9. Loans You Don’t Want to Get—or Give

High-rate loans were once the province of loan sharks, who worked on a fairly simple business plan: Pay us back, or we’ll break your kneecaps.

Today, however, high-rate loans are big business. Even after regulatory crackdowns reduced their numbers, there are still more payday loan outlets in the United States than there are McDonald’s restaurants. Attracted by the 400%+ annual interest rates these outfits charge, many big banks have gotten into the act by funding or owning payday lending arms. Other high-rate lenders are easy to find, as well. Title lenders and rent-to-own outfits can be found in most communities or quickly located on the Internet.

All are capitalizing on people’s desire for quick cash, regardless of the cost. Most target low-income working people who may feel they have limited options and who often don’t fully understand what they’re paying for these loans. Instead of a short-term solution, these loans often spiral into a long-term problem.

Here are some of the ones you should avoid:

Payday loans. Let’s say you need $100 on the 1st, but you don’t get paid until the 15th. Your local payday lender is happy to give you the money—in exchange for a fee of $15 or so. You write a postdated check for the amount you want plus the fee, and the payday lender promises not to cash your check until the 15th.

What you might not realize is that the fee you’re paying for that short-term loan represents an annualized interest rate of about 400% for a two-week loan. And if you “roll over” the loan—delay repayment for another two weeks in exchange for another fee—the amount you pay for that $100 loan can quickly spiral even higher. Many people find themselves in this vicious cycle, when what they thought would be a short-term loan stretches for weeks or months because they can’t pay back the original amount.

Rent-to-own deals. Whether you’re buying a television, computer, or sofa, rent-to-own stores will make sure you pay a substantial premium for paying over time. A television that retails for $400, for example, might cost you 78 weekly payments of $20, or a total of $1,560. If you saved the same $20 a week for five months, you could pay for the TV in cash—clearly a much better deal.

Title or “pink slip” loans. These loans are secured by the value of your car, and you’re required to hand over your title and often a spare set of keys to get the money. If you don’t pay back the loan within the allotted time frame, typically 30 days, you may be allowed to “roll over” the loan—or the lender may simply take your car. Think about that: You may have borrowed only $250 or $500, but the lender may get a car worth thousands of dollars. That’s why one consumer advocate has denounced such repossessions as legalized theft. The fact that you’re paying annualized interest rates of 290% or more just adds insult to potential injury.

Direct-deposit advances. If you have your paycheck deposited directly into your checking account, your bank may offer the “opportunity” to borrow against your next check. These advances come at a pretty steep price, however. Wells Fargo Bank, for example, charges $1.50 for every $20 you borrow. If you take a week to pay back the money, that’s an annualized percentage rate (APR) of nearly 400%; if you take the full 35 days allowed to repay, the APR is still close to 100%.

Unfortunately, as with other high-interest, short-term loans, many people don’t repay on time and wind up taking out advance after advance.

Refund anticipation loans. This was really big business for awhile—until the IRS stopped cooperating.

Here’s how it worked. A tax preparer filled out your return and then gave you a check on the spot (or within a couple of days) for an amount equal to your refund, “minus a few fees.” Those fees ate up as much as a third of your refund, however, and they represented another high-rate loan for a short-term debt.

People who used the service often didn’t realize that with electronic filing and direct deposit, they could get their tax refunds within 10 to 14 days. That’s what the tax preparer was doing—using e-file and direct deposit to speed the money along.

So for the “privilege” of not waiting those two weeks, you paid an average of 222% on a $1,980 refund loan, according to the National Consumer Law Center, which surveyed providers of refund anticipation loans.

To make these loans, though, the banks that worked with tax preparers needed some indication from the IRS that the refunds weren’t going to be held up or seized for unpaid taxes, defaulted student loans, or other debts. Otherwise, making the loans was too risky.

Consumer advocates attacked the IRS for cooperating with these high-rate lenders. In 2011, the IRS finally took the hint and decided to stop telling banks whether or not a refund would come through.

Some tax preparers are now offering “refund anticipation checks,” which aren’t loans but instead are intended as a way to get refunds quickly to people who don’t have regular bank accounts or who don’t want to pay a fee up front for tax preparation. Instead, the programs set up temporary bank accounts to receive the electronically deposited refund, and then issue the customer a check or a prepaid card, minus any fees. If the tax preparation fee is reasonable and you aren’t being charged other fees for the privilege, refund anticipation checks may be an okay deal if you don’t have a bank account. Otherwise, just opt for direct deposit.

Pawnshop loans. Whether the cost of a pawnshop loan is outrageous or merely expensive depends in large part on the laws in your state. Some limit pawnshop interest to around 25% a year; others allow shops to charge that much per month. “Storage” and “setup” fees can increase the toll.

Pawnshops have a high rate of default: About one in five items used as loan collateral is never reclaimed. If you’ll be parting permanently with the item anyway, consider selling it on eBay or to a dealer.

Buy here pay here lots. These outfits got a big boost from the pullback in subprime lending. After the financial crisis, people with bad credit had a tough time getting auto loans. “Buy here pay here” lots stepped into the breach, offering older, high-mileage cars at big markups and 20%+ interest rates. Many borrowers end up unable to make their outsized payments, so the lots can repossess the cars and sell them again. Because buyers are often required to come to the lot to make their monthly payments, it’s easier for the dealers to keep tabs on them, which makes repossession easier.

Three More Loans to Beware Of

Not all questionable loans come with triple-digit interest rates. Some have APRs that seem almost reasonable. But there may still be traps aplenty:

Debt-consolidation loans. Consolidate your high-rate credit card debt into one convenient loan with a low monthly payment—and you may end up paying through the nose.

Some debt-consolidation loans do exactly what they promise: Lower the total cost of your debt. But many lower your payments only because they stretch out your loan repayment term for years and years. You may wind up paying a higher interest rate on your debt, plus numerous fees that increase your costs.

“I recently was stupid and took out a personal loan at 22% to pay off my credit cards,” said Charlene from Salem, New Hampshire. “Now I have a loan for 84 months that seems to be adding on more interest than I’m paying. It’s hard to afford more than the minimum balance, and because I was three days late with a payment, they added on $500 in fees, including a late-payment fee, an over-the-limit fee, and finance charges. Now I just feel buried. I dug myself into a deeper hole and can’t ever imagine getting myself out of it.”

There’s also a lot of fraud in this area, with scam artists promising loans in return for big up-front fees or commissions.

If you do consider a debt-consolidation loan, deal only with lenders you know, such as a local credit union or well-known bank. Compare the interest rate and terms with what you’re paying now on the debt you hope to pay off. You shouldn’t have to pay hefty up-front fees or commissions to get the loan, and you should be able to pay off the debt in a reasonable length of time.

Margin loans. Brokerages typically allow you to borrow money using your securities (stocks, bonds, mutual funds, and so on) as collateral. The interest rate you pay is relatively low—usually one to three percentage points over the prime rate—which is why some people turn to margin loans as a source of emergency cash or to fund other investments.

The big risk is that your loan can be “called” with little warning. If the value of your securities drops, the brokerage can ask you to deposit more cash in your account to bring the balance up to its minimum standards. If you don’t respond quickly enough, the brokerage can seize your investments and sell them.

Inexperienced investors should steer clear of margin loans until they have a good feel for the possible swings the market can inflict on a portfolio. Even then, they should limit their borrowing to less than what a brokerage allows and have a ready source of cash to tap if their loans should be called.

Why You Don’t Want to Cosign a Loan

So far this chapter has focused on loans you don’t want to get. But there are loans you should avoid giving as well.

You might not think you’re lending anything when you cosign a loan for someone else. But although you’re not putting up any cash, you are lending your good name—and that might come back to haunt you. Read what happened to Doug in Ohio:

“I was the cosigner on a vehicle for my sister-in-law. I got the whole ‘You’re the only one who can help me,’ ‘If I don’t have a car, I can’t get to work, then I can’t pay my bills...’ and so on. Being soft-hearted, I gave in and cosigned for her. To make a long story short, she defaulted on the payments, had the vehicle voluntarily repossessed, and is currently filing bankruptcy on the balance, which is about $18,000. I by no means have the resources to pay for the defaulted portion, so I am in the process [of filing for bankruptcy too]. I already have two vehicles, a rent payment, insurance, a wife who is not working, and a four-year-old daughter. My credit rating before this incident was flawless, and I scored around 850. Now, from my most recent report, about a year ago, it’s at 650. I am so bummed out.”

Many people who cosign a loan are surprised to learn that legally they’re just as responsible for making the payments as the other borrower. Late payments or defaults wind up on both parties’ credit reports, and either party can be sued for repayment.

If someone asks you to cosign a loan, she probably has either bad credit or no credit. This means that either no lender is willing to take a chance on this person, or the lenders that are want to charge sky-high interest rates to reflect this borrower’s risk of default. If lenders have such a poor opinion of this borrower, you should think hard about whether you want to put your good credit rating in her hands.

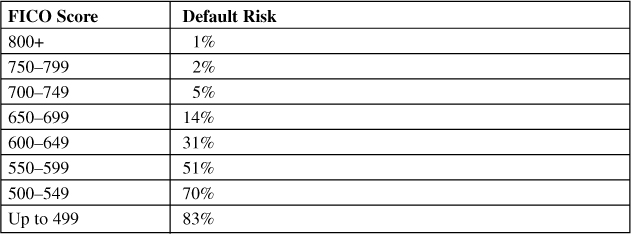

Table 9.1 shows the chances that a borrower will default based on her credit score. The chance that someone with a FICO score of 800 or above won’t pay her bill is just 1%, while someone in the 600 to 649 range is expected to default almost one third of the time. Below 500, the chances of default rise to 83%.

Table 9.1. The Risk of Default

Source: Fair Isaac

You might still decide to go ahead. Cosigning a loan can be a way to help a trusted young person build her credit history, or you might be helping someone who’s trying to recover after a credit disaster. Whatever your reason, take the following precautions:

• Don’t sign if you can’t afford to pay off the loan yourself. Picture the worst-case scenario: Your coborrower on a car loan skips town, for example, leaving you with the debt but no vehicle to sell to help pay off the loan. If you couldn’t make the payments, don’t cosign the loan.

• Don’t sign if you don’t have control over the payments. The lender isn’t required to notify you if your coborrower falls behind, so by the time you know there’s trouble, your credit’s probably already been trashed. Make sure that the loan statements and payment coupons are sent to you so that you can monitor the loan. Your coborrower can send the checks to you, and you can forward them to the lender. A hassle? Yes, but it’s a small price to pay to protect your credit.

The Right Way to Make a Personal Loan

Loans between friends and family members are actually pretty big business: The World Bank estimates that such borrowing totals about $300 billion a year, and the borrowed money provides as much as 41% of personal income in some developing countries.

But the way many people lend money to family and friends is far from businesslike. Often, there’s no discussion of interest rates, repayment terms, or the consequences of default. Frequently, what started as a loan turns into an involuntary gift when the lender fails to pay back the money.

Even when payments are made on time, the loan can strain the relationship. The lender might start questioning every purchase the borrower makes, with an eye to whether there will be enough money to make the next loan payment. The borrower picks up on the lender’s monitoring and resents the fact that he’s being judged.

This brew of ill feeling is why many people are dead set against mixing relationships and money. But private loans among friends or family members can have positive effects as well. They can help people buy homes, start businesses, or pay off high-rate debt.

The difference between a loan that’s successful and one that’s a disaster often has a lot to do with how much preparation the parties did up front. Consider the following questions:

Am I lending money I can’t really afford to lose? As one of my readers put it, “You should always be prepared for your loan to be a gift. If you get paid back, that’s just gravy.”

The person asking you for money is probably a worse-than-average risk. If he weren’t, he’d be able to get plenty of low-rate debt from a mainstream lender and wouldn’t need to bother you.

Whatever your relationship to the borrower, his need for cash isn’t more important than your financial survival. If you can’t afford to say good-bye to this money, don’t lend it.

How will this loan affect our relationship? Ask yourself how you would feel if the borrower immediately took off on an expensive vacation after accepting your money. If your blood pressure just went up a few notches, you might want to rethink the loan. You won’t be able to control what he does with the money after you make the loan.

Am I enabling or helping? “Helping” implies you’re giving someone a boost to a better life. A loan that allows someone to buy a house, start a business, or get an education is often such a “hand up,” rather than a handout.

Enabling, on the other hand, just allows the other party to continue the destructive behavior that got him into trouble in the first place. Any money lent to an addict, alcoholic, or compulsive gambler is almost certainly enabling (unless he’s in recovery). So, too, is a loan to someone who spends compulsively, repeatedly runs up credit card debt or “underearns”—a term used to describe people who settle for low-wage jobs when their skills and experience qualify them for much better-paying posts.

Have I consulted a tax pro? Any interest you charge can be taxed as income. But failing to charge interest, or not charging enough interest, can cause tax problems too, especially when you lend money to relatives. The IRS may “impute” the amount of interest it thinks you should have charged and tax you on that. Also, any part of the loan you forgive can be considered taxable income to the borrower.

There are ways around these tax headaches, but you’ll want a tax pro’s guidance if the loan is for more than $10,000 or your family has made other gifts or loans recently.

Do we have a contract? It’s a good idea to formalize any personal loan with a written contract that lays out the dollar amount of payments, the interest rate, the due date, and the penalties for late payments or defaults. Make sure both sides have signed and dated copies.

This will eliminate any confusion about whether this is, in fact, a loan and not a gift; the paperwork could also come in handy if the borrower defaults and you want to take a tax deduction for the loss. (Which isn’t easy, by the way, so consult a tax pro for details.)

Do I want to get a third party involved? Social lending sites including Prosper and ZimpleMoney will allow you to set up friends-and-family loans. One mother who used such a service told me she liked the fact that she didn’t have to be the loan “cop.” Her daughter—the borrower—confessed that having a third party involved made it much tougher to justify skipping a payment.

Summary

High-rate loans prey on consumers in a cash crunch, but there are usually good alternatives that will help you survive the crisis and keep more of your money in your pocket. You should also be wary of cosigning a loan or lending money to family or friends.

Credit Limits

• Don’t start the short-term loan cycle. Payday and other short-term lenders like to argue that they’re providing a popular “service” to cash-strapped borrowers. But the price borrowers pay to be serviced is simply too high. There are always other alternatives, including simply doing without the cash.

• Consider your alternatives. Cutting spending, raising extra cash, and negotiating with your creditors are better solutions than most high-rate loans.

• If you’re the lender rather than the borrower, consider the worst-case scenario. If you cosign a loan, late payments and defaults will show up on your credit report. If you do lend a friend or family member money, you should be prepared not to be repaid.

Shopping Tips

• Weigh all the costs of any loan. Lenders are required to disclose the APR of loans, as well as any fees involved. With this information, you can compare the costs of different kinds of loans so that you can pick the best alternative.

• Do the math. You can find the true cost of any loan by multiplying your monthly payments by the total number of payments and then adding in any up-front or back-end fees.