Who Regulates Financial Institutions?

Several different federal agencies regulate the different kinds of financial institutions. This section focuses briefly on those agencies. These agencies enforce the consumer protection laws discussed later in this chapter. State governments may also regulate financial institutions. However, this chapter does not discuss that type of regulation.

There are four federal regulatory agencies for U.S. financial institutions. These agencies make sure that U.S. financial institutions are sound, which means they are financially healthy and safe. These agencies also make sure that their institutions follow federal law. The federal bank regulatory agencies are:

- The Federal Reserve System

- The Federal Deposit Insurance Corporation

- The National Credit Union Administration

- The Office of the Comptroller of the Currency

TABLE 4-1 summarizes the agencies and the financial institutions that they regulate.

TABLE 4-1 Federal Banking Regulatory Agencies

| AGENCY NAME | PRIMARY REGULATORY RESPONSIBILITY |

|---|---|

Federal Reserve System (The Fed) |

State-chartered member banks Bank holding companies Foreign banks that operate in the United States Foreign branches of U.S. member banks |

Federal Deposit Insurance Corporation (FDIC) |

Federally insured depository institutions State-chartered banks that are not members of the Fed |

National Credit Union Administration (NCUA) |

Federally chartered credit unions Federally insured credit unions |

Office of the Comptroller of the Currency (OCC) |

Nationally chartered banks Federal savings associations U.S. federal branches of foreign banks |

The Federal Reserve System

Congress created the Federal Reserve System in 1913. The Federal Reserve Act of 1913 was passed to address financial uncertainty.11 Bank and business failures were having a tremendous impact on the U.S. economy. The Federal Reserve Act was intended to provide the nation with a more stable economy.

![]() NOTE

NOTE

The U.S. Gross Domestic Product (GDP) fell by 4.8 percent during the first quarter of 2020. This was a result of the 2020 COVID-19 nationwide public health emergency.12

The Federal Reserve System is the central bank of the United States.13 Essentially, it is a bank for other banks, as well as a bank for the federal government. The Fed, an independent federal agency that reports directly to Congress, is responsible for directing the nation’s monetary policy and maintaining the stability of the U.S. financial system.

In addition to serving as the bank for the U.S. government, the Fed is the main regulatory authority for:

![]() NOTE

NOTE

The Federal Reserve System is also known as “the Fed.”

- State-chartered banks that choose to become members of the Federal Reserve System

- Bank holding companies. The Fed also supervises companies that control banks (called bank holding companies)

- Foreign banks that operate in the United States

- Foreign branches of U.S. member banks.

State-chartered banks are not required to become Fed members. State-chartered banks that are not Fed members are regulated by the Federal Deposit Insurance Corporation (FDIC). National banks are required to be members of the Federal Reserve System, but they are not regulated by the Fed. The Fed supervises and examines the financial institutions that it regulates to make sure that those institutions are complying with the law. Because many different agencies regulate banks, the Fed’s enforcement authority extends to state member banks of the Fed and some foreign banks that operate in the United States.

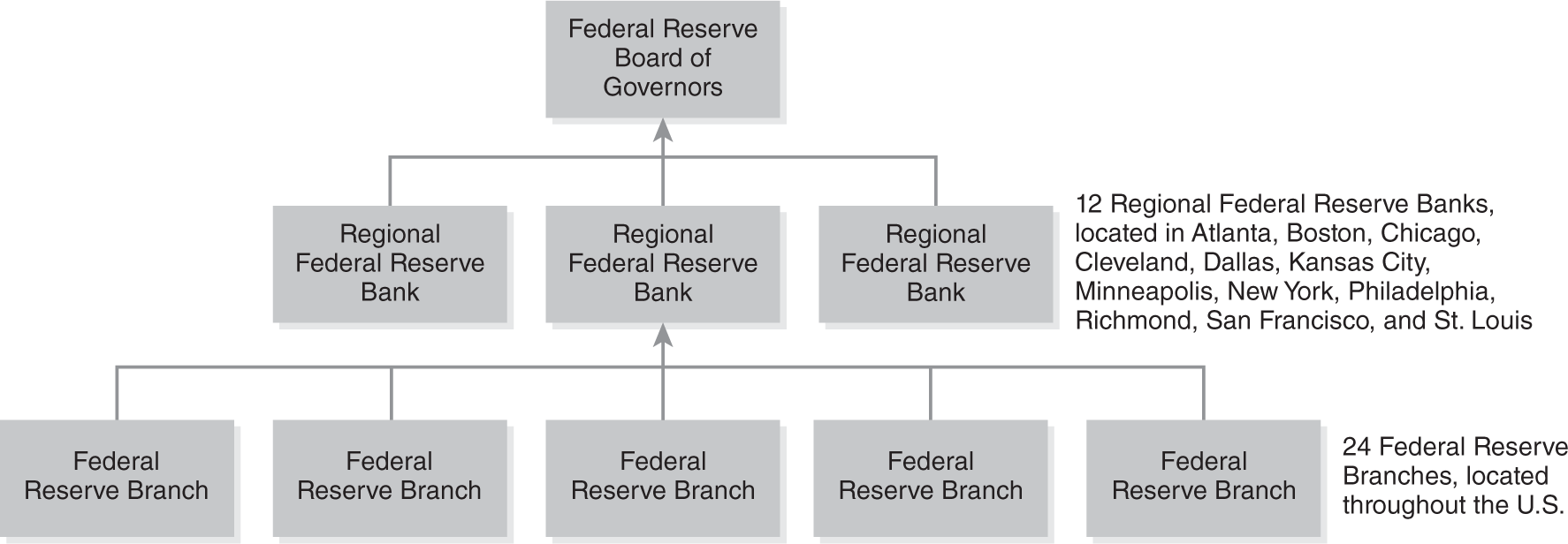

The structure of the Fed includes a Board of Governors, located in Washington, DC, and 12 regional Federal Reserve banks. The Board consists of seven members who are nominated by the president and must be confirmed by the Senate. Each member serves for a single 14-year term. The terms of each member are staggered so that only one term expires at a time. The chair and vice-chair of the Board of Governors are also nominated by the president and confirmed by the Senate. These positions are filled by current members of the Board of Governors, who serve in these positions for a 4-year term.

There are 12 regional Federal Reserve banks located throughout the United States that serve different geographic districts. These Reserve Banks have 24 branches that carry out a variety of banking functions. The main customers of the Reserve Banks are other banks; the Reserve Banks hold the cash reserves of other institutions and distribute U.S. currency and coin within their region. They also supervise and review member banks to make sure that they are sound. FIGURE 4-1 illustrates the structure of the Federal Reserve System.

FIGURE 4-1

The structure of the U.S. Federal Reserve System.

![]() NOTE

NOTE

A depositor is a person who has deposited money into an account at a bank. Deposit accounts allow money to be added and withdrawn by the account owner. A savings or checking account is a type of deposit account, whereas an investment account is not a deposit account.

Federal Deposit Insurance Corporation

The FDIC was formed in 1933 to provide deposit insurance to banks. Congress formed the FDIC originally as a temporary government corporation under the Banking Act of 1933.14 The FDIC was formed in response to bank failures during the Great Depression.

![]() NOTE

NOTE

From 1929 to 1933, bank failures resulted in about $1.3 billion in losses to depositors.

No depositor has lost any money on insured funds because of a bank failure since FDIC insurance began on January 1, 1934.15 Congress made the FDIC a permanent federal agency in 1935 under the Banking Act of 1935.

The FDIC insures deposits made in banks and savings associations. The FDIC ensures deposit accounts only. It does not insure securities or mutual funds. When the FDIC was formed in 1933, the original deposit insurance limit was $2,500. In 2020, the deposit insurance limit was 100 times that amount, or $250,000.

![]() NOTE

NOTE

To help protect the U.S. economy during the recession in 2008 to 2009, Congress raised the FDIC insurance amount to $250,000 per depositor.

The FDIC insures deposit accounts in almost every bank in the United States for protection in the event of a bank failure. If a bank fails, the FDIC returns the money that a customer put in the bank, up to the deposit insurance limit. However, the FDIC works to prevent bank failures by monitoring the economy. It also enforces regulations that require banks to act in a sound manner. All national banks are required by law to be insured by the FDIC.

The FDIC, the primary federal regulator for state-chartered banks that do not join the Federal Reserve System, examines and supervises over 3,000 banks. The FDIC reviews the banks that it regulates to make sure that those institutions are complying with the law.

The FDIC has a five-member board of directors. Three of the directors are appointed by the president and confirmed by the Senate. These members each serve 6-year terms. The other two members of the board are the government officials who serve as the comptroller of the currency and the director of the Consumer Financial Protection Bureau (CFPB). No more than three of the members of the FDIC board may be from the same political party. The chair and vice-chair of the board of directors are also nominated by the president and confirmed by the Senate. These positions are filled by current members of the board and have 5-year terms. The FDIC has eight regional offices.

National Credit Union Administration

Congress enacted the Federal Credit Union Act in 1934.16 That law allowed federally chartered credit unions to form. The National Credit Union Administration (NCUA) is an independent federal agency formed in 1970.17 Its role is to charter and supervise federal credit unions.

A credit union is a cooperative financial organization that can have federal, state, or corporate affiliations. Members of a credit union share the same affiliation. They might live in the same city or work for the same employer. A credit union is a nonprofit institution that is run by its members, who pool their money together at a credit union to save and make loans to one another.

![]() NOTE

NOTE

Federal credit unions often use the word federal in their name. They may also use the initials F.C.U., or “federal credit union.”

The NCUA operates the National Credit Union Share Insurance Fund (NCUSIF), created by Congress in 1970. All federal credit unions must be insured by the NCUSIF. This fund also insures deposits in state-chartered credit unions that qualify for the fund. The NCUSIF operates similar to the deposit insurance provided by the FDIC. It protects almost 95 million federal credit union account holders. It also insures a majority of state-chartered credit unions.

![]() NOTE

NOTE

No credit union member has lost any money on deposit accounts because of the failure of credit unions insured by the NCUSIF.

The NCUA supervises all federal credit unions and NCUSIF-insured state credit unions. It also issues guidance and enforces the provisions of the Federal Credit Union Act. The NCUA is the regulatory enforcement authority for federal credit unions, and it shares enforcement authority for some laws with other federal agencies. The NCUA enforces the GLBA consumer privacy provisions for federal credit unions. The FTC enforces those provisions for federally insured, state-chartered credit unions.

The NCUA has a three-member board of directors. The president nominates board members, who then must be confirmed by the Senate. Board members serve 6-year terms. Their terms are staggered so that only one term expires at a time. No more than two board members can be from the same political party. The NCUA has five regional offices across the United States that charter and supervise federal credit unions in their regions.

Office of the Comptroller of the Currency

The Office of the Comptroller of the Currency (OCC) was originally established in 1863.18 The National Bank Act of 1864 is the law that authorizes the OCC today. The OCC, which is a part of the U.S. Department of the Treasury, charters and supervises national banks and federal savings associations. Federal savings associations, also called thrifts, are organizations that accept savings account deposits and then invest the proceeds of those deposits in home mortgages. National banks and federal savings associations are members of the Federal Reserve System and are required to be insured by the FDIC.

![]() NOTE

NOTE

In July 2011, the Office of Thrift Supervision became part of the OCC. Before becoming part of the OCC, the Office of Thrift Supervision was the entity responsible for regulating federal savings associations.

The OCC is led by a comptroller who is appointed by the president, confirmed by the Senate, and serves a 5-year term. The comptroller also serves as a member of the board of directors of the FDIC. The OCC supervises and regulates about 1,400 national banks and federal savings associations. It has the authority to enforce laws and regulations against national banks and federal savings associations.

![]() NOTE

NOTE

National banks often use the word national or the phrase national association in their name. They also may use the initials “N.A.”

FYI

Federal savings banks and savings and loan associations often use the words federal, federal association, federal savings bank, or federal savings and loan association in their name. They also may include initials for those terms, such as “F.A.,” “F.S.B.,” or “F.S.L.A.”

Special Role of the Federal Financial Institutions Examination Council

Congress established the Federal Financial Institutions Examination Council (FFIEC) in 1979. It was created by the Financial Institutions Regulatory and Interest Rate Control Act of 1978 (FIRA).19 The FFIEC promotes uniform practices among the federal financial institutions and their regulators. Its purpose is to:

- Establish principles and standards for the examination of federal financial institutions.

- Develop a uniform reporting system for federal financial institutions.

- Conduct training for federal bank examiners.

- Make recommendations regarding bank supervision matters.

- Encourage the adoption of uniform principles and standards by federal and state banks.20

The council has six members. They are:

- The chair of the FDIC

- The chair of the NCUA

- The comptroller from the OCC

- The director of the CFPB

- A member of the Board of Governors of the Fed

- The chair of the FFIEC State Liaison Committee

The chair of the FFIEC serves for 2 years. The chair position rotates among members of the council. The member agencies fund the FFIEC.

![]() NOTE

NOTE

An examination is the periodic evaluation of a bank, which includes a review of the health of the bank and its compliance with banking regulations. An examination might include a review of management and operations, as well as the bank’s policies. A bank examiner is the person who conducts this review.

The FFIEC has six task forces. Representatives from each agency serve on each task force, which includes at least one senior official from each of the member agencies:21

- Consumer compliance—This task force promotes a uniform approach to consumer protection laws and regulations. It develops proposed policies and procedures for the agencies to use in their regulatory activities.

- Examiner education—This task force oversees the FFIEC’s intra-agency examiner education programs. The task force also develops specific programs in response to requests from the FFIEC or its members.

- Information sharing—This task force promotes sharing electronic information among FFIEC members to help them meet their regulatory responsibilities.

- Reports—This task force establishes uniform financial reports for FFIEC members.

- Supervision—This task force establishes supervision and examination procedures for FFIEC members. Its purpose is to help reduce regulatory burden by promoting effective supervision and examination practices.

- Surveillance systems—This task force develops systems to monitor the financial condition and performance of financial institutions.

The FFIEC is required to submit an annual report to Congress on its activities. The FFIEC does not regulate financial institutions because it has no authority to do so. The federal agencies carry out their own enforcement actions against banks in their jurisdiction.

Special Roles of the Consumer Financial Protection Bureau and the Federal Trade Commission

The CFPB and the Federal Trade Commission (FTC) are two entities that have consumer protection functions.

Consumer Financial Protection Bureau

The CFPB was created in 2010,22 and its purpose was to protect consumers in the financial industry. Unlike the Fed, FDIC, NCUA, and OCC, which regulate financial institutions directly, the CFPB focuses solely on consumers. The CFPB is an independent agency that ensures that all consumers have access to financial products and services. It also ensures that financial products and services are offered in ways that are fair and competitive. The CFPB has the authority to examine financial institutions to ensure that the institutions are complying with federal consumer financial laws.

The CFPB is led by a director who is nominated by the president and confirmed by the Senate. The CFPB has six primary divisions and several advisory committees, including:

- Consumer advisory board

- Community bank advisory council

- Credit union advisory council

- Academic research council

Federal Trade Commission

The FTC is an independent federal agency created by Congress in 1914 under the Federal Trade Commission Act.23 Similar to the CFPB, the FTC is an important regulatory authority for consumer protection issues. The mission of the FTC is to protect consumers and make sure that business is competitive. It tries to eliminate practices that are harmful to business. The FTC has responsibilities under 46 different federal laws. Most of these laws include consumer protection elements.

Under the Federal Trade Commission Act, the FTC can investigate “the organization, business, conduct, practices, and management of any person, partnership, or corporation engaged in or whose business affects commerce.”24 It also can stop unfair and deceptive acts or trade practices.25 Most of the FTC’s authority comes from this law. The FTC makes and enforces rules for some parts of the financial industry. However, the FTC cannot regulate banks, thrifts, or federal credit unions—the other federal banking regulatory agencies already regulate them. The FTC does enforce laws at nonbanking institutions such as consumer finance companies, debt counseling companies, and credit bureaus.

The FTC is led by five commissioners. Each commissioner serves a 7-year term. They are nominated by the president and confirmed by the Senate. The president also chooses one commissioner to act as the chair. To maintain the independence of the FTC, no more than three commissioners can belong to the same political party.26 The FTC has seven regional offices across the United States.

![]() NOTE

NOTE

Unfair trade practices are business practices that a consumer cannot avoid and that cause injury. Deceptive trade practices are any business practices that include false or misleading claims.

In 2012 the CFPB and the FTC signed an agreement to coordinate their efforts to protect consumers.27 The agreement also helped to avoid duplication of effort between the two agencies. As part of the agreement, the agencies agreed to meet regularly and to coordinate their rulemaking efforts. They also agreed to share consumer complaints. Both agencies work closely with federal banking regulatory agencies when enacting rules to protect consumer financial information.