15

Closing the Books in QuickBooks Online

After you have entered all of your business transactions into QuickBooks for the year, you will need to finalize your financial statements so that you can hand them off to your accountant to file your taxes. To ensure you have recorded all business transactions for the financial period, we have included a checklist that you can follow to close your books. Closing your books will ensure that no additional transactions are entered into QuickBooks once you have finalized your financial statements. If you have a bookkeeper or an accountant who manages your books, they should ensure that all of the steps have been completed. In this chapter, we will cover each item on the checklist. This includes reconciling all bank and credit card accounts, making year-end accrual adjustments (if applicable), recording fixed asset purchases made throughout the year, recording depreciation, taking a physical inventory, adjusting retained earnings, and preparing financial statements.

Pro Tip: Many of the tasks in this section are typically performed by an accountant. Adding your tax preparer or CPA as a user will allow them to access your QuickBooks data – this will allow the accountants to run reports and review the items needed, so that they can perform these tasks in service to preparing your tax return. Later in this chapter, we will show you how to give your accountant access to your data.

The chapter objectives are summarized as follows:

- Reviewing a checklist for closing your books

- Reconciling all bank and credit card accounts

- Making year-end accrual adjustments

- Reviewing new fixed asset purchases & adding them to the chart of account

- Making depreciation journal entries

- Taking physical inventory and recoding inventory adjustments

- Adjusting retained earnings for owner/partner distributions

- Recording journal entries

- Setting a closing date and password

- Preparing key financial reports

- Giving your accountant access to your data

By the end of this chapter, you will know all of the tasks you need to complete in order to close your books for the year. While most small businesses close their books annually, if you close your books on a monthly or a quarterly basis, you will still need to follow the steps outlined in this chapter. In the following section, we will cover the details of the checklist.

The US edition of QBO was used to create this book. If you are using a version that is outside the United States, the results may differ.

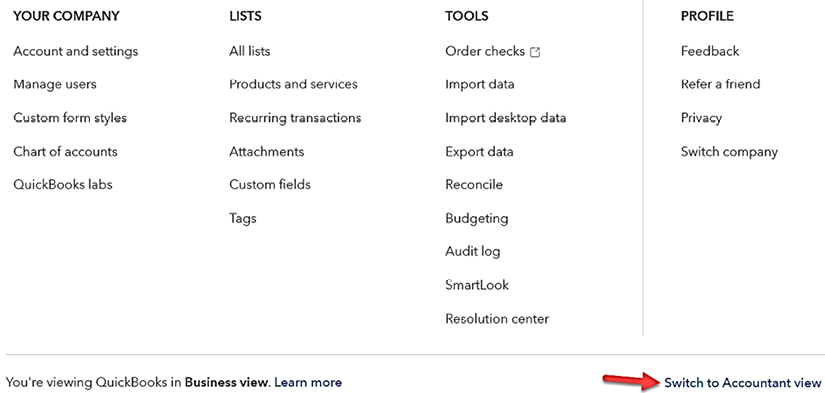

Please note the screenshots in this chapter have been taken using the Accountant view menu. In Chapter 1, Getting Started with QuickBooks Online, we introduced a new menu called Business view. If you are in Business view, you will need to switch to the Accountant view menu so that your screen resembles the images shown throughout this book. To do this, click on the gear (settings) menu (located in the upper-right corner) and select Switch to Accountant view as shown in Figure 15.1 below:

Figure 15.1: Switching to the Accountant view

Reviewing a checklist for closing your books

As discussed, there are several steps you will need to take in order to close your books for the financial period. How often you close your books (for example, monthly, quarterly, or annually) will determine how often you need to complete these steps. Remember the importance of closing your books, as this will ensure that all transactions for the financial period have been recorded and that your financial statements are accurate, which is important because your accountant will use them to file your business tax return.

The following is a checklist of the steps you need to complete in order to close your books. You should complete them in the order presented:

- Reconciling all bank and credit card accounts

- Making year-end accrual adjustments

- Reviewing new fixed asset purchases and adding them to the chart of accounts

- Making depreciation journal entries

- Taking physical inventory and reconciling this with your books

- Adjusting retained earnings for owner/partner distributions

- Setting a closing date and password

- Preparing key financial reports

The purpose of closing the books is to ensure that the elements that impact the financial statements are reviewed and deemed accurate before finalizing the financial statements, which will in turn be used to file your business tax return. We will discuss each of these eight steps in detail, starting with reconciling all bank and credit card accounts.

1. Reconciling all bank and credit card accounts

In Chapter 9, Reconciling Uploaded Bank and Credit Card Transactions, you learned how to reconcile your bank and credit card accounts. It’s important for you to reconcile these accounts before closing the books so that you can ensure that all income and expenses for the period have been recorded in QuickBooks.

This will ensure that your financial statements are accurate and that you don’t miss out on any tax deductions.

2. Making year-end accrual adjustments

If you are on the accrual basis of accounting, you need to make sure that all income and expenses that have been incurred for the period are recorded. As discussed in Chapter 1, Getting Started with QuickBooks Online, accrual basis accounting means that you recognize income when services have been rendered, regardless of when payment is received. The same concept is applied to expenses. For example, if you made a purchase in December but have not yet received the bill for it, you will need to record an adjusting journal entry before you close the books in order to record the purchase. Some examples of accruals that may be required are prepaid expenses and wages. Be sure to consult with your accountant for the proper recording of these transactions. We will discuss journal entries in more detail later in this chapter.

Pro Tip: Record all accounts receivable for the end of the period, which means invoicing all customers for work performed. This will ensure that all income is recorded and shows up on your profit and loss (income statement) report. Similarly, be sure to record all accounts payable (vendor bills) for any expenses incurred in the period. This will ensure that all expenses show up on the profit and loss (income statement).

3. Reviewing new fixed asset purchases and adding them to the chart of accounts

If you purchased any fixed assets during the year, you should add these to QuickBooks. As mentioned in Chapter 1, Getting Started with QuickBooks Online, fixed assets can be equipment purchased for your business such as computers or printers. Furniture such as a desk or chair are also considered fixed assets. Fixed assets are subject to depreciation, which is a tax-deductible expense. Depreciation is the reduction of the value of a fixed asset due to wear and tear. Tax-deductible expenses can reduce your tax bill, so you want to make sure that you take all of the deductions to which you are entitled. If you have not recorded new fixed asset purchases, then you will not have depreciation expenses recorded, which means you will miss out on what could be a significant tax deduction. It’s also important to conduct a physical check to ensure that all of the assets on the books still exist and have not been disposed of.

To add fixed assets to QuickBooks, you will need to have the following information on hand:

- Date of purchase

- Purchase price

- Type of asset

- Make and model (if applicable)

- Year

Pro Tip: Your tax preparer should have a detailed list of fixed assets that have been reported on previous tax returns. It is a good idea to review this list annually to ensure it includes new purchases and/or disposal of assets.

Follow these steps to add a fixed asset to QuickBooks:

- From the left menu bar, click on Accounting, as indicated in Figure 15.2:

Figure 15.2: Navigating to Accounting

- Select the chart of accounts and then click the New button, as indicated in Figure 15.3:

Figure 15.3: Clicking the New button

- For a new fixed asset, complete the fields as shown in Figure 15.4:

Figure 15.4: Entering details for a fixed asset

The following is a brief explanation of the fields that need to be completed for a new fixed asset:

- Account type: Select Assets as shown in Figure 15.4.

- Save account under: From the dropdown menu, select Computers & tablets.

- Tax form section: This field should auto-populate based on the information in the save account under field. In our example, Fixed Asset Computers is the correct tax form section.

- Account name: Type the name of the fixed asset in this field. In our example, this is

Office Computer. - Description: Type a more detailed description of the fixed asset in this field or you can enter the account name again. In our example, we have entered

Office Computer. - Starting date and opening balance: Select the date that the asset was purchased in the starting date field. In our example, this asset was purchased at the Beginning of this year. The original cost should be entered into the account balance field, In our example, the original cost is

$2,100. This amount will be used to calculate depreciation.

- Click the Save and Close button to add the asset to your chart of accounts list.

Be sure to complete these steps for each fixed asset you have purchased during the accounting period. After adding fixed assets to QuickBooks, you need to record depreciation expenses for the period.

4. Making depreciation journal entries

Depreciation is the reduction in value of an asset due to wear and tear after it has been in service for a period of time. To reflect the reduced value, you must record the depreciation expense in your books. Depreciation is also a tax-deductible expense, which can help to reduce your overall tax liability. After adding fixed assets to QuickBooks, you need to record depreciation expenses for the period. Unfortunately, QuickBooks does not compute depreciation for you. Therefore, you will need to calculate depreciation manually, or have your accountant do this for you. In the Recording journal entries section of this chapter, we will show you how to record journal entries in QuickBooks.

5. Taking physical inventory and recording inventory adjustments

Reconciling inventory involves making sure that the product you have on your shelf matches what your books reflect as on-hand inventory. You should take a physical inventory count at least once a year, if not more often. After taking a physical count, any discrepancies between the books and the physical count should be recorded in QuickBooks as inventory adjustments. After recording these inventory adjustments, your books and your warehouse will be in sync.

Follow these steps to record inventory adjustments in QuickBooks:

- Click on the + New button and select Inventory qty adjustment in the Other column, as indicated in Figure 15.5:

Figure 15.5: Choosing Inventory qty adjustment

- Complete the fields for the inventory adjustment, as indicated in Figure 15.6:

Figure 15.6: Completing the fields to record the inventory adjustment

The following is a brief explanation of the fields that need to be completed in order to record an inventory adjustment:

- Adjustment date: Enter the effective date of the adjustment. This date should be on or before the last day of the closing period. For example, if you close your books annually, this date should be as of 12/31/xx if you are on a calendar year.

- Inventory adjustment account: Inventory Shrinkage is the default account that will appear in this field. However, you can click the dropdown arrow and select a different account or add a new one.

- PRODUCT: From the dropdown menu, select the item for which you are making an adjustment.

- DESCRIPTION: This field will automatically be populated based on the description in QuickBooks. You can also enter a description directly in this field.

- QTY ON HAND: This field will automatically be populated with what you currently have recorded in QuickBooks. This field cannot be adjusted.

- NEW QTY: Enter the quantity, based on the physical count that was taken in this field.

- CHANGE IN QTY: QuickBooks automatically computes the adjustment required by taking the difference between the QTY ON HAND and NEW QTY values entered.

- Memo: Enter a brief explanation as to why the adjustment was made.

If you have extensive inventory tracking requirements that go beyond what’s available in QuickBooks Online, visit the Intuit app marketplace, where there are over 700 add-on programs that integrate seamlessly with QBO. In Chapter 16, Finding Apps and Handling Special Transactions in QuickBooks Online, we show you how to navigate the QuickBooks App Center.

6. Adjusting retained earnings for owner/partner distributions

Retained earnings are the cumulative amount of your income and expenses for the prior period(s). This amount will post to the retained earnings account after the end of your fiscal/calendar year has been closed. QuickBooks will automatically make this entry for you. Depending on the type of organization (Corporation, partnership, llc, sole proprietorship, or non-profit), you may need to move this balance to other equity accounts.

To distribute profits to the owners, you will need to create a journal entry to an equity account entitled owner’s draw or owner distributions and offset it with retained earnings. Be sure to consult with your CPA or tax preparer if you are not familiar with this process.

To summarize what we have covered so far, many of the steps in the closing process are designed to review the transactions that have been recorded throughout the fiscal year and make adjustments as needed for accruals such as wages, depreciation for fixed assets, and adjustments to retained earnings for owner/partner distributions. The primary way these closing adjustments are recorded is through journal entries. We will take a brief break from going through the checklist now, so that we can discuss this next.

Recording journal entries

A journal entry is used to adjust your books for transactions that have not been recorded throughout the year. Depreciation expense for fixed assets, income and expense accruals, and adjustments to retained earnings are three examples we have discussed in this chapter.

Follow these steps to record a journal entry in QuickBooks:

- Click the + New button and select Journal entry, as indicated in Figure 15.7:

Figure 15.7: Selecting Journal entry below the Other column

- A screen will appear similar to the one shown in the following screenshot:

Figure 15.8: Journal Entry template

The following is a brief explanation of the fields that need to be completed in order to record a journal entry:

- Journal date: Enter the effective date of the journal in this field.

- Journal no.: QuickBooks will automatically populate this field with the next available journal number. If this is the first journal entry you have recorded, you can enter a starting number (such as

1000), and QuickBooks will increment each journal entry number thereafter. - ACCOUNT: Select the account from the drop-down menu.

- DEBITS: Enter the debit amount in this field.

- CREDITS: Enter the credit amount in this field.

- DESCRIPTION: Type a detailed description of the purpose of the journal entry in this field. Adding a detailed description is recommended; it is helpful when referring to a journal entry and explaining why the entry was made.

- Memo: Include a brief description of the fixed asset that you are recording this journal entry for.

Be sure to record all journal entries prior to generating financial statements. If you give your CPA or accountant access to your data, they can record all of the necessary journal entries and then generate the financial reports required to file your tax returns. We are now ready to continue with our checklist.

7. Setting a closing date and password

In an effort to maintain the integrity of your data, you should set a closing date and password after you have entered all transactions for the closing period. By setting a closing date, users will receive a warning message if they attempt to enter transactions that affect the closing period. For example, if you set a closing date of 12/31/22, users will receive a warning message if they attempt to enter any transactions dated 12/31/22 or prior.

Follow these steps to set a closing date and password in QBO:

- Click on the gear icon and then select Account and Settings in the Your Company column, as indicated in Figure 15.9:

Figure 15.9: Selecting Account and Settings in the Your Company column

- Click on the Advanced tab, as indicated in Figure 15.10:

Figure 15.10: Clicking the Advanced option

- The Accounting preferences are located at the very top of the next screen, as indicated in Figure 15.11:

Figure 15.11: Reviewing Accounting preferences

In the Close the books section, you can enter the closing date (that is,

12/31/22), which will give users a warning if they attempt to enter transactions dated on the closing date or prior to that date. There are two types of warning messages. The first warning message is Allow changes after viewing a warning. This message will allow users to proceed with entering the transaction after they close out of the warning message. The second warning message is Allow changes after viewing a warning and entering a password. This message requires users to enter a password to proceed with entering transactions. To choose this option, select it from the dropdown field as shown in Figure 17.11 and enter the password you would like to use.

Pro Tip: Since QuickBooks does not have a formal closing process, this is highly recommended to keep users from making changes to years where tax returns have already been filed. Don’t give the closing password to anyone who is not authorized to enter transactions after the closing date.

8. Preparing key financial reports

After you have completed the first seven steps in the closing checklist, you are ready to prepare financial statements. There are three primary financial statements you will need to prepare:

- The trial balance

- The balance sheet

- The income statement (profit and loss report)

In Chapter 11, Business Overview Reports, you learned what the balance sheet and income statement reports are, how to interpret the data, and how to generate these reports in QuickBooks. Your accountant, or certified public accountant (CPA), will also request a trial balance report. A trial balance report lists all of the debits and credits recorded in QuickBooks for the period. If everything has been recorded properly, debits will always equal credits on this report.

Follow these steps to run a trial balance report in QuickBooks:

- Navigate to Reports, as indicated in Figure 15.12:

Figure 15.12: Clicking Reports to navigate to the Reports Center

- In the For my accountant section, click on Trial Balance, as indicated in Figure 15.13:

Figure 15.13: Running the trial balance report

- The trial balance report will appear. Click the Customize button to see the following options:

Figure 15.14: Reviewing the report customization options

There are a number of options available to customize the trial balance report. The following is a brief description of some of the information that can be customized:

- Report period: You can select a preset report period such as Last Year from the dropdown menu, or type a specific date range in the fields to the right of the preset field.

- Accounting method: As previously introduced in this book, you can choose the accounting method you want to be applied to the report, cash or accrual.

- Number format: There are a variety of options for formatting the numbers on a report. Omitting the cents and excluding accounts with a zero balance are just a couple of the options shown in the preceding screenshot.

- Rows/Columns: Choose which rows/columns are visible on the report.

- Header: You can edit the company name and the title of the report in the header section.

- Footer: You can choose to show the date/time when the report was prepared.

- Alignment: You can decide how to best align the information that appears in the header and footer sections of the report.

- When you are done with your customizations, click the Run report button.

- A report similar to the one in Figure 15.15 will appear:

Figure 15.15: Sample trial balance report

As discussed, the total debits column should always equal the total credits column, as it does in the preceding report. If it does not, you will need to look into any discrepancies. The good news is, 99.99% of the time, this report will balance because QuickBooks does not allow you to post one-sided journals, which means that for every debit, there is always an offsetting credit to keep things in balance.

Pro Tip: If you do have a trial balance that does not balance, you should calculate the difference between the debits and credits, and then look for that amount on the report. Most likely, there is an amount in one of the columns (debit or credit) that does not appear in the other column.

To summarize, you will need to review three key financial reports before closing your books: the balance sheet, the income statement, and the trial balance report. If you have a CPA or an accountant who reviews your financials and prepares your tax return, you can give that person access to your books so that they can run these reports without having to bother you. We will discuss giving your accountant access to your data next.

Pro Tip: Always review the information on your reports one last time before sharing them with any third party outside of your organization. You can set these reports up in memorized groups and send them instead of running them individually. Refer to Chapter 10, Report Center Overview, for more information on this.

Giving your accountant access to your data

If you have an accountant or tax preparer to whom you need to grant access to your data, you can create a secure user ID and password for them. All you need to do is request their email address so that you can send them an invitation to access your data.

Follow these steps to invite an accountant to access your QuickBooks data:

- Click on the gear icon and select Manage Users in the Your Company column, as indicated in Figure 15.16:

Figure 15.16: Selecting Manage Users from the Your Company column

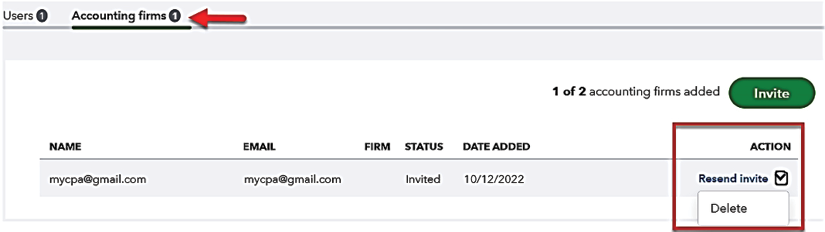

- On the Manage users page, click on Accounting firms, as indicated in Figure 15.17:

Figure 15.17: Clicking on Accounting firms

- Enter your accountant or tax professional’s email address and click on Invite, as indicated in Figure 15.18, to invite your accountant to access your QuickBooks data:

Figure 15.18: Clicking the Invite button

Your accountant will receive an email, inviting them to access your QBO account. They will need to accept the invitation and create a secure password. Their user ID will be the email address that you entered in the form (shown in Figure 15.18).

Once you have given your accountant access to your books, they can simply log in to QuickBooks to get the information they need to prepare your taxes. This is highly recommended if your accountant will be making any year-end adjustments. You can add/remove permissions access as needed if you prefer them only to have access at tax time. To resend an invite or delete access, go back to the Accounting firms tab, and click the arrow to the right of the Resend invite link:

Figure 15.19: Option to resend an invite from the Accounting firms page

Summary

In this chapter, you have learned about the key tasks that need to be completed to close your books for the accounting period. As discussed, you need to reconcile all bank and credit card accounts, record year-end accrual adjustments (if you are on the accrual basis of accounting), add fixed asset purchases, record depreciation expenses, take a physical inventory and make the necessary adjustments, adjust retained earnings for distributions made to the business owners, set a closing date and password, and prepare key financial statements. You can perform these tasks yourself, or you can give your accountant access to your QuickBooks data to take care of this for you.

This chapter is the last one that covers the QuickBooks features most small businesses will use. Congratulations on successfully completing all of the chapters thus far. In the next chapter, we will cover some additional topics, such as adding apps to QBO, managing credit card payments, and recording bad debt expenses.