Making Cost-Effective Energy Efficiency Fit Utility Business Models

Why has It Taken So Long?

Ralph Cavanagh†, Energy Program Co-Director, Natural Resources Defense Council, †The author gratefully acknowledges perceptive comments and editorial guidance from Sheryl Carter, Sierra Martinez, Patricia Remick, and Devra Wang. Figures 6.1, 6.3 and 6.4 were prepared by Sierra Martinez.

1 Introduction

Most utilities, whether publicly or privately owned, operate under a system of price regulation that treats them like commodity distribution businesses, whose principal rewards lie in boosting unit sales and reducing average unit costs. For electric utilities at least, this worked very well for much of the 20th century; from 1973–2000, for example, retail electricity sales more than doubled in the United States, while the population increased by only 33 percent.1

High confidence in rapid sales growth, coupled in many cases with automatic rate adjustments to ensure recovery of any increase in fuel costs, allowed many utilities to defer explicit requests for rate increases almost indefinitely; any escalation in non-fuel costs could be covered by rising electricity sales volumes. Customers, meanwhile, typically shouldered the risks and costs of any surges in fuel prices. Of course, this business model was inconsistent with any serious effort to promote energy efficiency, no matter how inexpensive it might be to achieve the savings.

As early as 1989, the National Association of Regulatory Utility Commissioners (NARUC) called on its members to encourage utilities to substitute cost-effective energy efficiency for more costly generation wherever feasible and to “ensure that the successful implementation of a utility’s least-cost plan is its most profitable course of action.”2 This chapter discusses why that objective remains unrealized, even as the nation moves urgently to accelerate energy efficiency progress, expand its renewable energy base, and upgrade its transmission and distribution grids.

For more than two decades, debates have raged over proposals to break the linkage between utilities’ financial health and their retail commodity sales, and to introduce earnings opportunities associated with energy efficiency gains in their service territories. In the United States, these decisions rest with state commissions (for shareholder-owned utilities) and local boards (for publicly-owned utilities).

Progress has been far too slow, in part because regulators and their staffs are protective of traditional practices, and in part because other parties, including the utilities themselves, have worried that change would introduce new risks or erode long-held advantages. Although California decoupled gas and electric utilities’ financial health from sales more than 30 years ago, by 2008 only a dozen other states had taken similar action on behalf of at least one natural gas utility; for electric utilities the count stood at just four. Four years later, following a national campaign that prominently included the Natural Resources Defense Council (NRDC), the totals had reached 21 and 15, respectively.

The case for swifter progress becomes more urgent daily, given both the magnitude of the nation’s unrealized efficiency potential, reinforced throughout this volume, and a widening consensus that robust growth in energy commodity sales is untenable on both economic and environmental grounds. From 2000–2011, for example, electricity sales lagged behind population growth for the first extended period in U.S. history (Figure 6.1); for natural gas utilities’ retail sales, the same trend is much more firmly established.3 Utilities across the nation face long-term prospects of at best modest increases in commodity sales, even as their needs to make and recover capital investments expand.

Figure 6.1 Trends in U.S. Electricity Consumption and Population, 1973–2011.4

The remainder of this chapter explains why utilities need a new business model (in section 2), advocates revenue decoupling as a necessary but not sufficient element, and outlines (in section 3) the performance-based earnings opportunities that are essential to having utilities’ profitability reflect their success in promoting cost-effective advances in energy efficiency and distributed generation.

2 A Broken Business Model

Given the sobering condition of federal and state governments’ balance sheets, most new electricity infrastructure will have to be financed with utility revenues, in competition with alternative solutions to meeting energy service needs.5 Moreover, much of the genius in such procurement is integration of diverse resources under ever-shifting real-time conditions. Demands for this kind of expertise are relatively new to an industry known mostly in decades past for managing giant construction projects. Consider, for example, one major electricity supplier’s recent summary of its resource plan:

Most of [our] incremental energy needs for the next several years can be met by meeting [our] conservation targets. In addition to relying on conservation, [we] plan to continue to:

![]() Rely on short- and mid-term wholesale power market purchases.

Rely on short- and mid-term wholesale power market purchases.

![]() Facilitate the effective, efficient and reliable integration of renewable resources to [our] system.

Facilitate the effective, efficient and reliable integration of renewable resources to [our] system.

![]() Increase transmission grid operating flexibilities, develop smart grid technologies, and directly involve electricity users through demand response programs.

Increase transmission grid operating flexibilities, develop smart grid technologies, and directly involve electricity users through demand response programs.

![]() Track, evaluate, and appropriately pursue availability of pumped storage and natural gas-fired resources for seasonal heavy load hour energy and/or balancing reserves.6

Track, evaluate, and appropriately pursue availability of pumped storage and natural gas-fired resources for seasonal heavy load hour energy and/or balancing reserves.6

For utility systems with responsibilities like these – which is to say most of them, at least in the United States – clarity will be needed regarding both cost recovery and accountability. For example, when and on what terms may distribution utilities enter into long-term contracts with generation service providers? How will distribution utility responsibilities interact with the opportunities created for competitive retail suppliers in states with retail competition? Who has the responsibility for identifying needed enhancements to the transmission network? How will transmission providers be paid for securing them, and who will pay? What, if any, rewards will be earned by utilities that reduce the cost of balancing their systems’ loads with variable-output generation from wind and solar plants?

Most nations rely at least in part on resource procurement and integration by regulated distribution companies. Even in countries and U.S. states (like Texas) that are inclined to view regulated utilities largely as managers of interconnected wires and pipes, with all or much resource procurement entrusted to other entities, utility-owned distribution systems increasingly need to address the challenge of integrating variable-output electricity production, and both electric and natural gas utilities’ customers collectively would benefit from help in substituting low-cost energy efficiency for higher-cost alternatives.

For this purpose, energy efficiency should be treated as a utility system resource that is the functional equivalent of other ways to meet customers’ aggregate demand. Regulators should aim to ensure an acquisition process open to all competitors, with results that minimize the life-cycle cost of reliable electricity service while meeting society’s environmental goals. Within the for-profit sector, the theme of NARUC’S 1989 resolution remains compelling: utilities that effectively manage resource procurement and integration should be more profitable than inferior performers. And publicly-owned utilities should not confront an automatic deterioration in creditworthiness if their energy efficiency efforts cause sales to decline or grow more slowly.

2.1 The Wrong Path: Higher Fixed Charges

Since both for-profit and non-profit utilities recover most of their fixed costs of service through charges on electricity and natural gas use, increases or reductions in consumption will affect fixed cost recovery, even though the costs themselves do not change. Overcoming this problem means ensuring that fluctuations in sales (either up or down) do not result in over- or under-recovery of utilities’ previously approved fixed costs.

The immediate temptation is to convert all or most fixed costs into fixed charges. This would indeed make the recovery of fixed costs independent of energy sales, but it would also significantly reduce customers’ rewards for reducing energy use. That is a step in the direction of what might be termed “all you can eat” rates, which reduce or eliminate customers’ rewards for saving energy by making their utility bills largely or wholly independent of total energy consumption. This may sound like an improbable caricature, but in 2012 it became a retail service option in Texas, where Reliant Energy Retail Services’ “Predictable” rate plan was precisely that: residential customers who enrolled paid $150 per month regardless of electricity use.

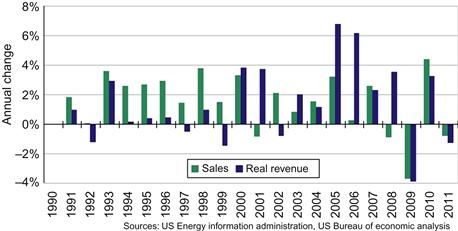

What the world needs now to encourage more energy efficiency is not rate designs that encourage energy waste, but a strong embrace of inverted rates, where the rule is “the more you use, the more you pay.” We need not and should not abandon reliance on commodity charges to recover the costs of electricity and natural gas service. Over the past 22 years, for example, as Figure 6.3 shows, U.S. electricity sales have declined by more than one percent only once (in 2009); in 18 of the 22 years, annual sales increased (although they have been increasing less rapidly than population since 2000). The changing electricity sales outlook does not portend sudden sharp declines that might force abandonment of volume-based cost recovery and the rewards it offers to those who use less. But utilities will legitimately question how the financial interests of their bondholders and shareholders can be squared either with rate designs that increase variability of revenue recovery, or with sustained recovery of largely fixed network costs over uncertain volumetric sales. Fortunately, there is a straightforward remedy called “revenue decoupling” that does not require changing rate designs or reducing rewards for customers who save energy.

2.2 The Revenue Decoupling Debate

If utilities continue relying on variable charges to recover all or most authorized fixed costs of service, disincentives for energy efficiency engagement will persist. Revenue decoupling uses small, regular rate adjustments to prevent over- or under-recovery of authorized costs. Under decoupling, a simple system of periodic true-ups in base rates either restores to the utility or gives back to customers the dollars that were under- or over-recovered because of fluctuations in retail sales. This corrects for disparities between the utility’s actual fixed cost recovery and the fixed-cost revenue requirements approved by utility regulators.8

Decoupling proposals were initially controversial among both utilities and consumer advocates, both of which were uncomfortable with a shift in the regulatory status quo and its allocation of revenue-based risks and opportunities. Electric utilities often were reluctant to surrender the upside in revenues associated with retail sales growth. For their part, many consumer advocates either opposed these proposals outright or sought to attach financial penalties in the form of reductions in utilities’ authorized returns on equity. Utility managements were understandably unenthusiastic about absorbing an automatic upfront loss to shareholders as part of a regulatory reform that was supposed to remove a financial obstacle to utilities’ promotion of energy efficiency gains.

In California, the state with by far the longest decoupling experience (starting in 1981),9 it has been at least a decade since any party challenged the mechanism or sought to link it with any form of financial penalty to either gas or electric utilities. Elsewhere, revenue decoupling retains powerful opponents, although an urgent recent search for common ground is yielding promising results. For example, the online journal ElectricityPolicy.com recently published an extended exchange between the author (representing the Natural Resources Defense Council [NRDC]) and John Howat of the National Consumer Law Center.10 NRDC is a long-time proponent of revenue decoupling, and NCLC is a leader among consumer advocates with a history of skepticism about the concept. An excerpt follows, which helps illuminate both the sources of resistance and the best ways to address them:

CAVANAGH [environmental perspective]: John, we’ve recently been in a hearing room together where, not for the first time, environmental and consumer advocates were at odds over whether to introduce revenue decoupling as part of a strategy for enhancing energy efficiency investment. What is your view here?

HOWAT [consumer perspective]: NCLC has on many occasions been critical of revenue decoupling mechanisms that blindly reward companies for reductions in sales for reasons that have nothing to do with utility-sponsored energy efficiency. But a well-structured decoupling mechanism is in my view far preferable to “straight-fixed variable” (SFV) design, for example, that penalizes low-volume utility consumers while removing volumetric pricing efficiency incentives for all utility customers. I urge colleagues to accept revenue decoupling that is directly tied to new investment in comprehensive, cost-effective energy efficiency programs and measures and that includes (1) rate increase collars that limit upside rate volatility, (2) explicit regulatory review and adjustment of return on equity to account for altered utility risk profiles (retrospective, but in a reasonable timeframe is fine with me), (3) review and adjustment of baseline utility cost structure assumptions including cost of capital on some regular basis, and (4) the “Tucson model” of implementing inclining block rates, where decoupling surcharges are tied to higher usage blocks and surcredits to the initial usage bock. Again, such a structure would, in my view, be far preferable to implementation of SFV in the name of promoting energy efficiency. Further, I’ve long agreed with you about the need to address the utility “throughput addiction,” and that best-quality energy efficiency represents our most valuable energy resource.

CAVANAGH: Let’s unpack this a bit, because I don’t see anything here that should divide us. I agree on the need to pair revenue decoupling with enhanced energy efficiency performance and benefits, and we have supported rate increase collars of three percent for electric utilities and five percent for gas utilities (with no limit on rate reductions associated with decoupling). I supported the Tucson Electric proposal that you cite, which would apply any decoupling-related rate increases to the highest use block of consumption in a rate structure, and apply any reductions to the baseline block (so that any decoupling adjustments would amplify rather than mute the rewards for saving energy that inclining block rates provide to customers). So far so good?

HOWAT: Yes, there is plenty of room to work together here. We need to break the link between utility profits and sales, and design the decoupling mechanism in a way that makes sense for consumers interested in stable prices and an appropriate regulatory treatment of the utility cost structure and risk profile.

CAVANAGH: On cost of capital adjustments, the crucial phrase in your response is “retrospective, but in a reasonable timeframe.” Our latest proposal, which you heard me defend before the Washington Commission, also reflects your call for “review and adjustment of baseline utility cost structure assumptions including cost of capital on some regular basis.” We recommend that Commissions not link decoupling mechanisms with targeted prospective reductions in cost of capital, which may or may not materialize (and have yet to be documented empirically after three decades of experience), but we support continuous review of any changes in utilities’ capital structure, whatever the cause, and full passthrough of any associated cost savings to customers. If, as authorities like the Regulatory Assistance Project maintain, decoupling should help establish a long-term foundation for consumer-friendly changes in capital structure, our proposal ensures prompt and full delivery of benefits if and when they appear.

HOWAT: I agree with you that the key, with respect to cost of capital adjustments, is in the assurance of periodic regulatory review. I was gratified to hear you state at the hearing in Washington that revenue decoupling should not be viewed as a means of doing away with regulatory process.11 Rather, it is a means of re-aligning incentives to eliminate utility aversion to effectively promoting energy efficiency programs that work.

CAVANAGH: Finally, can we agree that revenue decoupling appropriately treats the “throughput addiction” to which you refer, in the simplest possible way, by avoiding efforts to adjudicate inevitably speculative causes of increases or reductions in sales, and simply ensuring instead that utilities’ ability to recover fixed-cost revenue requirements is not affected by changes in retail sales that regulators did not anticipate when they set retail rates?

HOWAT: That is a great question that I frankly have struggled with over the years. Like many advocates, I have bristled at the prospect of “rewarding” utility companies for declining sales that have absolutely nothing to do with their efforts to enhance energy efficiency. After all, sales will decline in times of economic downturn, during mild weather conditions, when appliances become more efficient, when end-users invest in energy efficiency improvements on their own, and, in some instances, when fuel prices increase. However, because utilities inevitably file for rate increases anyway if revenues erode for any of the reasons listed above, and because revenue decoupling provides consumers with declining rates as sales increase for any reason, my thinking on this issue has evolved over time. I have come to agree that, as long as a utility company’s return on equity is appropriately adjusted to reflect changes in the sales risk faced by that company through implementation of revenue decoupling, and the measures mentioned above are part of the design, it is appropriate to embrace a full – rather than partial – decoupling mechanism.

CAVANAGH: All of this is very helpful and I seek only one final clarification: can we agree that such regulatory adjustments should reflect observed changes in cost of capital once the mechanism has been adopted? To use your earlier phrase: “retrospective, but in a reasonable timeframe.” We would support both regular reviews and immediate passthroughs of any savings; our objection is to imposing reductions in costs of capital prospectively, before there is evidence of whether and to what extent they have occurred.

HOWAT: I agree that as long as regulators retain full authority and responsibility to adjust return on equity to reflect changes in a company’s risk profile, adjustments specifically related to a company’s cost of capital may be made in a timely manner after evidence of actual increases or decreases is presented.

This dialogue suggests grounds for optimism about progress on revenue decoupling for electric and natural gas utilities. Figure 6.2 above shows that about half the states had embraced revenue decoupling for at least one of their investor-owned electricity and natural gas utilities by mid-2012, although decoupling mechanisms still covered well under half of total retail sales. Public power took its first strong step toward decoupling when the nation’s largest municipal utility, the Los Angeles Department of Water and Power (LADWP), released a proposal to adopt it in May of 2012.12

Figure 6.3 Annual Changes in Utilities’ Electricity Revenues and Sales.7

Some have argued for an approach called “lost revenue recovery” as an alternative to revenue decoupling.13 The superficially appealing rationale for such systems is that they focus solely on compensating utilities for lost revenues associated with their own energy efficiency programs, which allegedly removes any disincentive to help customers use less electricity and natural gas while leaving the allocation of other business risks unchanged.

But any such rationale is misleading in the extreme. Lost revenue recovery schemes leave intact automatic penalties, in the form of reduced fixed-cost recovery, for all cost-effective electricity savings not directly associated with a utility’s own programs, even when the company by action or inaction could make a material difference in prospects for those savings. Examples include federal and state efficiency standards and programs administered by other parties, all of which can benefit significantly from utility cooperation and support. Small-scale “distributed” generation on customers’ premises would produce the same kind of adverse balance sheet effects. Rewarding a utility for a limited category of adjudicated efficiency gains while penalizing it for all the rest is analogous to trying to drive with one foot on the brake and the other on the accelerator. Moreover, lost-revenue recovery would create a reason for utilities to promote programs that looked good on paper but delivered little or no savings in practice.14 And it would ensure adversarial discord over every savings calculation, since significant financial stakes and rate impacts would hinge on the results. Finally, and most tellingly, rate adjustments keyed solely to adjudicated savings would mean automatic annual rate increases (unless the company was wholly ineffective), whereas decoupling adjustments can be either positive or negative.

Some have argued that revenue decoupling pays utilities for savings that they didn’t help achieve. But decoupling mechanisms don’t “pay” anyone any incremental amount for anything; they simply allow utilities to receive no more and no less than the fixed-cost revenue requirement that their regulators have reviewed and approved. This underscores the point that revenue decoupling, while a crucial step in the right direction, is not a panacea. It removes a powerful disincentive for energy efficiency progress, but it does not by itself create the prospect of reward for exemplary results. Both are needed. In the hope that the revenue decoupling debate has been outlined fully above, the final section of this chapter turns to what remains to be done, even assuming that decoupling becomes a regulatory norm for electric and natural gas distribution systems in the United States and abroad.

3 Toward a New Utility Business Model

To sustain their excellence in efficiency, the investor-owned utilities that deliver three-quarters of the nation’s electricity and most of its natural gas will require more than just protection from instant pain. A dozen states have acted to assure that independently verified net energy efficiency savings to customers will also yield a reward for utility shareholders.15 One option is to allow utilities to earn a rate of return on approved efficiency expenditures that is at least equal to the compensation afforded prudent generation or grid investments. A better alternative, however, is a compensation system tied to independently verified performance in delivering cost-effective savings to customers, rather than just “tonnage of capital committed.”16 Whether the issue is power plant construction or energy efficiency incentives, there is growing discomfort about shareholder rewards based on how much a utility spent to get the desired result.17

A balance must be struck between rewarding performance at a reasonable level and creating outsized “compensation” that invites endless discord over savings estimates that can never achieve complete precision (because one can never know with certainty what would have happened without utility intervention). The “lost revenue recovery” mechanisms described earlier are doomed to failure because any reasonable level of adjudicated lost revenue recovery dramatically raises the cost of every kilowatt-hour saved, given the fraction of the typical kilowatt-hour charge that fixed cost recovery represents (at least half). Utilities with appreciable annual savings would generate guaranteed, escalating annual rate increases under this model, with results that would soon test even the most highly motivated regulators.18 As explained above, revenue decoupling avoids any possibility of these adverse cumulative impacts, by using regular and modest rate adjustments that go in both directions, with an eye solely to preventing annual fixed-cost recovery from either exceeding or dropping below a previously approved target.19

On the other hand, it is no solution for regulators to overlook or deny earnings opportunities altogether, either for energy efficiency or for the broader array of functions associated with effective management of upgraded grids and diversified resource portfolios. Instead, utility business models should involve a sharing between utility customers and shareholders of long-term cost savings from an effectively managed and integrated portfolio of electricity and natural gas resources. The incentive should encourage diversified portfolios of long- and short-term investments, which insulate customers from excessive exposure to volatile spot markets. This requires reasonable, objective benchmarks against which portfolio performance can be measured, and consensus-based ways to evaluate that performance. An urgent and unresolved item on regulatory agendas involves fleshing out the concept of performance-based resource procurement and integration incentives, and devising specific proposals for utility regulators and managers to consider.

Some lessons are already clear from California’s experience from 2006–2008 with performance-based energy efficiency incentives, which earned utilities more than $200 million but exacted a high price in terms of adversarial struggles and uncertainty (even though the sum in question represented less than two percent of utility profits over that period). Of particular importance is the now widely acknowledged point that performance benchmarks, once established, should not be subject to change in the middle of program implementation. Much of California’s discord reflected efforts to make significant retroactive adjustments in such benchmarks, based on disputes over how much credit utilities should receive for undisputed installations of cost-effective measures. Prominent among those disputes, for example, were whether and how much to alter initial estimates of how many utility customers would have installed compact fluorescent light bulbs if utilities had done nothing to promote them.

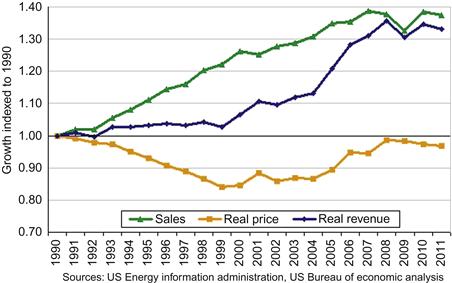

Even more important, it is past time to abandon ratemaking systems that rely on long- or short-term energy commodity rate caps as utilities’ principal incentive mechanism. These are still common worldwide; they would make sense only if society’s primary interest lay in minimizing commodity rates and maximizing sales, or if regulators thought it was practicable to achieve continuous reductions (or at worst a long-term freeze) in the delivered cost of kilowatt-hours and therms. Rate caps are flatly inconsistent with economic and environmental progress in a world of rising commodity costs, obvious infrastructure investment needs, and huge untapped energy efficiency opportunities that would raise commodity rates further by spreading fixed costs over smaller sales volumes, even though the energy efficiency improvements are overwhelmingly cost-effective (Figure 6.4).

Figure 6.4 Trends in Utilities’ Electricity Revenues, Sales, and Prices.20

[Cumulative growth in electric utilities’ real revenue (1990–2011) was about equal to growth in consumption. Both were up about a third (sales at 37 percent, and revenue at 33 percent). Real average prices per kWh are now about three percent less than they were in 1990, but with a clear rising trend since 1999.]

Instead, the principal aim of regulation should be to minimize the life-cycle costs of energy services. Utility managers themselves increasingly understand this and are emerging as advocates for change, which is among the best reasons for optimism about a prompt transition to a new business model. But success will require more engagement by all with a stake in reliable and affordable energy services.

4 Conclusions

Electricity and natural gas distribution no longer make sense as commodity businesses. No customer desires either fuel for its aesthetic qualities; it is reliable and affordable energy services that underpin healthy economies and improving standards of living. Everyone stands to benefit if utilities can help their customers find cost-effective strategies for getting more work out of less energy. At the same time, pressures are growing at all levels of society to reduce pollution emissions associated with fossil fuel use. If we were designing utility regulation for the first time, would anyone want to include potent rewards for promoting increased electricity and natural gas consumption? Yet that is the model to which most regulators and utilities remain tied, at least in part. Together, they now have an opportunity to invent the business anew, taking advantage of abundant experience in ways to chart a more productive course.

1Compare 2009 Statistical Abstract of the United States, p. l7 (Oct. 2008) (population) with U.S. Department of Energy, Energy Information Administration (May 2012) (electricity use).

2D. Moskovitz, Profits and Progress Through Least-Cost Planning (NARUC: November 1989), Appendix C.

3Ted Hesser’s chapter notes that 2007 marked a particularly pronounced shift in electricity consumption. A comparison of the Statistical Abstract of the United States (2012) with the Monthly Energy Review of the U.S. Department of Energy (May 2012) indicates that U.S. population growth from 2000–2010 was 10 percent; retail electricity sales grew by less than 9 percent from 2000–2011. Natural gas sales in the mid-2000 s were about the same as those in 1973, and subsequent increases are mostly attributable to shifts from coal to natural gas for electricity generation, which do not affect sales by gas distribution utilities.

4Electricity consumption data are from U.S. Energy Information Administration, Monthly Energy Review, Table 7.6, Electricity End Use, “Electricity End Use, Total” (June 27, 2012). Population data are from U.S. Census Bureau, Population Estimates, Table 1 – Annual Estimates of the Population for the United States, Regions, States, and Puerto Rico (December 2011).

5Matters are otherwise, of course, in places like China, France, and Russia, where national governments still routinely choose and finance electricity resources without any obvious reference to competitive considerations generally, or alternative energy efficiency opportunities in particular.

6The supplier in question is the Bonneville Power Administration, which sent out the quoted summary of its resource plan in a mass e-mail communication from John Taves, BPA Issues Final Resource Plan (Sept. 13, 2010).

7Sales and revenue data are from U.S. Energy Information Administration, Form EIA-826 Data Monthly Electric Utility Sales and Revenue Data, EIA-826 Sales and Revenue Spreadsheets (June 5, 2012). Revenues are presented in chained 2005 dollars. Nominal dollars of revenue were converted to chained dollars using U.S. Bureau of Economic Analysis, National Economic Accounts, Gross Domestic Product, Current-Dollar and "Real" GDP (June 28, 2012).

8For a full explanation and numerical illustrations, see R. Cavanagh, “Graphs, Words and Deeds,” MIT Innovations (Fall 2009), pp. 83–87.

9For more on the California PUC testimony that introduced revenue decoupling to the electricity sector in 1981, see R. Cavanagh, note 8 above, p. 89, n. 14.

10R. Cavanagh & J. Howat, “Finding Common Ground Between Environmental and Consumer Advocates,” ElectricityPolicy.com (April 2012).

11This is a reference to testimony at an April 2012 hearing before the Washington Utilities and Transportation Commission, which addressed a revenue decoupling proposal for Puget Sound Energy.

12LADWP, Power System Rate Proposal. FY 12/13 and FY 13/14, Summary and Supporting Information (May 3, 2012), p. 76. Publicly owned utilities often assume that their non-profit status and local control obviates the need for decoupling, overlooking the importance of assured fixed-cost recovery to financial ratings and the high transaction costs associated with formal rate adjustments in the absence of a pre-approved adjustment mechanism.

13An example is a settlement proposal approved by the Arizona Corporations Commission for Arizona Public Service (over strong objections from NRDC and the Southwest Energy Efficiency Project) in Docket No. E-01345A-11-0224 (May 2012).

14See, e.g., Arizona Corporations Commission, Docket No. G-01551A-10-0458, Decision No. 72723 (January 2012), pp. 39–40.

15For a compendium of precedents, see the website of the Edison Electric Institute’s Energy Efficiency Institute (http://www.edisonfoundation.net/iee). The key contrast between these mechanisms and the “lost revenue recovery” option criticized earlier is that the stakes per adjudicated unit of savings are much lower, which should ensure less discord and lower implementation costs.

16I first heard this characteristically vivid comparison from Tom Page, then CEO of San Diego Gas & Electric.

17Promising initial efforts have been launched by the Energy Foundation (under the leadership of former Colorado PSC Commissioners Ron Binz and Ron Lehr) and the Rocky Mountain Institute (where James Newcomb and Lena Hansen are heading a new Electricity Innovation Lab).

18Minnesota learned as much during the 1990 s, when the utility’s annual lost revenue recovery request reached levels comparable to its annual energy efficiency expenditures, and the Commission responded by terminating the recoveries. Minnesota Public Utilities Commission, Order Disallowing Recovery of Lost Margins and Other Incentives, Docket No. E-002/M-99-419 (July 27, 1999) (lost revenue request was $26.9 million, while program expenditures totaled $33.3 million). Duke Power’s widely publicized “Save-A-Watt” proposal attracted extensive opposition because of its reliance on generous payments to Duke for every kWh determined to have been saved through its programs; Duke opted recently in Ohio for revenue decoupling instead. Public Utility Commission of Ohio, Finding and Order, Case No. 5905-EL-RDR (May 30, 2012).

19The success of U.S. revenue decoupling mechanisms in avoiding appreciable rate impacts is documented thoroughly in Pamela Morgan, “Rate Impacts and Key Design Elements of Gas and Electric Utility Decoupling: A Comprehensive Review,” The Electricity Journal (October 2009).

20Sales, revenues, and price data are from U.S. Energy Information Administration, Form EIA-826 Data Monthly Electric Utility Sales and Revenue Data, EIA-826 Sales and Revenue Spreadsheets (June 5, 2012). Revenues and prices are presented in chained 2005 dollars. Nominal dollars of revenue were converted to chained dollars using U.S. Bureau of Economic Analysis, National Economic Accounts, Gross Domestic Product, Current-Dollar and "Real" GDP (June 28, 2012).