Budgeting the Project

Having finished the planning for the technical aspects of the project, there is one more important element of planning to finish that will then result in the final go-ahead from top management to initiate the project. A budget must be developed in order to obtain the resources needed to accomplish the project's objectives. A budget is simply a plan for allocating organizational resources to the project activities. PMBOK covers the topic of budgeting in Chapter 7 on Cost.

![]()

But the budget also serves another purpose: It ties the project to the organization's aims and objectives through organizational policy. For example, NASA's Mars Pathfinder-Rover mission embedded a new NASA policy—to achieve a set of limited exploration opportunities at extremely limited cost. In 1976, NASA's two Viking-Mars Lander missions cost $3 billion to develop. In 1997, however, the Pathfinder-Rover mission cost only $175 million to develop, a whopping 94 percent reduction. The difference was the change in organizational policy from a design-to-performance orientation to a design-to-cost orientation.

In Chapter 3, we described the project planning process as a set of steps that began with the overall project plan and then divided and subdivided the plan's elements into smaller and smaller pieces that could finally be sequenced, assigned, scheduled, and budgeted. Hence, the project budget is nothing more than the project plan, based on the WBS, expressed in monetary terms and it becomes a part of the Project Charter.

Once the budget is developed, it acts as a tool for upper management to monitor and guide the project. As we will see later in this chapter, it is a necessary managerial tool, but it is not sufficient. Appropriate data must be collected and accurately reported in a timely manner or the value of the budget to identify current financial problems or anticipate upcoming ones will be lost. This collection and reporting system must be as carefully designed as the initial project plans because late reporting, inaccurate reporting, or reporting to the wrong person will negate the main purpose of the budget. In one instance, the regional managers of a large computer company were supposed to receive quarterly results for the purpose of correcting problems in the following quarter. The results took 4 months to reach them, however, completely negating the value of the budgeting-reporting system.

In this chapter, we will first examine some different methods of budgeting and cost estimating, as used for projects. Then we will consider some ways to improve the cost estimation process, including some technical approaches such as learning curves and tracking signals. We will also discuss some ways to misuse the budget that are, unfortunately, common. Last, we discuss the problem of budget uncertainty and the role of risk management when planning budgets.

![]()

4.1 METHODS OF BUDGETING

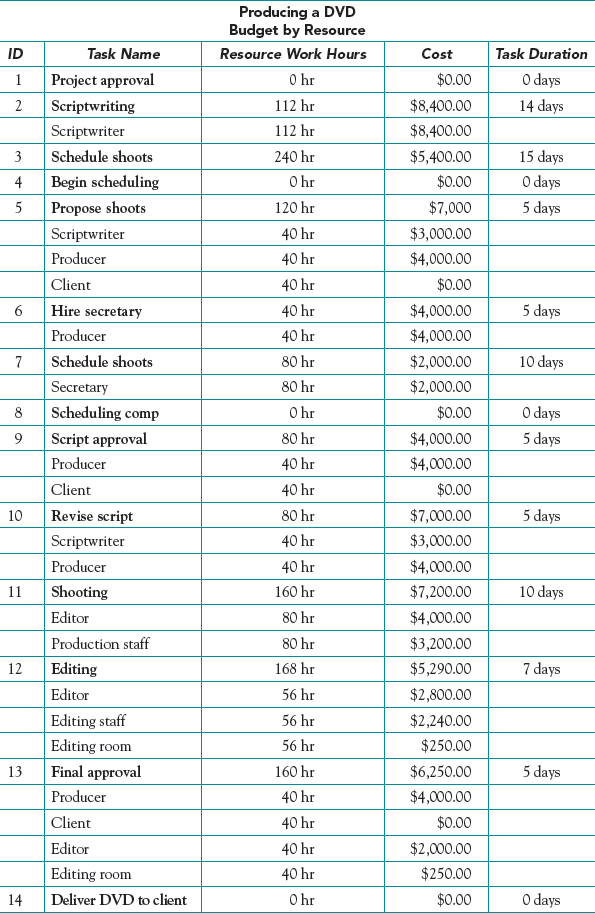

Budgeting is simply the process of forecasting what resources the project will require, what quantities of each will be needed, when they will be needed, and how much they will cost. Tables 4-1 and 4-2 depict the direct costs involved in making a short documentary film. Table 4-1 shows the cost per unit of usage (cost/hour) of seven different personnel categories and one facility. Note that the facility does not charge by the hour, but has a flat rate charge. Table 4-2 shows the resource categories and amounts used for each activity required to make the DVD. The resource costs shown become part of the budget for producing the documentary film. As you will see below, overhead charges may be added to these direct charges.

Most businesses and professions employ experienced estimators who can forecast resource usage with amazingly small errors. For instance, a bricklayer can usually estimate within 1 or 2 percent the number of bricks required to construct a brick wall of given dimensions. In many fields, the methods of cost estimation are well documented based on the experience of estimators gathered over many years. The cost of a building, or house, is usually estimated by the square feet of floor area multiplied by an appropriate dollar value per square foot and then adjusted for any unusual factors.

Budgeting a project such as the development of a control system for a new computer, however, is often more difficult than budgeting more routine activities—and even more difficult than regular departmental budgeting which can always be estimated as: “Same as last year plus X percent.” But project budgeters do not usually have tradition to guide them. Projects are, after all, unique activities. Of course, there may be somewhat similar past projects that can serve as a model, but these are rough guides at best. Forecasting a budget for a multiyear project such as a large product line or service development project is even more hazardous because the unknowns can escalate quickly with changes in technology, materials, prices, and even the findings of the project up to that point.

Table 4-1 Resource Cost per Unit for Producing a Short Documentary Film

Table 4-2 Budget by Resource for Producing a Short Documentary Film

Organizational tradition also impacts project budgeting. Every firm has its own rules about how overhead and other indirect costs are charged against projects. Every firm has its ethical codes. Most firms must comply with the Sarbanes-Oxley Act (SOX) and the Health Insurance Portability and Accountability Act (HIPAA). Most firms have their own accounting idiosyncrasies, and the PM cannot expect the accounting department to make special allowances for his or her individual project. Although accounting will charge normal expenditures against a particular activity's account number, as identified in the WBS, unexpected overhead charges, indirect expenses, and usage or price variances may suddenly appear when the PM least expects it, and probably at the worst possible time. (Price variances due to procurement, and the entire procurement process, are discussed in Chapter 12 of PMBOK, 2013.) There is no alternative—the PM must simply become completely familiar with the organization's accounting system, as painful as that may be.

![]()

In the process of gaining this familiarity, the PM will discover that cost may be viewed from three different perspectives (Hamburger, 1986). The PM recognizes a cost once a commitment is made to pay someone for resources or services, for example when a machine is ordered. The accountant recognizes an expense when an invoice is received—not, as most people believe, when the invoice is paid. The controller perceives an expense when the check for the invoice is mailed. The PM is concerned with commitments made against the project budget. The accountant is concerned with costs when they are actually incurred. The controller is concerned with managing the organization's cash flows. Because the PM must manage the project, it is advisable for the PM to set up a system that will allow him or her to track the project's commitments.

Another aspect of accounting that will become important to the unaware PM is that accountants live in a linear world. When a project activity has an $8,000 charge and runs over a four-month period, the accounting department (or worse, their software) sometimes simply spreads the $8,000 evenly over the time period, resulting in a $2,000 allocation per month. If expenditures for this activity are planned to be $5,000, $1,000, $1,000, and $1,000, the PM should not be surprised when the organization's controller storms into the project office after the first month screaming about the unanticipated and unacceptable cash flow demands of the project!

Next, we look at two different approaches for gathering the data for budgeting a project: top-down and bottom-up.

Top-down Budgeting

The top-down approach to budgeting is based on the collective judgments and experiences of top and middle managers concerning similar past projects. These managers estimate the overall project cost by estimating the costs of the major tasks, which estimates are then given to the next lower level of managers to split up among the tasks under their control, and so on, until all the work is budgeted.

The advantage of this approach is that overall budget costs can be estimated with fair accuracy, though individual elements may be in substantial error. Another advantage is that errors in funding small tasks need not be individually identified because the overall budget allows for such exceptions. Similarly, the good chance that some small but important task was overlooked does not usually cause a serious budgetary problem. The experience and judgment of top management are presumed to include all such elements in the overall estimate. In the next section, we will note that the assumptions on which these advantages are based are not always true.

Bottom-Up Budgeting

In bottom-up budgeting, the WBS identifies the elemental tasks, whose resource requirements are estimated by those responsible for executing them (e.g., programmer-hours in a software project). This can result in much more accurate estimates, but it often does not do so for reasons we will soon discuss. The resources, such as labor and materials, are then converted to costs and aggregated to different levels of the project, eventually resulting in an overall direct cost for the project. The PM then adds, according to organizational policy, indirect costs such as general and administrative, a reserve for contingencies, and a profit figure to arrive at a final project budget.

Bottom-up budgets are usually more accurate in the detailed tasks, but risk the chance of overlooking some small but costly tasks. Such an approach, however, is common in organizations with a participative management philosophy and leads to better morale, greater acceptance of the resulting budget, and heightened commitment by the project team. It is also a good managerial training technique for aspiring project and general managers.

Unfortunately, true bottom-up budgeting is rare. Upper level managers are reluctant to let the workers develop the budget, fearing the natural tendency to overstate costs, and fearing complaints if the budget must later be reduced to meet organizational resource limitations. Moreover, the budget is upper management's primary tool for control of the project, and they are reluctant to let others set the control limits. Again, we will see that the budget is not a sufficient tool for controlling a project. Top-down budgeting allows the budget to be controlled by people who play little role in designing and doing the work required by the project. It should be obvious that this will cause problems—and it does.

![]()

We recommend that organizations employ both forms of developing budgets. They both have advantages, and the use of one does not preclude the use of the other. Making a single budget by combining the two depends on setting up a specific system to negotiate the differences. We discuss just such a system below. The only disadvantage of this approach is that it requires some extra time and trouble, a small price to pay for the advantages. A final warning is relevant. Any budgeting system will be useful only to the extent that all cost/revenue estimates are made with scrupulous honesty.

Project budgeting is a difficult task due to the lack of precedent and experience with unique project undertakings. Yet, understanding the organization's accounting system is mandatory for a PM. The two major ways of generating a project budget are top-down and bottom-up. The former is usually accurate overall but possibly includes significant error for low-level tasks. The latter is usually accurate for low-level tasks but risks overlooking some small but potentially costly tasks. Most organizations use top-down budgeting in spite of the fact that bottom-up results in better acceptance and commitment to the budget.

4.2 COST ESTIMATING

In this section, we look at the details of the process of estimating costs and some dangers of arbitrary cuts in the project budget. We also describe and illustrate the difference between activity budgeting and program budgeting.

Work Element Costing

The task of building a budget is relatively straightforward but tedious. Each work element is evaluated for its resource requirements, and its costs are then determined. For example, suppose a certain task is expected to require 16 hours of labor at $10 per hour, and the required materials cost $235. In addition, the organization charges overhead for the use of utilities, indirect labor, and so forth at a rate of 50 percent of direct labor. Then, the total task cost will be

$235 + [(16 hr × $10/hr) × 1.5] = $475

In some organizations, the PM adds the overhead charges to the budget. In others, the labor time and materials are just sent to the accounting department and they run the numbers, add the appropriate overhead, and total the costs. Although overhead was charged here against direct labor, more recent accounting practices such as activity-based costing may charge portions of the overhead against other cost drivers such as machine time, weight of raw materials, or total time to project completion.

Direct resource costs such as for materials and machinery needed solely for a particular project are usually charged to the project without an overhead add-on. If machinery from elsewhere in the organization is used, this may be charged to the project at a certain rate (e.g., $/hr) that will include depreciation charges, and then will be credited to the budget of the department owning and paying for the machine. On top of this, there is often a charge for GS&A (general, sales, and administrative) costs that includes upper management, staff functions, sales and marketing, plus any other costs not included in the overhead charge. GS&A may be charged as a percentage of direct costs, all direct and indirect costs, or on other bases including total time to completion.

Thus, the fully costed task will include direct costs for labor, machinery, and resources such as materials, plus overhead charges, and finally, GS&A charges. The full cost budget is then used by accounting to estimate the profit to be earned by the project. The wise PM, however, will also construct a budget of direct costs for his or her own use. This budget provides the information required to manage the project without being confounded with costs over which he or she has no control.

Note that the overhead and GS&A effect can result in a severe penalty when a project runs late, adding significant additional and possibly unexpected costs to the project. Again, we stress the importance of the PM thoroughly understanding the organization's accounting system, and especially how overhead and other such costs are charged to the project.

Of course, this process can also be reversed to the benefit of the PM by minimizing the use of drivers of high cost. Sometimes clients will even put clauses in contracts to foster such behavior. For example, when the state of Pennsylvania contracted for the construction of the Limerick nuclear power generating facility in the late 1980s, they included such an incentive fee provision in the contract. This provision stated that any savings that resulted from finishing the project early would be split between the state and the contractor. As a result, the contractor went to extra expense and trouble to make sure the project was completed early. The project came in 8 months ahead of its 49-month due date and the state and the contractor split the $400 million savings out of the total $3.2 billion budget.

The Impact of Budget Cuts

In the previous chapter on planning, we described a process in which the PM plans Level 1 activities, setting a tentative budget and duration for each. Subordinates (and this term refers to anyone working on the project even though such individuals may not officially report to the PM and may be “above” the PM on the firm's organizational chart) then take responsibility for specifying the Level 2 activities required to produce the Level 1 task. As a part of the Level 2 specifications, tentative budgets and durations are noted for each Level 2 activity. The PM's initial budget and duration estimates are examples of top-down budgeting. The subordinate's estimates of the Level 2 task budgets and durations are bottom-up budgeting. As we promised, we now deal with combining the two budgets.

We will label the Level 1 task estimate of duration of the ith task as ti, and the respective cost estimate as ri, the t standing for “time” and the r for “resources.” In the meantime, the subordinate has estimated task costs and durations for each of the Level 2 tasks that comprise Level 1 task i. We label the aggregate cost and duration of these Level 2 activities as ri′ and ti′, respectively. It would be nice if ri, equaled ri′, but the reality is rarely that neat. In general, ri<<ri′ (The same is true of the time estimates, ti and ti′.) There are three reasons why this happens. First, jobs always look easier, faster, and cheaper to the boss than to the person who has to do them (Gagnon and Mantel, 1987). Second, bosses are usually optimistic and never admit that details have been forgotten or that anything can or will go wrong. Third, subordinates are naturally pessimistic and want to build in protection for everything that might possibly go wrong.

It is important that we make an assumption for the following discussion. We assume that both boss and subordinate are reasonably honest. What follows is a win-win negotiation, and it will fail if either party is dishonest. (We feel it is critically important to remind readers that it is never smart to view the other party in a negotiation as either stupid or ignorant. Almost without fail, such thoughts are obvious to the other party and the possibility of a win-win solution is dead.) The first step in reducing the difference between the superior's and subordinate's estimates occurs when the worker explains the reality of the task to the boss, and ri rises. Encouraged by the fact that the boss seems to understand some of the problems, the subordinate responds to the boss's request to remove some of the protective padding. The result is that ri′ falls.

The conversation now shifts to the technology involved in the subordinate's work and the two parties search for efficiencies in the Level 2 work plan. If they find some, the two estimates get closer still, or, possibly, the need for resources may even drop below either party's estimate.

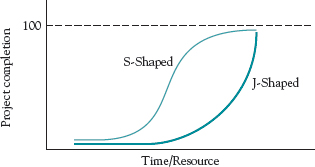

To complete our discussion, let's assume that after all improvements have been made, ri′ is still somewhat higher than ri. Should the boss accept the subordinate's cost estimate or insist that the subordinate accept the boss's estimate? To answer this question, we must recall the discussion of project life cycles from Chapter 1. We discussed two different common forms of life cycles, and these are illustrated again, for convenience, in Figure 4-1. One curve is S-shaped, and the other is J-shaped. As it happens, the shapes of these curves hold the key to our decision.

Figure 4-1 Two project life cycles (cf. Figures 1-2 and 1-3).

If the project life cycle is S-shaped, then with a somewhat reduced level of resources, a smaller than proportional cut will be made in the project's objectives or performance, likely not a big problem. If the project's life cycle is J-shaped, the impact of inadequate resources will be serious, a larger than proportional cut will be made in the project's performance. The same effect occurs during an “economy drive” when a senior manager decrees an across-the-board budget cut for all projects of, say, 5 or 10 percent. For a project with a J-shaped life cycle, the result is disaster. It is not necessary to know the actual shape of a project's life cycle with any precision. One needs merely to know the probable curvature (concave or convex to the baseline) of the last stage of the cycle for the project being considered.

The message here is that for projects with S-shaped life cycles, the top-down budgeting process is probably acceptable. For J-shaped life-cycle projects, it is dangerous for upper management not to accept the bottom-up budget estimates. At the very least, management should pay attention when the PM complains that the budget is insufficient to complete the project. An example of this problem is NASA's Space Shuttle Program, projected by NASA to cost $10-13 billion but cut by Congress to $5.2 billion. Fearing a cancellation of the entire program if they pointed out the overwhelming developmental problems they faced, NASA acquiesced to the inadequate budget. As a result, portions of the program fell 3 years behind schedule and had cost overruns of 60 percent. As the program moved into the operational flight stage, problems stemming from the inadequate budget surfaced in multiple areas, culminating in the Challenger explosion in January 1986.

Finally, in these days of increasing budget cuts and great stress on delivering project value, cuts to the organization's project portfolio must be made with care. Wheatly (2009) warns against the danger of focusing solely on ROI when making decisions about which projects will be kept and which will be terminated. We will have considerably more to say about this subject in Chapter 8.

An Aside

Here and elsewhere, we have preached the importance of managers and workers who are willing to communicate with one another frequently and honestly when developing budgets and schedules for projects. Such communication is the exception, not the rule. The fact that only a small fraction of software development projects are completed even approximately on time and on budget is so well known as to be legend, as is the record of any number of high technology industries. Sometimes the cause is scope creep, but top-down budgeting and scheduling are also prime causes. Rather than deliver another sermon on the subject, we simply reprint Rule #25 from an excellent book by Jim McCarthy, Dynamics of Software Development (1995).

I am amazed at the extent to which the software development community accepts bogus dictates, especially when it comes to scheduling. This astonishing passivity is emblematic of Old World behavior applied to New World problems. Given that it's extremely difficult (probably impossible) for a team of committed professionals to create a schedule that even approximates the rate at which the product ultimately materializes, it's utter madness that in many organizations the dates, the features, and the resources—the holy triangle—of a software development project are dictated by people unfamiliar with developing software. Too often people like “Upper Management” or “Marketing” or some other bogeymen conjure up the date. What's worse, by some malignant and pervasive twist of illogic, otherwise competent development managers accept this sort of folly as standard operating procedure.

I have polled dozens of groups of development managers, and my informal data gathering suggests that somewhere in the neighborhood of 30 to 40 percent of all development efforts suffer from dictated features, resources, and schedules. It should be a fundamental dogma that the person who has to do the work should predict the amount of time it will take. Of course, if accuracy isn't a goal, anybody can make foolish predictions.

In some ways, the root of all scheduling evil is that software developers and their managers abdicate their responsibility to determine the probable effort required to achieve a given set of results. The ultimate act of disempowerment is to take away the responsibility for the schedule from those who must live by it. To accept this treatment under any circumstances is no less heinous an act than imposing a bogus scheduling imperative on a team to begin with.

It's easy to sympathize with the urge for control and predictability that this phenomenon manifests, but why on earth should such organizational goofiness persist in the face of what always follows, repeated software calamity?

Often people and organizations have a hard time learning from their mistakes. We tend to be a bit thick sometimes. Our diagnosis of what went wrong the last time can be utterly erroneous, and so we gear up to do it all again—without ever even beginning to experience the core insights required for successful software development.

This blindness is especially likely after a disastrously late software project. Many team members want desperately never to repeat such a death march, so they leave the group. As evidenced by their urge to survive, these people are often the most vital members of the team. The remnant is left lurching about in a fog of blame. Like the Angel of Death, Guilt visits every cubicle. The managers are choking on their own failure, so their ability to lead is smothered. The marketing people have been made to look foolish, their promises just so much gas, and cynicism creeps into their messages. The executives are bewildered, embarrassed, and angry. The customers have been betrayed yet another time.

Slowly the fog dissipates, and a modicum of hope materializes. New team members re-inject a measure of the lost vitality into the team, and new (or forgetful) managers take the helm. The technological siren seduces the group once again. The executives, chastened but unlearning, plunk down enough dough and tell the team when the new project must be done. The cycle repeats.

How is a person to cope with such folly? If you find yourself in such an organizational situation, how should you respond? Keep in mind that in an asylum, the sane are crazy. And in an organization in which irrationality prevails, the irrationality tends to concentrate the further up you go. Your situation might be hopeless because the extent to which you are viewed as crazy will tend to intensify in direct proportion to the power of the observer. You might be able to cope with irrational and self-destructive organizational values, but you're unlikely to prosper in such a setting. A situation this gravely out of whack must be resolved, however. So you steel yourself and inform your dictators that, much as you would like to accept their dictates, you are unable to do so because reality requires otherwise. You remind them (tactfully) that their power is not magic, that their wishes don't make software. You help them envision a future in which people are striving to meet their own goals, things they've proposed to do over a certain interval and things that have a chance of being done even sooner than anticipated.

You need to build schedules meticulously from the bottom up. Each person who has a task to do must own the design and execution of that task and must be held accountable for its timely achievement. Accountability is the twin of empowerment. The two together can create a reasonable software development plan.

_______________________

Reprinted with the kind permission of Jim McCarthy, copyright holder, from Dynamics of Software Development by Jim McCarthy, Microsoft Press, Redmond, WA, 1995, pp. 88–89.

Activity vs. Program Budgeting

Traditional organizational budgets are typically activity oriented and based on historical data accumulated through an activity-based accounting system. Individual expenses are classified and assigned to basic budget lines such as phone, materials, fixed personnel types (salaried, exempt, etc.), or to production centers or processes. These lines are then aggregated and reported by organizational units such as departments or divisions.

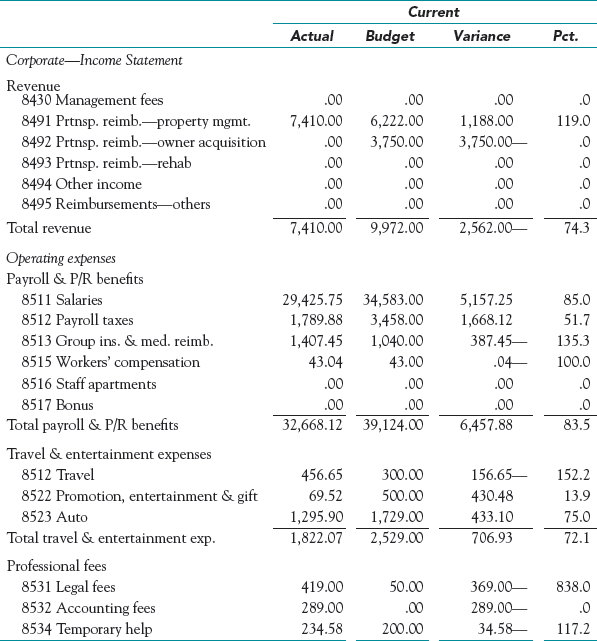

Project budgets can also be presented as activity budgets, such as in Table 4-3 where one page of a six-page monthly budget report for a real estate management project is illustrated. When multiple projects draw resources from several different organizational units, the budget may be divided between these multiple units in some arbitrary fashion, thereby losing the ability to control project resources as well as the reporting of individual project expenditures against the budget.

This difficulty gave rise to program budgeting, illustrated in Table 4-4. Here the program-oriented project budget is divided by task and expected time of expenditure, thereby allowing aggregation across projects. Budget reports are shown both aggregated and disaggregated by “regular operations,” and each of the projects has its own budget. For example, Table 4-3 would have a set of columns for regular operations as well as for each project.

Cost estimating is more tedious than complex except where overhead and GS&A expenses are concerned. Thus, the wise PM will learn the organization's accounting system thoroughly. Low budget estimates or budget cuts will not usually be too serious for S-shaped life-cycle projects but can be disastrous for exponential life-cycle projects. Two kinds of project budget exist, usually depending on where projects report in the organization. Activity budgets show lines of standard activity by actual and budget for given time periods. Program budgets show expenses by task and time period. Program budgets are then aggregated by reporting unit.

Table 4-3 Typical Monthly Budget for a Real Estate Project (page 1 of 6)

4.3 IMPROVING COST ESTIMATES

![]()

At the end of his “Don't Accept Dictation,” reprinted above, McCarthy wrote “Each person who has a task to do must own the design and execution of that task and must be held accountable for its timely achievement. Accountability is the twin of empowerment.” If empowerment is to be trusted, it must be accompanied by accountability. Fortunately, it is not difficult to do this. This section deals with a number of ways for improving the process of cost estimating and an easy way of measuring its accuracy. These improvements are not restricted to cost estimates, but can be applied to almost all of the areas in project management that call for estimating or forecasting any aspect of a project that is measured numerically; e.g., task durations, the time for which specialized personnel will be required, or the losses associated with specific types of risks should they occur. These improvements range from better formalization of the estimating/forecasting process, using forms and other simple procedures, to straightforward quantitative techniques involving learning curves and tracking signals. We conclude with some miscellaneous topics, including behavioral issues that often lead to incorrect budget estimates.

Table 4-4 Project Budget by Task and Month

Forms

The use of simple forms such as that in Figure 4-2 can be of considerable help to the PM in obtaining accurate estimates, not only of direct costs, but also when the resource is needed, how many are needed, who should be contacted, and if it will be available when needed. The information can be collected for each task on an individual form and then aggregated for the project as a whole.

Learning Curves

Suppose a firm wins a contract to supply 25 units of a complex electronic device to a customer. Although the firm is competent to produce this device, it has never produced one as complex as this. Based on the firm's experience, it estimates that if it were to build many such devices it would take about 4 hours of direct labor per unit produced. With this estimate, and the wage and benefit rates the firm is paying, the PM can derive an estimate of the direct labor cost to complete the contract.

Unfortunately, the estimate will be in considerable error because the PM is underestimating the labor costs to produce the initial units that will take much longer than 4 hours each. Likewise, if the firm built a prototype of the device and recorded the direct labor hours, which may run as high as 10 hours for this device, this estimate applied to the contract of 25 units would give a result that is much too high.

In both cases, the reason for the error is the learning exhibited by humans when they repeat a task. In general, it has been found that unit performance improves by a fixed percent each time the total production quantity doubles. More specifically, each time the output doubles, the worker hours per unit decrease by a fixed percentage of their previous value. This percentage is called the learning rate, and typical values run between 70 and 95 percent. The higher values are for more mechanical tasks, while the lower, faster-learning values are for more mental tasks such as solving problems. A common rate in manufacturing is 80 percent. For example, if the device described in the earlier example required 10 hours to produce the first unit and this firm generally followed a typical 80 percent learning curve, then the second unit would require .80 × 10 = 8 hours, the fourth unit would require 6.4 hours, the eighth unit 5.12 hours, and so on. Of course, after a certain number of repetitions, say 100 or 200, the time per unit levels out and little further improvement occurs.

Figure 4-2 Form for gathering data on project resource needs.

Mathematically, this relationship we just described follows a negative exponential function. Using this function, the time required to produce the nth unit can be calculated as

Tn = T1nr

where Tn is the time required to complete the nth unit, T1 is time required to complete the first unit, and r is the exponent of the learning curve and is calculated as the log(learning rate)/log(2). Tables are widely available for calculating the completion time of unit n and the cumulative time to produce units one through n for various learning rates; for example, see Meredith and Shafer (2013). The impact of learning can also be incorporated into spreadsheets developed to help prepare the budget for a project as is illustrated in the example at the end of this section.

![]()

The use of learning curves in project management has increased greatly in recent years. For instance, methods have been developed to approximate composite learning curves for entire projects (Amor and Teplitz, 1998), for approximating total costs from the unit learning curve (Camm, Evans, and Womer, 1987), and for including learning curve effects in critical resource diagramming (Badiru, 1995). The conclusion is that the effects of learning, even in “one-time” projects, should not be ignored. If costs are underestimated, the result will be an unprofitable project and senior management will be unhappy. If costs are overestimated, the bid will be lost to a savvier firm and senior management will be unhappy.

Media One Consultants

Media One Consultants is a small consulting firm that specializes in developing the electronic media that accompany major textbooks. A typical project requires the development of an electronic testbank, PowerPoint lecture slides, and a website to support the textbook.

A team consisting of three of the firm's consultants just completed the content for the first of eighteen chapters of an operations management textbook for a major college textbook publisher. In total, it took the team 21 hours to complete this content. The consultants are each billed out at $65/hour plus 20 percent to cover overhead. Past experience indicates that projects of this type follow a 78 percent learning curve.

The publisher's developmental editor recently sent an email message to the team leader inquiring into when the project will be complete and what the cost will be. Should the team leader attempt to account for the impact of learning in answering these questions? How big a difference does incorporating learning into the budget make? What are the managerial implications of not incorporating learning into the time and cost estimates?

The team leader developed the spreadsheet below to estimate the budget and completion time for this project. The top of the spreadsheet contains key parameters such as the learning rate, the consultants' hourly billout rate, the overhead rate, and the time required to complete the first chapter. The middle of the spreadsheet contains formulas to calculate both the unit cost and time of each chapter and the cumulative cost and time.

According to the spreadsheet, the cost of the project is $14,910 and will require in total 191.2 hours. Had the impact of learning not been considered, the team leader would have likely grossly overestimated the project's cost to be $29,484 (1,638 × 18) and its duration to be 278 (21 × 18) hours. Clearly, several negative consequences could be incurred if these inflated time and cost estimates were used. For example, the publisher might decide to reevaluate its decision to award the contract to Media One. Furthermore, the time when the team members would be able to start on their next assignment would be incorrectly estimated. At a minimum, this would complicate the start of future projects. Perhaps more damaging, however, is that it could lead to lost business if potential clients were not willing to wait for their project to begin based on the inflated time estimates.

Tracking Signals

In Chapter 3, we noted that people do not seem to learn by experience, no matter how much they urge others to do so. PMs and others involved with projects spend much time estimating—activity costs and durations, among many other things. There are two types of error in those estimates. First, there is random error. Errors are random when there is a roughly equal chance that estimates are above or below the true value of a variable, and the average size of the error is approximately equal for over and under estimates. (Naturally, we try to devise ways of estimating that minimize the size of these random errors.) If either of the above is not true for an estimator—either the chance of over or under estimates are not about equal or the size of over or under estimates are not approximately equal—the estimates are said to be biased. Random errors cancel out, which means that if we add them up the sum will approach zero. Errors caused by bias do not cancel out. They are systematic errors.

![]()

Calculation of a number called the tracking signal can reveal if there is systematic bias in cost and other estimates and whether the bias is positive or negative. Knowing this can then be quite helpful to a PM in making future estimates or on the critically important task of judging the quality of estimates made by others. Consider the spreadsheet data in Figure 4-3 where estimated and actual values for some factor are listed in the order they were made, indicated for ease of reference by “period.” In order to compare estimates of different resources measured in units and of different magnitudes, we will derive a tracking signal based on the ratio of actual to estimated values rather than the usual difference between the two.

To calculate the first period ratio in Figure 4-3, for example, we would take the ratio 163/155 = 1.052. This means that the actual was 5.2 percent higher than the estimate, a forecast that was low. In column D, we list these errors for each of the periods and then cumulate them at the bottom of the spreadsheet. Note that in columns D and E we subtract 1 from the ratio. This centers the data around zero rather than 1.0, which makes some ratios positive, indicating an actual greater than the forecast, and other ratios negative, indicating an actual less than the forecast. If the cumulative percent error at the bottom of the spreadsheet is positive, which it is in this case, it means that the actuals are usually greater than the estimates. The forecaster underestimates if the ratio is positive and overestimates if it is negative. The larger the percent error, the greater the forecaster's bias, systematic under- or overestimation.

Figure 4-3 Excel® template for finding bias in estimates.

Column E simply shows the absolute value of column D. Column F is the “mean absolute ratio,” abbreviated MAR, which is the running average of the values in column E up to that period. (Check the formulas in the spreadsheet of Figure 4-3.) The tracking signal listed in column G is the ratio of the running sum of the values in column D divided by the MAR for that period. If the estimates are unbiased, the running sum of ratios in column D will be about zero, and dividing this by the MAR will give a very small tracking signal, possibly zero. On the other hand, if there is considerable bias in the estimates, either positive or negative, the running sum of the ratios in column D will grow quite large. Then, when divided by the mean absolute ratio this will show whether the tracking signal is > 1 or < 1, and therefore greater than the variability in the estimates or not. If the bias is large, resulting in large positive or negative ratios, the resulting tracking signal will be correspondingly positive or negative.

It should be noted that it is not simply the bias that is of interest to the PM, although bias is very important. The MAR is also important because this indicates the variability of the estimates compared with the resulting actual values. With experience, the MAR should decrease over time though it will never reach zero. We strive to find a forecasting technique that minimizes both the bias and the MAR. By observing her own errors, the PM can learn to make unbiased estimates. When meeting with her subordinates in order to coach them on improving their estimates, it is important to recognize that most overestimates of duration or resource requirements are the result of an attempt by the subordinate to make “safe” estimates, and underestimates result from overoptimism. If subordinates overcorrect, the PM should avoid sharp criticism. Reasonable accuracy is the goal, but the uncertainty surrounding all projects does not allow random estimate errors to vanish.

Other Factors

Studies consistently show that between 60 and 85 percent of projects fail to meet their time, cost, and/or performance objectives. The record for information system (IS) projects is particularly poor, it seems. For example, there are at least 45 estimating models available for IS projects but few IS managers use any of them (Lawrence, 1994; Martin, 1994). While the variety of problems that can plague project cost estimates seem to be unlimited, there are some that occur with high frequency; we will discuss each of these in turn.

Changes in resource prices, for example, are a common problem. The most common managerial approach to this problem is to increase all cost estimates by some fixed percentage. A better approach, however, is to identify each input that has a significant impact on the costs and to estimate the rate of price change for each one. The Bureau of Labor Statistics (BLS) in the U.S. Department of Commerce publishes price data and “inflators” (or “deflators”) for a wide range of commodities, machinery, equipment, and personnel specialities. (For more information on the BLS, visit http://stats.bls.gov or www.bls.gov.)

Another problem is overlooking the need to factor into the estimated costs an adequate allowance for waste and spoilage. Again, the best approach is to determine the individual rates of waste and spoilage for each task rather than to use some fixed percentage.

A similar problem is not adding an allowance for increased personnel costs due to loss and replacement of skilled project team members. Not only will new members go through a learning period, which increases the time and cost of the relevant tasks, but professional salaries usually increase faster than the general average. Thus, it may cost substantially more to replace a team member with a newcomer who has about the same level of experience.

Then there is also the Brooks's “mythical man-month” effect* which was discovered in the IS field but applies just as well in projects. As workers are hired, either for additional capacity or to replace those who leave, they require training in the project environment before they become productive. The training is, of course, informal on-the-job training conducted by their coworkers who must take time from their own project tasks, thus resulting in ever more reduced capacity as more workers are hired.

And there is the behavioral possibility that, in the excitement to get a project approved, or to win a bid, or perhaps even due to pressure from upper management, the project cost estimator gives a more “optimistic” picture than reality warrants. Inevitably, the estimate understates the cost. This is a clear violation of the PMI's Code of Ethics. It is also stupid. When the project is finally executed, the actual costs result in a project that misses its profit goals, or worse, fails to make a profit at all—hardly a welcome entry on the estimator's résumé.

Even organizational climate factors influence cost estimates. If the penalty for overestimating costs is much more severe than underestimating, almost all costs will be underestimated, and vice versa. A major manufacturer of airplane landing gear parts wondered why the firm was no longer successful, over several years, in winning competitive bids. An investigation was conducted and revealed that, 3 years earlier, the firm was late on a major delivery to an important customer and paid a huge penalty as well as being threatened with the loss of future business. The reason the firm was late was because an insufficient number of expensive, hard to obtain parts was purchased for the project and more could not be obtained without a long delay. The purchasing manager was demoted and replaced by his assistant. The assistant's solution to this problem was to include a 10 percent allowance for additional, hard to obtain parts in every cost proposal. This resulted in every proposal from the firm being significantly higher than their competitors' proposals in this narrow margin business.

There is also a probabilistic element in most projects. For example, projects such as writing software require that every element work 100 percent correctly for the final product to perform to specifications. In programming software, if there are 1000 lines of code and each line has a .999 probability of being accurate, the likelihood of the final program working is only about 37 percent!

Sometimes, there is plain bad luck. What is indestructible, breaks. What is impenetrable, leaks. What is certified, guaranteed, and warranteed, fails. The wise PM includes allowances for “unexpected contingencies.”

There are many ways of estimating project costs; we suggest trying all of them and then using those that “work best” for your situation. The PM should take into consideration as many known influences as can be predicted, and those that cannot be predicted must then simply be “allowed for.”

Finally, a serious source of inaccurate estimates of time and cost is the all too common practice of some managers arbitrarily to cut carefully prepared time and cost estimates. Managers rationalize their actions by such statements as “I know they have built a lot of slop in those estimates,” or “I want to give them a more challenging target to shoot at.” This is not effective management. It is not even good common sense. (Reread the excerpt from McCarthy, 1995 appearing above.) Cost and time estimates should be made by the people who designed the work and are responsible for doing it. As we argued earlier in this chapter, the PM and the team members may negotiate different estimates of resources needs and task durations, but managerially dictated arbitrary cuts in budgets and schedules almost always lead to projects that are late and over budget. We will say more about this later.

Boston's Big Dig highway/tunnel project is one of the largest, most complex, and technologically challenging highway projects in U.S. history. The “Big Dig,” originally expected to cost less than $3 billion, was declared complete after two decades and $14.6 billion for planning and construction, almost a 500 percent cost overrun (Abrams, 2003 and PMI, August 2004). With an estimated benefit of $500 million per year in reduced congestion, pollution, accidents, fuel costs, and lateness, the project has an undiscounted payback of almost 30 years. This project was clearly one that offered little value to the city if it wasn't completed, and so it continued far past what planners thought was a worthwhile investment, primarily because the federal government was paying 85 percent of its cost. One clear lesson from the project has been that unless the state and local governments are required to pay at least half the cost of these megaprojects, there won't be serious local deliberation of their pros and cons. The overrun is attributed to two major factors: (1) underestimates of the initial project scope, typical of government projects; and (2) lack of control, particularly costs, including conflicts of interest between the public and private sectors.

There are numerous ways to improve the process of cost estimation ranging from simple but useful forms and procedures to special techniques such as learning curves and tracking signals. Most estimates are in error, however, because of simpler reasons such as not using available tools, common sense, or failing to allow for problems and contingencies, such as having to replace workers midstream. In addition, there are behavioral and organizational reasons, such as informal incentive systems that reward inaccurate estimates.

4.4 BUDGET UNCERTAINTY AND PROJECT RISK MANAGEMENT

In spite of the care and effort expended to create an accurate and fair budget, it is still only an estimate made under conditions of uncertainty. Because projects are unique, risk pervades all elements of the project, and particularly the project's goals of performance, schedule, and budget. We will discuss these issues of uncertainty and risk here, and offer some suggestions for dealing with them. PMBOK covers the topic of risk in Chapter 11 on Risk.

![]()

![]()

Budget Uncertainty

Perceptually, the PM sees the uncertainty of the budget like the shaded portion of Figure 4-4, where the actual project costs may be either higher or lower than the estimates the PM has derived. As we will describe later, however, it seems that more things can go wrong in a project and drive up the cost than can go right to keep down the cost. As the project unfolds, the cost uncertainty decreases as the project moves toward completion. Figures 4-5 (a), (b), and (c) illustrate this. An estimate at the beginning of the project as in Figure 4-4 is shown as the t0 estimate in Figure 4-5(a). As work on the project progresses, the uncertainty decreases as the project moves toward completion. At time t1 the cost to date is known and another estimate is made of the cost to complete the project, Figure 4-5(b). This is repeated at t2, Figure 4-5(c). Each estimate, of course, begins at the actual cost to date and estimates only the remaining cost to completion. The further the project progresses, the less the uncertainty in the final project cost. It is common in project management to make new forecasts about project completion time and cost at fixed points in the project life cycle, or at special milestones.

Figure 4-4 Estimate of project cost: estimate made at project start.

The reasons for cost uncertainty in the project are many: prices may escalate, different resources may be required, the project may take a different amount of time than we expected, thereby impacting overhead and indirect costs, and on and on. Earlier, we discussed ways to improve cost estimates, to anticipate such uncertainty, but change is a fact of life, including life on the project, and change invariably alters our previous budget estimates.

Three Causes for Change There are three basic causes for change in projects and their budgets and/or schedules. Some changes are due to errors the cost estimator made about how to achieve the tasks identified in the project plan. Such changes are due to technological uncertainty: a building's foundation must be reinforced due to a fault in the ground that wasn't identified beforehand; a new innovation allows a project task to be completed easier than was anticipated, and so on.

Other changes result because the project team or client learns more about the nature of the scope of the project or the setting in which it is to be used. This derives from an increase in the team's or client's knowledge or sophistication about the project deliverables. The medical team plans to use a device in the field as well as in the hospital. The chemists find another application of the granulated bed process if it is altered to include additional minerals.

The third source of change is the mandate: A new law is passed, a trade association sets a new standard, a governmental regulatory agency adopts a new policy. These changes alter the previous “rules of conduct” under which the project had been operating, usually to the detriment of the budget.

Figure 4-5 (a), (b), and (c) Estimates of project cost: estimates made at time t0, t1, and t2.

Handling Changes There are different ways to handle such changes. The least preferred way is simply to accept a negative change and take a loss on the project. The best approach is to prepare for change ahead of time by including provisions in the original contract for such changes. The easiest change to handle is when the change is the result of an increased specification by the client, yet even these kinds of changes are often mishandled by the project organization. The best practice is to include in the contract a formal change control procedure that allows for renegotiation of price and schedule for client-ordered changes in performance.

![]()

More difficult changes are those resulting from misunderstood assumptions, technological uncertainty, and mandates. Assumptions and some technological uncertainties are most easily handled by carefully listing all the assumptions, including those regarding technology, in the contract and stating that if these assumptions fail to hold, the project's cost and schedule may have to be adjusted.

Mandates are the most difficult to accommodate because they can affect anything about the project and usually come without warning. The shorter the project duration, however, the less likely an unexpected mandate will impact the project. Thus, when contracting for a project of extended duration, it is best to divide it into shorter segments and contract for only one segment at a time. Of course, this also gives clients the opportunity to reconsider whether they want to complete the full project, as well as giving the competition an opportunity to steal the remainder of the project from you. Nevertheless, if a client wants to cancel a contract and is locked into a long-term agreement, the project will not have a happy ending anyway. At least with shorter segments the client may be willing to finish a segment before dropping the project. In any event, if the client is pleased with your performance on one segment of the contract, it is unlikely that a competitor will have the experience and cost efficiencies that you have gained and will be able to steal the next segment. At the least, the client would be obligated to give you an opportunity to match their bid.

As changes impact the project's costs, the budget for the remainder of the project will certainly have to be revised. There are three ways to revise a budget during the course of a project, each depending on the nature of the changes that have been experienced. If the changes are confined to early elements of the project and are not seen to impact the rest of the project, then the new budget can be estimated as the old budget plus the changes from the early elements.

More frequently, something systemic has changed that will impact the costs of the rest of the project tasks as well, such as a higher rate of inflation. In this case, the new budget estimate will be the accumulated costs to date plus the previous estimates of the rest of the budget multiplied by some correction factor for the systemic change. Recall that the BLS is an excellent source for such historical data that will aid the PM in estimating an appropriate correction factor.

Last, there may be some individual changes now perceived to impact specific elements of the remaining project tasks. The new budget estimate will then be the actual costs to date plus the expected costs for the remaining project tasks. Generally, both systematic and individual changes in the project will be revised in all three ways at once.

Project Budgeting in Practice

According to the Oxford Review of Economic Policy, a study of 258 projects in 20 countries showed that nine out of ten projects experience cost overruns, and sometimes by over 100 percent! You might wonder how this can possibly happen, but it turns out that it happens quite easily, primarily due to the dynamics of people and groups making decisions in an organization over some period of time. Let's go through what happens in a typical project to see how this occurs.

To determine a project budget,* the project manager (PM) starts with the project plan or WBS to determine the various steps required in the project, the resource needs, labor hours, and associated costs. This cost estimate, plus a “contingency” of up to 25 percent added to either the labor hours or total cost, is then used as the project budget for both obtaining approval for the project and as a placeholder in the department's budget so the funds will be encumbered and unavailable for other purposes. (The addition of a contingency is standard practice and expected.)

However, top management is also responsible for constructing a budget for the company and may have also calculated some cost for this project, or the department that will be funding it. In the process, they will be using their own methods, such as the budget or cost of a previous but similar project, the amount of money the department was budgeted for last year, the amount of monies available for them to spend, the amount the project manager or department spent last year, gut-feel, and other such approaches. When this is aggregated by department, the totals are compared to what each department spent the previous year, what the company's departmental priorities are for this year, how the total budget compares with the total money available, and then the department is given an appropriate lump sum budget for the year. The department then allocates their departmental budget according to their priorities, and increments or decrements the project budgets by an amount to meet the department's budget. Thereupon the project's plan is adjusted, if possible, by the assigned budget rather than vice-versa, but typically the scope cannot be reduced so the PM tries to adjust the plan to suit.

But the dynamics are still not over. At some point(s) in the future, the department's budget may well be cut further, so all the projects' placeholder budgets are decremented even more, requiring additional “adjustments” to the project plan (but again without allowing a reduction in scope). According to one expert in project management (Swanson, 2011), due to natural optimism at project start most PMs underestimate their projects' costs by 30 percent or more. Given that their expense contingency was less than 25 percent even before these factors impacted the budget, it is no wonder that the great majority of projects have cost overruns.

4.5 PROJECT RISK SIMULATION WITH CRYSTAL BALL®

![]()

At this point, we will deal with one of the more quantitative methods of dealing with risk as it applies to the task of simulating budgets and cash flows. The essence of risk analysis is to make estimates or assumptions about the probability distributions associated with key parameters and variables and to use analytic decision models or Monte Carlo simulation models based on these distributions to evaluate the desirability of certain managerial decisions. Real-world problems are usually large enough that the use of analytic models is very difficult and time consuming. With modern computer software, simulation is not difficult. PMBOK describes the simulation process in Chapter 11 on Risk.

![]()

A mathematical model of the situation is constructed, and a simulation is run to determine the model's outcomes under various scenarios. The model is run (or replicated) repeatedly, starting from a different point each time based on random choices of values from the probability distributions of the input variables. Outputs of the model are used to construct statistical distributions of items of interest to decision makers, such as costs, profits, completion dates, or return on investment. These distributions are the risk profiles of the outcomes associated with a decision. Risk profiles can be considered by the manager when considering a decision, along with many other factors such as strategic concerns, behavioral issues, fit with the organization, cost and scheduling issues, and so on.

In the following section, using an example we have examined earlier in Chapter 1, we illustrate how Oracle Crystal Ball® 11.1.2.2 (CB), a widely used Excel® Add-In that is available with this book, can be used to improve the PM's understanding of the risks associated with managing projects.

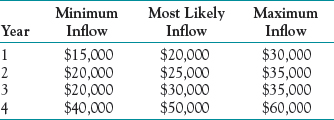

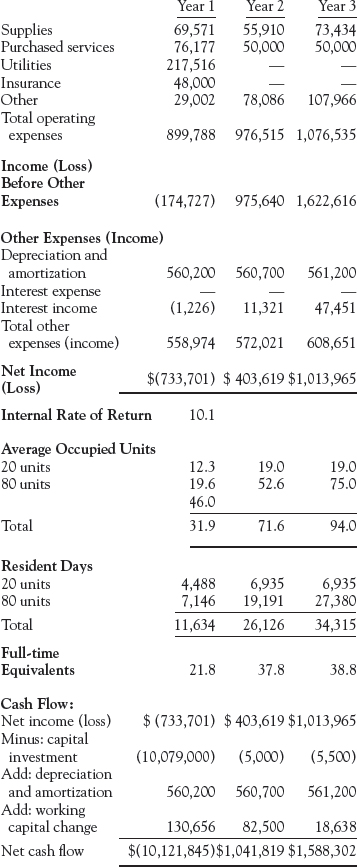

Reconsider the PsychoCeramic Sciences example we solved in Chapter 1 in the section devoted to finding the discounted cash flows associated with a project. Setting this problem up in Excel® is straightforward, and the earlier analytic solution is shown here for convenience as Table 4-5. We found that the project cleared the barrier of a 13 percent hurdle rate for acceptance. The net cash flow over the project's life is just under $400,000, and discounted at the hurdle rate plus 2 percent annual inflation, the net present value of the cash flow is about $18,000. The rate of inflation is shown in a separate column because it is another uncertain variable that should be included in the risk analysis.

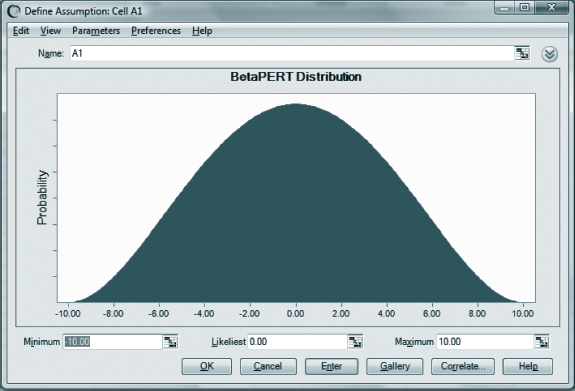

Assume that the expenditures in this example are fixed by contract with an outside vendor so that there is no uncertainty about the outflows; there is, of course, uncertainty about the inflows. Suppose that the estimated inflows are as shown in Table 4-6 and include a minimum (pessimistic) estimate, a most likely estimate, and a maximum (optimistic) estimate. (In Chapter 5, “Scheduling the Project,” we will deal in more detail with the methods and meaning of making such estimates. Shortly, we will deal with the importance of ensuring the honesty of such estimates.) Both the beta and the triangular statistical distributions are well suited for modeling variables with these three parameters. In earlier versions of CB the beta distribution was complicated and not particularly intuitive to use, so the triangular distribution was used as a reasonably good approximation of the beta. Use of a new beta distribution, labeled “BetaPERT” by CB in its distribution Gallery, has been simplified in version CB 11.1.2.2; we will use it in this example, and the simulations run elsewhere in this book.*

The hurdle rate of return is typically fixed by the firm, so the only remaining variable is the rate of inflation that is included in finding the discount factor. We have assumed a 2 percent rate of inflation with a normal distribution, plus or minus 1 percent (i.e., 1 percent represents ± 3 standard deviations).

It is important to point out that approaches in which only the most likely estimate of each variable is used are equivalent to assuming that the input data are known with certainty. The major benefit of simulation is that it allows all possible values for each variable to be considered. Just as the distribution of possible values for a variable is a better reflection of reality than the single “most likely” value, the distribution of outcomes developed by simulation is a better forecast of an uncertain future reality than is a forecast of a single outcome. In general, precise forecasts will be “precisely wrong.”

Table 4-5 Single-Point Estimates of the Cash Flows for PsychoCeramic Sciences, Inc.

Using CB to run a Monte Carlo simulation requires us to define two types of cells in the Excel® spreadsheet.* The cells that contain variables or parameters that we make assumptions about are defined as assumption cells. For the PsychoCeramic Sciences case, these are the cells in Table 4-5, columns B and G, the cash inflows and the rate of inflation, respectively. As noted above, we assume that the rate of inflation is normally distributed with a mean of 2 percent and a standard deviation of .33 percent. Likewise, we assume that yearly inflows can be modeled with a BetaPERT (or a triangular) distribution.

Table 4-6 Pessimistic (Minimum), Most Likely, and Optimistic (Maximum) Estimates for Cash Inflows for PsychoCeramic Sciences, Inc.

The cells that contain the outcomes (or results) we are interested in forecasting are called forecast cells. In PsychoCeramic's case we want to predict the NPV of the project. Hence, cell F17 in Table 4-5 is defined as a forecast cell. Each forecast cell typically contains a formula that is dependent on one or more of the assumption cells. Simulations may have many assumption and forecast cells, but they must have at least one of each. Before proceeding, open Crystal Ball® and make an Excel® spreadsheet copy of Table 4-5, adding column G for the inflation rate.

To illustrate the process of defining an assumption cell, consider cell B7, the cash inflow estimate for 2015. We can see from Table 4-6 that the minimum expected cash inflow is $35,000, the most likely cash flow is $50,000, and the maximum is $60,000.

If you have not already done so, load the Excel program on your computer. If prompted, click on “Use Crystal Ball” and then open the spreadsheet you made of Table A in Chapter 1 (also shown in Table 4-5). Given the information in Table 4-6, the process of defining the assumption cells and entering the pessimistic and optimistic data is straightforward and involves six steps:*

- Click on cell B7 to select it as the relevant assumption cell.

- Select the Crystal Ball tab in Excel and from the Crystal Ball ribbon, select “Define Assumption” at the very left of the Crystal Ball ribbon. CB's Distribution Gallery is now displayed as shown in Figure 4-6.

- CB allows you to choose from a wide variety of probability distributions. Click on the BetaPERT box and then click “OK” button to select it.

- CB's BetaPERT Distribution dialog box is displayed as in Figure 4-7. It may have numbers in the boxes but ignore them. If it does not otherwise appear exactly like Figure 4-7, click “Parameters” on the menu at the top of the BetaPERT Distribution dialog box, and then select “Minimum, Most Likely, Maximum” at the top of the drop-down menu.

- In the Name: textbox at the top of the dialog box enter a descriptive label, for example, Cash Inflow 2015. Then, enter the pessimistic, most likely, and optimistic estimates from Table 4-6 in the appropriate cells below the distribution.

- Click on the “Enter” button and then on the “OK” button.

Now repeat steps 1 through 6 for the remaining cash inflow assumption cells (cells B8:B15), using the information in Table 4-6.

Figure 4-7 Crystal Ball® dialog box for model inputs assuming the BetaPERT distribution.

When finished with the cash inflow cells, assumption cells for the inflation values in column G need to be defined. For these cells select the Normal distribution. We decided earlier to use a 2 percent inflation rate, plus or minus 1 percent. Recall that the normal distribution is bell-shaped and that the mean of the distribution is its center point. Also recall that the mean, plus or minus three standard deviations, includes 99+ percent of the data. The Normal Distribution dialog box, Figure 4-8, calls for the distribution's mean and its standard deviation. The mean will be 0.02 (2 percent) for all cells. The standard deviation will be .0033 (one-third of the ± percent range). (Note that Figure 4-8 displays only the first two decimal places of the standard deviation. The actual standard deviation of .0033 is used by the program, but if you wish to see the .0033 you may click on “Preferences” at the top of the box. Then click on “Chart,” “Axis,” “Cell format,” “Number,” and change the “2” to “4.” “OK” your way back to the input data sheet.) As you enter these data, the distribution will show a mean of 2 percent and a range from 1 percent to 3 percent.

Figure 4-8 Crystal Ball® dialog box for model inputs assuming the normal distribution.

Notice that there are two cash outflows for the year 2013, but one of those occurs at the beginning of the year and the other at the end of the year. The entry at the beginning of the year is not discounted, so there is no need for an entry in G4. (Some versions of CB insist on an entry, however, so go ahead and enter 2 percent with zero standard deviation.) Move on to cell G5, in the Name: textbox for the cell G5 enter Inflation Rate. Then enter .02 in the Mean textbox and .0033 in the Std. Dev. textbox. While the rate of inflation could be entered in a similar fashion for the following years, a more efficient approach is to copy the assumption cell G5 to G6. Since CB is an addin to Excel®, simply using Excel®'s copy and paste commands will not work. Rather, CB's own copy and paste commands must be used to copy the information contained in both assumption and forecast cells. The following steps are required:

- Place the cursor on cell G5.

- Click on “Copy” in the Crystal Ball ribbon.

- Highlight the range G6:G14.

- Click on “Paste” in the Crystal Ball ribbon.

Note that 2022 has two cash inflows, both occurring at the end of the year. Because we don't want to generate two different rates of inflation for 2022, the value generated in cell G14 should be used for both 2022 entries. Type =G14 in the G15 cell. Now we consider the forecast or outcome cell. In this example we wish to find the net present value of the cash flows we have estimated. The process of defining a forecast cell involves four steps.

- Click on the cell F17 to select it as containing an outcome that interests us.

- Select the menu option Define Forecast from the Crystal Ball ribbon at the top of the screen.

- CB's Define Forecast dialog box is now displayed. In the Name: textbox, enter a descriptive name such as Net Present Value of Project. Then enter a descriptive label such as Dollars in the Units: textbox.

- Click OK. There is only one Forecast cell in this example, but in other situations there may be several. Use the same four steps to define each of them.

When you have completed all entries, what was Table 4-5 is now changed and appears as Table 4-7.

We are ready to simulate. CB randomly selects a value for each assumption cell based on the probability distributions which we specified and then calculates the net present value of the cell values selected. By repeating this process many times, we can get a sense of the distribution of possible outcomes, or in this case the distribution of NPVs for this project.

Approximately in the center of the CB ribbon, you will see the Run Preferences. Below it is the “Trials” box. It should be set to “1000.” If not, simply enter 1000 in the box. To run the simulation, click the green Start Arrow in the CB ribbon.

Table 4-7 Three-Point Estimate of Cash Flows and Inflation Rate for PsychoCeramic Sciences, Inc. All Assumption and Forecast Cells Defined

The distribution of NPVs resulting from simulating this project 1,000 times is displayed in Figure 4-9. Statistical information on the distribution is shown in Figure 4-10. The NPVs had a mean of $11,086 and a standard deviation of $8,115. We can use this information to make probabilistic inferences about the NPV of the project such as what is the probability the project will have a positive NPV, what is the probability the project's NPV will exceed $10,000, or what is the probability the project's NPV will be between $5,000 and $10,000?

Figure 4-9 Frequency chart of the simulation output for net present value of Psycho-Ceramic Sciences, Inc. Project.

CB provides considerable information about the forecast cell in addition to the frequency chart including percentile information, summary statistics, a cumulative chart, and a reverse cumulative chart. For example, to see the summary statistics for a forecast cell, click on the Extract Data button in the CB ribbon and check Statistics in the dialog box that is displayed. The Statistics view for the frequency chart (Figure 4-9) is illustrated in Figure 4-10.

Figure 4-10 contains some interesting information. There are, however, several questions that are more easily answered by using Figure 4-9, the distribution of the simulation's outcomes. What is the likelihood that this project will achieve an NPV at least $10,000 above the hurdle rate including inflation? It is easy to answer this question. Note that there are black triangles at either end of the baseline of the distribution in Figure 4-9. By placing the cursor on the triangle on the left end of the simulation distribution baseline and sliding it to the $10,000 mark, the probability of a $10,000 or greater outcome can be read in the “Certainty” box. One can also find the same answer by deleting the “−Infinity” in the box in the lower left corner of the Frequency View and entering $10,000 in it.

Figure 4-10 Summary statistics of the PsychoCeramic Sciences, Inc. simulation.

Even in this simple example, the power of including uncertainty in project budgets should be obvious. Because a manager is always uncertain about the amount of uncertainty, it is also possible to examine various levels of uncertainty quite easily using CB. We could, for instance, alter the degree to which the inflow estimates are uncertain by expanding or contracting the degree to which optimistic and pessimistic estimates vary around the most likely estimate. We could increase or decrease the level of inflation. Simulation runs made with these changes provide us with the ability to examine just how sensitive the outcomes (forecasts) are to possible errors in the input data. This allows us to focus on the important risks and to ignore those that have little effect on our decisions.

Considering Disaster

![]()

In our consideration of risk management in the PsychoCeramic Sciences example, we based our analysis on an “expected value” approach to risk. The expected cost of a risk is the estimated cost of the risk if it does occur times the probability that it will occur. How should we consider an event that may have an extraordinarily high cost if it occurs, but has a very low probability of occurring? Examples come readily to mind: the World Trade Center destruction of 9/11, Hurricane Katrina, the BP oil spill in the Gulf of Mexico, the Hurricane Sandy floods of 2012 (a supposedly 500-year event!). The probability of such events occurring is so low that their expected value may be much less than some comparatively minor misfortunes with a far higher probability of happening.

If you are operating a business that uses a “just in time” input inventory system, how do you feel about a major fire at the plant of your sole supplier of a critical input to your product? The supplier reports that their plant has never had a major fire, and has the latest in fire prevention equipment. Does that mean that a major plant fire is impossible? Might some other disaster close the plant—a strike, an al Qaeda bomb? Insurance comes immediately to mind, but getting a monetary pay-back is of little use when you are concerned with the loss of your customer base or the death of your firm.

In an excellent book, The Resilient Enterprise, Yossi Sheffi (Sheffi, 2005) deals with the risk management of many different types of disasters. He details the methods that creative businesses have used to cope with disasters that struck their facilities, supply chains, customers, and threatened the future of their firms. The subject is more complex than we can deal with in these pages, but we strongly recommend the book, a “good read,” to use a reviewer's cliché.

In spite of the effort taken to make realistic budget estimates, it can still be useful to prepare for changes in the budget as the project unfolds. Such changes derive from multiple sources, including technology, economics, improved project understanding, and mandates. To the extent possible, it is best to include these contingencies in the contract in case they come to pass. Simulation is one excellent approach for determining the distribution of various possible outcomes occurring when risk is present in a project.

We are now ready to consider the scheduling problem. Because durations, like costs, are uncertain, we will continue our discussion of the matter, adding some powerful but reasonably simple techniques for dealing with the uncertainty surrounding both project schedule and cost.

REVIEW QUESTIONS

- Contrast the disadvantages of top-down budgeting and bottom-up budgeting.

- What is the logic in charging administrative costs based on total time to project completion?

- Would you expect a task in a manufacturing plant that uses lots of complex equipment to have a learning curve rate closer to 70 percent or 95 percent?

- How does a tracking signal improve budget estimates?

- Are there other kinds of changes in a project in addition to the three basic types described in Section 4.4? Might a change be the result of two types at the same time?

DISCUSSION QUESTIONS

6. Given the tendency of accountants to allocate a project's estimated costs evenly over the duration of the task, what danger might this pose for a project manager who faces the following situation? The major task for a $5 million project is budgeted at $3 million, mostly for highly complex and expensive equipment. The task has a six-month duration, and requires the purchase of the equipment at the beginning of the task to enable the project team to conduct the activities required to complete the task. The task begins December 1.

7. The chapter describes the problems of budgeting projects with S-shaped and J-shaped life-cycle curves. What might be the budget problems if the life cycle of a project was just a straight diagonal line from 0 at project start to 100 percent at project completion?

8. If a firm uses program budgeting for its projects, is an activity budget not needed? If it is, then of what value is the program budget?