11. Putting Your Debt Management Plan into Action

Now that you know more about debts and how they can be managed intelligently, you can put together a plan to deal with your finances in the smartest way. You can get rid of your most troublesome loans while increasing your financial flexibility and building your long-term net worth.

We’ll assume at this point that you can pay more than the minimum on your bills (or you suspect you can do so once you’ve trimmed a few expenses). If you’re still struggling with your debts or being hounded by creditors, you need to go back a chapter and read about managing a debt crisis.

Once your crisis is resolved and you’re back on your feet, you can get started with your long-term plan.

This program has six steps:

• Lower your interest rates where possible to make your debt more affordable.

• Track your spending so that you know where your money goes.

• Trim your expenses so that you’re spending on the important stuff.

• Look for cash to speed you toward your goals.

• Review your priorities so that you know what’s important and what’s not.

• Create a debt management plan that works for you.

Lower Your Interest Rates

You can speed up any debt repayment plan, or free up more cash for other goals, by getting your interest rates down. Here are some of the best places to try:

• Credit cards. If your credit scores are good, look for low-rate cards or low-rate balance transfer offers. Sites like CreditCards.com, CardRatings.com, CardHub, and NerdWallet, among others, have current offers. Make sure you understand all the fees involved and when any “teaser” rates expire. For more information, review Chapter 3, “Credit Cards.”

• Mortgages. If rates have dropped or your credit has improved significantly since you got your loan and you have some equity, refinancing might lower your rate and payments. But you need to beware of “quick fix” solutions that might leave you worse off in the long run. Review the information in Chapter 4, “Mortgages.”

• Auto loans. If you owe less on your car than it’s worth, you may be able to refinance to a lower interest rate. See Chapter 7, “Auto Loans.”

Another way to lower your interest costs is to transfer high-rate debt to a home equity loan or line of credit. However, you do not want to use this option until your spending is under control and you’re sure you aren’t headed for bankruptcy. Carefully review the information in Chapter 5, “Home Equity Borrowing,” before you consider such a transfer.

Converting high-rate debt to a retirement plan loan is another potential, if risky, option. Review Chapter 8, “401(k) and Other Retirement Plan Loans,” before you decide if this is an option for you.

Track Your Spending

Before you can decide where your money should go in the future, you need to figure out where it’s going now.

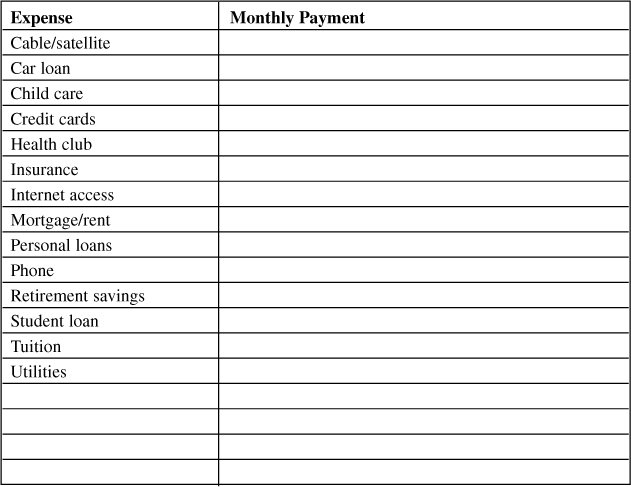

We’ll start with your regular bills (see Table 11.1)—what many people call “fixed” expenses (although few expenses are truly carved in stone).

The extra spaces are for you to enter the other monthly bills in your life, but remember that this worksheet is just a guideline. You may well create one of your own that’s more or less detailed. Instead of “Utilities,” you may decide to track your gas, electric, water, and garbage expenses separately, for example.

If you pay a bill annually, semiannually, or quarterly, figure out how much your total expense in that category is each year and divide by 12 to get your monthly cost. If your property taxes are $2,400 every six months, for example, you’d pay a total of $4,800 a year or $400 a month.

Vacations and holidays are other big money drainers. Estimate how much you spent last year and divide by 12 to get your monthly figure.

Finally, don’t forget to include money for car and home repairs. These expenses may not be regular, but they’re certainly inevitable. If you’re not sure how much to budget, look at your bills from last year and add a fudge factor of about 10%.

Once you’ve identified all these less-regular expenses, you’d be smart to add up the monthly costs you’ve calculated for them and sweep that amount into your savings account each month so that you don’t have to scramble when the bills are due.

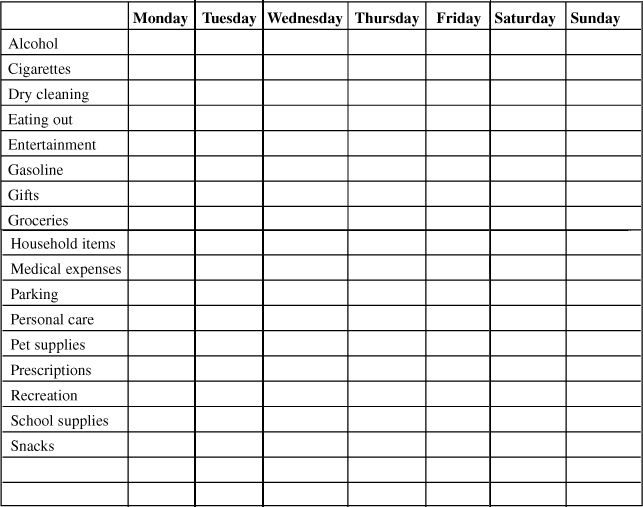

Next are your “variable” expenses. You can try to reconstruct these by looking at your credit card bills and checking account statements, but you’re bound to come across a $40 ATM withdrawal here and a $20 cash expenditure there that you can’t identify. Sometimes these can add up to hundreds of dollars.

A good way to track these slippery expenses is to get a small notebook and a pen and write down every purchase you make. (If you’re married or have a partner, get the other person involved as well.)

This exercise may sound dreary, but I guarantee the results will be eye-opening. I have yet to meet anyone who tried the notebook method who wasn’t surprised at how quickly those little dribs and drabs of spending add up. Do this exercise for a month, and you’ll have a very good idea where the “leaks” in your wallet are. Once a week, transfer the contents of your notebook to the worksheet shown in Table 11.2. (Make four copies so that you can have a full month’s worth of variable expenses to review.) At the end of the month, examine the totals for each category.

Table 11.2. Weekly Expenses Worksheet

Once you’ve got your totals, the real work can begin. The first step is to compare your total monthly spending (fixed plus variable) with your take-home pay.

If you’re operating at a loss (your expenses exceed your income), you obviously need to make some changes. But even if you’re in the black, you’ll still probably want to expand the gap between your income and your outgo to fund your debt management plan.

Creating a workable spending plan may require several attempts and lots of adjustments over time. Inevitably, you’ll forget some important expense or face setbacks that will leave you scrambling. Don’t give up. Just keep making tweaks until the plan really works for you.

Trim Your Expenses

For most people, cutting expenses is a lot easier than raising their incomes (although we’ll talk about that too in a bit). Name an expense, and there’s probably a way to trim it.

How practical those trims are and how much money you’ll save depends on your individual situation and how quickly you want to achieve your goals. Someone who’s bent on early retirement may be willing to get pretty frugal to leave the rat race behind; others may want to strike a more equal balance between current and future comforts. It’s up to you to decide what works for you and what doesn’t, but here are some areas to look at:

Housing and utilities. Moving to cheaper digs is one option; so is getting a roommate. We also discussed refinancing as a possible solution for homeowners. But short of that, there are other ways you can lower your overall housing costs:

• Opt for higher deductibles on your homeowner’s or renter’s insurance.

• Challenge your property tax assessment.

• Turn down your thermostat in winter and turn it up in summer to save heating and cooling costs.

• Do full loads of dishes or clothes, and consider hanging some clothes out to dry.

• Drop premium channels from your cable or satellite TV service, or drop the service altogether.

• Drop phone extras like call waiting or cancel your landline altogether in favor of cell phone service (or vice versa).

• Find a cheaper long-distance carrier (try SaveonPhone.com or LowerMyBills.com) or switch to Internet calling if you have high-speed Internet service.

• Check to see if a bundled service (phone, high-speed Internet, and television) might save you money.

Transportation. As discussed in Chapter 7, people who really want to save money on cars buy them used and drive them until the wheels fall off (well, almost). But there are plenty of other ways to save money:

• Boost the deductibles on your auto insurance policy.

• Make sure you’re getting the breaks you deserve (good driver, good student, multiple-car discounts) and that your policy accurately reflects the number of miles you drive.

• Consider canceling collision and comprehensive insurance on older cars. Check how much your car is currently worth at Edmunds.com; that’s about the check you can expect from your insurer. The smaller the check, the less sense it makes to continue this coverage. But be aware that the coverage on your personal car typically extends to rental cars. If you drop comprehensive and collision, you should consider buying the coverage from the rental agency when you rent a car.

• Investigate carpools and public transportation and ask at work about any subsidies offered for using these alternatives.

• Group your errands.

• Bike or walk as often as possible.

• Maintain your vehicles properly with regular oil and filter changes.

Food. This is a big expense for most families, and nationally the typical food budget is pretty evenly divided between eating in and eating out. You can save in both areas:

• Eat out less, and use coupons when you do.

• Pack a lunch and snacks for work.

• Make a few meatless meals each week.

• Use the weekly grocery store circulars to see what’s on sale, and plan meals accordingly.

• Buy generic rather than highly advertised brands.

• Buy fruits and vegetables in season.

• Patrol your refrigerator and freezer regularly so you can use food before it goes bad.

• Give up a vice (smoking, drinking, salty snack foods).

• Avoid overpackaged and overprocessed foods.

“Convenience” foods can be especially costly, so make sure they’re worth it. It takes only a few minutes and a couple dollars’ worth of produce to make fruit salad, for example; buying it precut and premixed can set you back $6 a pound.

Clothing. In some areas in Africa, donated apparel from America is called “dead people’s clothes” because folks there can’t conceive of a society so affluent that it would toss out perfectly serviceable items. You needn’t wear clothes until they’re in tatters, but there may be a number of ways you can cut down on costs:

• Check out consignment and thrift stores for gently used items.

• Know what looks good on you, and stick to classic styles rather than chasing trends.

• Buy pieces that work with what you already own.

• Avoid dry-clean-only pieces.

• Solicit hand-me-downs from friends and family or hold a clothing swap with friends. (One woman’s “fat pants” may be another woman’s maternity outfit.)

• Give kids a clothing allowance or offer “matching funds” for what they want to buy. (Nothing encourages youthful frugality like having to use their own money.)

You’ll find lots more ideas on Web sites like the Dollar Stretcher (www.stretcher.com) or in Amy Dacyczyn’s book The Tightwad Gazette (available at your local library—another great way to save money).

Of course, once you’ve sketched out a tentative budget for your expenses, you still have to stick to it. Here are some ways to avoid overspending:

• Don’t shop for recreation. Avoid stores or malls unless you have a specific, necessary purchase to make—and then buy your item and get the heck out. Don’t be lured by sales that entice you to spend more than you planned on unnecessary items; you’re not saving if you spend more than you planned in the first place.

• Use shopping lists. Merchants spend millions of dollars a year on strategies to get you to buy on impulse. Lists are your way of fighting back. For example, I made a list of the items we commonly purchase at our favorite grocery store and organized them by aisle. (This was pretty easy to create on the computer after a few shopping trips.) I make a dozen or so printouts at a time and attach them to the side of the freezer with a magnetic clip. We check off the items we need as we run out and take the list with us when we shop. We also have a couple of blank pads (also magnetized on the back) to write down items we need at the drugstore, warehouse store, and other shops.

• Dump catalogs. Tracey McBride, author of Frugal Luxuries, discussed how leafing through glossy catalogs can give her a severe case of the “I wants.” Even if she was perfectly happy with her life a moment earlier, the images in these catalogs can spawn a yearning that can be satisfied only with yet another credit card purchase. Do yourself a favor and get off the mailing lists or simply toss catalogs in the trash.

• Limit surfing. If online purchases are your Achilles’ heel, limit your time on the Internet. Remove your favorite shopping sites from your browser and move your computer to a more public place in your home if that’s what it takes to curb your habit.

Look for Cash

We’ll assume that you won’t win the Powerball lottery anytime soon and that your rich aunt Dottie, dog-lover that she is, will bequeath her fortune to the Pekinese Preservation Program. So what other ways can you make ends meet?

Boost your income. Working more hours, adding a second job, or asking for a raise are all time-honored ways of earning yourself out of a financial bind or freeing up more money for debt repayment plans.

Then again, you may need to find a better job—particularly if you have a history of “underearning,” or working for wages that are substantially less than what your education and experience should command. Some people get trapped in low-paying jobs because they really can’t find anything better, but others settle for less because they lack the confidence or drive to get what they deserve. If you think that may describe your situation, you may want to explore what’s holding you back and consider a support group, like Debtors’ Anonymous, whose members may be dealing with similar issues.

Adjust your withholding. Keep the money that’s yours rather than loaning it interest free to Uncle Sam. The IRS has issued 59.2 million refund checks for the 2011 tax year totaling $174.4 billion, with an average refund amount of $2,946. That’s $245 a month that those families could have applied to other goals. You can use a calculator on the IRS Web site (www.irs.gov) to refigure your withholding so that more of your money stays in your wallet.

Consider raiding your savings. After talking about the importance of financial flexibility, now I’m trying to get you to drain that emergency fund you so painfully scraped together? In many cases, yes. For example, it makes no sense to carry high-rate credit card debt when you have cash loitering in a low-interest savings account. You can always use those cards in an emergency; meanwhile, you’re not paying all that money in interest charges.

This holds true for investments you own outside your retirement funds, such as mutual funds in a brokerage account or stock options you haven’t exercised. You may want to consult a tax pro about the IRS implications of selling those investments, but typically they would be put to better use paying off high-rate debt.

What might not make sense is raiding your savings to pay off low-rate debt that won’t necessarily increase your financial flexibility, like student or car loans.

Sell some stuff. You may have some big stuff you can let go of, like an unneeded vehicle or jewelry that isn’t heirloom (or that is, but you’re willing to part with it). Even if you don’t, though, chances are good you have something to sell. Perhaps lots of somethings.

The size of the average new home has nearly doubled in the past 40 years, even as families have gotten smaller. Demand for storage facilities continues to rise as well, according to the Self Storage Association. One in 10 U.S. families rents a storage unit, up from 1 in 17 in 1995. All too often, what’s being stored winds up being worth less than the fees paid to store it. So why not turn some of your clutter to cash? You can have a garage sale or explore the world of online selling.

This latter option is so popular and so effective for many people that I’ve devoted the next section to it.

Sell Your Surplus Stuff Online

In the bad old days—say, 20 years ago—your options for selling your surplus possessions were pretty limited: yard sales, consignment shops, newspaper ads. A few Internet-savvy folks had access to online bulletin boards where they could trade their stuff, but the audience was still fairly small.

Today you can tap a massive worldwide market of potential buyers with relatively little effort. The huge success of eBay and other online “flea markets” has allowed millions of people to get top dollar for their stuff.

If you’ve never sold online before, getting started can seem daunting. You may have heard about spiraling fees at auction sites, problems caused by picky buyers, and even the possibility of fraud. But with a little research and a few precautions, you can prevent the most common problems and get your items sold with little hassle.

Four of the most popular sites are Amazon.com, Craigslist, eBay, and Half.com (now owned by eBay).

Each site has guides and FAQs (frequently asked questions) for newcomers, but these principles apply in general:

Research the site. Each site has its particular strengths. All four allow you to set a fixed price for your item; eBay also offers an auction feature that may land you more than you expected for your wares. (Most longtime eBay sellers have a story about an item they picked up for a song at a garage sale and then sold for a hefty profit at auction.)

Half.com is a good site for selling relatively new books, music, movies, and some electronics. So is Amazon.com, although it charges slightly more. Neither site charges for listings, which can be helpful if you’re not sure your item will sell, and both have easy sign-up procedures. Craigslist, which functions like a huge classified advertising section divided by cities, has no listing or selling fees. It’s often the best place to sell items you wouldn’t want to ship, such as furniture and other bulky stuff. eBay, with its millions of listings and tens of millions of active users, remains the go-to site for a laundry list of items, including collectibles, jewelry, designer or formal wear, or anything weird, rare, or hard-to-find. eBay has both listing and selling fees (also called commissions).

Research your item. See what others are charging and notice the words they use to describe the item. Using the right “keywords” can lure more potential buyers. It matters a lot to collectors if your old plates are fire sale or Fire King, for example.

Sell it right. Clear pictures of your item can help it sell; so too can including all the appropriate details (such as dimensions, weight, and materials used). Be honest about the condition because failing to do so will lead to unhappy buyers who will trash your all-important “seller feedback” ratings. If you want to sell more than one item, you need good ratings to encourage people to buy from you.

Consider costs. If your item is worth only a few bucks, a yard sale is probably a better way to sell it. Otherwise, your profit will be largely eaten up by fees, commissions, and shipping expenses or just the hassle of arranging delivery.

Stay alert. If you don’t check your e-mail for days or you drag your heels on shipping the item once it’s sold, buyers will complain and damage your seller ratings.

Protect yourself. Phony cashier’s checks and fake escrow sites are among the ways sellers can be defrauded. Unless you complete the transaction face-to-face and insist on cash (as do many people who use Craigslist), you’ll want to employ some kind of middleman. Amazon.com and Half.com collect and disburse money for their sellers, while eBay recommends using PayPal, an online payment service. If your buyer insists on using a particular escrow site, beware unless it’s one of the services specifically recommended by eBay (check the eBay site under “Services” for a list). Also employ some kind of package tracking so that your buyer can’t pretend the item never arrived.

You might want to explore other alternatives as well. So-called “trading assistants” can handle your eBay auctions for you; you just drop off your stuff, and they do the rest. The price is a bit steep, typically 30% or more of the final sale price, so it’s an option best kept for more expensive items that you don’t have time to handle yourself.

You also might look for trading forums on Web sites devoted to a specific hobby or vocation. Sites for computer buffs, for example, often contain a section where users can list items for sale. Just be sure to carefully read the rules and suggestions for newcomers before you post your item.

Review Your Priorities

Any financial plan is a juggling act of conflicting priorities and limited resources. You make only so much money (even if you add a second or third job), and your wants can be almost endless.

In earlier chapters, you read that debt repayment needs to be part of your larger financial strategy. Specifically, you need to make sure that you’re taking appropriate advantage of retirement savings opportunities and that you can access sufficient funds in an emergency. You’ll also want to think about your other important goals—the things you want to do, accomplish, or create for your family. As you work with your budget, you’ll want to make sure that these important areas are adequately addressed and funded. If you need a refresher on these concepts, reread Chapter 2, “Your Debt Management Plan.”

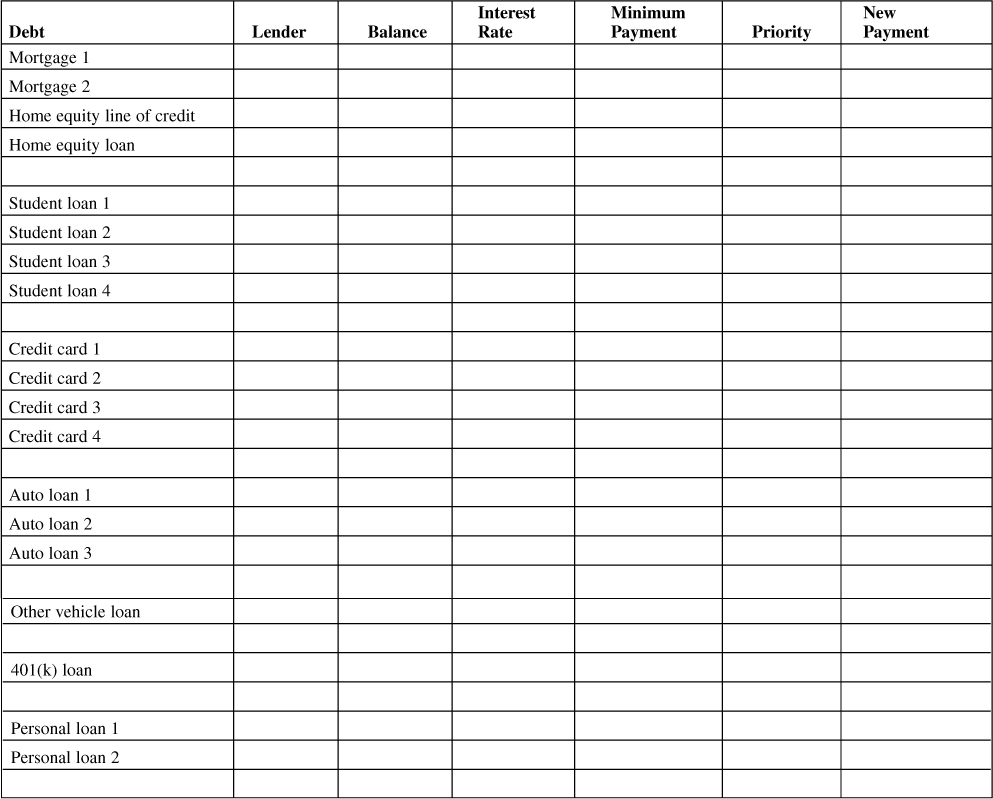

Also in Chapter 2, you used a worksheet to list all your debts and the relevant details, such as balances owed, interest rates, and so on. Now it’s time to go back over those debts, fill in any new interest rates or payments, and assign each a repayment priority: high, medium, or low. Use Table 11.3 to do this.

Table 11.3. Debt Repayment Worksheet

These priorities are entirely up to you, based on your knowledge of your goals and current financial situation.

Paying off credit card debt should usually be a high priority. It’s usually your most expensive debt, and even if you’ve currently got a low rate, you’re limiting your financial flexibility by carrying a balance.

Auto and student loans are usually medium- to low-priority debts. Paying them off typically doesn’t increase your financial flexibility much, and interest rates on these debts are usually quite reasonable. If these are your highest-rate loans, though, and you have extra money to pay them off, you might well decide to give them higher priority.

A home equity line of credit could be high-, medium-, or low-priority, depending on your circumstances. Generally, this relatively low-rate, potentially deductible debt will be far down on the payback list, but you may want to move it higher if a HELOC is your only source of emergency cash.

Paying off your mortgage, meanwhile, is usually a low priority. Generally, you should have retired all your other debts before you consider prepaying a mortgage.

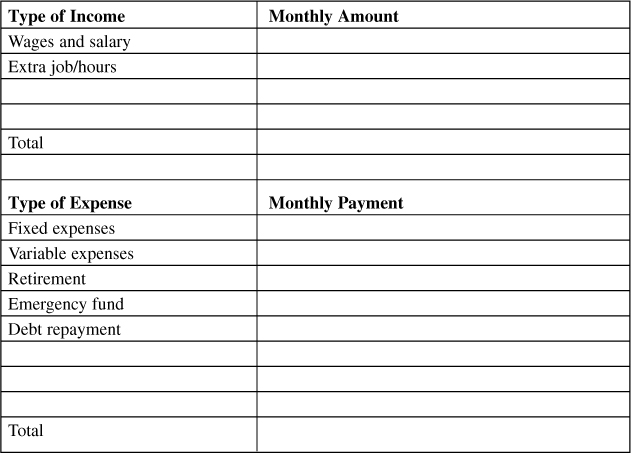

Once you’ve assigned priorities to your debts, you can start creating your debt repayment plan. You can use the worksheet shown in Table 11.4 to play with the numbers until you have a plan that works. After that’s done, you can return to Table 11.3 and fill in the new payments you want to make toward your highest-priority debt or debts. You can use the debt repayment calculators I mentioned in Chapter 2 to see how long it will take you to retire each debt using your plan.

Table 11.4. Debt Repayment Plan

Creating a financial plan that allows you to meet your current expenses, save for retirement, enhance your financial flexibility, and pay down your highest-priority debt isn’t easy, but now you have all the information you need to get going.

Stay on Track

I wish I could promise you smooth sailing from here on out, but few of us have lives that don’t throw us an occasional curveball.

Here’s my best advice for how to stay on track despite whatever comes:

• Get support. Living a frugal or even goal-centered life isn’t exactly a mainstream choice in America, where every time you turn around advertisers are shouting at you to spend more. That’s why it can be helpful to find others who share your goals. You may be able to find a “simple living” support or study group in your area. If you have a severe or uncontrollable spending problem, investigate Debtors Anonymous, which is a 12-step group based on the principles of Alcoholics Anonymous that can provide invaluable information and support.

• Use wish lists. If there’s something you really want, write it down and stick it in a prominent place, like your refrigerator. Wait three weeks and see if the purchase is still a priority. Many times, your desire for the item will have faded. (Some people put their wish lists next to a picture of their ultimate goal: a new home, perhaps, or a happy retired couple playing golf. That can help make the decision to forgo the impulse item a lot easier.)

• Boot bad influences. Almost inevitably, somebody in your life—perhaps many somebodies—won’t understand what you’re doing and may even feel threatened by it. The worst of these somebodies may actively try to undermine your attempts to reach your financial goals. For example, one of my readers described a friend who constantly invited her to expensive restaurants and concerts and determinedly rebuffed the reader’s suggestions that they find more affordable entertainment. Another had a mother-in-law who kept pushing him to enroll his children in a private school the family couldn’t afford, even though the public schools in their neighborhood were quite good. You may need to limit your interaction with these folks—at least until you can smile and ignore their needling.

• Beware of quick fixes. People who take shortcuts often find themselves not getting to their destination at all, and that’s particularly true with money. Get-rich-quick schemes, high-risk investments, gambling, and even chain letters may tempt you off the slow and steady path to building wealth. Just remember that every dollar you waste on any of these bogus “solutions” is a dollar that won’t get you closer to your goals.

• Watch for signs of “frugality burnout.” Feeling deprived can tempt you to throw in the towel on your financial plan, so make sure you build occasional treats into your budget—dinner out, a movie, a little mad money to waste any way you want. Go ahead and buy that latte or ice cream cone or get a manicure now and then. If you can’t afford to go away on vacation this year, take time off anyway and be a tourist in your own area. Don’t put off all your rewards for the future; enjoy a few today as well.

• Get back on the horse. No matter how carefully you plan and how committed you are to your goals, stuff can happen. You can lose a job, suffer an illness, get in an accident, or be thrown off track in any number of ways. You may despair of ever reaching your goals. In fact, you might need to figure out a new plan or even rethink your goals. Just remember, winners are the ones who don’t give up.

Some Final Thoughts

You’ve done the kind of work that creates success. You’ve examined your situation with clear eyes, ascertained your goals, and created a plan to achieve them.

As your wealth grows, you’ll be able to retire even more of your debt—but you’ll also be able to add new loans when needed without anxiety or unnecessary stress. Instead of feeling controlled by your debt, you can feel in control of your money.

I hope you’ll write to tell me about your plans, your challenges, and your successes. Readers’ stories helped shape this book, and perhaps something you’ve learned along the way might be helpful to others. The best way to reach me is through my Web site, www.asklizweston.com.

Good-bye, and good luck!