Earnings, Consumption and Life Cycle Choices*

Costas Meghir*, *Yale University, University College London, IFS and IZA

Luigi Pistaferri**, ** Stanford University, NBER, CEPR and IZA

Abstract

We discuss recent developments in the literature that studies how the dynamics of earnings and wages affect consumption choices over the life cycle. We start by analyzing the theoretical impact of income changes on consumption—highlighting the role of persistence, information, size and insurability of changes in economic resources. We next examine the empirical contributions, distinguishing between papers that use only income data and those that use both income and consumption data. The latter do this for two purposes. First, one can make explicit assumptions about the structure of credit and insurance markets and identify the income process or the information set of the individuals. Second, one can assume that the income process or the amount of information that consumers have are known and test the implications of the theory. In general there is an identification issue that has only recently being addressed with better data or better “experiments”. We conclude with a discussion of the literature that endogenizes people’s earnings and therefore change the nature of risk faced by households.

Keywords

Consumption; Risk; Income dynamics; Life cycle

1 Introduction

The objective of this chapter is to discuss recent developments in the literature that studies how the dynamics of earnings and wages affect consumption choices over the life cycle. Labor economists and macroeconomists are the main contributors to this area of research. A theme of interest for both labor economics and macroeconomics is to understand how much risk households face, to what extent risk affects basic household choices such as consumption, labor supply and human capital investments, and what types of risks matter in explaining behavior.1 These are questions that have a long history in economics.

A fruitful distinction is between ex-ante and ex-post household responses to risk. Ex-ante responses answer the question: “What do people do in the anticipation of shocks to their economic resources?”. Ex-post responses answer the question: “What do people do when they are actually hit by shocks to their economic resources?”. A classical example of ex-ante response is precautionary saving induced by uncertainty about future household income (see Kimball, 1990, for a modern theoretical treatment, and Carroll and Samwick, 1998, and Guiso et al., 1992, for empirical tests).2 An example of ex-post response is downward revision of consumption as a result of a negative income shock (see Hall and Mishkin, 1982; Heathcote et al., 2007). More broadly, ex-ante responses to risk may include:3 (a) precautionary labor supply, i.e., cutting the consumption of leisure rather than the consumption of goods (Low, 2005) (b) delaying the adjustment to the optimal stock of durable goods in models with fixed adjustment costs of the (S,s) variety (Bertola et al., 2005); (c) shifting the optimal asset allocation towards safer assets in asset pricing models with incomplete markets (Davis and Willen, 2000); (d) increasing the amount of insurance against formally insurable events (such as a fire in the home) when the risk of facing an independent, uninsurable event (such as a negative productivity shock) increases (known as “background risk” effects, see Gollier and Pratt, 1996, for theory and Guiso et al., 1996, for an empirical test); (e) and various forms of income smoothing activities, such as signing implicit contracts with employers that promise to keep wages constant in the face of variable labor productivity (see Azariadis, 1975 and Baily (1977), for a theoretical discussion and Guiso et al., 2005, for a recent test using matched employer-employee data), or even making occupational or educational choices that are associated with less volatile earnings profiles. Ex-post responses include: (a) running down assets or borrowing at high(er) cost (Sullivan, 2008); (b) selling durables (Browning and Crossley, 2003);4 (c) change (family) labor supply (at the intensive and extensive margin), including changing investment in the human capital of children (Attanasio et al., 2008; Beegle et al., 2004; Ginja, 2010); (d) using family networks, loans from friends, etc. (Hayashi et al., 1996; Angelucci et al., 2010); (e) relocating or migrating (presumably for lack of local job opportunities) or changing job (presumably because of increased firm risk) (Blanchard and Katz, 1992); (f) applying for government-provided insurance (see Gruber, 1997; Gruber and Yelowitz, 1999; Blundell and Pistaferri, 2003; Kniesner and Ziliak, 2002); (g) using charities (Dehejia et al., 2007).

Ex-ante and ex-post responses are clearly governed by the same underlying forces. The ex-post impact of an income shock on consumption is much attenuated if consumers have access to sources of insurance (both self-insurance and outside insurance) allowing them to smooth intertemporally their marginal utility. Similarly, ex-ante responses may be amplified by the expectation of borrowing constraints (which limit the ability to smooth ex-post temporary fluctuations in income). Thus, the structure of credit and insurance markets and the nature of the income process, including the persistence and the volatility of shocks as well as the sources of risk, underlie both the ex-ante and the ex-post responses.

Understanding how much risk and what types of risks people face is important for a number of reasons. First, the list of possible behavioral responses given above suggests that fluctuations in microeconomic uncertainty can generate important fluctuations in aggregate savings, consumption, and growth.5 The importance of risk and of its measurement is well captured in the following quote from Browning et al. (1999):

“in order to...quantify the impact of the precautionary motive for savings on both the aggregate capital stock and the equilibrium interest rate...analysts require a measure of the magnitude of microeconomic uncertainty, and how that uncertainty evolves over the business cycle”.

Another reason to care about risk is for its policy implications. Most of the labor market risks we will study (such as risk of unemployment, of becoming disabled, and generally of low productivity on the job due to health, employer mismatch, etc.) have negative effects on people’s welfare and hence there would in principle be a demand for insurance against them. However, these risks are subject to important adverse selection and moral hazard issues. For example, individuals who were fully insured against the event of unemployment would have little incentive to exert effort on the job. Moreover, even if informational asymmetries could be overcome, enforcement of insurance contracts would be at best limited. For these reasons, we typically do not observe the emergence of a private market for insuring productivity or unemployment risks. As in many cases of market failure, the burden of insuring individuals against these risks is taken on (at least in part) by the government. A classical normative question is: How should government insurance programs be optimally designed? The answer depends partly on the amount and characteristics of risks being insured. To give an example, welfare reform that make admission into social insurance programs more stringent (as heavily discussed in the Disability Insurance literature) reduce disincentives to work or apply when not eligible, but also curtails insurance to the truly eligible (Low and Pistaferri, 2010). To be able to assess the importance of the latter problem is crucial to know how much smoothing is achieved by individuals on their own and how large disability risk is. A broader issue is whether the government should step in to provide insurance against “initial conditions”, such as the risk of being born to bad parents or that of growing up in bad neighborhoods.

Finally, the impact of shocks on behavior also matters for the purposes of understanding the likely effectiveness of stabilization or “stimulus” policies, another classical question in economics. As we shall see, the modern theory of intertemporal consumption draws a sharp distinction between income changes that are anticipated and those that are not (i.e., shocks); it also highlights that consumption should respond more strongly to persistent shocks vis-a-vis shocks that do not last long. Hence, the standard model predicts that consumption may be affected immediately by the announcement of persistent tax reforms to occur at some point in the future. Consumption will not change at the time the reform is actually implemented because there are no news in a plan that is implemented as expected. The model also predicts that consumption is substantially affected by a surprise permanent tax reform that happens today. What allows people to disconnect their consumption from the vagaries of their incomes is the ability to transfer resources across periods by borrowing or putting money aside. Naturally, the possibility of liquidity constraints makes these predictions much less sharp. For example, consumers who are liquidity constrained will not be able to change their consumption at the time of the announcement of a permanent tax change, but only at the time of the actual passing of the reform (this is sometimes termed excess sensitivity of consumption to predicted income changes). Moreover, even an unexpected tax reform that is transitory in nature may induce large consumption responses.

These are all ex-post response considerations. As far as ex-ante responses are concerned, uncertainty about future income realizations or policy uncertainty itself will also impact consumption. The response of consumers to an increase in risk is to reduce consumption—or increase savings. This opens up another path for stabilization policies. For example, if the policy objective is to stimulate consumption, one way of achieving this would be to reduce the amount of risk that people face (such as making firing more costly to firms, etc.) or credibly committing to policy stability. All these issues are further complicated when viewed from a General Equilibrium perspective: a usual example is that stabilization policies are accompanied by increases in future taxation, which consumers may anticipate.

Knowing the stochastic structure of income has relevance besides its role for explaining consumption fluctuations, as important as they may be. Consider the rise in wage and earnings inequality that has taken place in many economies over the last 30 years (especially in the US and in the UK). This poses a number of questions: Does the rise in inequality translate into an increase in the extent of risk that people face? There is much discussion in the press and policy circles about the possibility that idiosyncratic risk has been increasing and that it has been progressively shifted from firms and governments onto workers (one of t-cited example is the move from defined benefit pensions, where firms bear the risk of underperforming stock markets, to defined contribution pensions, where workers do).6 This shift has happened despite the “great moderation” taking place at the aggregate level. Another important issue to consider is whether the rise in inequality is a permanent or a more temporary phenomenon, because a policy intervention aimed at reducing the latter (such as income maintenance policies) differs radically from a policy intervention aimed at reducing the former (training programs, etc.). A permanent rise in income inequality is a change in the wage structure due to, for example, skill-biased technological change that permanently increases the returns to observed (schooling) and unobserved (ability) skills. A transitory rise in inequality is sometimes termed “wage instability”.7

The rest of the chapter is organized as follows. We start off in Section 2 with a discussion of what the theory predicts regarding the impact of changes in economic resources on consumption. As we shall see, the theory distinguishes quite sharply between persistent and transient changes, anticipated and unanticipated changes, insurable and uninsurable changes, and—if consumption is subject to adjustment costs— between small and large changes.

Given the importance of the nature of income changes for predicting consumption behavior, we then move in Section 3 to a review of the literature that has tried to come up with measures of wage or earnings risk using univariate data on wages, earnings or income. The objective of these papers has been that of identifying the most appropriate characterization of the income process in a parsimonious way. We discuss the modeling procedure and the evidence supporting the various models. Most papers make no distinction between unconditional and conditional variance of shocks.8 Others assume that earnings are exogenous. More recent papers have relaxed both assumptions. We also discuss in this section papers that have taken a more statistical path, while retaining the exogeneity assumption, and modeled in various way the dynamics and heterogeneity of risk faced by individuals. We later discuss papers that have explored the possibility of endogenizing risk by including labor supply decisions, human capital (or health) investment decisions, or job-to-job mobility decisions. We confine this discussion to the end of the chapter (Section 5) because this approach is considerably more challenging and in our view represents the most promising development of the literature to date.

In Section 4 we discuss papers that use consumption and income data jointly. Our reading is that they do so with two different (and contrasting) objectives. Some papers assume that the life cycle-permanent income hypothesis provides a correct description of consumer behavior and use the extra information available to either identify the “correct” income process faced by individuals (which is valuable given the difficulty of doing so statistically using just income data) or identify the amount of information people have about their future income changes. The idea is that even if the correct income process could be identified, there would be no guarantee that the estimated “unexplained” variability in earnings represents “true” risk as seen from the individual standpoint (the excess variability represented by measurement error being the most trivial example). Since risk “is in the eye of the beholder”, some researchers have noticed that consumption would reflect whatever amount of information (and, in the first case, whatever income process) people face. We discuss papers that have taken the route of using consumption and income data to extract information about risk faced (or perceived) by individuals, such as Blundell and Preston (1998), Guvenen (2007), Guvenen and Smith (2009), Heathcote et al. (2007), Cunha et al. (2005), and Primiceri and van Rens (2009). Other papers in this literature use consumption and income data jointly in a more traditional way: they assume that the income process is correct and that the individual has no better information than the econometrician and proceed to test the empirical implications of the theory, e.g., how smooth is consumption relative to income. Hall and Mishkin (1982) and Blundell et al. (2008b) are two examples. In general there is an identification issue: one cannot separately identify insurance and information. We discuss two possible solutions proposed in the literature. First, identification of episodes in which shocks are unanticipated and of known duration (e.g., unexpected transitory tax refunds or other payments from the government, or weather shocks). If the assumptions about information and duration hold, all that remains is “insurability”. Second, we discuss the use of subjective expectations to extract information about future income. These need to be combined with consumption and realized income data to identify insurance and durability of shocks.9 The chapter concludes with a discussion of future research directions in Section 6.

2 The impact of income changes on consumption: some theory

In this section we discuss what theory has to say regarding the impact of income changes on consumption.

2.1 The life cycle-permanent income hypothesis

To see how the degree of persistence of income shocks and the nature of income changes affect consumption, consider a simple example in which income is the only source of uncertainty of the model.10 Preferences are quadratic, consumers discount the future at rate ![]() and save on a single risk-free asset with deterministic real return r, β(1 + r) = 1 (this precludes saving due to returns outweighing impatience), the horizon is finite (the consumer dies with certainty at age A and has no bequest motive for saving), and credit markets are perfect. As we shall see, quadratic preferences are in some ways quite restrictive. Nevertheless, this simple characterization is very useful because it provides the correct qualitative intuition for most of the effects of interest; this intuition carries over with minor modifications to the more sophisticated cases. In the quadratic preferences case, the change in household consumption can be written as

and save on a single risk-free asset with deterministic real return r, β(1 + r) = 1 (this precludes saving due to returns outweighing impatience), the horizon is finite (the consumer dies with certainty at age A and has no bequest motive for saving), and credit markets are perfect. As we shall see, quadratic preferences are in some ways quite restrictive. Nevertheless, this simple characterization is very useful because it provides the correct qualitative intuition for most of the effects of interest; this intuition carries over with minor modifications to the more sophisticated cases. In the quadratic preferences case, the change in household consumption can be written as

(1)

(1)

where a indexes age and t time, ![]() is an “annuity” parameter that increases with age and Ωi,a,t is the consumer’s information set at age a. Despite its simplicity, this expression is rich enough to identify three key issues regarding the response of consumption to changes in the economic resources of the household.

is an “annuity” parameter that increases with age and Ωi,a,t is the consumer’s information set at age a. Despite its simplicity, this expression is rich enough to identify three key issues regarding the response of consumption to changes in the economic resources of the household.

First, consumption responds to news in the income process, but not to expected changes. Only innovations to (current and future) income that arrive at age a (the term E(Yi,a+j,t+j|Ωi,a,t) − E(Yi,a+j,t +j|&i,a−1,t−1)) have the potential to change consumption between age a − 1 and age a. Anticipated changes in income (for which there is no innovation) do not affect consumption. Assistant Professors promoted in February may rent a larger apartment immediately, in the anticipation of the higher salary starting in September. We will record an increase in consumption in February (when the income change is announced), but not in September (when the income change actually occurs). This is predicated on the assumption that consumers can transfer resources from the future to the present by, e.g., borrowing. In the example above, a liquidity constrained Assistant Professor will not change her (rent) consumption at the time of the announcement of a promotion, but only at the time of the actual salary increase. With perfect credit markets, however, the model predicts that anticipated changes do affect consumption when they are announced. In terms of stabilization policies, this means that two types of income changes will affect consumption. First, consumption may be affected immediately by the announcement of tax reforms to occur at some point in the future. Consumption will not change at the time the reform is actually implemented. Second, consumption may be affected by a surprise tax reform that happens today.

The second key issue emerging from Eq. (1) is that the life cycle horizon also plays an important role (the term πα). A transitory innovation smoothed over 40 years has a smaller impact on consumption than the same transitory innovation to be smoothed over 10 years. For example, if one assumes that the income process is i.i.d., the marginal propensity to consume with respect to an income change from (1) is simply πα. Assuming r = 0.02, the marginal propensity to consume out of income shock increases from 0.04 (when A − α = 40) to 0.17 (when A − α = 5), and it is 1 in the last period of life. Intuitively, at the end of the life cycle transitory shocks would look, effectively, like permanent shocks. With liquidity constraints, however, shocks may have similar effects on consumption independently of the age at which they are received.

The last key feature of Eq. (1) is the persistence of innovations. More persistent innovations have a larger impact than short-lived innovations. To give a more formalcharacterization of the importance of persistence, suppose that income follows an ARMA(1,1) process:

![]() (2)

(2)

In this case, substituting (2) in (1), the consumption response is given by

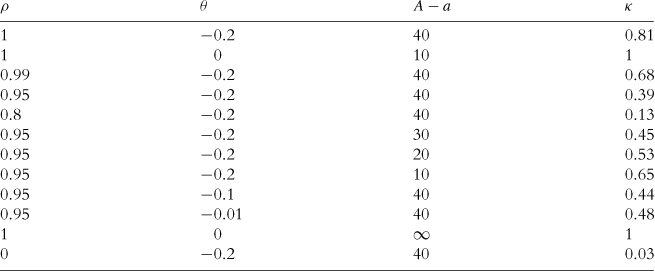

Table 1 below shows the value of the marginal propensity to consume κ for various combinations of ρ, θ, and A − a (setting r = 0.02). A number of facts emerge. If the income shock represents an innovation to a random walk process (ρ = 1, θ = 0), consumption responds one-to-one to it regardless of the horizon (the response is attenuated only if shocks end after some period, say L < A).11 A decrease in the persistence of the shock lowers the value of κ. When ρ = 0.8 (and θ = −0.2), for example, the value of κ is a modest 0.13. A decrease in the persistence of the MA component acts in the same direction (but the magnitude of the response is much attenuated). In this case as well, the presence of liquidity constraints may invalidate the sharp prediction of the model. For example, more and less persistent shocks may have a similar effect on consumption. When the consumer is hit by a short-lived negative shock, she can smooth the consumption response over the entire horizon by borrowing today (and repaying in the future when income reverts to the mean). If borrowing is precluded, short-lived or long-lived shocks have similar impacts on consumption.

The income process (2) considered above is restrictive, because there is a single error component which follows an ARMA(1,1) process. As we discuss in Section 3, a very popular characterization in calibrated macroeconomic models is to assume that income is the sum of a random walk process and a transitory i.i.d. component:

![]() (3)

(3)

![]() (4)

(4)

The appeal of this income process is that it is close to the notion of a Friedman’s permanent income hypothesis income process.12 In this case, the response of consumption to the two types of shocks is:

![]() (5)

(5)

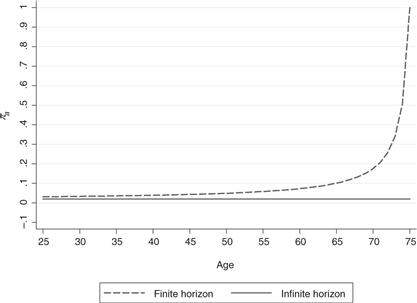

which shows that consumption responds one-to-one to permanent shocks but the response of consumption to a transitory shock depends on the time horizon. For young consumers (with a long time horizon), the response should be small. The response should increase as consumers age. Figure 1 plots the value of the response for a consumer who lives until age 75. Clearly, it is only in the last 10 years of life or so that there is a substantial response of consumption to a transitory shock. The graph also plots for the purpose of comparison the expected response in the infinite horizon case. An interesting implication of this graph is that a transitory unanticipated stabilization policy is likely to affect substantially only the behavior of older consumers (unless liquidity constraints are important—which may well be the case for younger consumers).13

Note finally that if the permanent component were literally permanent (pi,a,t = pi), it would affect the level of consumption but not its change (unless consumers were learning about pi, see Guvenen, 2007).

In the classical version of the LC-PIH the size of income changes does not matter. One reason why the size of income changes may matter is because of adjustment costs: Consumers tend to smooth consumption and follow the theory when expected income changes are large, but are less likely to do so when the changes are small and the costs of adjusting consumption are not trivial. Suppose for example that consumers who want to adjust their consumption upwards in response to an expected income increase need to face the cost of negotiating a loan with a bank. It is likely that the utility loss from not adjusting fully to the new equilibrium is relatively small when the expected income increase is small, which suggests that no adjustment would take place if the transaction cost associated with negotiating a loan is high enough.14 This “magnitude hypothesis” has been formally tested by Scholnick (2010), who use a large data set provided by a Canadian bank that includes information on both credit cards spending as well as mortgage payment records. As in Stephens (2008) he argues that the final mortgage payment represent an expected shock to disposable income (that is, income net of pre-committed debt service payments). His test of the magnitude hypothesis looks at whether the response of consumption to expected income increases depends on the relative amount of mortgage payments. See also Chetty and Szeidl (2007).15

Outside the quadratic preference world, uncertainty about future income realizations will also impact consumption. The response of consumers to an increase in risk is to reduce consumption—or increase savings. This opens up another path for stabilization policies. If the policy objective is to stimulate consumption, one way of achieving this would be to reduce the risk that people face. We consider more realistic preference specifications in the following section.

2.2 Beyond the pih

The beauty of the model with quadratic preferences is that it gives very sharp predictions regarding the impact on consumption of various types of income shocks. For example, there is the sharp prediction that permanent shocks are entirely consumed (an MPC of 1). Unfortunately, quadratic preferences have well known undesirable features, such as increasing risk aversion and lack of a precautionary motive for saving. Do the predictions of this model survive under more realistic assumptions about preferences? The answer is: only qualitatively. The problem with more realistic preferences, such as CRRA, is that they deliver no closed form solution for consumption—that is, there is no analytical expression for the “consumption function” and hence the value of the propensity to consume in response to risk (income shocks) is not easily derivable. This is also the reason why the literature moved on to estimating Euler equations after Hall (1978). The advantage of the Euler equation approach is that one can be silent about the sources of uncertainty faced by the consumer (including, crucially, the stochastic structure of the income process). However, in the Euler equation context only a limited set of parameters (preference parameters such as the elasticity of intertemporal substitution or the intertemporal discount rate) can be estimated.16 Our reading is that there is some dissatisfaction in the literature regarding the evidence coming from Euler equation estimates (see Browning and Lusardi, 1996; Attanasio and Weber, 2010).

Recently there has been an attempt to go back to the concept of a “consumption function”. Two approaches have been followed. First, the Euler equation that describe the expected dynamics of the growth in the marginal utility can be approximated to describe the dynamics of consumption growth. Blundell et al. (2008b), extending Blundell and Preston (1998) (see also Blundell and Stoker, 1994), derive an approximation of the mapping between the expectation error of the Euler equation and the income shock. Carroll (2001) and Kaplan and Violante (2009) discuss numerical simulations in the buffer-stock and Bewley model, respectively. We discuss the results of these two approaches in turn.

2.2.1 Approximation of the Euler equation

Blundell et al. (2008b) consider the consumption problem faced by household i of age a in period t. Assuming that preferences are of the CRRA form, the objective is to choose a path for consumption C so as to:

(6)

(6)

where Zi,a+j,t+j incorporates taste shifters (such as age, household composition, etc.), and we denote with Ea (.) = E(.|Ωi,a,t). Maximization of (6) is subject to the budget constraint, which in the self-insurance model assumes individuals have access to a risk free bond with real return r

![]() (7)

(7)

![]() (8)

(8)

with Ai,a,t given. Blundell et al. (2008b) set the retirement age after which labor income falls to zero at L, assumed known and certain, and the end of the life cycle at age A. They assume that there is no uncertainty about the date of death. With budget constraint (7), optimal consumption choices can be described by the Euler equation (assuming for simplicity that there is no preference heterogeneity, or υa = 0):

![]() (9)

(9)

As it is, Eq. (9) is not useful for empirical purposes. Blundell et al. (2008b) show that the Euler equation can be approximated as follows:

![]()

where ηi,a,t is a consumption shock with Ea−1(ηi,a,t) = 0, ![]() captures any slope in the consumption path due to interest rates, impatience or precautionary savings and the error in the approximation is

captures any slope in the consumption path due to interest rates, impatience or precautionary savings and the error in the approximation is ![]() .17 Suppose that any idiosyncratic component to this gradient to the consumption path can be adequately picked up by a vector of deterministic characteristics

.17 Suppose that any idiosyncratic component to this gradient to the consumption path can be adequately picked up by a vector of deterministic characteristics ![]() and a stochastic individual element ηi,a

and a stochastic individual element ηi,a

![]()

Assume log income is

![]() (10)

(10)

![]() (11)

(11)

where ![]() represent observable characteristics influencing the growth of income. Income growth can be written as:

represent observable characteristics influencing the growth of income. Income growth can be written as:

![]()

The (ex-post) intertemporal budget constraint is

where A is the age of death and L is the retirement age. Applying the approximation above and taking differences in expectations gives

![]()

where πa is an annuitization factor,  is the share of future labor income in current human and financial wealth, and the error of the approximation is

is the share of future labor income in current human and financial wealth, and the error of the approximation is ![]() . Then18

. Then18

![]() (12)

(12)

with a similar order of approximation error.19 The random term Ξi,a,t can be interpreted as the innovation to higher moments of the income process.20 As we shall see, Meghir and Pistaferri (2004) find evidence of this using PSID data.

The interpretation of the impact of income shocks on consumption growth in the PIH model with CRRA preferences is straightforward. For individuals a long time from the end of their life with the value of current financial assets small relative to remaining future labor income, ![]() , and permanent shocks pass through more or less completely into consumption whereas transitory shocks are (almost) completely insured against through saving. Precautionary saving can provide effective self-insurance against permanent shocks only if the stock of assets built up is large relative to future labor income, which is to say Ξi,a,t is appreciably smaller than unity, in which case there will also be some smoothing of permanent shocks through self-insurance.

, and permanent shocks pass through more or less completely into consumption whereas transitory shocks are (almost) completely insured against through saving. Precautionary saving can provide effective self-insurance against permanent shocks only if the stock of assets built up is large relative to future labor income, which is to say Ξi,a,t is appreciably smaller than unity, in which case there will also be some smoothing of permanent shocks through self-insurance.

The most important feature of the approximation approach is to show that the effect of an income shock on consumption depends not only on the persistence of the shock and the planning horizon (as in the LC-PIH case with quadratic preferences), but also on preference parameters. Ceteris paribus, the consumption of more prudent households will respond less to income shocks. The reason is that they can use their accumulated stock of precautionary wealth to smooth the impact of the shocks (for which they were saving precautiously against in the first place). Simulation results (below) confirm this basic intuition.

2.2.2 Kaplan and Violante

Kaplan and Violante (2009) investigate the amount of consumption insurance present in a life cycle version of the standard incomplete markets model with heterogenous agents (e.g., Rios-Rull, 1996; Huggett, 1996). Kaplan and Violante’s setup differs from that in Blundell et al. (2008b; BPP) by adding the uncertainty component μα to life expectancy, and by omitting the taste shifters from the utility function. μα is the probability of dying at age a. It is set to 0 for all a < L (the known retirement age) and it is greater than 0 for L ≤ a ≤ A. Their model also differs from BPP by specifying a realistic social security system. Two baseline setups are investigated—a natural borrowing constraint setup (henceforth NBC), in which consumers are only constrained by their budget constraint, and a zero borrowing constraint setup (henceforth ZBC), in which consumers have to maintain non-negative assets at all ages. The income process is similar to BPP.21 Part of Kaplan and Violante’s analysis is designed to check whether the amount of insurance predicted by the Bewley model can be consistently estimated using the identification strategy proposed by BPP and whether BPP’s estimates using PSID and CEX data conform to values obtained from calibrating their theoretical model.

Kaplan and Violante (2009) calibrate their model to match the US data. Survival rates are obtained from the NCHS, the intertemporal discount rate is calibrated to match a wealth-income ratio of 2.5, the permanent shock parameters ![]() and the variance of the initial draw of the process) are calibrated to match PSID data and the variance of the transitory shock

and the variance of the initial draw of the process) are calibrated to match PSID data and the variance of the transitory shock ![]() is set to the 1990–1992 BPP point estimate (0.05). The Kaplan and Violante (2009) model is solved numerically. This allows for the calculation of both the “true”22 and the BPP estimators of the “partial insurance parameters” (the response of consumption to permanent and transitory income shocks).

is set to the 1990–1992 BPP point estimate (0.05). The Kaplan and Violante (2009) model is solved numerically. This allows for the calculation of both the “true”22 and the BPP estimators of the “partial insurance parameters” (the response of consumption to permanent and transitory income shocks).

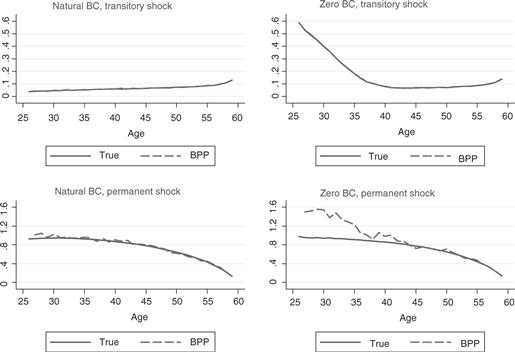

Figure 2 is reproduced from Kaplan and Violante (2009).23 It plots the theoretical marginal propensity to consume for the transitory shocks (upper panels) and the permanent shocks (lower panels) against age (continuous line) and those obtained using BPP’s identification methodology (dashed line). The left panels refer to the NBC environment; the right panels to the ZBC environment. A number of interesting findings emerge. First, in the NBC environment the MPC with respect to transitory shocks is fairly low throughout the life cycle, and similarly to what is shown in Fig. 1, increases over the life cycle due to reduced planning horizon effect. The life cycle average MPC is 0.06. Second, there is considerable insurance also against permanent shock, which increases over the life cycle due to the ability to use the accumulated wealth to smooth these shocks. The life cycle average MPC is 0.77, well below the MPC of 1 predicted by the infinite horizon PIH model.24 Third, the ZBC environment affects only the ability to insure transitory shocks (which depend on having access to loans), but not the ability to insure permanent shocks (which depend on having access to a storage technology, and hence it is not affected by credit restrictions). Fourth, the performance of the BPP estimators is remarkably good. Only in the case of the ZBC environment and a permanent shock does the BPP estimator display an upward bias, and even in that case only very early in the life cycle. According to KV the source of the bias is the failure of the orthogonality condition used by BPP for agents close to the borrowing constraint. It is worth noting that the ZBC environment is somewhat extreme as it assumes no unsecured borrowing. Finally, KV compare the average MPCs obtained in their model (0.06 and 0.77) with the actual estimates obtained by BPP using actual data. As we shall see, BPP find an estimate of the MPC with respect to permanent shocks of 0.64 (s.e. 0.09) and an estimate of the MPC with respect to transitory shocks of 0.05 (s.e. 0.04). Clearly, the “theoretical” MPCs found by KV lie well in the confidence interval of BPP’s estimates. One thing that seems not to be borne out in the data is that theoretically the degree of smoothing of permanent shocks should be strictly increasing and convex with age, while BPP report an increasing amount of insurance with age as a non-significant finding.25 As discussed by Kaplan and Violante (2009), the theoretical pattern of the smoothing coefficients is the result of two forces: a wealth composition effect and a horizon effect. The increase in wealth over the life cycle due to precautionary and retirement motives means that agents are better insured against shocks. As the horizon shortens, the effect of permanent shock resembles increasingly that of a transitory shock.

Figure 2 Age profile of MPC coefficients for transitory and permanent income shocks. Kaplan and Violante (2009)

Given that the response of consumption to shocks of various nature is so different (and so relevant for policy in theory and practice), it is natural to turn to studies that analyze the nature and persistence of the income process.

3 Modeling the income process

In this section we discuss the specification and estimation of the income process. Two main approaches will be discussed. The first looks at earnings as a whole, and interprets risk as the year-to-year volatility that cannot be explained by certain observables (with various degrees of sophistication). The second approach assumes that part of the variability in earnings is endogenous (induced by choices). In the first approach, researchers assume that consumers receive an uncertain but exogenous flow of earnings in each period. This literature has two objectives: (a) identification of the correct process for earnings, (b) identification of the information set—which defines the concept of an “innovation”. In the second approach, the concept of risk needs revisiting, because one first needs to identify the “primitive” risk factors. For example, if endogenous fluctuations in earnings were to come exclusively from people freely choosing their hours, the “primitive” risk factor would be the hourly wage. We will discuss this second approach at the end of the chapter, in Section 5.

There are various models proposed in the literature aimed at addressing the issue of how to model risk in exogenous earnings. They typically model earnings as the sum of a number of random components. These components differ in a number of respects, primarily their persistence, whether there are time- (or age- or experience-) varying loading factors attached to them, and whether they are economically relevant or just measurement error. We discuss these various models in Section 3.1. As said in the Introduction, to have an idea about the correct income process is key to understanding the response of consumption to income shocks.26 As for the issue of information set, the question that is being asked is whether the consumer knows more than the econometrician.27 This is sometimes known as the superior information issue. The individual may have advance information about events such as a promotion, that the econometrician may never hope to predict on the basis of observables (unless, of course, promotions are perfectly predictable on the basis of things like seniority within a firm, education, etc.).28

In general, a researcher’s identification strategy for the correct DGP for income, earnings or wages will be affected by data availability. While the ideal data set is a long, large panel of individuals, this is somewhat a rare event and can be plagued by problems such as attrition (see Baker and Solon, 2003, for an exception). More frequently, researchers have available panel data on individuals, but the sample size is limited, especially if one restricts the attention to a balanced sample (for example, Baker, 1997; MaCurdy, 1982). Alternatively, one could use an unbalanced panel (as in Meghir and Pistaferri, 2004; Heathcote et al., 2007). An important exception is the case where countries have available administrative data sources with reports on earnings or income from tax returns or social security records. The important advantage of such data sets is the accuracy of the information provided and the lack of attrition, other than what is due to migration and death. The important disadvantage is the lack of other information that is pertinent to modeling, such as hours of work and in some cases education or occupation, depending on the source of the data. Even less frequently, one may have available employer-employee matched data sets, with which it may be possible to identify the role of firm heterogeneity separately from that of individual heterogeneity, either in a descriptive way such as in Abowd et al. (1999), or allowing also for shocks, such as in Guiso et al. (2005), or in a more structural fashion as in Postel-Vinay and Robin (2002), Cahuc et al. (2006), Postel-Vinay and Turon (2010) and Lise et al. (2009). Less frequent and more limited in scope is the use of pseudo-panel data, which misses the variability induced by genuine idiosyncratic shocks, but at least allows for some results to be established where long panel data is not available (see Banks et al., 2001; Moffitt, 1993).

3.1 Specifications

The typical specification of income processes found in the literature is implicitly or explicitly motivated by Friedman’s permanent income hypothesis, which has led to an emphasis on the distinction between permanent and transitory shocks to income. Of course things are never as simple as that: permanent shocks may not be as permanent and transitory shocks may be reasonably persistent. Finally, what may pass as a permanent shock may sometimes be heterogeneity in disguise. Indeed these issues fuel a lively debate in this field, which may not be possible to resolve without identifying assumptions. In this section we present a reasonably general specification that encompasses a number of views in the literature and then discuss estimation of this model.

We denote by Yi,a,t a measure of income (such as earnings) for individual i of age a in period t. This is typically taken to be annual earnings and individuals not working over a whole year are usually dropped.29 Issues having to do with selection and endogenous labor supply decisions will be dealt with in a separate section. Many of the specifications for the income process take the form

![]() (13)

(13)

In the above e denotes a particular group (such as education and sex) and Xi,a,t will typically include a polynomial in age as well as other characteristics including region, race and sometimes marital status. From now on we omit the superscript “e” to simplify notation. In (13) the error term ui,a,t is defined such that E(ui,a,t|Xi,a,t) = 0. This allows us to work with residual log income ![]() , where

, where ![]() and the aggregate time effects

and the aggregate time effects ![]() can be estimated using OLS. Henceforth we will ignore this first step and we will work directly with residual log income yi,a,t, where the effect of observable characteristics and common aggregate time trends have been eliminated.

can be estimated using OLS. Henceforth we will ignore this first step and we will work directly with residual log income yi,a,t, where the effect of observable characteristics and common aggregate time trends have been eliminated.

The key element of the specification in (13) is the time series properties of ui,a,t. A specification that encompasses many of the ideas in the literature is

(14)

(14)

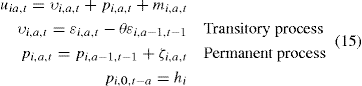

where L is a lag operator such that Lzi,a,t = Zi,a−1,t−1. In (14) the stochastic process consists of an individual specific life cycle trend (a × fi); a transitory shock υi,a,t, which is modeled as an MA process whose lag polynomial of order q is denoted ©q(L); a permanent shock Pp(L)pi,a,t = ζi,a,t, which is an autoregressive process with high levels of persistence possibly including a unit root, also expressed in the lag polynomial of order p, Pp (L); and measurement error mi,a,t which maybe taken as classical i.i.d. or not.

3.1.1 A simple model of earnings dynamics

We start with the relatively simpler representation where the term a × fi is excluded. Moreover we restrict the lag polynomials ©(L) and P(L): it is not generally possible to identify ©(L) and P(L) without any further restrictions. Thus we start with the typical specification used for example in MaCurdy (1982) and Abowd and Card (1989):

(15)

(15)

with mi,a,t, ζi,a,t and εεi,a,t all being independently and identically distributed and where hi reflects initial heterogeneity, which here persists forever through the random walk (a = 0 is the age of entry in the labor market, which may differ across groups due to different school leaving ages). Generally, as we will show, the existence of classical measurement error causes problems in the identification of the transitory shock process.

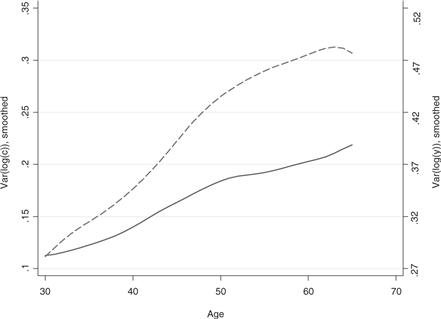

There are two principal motivations for the permanent/transitory decompositions: the first motivation draws from economics: the decomposition reflects well the original insights of Friedman (1957) by distinguishing how consumption can react to different types of income shock, while introducing uncertainty into the model.30 The second is statistical: At least for the US and for the UK the variance of income increases over the life cycle (see Fig. 3, which uses consumption data from the CEX and income data from the PSID). This, together with the increasing life cycle variance of consumption points to a unit root in income, as we shall see below. Moreover, income growth (Δyi,a,t) has limited serial correlation and behaves very much like an MA process of order 2 or three: this property is delivered by the fact that all shocks above are assumed i.i.d. In our example growth in income has been restricted to an MA(2).31

Figure 3 The variance of log income (from the PSID, dashed line) and log consumption (from the CEX, continuous line) over the life cycle.

Even in such a tight specification identification is not straightforward: as we will illustrate we cannot separately identify the parameter θ, the variance of the measurement error and the variance of the transitory shock. But first consider the identification of the variance of the permanent shock. Define unexplained earnings growth as:

![]() (16)

(16)

Then the key moment condition for identifying the variance of the permanent shock is

(17)

(17)

where q is the order of the moving average process in the original levels equation; in our example q = 1. Hence, if we know the order of serial correlation of log income we can identify the variance of the permanent shock without any need to identify the variance of the measurement error or the parameters of the MA process. Indeed, in the absence of a permanent shock the moment in (17) will be zero, which offers a way of testing for the presence of a permanent component conditional on knowing the order of the MA process. If the order of the MA process is one in the levels, then to implement this we will need at least six individual-level observations to construct this moment. The moment is then averaged over individuals and the relevant asymptotic theory for inference is one that relies on a large number of individuals N.

At this point we need to mention two potential complications with the econometrics. First, when carrying out inference we have to take into account that yi,a,t has been constructed using the pre-estimated parameters dt and β in Eq. (13). Correcting the standard errors for this generated regressor problem is relatively simple to do and can be done either analytically, based on the delta method, or just by using the bootstrap. Second, as said above, to estimate such a model we may have to rely on panel data where individuals have been followed for the necessary minimum number of periods/years (6 in our example); this means that our results may be biased due to endogenous attrition. In practice any adjustment for this is going to be extremely hard to do because we usually do not observe variables that can adequately explain attrition and at the same time do not explain earnings. Administrative data may offer a promising alternative to relying on attrition-prone panel data.

The order of the MA process for υi,a,t will not be known in practice and it has to be estimated. This can be done by estimating the autocovariance structure of gi,a,t and deciding a priori on the suitable criterion for judging whether they should be taken as zero. One approach followed in practice is to use the t-statistic or the F-statistics for higher order autocovariances. However, we need to recognize that given an estimate of q the analysis that follows is conditional on that estimate of q, which in turn can affect inference, particularly for the importance of the variance of the permanent effect ![]() .

.

3.1.2 Estimating and identifying the properties of the transitory shock

The next issue is the identification of the parameters of the moving average process of the transitory shock and those of measurement error. It turns out that the model is underidentified, which is not surprising: in our example we need to estimate three parameters, namely the variance of the transitory shock ![]() , the MA coefficient θ and the variance of the measurement error

, the MA coefficient θ and the variance of the measurement error ![]() .32 To illustrate the underidentification point suppose that |θ| < 1 and assume that the measurement error is independently and identically distributed. We take as given that q = 1. Then the autocovariances of order higher than three will be zero, whatever the value of our unknown parameters, which is the root of the identification problem. The first and second order autocovariances imply

.32 To illustrate the underidentification point suppose that |θ| < 1 and assume that the measurement error is independently and identically distributed. We take as given that q = 1. Then the autocovariances of order higher than three will be zero, whatever the value of our unknown parameters, which is the root of the identification problem. The first and second order autocovariances imply

(18)

(18)

The sign of E(gi,a,tgi,a–2,t−2) defines the sign of θ. Taking the two variances as functions of the MA coefficient we note two points. First, ![]() declines and

declines and ![]() increases when θ declines in absolute value. Second, for sufficiently low values of |θ| the estimated variance of the measurement error

increases when θ declines in absolute value. Second, for sufficiently low values of |θ| the estimated variance of the measurement error ![]() may become negative. Given the sign of θ (defined by I in Eq. (18)) this fact defines a bound for the MA coefficient. Suppose for example that θ < 0, we have that

may become negative. Given the sign of θ (defined by I in Eq. (18)) this fact defines a bound for the MA coefficient. Suppose for example that θ < 0, we have that ![]() , where

, where ![]() is the negative value of θ that sets

is the negative value of θ that sets ![]() in (18) to zero. If θ was found to be positive the bounds would be in a positive range. The bounds on θ in turn define bounds on

in (18) to zero. If θ was found to be positive the bounds would be in a positive range. The bounds on θ in turn define bounds on ![]() and

and ![]() .

.

An alternative empirical strategy is to rely on an external estimate of the variance of the measurement error, ![]() . Define the moments, adjusted for measurement error as:

. Define the moments, adjusted for measurement error as:

where ![]() is available externally. The three moments above depend only on θ,

is available externally. The three moments above depend only on θ, ![]() and

and ![]() . We can then estimate these parameters using a Minimum Distance procedure.

. We can then estimate these parameters using a Minimum Distance procedure.

Such external measures can sometimes be obtained through validation studies. For example, Bound and Krueger (1991) conduct a validation study of the CPS data on earnings and conclude that measurement error explains 35 percent of the overall variance of the rate of growth of earnings of males in the CPS. Bound et al. (1994) find a value of 26 percent using the PSID-Validation Study.33

3.1.3 Estimating alternative income processes

Time varying impacts An alternative specification with very different implications is one where

![]() (19)

(19)

where hi is a fixed effect while υi,a,t follows some MA process and mi,a,t is measurement error (see Holtz-Eakin et al., 1988). This process can be estimated by method of moments following a suitable transformation of the model. Define θt = dt/dt−1 and quasi-difference to obtain:

(20)

(20)

In this model the persistence of the shocks is captured by the autoregressive component of ln Y, which means that the effects of time varying characteristics are persistent to an extent. Given estimates of the levels equation in (20) the autocovariance structure of the residuals can be used to identify the properties of the error term dtΔυi,a,t + mi,a,t−θtmi,a−1,t−1.

Alternatively, the fixed effect with the autoregressive component can be replaced by a random walk in a similar type of model. This could take the form

![]() (21)

(21)

In this model pi,a,t = pi,a−1,t−1 + ζi,a,t as before, but the shocks have a different effect depending on aggregate conditions. Given fixed T a linear regression in levels can provide estimates for dt, which can now be treated as known.

Now define θt = dt/dt−1 and consider the following transformation

![]() (22)

(22)

The autocovariance structure of ln Yi,a,t − θt ln Yi,a−1,t−1 can be used to estimate the variances of the shocks, very much like in the previous examples. We will not be able to identify separately the variance of the transitory shock from that of measurement error, just like before. In general, one can construct a number of variants of the above model but we will move on to another important specification, keeping from now on any macroeconomic effects additive.

It should be noted that (22) is a popular model among labor economists but not among macroeconomists. One reason is that it is hard to use in macro models—one needs to know the entire sequence of prices, address general equilibrium issues, etc.

Stochastic growth in earnings Now consider generalizing in a different way the income process and allow the residual income growth (16) to become

![]() (23)

(23)

where the fi is a fixed effect. The fundamental difference of this specification from the one presented before is that the income growth of a particular individual will be correlated over time. In the particular specification above, all theoretical autocovariances of order three or above will be equal to the variance of the fixed effect fi. Consider starting with the null hypothesis that the model is of the form presented in (15) but with an unknown order for the MA process governing the transitory shock υi,a,t = Θq(L)εi,a,t. In practice we will have a panel data set containing some finite number of time series observations but a large number of individuals, which defines the maximum order of autocovariance that can be estimated. In the PSID these can be about 30 (using annual data). The pattern of empirical autocovariances consistent with (16) is one where they decline abruptly and become all insignificantly different from zero beyond that point. The pattern consistent with (23) is one where the autocovariances are never zero but after a point become all equal to each other, which is an estimate of the variance of fi.

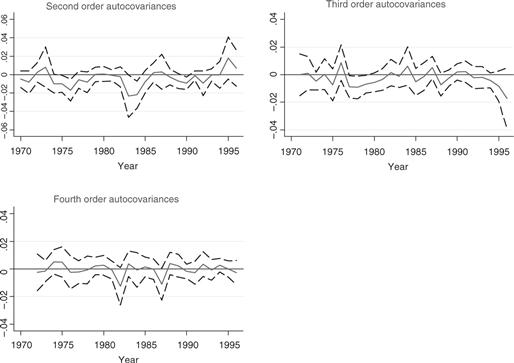

Evidence reported in MaCurdy (1982), Abowd and Card (1989), Topel and Ward (1992), Moffitt and Gottschalk (1994) and Meghir and Pistaferri (2004) and others all find similar results: Autocovariances decline in absolute value, they are statistically insignificant after the 1st or 2nd order, and have no clear tendency to be positive. They interpret this as evidence that there is no random growth term. Figure 4 uses PSID data and plot the second, third and fourth order autocovariances of earnings growth (with 95% confidence intervals) against calendar time. They confirm the findings in the literature: After the second lag no autocovariance is statistically significant for any of the years considered, and there are as many positive estimates as negative ones. In fact, there is no clear pattern in these estimates.

With a long enough panel and a large number of cross sectional observations we should be able to detect the difference between the two alternatives. However, there are a number of practical and theoretical difficulties. First, with the usual panel data, the higher order autocovariances are likely to be estimated based on a relatively low number of individuals. This, together with the fact that the residuals already contain noise from removing the estimated effects of characteristics such as age and even time effects will mean that higher order autocovariances are likely to be imprecisely estimated, even if the variance of fi is indeed non-zero. Perhaps administrative data is one way round this, because we will be observing long run data on a large number of individuals. However, such data is not always available either because it is not organized in a usable way or because of confidentiality issues.

The other issue is that without a clearly articulated hypothesis we may not be able to distinguish among many possible alternatives, because we do not know the order of the MA process, q, or even if we should be using an MA or AR representation, or if the “permanent component” has a unit root or less. If we did, we could formulate a method of moments estimator and, subject to the constraints from the amount of years we observe, we could estimate our model and test our null hypothesis.

The practical identification problem is well illustrated by an argument in Guvenen (2009). Consider the possibility that the component we have been referring to as permanent, pi,a,t, does not follow a random walk, but follows some stationary autoregressive process. In this case the increase in the variance over the life cycle will be captured by the term α × fi. The theoretical autocovariances of gi,a,t will never become exactly zero; they will start negative and gradually increase asymptotically to a positive number which will be the variance of fi, say ![]() . Specifically if pi,a,t = RPi,a−1,t−1 + ζi,a,t with |ρ| < 1, there is no other transitory stochastic component, and the variance of the initial draw of the permanent component is zero, the autocovariances of order k have the form

. Specifically if pi,a,t = RPi,a−1,t−1 + ζi,a,t with |ρ| < 1, there is no other transitory stochastic component, and the variance of the initial draw of the permanent component is zero, the autocovariances of order k have the form

![]() (24)

(24)

As ρ approaches one the autocovariances will approach ![]() . However, the autocovariance in (24) is the sum of a positive and a negative component. Guvenen (2009) has shown, based on simulations, that it is almost impossible in practice with the usual sample sizes to distinguish the implied pattern of the autocovariances from (24) from the one estimated from PSID data. The key problem with this is that the usual panel data that is available either follows individuals for a limited number of time periods, or suffers from severe attrition, which is probably not random, introducing biases. Thus, in practice it is very difficult to identify the nature of the income process without some prior assumptions and without combining information with another process, such as consumption or labor supply.

. However, the autocovariance in (24) is the sum of a positive and a negative component. Guvenen (2009) has shown, based on simulations, that it is almost impossible in practice with the usual sample sizes to distinguish the implied pattern of the autocovariances from (24) from the one estimated from PSID data. The key problem with this is that the usual panel data that is available either follows individuals for a limited number of time periods, or suffers from severe attrition, which is probably not random, introducing biases. Thus, in practice it is very difficult to identify the nature of the income process without some prior assumptions and without combining information with another process, such as consumption or labor supply.

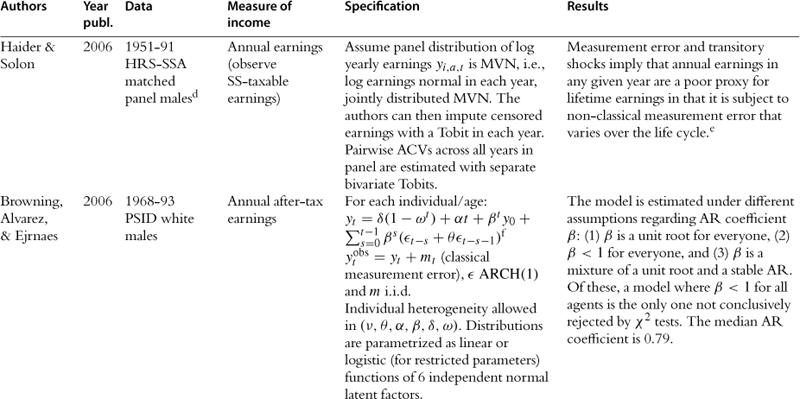

Haider and Solon (2006) provide a further illustration of how difficult it is to distinguish one model from the other. They are interested in the association between current and lifetime income. They write current log earnings as

yi,a,t = hi + afi

and lifetime earnings as (approximately)

log Vi = r − log r + hi + r−1 fi.

The slope of a regression of yi,a,t onto log Vi is:

![]()

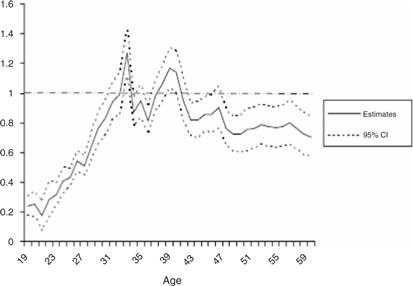

Hence, the model predicts that λa should increase linearly with age. In the absence of a random growth term ![]() , λa = 1 at all ages. Figure 5, reproduced from Haider and Solon (2006) shows that there is evidence of a linear growth in λa only early in the life cycle (up until age 35); however, between age 35 and age 50 there is no evidence of a linear growth in λa (if anything, there is evidence that λa declines and one fails to reject the hypothesis λa = 1); finally, after age 50, there is evidence of a decline in λa that does not square well with any random growth term in earnings.

, λa = 1 at all ages. Figure 5, reproduced from Haider and Solon (2006) shows that there is evidence of a linear growth in λa only early in the life cycle (up until age 35); however, between age 35 and age 50 there is no evidence of a linear growth in λa (if anything, there is evidence that λa declines and one fails to reject the hypothesis λa = 1); finally, after age 50, there is evidence of a decline in λa that does not square well with any random growth term in earnings.

Figure 5 Estimates of λa from Haider and Solon (2006).

Other enrichments/issues The literature has addressed many other interesting issues having to do with wage dynamics, which here we only mention in passing. First, the importance of firm or match effects. Matched employer-employee data could be used to address these issues, and indeed some papers have taken important steps in this direction (see Abowd et al., 1999; Postel-Vinay and Robin, 2002; Guiso et al., 2005).

A number of papers have remarked that wages fall dramatically at job displacement, generating so-called “scarring” effects (Jacobson et al., 1993; von Wachter et al., 2007). The nature of these scarring effects is still not very well understood. On the one hand, people may be paid lower wages after a spell of unemployment due to fast depreciation of their skills (Ljunqvist and Sargent, 1998). Another explanation could be loss of specific human capital that may be hard to immediately replace at a random firm upon re-entry (see Low et al., forthcoming).

3.1.4 The conditional variance of earnings

The typical empirical strategy followed in the precautionary savings literature, in the attempt to understand the role of risk in shaping household asset accumulation choices, typically proceeds in two steps. In the first step, risk is estimated from a univariate ARMA process for earnings (similar to one of those described earlier). Usually the variance of the residual is the assumed measure of risk. There are some variants of this typical strategy—for example, allowing for transitory and permanent income shocks. In the second step, the outcome of interest (assets, savings, or consumption growth) is regressed onto the measure of risk obtained in the first stage, or simulations are used to infer the importance of the precautionary motive for saving. Examples include Banks et al. (2001) and Zeldes (1989). In one of the earlier attempts to quantify the importance of the precautionary motive for saving, Caballero (1990) concluded −using estimates of risk from MaCurdy (1982)—that precautionary savings could explain about 60% of asset accumulation in the US.

A few recent papers have taken up the issue of risk measurement (i.e., modeling the conditional variance of earnings) in a more complex way. Here we comment primarily on Meghir and Pistaferri (2004).34

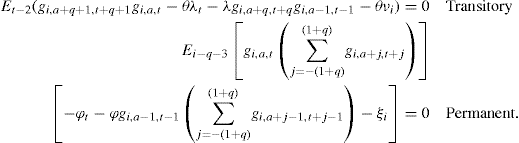

Meghir and Pistaferri (2004) Returning to the model presented in Section 3.1.1 we can extend this by allowing the variances of the shocks to follow a dynamic structure with heterogeneity. A relatively simple possibility is to use ARCH(1) structures of the form

![]() (25)

(25)

where Et–1 (.) denotes an expectation conditional on information available at time t − 1. The parameters are all education-specific. Meghir and Pistaferri (2004) test whether they vary across education. The terms γt and ϕt are year effects which capture the way that the variance of the transitory and permanent shocks change over time, respectively. In the empirical analysis they also allow for life cycle effects. In this specification we can interpret the lagged shocks (εi,a−1,t−1, ζi,a−1,t−1) as reflecting the way current information is used to form revisions in expected risk. Hence it is a natural specification when thinking of consumption models which emphasize the role of the conditional variance in determining savings and consumption decisions.

The terms v¿ and ξ; are fixed effects that capture all those elements that are invariant over time and reflect long term occupational choices, etc. The latter reflects permanent variability of income due to factors unobserved by the econometrician. Such variability may in part have to do with the particular occupation or job that the individual has chosen. This variability will be known by the individuals when they make their occupational choices and hence it also reflects preferences. Whether this variability reflects permanent risk or not is of course another issue which is difficult to answer without explicitly modeling behavior.35

As far as estimating the mean and variance process of earnings is concerned, this model does not require the explicit specification of the distribution of the shocks; moreover the possibility that higher order moments are heterogeneous and/or follow some kind of dynamic process is not excluded. In this sense it is very well suited for investigating some key properties of the income process. Indeed this is important, because as discussed earlier the properties of the variance of income have implications for consumption and savings.

However, this comes at a price: first, Meghir and Pistaferri (2004) need to impose linear separability of heterogeneity and dynamics in both the mean and the variance. This allows them to deal with the initial conditions problem without any instruments. Second, they do not have a complete model that would allow them to simulate consumption profiles. Hence the model must be completed by specifying the entire distribution.

Identification of the ARCH process If the shocks ε and ζ were observable it would be straightforward to estimate the parameters of the ARCH process in (25). However they are not. What we do observe (or can estimate) is gi,a,t = Δmi,a,t + (1+θL) Δεi,a,t + ζi,a,t. To add to the complication we have already argued that θ is not point identified. Nevertheless the following two key moment conditions identify the parameters of the ARCH process, conditional on the unobserved heterogeneity (η and ξ):

(26)

(26)

The important point here is that it is sufficient to know the order of the MA process q.36 We do not need to know the parameters themselves. The parameter θ that appears in (26) for the transitory shock is just absorbed by the time effects on the variance or the heterogeneity parameter. Hence measurement error, which prevents the identification of the MA process does not prevent identification of the properties of the variance, so long as such error is classical.

The moments above are conditional on unobserved heterogeneity; to complete identification we need to control for that. As the moment conditions demonstrate, estimating the parameters of the variances is akin to estimating a dynamic panel data model with additive fixed effects. Typically we should be guided in estimation by asymptotic arguments that rely on the number of individuals tending to infinity and the number of time periods being fixed and relatively short.

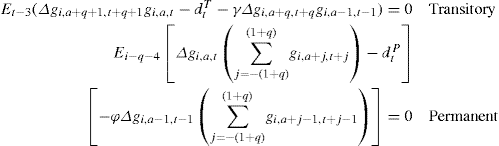

One consistent approach to estimation would be to use first differences to eliminate the heterogeneity and then use instruments dated t − 3 for the transitory shock and dated t − q − 4 for the permanent one. In this case the moment conditions become

(27)

(27)

where Δxt = xt − xt−1. In practice, however, as Meghir and Pistaferri (2004) found out, lagged instruments suggested above may be only very weakly correlated with the entities in the expectations above. This means that the rank condition for identification is not satisfied and consequently the ARCH parameters may not be identifiable through this approach. An alternative may be to use a likelihood approach, which will exploit all the moments implied by the specification and the distributional assumption; this however may be particularly complicated. A convenient approximation may be to use a within group estimator on (26). This involves subtracting the individual mean of each expression on the right hand side, i.e. just replace all expressions in (26) by quantities where the individual mean has been removed. For example gi,a+q+1,t+q+1gi,a,t is replaced by ![]() . Nickell (1981) and Nerlove (1971) have shown that this estimator is inconsistent for fixed T. Effectively this implies that the estimates may be biased when T is short because the individual specific mean may not satisfy the moment conditions for short T. In practice this estimator will work well with long panel data. Meghir and Pistaferri use individuals observed for at least 16 periods. Effectively, while ARCH effects are likely to be very important for understanding behavior, there is no doubt that they are difficult to identify. A likelihood based approach, although very complex, may ultimately prove the best way forward.

. Nickell (1981) and Nerlove (1971) have shown that this estimator is inconsistent for fixed T. Effectively this implies that the estimates may be biased when T is short because the individual specific mean may not satisfy the moment conditions for short T. In practice this estimator will work well with long panel data. Meghir and Pistaferri use individuals observed for at least 16 periods. Effectively, while ARCH effects are likely to be very important for understanding behavior, there is no doubt that they are difficult to identify. A likelihood based approach, although very complex, may ultimately prove the best way forward.

Other approaches

3.1.5 A summary of existing studies

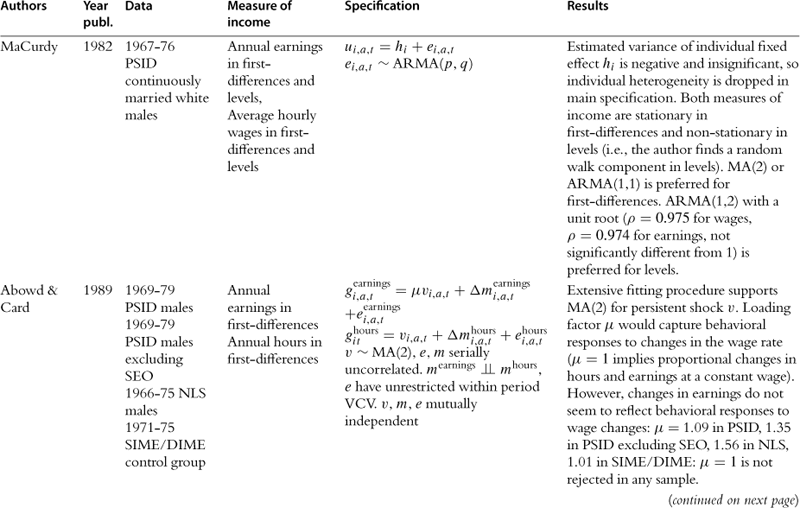

In this section we provide a summary of the key studies in the literature.37 Most of the information is summarized in Table 2, but we also offer a brief description of the key results of the papers in the text. Some of the earliest studies are those of Hause (1980), who was investigating the importance of on-the-job training, and Lillard and Willis (1978), who were interested in earnings mobility. Both find an important role for unobserved heterogeneity and conclude that the process of income is stationary. Hause used the idea of heterogeneous income profiles, which later played a central role in the debate in this literature.

Table 2

aAuthors cut sample by race (black/white).

bNo covariates, so profile heterogeneity captures differences across education groups (focus is on low education workers).

cI.e., gi,a,t = yi,a,t − yi,a−4,t−4 where t indexes quarters.

e> Sample average estimated ACVs pooled over full earnings history (from bivariate Tobit procedures) are very close to results from uncensored data in other studies (Baker and Solon, 2003, Bohlmark and Lindquist, 2006): ACV1 = 0.89, ACV2 = 0.82, ACV3 = 0.78, ACV4 = 0.75, ACV5 = 0.72, ACV6 = 0.69.

f[δ] = “long-run” average earnings; [ω] = inverse speed of convergence to “long-run” average earnings; [a] = linear time trend; [β] = AR(1) coefficient; [θ] = MA(1) coefficient; [ε] = ARCH WN, with constant η, ARCH coefficient ![]() .

.

gParametrization of the model makes it difficult to compare point estimates to other results from the literature. Results for impulse-response to particular shocks are interesting results, but the less detailed models in the income-process literature reviewed here typically present unconditional dynamic behavior rather than distinguishing particular shocks.

h“Joint” in the sense that it is more complex than the univariate earnings processes presented here, but still based only on labor market behavior; “statistical” in the sense that the model’s structural equations are not derived from utility maximization.

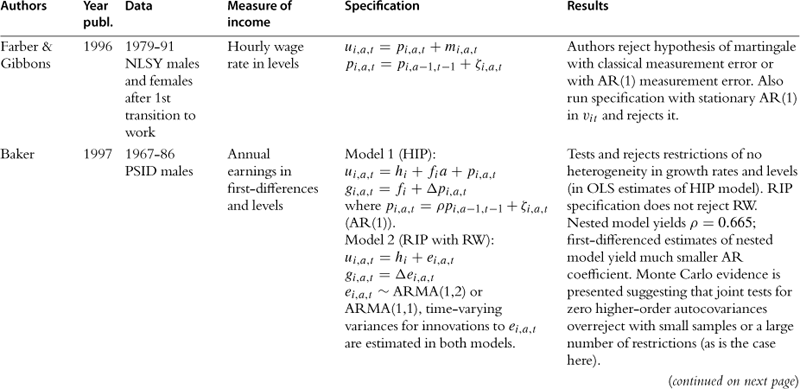

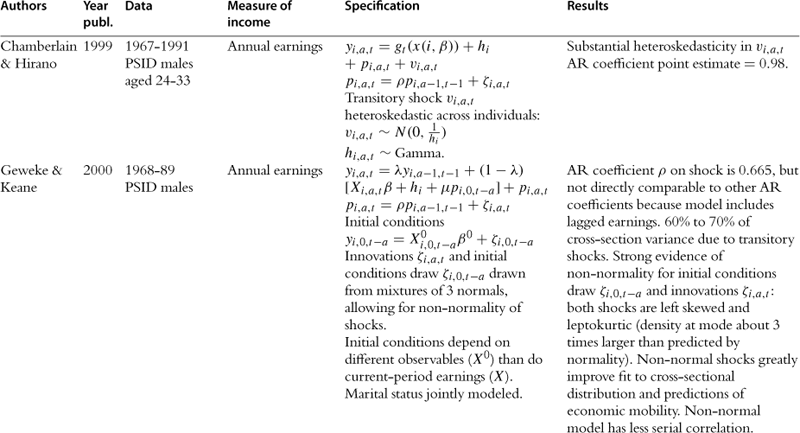

Following these papers are two of the most important works in this literature, namely MaCurdy (1982) and Abowd and Card (1989). Both use PSID data for ten years, but covering different time periods. Abowd and Card also use NLS data and data from an income maintenance experiment. The emphasis on these papers is precisely to understand the time series properties of earnings and extract information relating to the variance of the shocks. They both conclude that the best representation of earnings is one with a unit root in levels and MA(2) in first differences. Abowd and Card go further and also model the time series properties of hours of work jointly with earnings, potentially extracting the extent to which earnings fluctuations are due to hours fluctuations. The papers by Low et al. (forthcoming) and Altonji et al. (2009), which explicitly make the distinction between shocks and endogenous responses to shocks, can be seen as related to this work. Similar conclusions are reached by Topel and Ward (1992) using matched firm-worker administrative records spanning 16 years. They conclude that earnings are best described by a random walk plus an i.i.d. error.

In an important paper Gottschalk and Moffitt (1995) use the permanent-transitory decomposition to fit data on earnings and to try to understand the relative importance of the change in the permanent and transitory variance in explaining the changes in US inequality over the 1980s and 1990s. Their permanent component is defined to be a random walk with a time varying variance. The transitory component is an AR(1), also with time varying variance. Both variances were shown to increase over time. They also consider a variety of other models including most importantly the random growth model, where age is interacted with a fixed effect. As we have already explained, this is an important alternative to the random walk model because they both explain the increase in variance of earnings with age, but have fundamentally different economic implications. In their results the two models fit equally well the data38. Based on earlier results by Abowd and Card (1989), Gottschalk and Moffitt choose the random walk model as their vehicle for analysis of inequality and mobility patterns in the data.

Farber and Gibbons (1996) provide a structural interpretation of wage dynamics. The key idea here is that firms publicly learn the worker’s ability and at each point in time the wage is set equal to the conditional expectation of workers’ productivity. Among other results this implies that wage levels follow a martingale. The result is however fragile; for example, if heterogeneous returns to experience are allowed for, the martingale result no longer holds. Their results indeed reject the martingale hypothesis. The model is quite restrictive, because it does not allow for the incumbent firm to have superior information as in Acemoglu and Pischke (1998). Moreover, given the specification in levels (rather than in logs), the relevance of this paper to the literature we are discussing here is mainly because of its important attempt to offer a structural interpretation to wage dynamics rather than for its actual results.