10. Dealing with a Debt Crisis

Sometimes the signs of debt crisis are pretty obvious: Collection agencies are calling you night and day, or your car’s been taken by the repo man, or your stuff is piled in the street because you’ve just been evicted.

But there were probably plenty of warning signs along the way. If you’re experiencing any of the following, you’re facing a debt crisis:

• You pay only the minimums—or less—on your credit cards and other bills.

• You’re borrowing from one card or credit account to pay another.

• You can pay your bills only because you’re draining your savings or retirement accounts.

• You’re near the limit or maxed out on all or most of your credit cards.

• You’re charging a larger amount each month than you’re paying off.

• Your income is shrinking but your credit card balances are growing.

• You’re using credit to pay for essentials like food, rent, or gas, and you can’t pay the bill in full each month.

• You’re using payday lenders or other high-rate, short-term loans.

• You’re lying to your partner about your debt or fighting a lot about what you owe.

Angela and her husband make good money—about $60,000 each annually. But they also have $37,000 in credit card debt that’s accruing interest at about 18% a year. Lately, they’ve found that they can’t pay more than the minimum amounts due on each card.

“We don’t make any late payments,” Angela said, “but we also don’t have any free money every month.”

Even if they continue to pay on time, Angela and her husband are likely to face some financial setback—a car repair, reduced hours at work, an accident or illness—that will upset their overloaded applecart.

It’s human to want to hope for the best—that your unemployed spouse will land a job tomorrow, that your boss will give you that raise, that next month your expenses will be a bit lower so you can get ahead. You might even be dreaming that a timely inheritance or a big lottery win will bail you out of your predicament.

But wishing and dreaming won’t make it so. Debt problems don’t get better on their own, and usually they get much, much worse. The more your situation deteriorates, the fewer good options you’ll have left.

So whether the crisis is here, or just on its way, it’s important to take action now.

Dealing with Your Creditors

Go back to Chapter 2, “Your Debt Management Plan,” and the section titled “If You’re Already Drowning.” If you haven’t done so already, go through the exercises of identifying and prioritizing your bills, matching your resources with your debts, and figuring out a tentative game plan.

You’ll want to do this work before you pick up the phone to talk to any of your creditors. Otherwise, you’re at risk of being manipulated by the pushiest or most unpleasant lender. Knowing your priorities and resources is essential to crafting an effective debt crisis plan.

Also you need to be realistic about what debts you can pay and what debts you can’t. If you’re going to default on your credit cards or file bankruptcy, for example, there may be no point in talking to those creditors.

If you can pay, by contrast, staying in touch with creditors can help you preserve your options, as you’ll soon see.

Here’s what you need to know about approaching various kinds of lenders:

Mortgage lenders. You just have to Google “mortgage modification horror stories” to get a feeling for how tough it’s been in recent years for people to work out deals with their lenders. Distressed borrowers complained that their lenders repeatedly lost paperwork, gave contradictory or erroneous advice, and promised help while proceeding with foreclosures. Ever-changing government programs promised more relief than they actually delivered.

This subject can, and has, filled entire books, including the excellent The Foreclosure Survival Guide by attorney Stephen Elias. We’ll just hit the highlights here.

If you’re having trouble paying your mortgage, get in touch with a HUD-approved housing counselor. You can get referrals at www.hud.gov. Their services are free or low cost, in sharp contrast to the for-profit (and sometimes fraudulent) “we’ll save your home” services that advertise heavily, charge a fortune, and often produce no results.

HUD-approved housing counselors know about the various available programs to help you get a mortgage modification or refinance, even if you’re underwater on your home. They can review your situation, advise you on your options, and help walk you through the process.

A key decision you need to make is whether you actually want to keep your home. Some houses are worth so much less than their mortgages that they may not be worth fighting for; your credit may recover before the home’s value does. Only you can make the decision whether you want to try, and you’d be smart to read Elias’ book before you make up your mind.

If it’s time to let the house go, you have more choices to make: a short sale, a “deed in lieu,” or a foreclosure. With a short sale, the lender typically agrees to accept the proceeds of a sale as settlement of what you owe and agrees not to pursue you for the balance. Short sales are taking less time these days than they used to, but it can still be a long and grueling process. You’d be smart to have a good real estate agent, one experienced in negotiating short sales, on your side. You’ll also want a lawyer to review any agreement with the lender because some banks have been known to put language in the contract that leaves you on the hook for any unpaid debt.

A common myth is that a short sale is better for your credit scores than a foreclosure. That’s not true; the creators of the leading FICO credit score have made it clear that the impact is typically the same. The advantage with a short sale is that you spend less time in lenders’ “penalty boxes”—in many cases, you can get another home loan within two years, compared with five to seven years with a foreclosure.

The advantage to a foreclosure is that the process can take awhile, particularly in states that require the involvement of the courts. While the foreclosure grinds on, you can live in the home and save up the money you would otherwise use to pay your mortgage. With these savings, you can restart your financial life—and offer landlords big deposits to convince them to rent to you, despite your troubled credit.

A foreclosure could leave you exposed to lawsuits from the lenders over any unpaid debt, however, depending on the laws in your state. It makes sense to get advice from an experienced bankruptcy attorney if foreclosure is a possibility.

Another alternative is simply turning over your home to the bank, formally known as a “deed in lieu of foreclosure.” You don’t get to stay in the house, and your credit is damaged as much as with a short sale or foreclosure. But if you’re ready to be done with the mess and move on, it’s an option. Just make sure you consult a lawyer about your liability for any unpaid debt.

Auto lenders. Many people are shocked by how quickly a lender can repossess a car. Typically, you need to be only a day late with your payment for repossession to become a possibility.

If you’ve missed a payment or two and you want to try to keep your car, calling the lender can help stave off repossession. The lender may agree to an extension or even a refinance that could lower the payments. Some aren’t that flexible, though, which is why you may need to put off other bills in favor of making your car payments if money is tight (and you need the wheels to get to your job).

If you can’t make the payments, frankly, your options are grim. If you owe more than the car is worth, the lender may not only repossess the car but sue you for the unpaid balance. (This is also typically true if you try to cancel an auto lease prematurely.) That’s why some people try to buy time by hiding their car—either swapping vehicles with a friend who lives out of state or parking it blocks or miles away from their home and business.

If you’re fortunate enough to owe less on the car than it’s worth, you may want to sell it and buy something cheaper.

Student loan lenders. An official for Sallie Mae, the nation’s largest student lender, once told me that student loans are “the most consumer-friendly that’s out there”—and for the most part, he’s right.

Federal student loans typically offer borrowers a large array of payment options:

• Temporary suspension of payments (known as deferment or forbearance) if the borrower becomes unemployed or suffers financial hardship

• Partial payments under the same circumstances if the borrower can pay some but not all of what’s owed

• Various repayment options, including “income-sensitive” payments that depend on salary, and graduated payments that start small and rise over time

• Consolidation, which can stretch out repayment terms to 30 years or more and significantly lower monthly payments

• Loan rehabilitation, which expunges negative information from the borrower’s credit report after 12 consecutive monthly payments are made

If you ignore these options and default, however, you may be opening yourself to collection actions by some of the harshest and most efficient collectors in the world.

The U.S. Department of Education has a stable of private collection companies that help it reap $10 billion in defaulted loan payments every year. In fact, the DOE estimates it collects more than 100 cents on each dollar of defaulted student loan debt, thanks to accumulated interest and penalties. No longer is it easy, or perhaps even possible, to walk away from student loan debt without consequences, as was common in the 1980s.

Student loan collectors typically use state-of-the-art methods to help track down defaulters and identify the best ways to get them to pay. It’s routine, for example, for collectors to monitor your credit report so that they can see if your financial prospects are improving—and then they can swoop in for their share.

You can see why it is smart to contact your lenders long before collection is even a possibility. If you’re having trouble paying your loans, chances are good that you can work out some kind of repayment plan that meets your needs.

The IRS and other tax authorities. Like the U.S. Department of Education, the IRS has vast and efficient powers to collect the money you owe. The federal tax agency can garnish wages, seize tax refunds, and put liens on your property to ensure it gets its money. State and local governments often have similar powers and may be in an even bigger hurry to use them. (In California, for example, many tax pros negotiate first with the state’s Franchise Tax Board when a client is delinquent, only afterward moving on to talks with the IRS, which tends to move more slowly than the state.)

The good news is that you have some options. Most people who owe $50,000 or less, for instance, can set up an installment plan that allows them to pay their IRS bill over time. If the amount you owe is larger or you can’t pay it all, you can try making an “offer in compromise”—basically a settlement offer for less than you owe. Unfortunately, these offers are tricky to make and often languish at the IRS for months, so you’ll probably want to hire a tax pro who’s experienced in making offers that succeed.

Other tax authorities typically have similar programs and options.

Some old tax debt can be erased in bankruptcy. This, too, is a complicated area in which you’ll probably need some professional guidance.

Medical providers. Another area where collections activity has really increased is the realm of doctor and hospital bills. Collectors often go after uninsured patients with a vengeance, and insurance disputes are often “resolved” by turning to collection agencies when an insurer refuses to pay.

Your first line of defense is making sure your bills are accurate. Many, if not most, hospital bills contain costly errors that you can challenge to reduce your bill. Also stay on top of any bill improperly rejected by your insurer; you may need to make daily calls or enlist the help of your state insurance regulator to get the problem straightened out.

You also should explore alternative payment arrangements. Many hospitals have a “charity” budget that pays the bills of financially strapped patients who apply. Others will arrange installment plans, waive late fees, or reduce the total amount owed in return for lump-sum payments. Many doctors also are flexible with their patients who are having temporary financial difficulties.

If you want to continue seeing a particular doctor—your child has asthma, for example, and you want her to continue having access to a particular pediatrician—it makes sense to make your payments to that doctor a priority.

If at all possible, you want to work out some arrangement before your account is turned over to a collection agency. Your credit will be damaged by the collection account, and you’ll probably find yourself with fewer options for repayment. You might also be sued over the unpaid bill, which could lead to wage garnishment and other unpleasant collection actions.

Also remember that medical bills are among the unsecured debts that can be wiped out in bankruptcy. (That’s also true of most legal bills and bills for other professional services, like those provided by an accountant.) If your finances are headed down that rocky road, you may well decide to conserve whatever cash you have rather than making pointless payments toward your medical bills.

Credit card issuers. In the past, people with good credit could simply call up their issuers and ask for lower interest rates—and often got them. During the financial crisis, however, contacting some lenders became risky because they were just as likely to close your account or raise your interest rate, on the assumption that you wouldn’t call unless you were in trouble.

These days, lenders have settled down somewhat, but you might not want to ask for any favors if you don’t have to. Because people with high credit scores (FICOs of 750 or above) can qualify for low-rate balance transfer offers, you might search sites like CreditCards.com, CardRatings, LowCards.com or NerdWallet for a better deal.

If you don’t have great credit, your options are more limited. Policies vary by credit card issuer, but some work with troubled borrowers to waive interest rates and create an affordable repayment plan.

In fact, some will even “re-age” your debt. I’m not talking about the illegal kind of re-aging, where a collector changes the date of a delinquency to make it more recent and keep it on your credit report longer.

The kind of re-aging I’m referring to is actually beneficial to consumers. In exchange for your making a certain number of on-time payments, the creditor agrees to remove negative information from your credit bureau file. If this option is available and you can make the payments, grab it.

If your credit card company isn’t interested in working with you, consider enrolling in a debt management plan offered by a qualified nonprofit credit counselor. These agencies can often get your interest rate waived and set up a multiyear repayment plan.

Such plans have their downsides. As I mentioned in Chapter 2, enrollment in debt management by itself won’t hurt your FICO credit scores, but some of your creditors might report your payments as late to the credit bureaus, which can hurt your score. Other lenders may look on credit counseling as similar to Chapter 13 bankruptcy and not lend to you while you’re in the program or charge you higher interest rates.

You also need to pick your counseling agency very, very carefully, as Donna’s experience shows:

“I had good credit prior to turning my accounts over to this debt-management program, which has since destroyed my name and credit rating in just 11 months,” she wrote. “They were automatically deducting the monies out of my account on the 20th of every month [but] were not paying my bills for 20 to 24 days after receiving my money and not even paying the minimum required amount! [That] caused my creditors to report me to all three credit reporting agencies [Equifax, Experian, and TransUnion].”

That’s why you’ll want to check the Better Business Bureau (www.bbb.org) for complaints before signing up and make sure the agency is affiliated with the National Foundation for Credit Counseling (www.nfcc.org).

You’ll want to be reasonably sure you can make the payments. If you ultimately wind up in bankruptcy, your credit card debts could be erased, and the money you paid in the meantime won’t have accomplished much.

In fact, I typically advise people with troublesome credit card debt to make two appointments: one with a legitimate credit counselor, and one with an experienced bankruptcy attorney. That’s because people—including credit counselors—can be too optimistic about their ability to repay their debts. By the time they realize they’re in trouble and seek help, it may be too late. A lawyer can help you understand whether filing for bankruptcy might be a better option than continuing to struggle with unpayable debt.

Other unsecured lenders. This includes personal loans, payday advances, and other borrowing not attached to a certain asset, like a car or a house. Lenders vary enormously in how willing they are to work with troubled borrowers. As with credit card and medical bills, you should have a good idea about whether bankruptcy is an option before you approach an unsecured lender.

Child support and alimony. If you’re on the hook for these payments, you may be able to negotiate informally with your ex to lower the amount you pay. But if your ex balks, you may need to go to court to prove that your financial circumstances have deteriorated substantially. Also you typically can’t get rid of the amounts you already owe, although a court may be able to grant you a repayment schedule.

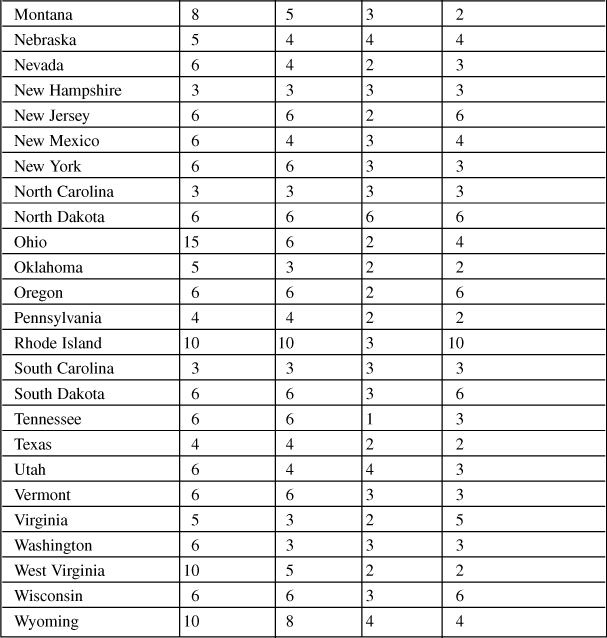

WHY YOU NEED TO FEAR A JUDGMENT

Statutes of Limitations in Years

Table 10.1. The Statute of Limitations (in Years) for Different Kinds of Agreements

Source: Nolo.com

Dealing with Collection Agencies

If you’ve left a bill unpaid for so long that it’s been turned over to a collector, your options and choice of best tactics have changed.

No longer can you hope to elicit the creditor’s interest in rehabilitating your debt and keeping you as a customer. At this point, your account typically has been “charged off”—an accounting term that means the creditor has decided that repayment is unlikely. The creditor usually takes a tax write-off for the loss and passes the account to collections.

Some creditors do their collections in-house using a special department. Others give the accounts to outside collection agencies on a “contingency” basis, which means the collector keeps a portion of what’s collected. Finally, a creditor may sell its overdue accounts to a collection agency outright for pennies on the dollar. (The price drops the older the debt or the more difficult the collection is perceived to be.)

In general, in-house collectors are the most flexible and the most likely to modify how the negative account appears on your credit report if you can repay or satisfactorily settle the debt.

But if you can repay even part of your debt, you should negotiate with a collector as to how the debt will be reported to credit bureaus. Most have more flexibility than they’re willing to admit to erase or minimize negative marks.

Here’s what you need to keep in mind:

Don’t ignore them. In the past, refusing to answer the phone or respond to collection letters was a legitimate tactic because it spared you potential verbal abuse and kept you from saying things that could come back to haunt you. Today, however, too many collectors respond to your lack of response by suing you. Even if you can’t pay, debt expert Gerri Detweiler advises, you should respond. Don’t launch into long excuses. Collectors really aren’t interested in your tales of woe; many just assume you’re lying, no matter what you say, and any details you divulge could be used against you. You also don’t want to make a bunch of promises you can’t keep, especially if the debt is still within the statute of limitations; the collector might get annoyed and decide to sue. Keep your responses as brief as possible. If you can’t pay, say so.

Know your rights. Tiffany owed $2,000 on her Visa, an account that had been turned over to a law firm for collection. Then she got an unexpected call—from someone who claimed to be a sheriff.

“[He said] that if I didn’t return the call from the collector (about the debt), a warrant would be issued,” Tiffany said.

Of course, the call wasn’t from a sheriff. Owing money typically isn’t a crime, and local law enforcement typically won’t issue warrants for credit card debts. Posing as a law enforcement officer is a crime, though. Unfortunately, it’s such a common tactic that it is specifically prohibited by the federal Fair Debt Collection Practices Act.

The act governs what third-party collection agencies can and can’t do in pursuit of a debt. It’s well worth reading. It is available on several Web sites, or you can get the Federal Trade Commission’s pamphlet on the issue by calling 1-877-FTC-HELP.

Here are some very common practices that are actually illegal:

• Calling you at odd hours, such as before 8:00 a.m. or after 9:00 p.m.

• Calling you repeatedly

• Calling you at work if you’ve made it clear that your employer doesn’t allow such calls

• Telling others, such as your friends, family, or neighbors, about the debt

• Using obscene or profane language

• Threatening any action that they don’t intend to take or that they are barred from taking, such as suing you over an out-of-statute debt

Collection agencies and other creditors also aren’t allowed to change the date on a delinquent debt to make it appear younger than it actually is, but such illegal practices are still surprisingly widespread.

Collectors also may fail to follow the law that governs what information they are supposed to provide you. Within five days after contacting you, the collector is supposed to send you a written notice telling you how much you owe, the creditor’s name, and what you must do if you believe you don’t owe the money.

If you send a letter disputing the debt to the collector within 30 days of getting the written notice, the collector is required to either send you proof of the debt, such as a copy of the bill for the amount owed, or cease collection activities.

Again, violations of the laws governing debt collection are so common that some borrowers have made a pastime out of suing collectors that break the law because consumers can collect up to $1,000 per violation in small-claims court. One of my readers, a tax preparer in Tucson, told me he collected $5,000 from collection agencies in a single year in small-claims court.

You also might consider visiting one of the many Internet message boards such as CreditBoards.com, where battle-hardened debtors share tips and ideas for dealing with creditors. Because tactics change constantly and vary by agency, these can be an invaluable resource. Just remember that anyone can join these forums; take the advice with a grain of salt and don’t rely on them for legal advice.

Negotiate hard. You’ll be in the best negotiating position if you can offer a lump sum to settle the debt with a collector. But even if you can offer only payments, try to offer less than you can actually pay. You might be surprised at how quickly your collectors agree to settle. Typically, a collector pays only pennies on the dollar to buy your debt, so even a small payment represents a profit. Start by offering 30% of the total and negotiate from there.

You should try hard to get some kind of concession from the collector about how the debt will be reported to the credit bureaus. Typically, you can’t get the original creditor to erase the original delinquency and charge-offs from your credit report. But collectors are often willing to go along with “pay for deletion,” which means they’ll stop reporting the collection account to the bureaus in exchange for your payment.

Some collectors take money from a debtor and then wind up selling the unpaid portion of the debt to another collector. Or a collector might report the unpaid portion as “forgiven debt” to the IRS—which promptly sends you a tax bill.

Dennis in Minnesota didn’t know this was a possibility when he negotiated a settlement with a collection agency. He had recently found a job after an extended period of unemployment and was eager to put this debt behind him and begin rebuilding his credit.

“The debt was settled for about 50 cents on the dollar,” Dennis wrote me. “A few days ago I received a notice from the IRS that I had failed to report income on my [latest] tax return. It turns out that the IRS considers the [unpaid debt to be] income. I had never considered this at the time and still cannot see how this can be considered income. But the IRS is the IRS, so I will pay the taxes that are due as soon as possible. I will also have to file an amended state tax form to finally get this matter straightened out.”

If Dennis had known about the potential tax treatment of unpaid debt, he might have been able to negotiate with the collection agency not to report it to the IRS—or he could at least have put aside some cash to pay the bill.

Interestingly, some borrowers report that collection agency representatives are more willing to play ball at the end of the month. These folks are usually paid on commission and may be facing quotas, just like car salespeople.

Trust no one. Obviously, with deception so widespread, you want to be skeptical in your negotiations. Just as the collector assumes you’re lying, you probably should assume the same about him or her. Some collectors will promise you just about anything in return for a payment and then renege.

Margaret thought she had a deal with the collection agency that took over her credit card debt:

“I agreed to pay the debt by sending $100 a month if they would not add any finance charges [or interest to the debt],” she wrote. “The debt started at $3,294, and after six months my debt is at $3,271, only $23 less, [even though] I’ve sent them $600.”

You’ll want to get any agreements you make with a collector in writing and in advance of sending any money. In fact, you should document everything about your negotiations. Keep good notes, and tape your conversations if at all possible. (In some states, it’s okay to record a telephone conversation without the other party’s permission, but to be safe you should tell the other party what you’re doing.)

Whatever happens, don’t give a creditor a postdated check or agree to automatic payments drawn from a bank account or charged to a credit card. Give collectors as little information as possible. Don’t reveal bank account numbers or where you work, for example.

For more information on dealing with collectors, check out Detweiler’s site, DebtCollectionAnswers.com.

What If Your Creditors Won’t Budge?

Barbara in Connecticut cosigned $40,000 in private student loans for her son, who then had trouble finding work after college. She and her husband had their own troubles, including injuries and job losses that reduced their income substantially.

The family fell behind on its payments, and the loans were turned over to collections. Their pleas for a repayment plan they can afford have been rebuffed.

“[We] feel as if we are living in a nightmare...we tried harder than hard,” Barbara wrote. “They could care less.”

The National Consumer Law Center runs a site called Student Loan Borrower Assistance at www.studentloanborrowerassistance.org that provides information and resources for dealing with troublesome student loan debt. If your efforts to negotiate with such lenders fail, or you’re having trouble reaching agreement with other creditors or collectors, consider hiring an attorney to make your case. You can get referrals from your local bar association or the National Association of Consumer Advocates at 202-452-1989 or www.naca.net.

Summary

Debt problems don’t get better on their own. The sooner you take action, the more options you’ll typically have to fix the situation:

• Make a plan. Before approaching your creditors, you need to prioritize your debts, identify your resources, and create a tentative payment plan.

• Know your options. Lenders’ willingness to negotiate and their options for pursuing payment vary widely. Your ability to erase debts also depends on your financial situation and the type of debt.

• Take great care in dealing with collectors. Unfortunately, violations of the federal laws designed to protect borrowers are fairly common. You should know your rights, negotiate hard, and document every agreement in writing.