 |

| Interest on bank deposit received | 20,000 |

| Sales (1,20,000 units) | 18,50,000 |

| Closing stock (30,000 units) | 1,60,000 |

The cost accounts reveal the following:

Direct material consumed: 2,20,000; Direct wages: Rs 80,000; Factory overheads at 20% on prime cost; Administration overheads at Rs 2 per unit produced and selling overheads at Rs 2 per unit sold.

Prepare: (a) Statement showing cost and profit; (b) Financial profit and loss accounts; and (c) Reconciliation statement.

(Madras, 1993)

Solution:

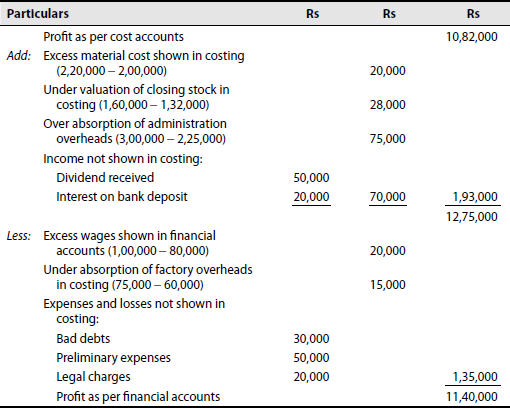

Statement showing cost and profit

Trading and profit and loss account

Reconciliation statement

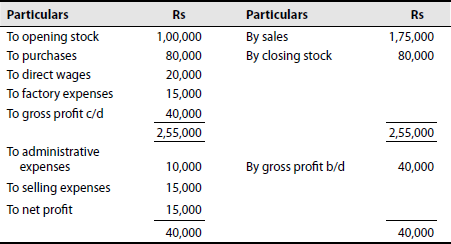

Problem 9. Prepare the following statements from the particulars given below:

- Statement of cost of manufacture,

- Statement of profit as per cost accounts,

- Profit as per financial accounts and

- A reconciliation statement.

| Rs | |

|---|---|

| Raw materials: | |

| Opening stock | 4,000 |

| Purchases | 24,000 |

| Closing stock | 6,000 |

| Finished goods: | |

| Opening stock | 8,000 |

| Closing stock | 2,000 |

| Wages | 20,000 |

| Sales | 79,650 |

| Office expenses | 6,100 |

| Works expenses | 7,750 |

Selling price = Cost + 25% (cost accounts)

As per the cost accounts, factory overheads are at 20% of prime cost and office overheads at 75% of factory overheads.

(Madras, 1995)

[Ans: (a) cost of production = Rs 46,000; (b) profit = Rs 13,275; sales = Rs 79,650; (c) profit = Rs 17,800; and (d) reconciliation = Rs 13,275 + 2,750 + 1,775 = Rs 17,800]

Hint: Stocks of finished goods are common for both accounts in the absence of information about units produced.

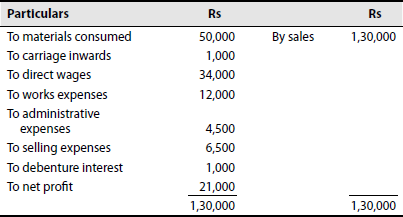

Illustration 10

The financial profit and loss account of a manufacturer for the year ended 31 March 1981 is as follows:

The net profit shown by the cost accounts for the year is Rs 22,270. After a detailed comparison of the two sets of accounts, it is found that

- the amount charged in the cost accounts in respect of overhead charges are as follows: works overhead charges = Rs 11,500; office overhead charges = Rs 4,590 and selling and distribution expenses = Rs 6,640.

- no charge has been made in the cost accounts in respect of debenture interest.

- You are required to reconcile the profits shown by two sets of accounts.

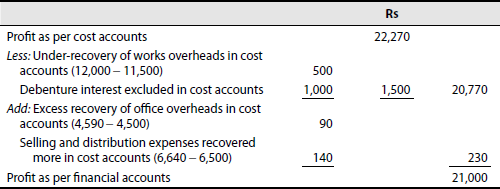

Solution:

Statement showing reconciliation

Problem 10. Find out the profit as per the costing books and reconcile it, from the following information, with that of financial books.

Trading and profit and loss account for the year ended 30 June 1983

In cost accounts, factory overheads is at 20% of prime cost, administration overheads at Rs 5 per unit produced and selling overheads at Rs 5 per unit sold. Opening finished goods balance was the same as in financial books.

[Ans: profit as per cost accounts = Rs 1,13,700; reconciliation = Rs 80,000 + 50,000 + 5,000 + 15,000 + 6,600 − 5,000 − 15,000 − 22,900 = Rs 1,13,700]

Illustration 11

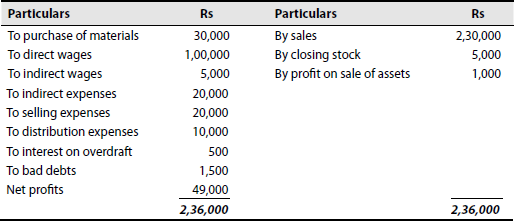

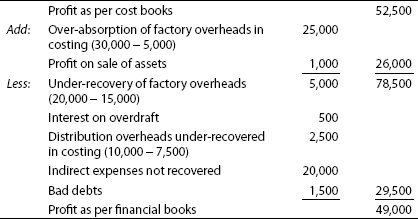

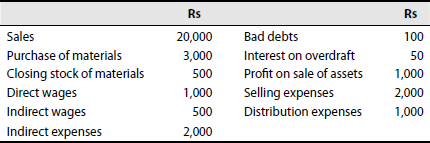

From the following data, calculate profit or loss in cost accounts as well as financial accounts and reconcile them:

| Rs | |

|---|---|

| Sales | 2,30,000 |

| Purchase of materials | 30,000 |

| Closing stock | 5,000 |

| Direct wages | 1,00,000 |

| Indirect wages | 5,000 |

| Bad debts | 1,500 |

| Indirect expenses | 20,000 |

| Interest on overdraft | 500 |

| Profit on sale of assets | 1,000 |

| Selling expenses | 20,000 |

| Distribution expenses | 10,000 |

In cost accounts

Manufacturing overheads recovered at 30% on direct wages

| Selling overheads recovered | Rs 15,000 |

| Distribution overheads recovered | Rs 7,500 |

(B.Com., 1993)

Solution:

Statement of cost and profit

| Particulars | Rs | Rs |

|---|---|---|

| Purchase of materials | 30,000 | |

| Less – closing stock | 5,000 | 25,000 |

| Direct wages | 1,00,000 | |

| Prime cost | 1,25,000 | |

| Factory overheads (30% on wages) | 30,000 | |

| Works cost | 1,55,000 | |

| Selling overheads | 15,000 | |

| Distribution overheads | 7,500 | |

| Cost of sales | 1,77,500 | |

| Profit | 52,500 | |

| Sales | 2,30,000 |

Profit and loss a/c (financial books)

Reconciliation statement

Problem 11. Find out the profit as per the closing records and financial accounts for product X from the following information and reconcile the result:

- Number of units produced and sold: 600 units.

- Direct material: Rs 3,600.

- Direct wages: Rs 3,000.

- Selling price per unit: Rs 30.

The works on cost is charged at 80% of the direct wages and the office on cost at 25% on works cost. The actual works expenses amounted to Rs 4,500 and the office expenses Rs 3,900. There was no opening or closing stock.

(Madras, 1985)

[Ans: profit as per cost accounts = Rs 6,750; profit as per financial accounts = Rs 3,000 nil reconciliation = Rs 6,750 − 2,100 − 1,650 = Rs 3,000]

Illustration 12

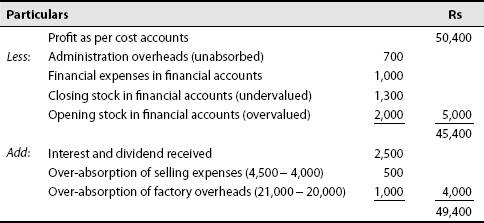

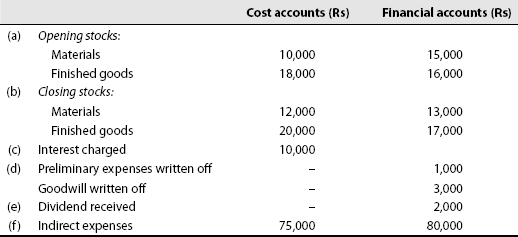

The following figures were available about Ashok Engineering Company for the year ended 31 December 1990:

| Particulars | Financial a/c (Rs) | Costs a/c (Rs) |

|---|---|---|

| Opening stock | ||

| Raw materials | 6,000 | 5,000 |

| Work-in-progress | 7,000 | 6,500 |

| Finished stock | 5,000 | 4,500 |

| Closing stock | ||

| Raw materials | 4,000 | 4,300 |

| Work-in-progress | 3,000 | 3,700 |

| Finished stock | 5,900 | 6,200 |

| Purchases | 40,000 | |

| Direct wages | 20,000 | |

| Indirect wages | 3,000 | |

| Factory expenses | 17,000 | 21,000 (absorbed) |

| Sales | 1,40,000 | |

| Administration expenses | 3,000 | 2,300 (absorbed) |

| Selling expenses | 4,000 | 4,500 (absorbed) |

| Financial expenses | 1,000 | |

| Interest and dividend received | 2,500 |

Compute the profit in financial accounts as well as in cost accounts and prepare a reconciliation statement, showing clearly the reasons for the variations of the two profit figures.

(B.Com., 1991)

Solution:

Statement of cost and profit

| Rs | |

|---|---|

| Opening stock of raw materials | 5,000 |

| Add: Purchase of raw materials | 40,000 |

| 45,000 | |

| Less: Closing stock of raw materials | 4,300 |

| Material consumed | 40,700 |

| Direct wages | 20,000 |

| Prime cost | 60,700 |

| Factory overheads | 21,000 |

| Add: Opening work-in-progress | 6,500 |

| 88,200 | |

| Less: Closing work-in-progress | 3,700 |

| Factory cost | 84,500 |

| Add: Administrative overheads | 2,300 |

| Cost of production | 86,800 |

| Add: Opening finished goods | 4,500 |

| 91,300 | |

| Less: Closing finished goods | 6,200 |

| Cost of goods sold | 85,100 |

| Selling expenses | 4,500 |

| Cost of sales | 89,600 |

| Profit | 50,400 |

| Sales | 1,40,000 |

Profit and loss account (financial books)

Reconciliation statement

Problem 12. The profit as per the cost accounts is Rs 1,50,000. The following details are ascertained on a comparison of the cost and financial accounts:

Find out the profit as per the financial accounts by drawing up a memorandum reconciliation account.

[Srivenkateswara]

[Ans: profit as per financial accounts = Rs 1,48,000]

Illustration 13

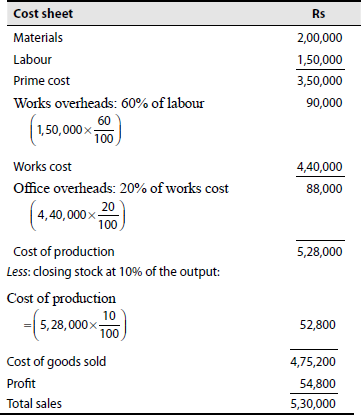

In a factory, works overheads are absorbed at 60% of labour and office expenses at 20% of works cost. The total expenditure is as follows:

| Rs | |

|---|---|

| Materials | 2,00,000 |

| Labour | 1,50,000 |

| Factory expenses | 98,000 |

| Office expenses | 87,000 |

| Total | 5,38,000 |

Of the output, 10% is in the stock and sales total up to Rs 5,30,000. Prepare a cost sheet and a reconciliation statement.

Solution:

To prepare a reconciliation statement, it is necessary to ascertain the profit and loss account and the profit as per cost accounts, as they are not provided in the problem.

Profit and loss account

Reconciliation statement

Problem 13. Profits disclosed by a company's cost accounts for the year 1995 was Rs 50,000. The following information is available:

- Overheads as per cost accounts were Rs 8,500 while Rs 7,000 was recorded as overheads in financial accounts.

- Director's fees shown in financial accounts only Rs 2,000.

- The company allocated Rs 5,000 as provision for doubtful debts.

- Depreciation was shown as Rs 750 in financial accounts whereas in cost accounts it was shown as Rs 1,500.

- Share transfer fees received during the year Rs 4,000.

- Provision for income tax was Rs 20,000.

Prepare cost and financial reconciliation statements.

(Madras, 1997)

[Ans: profit as per financial accounts = Rs 29,250]

Illustration 14

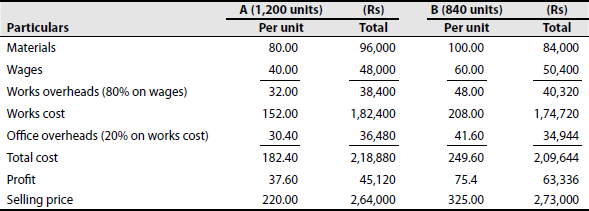

A radio manufacturing company, which commenced business on 1 January 1989, supplies you with the following information and you have to prepare a statement showing the profit per radio sold. Wages and materials are to be charged at actual cost, works overheads at 80% on wages and office overheads at 20% on works cost. You are required to prepare a statement reconciling the profit as shown by the profit and loss account for the year ended 31 December 1989 with that shown in the cost accounts.

Two types of radio sets are manufactured: -Models A and B. There were no radio sets in stock or in the course of manufacture at the end of the year and the number of radio sets sold during the year were: Model A = 1,200 and Model B = 840. The particulars given are as follows:

| A (Rs) | B (Rs) | |

|---|---|---|

| Materials per radio set | 80 | 100 |

| Wages per radio set | 40 | 60 |

| Selling price per radio set | 220 | 325 |

The indirect works expenses were Rs 90,000 and the indirect office expenses were Rs 70,000.

Solution:

Statement showing total profit and profit per radio sold

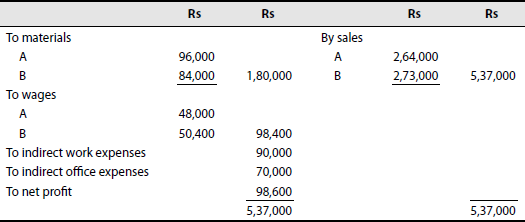

Profit and loss account for the year ended 31 December 1989

Statement showing reconciling the profit shown by the profit and loss account with that shown in cost accounts

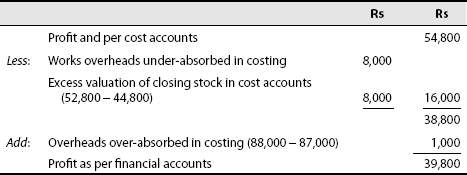

| Rs | |

|---|---|

| Profit as per profit and loss account | 98,600 |

| Add: works overheads undercharged in cost accounts (90,000 – 78,720) | 11,280 |

| 1,09,880 | |

| Less: office overheads overcharged in cost accounts (71,424 – 70,000) | 1,424 |

| Profit as per cost accounts | 1,08,456 |

| Model A = Rs 37.6 × 1,200 | 45,120 |

| Model B = Rs 75.4 × 840 = 63,336 | 63,336 |

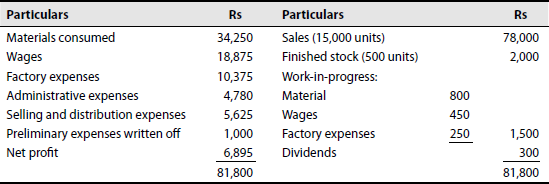

Problem 14. The summary of trading and profit and loss account of a company is as follows:

The company manufactures a standard unit. In the cost accounts, factory expenses have been allocated to production at 20% of prime cost, administration expenses at 0.30 paise per unit and selling and distribution expenses at 0.40 paise per unit. The net profit shown by the cost accounts was Rs 7,100.

Prepare:

- Control accounts for factory expenses, administration expenses, and selling and distribution expenses.

- A statement reconciling the profit disclosed by the cost records with that shown in the financial accounts.

(Madras, 1975)

[Ans: reconciliation: Rs 6,895 + 130 + 1,000 − 375 − 300 − 250 = Rs 7,100]

Hint: In costing finished stock value was taken as Rs 2,000 to arrive at the net profit of Rs 4,100.Difference in work-in-progress valuation = Rs 250.

Illustration 15

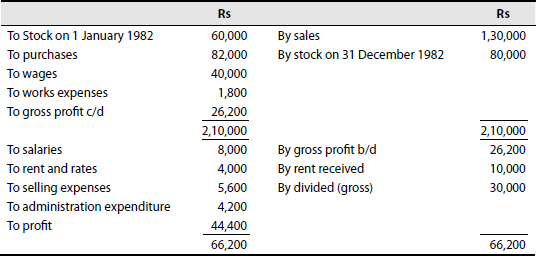

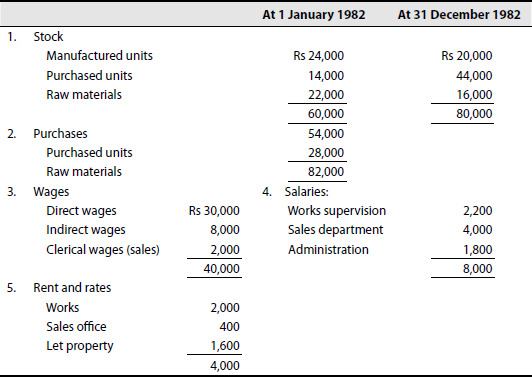

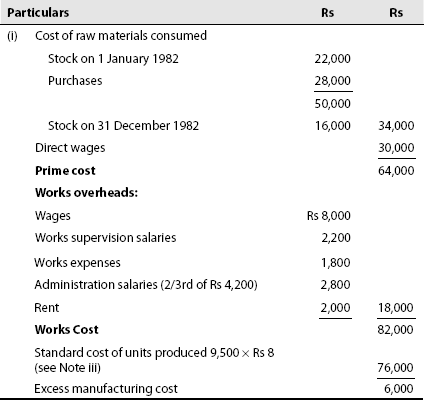

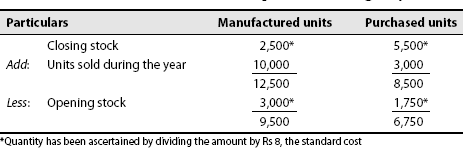

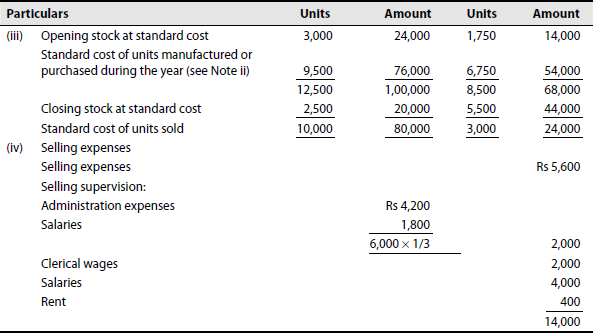

The trading and profit and loss account of M/S XY (P) Ltd for the year ended 31 December 1982 (as prepared by the head office accounts department) is summarized as follows:

Trading and profit and loss account

Following information was also supplied:

Other particulars:

- Purchased units 3,000 and manufactured units 10,000 were sold at the rate of Rs 10 each.

- Units were purchased at Rs 8 each. Units produced by the company were valued at Rs 8 each.

- Administrative expenditure: two-thirds to be charged to works supervision and one-third to sales supervision.

- Divided was on trade investments.

You are required to prepare a costing profit and loss account for the year ended 31 December 1982, for submission to the higher management.

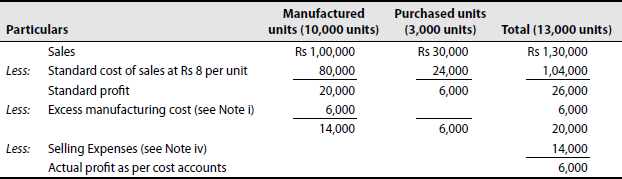

Solution:

Costing profit and loss account for the year ended 31 December 1982

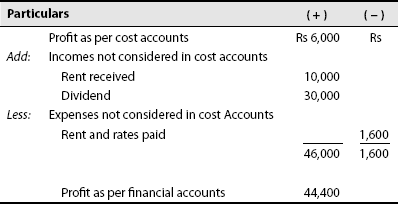

Statement reconciling the profit as per cost accounts with the profit as per financial accounts

Working Notes:

Statement of manufacturing cost

Statement of units manufactured or purchased during the year

Standard cost of sales

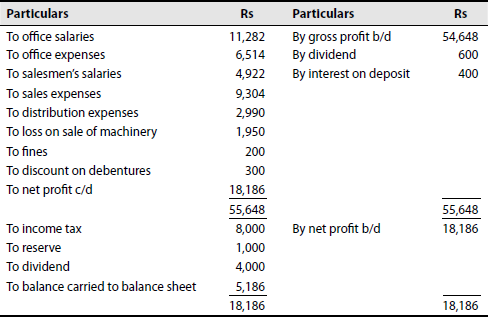

Problem 15. From the following profit and loss account draw up a memorandum reconciliation account, showing the profit as per cost accounts:

Profit and loss account (31 December 1986)

The cost accountant of the company has ascertained a profit of Rs 19,636 as per his books.

[ICWA, Inter]

[Ans: reconciliation = Rs 19,636 + 600 + 400 − 1,950 − 200 − 300 − 8,000 − 1,000 − 4,000 = Rs 5,186]

Illustration 16

When profits as per financial accounts is given

The following is a summary of the trading and profit and loss account of ****Messrs. Alpha Manufacturing Co. Ltd for the year ended 31 March 2001:

The company manufactures a standard unit. In the cost accounts:

- Factory expenses have been recovered from production at 20% on prime cost.

- Administration expenses at Rs 3 per unit on units produced.

- Selling and distribution expenses at Rs 4 per unit on units sold.

You are required to prepare a statement of cost and profit in cost books of the company and to reconcile the profit disclosed with that shown in the financial accounts.

Solution:

Statement of cost and profit

Reconciliation statement

[Ans: profit as per cost accounts = Rs 23,063]

Problem 16. According to the costing books of Sunlight Co. Ltd, the net profit was Rs 27,780. Prepare a reconciliation statement explaining the reasons for the differences in profits, from the following:

Profit and loss account for the year ended 31 December 1976

The costing records show the following:

| Rs | ||

|---|---|---|

| (a) | Closing stock | 25,630 |

| (b) | Direct wages recovered during the year | 16,720 |

| (c) | Works overheads recovered | 18,560 |

| (d) | Administration overheads charged | 15,460 |

| (e) | Selling expenses charged | 740 |

(Madras, 1987)

[Ans: reconciliation: Rs 27,780 + 1,070 + 1,000 − 4,570 − 2,000 − 560 = Rs 22,720]

CHAPTER SUMMARY

After going through this chapter one should be able to understand the reasons for the differences in cost profit and financial profit locate the items that would appear exclusively in cost and financial accountsand understand the process of reconciling cost profit and financial profits.

KEY FORMULAE

EXERCISE FOR YOUR PRACTICE

Objective-Type Questions

I. State whether the following statements are true or false:

- Cost and financial accounts are reconciled under non-integral accounting.

- Rent on owned buildings is not included in cost accounts.

- Income tax is provided only in cost accounts.

- Under-absorption of production overheads is deducted while reconciling cost profit with financial profits.

- Under valuation of closing stock in cost accounts is added while reconciling cost profit with financial profits.

- Under absorption = actual > estimated.

- Over absorption = actual > estimated.

- Costing profit and loss account and financial profit and loss account are the same.

- Capital losses shown in financial accounts are deducted while reconciling costing profits with financial profits.

- Under absorptions are caused by clerical errors.

[Ans: 1—true, 2—false, 3—false, 4—true, 5—true, 6—true, 7—false, 8—false, 9—true, 10—false]

II. Choose the correct answer:

- Which of the following items is include in cost accounts?

- Notional profit

- Rent receivable

- Transfer to general reserve

- None of these

- Cost and financial accounts are reconciled under

- Integral system

- Cost-control accounts system

- Both a and b

- None of these

- Which of the following items is not included in financial books?

- Loss on sale of fixed assets

- Interest on capital

- Notional rent

- Donations

- Which of the following items shall be added to costing profit to arrive at financial profit?

- Income tax paid

- Interest on debentures

- Under absorption of overheads

- Rent receivable

- When costing profit is Rs 13,500 and a charge in lieu of rent is Rs 2,000, then the financial profit should be

- Rs 13,500

- Rs 15,500

- Rs 11,500

- None of these

- While reconciling costing profits with financial profits, under recovery of works overheads is

- Deducted

- Added

- Not included

- Doubled

- While reconciling costing profits with financial profits, capital expenses and losses in financial accounts are

- Doubled

- Added

- Not included

- Subtracted

- When costing loss is Rs 7,600, office overheads under absorbed being Rs 800, the loss as per financial accounts should be

- Rs 6,800

- Rs 7,600

- Rs 8,400

- None of these

- Dividend interest on investment and discount are shown in

- Cost accounts

- Management accounts

- Book keeping

- Financial accounts

- In cost accounts, the stock is valued at

- Cost

- Market price

- No value

- Cost plus profit

[Ans: 1 — (a), 2 —(b), 3 —(c), 4 —(d), 5 —(b), 6 — (a), 7 —(d), 8 —(c), 9—(d), 10 —(a)]

DISCUSSION QUESTIONS

Short Answer-Type Questions

- What is reconciliation?

- State the importance of reconciliation.

- How do you solve the sum when both the profits are given?

- At what situation reconciliation statement need not be prepared?

- Give the accounting procedure when only one of the profits is given.

Essay-Type Questions

- Why is the reconciliation of cost and financial accounts necessary?

- State the possible reasons for difference in profits shown by financial accounts and cost accounts.

- What are the items to be added when cost profit is taken as the base?

- What are the items to be deducted when cost profit is taken as the base?

- What is the accounting procedure when both the profits are not given?

- Discuss the need for reconciliation of cost and financial accounts.

- State briefly the treatment of under or over absorption of overheads while reconciling costing profits with financial profits.

- How will you treat under or overvaluation of stocks in cost accounts while preparing reconciliation statement.

- Discuss the effect of under or over charge of depreciation in cost accounts and financial accounts.

PROBLEMS

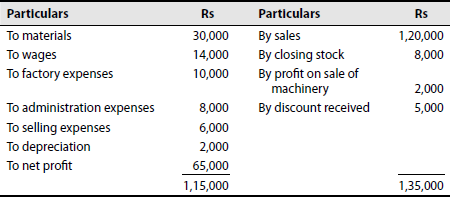

- ‘Native’ Co. Ltd suffered a loss of Rs 25,000 as per the financial accounts. On comparison with its costing records for the same year, the following differences were observed:

Prepare a reconciliation statement, with the help of the differences.

Rs Overvaluation of opening stock of materials in cost books 1,200 Under valuation of closing stock of finished goods in financial books 3,000 'Dormant’ materials written off (in financial books) 1,000 Under absorption of overheads 4,000 Fines levied by Municipality 500 Debenture interest paid 2,000 [Ans: loss as per cost accounts = Rs 15,700]

- The profit as per cost accounts in 1987 was Rs 1,65,300. The following details are ascertained on comparison of the cost and financial accounts:

You are required to draw a reconciliation statement.

(Madras, 1986)

[Ans: profit as per financial accounts = Rs 1,58,700]

Profit and Loss Account and additional information given—Cost sheet and reconciliation required

- From the following profit and loss account and additional information given, prepare: (a) a cost sheet and (b) reconciliation statement

Profit and loss account

In costing, opening materials were shown at Rs 7,000. The factory overheads were absorbed at Rs 14,000. Administration overhead charges 10% of works cost and selling overheads was 10% of sales.

[Ans: profit as per cost accounts = Rs 71,900; reconciliation = Rs 70,000 + 1,000 + 1,400 + 6,000 − 2,000 − 4,500 = Rs 71,900]

Hint: Closing materials are shown in costing at the same value as in financial accounts as it cannot be found separately.

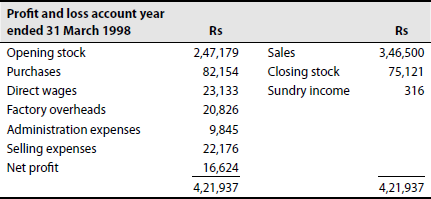

- Financial profit and loss account of a manufacturing Company for the year ended 31 March 1998 is as follows:

To net profit shown by the cost accounts for the year is Rs 16,270. Upon detailed comparison of the two sets of accounts it is found that:

- The amounts charged in the cost accounts in respect of overhead charges are as follows: works overhead charges = Rs 11,500; office overhead charges = Rs 4,590; selling and distribution expenses = Rs 6,640.

- No charge has been made in the cost accounts in respect of debenture interest.

Your are required to reconcile the profits shown by the two sets of accounts.

(B.Com. Punjab)

Hint: [Add: Over-absorption of administration overheads Rs 90 and S and D overheads Rs 140. Less: Under recovery of works expenses Rs 500 and debenture interest Rs 1,000]

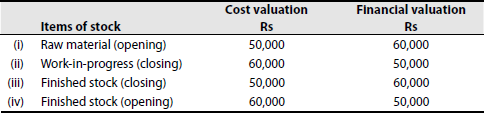

- In the reconciliation between cost and financial accounts, one of the areas of differences is different methods of stock valuation used. State with reasons, in each of the following circumstances whether costing profit will be higher or lower than the financial profit:

[Ans: Items (i) and (ii) will increase the profit each by Rs 10,000 and items (iii) and (iv) will decrease the profit each by Rs 10,000]

- A company maintains separate cost and financial accounts, and the costing profit for the year 1998 differed to that revealed in the financial accounts, which was shown as Rs 50,000.

The following information is available:

Cost accounts

RsFinancial account

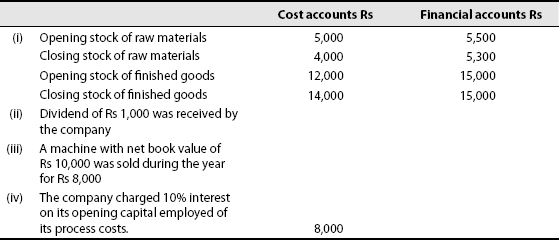

RsOpening stock of raw material 5,000 5,500 Closing stock of raw material 4,000 5,300 Opening stock of finished goods 12,000 15,000 Closing stock of finished goods 14,000 16,000 - Dividend of Rs 1,000 was received by the company.

- A machine with net book value of Rs 10,000 was sold during the year for Rs 8,000.

- The company charged 10% interest on its opening capital employed of Rs 80,000 to its process costs.

You are required to determine the profit figure which was shown in the cost accounts.

(B.Com. Delhi)

[Ans: profit as per cost accounts = Rs 43,200]

- During the year ended 31 March 1998 a company's profit as per financial accounts was Rs 16,624. Prepare a reconciliation statement and arrive at the profit as per cost accounts using the additional information given below:

The costing records show:

- Closing stock = Rs, 78, 197;

- direct wages = Rs 24,867;

- factory overheads absorbed= Rs 19,714;

- administration expenses calculated at 3% of sales; and

- selling expenses absorbed at 5% of sales.

(CS – Inter)

[Ans: profit as per cost accounts = Rs 23,063]

- From the following figures prepare a reconciliation statement:

Rs Net loss as per costing records 1,72,400 Works overheads under-recovered in costing 3,120 Administrative overheads recovered in excess 1,700 Depreciation charged in financial records 11,200 Depreciation recovered in costing 12,500 Interest received notincluded in costing 8,000 Obsolescence loss charged in financial records 5,700 Income tax provided in financial books 40,300 Bank interest credited in financial books 750 Stores adjustments (credit) in financial books 475 Value of opening stock in: Cost accounts 52,600 Financial accounts 54,000 Value of closing stock in: Cost accounts 52,000 Financial accounts 49,600 Interest charged in cost accounts but not in financial accounts 6,000 Preliminary expenses written off in financial accounts 800 Provision for doubtful debts in financial accounts 150 (CS INTER, 1997)

[Ans: net loss at per financial records = Rs 2,08,045]

- From the following details of Small Tools Ltd, compute the profit in financial accounts as well as in cost accounts and reconcile profit between cost and financial accounts showing clearly the reasons for the variation of the two profit figures:

In cost accounts:

Manufacturing overheads recovered at 300% on direct wages.

Selling overheads recovered Rs 1,500

Distribution overheads recovered Rs 700.

(B.Com. Andhra)

[Ans: profit as per financial accounts = Rs 11,850; profit as per cost accounts = Rs 11,300]

- The following is the summarized version of trading and profit and loss account of Continental Enterprises Limited for the year ended 31 March 1998.

During the year, 6,000 units were manufactured and 4,800 of these were sold.

The costing records show that works overheads have been estimated at Rs 3 per unit produced and administration overheads at Rs 1.50 per unit produced. The costing books show a profit of Rs 11,040.

Prepare a statement a cost and profit and reconcile the profit as per cost accounts and financial books.

(B.Com, Delhi)

[Ans: over-recovery of administration overheads = Rs 3,000; under recovery of factory overheads = Rs 4,800; over-valuation of closing stock in cost accounts = Rs 840].

- SV Ltd. has furnished you the following information from the financial books for the year ended 31 March 1998.

Profit and loss account for the year ended 31 March 1998

The cost sheet shows the cost of materials as Rs 26 per unit and the labour cost as Rs 15 per unit. The factory overheads are absorbed at 60% of labour cost and administration overheads at 20% of factory cost. Selling expenses are charged at Rs 6 per unit. The opening stock of finished goods is valued at Rs 45 per unit.

You are required to prepare:

- A statement showing profit as per cost accounts for the year ended 31 March 1998.

- Statement showing the reconciliation of profit disclosed in cost accounts with the profit shown in the financial accounts.

(CAINTER)

[Ans: (i) Rs 48,500]