Chapter Twelve

Project Cost Analysis

Abstract

This chapter essentially consists of understanding the Project Cost Analysis process, including budget development—an analysis project buyout and bid shopping. It goes on to highlight popular budgeting software like Projectmates, Smartsheet. This is followed by an analysis of General Conditions and Supplemental Conditions in the project manual and why they are important to the contract. Similarly, budget allowances are covered and what they normally consist of. The various types of contingencies and allowances and their importance are then explained. The ingredients for successful Green Project Cost Management as well as Successful Cost Management Procedures and objectives are investigated. Additionally, the various hard costs and soft costs are studied and clarified. Toward the end, the different phases a project must go through from design concept to completion and occupancy are explained. Finally, the preconstruction conference and notice to proceed and substantial completion are examined.

Keywords

As-built drawings; Cash flow; Contingency clause; Databases; Hard costs; Overhead; Project buyout; Risk allowances; Soft costs; Substantial completion

12.1. General Overview

The construction industry has substantial environmental, social, and economic impacts on society. Because of this, society is witnessing an unusually rapid growth of the green building sector—mainly to mitigate the negative impacts associated with construction-related activities. To assist in this effort, successful development projects are grounded in painstaking analysis and rigorous planning to help formulate a comprehensive compilation of construction-related cost information as this is a pivotal tool for assessing the merits of a proposed construction undertaking. There are many software packages on the market like “Projectmates,” which has capabilities ranging from document management and scheduling to financial budgeting and change order management. Projectmates software contains over 40 different modules for almost every type of construction project and can save considerable time as well as increase accountability among the various project participants. Also, while owners may choose to delegate responsibilities to other professionals on the project team, such decisions are left to their discretion and control. It should be noted that Projectmates has dramatically improved the construction programs for countless organizations with vastly different backgrounds and needs.

Viewpoint Construction Software is another software package of many on the market that is dedicated to providing advanced, easy-to-use, and efficient management software and which is said to be available exclusively to the construction industry. Project Managers and estimators are indeed fortunate that there is such a wide range of computer-aided cost estimation software systems available, ranging in sophistication from simple spreadsheet calculation software to integrated systems involving design and price negotiation over the Internet. While such software involves costs for purchase, maintenance, training, and computer hardware, the user will experience significant benefits. In particular, cost estimates may be prepared more rapidly and with less effort. Professor Chris Hendrickson, Codirector of the Green Design Institute, depicts some of the more common features of computer-aided cost estimation software such as:

• Databases for unit cost items such as worker wage rates, equipment rental, or material prices. These databases can be used for any cost estimate required. If these rates change, cost estimates can be rapidly recomputed after the databases are updated.

• Databases of expected productivity for different components types, equipment and construction processes.

• Import utilities from computer-aided design software for automatic quantity takeoff of components. Alternatively, special user interfaces may exist to enter geometric descriptions of components to allow automatic quantity takeoff.

• Export utilities to send estimates to cost control and scheduling software. This is very helpful to begin the management of costs during construction.

• Version control to allow simulation of different construction processes or design changes for the purpose of tracking changes in expected costs.

• Provisions for manual review, override, and editing of any cost element resulting from the cost estimation system.

• Flexible reporting formats, including provisions for electronic reporting rather than simply printing cost estimates on paper.

• Archives of past projects to allow rapid cost estimate updating or modification for similar designs.

The construction industry continues to have procurement problems arising from an impractical division between the design and construction process, a lack of organization among subcontractors, strained relationships between design professionals and construction team members within the integrated project team, outdated design and construction techniques, preventable delays, and inferior quality end product. However, in recent years the construction industry has demonstrated significant improvements in application of new technology and methods in which clients have been the driving force for change leading to the development of improved and more sophisticated services (e.g., project management, facilities management, better handle on cash flow, and alternate procurement methods). This need for change originated from the desire for a more competitive and efficient industry. Education programs have also been created to merge construction and design to emphasize multiskilled trades.

When it comes to green building a Davis Langdon study, “Costing Green: A Comprehensive Cost Database and Budgeting Methodology” compared the square-foot construction costs of 61 buildings pursuing Leadership in Energy and Environmental Design (LEED) certification to those of similar conventional buildings without green objectives. Taking into consideration climate, location, and other variables, the study came to the conclusion that for many of the sustainable projects, aiming for LEED certification, resulted in little or no impact on the general budget.

Another point worth noting is that construction lending is basically real estate lending and the construction lender should therefore be aware that the primary security of the loan is primarily the real estate to be developed and that in order for the loan to be repaid the development has to be completed. Experience shows that few real estate borrowers are able to repay a construction loan from the assets listed in their financial statements. The borrower’s professional and financial capabilities are key elements in the loan determination and should be thoroughly looked into before a loan commitment is made.

Professor Hendrickson says, “The costs of a constructed facility to the owner include both the initial capital cost and the subsequent operation and maintenance costs. Each of these major cost categories consists of a number of cost components.”

To be able to determine the capital cost for a construction project, it is necessary to estimate the expenses related to the initial erection of the facility which according to Hendrickson include:

• Land acquisition, including assembly, holding, and improvement

• Planning and feasibility studies

• Architectural and engineering design

• Construction, including materials, equipment, and labor

• Field supervision of construction

• Construction financing

• Insurance and taxes during construction

• Owner’s general office overhead

• Equipment and furnishings not included in construction

• Inspection and testing.

In addition, the project owner must also consider the operation and maintenance cost of the project over its life cycle for which Hendrickson includes the following expenses:

• Land rent, if applicable

• Operating staff

• Labor and material for maintenance and repairs

• Periodic renovations

• Insurance and taxes

• Utilities

• Owner’s other expenses.

The consequence and significance of each of the above cost elements rely on the project’s type, size, and location as well as the management organization, among many other considerations. As far as the owner is concerned, the ultimate objective is achieving the lowest possible overall project cost that at the same time meets the specified quality and investment objectives of the project.

A well-defined Project Budget includes all the possible hard and related construction costs and identifies where the funds are coming from. To estimate the total project cost (TPC) therefore one must include all hard and soft costs to make the building complete and useable as intended. Costs would include construction costs, construction contingency, architect/engineer fee, project contingency, owner services, and administrative fees. Depending on the general conditions and contract documents requirements, the TPC may also include infrastructure costs, furniture and equipment costs, voice/data costs, instructional technology costs, moving costs, and custodial equipment costs.

Construction cost, on the other hand, is the fee charged by a general contractor or construction firm for a project. Construction costs per gross square foot will vary from state to state, whether the project is new construction or renovation and the type, size, and complexity of the project (e.g., office, educational, hospital, hotel, school, residential, etc.).

According to Hendrickson the important thing is for “design professionals and construction managers to realize that while the construction cost may be the single largest component of the capital cost, other cost components are not insignificant. For example, land acquisition costs are a major expenditure for building construction in high-density urban areas, and construction financing costs can reach the same order of magnitude as the construction cost in large projects such as the construction of nuclear power plants.

From the owner’s perspective, it is equally important to estimate the corresponding operation and maintenance cost of each alternative for a proposed facility to analyze the life cycle costs. The large expenditures needed for facility maintenance, especially for publicly owned infrastructure, are reminders of the neglect in the past to consider fully the implications of operation and maintenance cost in the design stage.”

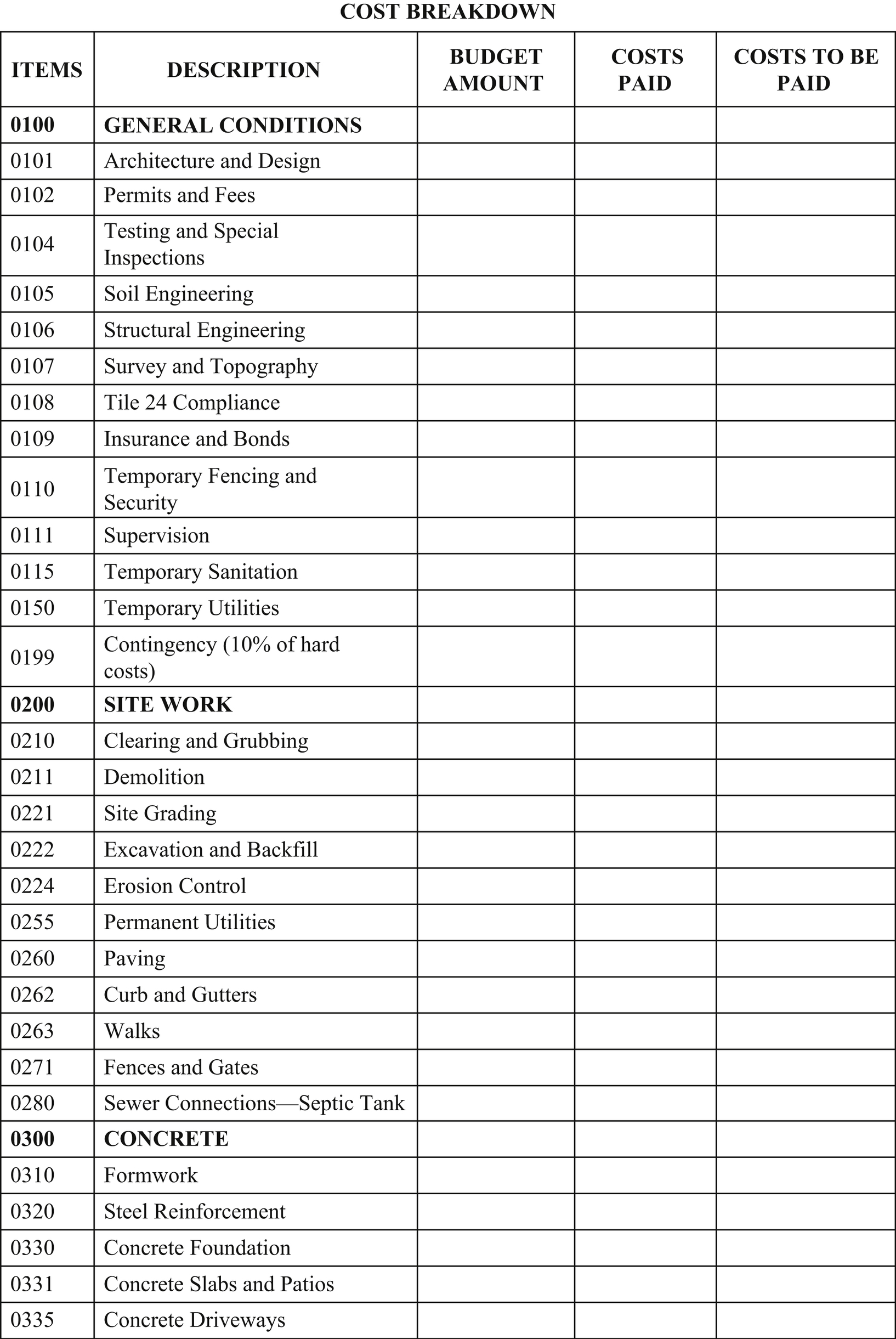

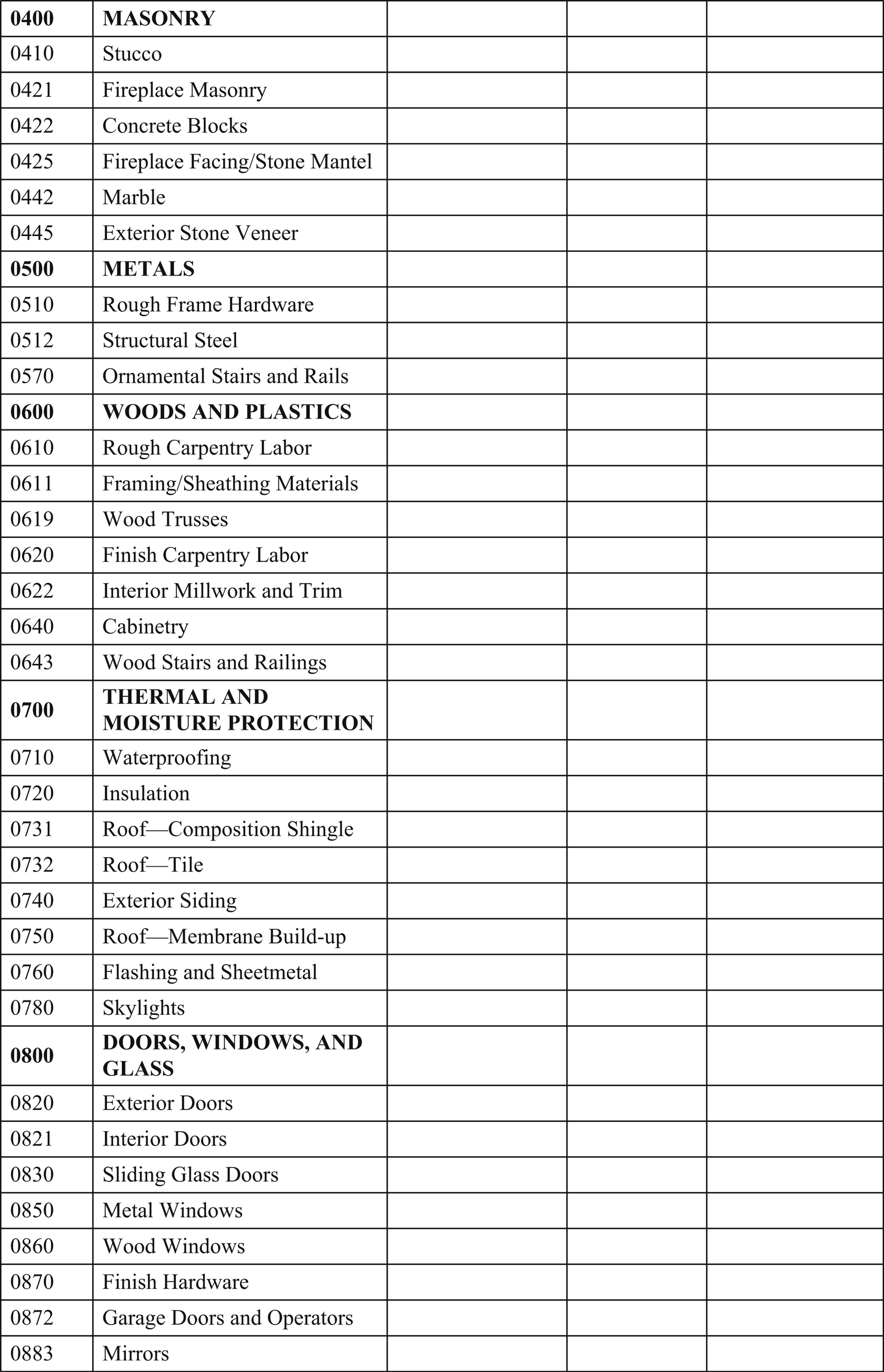

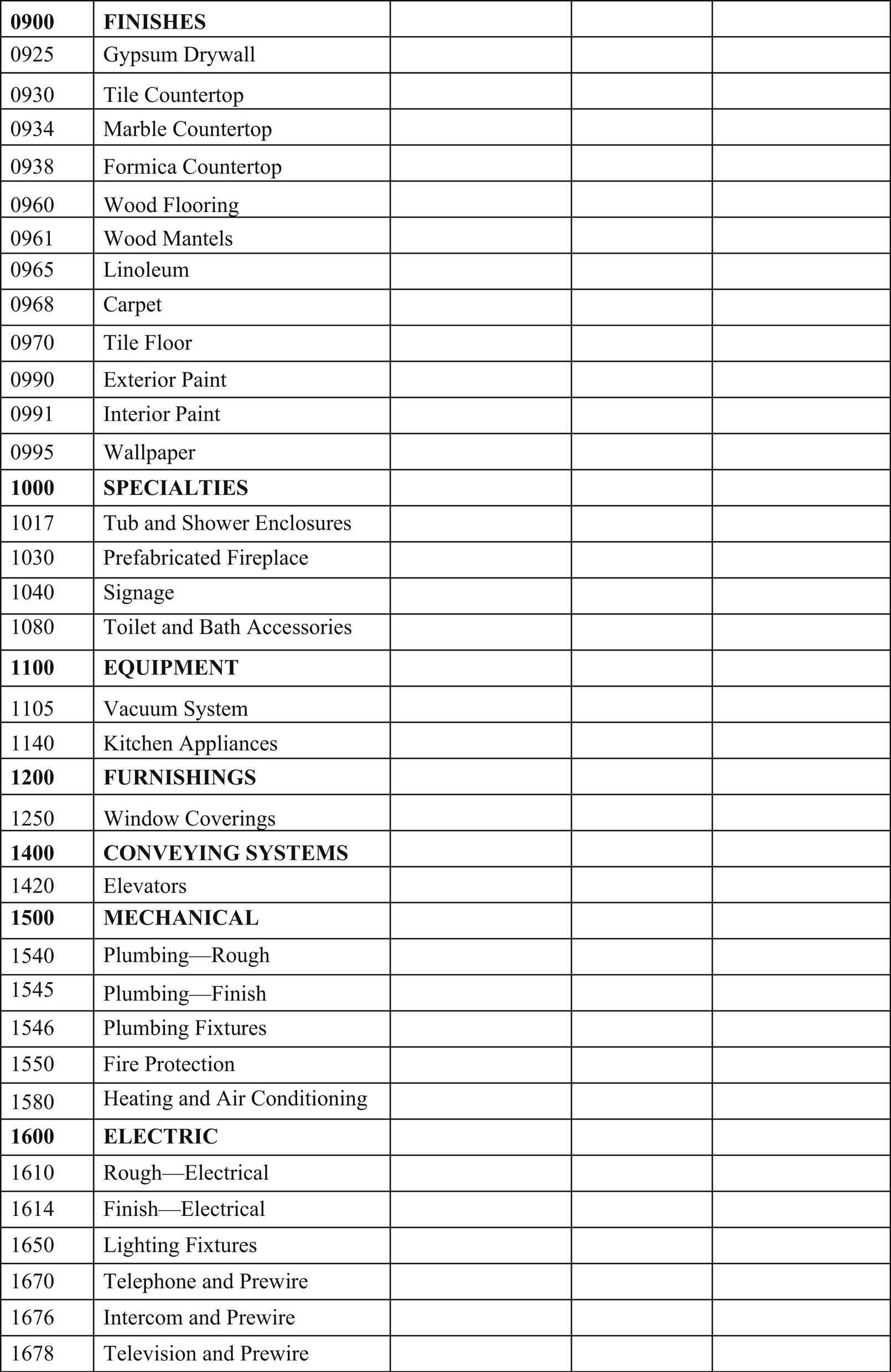

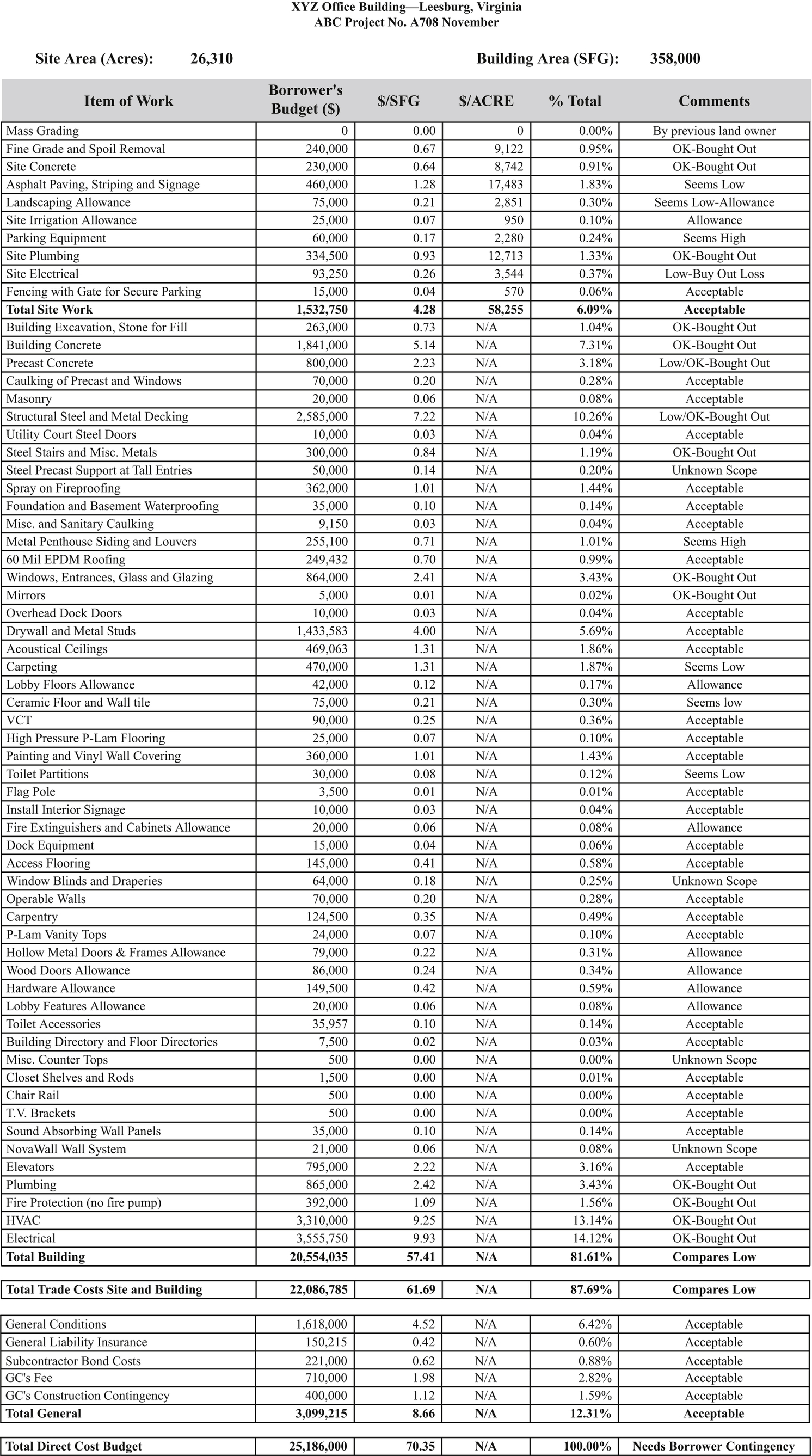

Most construction budgets contain a contingency clause for unexpected cost overruns that may occur during construction. While this contingency amount may be included within each cost item, it is preferably included as a single category namely a construction contingency, which is normally a percentage of the project’s estimated cost. This contingency amount is based on several factors including the complexity and size of the project and whether it is new construction or renovation, etc. For example, for large new construction projects the contingency is generally about 5% of the total cost, whereas for renovations, it may be roughly 7%. Likewise, for small interior projects, it may be as high as 10%. Any remaining contingency amounts can be released upon substantial completion of the project. However, it should be noted that in many cases neither the architect nor the contractor know the contingency amount in place. On this, the Engineering News-record says that “On average, owners share contingency information with their architects a little over half the time (58%) and with their contractors 43% of the time.” In Fig. 12.1, below is a sample project cost breakdown showing the main elements to be considered when preparing a budget estimate for the project.

Figure 12.1 An example of a project cost breakdown and budget estimate. To estimate the total project cost (TPC), it is necessary to include all hard and soft costs to fully execute the building as intended. TPCS include construction costs, contingencies, architect/engineer fee, owner services, and administrative fees. Depending on the general conditions and contract documents requirements, the TPC may also include infrastructure costs, furniture and equipment costs, instructional technology costs, moving costs, and other costs.

The developer’s, builder’s or CM’s fee is usually released as a direct percentage of the value of the subcontractual work completed to date.

12.2. Budget Development—An Analysis

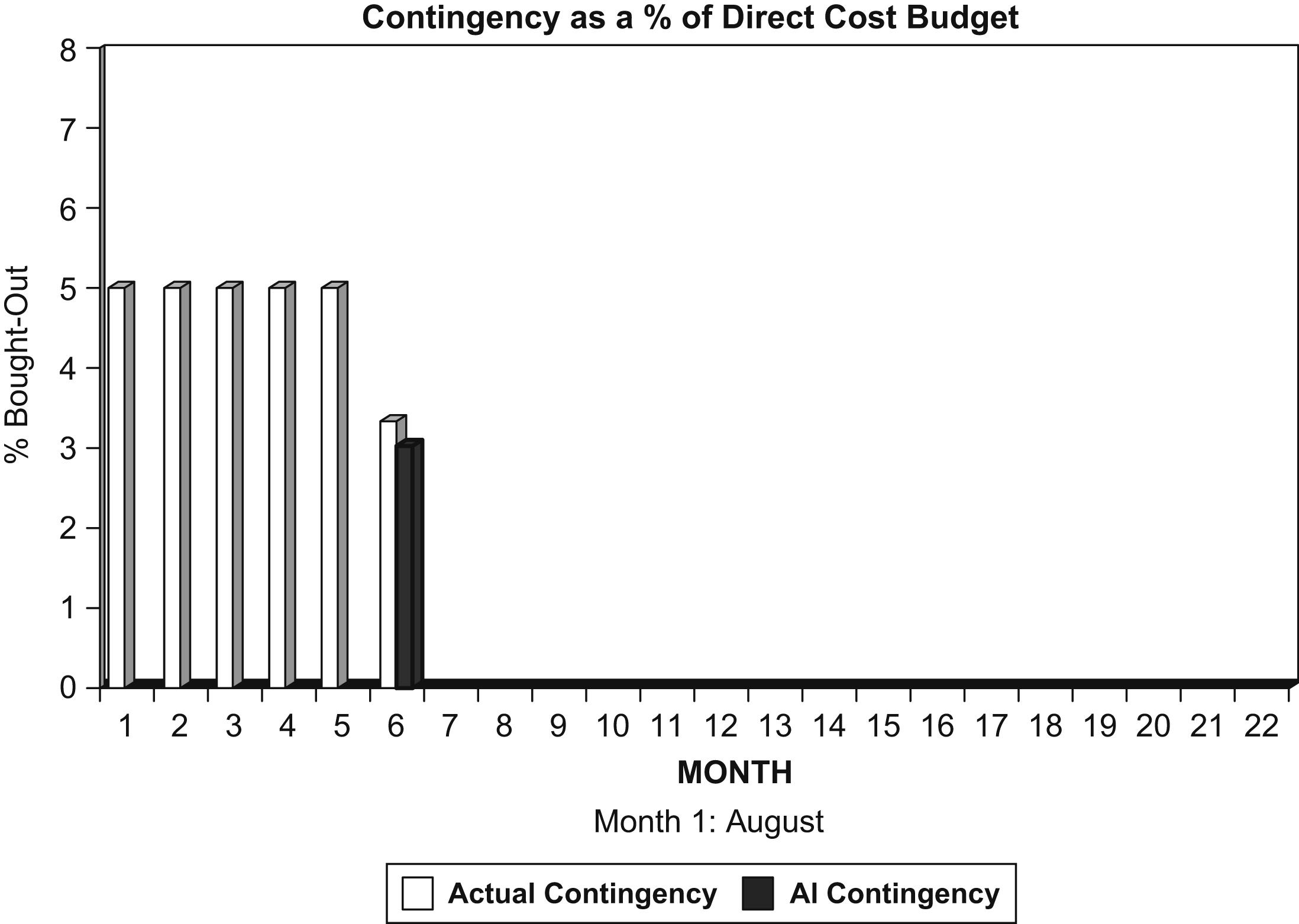

A project budget estimate is a financial plan to design and build a particular project and setting out the estimated costs to complete the project. Regardless of whether the project to be constructed is large or small, a prudent developer will certainly find it necessary to develop a budget for it. The primary purpose of preparing a budget is to understand and control costs and cost overruns. Cost overruns are mitigated by the inclusion of appropriate contingencies in the budget estimate to cover change orders, etc., and these contingency allowances are disbursed as the projects proceeds to cover the additional costs. Sometimes, construction budgets are formulated using only the “hard construction costs,” without any consideration for the “soft costs,” setting their maximum available amount of money at a level well below what will be necessary to satisfactorily complete the project as intended. Fig. 12.2 is a graph that illustrates the relationship of the contingency as a percentage of the direct cost budget.

Figure 12.2 Graph illustrating relationship of contingency as percentage of direct cost budget as the construction process proceeds.

Randy White CEO of White Hutchinson Leisure & Learning Group says, “Many a project gets into serious trouble when, for whatever reason, the project can’t be developed within the budget. Usually, by the time the problem is discovered, it’s too late to increase the budget, as financing has already been secured. So to keep the project within budget, critical features end up being compromised, such as the theming, finishes, and the quality of the materials, furniture and equipment, the things that really matter the most to creating the guest experience. Or certain attractions are eliminated, so the project never performs as originally planned and projections are never achieved. In fact, such last-minute deletions and changes can seriously threaten a project’s very long-term survival.”

For obtaining a construction loan it is particularly important to have a Budget for the project in place. Thus prior to calculating the required construction loan amount, a basic budget is needed, the main components of which include:

1. Hard costs: direct costs associated with the labor and materials used for the actual physical construction costs of the project

2. Soft costs: indirect or “off-site” costs not directly related to labor or materials for construction (architectural plans, engineering, and permit fees)

3. Closing costs: all costs associated with origination and closing the construction loan such as title cost, loan fees, discount fees, insurance, appraisals, and closing fees

4. Land acquisition costs

5. Inspection fees

6. Reserves: consisting of estimated interest on the loan during construction and contingency reserve for unforeseen expenses and cost overruns

7. Possible equipment, furnishings, and other unforeseen necessities

As previously mentioned, the total cost of construction is obtained by adding all the costs incurred in the project including soft and hard costs. Most projects are constrained by limited monetary funding resources. Consequently, they need to have a budget in place to initially define its funding requirement. The project manager develops the budget based on the cost estimates calculated at the beginning of each project phase and refined once there is more accurate information defining the project’s scope. Refining the budget occurs through studies and analysis in the design development process. When Owners try to fix the budget too early in the project life cycle, they are surprised by the significant increases in the budget over what was set forth. Randy White says that “This reoccurring problem is often caused by the nature of the design process. Design proceeds from general to specific and from conceptual to detailed. Accordingly, there is limited ability to accurately predict construction costs at the onset when initial project planning takes place and accurate costs are needed as part of the business plan to secure financing.” With respect to project cost overruns, White says, “Cost overruns are also caused by the traditional design-bid-build process. First the project is designed, and then a contractor is selected by either competitive bid or negotiation to build the project. This process precludes value engineering until the project is already designed. So by the time the bid comes in over budget, the only way to reduce costs is to make major compromises in finishes, quality or components.”

One of the critical tasks and assignments of the Project Manager (PM) is the development and tracking of the project budget. The PM first develops a project budget in the early feasibility phase and continues to refine it throughout the different project phases until the project is “bought out” by the general contractor prior to the start of the construction phase. All the elements of the budget should be clearly defined and fine-tuned throughout each phase. Specialized estimating software is often used to create, develop, monitor, and track budgets. When developing a budget, there are certain logical steps that should be followed:

Step 1: It is important to determine precisely how much money is available for the project when attempting to develop a project budget. This should include all costs from project initiation as a concept through the award of a construction contract to completion. At various points within the different stages, more detail, specificity and definition are developed and these estimates become more certain and realistic.

Step 2: Determine the mandatory or vital expenses for the project to succeed. Each project has certain requirements that are essential to the project’s success and these should be given priority in the project’s budget. For example, incorporating certain green features to achieve LEED certification is very important, which means that these should be high on the priority list for the project’s budget.

Step 3: Collect preliminary estimates from several companies and contractors. Upon having identified the key elements of the project budget, you can start requesting estimates from area businesses to determine which offers the best price or value for building the project. In any case, preconceived cost indices can often be unrealistic and misleading. Building a new building project in an urban setting, for example, is far more costly than on a green field site. Construction managers usually have a good understanding of true market conditions and pricing in specific regions because their livelihood depends on it. Should your project budget not align with the project’s expectations, then one or both will need realignment.

Step 4: Once the final budget is determined, it should be clearly spelled out and written down on paper and distributed to all the team members to ensure that everyone is on the same page. In the final analysis, it will also depend largely on the type of contract entered into between the owner and the contractor, e.g., whether it is a design-bid-build, design-build, cost-plus, etc.

Furthermore, total reliance on “program” and/or “preliminary” level estimates for setting a final project construction budget is inappropriate because it is far too early in the project’s design/construction process. Until the time when a fairly accurate budget estimate can be developed, the project remains too conceptual in terms of scope and program size to accurately estimate final costs. After the Architect completes the schematic design phase, the project’s scope of work is more clearly defined to the extent that a realistic budget estimate can be arrived at to provide effective discipline and direction on the project. However, this is still insufficient to bid the project and will not be able to do so until the contract documents are completed including all plans and specifications. The different phases or milestones a project must go through from design concept to completion and occupancy are:

1. Project Initiation Program Budget Estimate

2. Planning/Programming Preliminary Project Estimate

3. Design (Conceptual Design, Schematic Design Budget Estimate)

4. Contract Documents (Drawings, Project Manual, etc.)

5. Bidding of Contract, Awarding of Contract—Project Estimate

6. Construction Phase, Commissioning

7. Occupancy Phase.

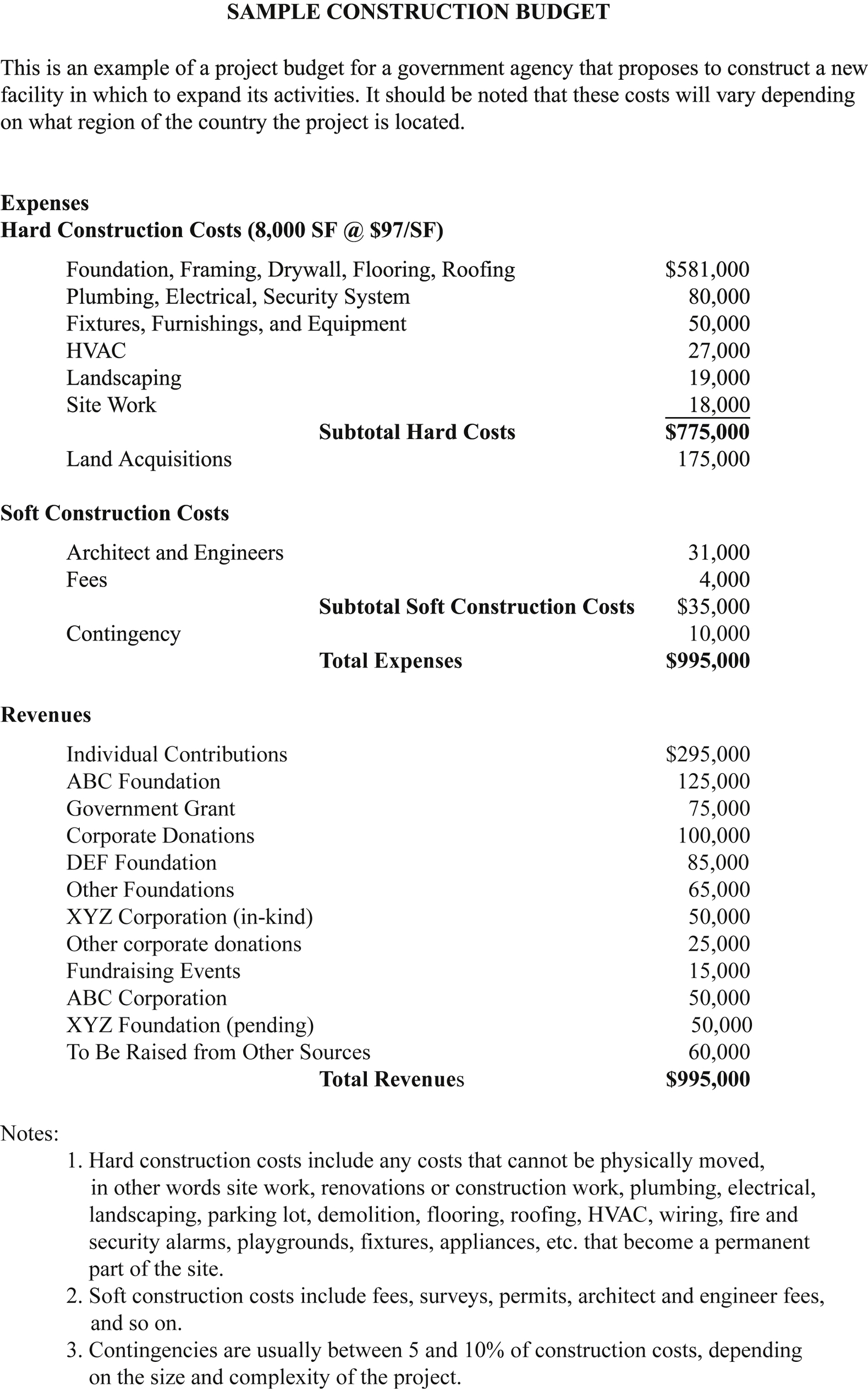

Fig. 12.3 below is an example of preliminary construction budget for a typical project (new construction). This is an example of a project budget for a government agency that proposes to construct a new facility in which to expand its activities. It should be noted that these costs will vary depending on what region of the country the project is located.

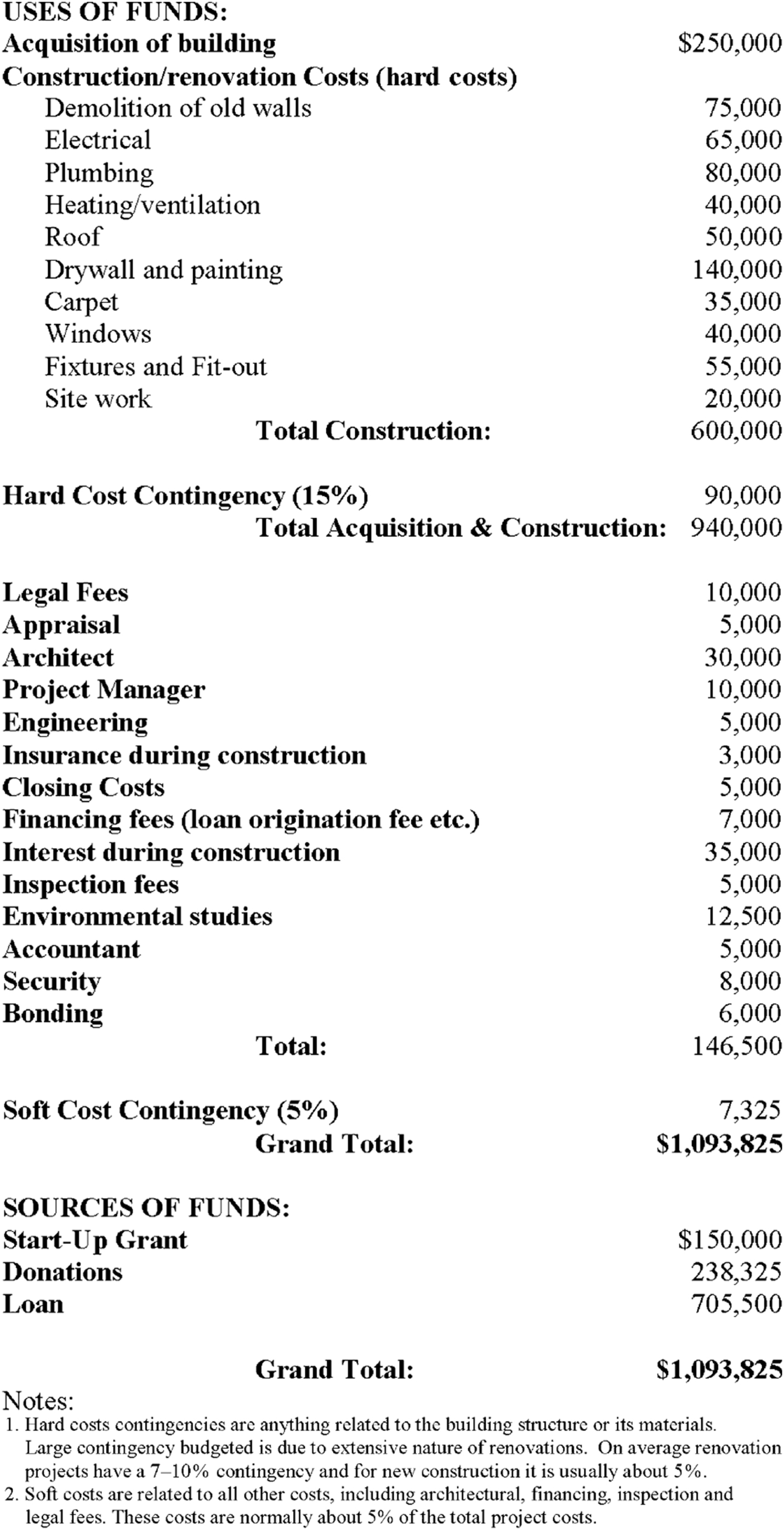

Another example of a simple project budget is in Fig. 12.4 which is adopted from Charter School Facilities—A Resource Guide on Development and Financing, which shows the typical components of a project budget; it includes the purchase and renovation of a building as opposed to new construction.

12.3. Project Buyout and Bid Shopping

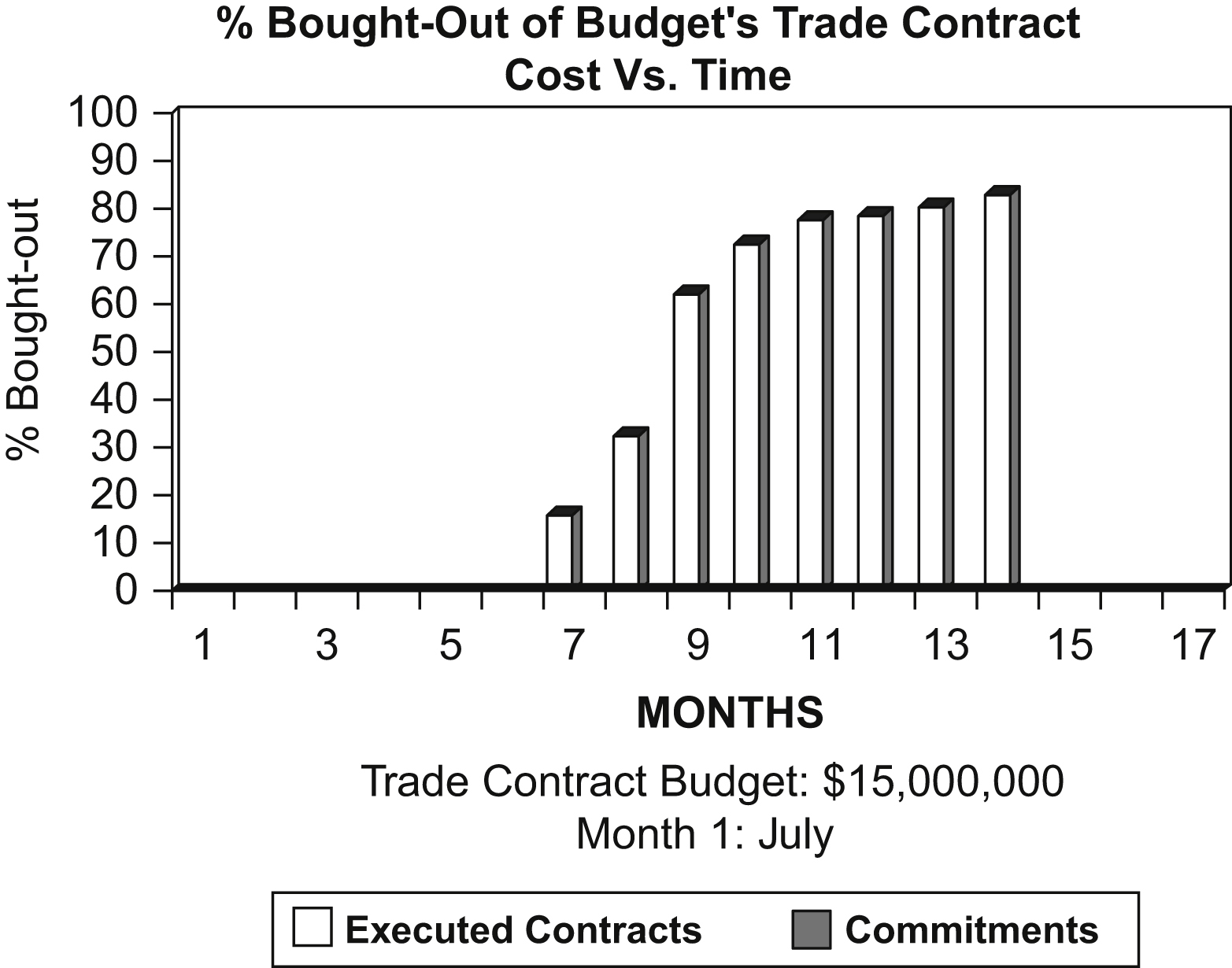

Project buyout and bid shopping are two concepts familiar to most construction professionals. The term buyout, as it relates to construction project mobilization, basically refers to procuring materials and equipment that will be employed in the project and arranging subcontracts. Buyout is the time interval between the preconstruction and the construction phases of a project and is among the most critical first steps in the overall profitability of a construction project. And even before breaking ground, making or losing money could be predetermined based on how well the project is bought out. Also it is during buyout that purchase orders and subcontracts are issued. This includes selection of both suppliers and subcontractors and finalizing their purchase orders or subcontracts. Unfortunately, buyouts are necessary because often due to time constraints during the bidding phase of a project, complete, meticulous analyses of bids by subcontractors may not have been made. Fig. 12.5 is a diagram showing percentage of buyouts of budget’s trade contract cost versus time.

Most construction literature ignores the issue of buyout and concentrates on addressing either estimating or project management. The process starts during the tender preparation stage, as the contractor solicits and assesses offers in the process of assembling the cost estimate. Should the contractor’s proposal be successful and the contractor is awarded the contract, the next step is to attempt to contract with the firm that submitted the best offer. Material procurement and subcontracting are typically the two distinct parts of the buyout process discussed, even though both may be the responsibility of a single department or individual.

Figure 12.5 Diagram showing percentage of buyouts (executed and committed) of budget’s trade contract cost versus time. The estimated budget in this case is $15,000,000.

Most construction professionals are familiar with the concepts of project buyout and bid shopping. Project buyout is an ethical and necessary practice conducted during the preconstruction process, which enables a general contractor to clarify scopes of work and streamline specific activities for the project. As construction professionals more fully understand the ethical issues separating the unacceptable practice of bid shopping from the ethical practice of project buyout, the efficiency and quality of the estimating and subsequent project management processes will be improved. Estimators are normally required to bear the responsibility of obtaining bids and performing project buyout while maintaining high ethical standards.

A buyout estimate is different from a bid estimate. A bid estimate is detailed to bid a project, whereas the purpose of a buyout estimate is to order materials once the project becomes a viable job for the contractor or subcontractor. A typical example of a bid estimate versus a buyout estimate would be metal studs for drywall. During the bid period, it is good enough to know the total linear footage of studs by size and gauge. A buyout however requires greater detail, for example, in addition to the bid information a buyout would require the lengths for each application. However, in mechanical and electrical scopes of work, the bid estimate and buyout estimates are very similar.

Project buyout takes place between the award of a bid to the general contractor and the issuing of subcontracts and purchase orders. While bid shopping is not illegal, it is considered an unethical practice where details of a bid are revealed to a competitor in an effort to solicit an overall lower bid. A better understanding of ethical versus acceptable construction practices can only help construction professionals identify the basic differences between bid shopping and project buyout while at the same time steering clear of unethical practices and still remain competitive.

According to Cody Andreasen, Mark Lords, and Kevin R. Miller, of Brigham Young University, “The justification, for some contractors, when arguing in favor of bid shopping is, that if a bid is revealed to another subcontractor, then a lower bid may be forth coming, which may translate into a lower overall bid on the project, benefit the owner, and thus increase the likelihood of being awarding the project. It can be argued that this is no different than shopping for a car or bartering for goods in a foreign country. However, in the auto industry there is an expectation that pricing will be disclosed to other dealers in the buying process. That expectation does not exist in the construction industry. A construction project is something yet to be built. It is not an existing product and any changes in the cost typically will affect the quality or schedule of the project. Therefore, the owner is not receiving the same product if bid shopping occurs.”

Bid shopping essentially occurs when a general contractor discloses the bid price of one subcontractor or supplier to its competitors in an endeavor to obtain a lower bid than that on which the general contractor based the original bid to the owner. However, a technique that is often used to prevent bid shopping is for a subcontractor to submit a bid at the last minute, thus preventing the general contractor receiving the bid from shopping it.

By and large, bid shopping occurs because most subcontractors being shopped believe that if they do not reduce their price they will not get the job. Additionally, if business is slow, subcontractors may be willing to accept lower profit margins just to keep their crews busy even when it means they will only break even on the project. Sometimes, the general contractor will induce a subcontractor additional work upon being awarded the job. Although it may appear that the owner is the principal beneficiary of bid shopping by receiving a lower price for the project, usually one finds that the owner also receives a lower quality project in addition to running greater risks and warranty problems down the road. The Associated General Contractors of America (AGC) describes the practice of bid shopping as “abhorrent” and is totally opposed to it. These feelings are shared by the American Subcontractors Association (ASA), which considers bid shopping and bid peddling as unethical. This view is also shared by other contractor trade associations such as the AGC, ASA, and ASC. Moreover, this viewpoint appears to be shared by the courts that have opined on bid shopping.

The main benefits of project buyout according to the Brigham Young University authors are that “Project buyout allows a period of time for the contractor to ensure that each scope of work is covered by only one subcontractor. Occasionally a contractor finds that two subcontractors submitted bids for an overlapping scope of work. Since both subcontractors do not need to perform the work, the general contractor will determine which subcontractor will perform the work for the overlapping scopes. The subcontractor that does not perform the overlapping work will generally provide a credit to the general contractor for the reduction in their scope of work. If the opposite is found and there has been work that was assumed to be included in a subcontractor’s scope of work, but was not included in the bid, the general contractor generally negotiates with a subcontractor to have the work included in their subcontract and that negotiation may increase the contract amount for the subcontractor.

Another instance where changes could be made during the project buyout process results when a subcontractor anticipated a different project schedule than the general contractor. As a result, the subcontractor may not have sufficient crews to complete the job in the time frame or manner desired by the general contractor. In this case, the general contractor may elect to use a different subcontractor to maintain the project schedule.”

Darin C. Zwick and Kevin R. Miller authors of an article entitled, Project Buyout emphasize the importance of completing the buyout process as early as possible and say, “By completing buyout early, future delays are avoided in the event that a given scope of work is difficult to buyout due to conflicts with subcontractors or suppliers. It also protects the project from price escalation.

Other tasks that occur during the buyout process by the general contractor include checking the following items to ensure that the subcontractor can perform the work for the project:

• Insurance and liability coverage

• Evidence of state Workman’s Compensation coverage

• Evidence of proper local and state subcontractor licenses

• Evidence of proper bonding requirements if required.

The expiration dates of the previous items need to be verified to prevent lapses of coverage while the subcontractor is working on the project.

Another consideration that companies need to examine during the buyout process is the financial stability of the subcontractors and vendors. During economic downturns, companies may declare bankruptcy, leaving the general contractors in a precarious situation.”

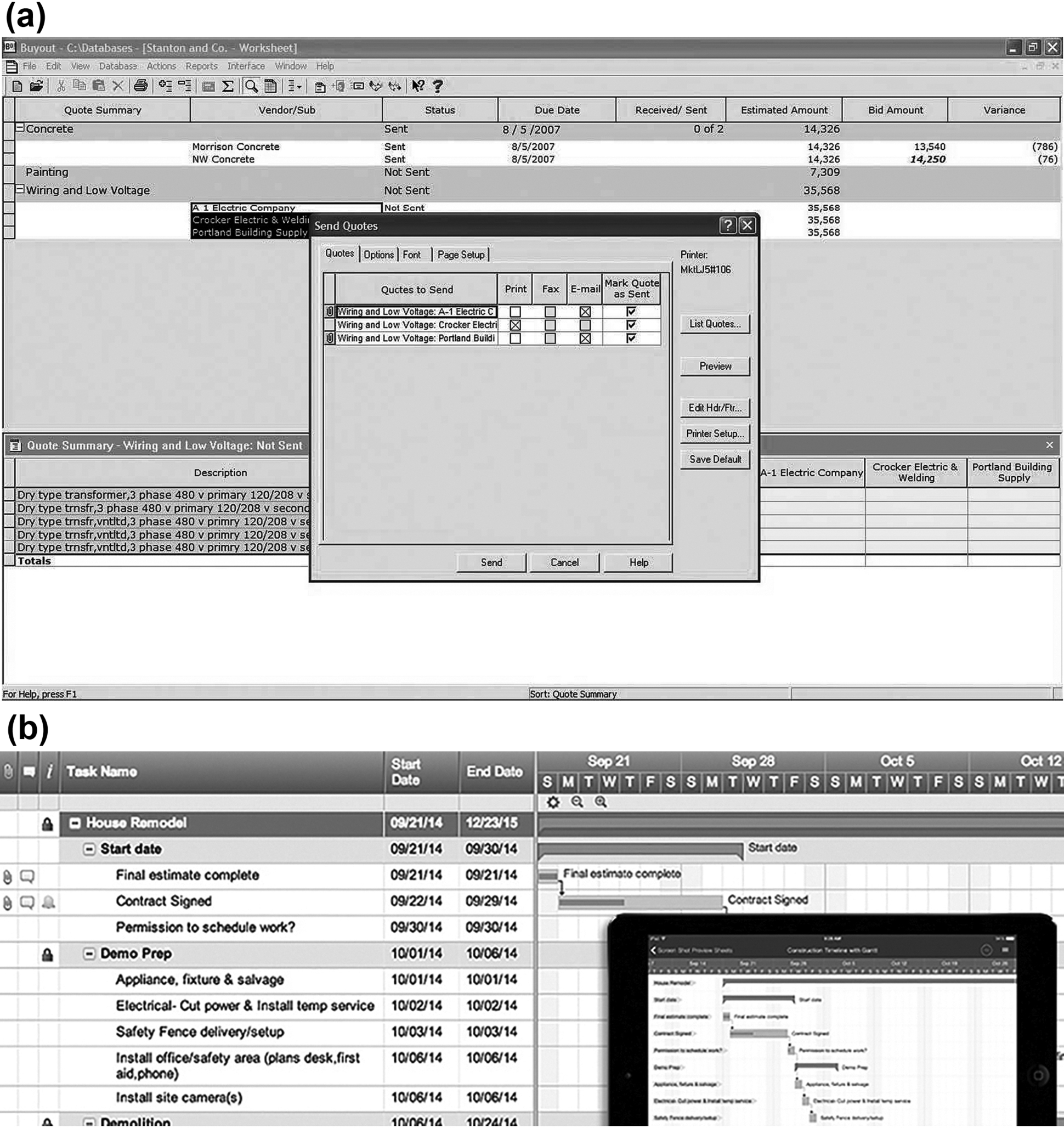

Among the main duties of the project buyout specialist is to focus on awarding scopes of work to subcontractors and to act as a liaison between field operations and subcontractors while keeping the contract amount in budget. This is particularly important because it relates to disputes and problems that often exceed field management’s ability to solve matters in a timely manner. During the preconstruction phase, this includes technical support to both the design-build and estimating departments. In addition, the buyout specialist is responsible for the acquisition of new subcontractors for all projects including cost control, adherence to corporate and contract compliance, quality control, and customer satisfaction. The project buyout specialist is also responsible for the quality and completeness of project buyout and small business utilization as well as customer relations and client satisfaction in all areas within the firm. To achieve maximum support for and from each staff member requires team building and a holistic approach. This includes setting and monitoring goals and collaborating with purchasing and operational goal setting. Over the last few years, there has been a significant wave of web and cloud apps, which are streamlining communication and simplifying and improving efficiency in construction management. For example, there are currently several proprietary buyout software packages on the market that can save time and reduce effort by automating the bid solicitation process. Buyout software also provides an important tool for determining where the project is in the buyout process at any particular moment. It can also establish the percent complete, minimize exposure, and rapidly see how the actual prices compare with the estimated costs. Moreover, it can offer access to standard cost codes, categories, and tax groups stored in various applications such as accounts payable applications. One example of such software is from Sage Software, Inc. (www.sagecre.com), which offers a software package called “Buyout” that reportedly has the following features (Fig. 12.6a):

• Builds a worksheet of material and subcontract items to be bought out automatically by reading the estimating file

• Combines multiple estimates into a single worksheet, an important feature for contractors who receive price discounts based on volume purchases

• Creates one-time items in the Buyout item window

• Views items the way you want to see them—by WBS, location, phase, material class, and so forth

• Groups materials or subcontract items for ease in obtaining prices. Create quote sheets and assign material items and subcontract items to the quote sheets

• Assigns multiple vendors and subcontractors to quote sheets

• Uses prices from Buyout’s standard price database for items in the quote sheet

• Automatically submits requests for quotes and sends purchase orders via e-mail, fax, or hard copy

• Splits items out of one quote for the creation of a new quote sheet

Figure 12.6 (a) an illustration of computer-based “buyout” software helps sort the items in an estimate into desired groups of materials, produce documents, and perform the tasks necessary to buy out a job. Amongst other features, it can automatically generate, sort, and send RFQs to suppliers, and subcontractors via e-mail, fax, or printed hard copy. It also records, tracks, analyzes, and selects bids received. One of the more important features is the ability to transfer commitments to purchasing for purchase order and subcontract generation. (b) smartsheet is a popular and effective construction management tool with excellent collaboration and communication features.

• Saves prices from the quote sheet to a Buyout standard price database

• Changes prices for any item and updates the estimating database with pricing from Buyout

• Generates Requests for Quotes (RFQs) and Purchase Orders (POs) directly from Buyout and issues them automatically via e-mail, fax, or hard copy

• Updates estimates with Buyout prices, revised quantities, and vendor/subcontractor selections.

Smartsheet is another popular spreadsheet-inspired work management tool with robust collaboration and communication features (Fig. 12.6b). The program has numerous prebuilt construction templates; likewise, it is not complicated to create a timeline, track progress, manage documents, and consolidate the details. Furthermore, with Smartsheet, Gantt charts are spontaneously created and adjust automatically whenever a change is made, thus keeping team members and stakeholders constantly up-to-date. In addition, team members can have discussions directly in the sheet and set reminders and alerts, so team members are always on the same page.

12.4. General Conditions and Supplemental Conditions

The General Conditions are among the most important documents in the project manual because it sets forth and defines the rights and responsibility of the different parties, particularly the owner and contractor in the construction process as well as the specific terms of the contract. It also specifies and defines the surety bond provider, the design professional’s role, authority, and responsibilities, and the requirements governing the various parties’ business and legal relationships. These conditions are “general” and can apply to almost any project. It is vital that the contractor knows exactly what is contained in this section.

It should be noted that many trade and professional organizations have developed their own standard documents and general conditions. The most widely used may be those published by the American Institute of Architects (AIA), specifically AIA Document A201. This document has been well tested in the courts and is familiar to most contractors. The ConsensusDOCS 200, Standard Agreement and General Conditions between Owner and Contractor, is also widely used. Likewise, ConsensusDOCS 410, Agreement and General Conditions between Owner and Design-Builder [Cost of Work Plus Fee with Guaranteed Maximum Price (GMP)] is sometimes used. There are a number of standard clauses that typically appear in the general conditions. Below are some of the main standard clauses that typically appear in the General Conditions with a brief description of each (Bear in mind that they may vary depending on the type of general conditions contract):

Definitions and General Provisions: This clause provides definitions for the purpose of the Contract Documents relevant to the contracts, the work, and the drawings and specifications. It also clarifies the ownership, use, and overall intent of the contract documents.

Owner Responsibilities: This section defines the information and services that the owner is required to supply. It also defines the owner’s rights and responsibilities and the owner’s right to stop or carry out the work.

Contractor General Obligations and Responsibilities: This section lays out the obligations of the contractor regarding construction procedures and site operations, employees, labor and materials, warranty, taxes, permits, fees and notices, schedules, samples and product data, and cleaning up. This clause essentially states that the Contractor is required to execute and complete the Works and remedy any defects therein in strict accordance with the Contract, with due care and diligence and to the satisfaction of the Architect, and shall provide all labor, including the supervision thereof, materials, and all other things, whether of a temporary or permanent nature. The Contractor shall also take full responsibility for the adequacy, stability, and safety of all site operations and methods of construction, but the Contractor shall not be responsible, unless expressly stated otherwise in the Contract, for the design or specification of the Permanent Works or of any Temporary Works prepared by the Architect.

Administration of the Contract: This section describes the duties, responsibilities, and authority of the architect for the administration of the contract. Specific clauses are included dealing with the architect’s responsibility for making periodic site inspections and issuing periodic reports to the owner or lender. This section also deals with issuing modifications in drawings and technical specifications and assisting the Contractor in the preparation of change orders and other contract modifications, as well as assisting in inspections, signing Certificates of Completion, and making recommendations with respect to acceptance of work completed under the contract. The Architect is also required to review detailed drawings and shop drawings, price breakdown, and progress payments estimates as well as how requests for additional time, claims, and disputes will be handled.

Preconstruction Conference and Notice to Proceed: This section deals with the procedures to conduct a preconstruction conference to acquaint the different parties with one another. For example, within 10 calendar days (or as stated in the contract documents) of contract execution, and prior to the commencement of work, the Contractor shall attend a preconstruction conference with representatives of the Owner, Architect, and other interested parties and stakeholders. This clause requires that the contractor can only begin work upon receipt of a written Notice to Proceed from the Owner or designee. The Contractor may not begin work prior to receiving such notice.

Availability and Use of Utility Services: This section deals with the availability of utility services. Here the Project Owner shall ensure that all reasonably required amounts of utilities are available to the Contractor from existing outlets and supplies, as specified in the contract. Unless otherwise provided in the contract, the amount of each utility service consumed shall be charged to or paid for by the Contractor at prevailing rates charged to the Owner.

Assignment and Subcontracting: This section deals with the assignment and awarding of subcontracts by the general contractor for portions of the work. This clause generally states that the Contractor shall not, except after obtaining prior written approval of the Project Owner, assign, transfer, pledge, or make other disposition of the Contract or any part thereof or of any of the Contractor’s rights, claims, or obligations under the Contract. In the event the Contractor requires the services of subcontractors, the Contractor shall also obtain prior written approval of the owner for all such subcontractors. The approval of the Owner does not relieve the Contractor of any of his obligations under the Contract, and the terms of any subcontract shall be subject to and be in conformity with the provisions of the Contract.

Construction by Owner or Others: This clause deals with the owner’s right to perform some of the construction work with his/her own forces or to award separate contracts to other parties besides the general contractor. The Contractor shall in accordance with the requirements of the Architect/Project Manager and the contract affords all reasonable opportunities for carrying out portions of the work by the owner or to any other contractors employed by the owner and their workmen or the owner’s workmen who may be employed in the execution on or near the Site of any work not included in the Contract or of any contract which the Owner may enter into in connection with or ancillary to the Works.

Permits and Codes: This section basically states that the Contractor shall give all notices and comply with all applicable laws, ordinances, codes, rules, and regulations. Before installing the work, the Contractor shall examine the drawings and the specifications for compliance with applicable codes and regulations bearing on the work and shall immediately report any discrepancy it may discover to the Architect/Project Manager.

Change Orders: This section explains how changes are authorized and processed according to the relevant clauses of the contract. Changes orders are one of the areas of greatest contention between the owner and the contractor. Generally, the Architect may instruct the Contractor, with the approval of the Owner and by means of Change Orders, all variations in quantity or quality of the Works, in whole or in part, that are deemed necessary by the Architect. Processing of change orders shall be governed by appropriate clauses of the General Conditions.

Construction Progress Schedule: Time is always a pivotal factor on any project. Project schedules depict project start-up, progress, and anticipated completion dates. It also addresses issues associated with delays and extensions of time to the contract. For example, schedules shall take the form of a progress chart of suitable scale to indicate appropriately the percentage of work scheduled for completion by any given date during the construction period.

Progress Payments: This section specifies how applications for progress payments are to be processed. It states that the Owner/Lender shall make progress payments approximately every 30 days as the work proceeds, on estimates of work completed and which meets the standards of quality established under the contract, as approved by the Project Manager/Architect. Before the first progress payment can be processed under this contract, the Contractor shall furnish a breakdown of the total contract price showing the amount included therein for each principal category of the work, which shall substantiate the payment amount requested to provide a basis for determining progress payments. This section also deals with the withholding of payments and failure to pay issues.

Protection of Persons and Property: This section is intended to address issues relating to safety of both the project owner’s property and the people on the project. It deals with specific issues such as the handling of hazardous materials and emergencies, as well as overall safety programs and requirements. The Contractor shall (unless stated otherwise in the contract) indemnify, hold, and save harmless and defend at his/her own expense the project owner, its officers, agents, and employees from and against all suits, claims, demands, proceedings, and liability of any nature or kind, including costs and expenses, for injuries or damages to any person or any property which may arise out of or in consequence of acts or omissions of the Contractor or its agents, employees, or subcontractors in the execution of the contract.

Insurance of Works and Bonds: This section deals with insurance (including liability insurance) and bonding requirements of the various parties and which should cover the period stipulated and also cover the Defects Liability Period for loss or damage arising from a cause occurring prior to the commencement of the Defects Liability Period and for any loss or damage experienced by the Contractor in the course of any operations carried out for the purpose of complying with the contract obligations.

Examination of Work Before Covering Up: This clause has to do with acceptance of the work by the architect (as agent of the owner). It stipulates how and when the contractor is responsible for uncovering and/or correcting any work deemed unacceptable. Therefore, no work shall be covered up or put out of view without the prior approval of the Project Manager/Architect. The Contractor shall afford full opportunity for the Project Manager/Architect to examine and measure any work which is about to be covered up or put out of view and to examine foundations before permanent work is placed thereon. The Contractor shall give due notice to the Project Manager/Architect whenever any such work or foundations is ready for examination and shall without unreasonable delay advise the Contractor accordingly to attend for the purpose of examining and measuring such work.

Clearance of Site on Substantial Completion: This section essentially stipulates that upon the substantial completion of the Works the Contractor shall clear away and remove from the Site all rubbish, constructional plant, surplus materials, and temporary works so as to leave the whole of the site and works clean and in a workman-like condition to the satisfaction of the Project Manager/Architect.

As-Built Drawings: “As-built drawings,” as used in this clause, refers to drawings submitted by the Contractor or subcontractor at any tier to show the construction of a particular structure or work as actually completed under the contract. “As-built drawings” shall be synonymous with “Record drawings.”

Miscellaneous Provisions: This section deals with various matters such as liquidated damages, taxation, disputes, prohibition against liens, warranty of construction, energy efficiency and other green issues, waiver of consequential damages, etc.

Termination/Suspension of the Contract: Either party has the right to terminate the contract under certain conditions. The conditions under which the parties may terminate or suspend the contract are clarified in this clause. For example, the Contractor shall on the written order of the Architect/Project Manager suspend the progress of the Works or any part thereof for such time or times and in such manner as required by the Architect/Project Manager and shall, during such suspension, properly protect and secure the Works as specified by the Architect/Project Manager. The Project Owner should be notified and written approval sought for any suspension of work in excess of 3 days.

12.4.1. Supplemental Conditions

These are special conditions also known as supplementary general conditions, special provisions, or particular conditions, that normally deal with matters that are project specific and which are beyond the scope of the standard General Conditions. These sections may either add to or amend provisions in the general conditions. Examples of project-specific information that may appear in the supplemental conditions include:

• Safety and protection requirements

• Scheduling

• Contractor’s bond requirements

• Bonus payment information

• Defects liability period

• Cost fluctuation adjustments

• Progress payment retainage

• Services provided by Owner

• Temporary facilities provided by Owner

• Owner provided materials

• Cleanup and restoration.

12.5. Contingencies and Allowances

There are many definitions for a “Contingency”. For example, The Association for the Advancement of Cost Engineering defines contingency as “An amount added to an estimate to allow for items, conditions, or events for which the state, occurrence, or effect is uncertain and that experience shows will likely result, in aggregate, in additional costs.” David H. Hart, AIA, describes contingency as “a predetermined amount or percentage of the contract held for unpredictable changes in the project.” He goes on to say, “A contingency is a helpful risk management tool that financially prepares owners for addressing risk within the project.”

From the above, it is clear that contingencies are generally necessary to cover unknowns, unforeseen, and/or unanticipated conditions or circumstances that are not possible to adequately evaluate or determine from the information on hand at the time the cost estimate is prepared. Contingency allocations specifically relate to project uncertainties of the current known and defined project scope and that may arise and are not a prediction of future project scope or schedule changes. The amount of contingency allocated relates to the amount of assessed risk and should not be reduced without appropriate supporting justification. Furthermore, inclusion of a contingency amount in the cost estimate mitigates the impact of cost increases inherent in an overly optimistic estimate and provides for the opportunity of an earlier discussion of how to address potentially adverse circumstances.

Contingencies in a project budget represent the degree of risk within the estimate and are traditionally calculated as an across-the-board percentage addition on the base estimate, typically based on initial estimates, previous experience, and historical data. This estimating approach has serious flaws because it is generally illogically arrived at and therefore often not appropriate for the project at hand. Moreover, this method of arbitrary contingency calculation is difficult for an estimator to justify or defend. A percentage addition results in a single-figure prediction of estimated cost, which is often unjustified because it does not reflect reality nor does it encourage creativity in estimating practice.

Examples of typical contingency types normally found in budgets and that should be considered when major projects are involved:

• The Owner’s Contingency: It is virtually impossible to produce a perfect set of construction documents, leaving room for miscalculations and omissions, which is why applying a standard amount to each project can lead to cost overruns, accusations, and litigation. And it is very important to adequately establish an allowance of the right size, that is neither too low nor too high. An owner’s program almost always changes, if only marginally, during the life of a project, and changes or modifications to the scope of work typically occur in response to internal programmatic changes. The contingency is one way to mitigate the impact of changes in scope or errors and omissions.

• Construction contingency is basically used to cover cost growth during construction. It is a percentage of construction cost held by the PM to resolve issues during construction, which is why it should not be used until the project is in the construction phase. Having a contingency for the contractor’s needs will vary with the type of delivery method. This contingency will be higher for renovations in older buildings, buildings with complicated site conditions, or in complex projects. The construction contingency is contained in the contractor’s GMP but the PM must approve use of these funds prior to being committed by the general contractor.

• Design contingency is for changes or modifications during the design process for such factors as incomplete scope definition and inaccuracy of estimating methods and data. Design contingency amounts are based on the amount of design completed and are a percentage of construction cost held to represent the completeness of the design. The design contingency is understandably higher during the early phase of the project’s design. As the design is completed and the scope of work is more defined, this contingency is reduced until it becomes zero in the cost element at the completion of the permit phase.

• Project contingency is a percentage of project cost retained for risks in other project costs such as professional fees, hazardous materials abatement (e.g., asbestos), communications wiring, etc. Money allocated as contingency in the project budget should not be utilized for additional scope or other changes to the project once the design is completed.

• Program contingency is optional and may be employed to cover scope or program changes requested by the User Group or owner. An alternative to this contingency is to have the General Contractor carry an allowance line item in the GMP contract.

• Various other contingencies for areas or items that may show a high potential for risk and change, i.e., environmental mitigation, utilities, highly specialized designs, etc.

12.5.1. Construction Contingencies

As previously mentioned, the construction contingency is essentially a set percentage of the construction contract amount budgeted for unexpected and unforeseen emergencies or design shortfalls identified after a construction project has commenced. When underwriting a commercial construction loan request, it is prudent to analyze the four major elements of the total construction cost which are the land cost, the hard costs, the soft costs, and the contingency reserve. Since there are always cost overruns in almost any commercial construction process, a contingency reserve is put in place to build in a cushion in the project’s construction budget to cover these cost overruns. And while there is no specific formula for computing a contingency reserve, many underwriters feel comfortable using 5% of the construction estimate/bid for new construction (although in complicated projects the contingency can be as high as 10%) and 7% of the construction estimate/bid for remodeling/renovation projects. The land costs are not included because it is usually known in advance and is fixed. It is therefore unlikely that there will be a cost overrun connected to the purchase of the land itself.

A construction contingency is included in the budget to allow the project to proceed with minimal interruption for small or insignificant (nonscope) changes or cost overruns. The typical construction contract will include a specific completion date or specific number of working days to complete, and the contractor can be required to pay liquidated damages if the work is not completed within this specified period. At the same time, the contractor is entitled to proceed with the work without undue interruption. To minimize delays due to external causes, the client must be capable of implementing minor (i.e., nonscope) changes without causing any administrative delay.

Whatever the case, changes are always likely to occur on construction projects. The owner must therefore ensure that an appropriate contingency is included to cover the costs of any changes in the scope of a project, such as adding upgrades, additional equipment or perhaps enlarge the footprint of the building. Moreover, financing costs may change with the market. A small contingency may be sufficient to cover final documentation of drawings by designers, but the owner should plan for a construction contingency of roughly 3% to cover the changes in market conditions, and potential variances.

The objective of contingency planning is to determine a confidence value by means of a percentage in potential cost and schedule growth. The contingency value is an indicator of the level or degree of project development, and typically, the less defined a project, the higher the contingency value. Issues such as scope definition and quality assurance have a significant impact on confidence, risks, and resulting contingency development. In determining a contingency value, consideration must be given to the details and information available at each stage of planning, design, and construction for which a cost estimate is being prepared.

As previously mentioned, most construction budgets contain an allowance for contingencies or unexpected costs occurring during construction. This contingency amount may either be included within each cost item or be included as a single category in the construction contingency. The estimated amount of contingency to be retained is based on historical experience and the anticipated difficulty of a particular construction project. For example, one construction firm places estimates of the anticipated cost into five specific categories. These are:

• Design development changes,

• Schedule adjustments,

• Differing site conditions for those expected, and

• Third-party requirements imposed during construction, such as new permits.

Any contingent amounts not disbursed during construction process can be released toward the end of construction to the project owner or alternatively used to add additional project elements. The construction cost process consists of two essential components, Hard Costs and Soft Costs.

Hard Costs are considered to be by far the largest portion of the allocated expenses in a construction budget and generally consist of all of the costs for physical items and visible improvements (i.e., actual construction costs incurred to build the project), line items including site preparation (grading/excavating), concrete, framing, electrical, carpentry, roofing, and landscaping. Hard costs are often referred to as the bricks and mortar expenses. In some cases, it may include the land, but that particular cost is usually separated to find out the actual construction expenses.

Soft Costs are the nonphysical expenses and involve all of the other fees involved in the completion of the project. Typical soft costs include architecture and engineering fees, as well as soft costs transfer taxes, origination points, mortgage insurance (if applicable), overhead expenses, attorney fees, professional fees, permits, title insurance, appraisal fee, testing, hazard insurance, marketing, construction insurance, etc. Another primary soft cost category if applicable is that of fixtures, furnishing, and equipment (FF&E). Soft costs can also be expenses that continue even after a project is completed, such as building maintenance, insurance, security, and other ongoing fees needed for an asset’s upkeep. One soft cost that has in recent years become much more prevalent is LEED certification for commercial real estate projects, particularly as more municipalities are offering incentives for green buildings and developers recognize the long-term savings from owning sustainable assets. Generally speaking, the soft costs are estimated as a percentage of the total project budget during the planning stages of a project. And as the planning and design of a project progresses, the soft cost contingency percentage can be increased or decreased.

To arrive at the total cost of a commercial construction project, one must include the hard costs, soft costs, the cost of land, as well as the contingency reserve, which for new construction is generally about 5% of the TPC.

Design professionals are able to establish a project costs estimate by the employment of several methods. For example, one approach is to use estimates whose development is based on project parameters and major cost elements, or which are based on an analysis of historical bid data, actual cost, or a combination of these methods. But whatever method is used, in the final analysis, special care must be taken to ensure that the capital cost estimate undertaken is complete and is realistic and not over optimistic. Underestimation of project construction and related costs is one of the more common problems faced in the economic analysis and budgeting of a project. Contingency funding is a fiscal planning tool that is used to help manage the risk of cost escalations and cover potential cost estimate shortfalls. Inclusion of a contingency amount in the cost estimate will mitigate the adverse impact of cost increases inherent in an overly optimistic estimate and provide an opportunity for an earlier discussion of how potential circumstances can be addressed.

Having an overall management contingency is strongly advised for large projects. This contingency is usually a “stand-alone” amount of the cost estimate that is managed by an executive and used for a broad array of uncertainties and potential risks. Some of the Project Oversight Management contingency allowance will be disbursed to manage costs, manage the approved budget and schedule deviations, address adverse impacts caused by modifications, and for initiatives being analyzed or implemented to address or mitigate potential cost overruns or schedule delays.

Management of the transfer of costs to and from contingency and allowance line items needs to be administered and tracked carefully to allow decision-makers to take appropriate action. Cost transfers should correspond to the major component type of cost escalation. Thus if a proposed work is clearly outside of a well-defined scope but is found to be essential to the well-being of the project and can be readily justified, then a management decision can be made to disburse payment for the added work or change order from either the management contingency or another appropriate contingency. On the other hand, if there are distinct fees or FF&E issues that have a fees or FF&E contingency, careful tracking of these particular contingencies can help the PM and management to better analyze potential cost overruns. The rationale for supporting contingency transfers should be noted and incorporated into all relevant reporting. This is to allow a periodic comparison analysis of available contingency amounts to establish contingency usage rates. This analysis will alert project managers if potential problems exist as well as confirm if a reasonable and sufficient amount of contingency remains to keep the project within the latest approved budget.

Construction cost estimates should not be presented as a lumpsum total, but rather as the sum of costs for each major element of the project. The contingency allowances can be clearly identified as individual line items associated with each major element. This allows the PM and reviewers of future updates to track where and how project costs are changing and how they may impact the completion of the project. This may be achieved by providing information on reoccurring patterns and reasons behind cost escalation. Contingencies are normally disclosed as a dollar value or a percent of the major element cost.

12.5.2. Budget Allowances

Budget Allowances are generally similar to contingencies in that their purpose is to reserve funds for circumstances that are ill-defined and thus more prevalent in the earlier design phases of a project when the uncertainties are most evident. However, unlike contingencies, Allowances are usually identifiable single items/issues and are placed in budgets as individual line items. Certain Allowances may also be carried by the General Contractor upon attaining the approval of the PM and provided they do not exceed their budgets or estimates to cover such items that they believe may arise (based on prior experience). Furthermore, as an optional allowance, the General Contractor may also carry a contingency to cover scope or program changes that the User Group/Owner may request during construction. This Allowance is an agreed upon amount between the Contractor and the PM and must be approved by the PM prior to being committed by the Contractor. The PM can carry Allowances in any of the Cost and Time Summary categories for questionable or additive alternate construction and nonconstruction items as necessary.

In discussing allowances, Sabo & Zahn, Attorneys at Law state that “An allowance is a line item in a construction budget that serves as a placeholder during the bidding and initial construction contract phase. It is used when a particular item to be used in the construction has not been picked or completely specified. For example, if the carpeting has not been selected at the time of bidding, rather than delay the bidding, an allowance for the carpeting can be used. Normally, in this situation the total amount of carpeting to be used is known. If, for instance, the house will have 300 yards of carpeting, with a $50 per square yard allowance, the contractor will include a carpet allowance of $15,000 in the bid. This allowance will cover the cost of the materials as well as the cost of installation. The contractor will also have its overhead and profit included in the proper category. At some later date, the owner will pick the actual carpeting. If the actual cost for that carpeting is $60 per yard, then the contractor will be entitled to a change order for the increased cost—in this example, $3000. On the other hand, if the actual cost of the carpeting turns out to be only $40, then the change order will reflect a deduct of $3000.

The key to properly administering allowances is to account for them by proper change orders. At the time that the actual material is selected and approved by the owner, a change order must be issued and signed. This change order must indicate that the allowance for that item is being deleted, with a credit to the contract for the allowance amount, with a corresponding increase in the construction cost in the amount of the actual cost. In our example with a $60 carpet cost, the allowance of $15,000 would be credited to the owner and the $18,000 actual cost would be added to the contract, for a net increase of $3000.” However, the best practice is not to provide any allowances if possible, but instead ensure that everything is clearly identified and specified prior to solicitation of bids.

In this respect, the allowance section of AIA Document A201-1997 states that, “The Contractor shall include in the Contract Sum all allowances stated in the Contract Documents. Items covered by allowances shall be supplied for such amounts and by such persons or entities as the Owner may direct, but the Contractor shall not be required to employ persons or entities to whom the Contractor has reasonable objection.”

The AIA Document A201-1997 also states that, “Unless otherwise provided in the Contract Documents:

1. allowances shall cover the cost to the Contractor of materials and equipment delivered at the site and all required taxes, less applicable trade discounts;

2. Contractor’s costs for unloading and handling at the site, labor, installation costs, overhead, profit and other expenses contemplated for stated allowance amounts shall be included in the Contract Sum but not in the allowances;

3. whenever costs are more than or less than allowances, the Contract Sum shall be adjusted accordingly by Change Order. The amount of the Change Order shall reflect (1) the difference between actual costs and the allowances under Clause 3.8.2.1 and (2) changes in Contractor’s costs under Clause 3.8.2.2.”

The AIA document further stipulates that materials and equipment under an allowance shall be selected by the Owner within sufficient time to avoid causing delay to the Work. This means that if the additional time caused by the delay is sufficiently significant, the contractor may be entitled to additional compensation due to that delay.

12.6. Green Project Cost Management

Optimum results are most often achieved when the project’s activities are integrated and costs are managed collaboratively. The integrated project team should always be engaged at the earliest phases of design, using target costing, value management, and risk management. Owners/developers are sometimes tempted to put in place a guaranteed maximum price on the project before the design stage is complete, but this should be resisted to ensure quality and functionality for the building owner or stakeholder. If the project owner comes under pressure to seek a fixed price at an earlier stage of the process, it would be prudent to agree on an incentive scheme for the sharing of benefits. It goes without saying that the owner should have a clear understanding of actual construction costs, both hard and soft costs. Likewise, the owner and project manager must be able to identify and differentiate between underlying costs and risk allowances in addition to being able to distinguish between profit and overhead margins.

12.6.1. Successful Cost Management Procedures

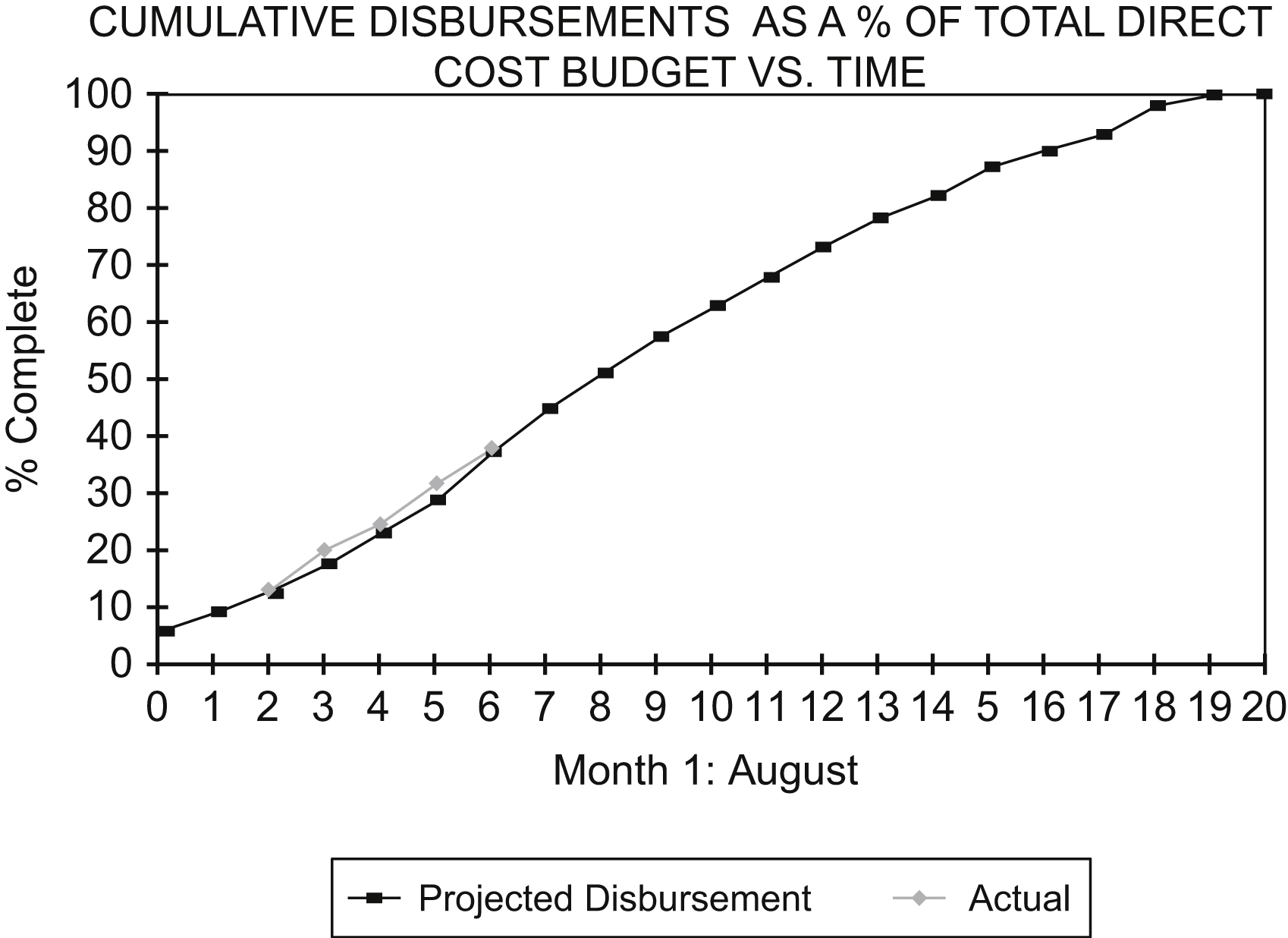

The project manager (PM) is generally responsible for management of the running and overall cost of the project and who in turn reports regularly to the owner (or lender, depending on the contract documents). One of the project manager’s responsibilities is to maintain ongoing reviews of designs as they develop and provide advice on costs to the integrated project team as well as receive feedback from the project team. This continuous cost oversight is of particular benefit in assessing individual decisions and is especially useful on large and complex schemes. It may also prove useful to schedule in periodic formal assessments of the whole scheme, as budgetary estimates, at each phase of the project (Fig. 12.7). The roles and responsibilities and limits of authority for the project manager’s role should be clearly agreed upon at the start of the project, so that everyone knows exactly what the PM is empowered to do in managing project costs and cost overruns.

The UK Office of Government Commerce indicates that the main ingredients for successful project cost management are:

• to manage the base estimate and risk allowance

• to operate change control procedures

• to produce cost reports, estimates and forecasts. The project manager is directly responsible for understanding and reporting the cost consequences of any decisions and for initiating corrective actions if necessary

Figure 12.7 An example of a cumulative disbursements schedule as a percentage of total direct cost budget versus time and based on the current project budget and 20.5-month construction period. The CM’s projection of disbursements is shown plotted in the graph and generally follows a realistic “S” curve. The project’s cumulative net direct cost disbursements to date indicate being roughly in line with initial budget estimates.

• to manage expenditure of the risk allowance

• to initiate action to avoid overspend

• to issue a monthly financial status report.

Additionally, the cost management objectives during the construction phase include delivery of the project at the appropriate capital cost using the value criteria established at the project’s inception and ensuring that throughout the project, comprehensive and accurate accounts are kept of all transactions, payments, and changes.

Likewise, the UK Office of Government Commerce also believes that the chief areas that cost management teams should consider during the design and execution of a construction project are:

• Identifying elements and components to be included in the project and constricting expenditure accordingly.

• Defining the project program from inception to completion.

• Making sure that designs meet the scope and budget of the project and delivering quality is appropriate and conforms to the brief.

• Checking that orders are properly authorized.

• Monitor all expenditure relating to risks to ensure that it is appropriately allocated from the risk allowance and properly authorized. Also monitor use of risk allowance to assess impact on overall outturn cost.

• Maintaining strict planning and control of both commitments and expenditure within budgets to help prevent any unexpected cost over/under runs. All transactions are to be properly recorded and authorized and where appropriate, decisions are justified.

12.6.2. Risk Allowance Management

It should be no surprise that the construction business can be very risky for the owner as well as the contractor; this is due mainly to the plethora of risks caused by unexpected and noncontrollable issues, explaining why risk allowances are needed to be put in place. Risk allowances should be managed by the party that is in the best position to manage the risks, which is usually the project owner or someone representing the owner, with the advice and support of the project manager. What risk allowance management essentially consists of is a procedure to move costs out of the risk allowance column into the base estimate for the project work either as risks materialize or actions taken to manage the risks. Formal procedures are required to be put in place for controlling quality, cost overruns, project delays, and change orders. Risk allowances should not be disbursed unless the identified risks to which they relate actually occur. When risks occur that have not previously been identified, they should be treated as change orders to the project. Likewise, risks that materialize but have insufficient risk allowance allocated for them should also be treated as change orders (variation orders).

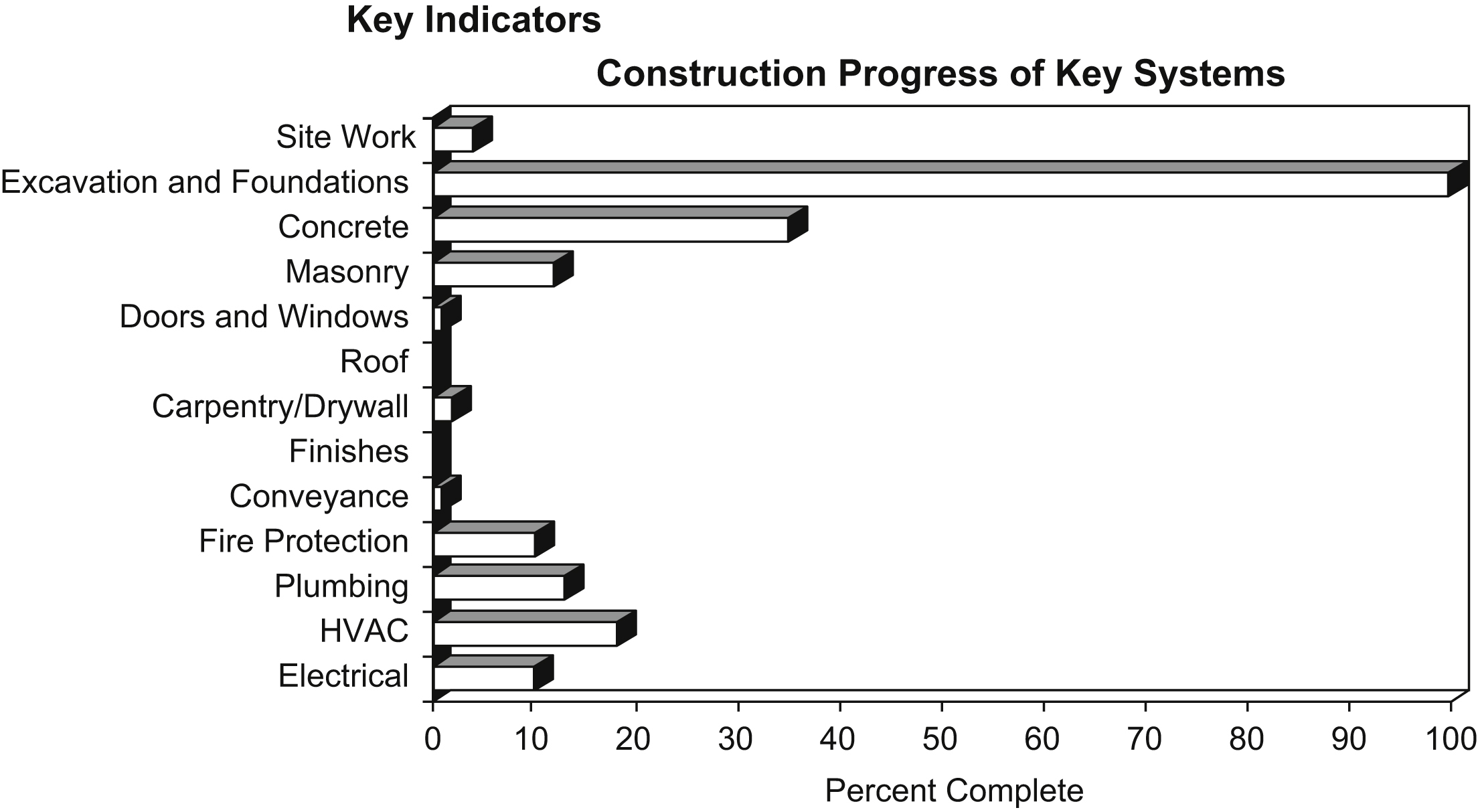

Fig. 12.8 is a graph that is designed to assist the PM and owner in monitoring the key elements of the project as well as present an overall picture of how the project is progressing. It should be noted that the graph is to be supplemented with notes for each key element. For example, “Site Work: The site has been cleared. The north waterline connection, and two (2) north and two (2) south sanitary connections have been installed and stubbed through the foundation wall. Electrical connections to the temporary switchgear have been made. A temporary concrete sidewalk has been placed along Washington Avenue.”

It is always preferable to define potential risks by allocating specific costs to them, as opposed to just inflating the total cost to compensate for inadequate early planning. A risk-allocated cost contingency is normally needed and included in the TPC estimate to help mitigate potentially significant risks. Risk management and contingency funding is particularly useful for mitigating those risks that cause cost escalations and project cost overruns during the course of a project’s execution.

Figure 12.8 Graph designed to assist the Project Manager and Owner in monitoring the key elements of the project as well as present an overall picture of how the project is progressing.

In the process of preparing the initial project budget, it is strongly recommended to perform a risk assessment on the entire project to identify and quantify the potential risk areas and types. This will help mitigate the uncertainties and help create a conservative cost expectation. Risk assessments should also be performed on a regular basis throughout the project’s execution and to update contingency amounts. Examples of risk assessment areas that may cause concern include failure to perform, analysis of heterogeneous or irregular site conditions, utility impacts, hazardous materials, environmental impacts, third-party concerns, etc. When quantifying risk as a contingency amount, expectation of occurrence, severity, and anticipated dollar value are variables that may be considered and utilized. After all known risk mitigation, the budget’s cost estimate contingency allowance levels should reflect the actual amount of remaining risk associated with the project’s major cost elements. An overall management contingency can also be included to cover unknown, unanticipated risks.

Risks and risk allowances should normally be reviewed and evaluated on a regular basis, particularly when formal estimates are prepared, from the design, construction phases through substantial completion and occupancy. The introduction of changes after the briefing and outline design stages are complete should be avoided as much as possible. Change orders can be minimized by ensuring that from the start of the project the contract documents are as clear, complete, and comprehensive as possible and that it has been approved by the stakeholders. This may require early meetings with planning authorities to discuss their requirements and to ensure that the designs are adequately developed and coordinated before construction begins. For renovation of existing buildings the type of risks may differ slightly and may require site investigations or condition surveys.

12.6.3. Cost Planning

Over the years, we have witnessed many ups and downs in the construction industry. During economic downturns, the construction industry experiences more than its fair share of bankruptcies. Many of these bankruptcies could have been prevented had the project owner and Project Manager taken adequate precautions. Perhaps the primary cause of bankruptcies is due to inadequate cash resources and failure to convince creditors and the main project lender (if the project is financed) that this inadequacy is only temporary. The need to forecast cash requirements and a project’s expected cash flow (i.e., transfer of money into or out of the firm) is important for the project to succeed, particularly if there are cost overruns, economic recession, etc. Cash flow planning can take many forms but is necessary as there will always be a time lag between an entitlement to receive a payment for work executed and actually receiving it.