3

Migrating to QuickBooks Online

Regardless of whether you are currently using another form of accounting software or spreadsheets to manage the books for your business, you will need to gather a few key documents and bits of information to migrate over to QuickBooks Online (QBO), a list of which we gave you at the start of the previous chapter. In addition, the date on which you decide to start implementing QuickBooks will also determine what information is required for a smooth migration. Providing all of the information required will ensure that QuickBooks is properly set up prior to you using it to track your business income and expenses. Otherwise, you could encounter inaccurate and unreliable financial statements, which will make it hard to know your business’ overall health and make filing taxes difficult.

In this chapter, we will help you determine if QBO is right for your business and discuss questions you need to answer before conversion regarding how you will run your business. Then, we will cover the steps of converting your QuickBooks Desktop (QBD) data to QBO. If you are unable to convert your data, you can choose one of the alternatives to converting QBD data. The final section in this chapter will cover how to convert from Excel spreadsheets or pen & paper to QBO.

In this chapter, we will cover the following five key concepts:

- Deciding if QuickBooks Online is right for your business

- Questions to ask yourself in preparation for data conversion

- Converting QuickBooks Desktop data to QBO

- Alternatives to converting QuickBooks Desktop data to QBO

- Converting from Excel spreadsheets or pen & paper to QBO

The US edition of QBO was used to create this book. If you are using a version that is outside of the United States, results may differ.

Deciding if QuickBooks Online is right for your business

It’s important to make sure that moving your business to QBO is the right thing to do. While QuickBooks Online is ideal for many businesses, if one or more of the following is true about your business, you may want to reconsider:

- Multiple businesses: If you have more than one business to manage, you need to know that you will need to purchase a separate QBO subscription plan for each business that has its own federal tax identification number. For example, let’s say I have a tax preparation business and I have a few luxury properties that I rent on Airbnb. These are two separate businesses, which means I would need to purchase two QBO plans. The good news is you can easily create a new QBO account within an existing account and simply toggle between the two as opposed to having two separate logins.

- Comprehensive inventory accounting requirements: If your business manufactures products that require the tracking of multiple items using a bill of materials, you may want to consider using QuickBooks Desktop. In addition, QBO uses the FIFO method to track inventory. That means if you use LIFO or average cost to keep track of your inventory, you will need to convert to FIFO if you plan to convert to QBO.

- Specialized industries: If you are a general contractor, manufacturing and wholesale, retail, non-profit, or professional services business, you may want to consider using QuickBooks Desktop instead of QBO. QuickBooks Desktop has customized software that includes a custom chart of accounts and reports for businesses in these industries. While QBO can be customized to meet the needs of these industries, you will have to invest the time to make the necessary adjustments.

If you decide that QBO is the right move for your business and you are currently using QBD, you need to review the list of key features that you may currently use in QBD that are not available in QBO. Finally, you need to review the data that will not convert from QBD to QBO.

This is important because there may be features that are not available in QBO that you need to run your business. You also need to determine whether you actually need the information that does not convert over to QBO. If you are not currently using QBD, you can skip to the Questions to ask yourself in preparation for data conversion section.

Functionality not available in QBO

QBO does not include the ability to create sales orders or automatically manage fixed assets. Therefore, we do not recommend that you convert from QBD to QBO unless you have a workaround for the following features:

- Sales orders: A form used to record and track customer orders. A sales order will commit the quantity ordered or trigger a backorder if the product is out of stock.

- Automatic fixed asset tracking with Fixed Asset Manager: QBO doesn’t automatically depreciate fixed assets like the Fixed Asset Manager feature used with QBD. However, you can set up your assets and manually record depreciation in all QBO subscription plans.

If you currently use these features in QBD, you should either find a workaround in QBO or postpone converting over to QBO if they are critical to your business.

QuickBooks Desktop data that will not convert to QBO

As we mentioned previously, QBD and QBO are two completely different products. QBD is available for Windows and iOS platforms, whereas QBO is cloud-based software, which means you simply need internet access and it can be used on any platform. With that said, there are several data points that will not convert to QBO.

The following table provides a summary of the data that will not convert to QBO, along with a workaround in QBO. For the complete list of Desktop features and how they will (or will not) convert to QBO, read What to expect when you switch from QBD to QBO, an article by Intuit: https://quickbooks.intuit.com/learn-support/en-us/convert-data-files/what-to-expect-when-you-switch-from-quickbooks-desktop-to/00/186758.

|

QBD data that will not convert to QBO |

Workaround in QBO |

|

Custom sales form templates for estimates, invoices, and sales receipts |

Create new templates using the built-in template layout designer in QBO. |

|

Bank and credit card connections, and downloaded bank activity pending review |

Re-establish a connection in QBO for all bank and credit card accounts. Review all downloaded transactions prior to proceeding with the conversion. |

|

Reconciliation reports for all bank and credit card accounts previously reconciled |

Since all transactions with the reconciled status, R, will convert, do one big reconciliation, or redo them individually to recreate the reports in QBO. |

|

Memorized reports |

Memorized reports will not move to QBO. In QBO, re-create reports that you run often and save them in Favorites. |

|

Audit trail report with historical activity |

Print and save the audit trail report from QBD. Refer to the backup QBD file (covered later in this chapter). |

|

Balance sheet budgets |

Budgets are only available in QBO Plus and Advanced subscriptions. However, you can only create profit and loss budgets, not balance sheet budgets in QBO. |

|

Multi-Currency |

Multi-Currency is only available in QBO Plus and Advanced subscriptions. However, transactions with 3 different currency types won’t copy to QBO. |

|

Price Levels |

While price levels will not convert to QBO, if you have QBO Plus or Advanced you can manually set up the price levels. |

|

Mileage Tracking |

Mileage tracking is available in all QBO subscription plans. However, you will need to manually add any previous mileage recorded in QBD into QBO. |

|

QuickBooks Payments |

You will need to unlink your Payments account from your QBD file and relink the account to QBO after you convert. |

|

Users and Permissions |

Existing users in QBD don’t automatically have access to QBO. They need to be invited to QBO to gain access. We cover how to give other users access in Chapter 4, Customizing QuickBooks for Your Business. |

|

Accumulated closing date exceptions |

Closing date exceptions in QBD will not transfer over to QBO but new exceptions from the date of the conversion will be tracked. |

Table 3.1: Workarounds in QBO for QBD data that will not convert

You should determine whether the workaround is an ideal solution, or if you can run your business without bringing over certain data. After you have compiled key information, asked yourself a few questions, and familiarized yourself with the data that will not convert, you are ready to convert your data. Next, we will cover the questions you need to answer in order to determine the type of setup you will need.

Questions to ask yourself in preparation for data conversion

When setting up your QuickBooks company file, you will need to determine whether you want to bring over any data from your existing accounting program. Additionally, you need to know what features you want to use in QuickBooks. Answering the following questions will help determine what type of setup you need to manage your day-to-day business activities:

- How much historical data do you want to bring over to QuickBooks?

If you are converting in the middle of the year, you need to determine whether you will bring over all the transactions that have occurred thus far, or just start from the current month you are in. The benefit of bringing over transactions that go back to the beginning of the year is that it will allow you to run financial statements in QuickBooks for the entire year, as opposed to only part of the year. Keep in mind that it will be more time-consuming to do this, so you will need to weigh the cost versus the benefit to determine whether it is worth it.

Pro Tip: Best practice is to start tracking your data in QuickBooks at the beginning of a year, quarter, or month. For example, let’s say after filing your taxes on April 15th you decide you want to start using QBO. If it’s not feasible or cost-effective to go back to January 1st, then go back to April 1st (the beginning of a month and the 2nd quarter) and start using QuickBooks from that date forward. At least you will have 9 months’ worth of data in QBO and only 3 months (January to March) of doing it the “old way.”

- How much detailed information do you want to bring over to QuickBooks?

If you do decide to bring over the historical information for an entire year, you’ve got two options. First, you can enter each transaction individually into QuickBooks. Depending on how much data you have, this could be quite labor-intensive and expensive if you have to pay someone else to do it. Second, you can create a summary journal entry that is a lot faster than entering each individual transaction, but you will not have the details of each transaction in QuickBooks. If you have a ton of transactions, then using a summary journal entry is going to be the best option for you. However, if you don’t have a lot of activity, then enter transactions individually.

Pro Tip: While it can be time-consuming, entering historical transactions is a great way to learn how to use QBO.

- Do you create estimates or proposals for existing or prospective customers?

If you plan to create estimates in QuickBooks, you will need to make that selection during the setup process. Once you do so, a couple of benefits are that you can easily email estimates and track the status of when the estimates are approved, or not approved, by the customer.

- Do you plan to create billing statements for customers?

During the QBO setup process, you can select the option to create billing statements. Depending on the type of business you own, you may want to generate billing statements for customers on a weekly, monthly, quarterly, or ad hoc basis. This is common for doctor’s offices and for companies that provide services to customers on a recurring basis (for example, monthly, quarterly, or annually).

- Do you want to use invoices to bill customers?

If you choose to create billing statements for some customers but want to create invoices for others, you can do that in QuickBooks. Invoices are commonly used to bill customers to whom you have extended credit terms. This means that payment is not due when you provide goods and/or services. Instead, you send these customers an invoice that includes a due date, and they are expected to remit payment before or by the due date. For example, Net 30 payment terms means that the bill is due 30 days after the date on the invoice.

- Do you want to keep track of your bills through QuickBooks?

During the QBO account setup process, you will need to choose whether or not you want to track and pay bills in QuickBooks. If you have a lot of bills to keep track of, you should consider entering all bills into QuickBooks. Once you enter a bill into QuickBooks, it will alert you when the bill is getting close to the due date. You can pay the bill through online banking, or you can pay the bill by writing a check directly from QuickBooks. If you don’t receive a lot of paper bills, then it may not be ideal to track unpaid bills through QuickBooks. Instead, you can track bills as they are paid from your bank/credit card account.

- Do you want to keep track of inventory through QuickBooks?

If you need to keep track of inventory purchases by tracking quantities and costs, then you need to track the inventory in QuickBooks. QBO Plus and QBO Advanced are the only plans that include inventory tracking. Inventory must be activated during the QBO account setup process. However, if you prefer to keep track of sales only, you do not need inventory tracking which means the QBO Simple Start or Essentials plans will work for you.

- Do you have employees or 1099 contractors?

Payroll is not automatically activated when you set up your QBO account. You will need to purchase a payroll subscription in order to activate this feature and complete the setup. If you have employees or 1099 contractors that you need to track in QuickBooks, see Chapter 14, Managing Employees and 1099 Contractors in QuickBooks Online, to learn how to set up and track payments to 1099 contractors and your options for paying employees.

Make sure you add them to the list of vendors that you will import into QuickBooks.

- Do you need to track income and expenses by department, business segment, or location?

If you need to track income and expenses by department or business segment, you will need to turn on class tracking in the QBO account setup process. You can also turn on location tracking if you have more than one store or office location you need to keep track of. Class tracking and location tracking are only available in QBO Plus and QBO Advanced plans.

Similar to the key information and documents discussed in the previous section, it’s important for you to think about how you want to use QuickBooks. Answering a few simple questions can help you determine what features you need to turn on in QBO to manage your books.

Converting QuickBooks Desktop data to QBO

Now that you are familiar with most of the limitations of converting data from QBD to QBO, we will walk through the steps for doing this. There are seven primary steps involved with converting data from QBD to QBO:

- Checking the target count

- Creating a QuickBooks Online account

- Backing up your QuickBooks Desktop file

- Checking for updates

- Running the QuickBooks Desktop conversion tool

- Logging in to QuickBooks Online

- Verifying that all of your data was converted

Let’s take a look at each of these steps, one by one.

Checking the target count

In order to convert your Desktop data to Online, your target count must not exceed 750,000.

To check your target count, open your QuickBooks file. From the home page, press Ctrl + 1 on your keyboard, which will open the Product Information screen. On this screen, you will find your product license number, the location of your company file, and other key data points, such as the target count.

The following screenshot includes an example of the target count on the Product Information screen. For this company file, the target count is 5,937, which is well below the 750,000 limit:

Figure 3.1: Checking the total targets

Pro Tip: If your file exceeds the maximum 750,000 targets, you can try to reduce the targets by condensing your QuickBooks file. Read this article by Intuit, Condense your QBD file for import to QBO (https://quickbooks.intuit.com/learn-support/en-us/migrate-services/condense-your-quickbooks-desktop-file-for-import-to-quickbooks/00/186240), to learn how this works.

CAUTION: If this process does not reduce the targets, you cannot convert your file to QBO. Instead, you will need to choose one of the alternatives we will cover later in this chapter.

If your QuickBooks file is below the 750,000 limit, you can proceed to create a QBO account.

Creating a QBO account

Prior to converting your data, you must already have a QBO account. If you don’t have a QBO account, refer back to Chapter 1, Getting Started with QuickBooks Online, to learn how to set one up. If you have an existing account, you must convert your QBD data within the first 60 days of your QBO subscription date. If you are past the 60 days, you will need to cancel your account and create a new QBO subscription.

To recap, follow these steps to create a QBO account:

- Go to www.intuit.com.

- Click on Products and choose QuickBooks Online.

- Click on Plans & Pricing.

- Choose one of the following QBO subscription plans:

- Simple Start

- Essentials

- Plus

- Advanced

- Refer back to Chapter 1, Getting Started with QuickBooks Online for a detailed guide to setting up your account.

The final step is to log out of your account. As we go through the Logging into QuickBooks Online section below, the system will prompt you to log back in when appropriate.

After creating your QBO account, you are ready to convert your data. Before converting your Desktop data, it’s important to save a backup of your QuickBooks file. If there is an error when converting your data, you can always refer back to the backup file if you need to. Let’s walk through backing up your QBD file.

Backing up your QuickBooks Desktop file

Converting your data does not change it. However, you should always have a backup copy of your data prior to conversion.

Follow these steps to create a backup copy of your QuickBooks file:

- Click on the File menu.

- Select Create Copy.

- Select Backup copy, as indicated in Figure 3.2:

Figure 3.2: Creating a backup copy

- Follow the onscreen instructions to save your file to a local drive.

Now that you have a backup copy of your QuickBooks Desktop data, you can proceed with the conversion. To avoid errors when converting your data, you need to ensure that you are working with the latest version of QuickBooks Desktop.

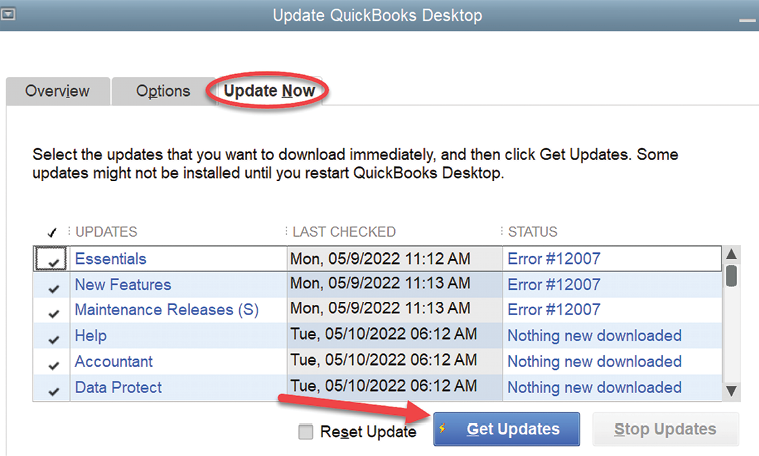

Checking for updates

Before using the conversion tool, you need to make sure you have the most recent version of the tool. For QuickBooks Pro, Premier, and Enterprise users, follow these instructions to check for updates:

- From the Help menu at the very top of the home page, select Update QuickBooks Desktop…:

Figure 3.3: The Update QuickBooks Desktop setting

- Next, click on the Update Now tab, select all the updates by putting a checkmark in the first column to select the available updates, and click Get Updates, as indicated in Figure 3.4:

Figure 3.4: Getting all updates

Once your QuickBooks software has been updated to the most recent version, you are ready to run the QBD conversion-to-QBO tool. We will cover this in detail next.

Running the QBD conversion-to-QBO tool

There is a QBD conversion tool within QuickBooks Desktop. To access it, from the Company menu, select Export Company File to QuickBooks Online, as indicated in Figure 3.5:

Figure 3.5: The Export Company File to QuickBooks Online option

Select Start your export. The next screen will allow you to log in to the QBO account that you set up in the Creating a QBO account section. To complete the QBD data conversion, log in to your QBO account.

Pro Tip: You must log in as an administrator to import your data into QBO. If you are the only user, you are automatically the administrator.

Logging in to QBO

After exporting your QuickBooks data file, the login screen for QBO will appear. Follow the steps outlined here:

- Enter your secure email or user ID and password for your QBO account:

Figure 3.6: Signing into QBO

- Follow the onscreen instructions to complete the upload.

Pro Tip: If you track inventory in QBD, select yes to bring inventory into QBO and enter the as of date. Select no if you don’t want to bring inventory into QBO and plan to set up new items later on.

Once the upload is complete, you will see an onscreen notification that your data has been successfully uploaded. When your data is ready, you will receive an email from the Intuit support team. The length of time this will take will depend on how large your company file is. In general, this takes place within 1 to 24 hours, at the most.

Once you have received an email from the Intuit support team confirming your data has been uploaded, the final step in converting your data is to verify that the data in your QBO file is correct.

Verifying that all of your data was converted

The final step in the conversion process is to verify that all your data was successfully imported into QuickBooks Online. To do this, you need to run a profit and loss report and a balance sheet report in both QuickBooks Online and QuickBooks Desktop. For instructions on how to run these reports in QBO, head over to Chapter 11, Business Overview Reports. Be sure to use the following report parameters:

- All dates

- Accrual accounting method

Compare the reports to see if they match. If they don’t, contact the Intuit support team by clicking on the Help menu in your QBO file and then selecting the option to chat with a support representative, or contact them by telephone. A support representative will assist you with troubleshooting any out-of-balance issues.

Once you have verified that your data was successfully converted to QBO, you are ready to start using QBO to manage your bookkeeping. You should keep the backup file created in the previous section, in case you discover an issue later on.

Alternatives to converting a QuickBooks Desktop file to QBO

If you are unable to convert your existing QuickBooks Desktop data to QBO, you have a few other options to choose from:

- Option 1 is to export all of your lists (vendors, customers, accounts, products and services, etc.) to Excel and then import that data into QBO. From there, you can connect your bank and credit card accounts and start using QBO to manage your business without bringing over historical data. The good news is that you can always refer back to the backup file for QBD if you need to.

- Option 2 is to import all of your lists and record a summary journal entry of historical data in QBO. This option is ideal if you need to have the historical data in QBO but you don’t have a lot of time to enter all of the details or you don’t want to pay someone to do it.

- Option 3 is to import all of your lists and record the details of historical data into QBO. This option would be ideal if you are converting in the middle of the year and want to have a full year’s worth of data in QBO for year-end reports. Depending on how much data you have, this option will also be the most time-consuming and costly if you hire someone to do it.

In this section, we will show you how to import your list data into QBO, record a summary journal entry of historical data, and record the details of historical data into QBO.

Importing list data into QBO

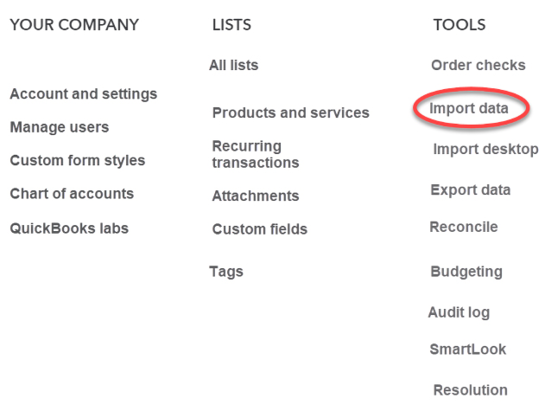

If you can organize your data into an Excel or CSV file, you can easily import that data into QBO. Currently, you can import data from your financial institution, customer lists, vendor lists, chart of accounts, products and services, and invoices. Follow the steps below to import this data into QBO:

- Click on the gear icon and select Import data, as shown in Figure 3.7:

Figure 3.7: The Import data option

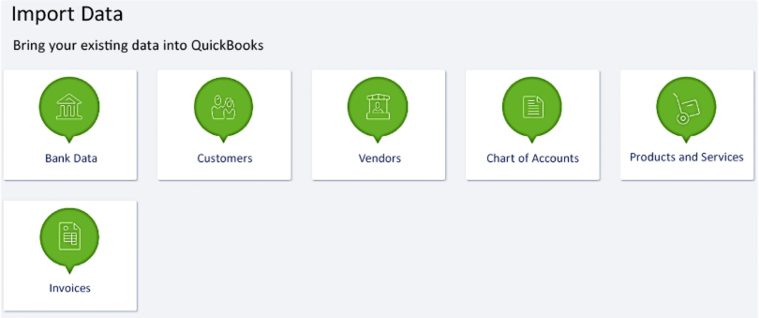

- The following screen will appear:

Figure 3.8: The Import Data screen

- Click on the icon that represents the type of data you would like to import and follow the onscreen instructions to import the data into QBO.

For step-by-step instructions on importing bank data and a chart of accounts, refer to Chapter 4, Customizing QuickBooks for Your Business. To learn how to import customers, vendors, and products and services data, refer to Chapter 5, Managing Customer, Vendor, and Products and Services Lists.

If you don’t have the time to enter individual transactions, you can opt for recording a summary journal entry.

Recording a summary journal entry of historical data in QBO

A summary journal entry will only include lump sum total amounts. To enter balances for balance sheet accounts, you should run a balance sheet report in your current accounting system for the last day of the year for which you are bringing over data. If you would like to also bring over income and expense data, you need to print an income statement from your existing accounting system, as of the last day of the year (i.e. 12/31/20XX) for which you are bringing over data. Enter the totals for each account into QuickBooks.

Pro Tip: Make sure the accounts that appear on both the balance sheet and income statement reports have been created in QuickBooks before you create the journal entry. In Chapter 4, Customizing QuickBooks for Your Business, we show you how to create new accounts.

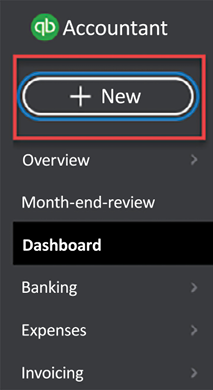

Follow these steps to create a journal entry in QBO:

- Navigate to the journal entry screen by clicking on the + New button on the left navigation bar, as indicated here:

Figure 3.9: The + New button

- In the OTHER column, click on Journal entry, as follows:

Figure 3.10: Navigating to the journal entry form

- Complete the fields in the journal entry form:

Figure 3.11: The journal entry form

You will need to complete eight fields. Here is a brief explanation of what information to include in each field:

- Journal date (1): Enter the effective date of the journal entry. For example, you would enter the last date of the fiscal year for which you are bringing data over (for example, December 31, 20XX).

- Journal no. (2): QuickBooks will automatically assign a journal entry number, beginning with 1. However, you can start with a different number, such as 1000, and QuickBooks will automatically increment each journal number thereafter.

- ACCOUNT (3): From the drop down menu, select the account(s) that require a debit. After all debits have been entered, you can enter the accounts that will be credited right after.

- DEBITS (4): Enter all debit amounts in this field.

- CREDITS (5): Enter all credit amounts in this field.

- DESCRIPTION (6): Enter a brief description of the purpose of the journal entry (for example, to bring over existing balances as of December 31, 2022).

- NAME (7): If a line item is for a specific customer, you can select the appropriate customer from the drop down menu.

Pro Tip: The Name field is used in those instances when you are making an adjustment to the accounts receivable balance for a specific customer.

So far, we’ve covered two of the three alternatives to converting QBD data to QBO, importing lists and recording a summary journal entry. The final option and the best option, in my opinion, is to record all details of historical data in QBO. To clarify, there is no need to bring over data if you have already filed your tax returns for that year. However, you do need to keep your backup for those prior years in case you are ever audited.

If you are in the middle of a year or even the end of the year it is ideal to record details of historical data for the current year if you have the resources to do so. We will cover how to do this next.

Recording details of historical data in QBO

As mentioned previously, the ideal method of entering historical data into QBO is to enter individual transactions. While this is more time-consuming than completing a summary journal entry, it includes all the details of each transaction.

Individual transactions must be entered in the correct order to avoid any issues. The order in which to enter historical transactions into QBO is as follows:

- Purchase orders, bills and payments, credits from vendors, credit card charges, checks, inventory on hand

- Employee timesheets, billable hours

- Invoices, sales receipts, credit memos, returns

- Customer payments, bank deposits

- Sales taxes paid, payroll transactions

- All banking transactions (not previously entered), credit card transactions (not previously entered), reconcile all bank and credit card accounts

It’s important that you follow these steps to avoid issues later on.

Converting from Excel spreadsheets or pen & paper to QBO

There are four primary steps for converting from Excel spreadsheets to QBO:

- Complete the initial company file setup.

- Make sure that you have a separate Excel spreadsheet for each type of list: customers, vendors, and products and services.

- Import all list information for customers, vendors, and products and services. Refer to the Importing list data into QBO section above for detailed instructions.

- Import your chart of accounts list or update the default listing in QuickBooks to match your current list.

- Verify the accuracy of the data that has been converted.

In Chapter 2, Company File Setup, we covered in detail how to complete the initial company file setup. Refer to Chapter 4, Customizing QuickBooks for Your Business, to learn how to import all of your lists data.

Summary

We have covered what you need to consider when deciding if QBO is right for your business, what questions to ask yourself, the steps needed to convert your QBD data to QBO, alternatives to converting your QBD data if you are unable to do so, and how to convert from Excel spreadsheets or pen & paper to QuickBooks Online. Once all of your data has been converted and verified, you are ready to customize QuickBooks Online for your business.

In the next chapter, we will show you how to customize QuickBooks Online for your business.